A Heat Kernel Approach to Interest Rate Models

Abstract.

We construct default-free interest rate models in the spirit of the well-known Markov funcional models: our focus is analytic tractability of the models and generality of the approach. We work in the setting of state price densities and construct models by means of the so called propagation property. The propagation property can be found implicitly in all of the popular state price density approaches, in particular heat kernels share the propagation property (wherefrom we deduced the name of the approach). As a related matter, an interesting property of heat kernels is presented, too.

Key Wordes: Interest rate models, Markov-functional, state price density, heat kernel.

1. Introduction

The heat kernel approach (HKA for short), which will be presented and discussed in this paper, is a systematic method to construct state price densities which are analytically tractable. To be precise on analytic tractability, we mean with this notion that bond prices can be calculated explicitly, and that caps, swaptions or other derivatives on bonds can be calculated up to one integration with respect to the law of the underlying factor Markov process. Therefore such models can be easily calibrated to market data and are useful for pricing and hedging purposes, but also for purposes of risk management.

The original motivation of introducing the HKA was in modelling of interest rates with jumps. In the HJM framework (Heath, Jarrow and Morton, 1992), the drift condition becomes quite complicated (see H. Shirakawa’s pioneering work (Shirakawa, 1991), see also (Akahori and Tsuchiya, 2006) and references therein) if taking jumps into account, while in the spot rate approach, one will find it hard to obtain explicit expressions of the bond prices (the affine class is almost the only exception). In (Akahori and Tsuchiya, 2006), the state price density approach111The state price density, which is sometimes called the pricing kernel, or the state price deflater, is, roughly speaking, a Radon Nikodym derivative multiplied by a stochastic discount factor. A brief survey of the state price density and its relation to the interest rate modelling will be given in section 2.1. is applied and by means of transition probability densities of some Lévy processes explicit expressions of the zero coupon bond prices are obtained. The HKA is actually a full extension of the method, and thanks to the generalization its applications are now not limited to jump term structure models as we will show in the sequel.

Before the presentation of the theorem, we will give a brief survey of the state price density approaches such as the potential approach by L.C.G. Rogers (Rogers, 1997) or Hughston’s approach (Flesaker and Hughston, 1992) (Lane P. Hughston, 2005), etc, in Section 2.1 and Section 2.2. Our models are within the class of Markov functional models proposed by P. Hunt, J. Kennedy and A. Pelsser (Hunt, Kennedy and Pelsser, 2000), and therefore compatible with their practical implementations. One of the contributions of the HKA to the literature could be to give a systematic way to produce Markov functional models.

As a whole, this paper is meant to be an introduction to the HKA, together with some examples. Topics from practical viewpoint like fitting to the real market, tractable calibration, or econometric empirical studies, are not treated in this paper. Nonetheless we note that HKA is an alternative approach to practical as well as theoretical problems in interest rate modeling.

2. State price density approaches

2.1. State price density approach to the interest rate modeling

We will start from a brief survey of state price densities. By a market, we mean a family of price-dividend pairs , , which are adapted processes defined on a filtered probability space . A strictly positive process is a state price density with respect to the market if for any , it holds that

| (2.1) |

or for any ,

| (2.2) |

In other words, gives a (random) discount factor of a cash flow at time multiplied by a Radon Nikodym derivative.

If we denote by the market value at time of zero-coupon bond with maturity , then the formula (2.2) gives

| (2.3) |

From a perspective of modeling term structure of interest rates, the formula (2.3) says that, given a filtration, each strictly positive process generates an arbitrage-free interest rate model. On the basis of this observation, we can construct arbitrage-free interest rate models. Notice that we do not assume to be a submartingale, i.e. in economic terms we do not assume positive short rates.

2.2. The Flesaker-Hughston model, the Potential Approach and an approach by Wiener chaos

The rational log-normal model by Flesaker and Hughston (Flesaker and Hughston, 1992) was a first successful interest rate model derived from the state price density approach. They put

where and are deterministic decreasing process, is a one dimensional standard Brownian motion and is a constant. The model is an analytically tractable, leads to positive-short rates, and is fitting any initial yield curve. Furthermore closed-form solutions for both caps and swaptions are available. Several extensions of this approach are known.

In (Rogers, 1997), L.C.G. Rogers introduced a more systematic method to construct positive-rate models which he called the potential approach. Actually he introduced two approaches; in the first one,

where is the resolvent operator of a Markov process on a state space , is a positive function on , and is a positive constant. In the second one, is specified as a linear combination of the eigenfunctions of the generator of . Note that when is a Brownian motion, for any is an eigenfunction of its generator, and the model gives another perspective to the rational lognormal models above.

