Asymptotic formulae for implied volatility in the Heston model ††thanks: The authors would like to thank J. Appleby, J. Feng, J.P. Fouque, J. Gatheral, A. Gulisashvili, M. Keller-Ressel, A. Lewis, R. Lee and C. Martini for many useful discussions and the anonymous referees for useful comments.

Abstract

In this paper we prove an approximate formula expressed in terms of elementary functions for the implied volatility in the Heston model. The formula consists of the constant and first order terms in the large maturity expansion of the implied volatility function. The proof is based on saddlepoint methods and classical properties of holomorphic functions.

1 Introduction

In financial markets stochastic models are widely used by traders and risk managers to price and hedge financial products. The models are chosen on economic grounds to reflect the observed characteristics of market data, such as leptokurtic returns of asset prices and random instantaneous volatility of these returns. Pricing and hedging in realistic models are numerically intensive procedures that need to be performed very quickly because future investment decisions depend on the outcomes of these computations. Therefore market practitioners pay particular attention to tractability when deciding which model to use. Among the plethora of possible choices, stochastic volatility models are extremely popular particularly in equity, foreign exchange and interest rate markets since (i) they feature most of the characteristics of these markets, and (ii) they are numerically tractable.

In practice, stochastic volatility models are first calibrated on market data, then used for pricing. Pricing financial products is mathematically tantamount either to solving a PDE problem with boundary conditions (the final payoff of the product) or to calculating the expectation of this payoff using probabilistic tools such as Monte Carlo simulation or stochastic integration. For most models closed-form formulae are scarcely available, and accurate algorithms have been extended and used such as finite-differences [24], ADI schemes [21], or quadrature [2] methods. The calibration step involves a proper selection of the data to be fitted by a model. A common practice is to calibrate the so-called implied volatility rather than option prices directly. The implied volatility is a standardised measure of option prices which makes them comparable even though the underlying assets are not the same. Since this calibration step is based on optimisation algorithms, the lack of a closed-form formula for the implied volatility makes it very time consuming. For instance, the SABR stochastic volatility model has become very popular because a closed-form approximation formula for the implied volatility was derived in [18] and hence made the model easily tractable. Likewise, perturbation methods as developed in [13] have proved to be very useful for obtaining a closed-form approximation formula of option prices. Although these methods only hold under some constraints on the parameters, they provide useful initial reference points for calibration.

The Heston model [20] introduced in 1993 has become one of the most widely used stochastic volatility models in the derivatives market (see [14], [27], [2], [3], [28]). In this paper, we provide a closed-form approximation for the implied volatility in this model. The idea behind this result is the following: suppose one wants to calibrate the Heston model on market data. This can be performed in two different ways: (i) one uses a global optimisation algorithm, which involves computing the implied volatility at each observed point until the algorithm converges; (ii) one specifies an initial set of parameters for the model and runs a local optimisation algorithm such as the least-squares method. The latter solution is the most widely used in practice since it is less computer-intensive. However its robustness heavily relies on the initial set of parameters to be specified. Simple closed-form approximations for the Heston model make this choice robust and accurate. One first calibrates the approximation on market data—which is straightforward since this is a closed-form—then one uses this calibrated set of parameters as a starting point in the whole calibration process.

Let us consider an European option with maturity and maturity-dependent strike , then our main result is the following asymptotic closed-form formula for the implied volatility :

| (1) |

as the maturity tends to infinity, where is defined in (18), in (12) and in (17). For a constant strike , we obtain the following formula:

| (2) |

as the maturity tends to infinity, where is given by (8) and by (9).

It is a well-known fact that for a fixed strike, the implied volatility flattens as the maturity increases [31]; this is confirmed by formula (2) above, the zeroth order term of which was already known (see [27], [12]). However, the maturity-dependent strike formulation in formula (1) above reveals that the implied volatility smile does not flatten but rather spreads out in a very specific way as the maturity increases.

In the fixed-strike case, Lewis [27] pioneered the research on large-time asymptotics of implied volatility in stochastic volatility models by studying the first eigenvalue and eigenfunction of the generator of the underlying stochastic process. Recently Tehranchi [33] studied the large-time behaviour of the implied volatility when the stock price is a non-negative local martingale and obtained an analogue of formula (2) in that setting. Comparatively, there has been a profusion of work on small-time asymptotics, based on differential geometry techniques [19], PDE methods [6] or large deviations techniques ([11] and [10]). Likewise, many papers have studied the behaviour of the implied volatility smile in the wings (see [4], [5], [16], [17], [25]).

