Discrete Hamilton–Jacobi Theory

Abstract.

We develop a discrete analogue of Hamilton–Jacobi theory in the framework of discrete Hamiltonian mechanics. The resulting discrete Hamilton–Jacobi equation is discrete only in time. We describe a discrete analogue of Jacobi’s solution and also prove a discrete version of the geometric Hamilton–Jacobi theorem. The theory applied to discrete linear Hamiltonian systems yields the discrete Riccati equation as a special case of the discrete Hamilton–Jacobi equation. We also apply the theory to discrete optimal control problems, and recover some well-known results, such as the Bellman equation (discrete-time HJB equation) of dynamic programming and its relation to the costate variable in the Pontryagin maximum principle. This relationship between the discrete Hamilton–Jacobi equation and Bellman equation is exploited to derive a generalized form of the Bellman equation that has controls at internal stages.

Key words and phrases:

Hamilton–Jacobi equation, Bellman equation, dynamic programming, discrete mechanics, discrete-time optimal control2010 Mathematics Subject Classification:

70H20, 49L20, 93C55, 49J15, 70H05, 70H251. Introduction

1.1. Discrete Mechanics

Discrete mechanics is a reformulation of Lagrangian and Hamiltonian mechanics with discrete time, as opposed to a discretization of the equations in the continuous-time theory. It not only provides a systematic view of structure-preserving integrators, but also has interesting theoretical aspects analogous to continuous-time Lagrangian and Hamiltonian mechanics [see, e.g., 30; 33; 34]. The main feature of discrete mechanics is its use of discrete versions of variational principles. Namely, discrete mechanics assumes that the dynamics is defined at discrete times from the outset, formulates a discrete variational principle for such dynamics, and then derives a discrete analogue of the Euler–Lagrange or Hamilton’s equations from it.

The advantage of this construction is that it naturally gives rise to discrete analogues of the concepts and ideas in continuous time that have the same or similar properties, such as symplectic forms, the Legendre transformation, momentum maps, and Noether’s theorem [30]. This in turn provides us with the discrete ingredients that facilitate further theoretical developments, such as discrete analogues of the theories of complete integrability [see, e.g., 31; 33; 34] and also those of reduction and connections [20; 28; 25]. Whereas the main topic in discrete mechanics is the development of structure-preserving algorithms for Lagrangian and Hamiltonian systems [see, e.g., 30], the theoretical aspects of it are interesting in their own right, and furthermore provide insight into the numerical aspects as well.

Another notable feature of discrete mechanics, especially on the Hamiltonian side, is that it is a generalization of (nonsingular) discrete optimal control problems. In fact, as stated in Marsden and West [30], discrete mechanics is inspired by discrete formulations of optimal control problems (see, e.g., Jordan and Polak [21] and Cadzow [9]).

1.2. Hamilton–Jacobi Theory

In classical mechanics [see, e.g., 24; 3; 29; 16], the Hamilton–Jacobi equation is first introduced as a partial differential equation that the action integral satisfies. Specifically, let be a configuration space and be its cotangent bundle; and let and be arbitrary and suppose that is a solution of Hamilton’s equations

| (1.1) |

with the endpoint condition . Then calculate the action integral along the solution over the time interval , i.e.,

| (1.2) |

where we regard the resulting integral as a function of the endpoint with being the set of positive real numbers. Then by taking variation of the endpoint , one obtains a partial differential equation satisfied by :

| (1.3) |

This is the Hamilton–Jacobi equation.

Conversely, it is shown that if is a solution of the Hamilton–Jacobi equation then is a generating function for the family of canonical transformations (or symplectic flows) that describe the dynamics defined by Hamilton’s equations. This result is the theoretical basis for the powerful technique of exact integration called separation of variables.

1.3. Connection with Optimal Control and The Hamilton–Jacobi–Bellman Equation

The idea of Hamilton–Jacobi theory is also useful in optimal control theory (see, e.g., Jurdjevic [22] and Bertsekas [6]). Consider a typical optimal control problem

subject to the constraints,

and and . We define the augmented cost functional:

where we introduced the costate , and also defined the control Hamiltonian,

Assuming that

uniquely defines the optimal control , we set

We also define the optimal cost-to-go function

where for is the solution of Hamilton’s equations with the above such that ; and is the optimal cost

and the function is defined by

Since this definition coincides with Eq. (1.2), the function satisfies the H–J equation (1.3); this reduces to the Hamilton–Jacobi–Bellman (HJB) equation for the optimal cost-to-go function :

| (1.4) |

It can also be shown that the costate of the optimal solution is related to the solution of the HJB equation.

1.4. Discrete Hamilton–Jacobi Theory

The main objective of this paper is to present a discrete analogue of Hamilton–Jacobi theory within the framework of discrete Hamiltonian mechanics [23], and also to apply the theory to discrete optimal control problems.

There are some previous works on discrete-time analogues of the Hamilton–Jacobi equation, such as Elnatanov and Schiff [13] and Lall and West [23]. Specifically, Elnatanov and Schiff [13] derived an equation for a generating function of a coordinate transformation that trivializes the dynamics. This derivation is a discrete analogue of the conventional derivation of the continuous-time Hamilton–Jacobi equation [see, e.g., 24, Chapter VIII]. Lall and West [23] formulated a discrete Lagrangian analogue of the Hamilton–Jacobi equation as a separable optimization problem.