In (Lane P. Hughston, 2005) L. Hughston and A. Rafailidis proposed yet another framework for interest rate modelling based on the state price density approach, which they call a chaotic approach to interest rate modelling. The Wiener chaos expansion technique is then used to formulate a systematic analysis of the structure and classification of interest rate models. Actually, M.R. Grasselli and T.R. Hurd (Grasselli and Hurd., 2003) revisit the Cox-Ingersoll-Ross model of interest rates in the view of the chaotic representation and they obtain a simple expression for the fundamental random variable as holds. In line with these, a stable property of the second-order chaos is shown in (Akahori and Hara, 2006).

3. The Heat Kernel Approach

In this section we present the simple concepts of the heat kernel approach (HKA) and several classes of possibly interesting examples. The guiding philosophy of HKA is the following: if one can easily calculate expectations of the form for some factor Markov process , and if one knows explicitly one additional function depending on time and the state variables, then one can construct explicit formulas for bond prices, and analytically tractable formulas for caps, swaptions, etc (i.e., those formulas are evaluated by one numerical integration with respect to the law of the underlying Markov process). In other words, any explicit solution of a well-understood Kolmogorov equation with respect to some Markov process leads to a new class of interest rate models.

3.1. Basic concept

We consider a general Markov process on a polish state space and a probability space with filtration .

Definition 3.1.

Let defined on be a strictly positive function. It is said to satisfy the propagation property with respect to if

| (3.1) |

for all and . We assume furthermore that for .

Let satisfy the propagation property with respect to the Markov process and . We define then a state price density through

| (3.2) |

We clearly have the following basic assertion:

Theorem 3.2.

Bond prices are given through

for and .

Proof.

The bond prices are calculated with respect to the state price density (3.2) through

Actually, by the Markov property and by the propagation property we can calculate the right hand side,

for all and . ∎

Remark 3.3.

Notice that this remarkable simple formula is given with respect to the historical/physical measure.

A derivative with payoff on for some has at time the price

which is analytically tractable if one knows how to calculate expectations of the form .

Remark 3.4.

Notice that the initial term structure is given in the previous setting through

for .

3.2. Generic example

Let with a polish state space on a probability space with filtration . Take a measurable, bounded , then

| (3.3) |

satisfies the propagation property (3.1).

This example demonstrates that the previous theory covers the results of (Akahori and Tsuchiya, 2006). Indeed, consider a -dimensional Lévy process starting at in its natural filtration. We assume that it has a density with respect to Lebesgue measure. Then defines a Markov process on and we have that

| (3.4) |

for and .

Notice that this example can be associated to the previous Example 3.2 if one allows in the sense of distributions.

3.3. A generic affine example

Consider an affine Markov process on and such that exist. Then we define

for some numbers . In the spirit of the previous generic example we obtain

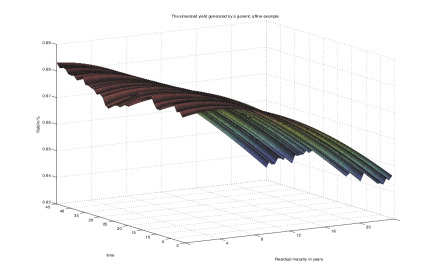

for and each initial value . Notice that the “Laplace transforms” are easily calculated for affine processes, which yields a concrete representation of the prices in the physical measure. These models are completely new interest models constructed from affine models. For instance, the derived short rate models have interesting (econometric) features. An example driven by the affine Cox-Ingersoll-Ross process is visualized in Figure 1.

3.4. Pricing formula of Swaptions

The pay-off (at its maturity ) of a (unit of) swaption is

| (3.5) |

where with is the tenor structure of the swap contract, and

is the swap rate (see e.g. (Brigo and Mercurio, 2006)*Chapter 1, section 6). Note that (3.5) can be rewritten as

| (3.6) |

Therefore in the state price density approach, the quantity

gives a fair price of the swaption. Substituting

we get

By HKA, namely

where has the propagation property w.r.t. a Markov process . We have

| (3.7) |

which is again – up to integration with respect to the law of – explicit.

3.5. Relations to short rate models

Assume that is differentiable with respect to . Then the short rate of the previous interest rate model is given through

Since the sign of the short rate is determined through

Notice that we do not necessarily have a short rate process.

3.6. Eigenfunction models

Take a finite dimensional manifold and take a Markov process with values in . A non-vanishing function with

| (3.8) |

for some is called eigenfunction of . Let , be eigenfuntions with eigenvalues , and let be decreasing functions. Set

then we notice that is a supermartingale, too. If is strictly positive and , then we can construct an arbitrage-free positive interest rate model by setting as a state price density. We call such models the eigenfunction models.