The proof of our main result, Theorem 2.2, is based on two methods: first, we use saddlepoint approximation methods to study the behaviour of the call price function as an inverse Fourier transform. This idea has already been applied by several authors, including [9], [15], [1] and [30] in order to speed up the computation of option pricing algorithms based on inverse Fourier transforms. We are also able to obtain the saddlepoint in closed form, thus avoiding any numerical approximations in determining it. The second step in our proof relies on Cauchy’s integral theorem and contour integration for holomorphic functions in order to obtain precise estimates of call option prices in the large maturity limit.

The paper is organised as follows. Section 2 contains the large-time asymptotic formula for call options under the Heston and the Black-Scholes models, both in the maturity-dependent and in the fixed-strike case. The proof of the main theorem, Theorem 2.2, is given in Section 5. In section 3, we translate these results into implied volatility asymptotics and prove formulae (1) and (2) above. In Section 4, we calibrate the Heston model and provide numerical examples based on formulae (1) and (2).

2 Large-time behaviour of call options

Throughout this article, we work on a model with a filtration supporting two Brownian motions, and satisfying the usual conditions. Let denote a stock price process and we let . Interest rates and dividends are considered null. We assume the following Heston dynamics for the log-stock price:

| (3) |

with .

The Feller condition ensures that is an unattainable boundary for the process . If this condition is violated zero is an attainable, regular and reflecting boundary (see chapter 15 in [22] for the classification of boundary points of one-dimensional diffusions). Since the analysis in this paper relies solely on the study of the behaviour of the Laplace transform of the process , which remains well defined even if the Feller condition is not satisfied, we do not assume that the inequality holds.

Let us now define , , and . Throughout the whole paper, we will assume . This assumption ensures (see Theorem 2.1 in [12]) that moments of greater than exist for all times . This condition is fundamental for the analysis in the paper and is usually assumed in the literature (see [23] and [3]). When this condition is violated the limiting logarithmic Laplace transform defined in (4) of the process does not have the same properties, and further research is needed to understand how the implied volatility behaves in this case. We know from [3] and [12] that is the mean-reversion level of the process under the so-called Share measure that is equivalent to the original probability measure with the Radon-Nikodym derivative given by the share price itself. If , the process will be neither mean-reverting nor ergodic under the Share measure. In the equities market this does not constitute a problem since the calibrated correlation is always negative. However this assumption may be restrictive in markets such as foreign exchange, and further research is required to relax it. Let be the limiting logarithmic moment generating function of defined as

| (4) |

for all such that the limit exists and is finite. It follows from [3] that is a well defined and strictly convex function on and is infinite outside, where

| (5) |

with and . Furthermore the function takes the following form

| (6) |

where

| (7) |

and we take the principal branch for the complex square root function in (7).

Let us now define the Fenchel-Legendre transform of , which was computed in [12] and is given by the formula

| (8) |

where the function is defined by

| (9) |

Tedious but straightforward calculations using the explicit formulae above yield the following proposition.

Proposition 2.1.

The function , where and are defined in (5), is strictly increasing, infinitely differentiable and satisfies the following properties

as well as the equation

| (10) |

Since the image of is , the function is well defined on . The following properties of are easy to prove and will be used throughout the paper:

-

(a)

for all ;

-

(b)

for all ;

-

(c)

is non-negative, has a unique minimum at and ;

-

(d)

is non-negative, has a unique minimum at and .

From the definition (8) of and relation (10), the equality in (a) follows. The inequality in (b) is a consequence of (a) and Proposition 2.1. Now, (a), (b) and Proposition 2.1 imply that is the only local minimum of the function and is therefore a global minimum. The definition of given in (8) implies . Since the stock price is a true martingale (see [3]), we have and Proposition 2.1 implies that . This proves (c). From (a) and Proposition 2.1, we know that the function has a unique minimum attained at and . Therefore (b) implies (d).

2.1 Large-time behaviour of call options under the Heston model

In this section, we derive the asymptotic behaviour of call option prices under the Heston dynamics (3) as the maturity tends to infinity, both for maturity-dependent and for fixed strikes. Before diving into the core of this paper, let us introduce the function by

| (11) |

which will feature in the main formulae of Theorem 2.2 and Proposition 2.7. The next theorem is the main result of the paper and its proof is given in Section 5.