1.5. Main Results

Our work was inspired by the result of Elnatanov and Schiff [13] and starts from a reinterpretation of their result in the language of discrete mechanics. This paper further extends the result by developing discrete analogues of results in (continuous-time) Hamilton–Jacobi theory. Namely, we formulate a discrete analogue of Jacobi’s solution, which relates the discrete action sum to a solution of the discrete Hamilton–Jacobi equation. This also provides a very simple derivation of the discrete Hamilton–Jacobi equation and exhibits a natural correspondence with the continuous-time theory. Another important result in this paper is a discrete analogue of the Hamilton–Jacobi theorem, which relates the solution of the discrete Hamilton–Jacobi equation with the solution of the discrete Hamilton’s equations.

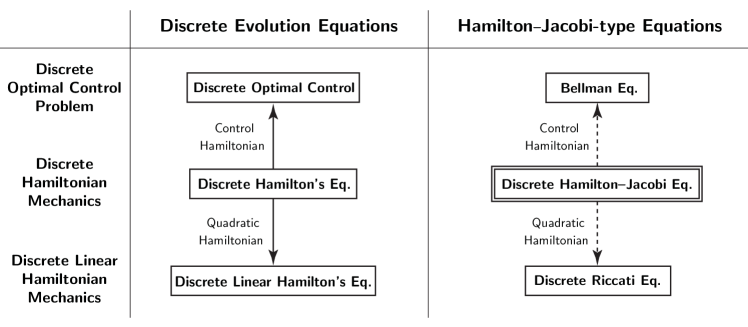

We also show that the discrete Hamilton–Jacobi equation is a generalization of the discrete Riccati equation and the Bellman equation (see Fig. 1). Specifically, we show that the discrete Hamilton–Jacobi equation applied to linear discrete Hamiltonian systems and discrete optimal control problems reduces to the discrete Riccati and Bellman equations, respectively. This is again a discrete analogue of the well-known results that the Hamilton–Jacobi equation applied to linear Hamiltonian systems and optimal control problems reduces to the Riccati (see, e.g., Jurdjevic [22, p. 421]) and HJB equations (see Section 1.3 above), respectively.

The link between the discrete Hamilton–Jacobi equation and the Bellman equation turns out to be useful in deriving a class of generalized Bellman equations that are higher-order approximations of the original continuous-time problem. Specifically, we use the idea of the Galerkin Hamiltonian variational integrator of Leok and Zhang [26] to derive discrete control Hamiltonians that yield higher-order approximations, and then show that the corresponding discrete Hamilton–Jacobi equation gives a class of Bellman equations with controls at internal stages.

1.6. Outline of the Paper

We first present a brief review of discrete Lagrangian and Hamiltonian mechanics in Section 2. In Section 3, we describe a reinterpretation of the result of Elnatanov and Schiff [13] in the language of discrete mechanics and a discrete analogue of Jacobi’s solution to the discrete Hamilton–Jacobi equation. The remainder of Section 3 is devoted to more detailed studies of the discrete Hamilton–Jacobi equation: its left and right variants, more explicit forms of them, and also a digression on the Lagrangian side. In Section 4, we prove a discrete version of the Hamilton–Jacobi theorem. In Section 5, we apply the theory to linear discrete Hamiltonian systems, and show that the discrete Riccati equation follows from the discrete Hamilton–Jacobi equation. Section 6 establishes the link with discrete-time optimal control and interprets the results of the preceding sections in this setting. Section 7 further extends this idea to derive a class of Bellman equations with controls at internal stages.

2. Discrete Mechanics

This section briefly reviews some key results of discrete mechanics following Marsden and West [30] and Lall and West [23].

2.1. Discrete Lagrangian Mechanics

A discrete Lagrangian flow , on an -dimensional differentiable manifold , can be described by the following discrete variational principle: Let be the following action sum of the discrete Lagrangian :

| (2.1) |

which is an approximation of the action integral as shown above.

Consider discrete variations , for , with . Then, the discrete variational principle gives the discrete Euler–Lagrange equations:

| (2.2) |

This determines the discrete flow :

| (2.3) |

Let us define the discrete Lagrangian symplectic one-forms by

| (2.4a) | ||||

| (2.4b) | ||||

Then, the discrete flow preserves the discrete Lagrangian symplectic form

| (2.5) |

Specifically, we have

2.2. Discrete Hamiltonian Mechanics

Introduce the right and left discrete Legendre transforms by

| (2.6a) | ||||

| (2.6b) | ||||

respectively. Then we find that the discrete Lagrangian symplectic forms Eq. (2.4) and (2.5) are pull-backs by these maps of the standard symplectic form on :

Let us define the momenta

Then, the discrete Euler–Lagrange equations (2.2) become simply . So defining

one can rewrite the discrete Euler–Lagrange equations (2.2) as follows:

| (2.7) |

Furthermore, define the discrete Hamiltonian map by

| (2.8) |

Then, one may relate this map with the discrete Legendre transforms in Eq. (2.6) as follows:

| (2.9) |

Furthermore, one can also show that this map is symplectic, i.e.,

This is the Hamiltonian description of the dynamics defined by the discrete Euler–Lagrange equation (2.2) introduced by Marsden and West [30]. Notice, however, that no discrete analogue of Hamilton’s equations is introduced here, although the flow is now on the cotangent bundle .

