State space collapse and diffusion approximation for a network operating under a fair bandwidth sharing policy

Abstract

We consider a connection-level model of Internet congestion control, introduced by Massoulié and Roberts [Telecommunication Systems 15 (2000) 185–201], that represents the randomly varying number of flows present in a network. Here, bandwidth is shared fairly among elastic document transfers according to a weighted -fair bandwidth sharing policy introduced by Mo and Walrand [IEEE/ACM Transactions on Networking 8 (2000) 556–567] []. Assuming Poisson arrivals and exponentially distributed document sizes, we focus on the heavy traffic regime in which the average load placed on each resource is approximately equal to its capacity. A fluid model (or functional law of large numbers approximation) for this stochastic model was derived and analyzed in a prior work [Ann. Appl. Probab. 14 (2004) 1055–1083] by two of the authors. Here, we use the long-time behavior of the solutions of the fluid model established in that paper to derive a property called multiplicative state space collapse, which, loosely speaking, shows that in diffusion scale, the flow count process for the stochastic model can be approximately recovered as a continuous lifting of the workload process.

Under weighted proportional fair sharing of bandwidth () and a mild local traffic condition, we show how multiplicative state space collapse can be combined with uniqueness in law and an invariance principle for the diffusion [Theory Probab. Appl. 40 (1995) 1–40], [Ann. Appl. Probab. 17 (2007) 741–779] to establish a diffusion approximation for the workload process and hence to yield an approximation for the flow count process. In this case, the workload diffusion behaves like Brownian motion in the interior of a polyhedral cone and is confined to the cone by reflection at the boundary, where the direction of reflection is constant on any given boundary face. When all of the weights are equal (proportional fair sharing), this diffusion has a product form invariant measure. If the latter is integrable, it yields the unique stationary distribution for the diffusion which has a strikingly simple interpretation in terms of independent dual random variables, one for each of the resources of the network. We are able to extend this product form result to the case where document sizes are distributed as finite mixtures of exponentials and to models that include multi-path routing. We indicate some difficulties related to extending the diffusion approximation result to values of .

We illustrate our approximation results for a few simple networks. In particular, for a two-resource linear network, the diffusion lives in a wedge that is a strict subset of the positive quadrant. This geometrically illustrates the entrainment of resources, whereby congestion at one resource may prevent another resource from working at full capacity. For a four-resource network with multi-path routing, the product form result under proportional fair sharing is expressed in terms of independent dual random variables, one for each of a set of generalized cut constraints.

doi:

10.1214/08-AAP591keywords:

[class=AMS] .keywords:

., , and T1Supported in part by EPSRC Grant GR/586266/01. T2Supported in part by NSF Grant DMS-06-04537.

1 Introduction

We consider a connection-level model of Internet congestion control introduced and studied by Massoulié and Roberts RM . This stochastic model represents the randomly varying number of flows present in a network where bandwidth is dynamically shared between flows that correspond to continuous transfers of individual elastic documents. This model, which we shall refer to as a flow-level model, assumes a “separation of time scales” such that the time scale of the flow dynamics (i.e., of document arrivals and departures) is much longer than the time scale of the packet level dynamics on which rate control schemes such as the Transmission Control Protocol (TCP) converge to equilibrium. We consider the flow-level model operating under a family of bandwidth sharing policies introduced by Mo and Walrand MW , called weighted -fair policies. Here, is a parameter lying in . The case is called weighted proportional fair sharing and the case corresponds to what is called weighted max–min fair.

Assuming Poisson arrivals and exponentially distributed document sizes, de Veciana, Lee and Konstantopoulos DLK and Bonald and Massoulié BM studied stability of the flow-level model operating under weighted -fair bandwidth sharing policies (including limiting values of ). Lyapunov functions constructed in DLK for weighted max–min fair and proportionally fair policies, and in BM for weighted -fair policies [], imply positive recurrence of the Markov chain associated with the model when the average load on each resource is less than its capacity. Lin, Shroff and Srikant LinSch2004 , LinSchSri2006 , Sri2004 have recently given sufficient conditions for stability of a Markov model under a back-pressure algorithm when the assumption of time scale separation is relaxed. For more general document size distributions, there are a few results for specific values of or for specific distributions or topologies that provide sufficient conditions for stability of the flow-level model operating under bandwidth sharing policies Bra2005 , CST2006 , LaBeSr2004 , Mas2005 . A summary of these results is provided in the introduction to growil06 . In general, it remains an open question whether, with renewal arrivals and arbitrarily (rather than exponentially) distributed document sizes, the flow-level model is stable under an -fair bandwidth sharing policy [] when the nominal load placed on each resource is less than its capacity (see growil06 , growil07 for some first steps in this direction). Here, we restrict our attention to the case of Poisson arrivals and exponential document sizes, for which stability is well understood.

We are interested in using diffusion approximations to explore the performance of the flow-level model operating under a weighted -fair bandwidth sharing policy when the average load placed on each resource is approximately equal to its capacity, that is, the system is heavily loaded. We are particularly interested in manifestations of the phenomenon of entrainment, whereby congestion at some resources may prevent other resources from working at their full capacity.