Theorem 2.2.

Remark 2.3.

Remark 2.4.

It is proved in Proposition 2.1 that and . Note further that and .

Remark 2.5.

In order to precisely compare our result to the existing literature, we prove the following lemma, which gives the asymptotic behaviour of vanilla call options when the strike is fixed, independent of the maturity. The following lemma was derived in [27], Chapter 6; a rigorous proof is detailed here in Appendix A.

Lemma 2.6.

Under the same assumptions as Theorem 2.2, for any , we have the following behaviour for a call option with fixed strike ,

2.2 Large-time behaviour of the the Black-Scholes call option formula

By a similar analysis, we can deduce the large-time asymptotic call price for the Black-Scholes model. This result is of fundamental importance for us since it will allow us to compute the implied volatility by comparing the Black-Scholes and the Heston call option prices. Throughout the rest of the paper, we let denote the Black-Scholes price of a European call option written on a reference stock price , with strike , initial stock price , time-to-maturity , and volatility (with zero interest rate and zero dividend). Similar to Section 2, let us define the function as in (4), where . In the Black-Scholes case, it reads

| (14) |

Similarly to (8), we can define the functions and , by

| (15) |

and

| (16) |

The following proposition, proved in Appendix B, gives the behaviour of the Black-Scholes price as the maturity tends to infinity.

Proposition 2.7.

Let and let the real number satisfy for large times . Then for all , we have the following asymptotic behaviour for the Black-Scholes call option formula in the large-strike, large-time case

where

| (17) |

and where the function is defined in (11).

Remark 2.8.

If we set in Proposition 2.7, we obtain the large-time expansion for a call option under the standard Black-Scholes model with volatility and log-moneyness equal to .

As in the Heston model above, we derive here the equivalent of Proposition 2.7 when the strike does not depend on the maturity anymore.

Lemma 2.9.

With the assumptions above, we have the following behaviour for the Black-Scholes call option formula in the fixed-strike, large-time case

3 Large-time behaviour of implied volatility

The previous section dealt with large-time asymptotics for call option prices. In this section, we translate these results into asymptotics for the implied volatility. Recall that [12] and [27] have already derived the leading order term for the implied volatility in the large-time, fixed-strike case. Our goal here is to obtain the leading order and the correction term in the large-time, large-strike case. Theorem 3.1 provides the main result, i.e. the large-time behaviour of the implied volatility in the large strike case. In the following, will denote the implied volatility corresponding to a vanilla call option with maturity and (maturity-dependent) strike in the Heston model (3). We now define the functions and by

| (18) |

and

| (19) |

where is defined in (12), in (17), in (13), in (6), in (9) and in (8). They are all completely explicit, so that the functions and are also explicit. From the properties of proved on page 2.1, and are non-negative, so that is a well defined real number for all . Then the following theorem holds.

Theorem 3.1.

The functions and are continuous on and

Furthermore the error term tends to zero as goes to infinity uniformly in on compact subsets of .

Proof.

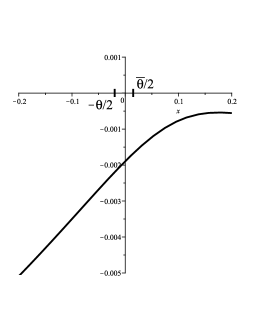

We first prove that the functions and are continuous. In fact, the continuity of the function follows from properties (c) and (d) on page 2.1. We have already observed that the function defined in (12) is discontinuous at and (see Remark 2.3). Elementary calculations show that in the neighbourhood of we have the following expansion (where )

This expansion, together with formula (17), implies that the function is also discontinuous at and . Since the quotient is strictly positive on , the function is therefore continuous on this set. The expansion above can also be used to obtain the following expression

which implies the equality . A similar argument shows continuity of at .