Lall and West [23] pushed this idea further to give discrete analogues of Hamilton’s equations: From the point of view that a discrete Lagrangian is essentially a generating function of type one [16], we can apply Legendre transforms to the discrete Lagrangian to find the corresponding generating functions of type two or three [16]. In fact, they turn out to be a natural Hamiltonian counterpart to the discrete Lagrangian mechanics described above. Specifically, with the right discrete Legendre transform

| (2.10) |

we can define the following right discrete Hamiltonian:

| (2.11) |

Then, the discrete Hamiltonian map is defined implicitly by the right discrete Hamilton’s equations

| (2.12a) | |||

| (2.12b) | |||

which are precisely the characterization of a symplectic map in terms of a generating function, , of type two. Similarly, with the left discrete Legendre transform

| (2.13) |

we can define the following left discrete Hamiltonian:

| (2.14) |

Then, we have the left discrete Hamilton’s equations

| (2.15a) | |||

| (2.15b) | |||

which corresponds to a symplectic map expressed in terms of a generation function, , of type three.

On the other hand, Leok and Zhang [26] demonstrate that discrete Hamiltonian mechanics can be obtained as a direct variational discretization of continuous Hamiltonian mechanics, instead of having to go via discrete Lagrangian mechanics.

3. Discrete Hamilton–Jacobi Equation

3.1. Derivation by Elnatanov and Schiff

Elnatanov and Schiff [13] derived a discrete Hamilton–Jacobi equation based on the idea that the Hamilton–Jacobi equation is an equation for a symplectic change of coordinates under which the dynamics becomes trivial. In this section, we would like to reinterpret their derivation in the framework of discrete Hamiltonian mechanics reviewed above.

Theorem 3.1.

Suppose that the discrete dynamics is governed by the right discrete Hamilton’s equations (2.12). Consider the symplectic coordinate transformation that satisfies the following:

-

(i)

The old and new coordinates are related by the type-one generating function111This is essentially the same as Eq. (2.7) in the sense that they are both transformations defined by generating functions of type one: Replace by . However they have different interpretations: Eq. (2.7) describes the dynamics or time evolution whereas Eq. (3.1) is a change of coordinates. :

(3.1) -

(ii)

the dynamics in the new coordinates is rendered trivial, i.e., .

Then, the set of functions satisfies the discrete Hamilton–Jacobi equation:

| (3.2) |

or, with the shorthand notation ,

| (3.3) |

Proof.

The key ingredient in the proof is the right discrete Hamiltonian in the new coordinates, i.e., a function that satisfies

| (3.4) |

or equivalently,

| (3.5) |

3.2. Discrete Analogue of Jacobi’s Solution

This section presents a discrete analogue of Jacobi’s solution. This also gives an alternative derivation of the discrete Hamilton–Jacobi equation that is much simpler than the one shown above.

Theorem 3.3.

Consider the action sums, Eq. (2.1), written in terms of the right discrete Hamiltonian, Eq. (2.11):

| (3.8) |

evaluated along a solution of the right discrete Hamilton’s equations (2.12); each is seen as a function of the end point coordinates and the discrete end time . Then, these action sums satisfy the discrete Hamilton–Jacobi equation (3.3).

Proof.

Remark 3.4.

Recall that, in the derivation of the continuous Hamilton–Jacobi equation [see, e.g., 15, Section 23], we consider the variation of the action integral, Eq. (1.2), with respect to the end point and find

| (3.11) |

This gives

and hence the Hamilton–Jacobi equation

In the above derivation of the discrete Hamilton–Jacobi equation (3.3), the difference in two action sums, Eq. (3.9), is a natural discrete analogue of the variation in Eq. (3.11). Notice also that Eq. (3.9) plays the same essential role as Eq. (3.11) does in deriving the Hamilton–Jacobi equation. Table 1 summarizes the correspondence between the ingredients in the continuous and discrete theories (see also Remark 3.4).

| Continuous | Discrete |

|---|---|

| , | |

3.3. The Right and Left Discrete Hamilton–Jacobi Equations

Recall that, in Eq. (3.8), we wrote the action sum, Eq. (2.1), in terms of the right discrete Hamiltonian, Eq. (2.11). We can also write it in terms of the left discrete Hamiltonian, Eq. (2.14), as follows:

| (3.12) |

Then, we can proceed as in the proof of Theorem 3.3: First, we have

| (3.13) |

where is considered to be a function of and , i.e., . Taking the derivative of both sides with respect to , we have

However, the terms in the brackets vanish because the left discrete Hamilton’s equations (2.15) are assumed to be satisfied. Thus, we have

| (3.14) |

Substituting this into Eq. (3.13) gives the discrete Hamilton–Jacobi equation with the left discrete Hamiltonian:

| (3.15) |

We refer to Eqs. (3.3) and (3.15) as the right and left discrete Hamilton–Jacobi equations, respectively.

3.4. Explicit Forms of the Discrete Hamilton–Jacobi Equations

The expressions for the right and left discrete Hamilton–Jacobi equations in Eqs. (3.3) and (3.15) are implicit in the sense that they contain two spatial variables and ; Theorem 3.3 suggests that one may consider and to be related by the discrete Hamiltonian dynamics defined by either the right or left discrete Hamilton’s equations (2.12) or (2.15), or equivalently, the discrete Hamiltonian map defined in Eq. (2.8). More specifically, we may write in terms of . This results in explicit forms of the discrete Hamilton–Jacobi equations, and we shall define the discrete Hamilton–Jacobi equations by the resulting explicit forms. We will see later in Section 6 that the explicit form is compatible with the formulation of the Bellman equation.

