A random-projection based procedure to test if a stationary process is Gaussian

Abstract

In this paper we address the statistical problem of testing if a stationary process is Gaussian. The observation consists in a finite sample path of the process. Using a random projection technique introduced and studied in [7] in the frame of goodness of fit test for functional data, we perform some decision rules. These rules really stand on the whole distribution of the process and not only on its marginal distribution at a fixed order. The main idea is to test the Gaussianity on the marginal distribution of some random linear combinations of the process. This leads to consistent decision rules. Some numerical simulations show the pertinence of our approach.

Key words and phrases: Gaussianity Test, Strictly Stationary Random Process, Random Projection, Consistent Test

A.M.S. 1980 subject classification: A60G

1 Introduction

In many concrete situations the statistician observes a finite path of a real temporal phenomena. A common modeling is to assume that the observation is a finite path of a second order weak stationary process (see, for example, [15]). This means that the random variable (r.v.) is, for any , square integrable and that the mean and the covariance structure of the process is invariant by any translation on the time index. That is, for any does not depend on and only depends on the distance between and . A more popular frame is the Gaussian case where the additional Gaussianity assumption on all finite marginal distributions of the process is added. In this case, as the multidimensional Gaussian distribution only depends on moments of order one and two, the process is also strongly stationary. This means that the law of all finite dimensional marginal distributions are invariant if the time is shifted:

Gaussian stationary process are very popular because they share plenty of very nice properties concerning their statistics or prediction (see, for example, [3] or [29]). Hence, an important topic in the field of stationary process is the implementation of a statistical procedure that allows to assess Gaussianity. In the last three decades, many works have been developed to build such methods. For example, in [11] a test based on the analysis of the empirical characteristic function is performed. In [21] based on the skewness and kurtosis test or also called Jarque-Bera test. In [24] based on both, empirical characteristic function and skewness and kurtosis. In [30] we can find another test, this based on the bispectral density function. An important drawback of these tests is that they only consider a finite order marginal of the process (generally the order one marginal!). Obviously, this provides tests at the right level for the intended problem; but these tests could be at the nominal power against some non-Gaussian alternatives. For example, in the case of a strictly stationary non-Gaussian process having one-dimensional Gaussian marginal.

In this paper, we propose a procedure to assess that a strictly stationary process is Gaussian. Our test is consistent against every strictly stationary alternative satisfying regularity assumptions. The procedure is a combination of the random projection method (see [7] and [8]) and classical methods that allow to assess that the one-dimensional marginal of a stationary process is Gaussian (see the previous discussion).

Regarding the random projection method, we follow the same methodology as the one proposed in [8]. Roughly speaking, it is shown therein that (only) a random projection characterizes a probability distribution. In particular, we employ the results of [7] where the main result of [8] is generalized to obtain goodness-of-fit tests for families of distributions, and in particular for Gaussian families.

Therefore, given a strictly stationary process, , we are interested in constructing a test for the null hypothesis is Gaussian. Notice that holds if, and only if, is Gaussian. So that, using the random projection method, [7], this is, roughly speaking, equivalent to that a (one-dimensional) randomly chosen projection of is Gaussian. This idea allows to translate the problem into another one consisting on checking when the one-dimensional marginal of a random transformation of is Gaussian. This can be tested using a usual procedure. Here, we will employ the well-known Epps test, [11], and Lobato and Velasco skewness-kurtosis test, [21]. We also use a combination of them as a way to alleviate some problems that those tests present.

Furthermore, Epps test checks whether the characteristic function of the one-dimensional marginal of a strictly stationary process coincides with the one of a Gaussian distribution. This checking is performed on a fixed finite set of points. As a consequence, it cannot be consistent against every possible non-Gaussian alternative with non-Gaussian marginal. However, in our work, the points employed in Epps test will be also drawn at random. This will provide the consistency of the whole test. Regarding Lobato and Velasco skewness-kurtosis test we will prove the consistency of the test under different hypothesis than those in [21].

The paper is organized as follows. In the next section we will give some basic definitions and notations. In Section 3, we discuss some useful known results. One concerns the random projection method, some Gaussianity tests for strictly stationary processes and another a procedure for multiple testing. It also contains a new result characterizing Gaussian distributions. In Section 4 we introduce our procedure and analyze its asymptotic behavior. Section 5 contains some details on the practical application of the method and Section 6 includes the results of the simulations. The paper ends with a discussion. In the whole paper all the processes are assumed to be integrable.

2 Notations and basic definitions

If is a random variable, we denote by its characteristic function; denotes the characteristic function of the Gaussian distribution with mean and variance .

denotes a separable Hilbert space with inner product and norm . denotes a generic orthonormal basis of and the -dimensional subspace spanned by . For any subspace, we write for its orthogonal complement. If D is an -valued random element, then denotes the projection of D on the subspace of .

and denote indistinctly a process. Through the following, when we say that a process is stationary we mean that it is strictly stationary. Given a stationary process let us denote, if they exists, the mean and with the centered moment of order Further, let with be the autocovariance of order .

Let be a sample of equally spaced observations of the random process Let be its sample mean, for its sample centered moment of order and

for the sample autocovariance of order When it is clear to which process they are referring we suppress the subindex Note that then we write as . For the sake of simplicity, let us denote and analogously

Finally, by i.i.d.r.vs. we mean independent and identically distributed random variables.

We assume that all the random elements are defined on the same, rich enough, probability space .

3 Preliminary results

In this section we discuss both a characterization of Gaussian distributions in infinite dimensional spaces, a characterization of the one-dimensional Gaussian distributions and two tests of Gaussianity for stationary processes. We also recall some facts on multiple testing procedure. All this material are tools for our results.

Excluding the characterization of the one-dimensional Gaussian distributions (Proposition 3.4), the results in this section are well known and they are included here for the sake of completeness.

3.1 Characterization of Gaussian distributions in Hilbert spaces

The result of this subsection comes from [7]. It is based on the use of dissipative distributions which are defined next.

Definition 3.1.

Let D be an -valued random element. We will say that its distribution is dissipative if there exists an orthonormal basis of such that

-

1.

, for all (see Section 2 for the definition of ).

-

2.

The conditional distribution of given is absolutely continuous with respect to the -dimensional Lebesgue measure.

Theorem 3.6 in [7] states the following:

Theorem 3.2 (Cuesta-Albertos et al. (2007)).