We now prove the formula in the theorem in the case (recall that ). Note that as defined in (18) satisfies the following quadratic equation

| (20) |

where is given by (8) and by (15). The proof of the theorem is in two steps: first, we prove the uniform convergence (on small intervals) of the implied variance to , then we derive a similar result for the first order correction term. As a first step, we have to prove that, for all , there exists such that for all and all in some small neighbourhood of we have . By Theorem 2.2 and (20) we know that for all , there exists and an interval containing such that for all in this interval and all we have the lower bound

| (21) |

and the upper bound

| (22) |

Note that

since by property (d) on page 2.1. For fixed, the function defined on is continuous and strictly decreasing, where is given in (15). Thus, for any such that for all in the small neighbourhood of define

Note that the limits are uniform in on the chosen neighbourhood of . Combining (21), (22) and Proposition 2.7, there exists such that for all and all near we have

and

Thus, by the monotonicity of the Black-Scholes call option formula as a function of the volatility, we have the following bounds for the implied volatility at maturity

In the second step of the proof we show that for all there exist and a small neighbourhood of such that, for all and all in this neighbourhood, the following holds

| (23) |

Note that the definition in (19) implies

Theorem 2.2 implies that for any there exist a small interval containing and such that for all in this interval and all we have

| (24) |

and

Let and define . The reason for this definition lies in the following identity

which holds by definition (17). By (24) there exist and a neighbourhood of such that for all in this neighbourhood and all we have

and

By strict monotonicity of the Black-Scholes price as a function of the volatility, we obtain

for all in some interval containing and all . This proves (23). An analogous argument implies the inequality in (23) for since the functions and are continuous on this set and by (20) the following identity holds

(the function is defined in (11)). In the cases a similar argument proves (23) at the point but not necessarily on its neighbourhood.

All that is left to prove is that the inequality in (23) holds uniformly on compact subsets of the complement . To every point in a compact set we can associate a small interval that contains it such that inequality (23) holds for all in that interval and all large times . This defines a cover of the compact set. We can therefore find a finite collection of such intervals that also covers our compact set. It now follows that the inequality in (23) holds for any in the compact set and all times that are larger than the maximum of the finite number of that correspond to the intervals in the finite family that covers the original set. ∎

3.1 The large-time, fixed-strike case

This section is the translation of Lemmas 2.6 and 2.9 in terms of implied volatility asymptotics, and improves the understanding of the behaviour of the Heston implied volatility in the long term. Let denote the implied volatility corresponding to a vanilla call option with maturity and fixed strike in the Heston model (3). Let us define the function by

| (25) |

where is defined in (12), in (8) and in (9). Elementary calculations show that . From the properties of on page 2.1, is then well defined as a real number for all .

Theorem 3.2.

Proof.

The proof of this theorem is similar to the proof of Theorem 3.1. It is in fact simpler because we do not have to consider special cases for . We therefore only give an argument that implies the inequality

| (26) |

holds on some small neighbourhood of for all large . Lemma 2.6 and (25) imply that for all , there exists a and a neighbourhood of such that for all in this neighbourhood and all we have

For any a continuity argument implies the existence of , which tends to zero uniformly on a neighbourhood of , such that

Therefore there exists and an interval containing such that for all in this interval and all we have

The monotonicity of the Black-Scholes formula as a function of the volatility implies (26). The proof can now be concluded in the same way as in Theorem 3.1. ∎

4 Numerical results

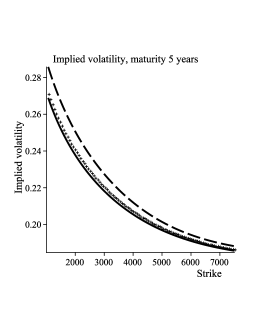

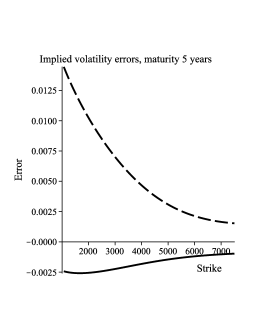

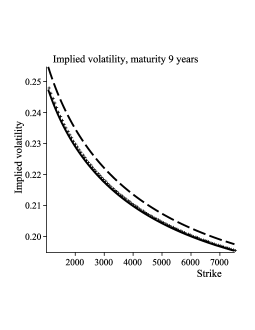

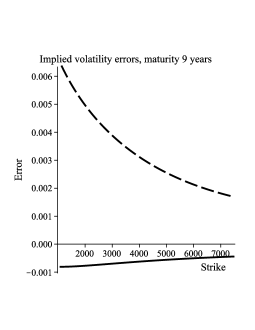

We present here some numerical evidence of the validity of the asymptotic formula for the implied volatility obtained in Theorem 3.1. We calibrated the Heston model on the European vanilla options on the Eurostoxx 50 on February, 15th, 2006. The maturities range from one year to nine years, the strikes from up to , and the initial spot equals . The calibration, performed using the Zeliade Quant Framework, by Zeliade Systems, on the whole implied volatility surface gives the following parameters: , , , and . We then use these calibrated parameters to generate an implied volatility smile for two different maturities, and years (note that for convenience the smiles were generated with interest rates and dividends equal to zero). The two plots below contain the generated implied volatility smile for the Heston model for the two maturities as well as the zeroth and first order approximations obtained in (18) and in Theorem 3.1. The errors plotted are the differences between the generated Heston implied volatility and the implied volatility obtained by the two asymptotic approximations.