For the right discrete Hamilton–Jacobi equation (3.3), we first define the map as follows: Replace in Eq. (2.12a) by as suggested by Eq. (3.10):

Assuming this equation is solvable for , we define by , i.e., is implicitly defined by

| (3.16) |

We may now identify with in the implicit form of the right Hamilton–Jacobi equation (3.3):

| (3.17) |

where we suppressed the subscript of since it is now clear that is an independent variable as opposed to a function of the discrete time . We define Eq. (3.17) to be the right discrete Hamilton–Jacobi equation. Notice that these are differential-difference-functional equations defined on , with the spatial variable and the discrete time .

For the left discrete Hamilton–Jacobi equation (3.15), we define the map as follows:

| (3.18) |

where is the cotangent bundle projection; equivalently, is defined so that the diagram below commutes.

Notice also that, since the map is defined by Eq. (2.15), is defined implicitly by

| (3.19) |

In other words, replace in Eq. (2.15a) by as suggested by Eq. (3.14), and define as the in the resulting equation.

We may now identify with in Eq. (3.15):

| (3.20) |

where we again suppressed the subscript of . We define Eqs. (3.17) and (3.20) to be the right and left discrete Hamilton–Jacobi equations, respectively.

Remark 3.6.

Notice that the right discrete Hamilton–Jacobi equation (3.17) is more complicated than the left one (3.20), particularly because the map appears more often than does in the latter; notice here that, as shown in Eq. (3.18), the maps in the discrete Hamilton–Jacobi equations (3.17) and (3.20) depend on the function , which is the unknown one has to solve for.

However, it is possible to define an equally simple variant of the right discrete Hamilton–Jacobi equation by writing in terms of : Let us first define by

or so that the diagram below commutes.

Now, in Eq. (3.3), change the indices from to and identify with to obtain

where we again suppressed the subscript of . This is as simple as the left discrete Hamilton–Jacobi equation (3.20). However the map is, being backward in time, rather unnatural compared to . Furthermore, as we shall see in Section 6, in the discrete optimal control setting, the map is defined by a given function and thus the formulation with will turn out to be more convenient.

3.5. The Discrete Hamilton–Jacobi Equation on the Lagrangian Side

First, notice that Eq. (2.1) gives

| (3.21) |

This is essentially the Lagrangian equivalent of the discrete Hamilton–Jacobi equation (3.17) as Lall and West [23] suggest. Let us apply the same argument as above to obtain the explicit form for Eq. (3.21). Taking the derivative of the above equation with respect to , we have

and hence from the definition of the left discrete Legendre transform, Eq. (2.6b),

Assuming that is invertible, we have

where we defined the map as follows (see the commutative diagram below):

| (3.22) |

where is the projection to the second factor, i.e., . Thus, eliminating from Eq. (3.21) and then replacing by , we obtain the discrete Hamilton–Jacobi equation on the Lagrangian side:

| (3.23) |

The map defined in Eq. (3.22) is identical to defined above in Eq. (3.18) as the commutative diagram below demonstrates.

The commutativity of the square in the diagram defines the as we saw earlier, whereas that of the right-angled triangle on the lower left defines the in Eq. (3.22); note the relation from Eq. (2.9).

4. Discrete Hamilton–Jacobi Theorem

The following gives a discrete analogue of the geometric Hamilton–Jacobi theorem by Abraham and Marsden [1, Theorem 5.2.4]:

Theorem 4.1 (Discrete Hamilton–Jacobi).

Proof.

To prove the first assertion, first recall the implicit definition of in Eq. (3.16):

| (4.5) |

In particular, for , we have

| (4.6) |

where we used Eq. (4.1) and (4.2). On the other hand, taking the derivative of Eq. (3.17) with respect to ,

which reduces to

due to Eq. (4.5). Then, substituting gives

Using Eqs. (4.1) and (4.2), we obtain

| (4.7) |

Eqs. (4.6) and (4.7) show that the sequence satisfies the right discrete Hamilton’s equations (2.12).

Now, let us prove the latter assertion. First, recall the implicit definition of in Eq. (3.19):

| (4.8) |

In particular, for , we have

| (4.9) |

where we used Eq. (4.3) and (4.4). On the other hand, taking the derivative of Eq. (3.17) with respect to yields,

which reduces to

due to Eq. (4.8). Then, substituting gives

since is invertible by assumption. Then, using Eqs. (4.3) and (4.4), we obtain

| (4.10) |

Eqs. (4.9) and (4.10) show that the sequence satisfies the left discrete Hamilton’s equations (2.15). ∎

5. Application To Discrete Linear Hamiltonian Systems

5.1. Discrete Linear Hamiltonian Systems and Matrix Riccati Equation

Example 5.1 (Quadratic discrete Hamiltonian—discrete linear Hamiltonian systems).

Consider a discrete Hamiltonian system on (the configuration space is ) defined by the quadratic left discrete Hamiltonian

| (5.1) |

where , , and are real matrices; we assume that and are invertible and also that and are symmetric. The left discrete Hamilton’s equations (2.15) are

or

| (5.2) |

and hence are a discrete linear Hamiltonian system (see Section A.1).

Now, let us solve the left discrete Hamilton–Jacobi equation (3.20) for this system. For that purpose, we first generalize the problem to that with a set of initial points instead of a single initial point . More specifically, consider the set of initial points that is a Lagrangian affine space (see Definition A.2) which contains the point . Then, the dynamics is formally written as, for any discrete time ,

where is the discrete Hamiltonian map defined in Eq. (2.8). Since is a symplectic map, Proposition A.4 implies that is a Lagrangian affine space. Then, assuming that is transversal to , Corollary A.6 implies that there exists a set of functions of the form

| (5.3) |

such that ; here are symmetric matrices, are elements in , and are in .