Let be a dissipative distribution on . If X is an -valued random element and

then X is Gaussian.

The importance of this result relies on the fact that if is dissipative then the following law holds

Moreover, X is not Gaussian if, and only if,

In other words, if we ask if the distribution of X is Gaussian, then the only thing we have to do is to select at random a point using a dissipative distribution and check if the real-valued random variable is Gaussian. We will obtain the right answer with probability one.

3.2 Characterization of one-dimensional Gaussian distributions

We start this subsection by stating the definition of analytic characteristic function which has been taken from [20].

Definition 3.3.

A characteristic function is said to be analytic if there exist

-

•

a complex valued function, , of the complex variable which is holomorphic in a circle where

-

•

a positive real number such that for

That is, an analytic characteristic function is a characteristic function which coincides with a holomorphic function in some neighborhood of zero.

Some properties on analytic characteristic functions may be found in [20]. In particular, it is proved therein that the characteristic function of a Gaussian distribution is analytic (this is a well known fact). Some other well-known distributions having analytic characteristic function are the binomial, Poisson and gamma distributions but not the Cauchy one.

The following result will be useful to assess that our goodness of fit test will work with all non-Gaussian alternatives.

Proposition 3.4.

Let be a Borel probability measure defined on . Assume that is absolutely continuous with respect to the Lebesgue measure. Let be a r.v. having an analytic characteristic function .

Then, is Gaussian if, and only if,

| (1) |

Proof.

Necessary part is obvious. Let us show the sufficiency. As satisfies (1), and is absolutely continuous, we have that the set is infinite and not denumerable. Thus, it contains at least an accumulation point.

Furthermore, the function is analytic, and it vanishes on . Therefore, this function has a non-isolated zero but the only analytical function with at least a non-isolated zero is the null function which proves the result (see for example [28]). ∎

3.3 Classical tests of Gaussianity for stationary processes

Through this section we present some useful popular tests for checking whether a stationary random process is Gaussian.

3.3.1 Epps test

The test discussed in this section is a particular case of the one studied in Section 3 of [11]. We begin with some notations and definitions. Given , let us define

where T denotes transposition.

Let and let be the -dimensional column vector composed by the real and complex parts of the empirical characteristic function computed at . That is

Further let, for real and , the -dimensional vector composed by the real and complex parts of computed at :

We denote by the spectral density matrix (see for example [2]) of the process

at frequency . Notice that if we assume that is a Gaussian stationary process with

| (2) |

then the existence of is one of the conclusions of Lemma 2.1 in [11]. For the construction of the test statistic we will use the following estimator of :

| (3) |

where and denotes the integer part. The estimator (3) was used in [11], but with replaced by a general constant in the interval Notice also that it is a particular case of the one proposed in [12]. In [11] it is proved that if is Gaussian, stationary and satisfies (2), then converges almost surely to Let be the generalized inverse of and let be the quadratic form

| (4) |

Let be an open bounded subset of and let . We state two assumptions.

- H1.

-

The set is nowhere dense in

- H2.

-

For each we have, and

Theorem 3.5 (Epps (1987)).

Let be a stationary Gaussian process satisfying (2). Let be an open and bounded subset of and such that H1. and H2. hold. Further, let be the minimizer on nearest to of the map

Assume further that is positive definite. Then, for each fixed , converges in distribution to .

Remark 3.5.1.

Obviously a test based on Theorem 3.5 may be not consistent. Indeed, it only focuses on the values of the characteristic function at some points. In other words, the test could not detect some alternatives with Gaussian one-dimensional marginal. Even the test fails against alternatives with non-Gaussian one-dimensional marginal but that satisfy that the characteristic functions of the one-dimensional marginal coincides with the one of the corresponding Gaussian at the selected points.

3.3.2 Lobato and Velasco test

The test to assess normality of time series discussed in this Subsection was introduced in [21]. It uses the skewness-kurtosis test statistic, also called Jarque-Bera test (see [6] and [18]), but improves previous tests of this kind because the statistic is studentized by standard error estimators.

Given a process let us denote . This is an estimator of The test proposed in [21] handles the statistic:

Theorem 3.6 (Lobato and Velasco (2004)).

Let be an ergodic stationary process.

-

•

If is Gaussian and satisfies then in distribution.

-

•

If satisfies

-

–

,

-

–

for q=2,…,16, where denotes the th-order cumulant of

-

–

for where denotes the -field generated by , and

-

–

for

then the statistic diverges to infinity whenever or

-

–

In Section 4 we will prove this theorem under lighter assumptions on the alternative. We will need the following recent result taken from [19]. It is an improvement of the well-known result in [1].

Theorem 3.7 (Kavalieris (2008)).

Let be a stationary process with the representation

| (5) |

Assume that for some If for and then

3.4 Multiple testing

In Section 5 we will propose to use several tests to assess the Gaussianity of a process. Thus we obtain several -values , where is the number of procedures used.

The most popular way to handle several -values is to use the Bonferroni correction. However, it is very well-known that this procedure is too conservative. Several alternatives have been proposed in the literature in order to alleviate this problem. Here, we will employ the false discovery rate (FDR). The FDR is the expected proportion of wrongly rejected hypotheses along the tests. Taking into account that all the hypothesis we have are equivalent, the FDR coincides with the level of the procedure.

The FDR was introduced in Benjamini and Hochberg [4] for independent tests. Here, we employ the improvement proposed in [5] that does not require dependence assumptions among the tests. This procedure, when applied to our case, works as follows:

Theorem 3.8 (Benjamini and Yekutieli (2001)).

Let us assume that we apply statistical tests to check the same null hypothesis and that the ordered -values that we obtain are where .

Let . The FDR of the test which rejects if the set

is not empty is, at most, .

Therefore, according to the previous theorem, if we denote

we can reject at any level and then, we can take as the resulting -value of the procedure.

4 A Gaussianity test for stationary processes

In this section we present a universal test to check if the distribution of a stationary process is Gaussian. Thus, given a stationary process of real-valued random variables we are interested in constructing a test for the null hypothesis

against the alternative

Notice holds if, and only if, for all is a Gaussian vector. As X is stationary, it is equivalent to the distribution of is Gaussian. In addition, it is the sames as the Gaussianity of the process for any To check whether is Gaussian, we only need to include in an appropriate Hilbert space, then select a vector h using a dissipative distribution, and compute the scalar product because, according to Theorem 3.2, almost surely, is Gaussian if, and only if, is Gaussian.