5 Proof of Theorem 2.2

The proof of the theorem is divided into a series of steps: we first write the Heston call price in terms of an inverse Fourier transform of the characteristic function of the stock price (5.1). Then we prove a large-time estimate for the characteristic function (Lemma 5.1). The next step is to deform the contour of integration of the inverse Fourier transform through the saddlepoint of the integrand (Equation (9) and Proposition 2.1). Finally, studying the behaviour of the integral around this saddlepoint (Proposition 5.8) and bounding the remaining terms (Lemma 5.6) completes the proof. The special cases and in formula (12) are proved in Sections 5.3 and 5.4.

5.1 The Lee-Fourier inversion formula for call options

Using similar notation to Lee [26], set

and define the characteristic function of by

From Theorem 1 in [28] and Proposition 3.1 in [3], we know that can be analytically extended for any such that , and from our assumptions on the parameters in Section 2, for all . By Theorem 5.1 in [26], for any , we have the following Fourier inversion formula for the price of a call option on

where and is a contour such that . The first four terms on the right hand side are complex residues that arise when we cross the poles of at and . We now set , substitute to , and use the fact that is a true martingale for all (see Proposition 2.5 in [3]). From now on, as will always denote a complex number, we use the notation for . Note that

that is an even function and an odd function. Clearly the normalised call price is real, so if we take the real part of both sides and break up the integral, we obtain

| (27) |

for any , where, for any , we define the contours

| (28) |

and

| (29) |

For ease of notation, we do not write explicitly the dependence of these contours on . We will see later how to choose . In the following lemma, we characterise the large-time asymptotic behaviour of the characteristic function .

Lemma 5.1.

If is not in , this large time behaviour of still holds, but might be null (for instance if ) so that does not tend to as .

Proof.

From [2], we have, for all such that ,

| (30) |

where is defined in (7), is the analytic extension of formula (6) and the correct branch for the complex logarithm and the complex square root function is the principal branch (see also [2] and [28]) and is defined by

| (31) |

For all such that , we have . Let

Then we have

Then, as tends to infinity we have

for some constant . Set and the lemma follows. ∎

5.2 The saddlepoint and its properties

We first recall the definition of a saddlepoint in the complex plane (see [7]):

Definition 5.2.

Let be an analytic complex function on an open set . A point such that the complex derivative vanishes is called a saddlepoint.

Note that the function defined in (4) can be analytically extended and we define for every the function by

| (32) |

Note that the exponent of the integrand in (5.1) has the form by Lemma 5.1, therefore the saddlepoint properties of given in the following elementary lemma are fundamental.

Lemma 5.3.

The saddlepoints of the complex function are given by

where .

Proof.

Since we are looking for the saddlepoint in , we can use the representation in (6) for the function . Therefore the equation is quadratic and hence has the two purely imaginary solutions since the expression is strictly positive for any . It is also clear from the definition of and given in (5) and the assumptions on the coefficients that , and therefore are saddlepoints of . ∎

The next task is to choose the saddlepoint of the function in such a way that it converges to the saddlepoint of the function for all , where is given by (14), in the Black-Scholes model as both the volatility of volatility and the correlation in model (3) tend to zero. It is easy to see that the saddlepoint of equals for any , were is given by (16). We can rewrite defined in Lemma 5.3 as

| (33) |

where is defined page 2. The first term converges to and the last one to as tends to . When both and tend to , a Taylor expansion at first order of the third term gives

| (34) |

Take now the positive sign in (33), then the second and third terms cancel out in the limit because converges to as tends to . In that case we have for all , where the Black-Scholes variance is equal to . If we were to take for the saddlepoint, in the limit we would not recover by (34), since the function has no limit as the pair tends to . Therefore we define the saddlepoint to be . Moreover we observe the following equality

where is defined in (9).