Now that we know the form of the solution, we substitute the above expression into the discrete Hamilton–Jacobi equation to find the equations for , , and . Notice first that the map is given by the first half of Eq. (5.2) with replaced by :

| (5.4) |

Then, substituting Eq. (5.3) into the left-hand side of the left discrete Hamilton–Jacobi equation (3.20) yields the following recurrence relations for , , and :

| (5.5a) | ||||

| (5.5b) | ||||

| (5.5c) | ||||

where we assumed that is invertible.

Remark 5.2.

Remark 5.3.

We can rewrite Eq. (5.5a) as follows:

| (5.6) |

Notice the exact correspondence between the coefficients in the above equation and the matrix entries in the discrete linear Hamiltonian equations (5.2). In fact, this is the discrete Riccati equation that corresponds to the iteration defined by Eq. (5.2). See Ammar and Martin [2] for details on this correspondence.

To summarize the above observation, we have:

Proposition 5.4.

In other words, the discrete Hamilton–Jacobi equation is a nonlinear generalization of the discrete Riccati equation.

6. Relation to the Bellman Equation

In this section, we apply the above results to the optimal control setting. We will show that the (right) discrete Hamilton–Jacobi equation (3.17) gives the Bellman equation (discrete-time HJB equation) as a special case. This result gives a discrete analogue of the relationship between the H–J and HJB equations discussed in Section 1.3.

6.1. Discrete Optimal Control Problem

Let be the state variables in a vector space with and fixed and be controls in the set . With a given function , define the discrete cost functional

Then, we formulate the Standard Discrete Optimal Control Problem as follows [see, e.g., 21; 9; 4; 17]:

Problem 6.1 (Standard Discrete Optimal Control Problem).

Minimize the discrete cost functional, i.e.,

| (6.1) |

subject to the constraint,

| (6.2) |

6.2. Necessary Condition for Optimality and the Bellman Equation

We would like to formulate the necessary condition for optimality. First, introduce the augmented discrete cost functional:

where we introduced the costate with , and also defined the discrete control Hamiltonian

| (6.3) |

Then, the optimality condition, Eq. (6.1), is restated as

In particular, extremality with respect to the control implies

| (6.4) |

Now, we assume that is sufficiently regular so that this equation uniquely determines the optimal control ; and therefore, is a function of and , i.e., . We then define

| (6.5) |

and also the optimal discrete cost-to-go function

| (6.6) |

where is the optimal discrete cost functional, i.e.,

and

The above action sum has exactly the same form as Eq. (3.8) formulated in the framework of discrete Hamiltonian mechanics. Therefore, our theory now directly applies to this case: The corresponding right discrete Hamilton’s equations (2.12) are, using the expression in Eq. (6.5),

Therefore, Eq. (3.16) gives the implicit definition of as follows:

| (6.7) |

Hence, the (right) discrete Hamilton–Jacobi equation (3.17) applied to this case gives

and again using the expression for the Hamiltonian in Eq. (6.5), this becomes

Since , we obtain

| (6.8) |

which is the Bellman equation (see, e.g., Bellman [4, 5] and Bertsekas [6]).

Remark 6.2.

Notice that the discrete HJB equation (6.8) is much simpler than the discrete Hamilton–Jacobi equations (3.17) and (3.20) because of the special form of the control Hamiltonian Eq. (6.5). Also, notice that, as shown in Eq. (6.7), the term is written in terms of the given function . See Remark 3.6 for comparison.

6.3. Relation between the Discrete H–J and Bellman Equations and its Consequences

Summarizing the observation made above, we have

Proposition 6.3.

This observation leads to the following well-known fact:

Proposition 6.4.

Let be a solution to the Bellman equation (6.8). Then, the costate in the discrete maximum principle is given as follows:

where with the optimal control .

7. Generalized Bellman Equation with Internal-Stage Controls

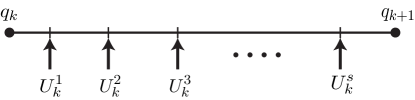

In the previous section, we showed that the discrete Hamilton–Jacobi equation recovers the Bellman equation if we apply our theory to the Hamiltonian formulation of the Standard Discrete Optimal Control Problem 6.1. In this section, we generalize the approach to derive what may be considered as higher-order discrete-time approximations of the HJB equation (1.4). Namely, we derive a class of discrete control Hamiltonians that use higher-order approximations (a more general version of Eq. (6.3)) by employing the technique of Galerkin Hamiltonian variational integrators introduced by Leok and Zhang [26]; and then, we apply our theory to obtain a class of generalized Bellman equations that have controls at internal stages.

7.1. Continuous-Time Optimal Control Problem

Let us first briefly review the standard formulation of continuous-time optimal control problems. Let be the state variable in a vector space , and fixed in , and be the control in the set . With a given function , define the cost functional

Then, we formulate the Standard Continuous-Time Optimal Control Problem as follows:

Problem 7.1 (Standard Continuous-Time Optimal Control Problem).

Minimize the cost functional, i.e.,

subject to the constraints,

and and .

A Hamiltonian structure comes into play with the introduction of the augmented cost functional:

where we introduced the costate , and also defined the control Hamiltonian,

| (7.1) |

7.2. Galerkin Hamiltonian Variational Integrator

Recall, from Leok and Zhang [26, Section 2.2], that the exact right discrete Hamiltonian is a type-two generating function for the original continuous-time Hamiltonian flow, defined by

| (7.2) |

where is the time step; is the set of continuously differentiable curves on over the time interval ; an extremum is achieved for the exact solution of Hamilton’s equations (1.1) that satisfy the specified boundary conditions. Therefore, it requires the exact solution to evaluate the the above integral, and so the exact discrete Hamiltonian cannot be practically computed in general.