Concerning the Hilbert space in which the process is included, let us consider the space of sequences

with and endowed with the scalar product

It is easy to see that if X is a stationary process and if the variance of is finite, then, almost surely, and that the Gaussianity in this space is equivalent to the (usual sense) Gaussianity of The reason is that is finite if it is so the variance of

Now we need a dissipative distribution on We will use the so-called Dirichlet distribution (see [26]). We build this distribution using the so-called stick breaking method. That is, let and consider the probability distribution which selects a random point in according to the following iterative procedure:

-

•

is chosen with the beta distribution of parameters and

-

•

Given , is chosen with the beta distribution of parameters and times

Let us define for and take It can be easily checked that the distribution of H is dissipative (see Definition 3.1). Moreover, almost surely because, as shown in Proposition 4.1, , almost surely.

Proposition 4.1.

Let be a stochastic process constructed as described above. Let be the mean of the beta distribution of parameters and Then, we have that

-

1.

.

-

2.

, almost surely.

Proof.

Obviously 1. holds for . Thus, let us assume that 1. is satisfied for and let us show that it also holds for . By construction, we have that if is a random variable with beta distribution of parameters and , then

where last equality comes from the application of the formula giving the sum of numbers in a geometric progression. Concerning 2., we have that

| (6) |

Indeed, by construction, for every , . However, applying 1., we have that

Now, let be a fixed realization of the random element drawn independently of the process X. Let us consider the process given by the projections of on the one-dimensional subspace generated by i.e.

| (7) |

As we will see in Proposition 4.3, the properties of the process X are inherited by the process Y. Moreover, according to Theorem 3.2, to assess the Gaussianity of X is enough to do the job on the one-dimensional marginal distributions of Y. This can be done for instance with Epps or Lobato and Velasco tests presented in Section 3.3 whenever Y satisfies the appropriate assumptions. The following Subsections are devoted to this task.

Lemma 4.2.

Let X be an ergodic and stationary process such that If we select H as described above, then,

-

1.

almost surely.

-

2.

Almost surely, the random variable is conditionally integrable given .

Proof.

In the sequel denotes the conditional autocovariance of order of given . That is, denoting by the conditional expectation of given ,

Proposition 4.3.

Let be an ergodic and stationary process such that with Then, conditionally on , the process defined in (7) is ergodic and stationary. In addition, and are finite.

Proof.

is a stationary ergodic process. So that, conditionally on , is also a stationary ergodic process (see [10] page 458).

By 2. in Lemma 4.2, we have that

exists. So that, using the dominated convergence theorem, we obtain that

and

Obviously, , where

-

•

-

•

-

•

If as and , we have Thus,

because Then, and so, 1. in Lemma 4.2 implies

Concerning as and , we can apply the inequality (see [22] p.157) to to obtain that there exists such that Thus,

Then, using the same tricks as for

we obtain that

For , the fact that , implies that there

exists an such that for all . Therefore,

By 1. in Lemma 4.2, to show that , we only need to prove that . Furthermore, applying Jensen inequality and 1. in Proposition 4.1, we have that

| (8) |

This last series is convergent (). Hence, is finite almost surely and the proof is ended. ∎

4.1 Conditions to apply Epps test

In this subsection we analyze the theoretical behavior of Epps test when applied to the randomly projected process (see Theorem 4.7). Moreover, in a corollary (Corollary 4.8) we will show that if is drawn randomly, then the Epps test is consistent against many more alternatives.

Let us first state Lemma 4.4 that gives the consistency for the estimator of the spectral density function at zero defined in (3). Let us denote by the fourth-order cumulant of and where, for instance, is the -th component of the vector (see Subsection 3.3.1).

Lemma 4.4.

Let . If Y is a stationary process such that

| (9) |

then,

Proof.

It is straightforward from the proof of Lemma 2.2 in [11] but substituting by (9) the use of (2) and Gebelein inequality, [14], for Gaussian processes. Gebelein inequality says that the autocovariance of a multidimensional process is smaller or equal than the product of variances of the marginals. ∎

Lemma 3.1 in [11] proves that if Y is a stationary Gaussian process that satisfies (2), then (9) holds. In [23], Gebelein inequality is extended to two-dimensional vectorial processes with diagonal densities. So that, any stationary process that satisfies (2) and whose two-dimensional marginal has diagonal density, also satisfies (9).

Let be an open and bounded subset of In [11], it is proved that H1 and H2 (see Subsection 3.3.1) are satisfied if is equal to a rational number times Now, thanks to Lemma 4.5 below, we have that can be taken at random and still fulfill H1 and H2.

Lemma 4.5.

Assume that () is drawn randomly and has distribution having the following properties. First is such that and are independent and identically distributed and have a density. Further, for is a rational number times Then, H1 and H2 are fulfilled almost surely.

Proof.

Proceeding as in [11] we have that

Now, in order to get that the cardinal of is larger than one, we need is equal to a rational number times However, this happens with probability zero and so, with probability one Thus, H1 and H2 follow directly. ∎

Note that in case Lemma 4.5 remains valid if we draw independently at random In addition, thanks to this lemma we have the following corollary of Theorem 3.5.

Corollary 4.6.

In the next theorem, the function also depends on the random . However, for the sake of simplicity we have not express the functional relationship.

Theorem 4.7.

Let X be an ergodic stationary process satisfying (2). Draw respectively as in Lemma 4.5 and h independently of using (as described above).

Assume that, conditionally on , defined in (7) satisfies (9), that the characteristic function of its one-dimensional marginal is analytic and that exists and is positive definite for almost every . Let be the quadratic form defined in (4) applied to Y and its minimizer on nearest to Let further

Then, X is Gaussian if, and only if,

Proof.

Necessary part is obvious, because if X is Gaussian, then Y also is Gaussian and Proposition 4.3 implies that Y satisfies the assumptions of Corollary 4.6.

Let us show the sufficient part.

As we have that there exist and with and such that converges in law to a non-degenerated distribution. In addition, we may assume without loss of generality that and Indeed, as is an analytic characteristic function it has only isolated zeros.

Therefore, converges in probability to zero.

By Lemma 4.4,

converges to Thus, is positive definite because it is the inverse of . This together with (4) gives that

| (10) |

Since is an ergodic stationary process, by [10] page 458 we have that is also an ergodic stationary process. Thus, as and for all we have by Theorem 2 of Chapter IV in [16] that

From this and (10) we may conclude that converges in probability to ().