3.7. Swaption Formula via eigenfunction models

The formula (3.7) becomes extremely simple when we use the eigenfunction model.

| (3.9) |

where satisfies (3.8). By applying (3.9) on (3.7), we obtain the following result.

Theorem 3.6.

The pricing formula of the swaption is

where

and

Example 3.7 (Brownian motion with drift).

Let be a Brownian motion with drift: whose generator is where . For with , we have

Therefore, if is such that (this is always possible, take for example), then the state price density

where , gives a positive rate model. In this case

where

Notice that the Black-Scholes formula for the price at time of the call option with the strike and the maturity is given by

Remark 3.8.

This example corresponds to the Flesaker-Hughston’s rational log-normal model (Flesaker and Hughston, 1992).

Example 3.9 (squared OU process).

Let be an Ornstein-Uhlenbeck process on , whose generator is given by

where . Setting , we have

Therefore we have that is an eigenfunction with the eigenvalue . Setting and , we obtain

| (3.10) |

where ,

| (3.11) |

and

| (3.12) |

For the proof see the Appendix 5.

4. HKA and Positive Rate Models

As we have pointed out the propagation property of does not ensure that the process is a supermartingale. Thus, the interest rate model with does not exclude the possibility of negative rates. In this section we provide models based on HKA and leading to positive short rates.

4.1. Weighted heat kernel approach

Let be a positive function with propagation property with respect to a Markov process , and a weight such that for arbitrary and . Set

Then we have

Proposition 4.1.

The process is a supermartingale.

Proof.

For and , we have

Here we have used the propagation property of . Since

we have the desired result. ∎

4.2. Killed Heat kernel approach

Let be a non-negative, measurable function defined on . Put

and

| (4.1) |

Then the bond market spanned by is arbitrage-free with respect to the state price density

Indeed, this corresponds to an additional factor for added to the Markov process . Since is again a Markov process on , we notice that

defined on satisfies the propagation property. Therefore the previously described bond prices are arbitrage-free with respect to the stated state price densities for initial values . Since is decreasing in the short rates are again positive.

4.3. Trace approach

We give a third, more involved method to obtain positive rate models. Though it is only valid for symmetric Lévy processes at this stage, again the class is completely new. Let be a -dimensional Lévy process, which is symmetric in the sense that . We define . Note that in this case its Lévy symbol is positive and symmetric, i.e.

for some

which is symmetric in the sense that .

Let be a measure on such that

for any Borel set . Put

assuming it is finite (except at ) for each .

Lemma 4.2.

The function is non-negative and has the propagation property with respect to .

Proof.

First, notice that by the symmetry of we have

| (4.2) |

and for any . Then by Bochner’s theorem we know that is non-negative definite and we see that for any .

Since , for any and , we have

∎

Remark 4.3.

If the Fourier transform

exists and is bounded in , then by the symmetry of it holds that , and has the following expression:

On the other hand, let be the Lebesgue measure of . If the density of exists in , we have

That is, is the heat kernel.

We are now able to prove the following theorem on supermartingales constructed from heat kernels:

Theorem 4.4.

Let be a positive constant greater than and let be any positive constant. Set . Then is a supermartingale with respect to the natural filtration of .

Proof.

By the expression (4.2), we have

| (4.3) |

Since and is positive,

| RHS of (4.3) | ||

Thus we obtain

and then

| (4.4) |

On the other hand, by an elementary inequality we have

and since is positive, we obtain

| (4.5) |

Combining (4.4) and (4.5), we have

| (4.6) |

The right-hand-side of (4.6) is non-negative since and

is decreasing in . Finally, since we have

we now see that is a supermartingale. ∎

4.4. Examples

By the above theorem, we can now construct a positive interest rate model by setting to be a state price density, or equivalently

Here we give some explicit examples. In all examples, is a constant greater than and some positive constant.

Example 4.5 (Heat Kernel with Trace).

A simple example is obtained by letting

where the bond prices are expressed as

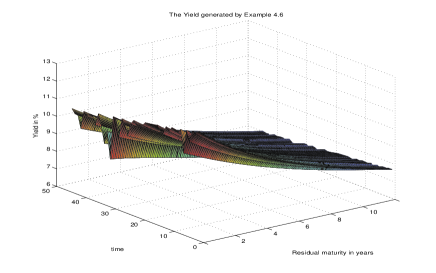

Example 4.6 (Quadratic Gaussian with Trace).

A similar model can be obtained by setting, for ,

A visualization of this model is shown in Figure 2.