The key idea of Galerkin Hamiltonian variational integrators [26] is to replace the set of curves by a certain finite-dimensional space so as to obtain a computable expression for a discrete Hamiltonian.

7.3. Galerkin Discrete Control Hamiltonian

Here, we would like to apply the above idea to the control Hamiltonian, Eq. (7.1), to obtain a discrete control Hamiltonian.

Let be a finite-dimensional space of curves defined by

with the basis functions .

-

1.

Use the basis functions to approximate the velocity over the interval ,

where and for each .

-

2.

Integrate over to obtain the approximation for the position , i.e.,

where we applied the boundary condition . Applying the boundary condition at the other endpoint yields

where . Furthermore, we introduce the internal stages,

(7.3) where .

-

3.

The exact discrete control Hamiltonian is defined as in Eq. (7.2):

Again this is practically not computable, and so we employ the following approximation: Use the numerical quadrature formula

with constants and the finite-dimensional function space to construct as follows:

where we set and and defined

where we defined and used the expression for the control Hamiltonian in Eq. (7.1); note that and for each , and that takes values in . In order to obtain an expression for , we first compute the stationarity conditions for under the fixed boundary condition :

(7.4a) (7.4b) for .

-

4.

By solving the stationarity conditions (7.4), we can express the parameters and in terms of , , and , i.e., and : In particular, assuming for each , Eq. (7.4b) gives ; this gives a set of nonlinear equations222Recall that and takes values in . satisfied by .333Note from Eq. (7.3) that is written in terms of and . Therefore, we have

Notice that the internal-stage momenta, , disappear when we substitute . Therefore, we obtain the following Galerkin discrete control Hamiltonian:

(7.5)

7.4. The Bellman Equation with Internal-Stage Controls

The Galerkin discrete control Hamiltonian, Eq. (4), gives

| (7.6) |

with

| (7.7) |

and

| (7.8) |

This is a generalized version of Eq. (6.3) with internal-stage controls as opposed to a single control per time step (see Fig. 2). Now assume that

| (7.9) |

is solvable for to give the optimal internal-stage controls . Then, we may apply the same argument as in Section 6: In particular, the right discrete Hamilton–Jacobi equation (3.17) applied to this case gives the following Bellman equation with internal-stage controls:

| (7.10) |

The following example shows that the standard Bellman equation (6.8) follows as a special case:

Example 7.2 (The standard Bellman equation).

Let , and select

Then, we have , , and . Hence, Eq. (7.3) gives (we set the endpoints to be here), and Eq. (7.4b) gives

However, the control is defined as follows (we shift the time intervals from to here):

So, we have , and thus, Eqs. (7.7) and (7.8) give

and

respectively. Notice that this approximation gives the forward-Euler discretization of the Standard Continuous-Time Optimal Control Problem 7.1 to yield the Standard Discrete Optimal Control Problem 6.1. In fact, the Bellman equation with internal-stage controls, Eq. (7.10), reduces to the standard Bellman equation (6.8):

| (7.11) |

7.5. Application to the Heisenberg System

Let us now apply the above results to a simple optimal control problem to illustrate the result:

Example 7.4 (The Heisenberg system; see, e.g., Brockett [8] and Bloch [7]).

8. Conclusion and Future Work

We developed a discrete-time analogue of Hamilton–Jacobi theory starting from the discrete variational Hamiltonian mechanics formulated by Lall and West [23]. We reinterpreted and extended the discrete Hamilton–Jacobi equation given by Elnatanov and Schiff [13] in the language of discrete mechanics. Furthermore, we showed that the discrete Hamilton–Jacobi equation reduces to the discrete Riccati equation with a quadratic Hamiltonian, and also that it specializes to the Bellman equation of dynamic programming if applied to standard discrete optimal control problems. These results are discrete analogues of the corresponding known results in the continuous-time theory. Application to discrete optimal control also revealed that the Discrete Hamilton–Jacobi Theorem 4.1 specializes to a well-known result in discrete optimal control theory. We also used a Galerkin-type approximation to derive Galerkin discrete control Hamiltonians. This technique gave an explicit formula for discrete control Hamiltonians in terms of the constructs in the original continuous-time optimal control problem. By viewing the Bellman equation as a special case of the discrete Hamilton–Jacobi equation, we could introduce the discretization technique for discrete Hamiltonian mechanics into the discrete optimal control setting; this lead us to a class of Bellman equations with controls at internal stages.

We are interested in the following topics for future work:

-

•

Application to integrable discrete systems: Theorem 4.1 gives a discrete analogue of the theory behind the technique of solution by separation of variables, i.e., the theorem relates a solution of the discrete Hamilton–Jacobi equations with that of the discrete Hamilton’s equations. An interesting question then is whether or not separation of variables applies to integrable discrete systems, e.g., discrete rigid bodies of Moser and Veselov [31] and various others discussed by Suris [33, 34].

-

•

Development of numerical methods based on the discrete Hamilton–Jacobi equation: Hamilton–Jacobi equation has been used to develop structured integrators for Hamiltonian systems. Ge and Marsden [14] developed a numerical method that preserves momentum maps and Poisson brackets of Lie–Poisson systems by solving the Lie–Poisson Hamilton–Jacobi equation approximately. See also Channell and Scovel [11] (and references therein) for a survey of structured integrators based on the Hamilton–Jacobi equation. The present theory, being inherently discrete in time, potentially provides a variant of such numerical methods.