Let us see how this implies that the sequence converges.

We have that

and, since and , this implies that there exists such that in probability. Note that there exists such that

As , if we take , then, we have that

Analogously, we have that

in probability,

and as we obtain

| (11) |

Denoting , we obtain that

Together with (11) this gives

Remark 4.7.1.

Applying the arguments of Theorem 4.7 directly to the process , we obtain the following corollary. It gives a modification of Epps test with better consistency properties.

Corollary 4.8.

Let X be an ergodic stationary process. Assume that the characteristic function of its one-dimensional marginal is analytic. Assume further that (2) holds. Let us take as in Lemma 4.5, as in (4), let be its minimizer on nearest to and

If we assume that exists and is positive definite, then, X is Gaussian if, and only if,

Remark below can be obviously deduced from Theorems 3.5 and 4.7. This remark allows to perform a test based on the asymptotic distribution of

Remark 4.8.1.

In addition, we have the following corollary.

4.2 Conditions to apply Lobato and Velasco test

In this subsection we show that a slight modification of the statistic satisfies Theorem 3.6 under different assumptions than the ones used in [21].

The test statistic is

with

where, according to Theorem 3.7, we take for and Thus, the differences between and are the absolute values in the denominator and the number of terms involved in

Theorem 4.10.

Let be an ergodic and stationary process such that We have that

-

1.

If is a Gaussian process, then

-

2.

If can be written as (5) and then, conditionally on , diverges almost surely to infinity whenever or

Proof.

Using Proposition 4.3 for we get that is an ergodic and stationary process with

If is Gaussian, the process is also Gaussian. Thus, assumptions of the first part of Theorem 3.6 hold for the process and so

Now, as Y is Gaussian, by [13] page 568, we have that for Repeating the proof of Lemma 1 in [21], we have that and so, we may conclude that which shows 1.

Let us prove now statement 2. First, let us show that , almost surely, for

By Hölder inequality we have that and, as by Proposition 4.1 almost surely, we can apply Jensen inequality. We obtain that

Thus, almost surely, for By [10], page 458, we have that is stationary and ergodic, for all Therefore, Theorem 2 of Chapter IV in [16] implies that

| (12) |

Further, let us prove that for almost every h and We have

Taking into account that with and we have

and then we obtain Let us prove now that

Note that as we also have

because are i.i.d.r.vs. with So that Further, using Theorem 3.7 we obtain that

Thus, Then, by proceeding similarly as in the proof of Proposition 4.3, we get and so, for Using (12) we may conclude that 2. holds. ∎

Finally, applying Theorem 4.10 directly to the process , we obtain the following corollary.

Corollary 4.11.

Let be an ergodic and stationary process such that We have that

-

1.

If is a Gaussian process, then

-

2.

If can be written as (5) and then, conditionally on , diverges almost surely to infinity whenever or

5 The tests in practice

In this section we discuss the practical implementation of the gaussianity test. We start doing some remarks on Epps test.

5.1 Remark on Epps test

Although Theorem 3.5 works for any with which satisfying H1 and H2, in [11] it is stated that:

-

•

When either is large or the spacing between the is small, relative to the scale of the data, the matrix often appears computationally singular.

-

•

Also, values of which are large, relative to the scale of the data, makes difficult to find a minimum of with much precision.

Epps suggests to take

| (13) |

Recall that denotes the sample variance of the process. He proved that Theorem 3.5 works taking such In the simulations of Epps, and also in the ones of [21], and

However, we need to draw randomly in order to have a consistent test (Theorem 4.7). So, we take distributed as the absolute value of a standard normal distribution and distributed as the absolute value of a normal distribution with mean zero and variance With this selection, although seldom, we have found that could be singular. This is the main reason to choose as the generalized inverse of

5.2 The random projection procedure to test Gaussianity

The theoretical development of Section 4 was carried out assuming that the observed sample is infinite. However, in practice, only a finite number of measurements are available. So that, only a finite number of components of h are computed. This last difficulty is handled by fixing a small (equal to in the simulations that we present in Section 6) and by taking with

where are drawn by the stick breaking procedure described in Section 4. Further, is fixed such that Concerning the projected process, some possibilities are available, but here we use

Let us give a short comment on the choice of the parameters of the beta distribution used to generate Here we have to deal with the following situation: If is large, then the random variables are linear combinations of many random variables from the first sample and then, because of the Central Limit Theorem, the distribution of the random variables will become closer to a normal law. That will cause some loss of power when the marginal of X is not Gaussian. Thus, in order to detect a non-Gaussian marginal, it is wise to select and in such a way that is small or even or . This goal is achieved if we take and . Our selection in Section 6 is . However, in this case the samples and are quite similar. So that, the test will not be good in detecting non-Gaussian alternatives with Gaussian marginal. In order to overcome this problem we should take h in such a way that the projections mix several variables from the initial sample. To achieve this goal we need to take but with being not too big to avoid the effect of the Central Limit Theorem. In this case, a selection like and seems appropriate. Therefore, it seems that in a practical situation we should decide which alternative is more plausible and then, select the appropriate parameters. However, there is another possibility: select two projections (one with each pair of parameters) and apply Theorem 3.8 to mix the -values. This is our proposal.

Finally, we need a Gaussianity test for the one dimensional marginal of . We have seen two such tests (which have some advantages and disadvantages discussed in Section 6) and we can also mix them. Having all these requirements in mind, we propose the following procedure:

-

1.

Draw with the distribution and apply Epps test to the projections to obtain the -value .

-

2.

Draw (independently of ) with the distribution and apply Lobato and Velasco test to the projections to obtain the -value .

-

3.

Draw (independently of and ) with the distribution and apply Epps test to the projections to obtain the -value .

-

4.

Draw (independently of , and ) with the distribution and apply Lobato and Velasco test to the projections to obtain the -value .

-

5.

Combine the -values using the procedure described in Section 3.4 to decide the Gaussianity hypothesis at the level . Thus, ordering these four -values such that we obtain that the -value of the random projection test is equal to

6 Simulations

In this section we study the behavior of the proposed procedure in different situations. We have used the same distributions as in [21], in order to perform comparisons. Further, we will study a situation where the process has Gaussian marginal but is not Gaussian (see Section 6.1). In addition, in Subsection 6.2 we apply the random projection test to real data.