Remark 5.4.

In the fixed strike case, i.e. when , we obtain

The corresponding saddlepoint is the same as the one in Chapter 6 in [27].

The following lemma is of fundamental importance and will be the key tool for Proposition 5.8.

Lemma 5.5.

Let . Then, for any , the function has a unique minimum at and is strictly decreasing (resp. increasing) for (resp. ).

Proof.

Note that the statement in the lemma is equivalent to the map having a unique minimum at for any and being increasing (resp. decreasing) on the positive (resp. negative) halfline. Let , then

where

From the identity and the fact that the principal value of the square-root is used, we get

| (35) |

is monotonically increasing in , and . First, note

that , hence is a parabola with a unique minimum at , so that, from (35), it suffices to prove the following claim:

Claim: For every , the function has a unique (strictly positive) minimum attained at and is strictly increasing (resp. decreasing) for (resp. ).

Let us write , for all , where . We have

| (36) |

The coefficient and the constant are strictly positive, so the claim follows if for all , where

The discriminant is , so that has no real root and is hence always strictly positive. This proves the claim and concludes the proof of the lemma. ∎

The following two results complete the proof of Theorem 2.2, by studying the behaviour of the two integrals in (5.1) as the time to maturity tends to infinity. The following lemma proves that the integral along is negligible and Proposition 5.8 hereafter provides the asymptotic behaviour of the integral along the contour .

Lemma 5.6.

For any and any , there exists such that for every with , we have

| (37) |

Therefore

| (38) |

where the contour is defined in (28).

Remark 5.7.

Proof.

We only need to prove (38). Recall from Lemma 5.1, after some rearrangements, that

It follows from equations (7), (6) and (31) that

Hence there exists a constant , independent of and , such that the following inequality holds

Define . Then if , where the positive constant is given in definition (28), the equality (38) follows. ∎

Proof.

Let . Applying Lemma 5.1 on the compact interval , we have

for large enough. By Lemma 5.5, we know that has a unique minimum at and the value of the function at this minimum equals by the definition of . The functions and are analytic along the contour of integration and thus, by Theorem 7.1, section 7, chapter 4 in [29], we have

as tends to infinity. The term is a higher order term which we can ignore at the level we are interested in. ∎

Lemma 5.6 and Proposition 5.8 complete the proof of Theorem 2.2 for the general case. Concerning the two special cases, we first introduce a new contour, the path of steepest descent, which represents the optimal (in a sense made precise below) path of integration. Note that, the general case can also be proved using this path, but Lemma 5.5 simplifies the proof.

5.3 Construction of the path of steepest descent

We first recall the definition of the path of steepest descent before computing it explicitly for the Heston model in the large time case.

Definition 5.9.

(see [32]) Let and be an analytic complex function. The steepest descent contour is a map such that

-

•

has a minimum at some point and along .

-

•

is constant along .

These two conditions imply that .

The following lemma computes the path of steepest descent explicitly in the Heston case for the function given in (32) passing through .

Lemma 5.10.

The path of steepest descent in the Heston model is the map defined by

where

| (40) |

Note that is strictly positive, so that the function is well defined.

Proof.

By definition, the contour of steepest descent is such that the function remains constant. So we look for the map such that , for all because is already real. Using the identity , for all , we find that the function is real along the contour . Note also that this contour is orthogonal to the imaginary axis at (see Exercise 2, Chapter 8 in [32]). ∎

Remark 5.11.

-

•

The contour depends on , but for clarity we do not write this dependence explicitly.

-

•

The construction of is such that the saddlepoint defined in (9) satisfies .

-

•

We have is an even function of , i.e. is symmetric around the imaginary axis.

We now prove Theorem 2.2 in the two special cases . In these cases, we need a result similar to Proposition 5.8, as Lemma 5.6 still holds, i.e. we need the asymptotic behaviour of the integral in (39) for the two special cases. The problem with these special cases is that in the integrand in (39) has a pole at the saddlepoint, so we need to deform the contour using Cauchy’s integral theorem and take the real part to remove the singularity, before we can use a saddlepoint expansion.