Example 4.7 (Cauchy with Trace).

Let be a Cauchy process in starting from . The explicit form of the transition density of is known to be

| (4.7) |

where and (see e.g.(Sato, 1999)). Note that Cauchy processes are strictly stable (or self-similar) process with parameter ; namely,

This property is seen from their Lévy symbol: actually we have

If we set , the density turns symmetric and therefore, setting , we obtain an explicit positive term structure model. We give the explicit form of the bond prices in the case of :

The model is a modification of the Cauchy TSMs given in (Akahori and Tsuchiya, 2006).

Let be Lévy process and be a subordinator independent of . Recall that the process is usually called the subordination of by the subordinator . Among the subordinations of the Wiener process, two classes are often used in the financial context; one is the Variance Gamma processes and the other is Normal Inverse Gaussian processes, since they are analytically tractable (see (Rama Cont, 2004) and references therein). The subordinator of a Variance Gamma process (resp. Normal Inverse Gaussian process) is a Gamma process (resp. Inverse Gaussian process). If we let the drift of the Wiener process be zero, then the densities of the subordinated processes satisfies the condition for Theorem 4.4.

Example 4.8 (Variance Gamma TSMs with Trace).

The Gamma subordinator is a Lévy process with

where and are positive constants. Then the heat kernel of the subordinated Wiener process is

| (4.8) |

From this expression we have

The heat kernel (4.8) can be expressed in terms of the modified Bessel functions , , which has an integral representation

| (4.9) |

Actually we have

Example 4.9 (Normal Inverse Gaussian TSMs with Trace).

The heat kernel of the inverse Gaussian subordinator is

where and are positive constants. The heat kernel of the subordinated Wiener process is

Applying (4.9), we obtain

In particular, we have

5. Appendix

Lemma 5.1.

For , , and , it holds

| (5.1) |

where

| (5.2) |

Proof.

| (5.3) |

∎

A proof of (3.10) with (3.11) and (3.12)

Notice that

| (5.4) |

where

| (5.5) |

References

- (1)

- Akahori and Hara (2006) Akahori, Jirô and Kesuke Hara, “Lifting quadratic term structure models to infinite dimension,” Mathematical Finance, 2006, 16 (4), 635–645.

- Akahori and Tsuchiya (2006) by same author and Takahiro Tsuchiya, “What is the natural scale for a Lévy process in modelling term structure of interest rates?,” Asia-Pacific Financial Markets, 2006, 13 (4), 299–313.

- Brigo and Mercurio (2006) Brigo, Damiano and Fabio Mercurio, Interest Rate Models - Theory and Practice: With Smile, Inflation and Credit (Springer Finance), Springer, September 2006.

- Rama Cont (2004) Cont, Peter Tankov Rama, Financial modelling with jump processes Chapman & Hall/CRC Financial Mathematics Series, Chapman & Hall/CRC, Boca Raton, FL, 2004.

- Flesaker and Hughston (1992) Flesaker, Bjorn and L.P. Hughston, “Positive Interest,” Risk Magazine, 1992, 9 (1), 46–49.

- Grasselli and Hurd. (2003) Grasselli, M. R. and T. R. Hurd., “Wiener Chaos and the Cox-Ingersoll-Ross model,” 2003.

- Heath et al. (1992) Heath, David, Robert Jarrow, and Andrew Morton, “Bond pricing and the term structure of interest rates: a new methodology for contingent claims valuation,” Econometrica, 1992, 60 (1), 77–105.

- Lane P. Hughston (2005) Hughston, Avraam Rafailidis Lane P., “A chaotic approach to interest rate modelling,” Finance and Stochastics, 2005, 9 (1), 43–65.

- Hunt et al. (2000) Hunt, Phil, Joanne Kennedy, and Antoon Pelsser, “Markov-functional interest rate models,” Finance and Stochastics, 2000, 4 (4), 391–408.

- Rogers (1997) Rogers, L. C. G., “The potential approach to the term structure of interest rates and foreign exchange rates,” Math. Finance, 1997, 7 (2), 157–176.

- Rogers (2006) by same author, “One for all: the potential approach to pricing and hedging,” 2006, 8, 407–421.

- Sato (1999) Sato, Keniti, Lévy processes and infinitely divisible distributions, Vol. 68 of Cambridge Studies in Advanced Mathematics, Cambridge University Press, 1999. Translated from the 1990 Japanese original; Revised by the author.

- Shirakawa (1991) Shirakawa, Hiroshi, “Interest rate option pricing with Poisson-Gaussian forward rate curve processes,” Math. Finance, 1991, 1 (1), 77–94.