The authors of [21] study the case of an AR(1) process depending on a parameter defined by

| (14) |

where and are i.i.d. random variables with distribution which may be any of the following ones:

-

•

standard normal (N(0,1)),

-

•

standard log-normal (log N),

-

•

Student with 10 degrees of freedom, (),

-

•

chi-squared with () and degrees of freedom (),

-

•

uniform on (),

-

•

beta with parameters ().

To simulate the process, we generate a large number of independent realizations with distribution and we take

-

•

-

•

It is obvious that if , this process is not stationary. For instance, which is not constant and, obviously, the differences increase with . In order to alleviate this problem, we disposed a certain number, past, of observations. We have taken equal to and equal to which are the sample sizes handled in [21].

We have performed 5000 simulations in each situation. In every run we have computed the -values using the asymptotic distributions. This could have caused that sometimes the rejection rates under the null hypothesis are far away from the nominal level (mostly for the lowest sample size ) and that they decrease under some alternatives with the sample size (mostly for high values of ).

There are some differences between our rates and those published in [21]. We think they could be due to the fact that the past taken in [21] is not large enough. For example, in the case , and being we obtain a rejection rate of when using Epps test while in [21] they obtain one of which is appreciatively worse. As explained before, our simulations were made with past, but from Table 6.1 we see that is a rejection rate reasonable for past and that the rejection rates increase with past, approaching to the value we have obtained.

| past | 0 | 1 | 2 | 10 |

|---|---|---|---|---|

| rejections | .0750 | .1378 | .1998 | .2210 |

Table 6.1.

Rejection rates along 5,000 simulations for different past, with Epps test, a and

We have observed the same problem with Lobato and Velasco test, excepting that with this other test our rejection rates are lower than those reported in [21].

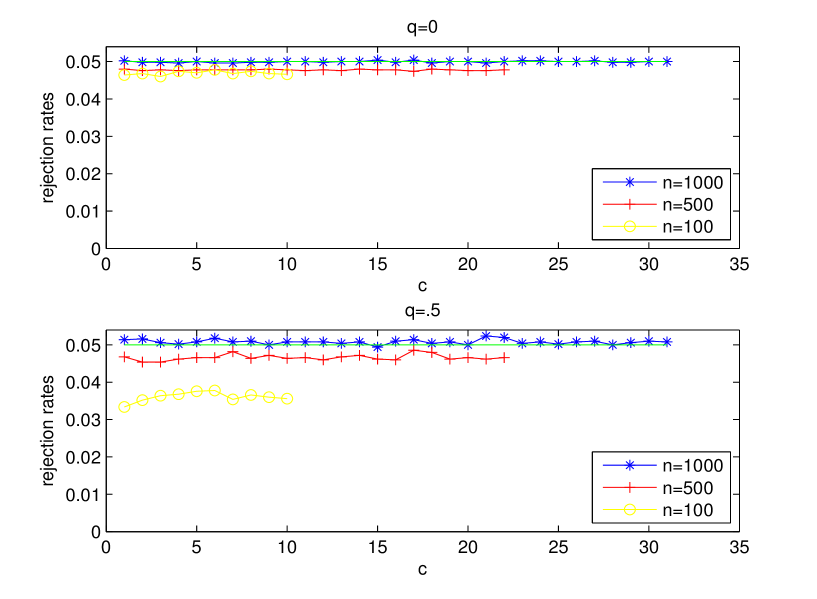

Furthermore, another difference to bold between what we do here and [21] is that in Subsection 4.2 a sum until is involved in the estimation of while in [21] the sum goes until where is the sample size. Here, we have to take where with and . Thus, may be as close as desired to .5 and so, we have decide to fix its value at for the simulations. In order to select the right value of , we have made a small analysis to see how sensitive is the method to this parameter. We run Lobato and Velasco test under the null hypothesis for all values of and where and Therefore, and The results suggest that the value of has not much influence in the rejection rates and so, we choose The results for the cases and appear in Figure 1. It is worth saying that the situation for is a bit different than for the other values, as with the rejection rates look constant till a point in which those rates strongly decrease.

Tables 6.2, 6.3 and 6.4 contain the rejection rates for several procedures when applied at the level . Next we mention the procedures we have selected and make some comments on the results of our simulations.

-

1.

Epps test, E-test. We take in (13).

It seems that this test behaves poorly when is . Moreover, broadly speaking, its power decreases for the considered alternative distributions when increases, having low powers when . Note also that under the null hypothesis (excepting the case with ), the rejection rates are above the level of the test and that they increase with

The power decreases when the sample size increases in the cases in which and the alternative is or (and even with when ).

-

2.

Lobato and Velasco test, G-test. The rejection rates displayed have been simulated using the statistic . However, they are similar to those obtained using .

The G-test has very low powers when is large, sometimes even lower than those of the E-test. In addition it suffers from a lack of power when is or . The rejections under the null hypothesis are above the level of the test only in 4 cases out of 24. In contrast with the E-test, here the rejection rates under the null hypothesis decrease when increases.

-

3.

Combined Epps and Lobato and Velasco test, GE-test. In previous paragraphs we have commented some problems of the E and G tests which go, let us say, in opposite directions. In order to solve these problems we combine both tests, using the multiple testing procedure presented in Section 3.4.

As stated in Subsection 5.1, the GE-test have been obtained by drawing independently with absolute value of a standard normal distribution and with absolute value of a normal distribution with mean zero and standard deviation However, it is worth noting that the rejection rates we have obtained have been a bit larger than in the case we take

-

4.

Random projection test, RP-test. We apply this test following the guidelines provided in Subsection 5.2.