5.4 Proof of the call price expansion for the special cases

We here prove Theorem 2.2 in the case for which , , and for simplicity we also assume that (the other cases follows similarly). From (40), we see that in this case, lies below the horizontal contour such that (in the other case, lies above ). We want to construct a new contour leaving the pole outside. Let and denote the clockwise oriented circular keyhole contour parameterised as around the pole. To leave the pole outside the new contour of integration, we need to follow on , switch to the keyhole contour as soon as we touch it, follow it clockwise (above the pole), and get back to on . As is below , it intersects on its lower half, which can be analytically represented as such that . From (40), the two contours intersect at . Choose now (Lemma 5.12 makes the choice of precise and must be such that ) and define the following contours (they are all considered anticlockwise, see Figure 4)

-

•

given by , with defined in (40);

-

•

is the restriction of to the union of the intervals ;

-

•

is the portion of the circular keyhole contour which lies above , i.e. the upper half keyhole contour as well as the two sections of between and ;

-

•

are the two vertical strips joining to .

By Cauchy’s integral theorem, we now have

| (41) |

Recall that the curves and are defined in (29) and (28) respectively and rewrite (41) as

| (42) |

The integral on the left-hand side is equal to the normalised call price by Theorem 5.1 in Lee [26], which is independent of (this holds because ). For close to , we have

so that

| (43) |

Lemma 5.12 gives the behaviour of the last integral on the rhs of (5.4) as tends to for small enough.

The other integrals can be bounded as follows. By Lemma 5.6, the integral along is , for , , as tends to .

The curves are both vertical strips of length and therefore their images are compact sets. Applying the tail estimate of Lemma 5.6 along , we know that for any , there exist and such that

Lemma 5.5 implies that the real function attains its global minimum at for any fixed and is strictly decreasing (resp. increasing) for (resp. ). It therefore follows that the function , where , attains its minimum value , where is defined in (40), at the points . It can be checked directly that , and and hence for every there exists such that the following inequality holds

Therefore Lemma 5.1 yields the following inequality

We now prove the following lemma about the integral along as tends to .

Proof.

Recall that is the contour of steepest descent defined in Lemma 5.10 and that the curve is its restriction to the intervals . Note that is an even function and is an odd function. We therefore obtain

| (44) |

From (40), for around , we have , so , i.e. taking the real part removes the singularity at . Using Lemma 5.1, we then have

for some large enough, where we define the function by

Then, from (40), we have the following expansion

| (45) |

We can therefore extend the function to the map for some , where is an open disc of radius . Note that for we have and hence the function does not have a singularity at .

References

- [1] Ait-Sahalia, Y. & Yu, J. 2006 Saddlepoint Approximations for Continuous-Time Markov Processes. Journal of Econometrics, 134, 507-551. (doi:10.1016/j.jeconom.2005.07.004).

- [2] Albrecher, H., Mayer, P., Schoutens, W. & Tistaert, J. 2007 The Little Heston Trap. Wilmott Magazine, January issue, 83-92.

- [3] Andersen, L.B.G. & Piterbarg, V.V. 2007 Moment Explosions in Stochastic Volatility Models. Finance & Stochastics 11 (1), 29-50. (doi: 10.1007/s00780-006-0011-7).

- [4] Benaim, S. & Friz, P. 2009 Regular Variation and Smile Asymptotics. Mathematical Finance 19 (1), 1-12. (doi:10.1111/j.1467-9965.2008.00354).

- [5] Benaim, S. & Friz, P. 2008 Smile Asymptotics 2: Models with Known Moment Generating Functions. Journal of Applied Probability 45 (1), 16-32. (doi:10.1239/jap/1208358948).

- [6] Berestycki, H., Busca, J. & Florent, I. 2004 Computing the Implied Volatility in Stochastic Volatility models. Comm. Pure App. Math. 57 (10), 1352-1373. (doi:10.1002/cpa.20039).

- [7] Bleistein, N. & Handelsman, R.A. 1975 Asymptotic expansions of integrals. New York, London, Holt, Rinehart and Winston.

- [8] Butler, R.W. 2007 Saddlepoint Approximations with Applications. Cambridge University Press.

- [9] Carr, P. & Madan, D. 2009 Saddlepoint Methods for Option Pricing. Journ. Comp. Fin. 13 (1), 49-62.

- [10] Feng, J., Forde, M. & Fouque, J.P. 2009 Short maturity asymptotics for a fast mean-reverting Heston stochastic volatility model. SIAM Journal of Financial Mathematics 1, 126-141. (doi:10.1137/090745465).