-

•

Extension to discrete nonholonomic and Dirac mechanics: The present work is concerned only with unconstrained systems. Extensions to nonholonomic and Dirac mechanics, more specifically discrete-time versions of the nonholonomic Hamilton–Jacobi theory [19; 12; 32; 10] and Dirac Hamilton–Jacobi theory [27], are another direction for future research.

-

•

Relation to the power method and iterations on the Grassmannian manifold: Ammar and Martin [2] established links between the power method, iterations on the Grassmannian manifold, and the Riccati equation. The discussion on iterations of Lagrangian subspaces and its relation to the Riccati equation in Sections 5.1 and A.2 is a special case of such links. On the other hand, Proposition 5.4 suggests that the discrete Hamilton–Jacobi equation is a generalization of the Riccati equation. We are interested in exploring possible further links implied by the generalization.

-

•

Galerkin discrete optimal control problems: The Galerkin discrete control Hamiltonians may be considered to be a means of formulating discrete optimal control problems with higher-order of approximation to a continuous-time optimal control problem. This idea generalizes the Runge–Kutta discretizations of optimal control problems (see, e.g., Hager [18] and references therein). In fact, Leok and Zhang [26] showed that their method recovers the SPRK (symplectic-partitioned Runge–Kutta) method. Therefore, this approach is expected to provide structure-preserving higher-order numerical methods for optimal control problems.

Acknowledgments

This work was partially supported by NSF grants DMS-604307, DMS-0726263, DMS-0907949, and DMS-1010687. We would like to thank the referees, Jerrold Marsden, Harris McClamroch, Matthew West, Dmitry Zenkov, and Jingjing Zhang for helpful discussions and comments.

Appendix A Discrete Linear Hamiltonian Systems

A.1. Discrete Linear Hamiltonian Systems

Suppose that the configuration space is an -dimensional vector space, and that the discrete Hamiltonian or is quadratic as in Eq. (5.1). Also assume that the corresponding discrete Hamiltonian map is invertible. Then, the discrete Hamilton’s equations (2.12) or (2.15) reduce to the discrete linear Hamiltonian system

| (A.1) |

where is a coordinate expression for and is the matrix representation of the map under the same basis. Since is symplectic, is an symplectic matrix, i.e.,

| (A.2) |

where the matrix is defined by

with the identity matrix.

A.2. Lagrangian Subspaces and Lagrangian Affine Spaces

Let us recall the definition of a Lagrangian subspace:

Definition A.1.

Let be a symplectic vector space with the symplectic form . A subspace of is said to be Lagrangian if for any and .

We introduce the following definition for later convenience:

Definition A.2.

A subset of a symplectic vector space is called a Lagrangian affine space if for some element and a Lagrangian subspace .

The following fact is well-known (see, e.g., Jurdjevic [22, Theorem 6 on p. 417]):

Proposition A.3.

Let be a Lagrangian subspace of and be a symplectic transformation. Then, for any , the image of under the -fold composition of , i.e.,

is also a Lagrangian subspace of .

A similar result holds for Lagrangian affine spaces:

Proposition A.4.

Let be a Lagrangian affine space of and be a symplectic transformation. Then is also a Lagrangian affine space of for any . More explicitly, we have

Proof.

Follows from a straightforward calculation. ∎

A.3. Generating Functions

Now, consider the case where to apply the results from Section A.2 to the setting in Section A.1. This is a symplectic vector space with the symplectic form defined by

The key result here regarding Lagrangian subspaces on is the following:

Proposition A.5.

A Lagrangian subspace of that is transversal to is the graph of an exact one-form on , i.e., for some function which has the form

| (A.3) |

with some symmetric linear map and an arbitrary real scalar constant . Moreover, the correspondence between the Lagrangian subspaces and such functions (modulo the constant term) is one-to-one.

Proof.

First, recall that a Lagrangian submanifold of that projects diffeomorphically onto is the graph of a closed one-forms on (see Abraham and Marsden [1, Proposition 5.3.15 and the subsequent paragraph on p. 410]). In our case, is a vector space, and so the cotangent bundle is identified with the direct sum . Now, a Lagrangian subspace of that is transversal to projects diffeomorphically onto , and so is the graph of a closed one-form. Then, by the Poincaré lemma, it follows that any such Lagrangian subspace is identified with the graph of an exact one-form with some function on , i.e., .

However, as shown in, e.g., Jurdjevic [22, Theorem 3 on p. 233], the space of Lagrangian subspaces that are transversal to is in one-to-one correspondence with the space of all symmetric maps , with the correspondence given by . Hence, , or more specifically,

This implies that has the form

with an arbitrary real scalar constant . ∎

Corollary A.6.

Let be a Lagrangian affine space, where is an element in and is a Lagrangian subspace of that is transversal to . Then, is the graph of an exact one-form with a function of the form

| (A.4) |

with some symmetric linear map and an arbitrary real scalar constant .

References

- Abraham and Marsden [1978] R. Abraham and J. E. Marsden. Foundations of Mechanics. Addison–Wesley, 2nd edition, 1978.

- Ammar and Martin [1986] G. Ammar and C. Martin. The geometry of matrix eigenvalue methods. Acta Applicandae Mathematicae, 5(3):239–278, 1986.