When is negative and we are under the alternative, we always get the highest rejection rates with the RP-test. The most striking behavior of this test happens for and and where the RP-test obtains rejection rates larger than while the second more successful test remains below . For the remaining values, it happens that the rejection rates using the RP-test are between the rates obtained with the E, G and GE tests but closer to the highest than to the lowest.

| Test | N(0,1) | log N | ||||||

|---|---|---|---|---|---|---|---|---|

| E | .1264 | .0508 | .1104 | .0656 | .1124 | .1390 | .1354 | |

| -.9 | G | .0292 | .1414 | .0310 | .0840 | .0332 | .0290 | .0266 |

| GE | .0942 | .1422 | .0908 | .1072 | .0920 | .1020 | .1010 | |

| RP | .1380 | .8070 | .1742 | .7576 | .3076 | .2620 | .3902 | |

| E | .0724 | .6780 | .0556 | .8514 | .2058 | .5408 | .4914 | |

| -.5 | G | .0504 | .9986 | .1692 | .9986 | .4602 | .0102 | .1696 |

| GE | .0774 | .9976 | .1582 | .9972 | .4552 | .4454 | .4154 | |

| RP | .0752 | .9998 | .1980 | 1 | .5824 | .6404 | .7460 | |

| E | .0632 | .9616 | .0830 | .9964 | .5372 | .9918 | .9704 | |

| 0 | G | .0458 | 1 | .2820 | 1 | .7898 | .5404 | .7520 |

| GE | .0732 | 1 | .2402 | 1 | .8074 | .8596 | .8706 | |

| RP | .0772 | 1 | .2288 | 1 | .7640 | .8496 | .9054 | |

| E | .0682 | .8594 | .0608 | .9582 | .2610 | .5618 | .5562 | |

| .5 | G | .0384 | .9990 | .1696 | .9982 | .4118 | .0010 | .1102 |

| GE | .0642 | .9990 | .1444 | .9988 | .4700 | .4680 | .4882 | |

| RP | .0750 | .9908 | .1132 | .9880 | .5226 | .3256 | .7500 | |

| E | .0710 | .6118 | .0582 | .8106 | .2006 | .3462 | .3650 | |

| .6 | G | .0358 | .9884 | .1162 | .9772 | .2858 | .0012 | .0592 |

| GE | .0640 | .9882 | .1144 | .9832 | .3218 | .2800 | .3086 | |

| RP | .0802 | .9536 | .1030 | .9262 | .5164 | .2580 | .7744 | |

| E | .0838 | .3250 | .0626 | .4640 | .1492 | .2032 | .2214 | |

| .7 | G | .0260 | .9076 | .0814 | .8196 | .1610 | .0036 | .0334 |

| GE | .0714 | .9042 | .0866 | .8448 | .1998 | .1634 | .1802 | |

| RP | .0784 | .8022 | .0926 | .7010 | .5754 | .2902 | .8060 | |

| E | .1034 | .1552 | .0810 | .2004 | .1324 | .1620 | .1596 | |

| .8 | G | .0206 | .6146 | .0466 | .4406 | .0708 | .0046 | .0166 |

| GE | .0726 | .6118 | .0796 | .4488 | .1122 | .1154 | .1136 | |

| RP | .0896 | .4928 | .0932 | .3264 | .6766 | .3950 | .8782 | |

| E | .1752 | .1264 | .1618 | .1368 | .1612 | .1870 | .1680 | |

| .9 | G | .0106 | .1558 | .0094 | .0714 | .0150 | .0054 | .0086 |

| GE | .1074 | .1844 | .0968 | .1190 | .0980 | .1182 | .1072 | |

| RP | .1168 | .1982 | .1174 | .1338 | .8702 | .6788 | .9662 |

Table 6.2.

Rejection rates at level of a process defined by (14). Sample size

| Test | N(0,1) | log N | ||||||

|---|---|---|---|---|---|---|---|---|

| E | .0744 | .3720 | .0584 | .2162 | .0712 | .0918 | .0850 | |

| -.9 | G | .0708 | .8838 | .0840 | .6202 | .1142 | .0462 | .0754 |

| GE | .0780 | .8604 | .0924 | .5400 | .1116 | .0866 | .0952 | |

| RP | .0810 | .9990 | .2260 | .9928 | .6924 | .4630 | .6918 | |

| E | .0594 | 1 | .1334 | 1 | .7730 | .9924 | .9922 | |

| -.5 | G | .0472 | 1 | .4580 | 1 | .9960 | .9656 | .9976 |

| GE | .0476 | 1 | .3784 | 1 | .9912 | .9514 | .9914 | |

| RP | .0490 | 1 | .5090 | 1 | .9998 | .9946 | 1 | |

| E | .0566 | 1 | .3292 | 1 | .9982 | 1 | 1 | |

| 0 | G | .0480 | 1 | .7428 | 1 | 1 | 1 | 1 |

| GE | .0510 | 1 | .6756 | 1 | 1 | 1 | 1 | |

| RP | .0554 | 1 | .6188 | 1 | 1 | 1 | 1 | |

| E | .0654 | 1 | .1476 | 1 | .8808 | .9918 | .9960 | |

| .5 | G | .0454 | 1 | .4340 | 1 | .9972 | .9704 | .9988 |

| GE | .0516 | 1 | .3816 | 1 | .9924 | .9504 | .9962 | |

| RP | .0618 | 1 | .2656 | 1 | .9610 | .7440 | .9634 | |

| E | .0566 | .9998 | .1026 | 1 | .7084 | .8286 | .9090 | |

| .6 | G | .0470 | 1 | .3336 | 1 | .9582 | .4678 | .8858 |

| GE | .0570 | 1 | .2692 | 1 | .9388 | .6944 | .8870 | |

| RP | .0610 | 1 | .1794 | 1 | .8604 | .4730 | .9006 | |

| E | .0708 | .9996 | .0786 | 1 | .4704 | .4042 | .5810 | |

| .7 | G | .0474 | 1 | .1970 | 1 | .7592 | .0644 | .4040 |

| GE | .0598 | 1 | .1670 | 1 | .7332 | .3640 | .5768 | |

| RP | .0702 | 1 | .1282 | 1 | .6986 | .2616 | .8786 | |

| E | .0776 | .9780 | .0710 | .9638 | .2500 | .1948 | .2564 | |

| .8 | G | .0744 | .9998 | .0976 | .9980 | .3908 | .1524 | .2628 |

| GE | .0702 | .9998 | .1102 | .9978 | .3972 | .1848 | .2960 | |

| RP | .0710 | .9986 | .0910 | .9908 | .6834 | .2484 | .9208 | |

| E | .1156 | .5708 | .0944 | .4674 | .1526 | .1430 | .1560 | |

| .9 | G | .0232 | .8356 | .0370 | .5404 | .0764 | .0138 | .0336 |

| GE | .0802 | .8708 | .0838 | .6378 | .1490 | .1092 | .1390 | |

| RP | .0860 | .7996 | .0770 | .5510 | .8430 | .4818 | .9772 |

Table 6.3.