- [11] Forde, M. & Jacquier, A. 2009 Small-time asymptotics for implied volatility under the Heston model. International Journal of Theoretical and Applied Finance 12 (6), 861-876. (doi:10.1142/S021902490900549).

- [12] Forde, M. & Jacquier, A. 2010 The large-maturity smile for the Heston model. Forthcoming in Finance & Stochastics.

- [13] Fouque, J.P., Papanicolaou, G. & Sircar, R.K. 2000 Derivatives in financial markets with stochastic volatility. Cambridge University Press, Cambridge.

- [14] Gatheral, J. 2006 The volatility surface: A practitioner’s guide. Wiley Finance, New York.

- [15] Glasserman, P. & Kim, K. 2009 Saddlepoint Approximations for Affine Jump-Diffusion Models. Journal of Economic Dynamics and Control 33, 37-52. (doi:10.1016/j.jedc.2008.04.007).

- [16] Gulisashvili, A. 2009 Asymptotic Formulas with Error Estimates for Call Pricing Functions and the Implied Volatility at Extreme Strikes. Preprint available at arxiv1.library.cornell.edu/abs/0906.0394.

- [17] Gulisashvili, A. & Stein, E. 2010 Asymptotic Behavior of the Stock Price Distribution Density and Implied Volatility in Stochastic Volatility Models. Forthcoming in Applied Mathematics and Optimization. (doi:10.1007/S00245-009-9085-x).

- [18] Hagan, P., Kumar, D., Lesniewski, A. & Woodward, D. 2002 Managing smile risk. Wilmott Magazine, September issue, 84-108.

- [19] Henry-Labordère, P. 2005 A general asymptotic implied volatility for stochastic volatility models. Preprint available at arxiv.org/abs/cond-mat/0504317.

- [20] Heston, S.L. 1993 A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies 6, 237-343. (doi:10.2307/2962057).

- [21] Hout, K.J.I. & Foulon, S. 2010 ADI Finite difference schemes for option pricing in the Heston model with correlation. Forthcoming in International Journal of Numerical Analysis and Modeling 7 (2), 303-320.

- [22] Karlin, S. & Taylor, H.M. 1981 A second course in stochastic processes. Academic Press.

- [23] Keller-Ressel, M. 2010 Moment Explosions and Long-Term Behavior of Affine Stochastic Volatility Models. Forthcoming in Mathematical Finance.

- [24] Kluge, T. 2002 Pricing Derivatives in Stochastic Volatility Models using the Finite Difference Method. Diploma thesis, Technical University, Chemnitz, available at archiv.tu-chemnitz.de/pub/2003/0008/index.html

- [25] Lee, R.W. 2004 The Moment Formula for Implied Volatility at Extreme Strikes. Mathematical Finance 14 (3) , 469-480. (doi:10.1111/j.0960-1627.2004.00200).

- [26] Lee, R.W. 2004 Option Pricing by Transform Methods: Extensions, Unification, and Error Control. Journal of Computational Finance 7 (3), 51-86.

- [27] Lewis, A. 2000 Option valuation under stochastic volatility, Finance Press, California, USA.

- [28] Lord, R. & Kahl, C. 2010 Complex Logarithms in Heston-Like Models. Forthcoming in Mathematical Finance.

- [29] Olver, F.W. 1974 Asymptotics and Special Functions. Academic Press.

- [30] Rogers, L.C.G. & Zane, O. 1999 Saddlepoint approximations to option prices. Annals of Applied Probability 9, 493-503. (doi:10.1214/aoap/1029962752).

- [31] Rogers, L.C.G. & Tehranchi, M.R. 2010 Can the implied volatility move by parallel shifts? Finance & Stochastics 14 (2), 235-248. (doi:10.1007/s00780-008-0081-9).

- [32] Stein, E.M. & Sharkarchi, R. 2003 Complex Analysis. Princeton University Press.

- [33] Tehranchi, M.R. 2009 Asymptotics of implied volatility far from maturity. Journal of Applied Probability 46 (3), 629-650. (doi:10.1239/jap/1253279843).

APPENDIX

Appendix A Proof of Lemma 2.6

Appendix B Proof of Proposition 2.7

Let us now consider a squared volatility of the form , then the Black-Scholes call option reads

| (A-1) |

and let . Recall that (see [29])

| (A-2) |

The case . As , there exists such that for all , . From (A-1), we have, using a Taylor expansion for ,

The cases and follow likewise.

The case . From (A-1), we have

The case is analogous.