- Arnold [1989] V. I. Arnold. Mathematical Methods of Classical Mechanics. Springer, 1989.

- Bellman [1971] R. Bellman. Introduction to the Mathematical Theory of Control Processes, volume 2. Academic Press, 1971.

- Bellman [1972] R. Bellman. Dynamic programming. Princeton University Press, 1972.

- Bertsekas [2005] D. P. Bertsekas. Dynamic Programming and Optimal Control, volume 1. Athena Scientific, 2005.

- Bloch [2003] A. M. Bloch. Nonholonomic Mechanics and Control. Springer, 2003.

- Brockett [1981] R. W. Brockett. Control theory and singular Riemannian geometry. In P. J. Hilton and G. S. Young, editors, New Directions in Applied Mathematics, pages 11–27. Springer, 1981.

- Cadzow [1970] J. A. Cadzow. Discrete calculus of variations. International Journal of Control, 11(3):393–407, 1970.

- Cariñena et al. [2010] J. F. Cariñena, X. Gracia, G. Marmo, E. Martínez, M. C. Munõz Lecanda, and N. Román-Roy. Geometric Hamilton–Jacobi theory for nonholonomic dynamical systems. International Journal of Geometric Methods in Modern Physics, 7(3):431–454, 2010.

- Channell and Scovel [1990] P. J. Channell and C. Scovel. Symplectic integration of Hamiltonian systems. Nonlinearity, 3(2):231–259, 1990.

- de León et al. [2010] M. de León, J. C. Marrero, and D. Martín de Diego. Linear almost Poisson structures and Hamilton–Jacobi equation. Applications to nonholonomic mechanics. Journal of Geometric Mechanics, 2(2):159–198, 2010.

- Elnatanov and Schiff [1996] N. A. Elnatanov and J. Schiff. The Hamilton–Jacobi difference equation. Functional Differential Equations, 3(279–286), 1996.

- Ge and Marsden [1988] Z. Ge and J. E. Marsden. Lie–Poisson Hamilton–Jacobi theory and Lie–Poisson integrators. Physics Letters A, 133(3):134–139, 1988.

- Gelfand and Fomin [2000] I. M. Gelfand and S. V. Fomin. Calculus of Variations. Dover, 2000.

- Goldstein et al. [2001] H. Goldstein, C. P. Poole, and J. L. Safko. Classical Mechanics. Addison Wesley, 3rd edition, 2001.

- Guibout and Bloch [2004] V. Guibout and A. M. Bloch. A discrete maximum principle for solving optimal control problems. In 43rd IEEE Conference on Decision and Control, volume 2, pages 1806–1811 Vol.2, 2004.

- Hager [2000] W. W. Hager. Runge–Kutta methods in optimal control and the transformed adjoint system. Numerische Mathematik, 87(2):247–282, 2000.

- Iglesias-Ponte et al. [2008] D. Iglesias-Ponte, M. de León, and D. Martín de Diego. Towards a Hamilton–Jacobi theory for nonholonomic mechanical systems. Journal of Physics A: Mathematical and Theoretical, 41(1), 2008.

- Jalnapurkar et al. [2006] S. M. Jalnapurkar, M. Leok, J. E. Marsden, and M. West. Discrete Routh reduction. Journal of Physics A: Mathematical and General, 39(19):5521–5544, 2006.

- Jordan and Polak [1964] B. W. Jordan and E. Polak. Theory of a class of discrete optimal control systems. Journal of Electronics and Control, 17:694–711, 1964.

- Jurdjevic [1997] V. Jurdjevic. Geometric control theory. Cambridge University Press, Cambridge, 1997.

- Lall and West [2006] S. Lall and M. West. Discrete variational Hamiltonian mechanics. Journal of Physics A: Mathematical and General, 39(19):5509–5519, 2006.

- Lanczos [1986] C. Lanczos. The Variational Principles of Mechanics. Dover, 4th edition, 1986.

- Leok [2004] M. Leok. Foundations of Computational Geometric Mechanics. PhD thesis, California Institute of Technology, 2004.

- Leok and Zhang [2011] M. Leok and J. Zhang. Discrete Hamiltonian variational integrators. IMA Journal of Numerical Analysis, 2011.

- [27] M. Leok, T. Ohsawa, and D. Sosa. Hamilton–Jacobi theory for degenerate Lagrangian systems with constraints. in preparation.

- Leok et al. [2004] M. Leok, J. E. Marsden, and A. Weinstein. A discrete theory of connections on principal bundles. Preprint, 2004.

- Marsden and Ratiu [1999] J. E. Marsden and T. S. Ratiu. Introduction to Mechanics and Symmetry. Springer, 1999.

- Marsden and West [2001] J. E. Marsden and M. West. Discrete mechanics and variational integrators. Acta Numerica, pages 357–514, 2001.

- Moser and Veselov [1991] J. Moser and A. P. Veselov. Discrete versions of some classical integrable systems and factorization of matrix polynomials. Communications in Mathematical Physics, 139(2):217–243, 1991.

- Ohsawa and Bloch [2009] T. Ohsawa and A. M. Bloch. Nonholonomic Hamilton–Jacobi equation and integrability. Journal of Geometric Mechanics, 1(4):461–481, 2009.

- Suris [2003] Y. B. Suris. The problem of integrable discretization: Hamiltonian approach. Birkhäuser, Basel, 2003.

- Suris [2004] Y. B. Suris. Discrete Lagrangian models. In Discrete Integrable Systems, volume 644 of Lecture Notes in Physics, pages 111–184. Springer, 2004.