Rejection rates at level of a process defined by (14). Sample size

| Test | N(0,1) | log N | ||||||

| E | .0648 | .7836 | .0578 | .4572 | .0826 | .0888 | .0942 | |

| -.9 | G | .0902 | .9934 | .1206 | .8932 | .2448 | .0760 | .1358 |

| GE | .0880 | .9856 | .1002 | .8560 | .2190 | .1004 | .1450 | |

| RP | .0940 | 1 | .3344 | .9998 | .8686 | .5876 | .8056 | |

| E | .0530 | 1 | .2574 | 1 | .9764 | 1 | 1 | |

| -.5 | G | .0436 | 1 | .6778 | 1 | 1 | 1 | 1 |

| GE | .0450 | 1 | .6040 | 1 | 1 | 1 | 1 | |

| RP | .0378 | 1 | .7498 | 1 | 1 | 1 | 1 | |

| E | .0490 | 1 | .5946 | 1 | 1 | 1 | 1 | |

| 0 | G | .0546 | 1 | .9364 | 1 | 1 | 1 | 1 |

| GE | .0486 | 1 | .9162 | 1 | 1 | 1 | 1 | |

| RP | .0422 | 1 | .8734 | 1 | 1 | 1 | 1 | |

| E | .0550 | 1 | .2534 | 1 | .9966 | 1 | 1 | |

| .5 | G | .0482 | 1 | .6788 | 1 | 1 | 1 | 1 |

| GE | .0424 | 1 | .6016 | 1 | 1 | 1 | 1 | |

| RP | .0484 | 1 | .4348 | 1 | .9994 | .9738 | .9996 | |

| E | .0566 | 1 | .1718 | 1 | .9580 | .9800 | .9974 | |

| .6 | G | .0472 | 1 | .5112 | 1 | .9996 | .9724 | .9996 |

| GE | .0464 | 1 | .4234 | 1 | .9996 | .9550 | .9986 | |

| RP | .0584 | 1 | .2812 | 1 | .9902 | .7110 | .9804 | |

| E | .0594 | 1 | .1162 | 1 | .7720 | .6338 | .8632 | |

| .7 | G | .0418 | 1 | .3104 | 1 | .9744 | .3642 | .8830 |

| GE | .0558 | 1 | .2380 | 1 | .9672 | .5642 | .8724 | |

| RP | .0598 | 1 | .1754 | 1 | .8888 | .3554 | .9036 | |

| E | .0690 | .9998 | .0720 | 1 | .4342 | .2288 | .4108 | |

| .8 | G | .0500 | 1 | .1638 | 1 | .6804 | .0432 | .3284 |

| GE | .0670 | 1 | .1294 | 1 | .6708 | .2216 | .4450 | |

| RP | .0654 | 1 | .0996 | 1 | .7144 | .1920 | .9076 | |

| E | .0902 | .9152 | .0880 | .7690 | .1836 | .1170 | .1686 | |

| .9 | G | .0346 | .9944 | .0636 | .9136 | .1574 | .0174 | .0574 |

| GE | .0690 | .9926 | .0798 | .9206 | .2178 | .1040 | .1596 | |

| RP | .0736 | .9844 | .0678 | .8580 | .8328 | .3946 | .9774 |

Table 6.4.

Rejection rates at level of a process defined by (14). Sample size

6.1 A strictly stationary non-Gaussian process with Gaussian marginal

In this subsection we discuss the behavior of the proposed procedure when used on a non-Gaussian process with Gaussian marginal. We have worked with the process introduced in Example 2.3 in [9]. Its construction is explained here for the sake of completeness.

Let be a prime number, and let , and be mutually independent random variables all uniformly distributed on . Set

where stands for sum modulus . According to [9] the sequence is composed by pairwise independent random variables and it is stationary. Moreover, these random variables are not mutually independent because, by construction, for every we have that

and so,

| (15) |

Therefore, the knowledge of the random variables completely determines the value of .

Now, given , let be the quantile of order of the standard Gaussian distribution. For every , let us define the random variable conditionally to as follows: If , then draw the value of with a standard Gaussian distribution conditioned to be in the interval , and independent of all the other random variables.

Since is uniformly distributed on , we obviously have that is a standard Gaussian r.v.. Moreover, the sequence inherits the remaining properties of . It is a strictly stationary sequence of pairwise independent Gaussian random variables.

However, if and we are aware of the values , we can recover the values and, because of (15), we may deduce the value of . With this information, we know to which interval belongs. Therefore, the random variables are not mutually independent and so, the process is not Gaussian.

We have simulated the previous process times for different values of and sample sizes Then, we have applied the RP test at the level The rejection rates appear in Table 6.5.

| .1448 | .1268 | .1676 | .1516 | .1602 | .1380 | .1146 | |

| .3698 | .3654 | .4938 | .5154 | .5822 | .5590 | .5588 | |

| .6382 | .6386 | .6814 | .7250 | .7802 | .7608 | .7700 |

Table 6.5.

Rejection rates for different sample sizes applying the RP test to the process at the level .

For comparison, we show in Table 6.6 the rates of rejection when using the E, G and GE tests in the case . Since these tests check for the non-Gaussianity of the marginal, the rejection rates are not too high. However, it is worth to pay some attention to the rejection rates in this table. To begin with, they are below the intended level (except GE with ), but, more surprisingly, they show some decrease when the sample size increases. We think that this is due to the fact that these tests see the process as more Gaussian than a Gaussian process.

The reason is that when we generate observations of a Gaussian process, approximately a proportion of observations are in the interval with However, the process generate exactly a proportion of observations in each interval . So that, it has a “more Gaussian” behavior than expected. Consequently the rejection rates are lower than and this fact becomes more apparent when increases.

| E | .0338 | .0266 | .0186 |

|---|---|---|---|

| G | .0372 | .0336 | .0326 |

| GE | .0520 | .0336 | .0206 |

Table 6.6.

Rejection rates using the E, G and GE tests of the process with , at the level .

6.2 Real data

In this subsection we work with the well-known Canadian lynx and Wolfer sunspot data in order to illustrate the behavior of the random projection test. The Canadian lynx data consists on the annual record of the number of lynxes trapped in the Mackenzie River district of the North-West Canada for the period from 1821 to 1934 while the Wolfer sunspot data consists on the annual record of the sunspot activity in the period from 1700 to 1960. These data were used in [11] and previously in [30], obtaining in both cases that the processes are not Gaussian.

We perform the random projection procedure to the lynx and sunspot data following the indications in Subsection 5.2. The obtained -values are displayed in Table 6.7 together with those gotten in [11] and in [30].

| RP | Epps | S.R. & G | |

|---|---|---|---|

| lynx | |||

| sunspot |

Table 6.7.

7 Discussion

In this paper we have introduced the random projection test, RP-test, to check the Gaussianity of stationary processes. Given a sample, this test is based in a three steps procedure. First, it is required to draw a vector h in a suitable Hilbert space. Then, the sample is projected on the one-dimensional space spanned by . Finally, we take advantage of the fact that, with probability one, the initial process is Gaussian if the marginal of the projected one is Gaussian. Therefore, we only need to use a test to check the Gaussianity of the marginal of a stationary process. In the final step we use a combination of the Epps and Lobato and Velasco tests.

The comparison of the RP-procedure with the Epps and Lobato and Velasco tests (as well as with the combination of them) in situations in which the marginal is not Gaussian is not bad, and there are cases in which the proposed test is clearly better. Moreover, the RP test is able to detect alternatives with Gaussian marginal, while the other tests are not designed to do this task.

In spite of the rejection rates shown in Table 6.5 are above the nominal level, they are not so high, mostly when the sample size is . A simple way to improve these rates is to increase the number of random projections using the correction described in Section 3.4. From Table 7.1 it can be seen how an increase in the number of employed random projections improves noticeably the rates. In this table half of the projections are taken using the distribution and the other half with the and in each case we compute half of the -values with the E test and the other half with the G test.

| .1448 | .1906 | .2288 | .2674 | |

| .3654 | .5772 | .6988 | .8064 | |

| .6814 | .7688 | .8498 | .8628 |

Table 7.1.

Rejection rates for different sample sizes applying the RP test with projections to the process with .

Acknowledgment. This research has been carried out partially during a stay of J.A. Cuesta-Albertos at Université Paul Sabatier, Toulouse, France, supported by the Spanish Ministerio de Educación under grant PR2009-0355.

References

- [1] An, H.Z., Chen, Z.G. and Hannan, E.J. (1982). Autocorrelation, autoregression and autoregressive approximation. Ann. Statist. 10(3), 926–936.

- [2] Anderson, T. W. (2003). An introduction to multivariate statistical analysis. John Wiley & Sons.

- [3] Azencott, R and Dacunha-Castelle, D. (1986). Series of Irregular Observations: Forecasting and Model Building. Springer.

- [4] Benjamini, Y. and Hochberg, Y. (1995). Controlling the false discovery rate: a practical and powerful approach to multiple testing. J. Roy. Statist. Soc. Ser. B 57(1), 289–300.

- [5] Benjamini, Y. and Yekutieli, D. (2001). The control of the false discovery rate in multiple testing under dependency. Ann. Statist. 29(4), 1165–1188.

- [6] Bowman, K.O. and Shenton, L.R. (1975). Omnibus test contours for departures from normality based on and Biometrika 62(2), 243–250.

- [7] Cuesta-Albertos, J.A., del Barrio, T., Fraiman, R. and Matrán, C. (2007). The random projection method in goodness of fit for functional data. Computat. Statist. Data Anal. 51, 4814–4831.

- [8] Cuesta-Albertos, Fraiman, R. and Ransford, T. (2007). A sharp form of the Cramér-Wold theorem. J. Theoret. Probab. 20, 201–209.

- [9] Cuesta-Albertos, J.A. and Matrán, C. (1991). On the asymptotic behavior of sums of pairwise independent random variables. Statist. Probab. Lett. 11(3), 201–210.

- [10] Doob, J.L. (1953). Stochastic Processes. John Wiley & Sons.

- [11] Epps, T. W. (1987). Testing that a stationary time series is Gaussian. Ann. Statist. 15 (4), 1683–1698.

- [12] Gaposhkin, V. F. (1980). Almost sure convergence of estimates for the spectral density of a stationary process. Theory Probab. Appl. 25, 169–176.

- [13] Gasser, T. (1975). Goodness-of-fit tests for correlated data. Biometrika 62(3), 563–570.

- [14] Gebelein, H. (1941). Das statistische Problem der Korrelation als Variations- und Eigenwertproblem und sein Zusammenhang mit der Ausgleichsrechnung. Z. Angew. Math. Mech. 21, 364–379.

- [15] Gershenfeld, N (2000). The nature of mathematical modeling Cambridge: Cambridge Univ. Press.

- [16] Hannan, E.J. (1970). Multiple Time Series. John Wiley & Sons.

- [17] Ibragimov, I.A. and Rozanov, Y. A. (1978) Gaussian random processes. Springer.

- [18] Jarque, C.M. and Bera, A.K. (1987). A test for normality of observations and regression residuals. Internat. Statist. Rev. 55, 163-172.

- [19] Kavalieris, L. (2008). Uniform convergence of autocovariances. Statist. Probab. Lett. 78(6), 830–838.

- [20] Laha, R.G. and Rohatgi, V.K. (1979). Probability Theory. John Wiley & Sons.

- [21] Lobato, I.N. and Velasco, C. (2004). A simple test of normality for time series. Econometric Theory. 20(4), 671–689.

- [22] Loève, M. (1977). Probability Theory I. Springer.

- [23] Mielniczuk, J. (2000). Some properties of random stationary sequences with bivariate densities having diagonal expansions and nonparametric estimators based on them. J. Nonparametr. Statist. 12(2), 223–243.

- [24] Moulines, E. and Choukri, K. (1996). Time-domain procedures for testing that a stationary time-series is Gaussian. IEEE Trans. Sig. Proc. 44(8), 2010–2025.

- [25] Nelder, J.A. and Mead, R. (1965). A simplex method for function minimization. Comput. J. 7, 308–313.

- [26] Pitman, J. (2006). Combinatorial stochastic processes. Lectures from the 32nd Summer School on Probability Theory held in Saint-Flour. Springer.

- [27] Press, W.H., Teukolsky, S.A., Vetterling, W.T. and Flannery, B.P. (2007). Numerical Recipes. The Art of Scientific Computing. Cambridge University Press.

- [28] Rudin, W. (1966). Real and Complex Analysis Mc Graw-Hill.

- [29] Stein, M. (1999). Interpolation of Spatial Data: Some Theory for Kriging. Springer.

- [30] Subba Rao, T. and Gabr, M.M. (1980). A test for linearity of stationary time series. J. ime Ser. Anal. 1, 145–158.