There are several motivations for our work. One source of motivation lies in fixed-point approximations of network performance for TCP networks (see BUT , GSV , REV ). These approximations require, as input, information on the joint distribution of the numbers of flows present on different routes, where dependencies between these numbers may be induced by the bandwidth sharing mechanism. Similarly, an understanding of such joint distributions seems important if the performance models for a single bottleneck described by Ben Fredj et al. BF are to be generalized to a network.

Another motivation is that the flow-level model typically involves the simultaneous use of several resources. Due to the exponential document sizes, this model can be equated (in distribution) with a stochastic processing network (SPN) as introduced by Harrison HAR . Open multiclass queueing networks operating under head-of-the-line (HL) service disciplines are a special case of SPNs without simultaneous resource possession. For certain queueing networks of this type, it has been shown BR , Wi that suitable asymptotic behavior of critical fluid models implies a property called multiplicative state space collapse, which, in turn, validates the use of Brownian model approximations for these networks in heavy traffic. For more general SPNs, investigation of the behavior of critical fluid models, of a related notion of multiplicative state space collapse and of the implications for diffusion approximations are in the early stages of development. The analysis in this paper can be viewed as a contribution to such an investigation for models involving simultaneous resource possession. For another contribution, see the paper of Ye and Yao YY , who consider a stochastic processing network with simultaneous resource possession; in contrast to the fully heavily loaded, multiple bottleneck situation considered here, Ye and Yao consider the situation of a single heavily loaded bottleneck. A further recent contribution is the important paper of Shah and Wischik SW , who have proven multiplicative state space collapse for a class of “switched” networks with multiple bottlenecks operating under a family of scheduling policies related to the maximum weight algorithm introduced by Tassiulas and Ephremides TE .

Finally, although we restrict to exponential document sizes in this paper, we would like to relax that assumption in future work. Although this involves a significantly more elaborate stochastic model (see growil06 ) to keep track of residual document sizes (because of the processor sharing nature of the bandwidth sharing policy), knowing the results for exponential document sizes is likely to be useful for such work.

1.1 Overview

In this paper, we consider the flow-level model with Poisson arrivals and exponentially distributed document sizes operating under a weighted -fair bandwidth sharing policy for . We focus on the heavy traffic regime in which the average load placed on each resource is approximately equal to its capacity. We recall the definition of a critical fluid model from the prior work KW of two of the authors; this model is a formal functional law of large numbers approximation to the flow-level model. The asymptotic behavior of this critical fluid model was studied in KW . Here, we show how this behavior can be used to prove a property called multiplicative state space collapse. Loosely speaking, this says that in diffusion scale, the flow count process can be approximately recovered by a continuous lifting of the lower-dimensional workload process. Given the asymptotic behavior of the critical fluid model, our proof of multiplicative state space collapse follows a general line of argument pioneered by Bramson in BR , where open multiclass queueing networks operating under certain head-of-the-line (HL) service disciplines are treated. There are some differences in setup and proof details between our treatment and Bramson’s BR . These are described in detail at the beginning of Section 6. However, we wish to emphasize that our main line of argument follows that of Bramson BR . It is interesting to note that, in contrast to prior results on state space collapse for open multiclass queueing networks, our lifting map can be nonlinear (for ).

The multiplicative state space collapse result leads to a natural conjecture for a diffusion approximation to the workload process. For the case of weighted proportional fair sharing of bandwidth (), we combine multiplicative state space collapse with uniqueness in law for the diffusion DW and an invariance principle KaWi for semimartingale reflecting Brownian motions living in domains with piecewise smooth boundaries to obtain a diffusion approximation for the flow count process under a mild local traffic condition. This diffusion lives in a polyhedral cone. It behaves like Brownian motion in the interior of the cone and is confined to the cone by reflection (or regulation) at the boundary where the direction of reflection is constant on any given boundary face. We illustrate this diffusion approximation result for a simple two-resource linear network. Then, the diffusion lives in a wedge that is a strict subset of the positive quadrant. This geometrically illustrates the entrainment of resources, whereby congestion at one resource may prevent another resource from working at full capacity. We also observe how the wedge can vary with the weights. Ongoing work is directed toward establishing diffusion approximations for the workload process when . We mention some of the difficulties associated with this. These center around the fact that when and the workload dimension is three or higher, although the state space for the proposed diffusion approximation for the workload process is a cone, it is not a polyhedral cone. Indeed, the cone has curved boundary faces that intersect nonsmoothly and can even meet in cusp-like singularities. The current lack of a general existence and uniqueness theory (and an associated invariance principle) for reflecting Brownian motions in such domains is a major obstacle to proving the conjecture for .

In the case of proportional fair sharing, that is, when and all of the weights for the bandwidth sharing policy are equal, we show that the approximating diffusion has a product form invariant measure. When the latter is integrable over the state space, our results suggest a strikingly simple approximation for the joint stationary distribution of the number of flows present on different routes under proportional fair sharing and the mild local traffic condition. In this, each of the resources of the network has associated with it a dual random variable. These dual variables are independent and exponentially distributed, and the formal approximation to the number of flows on a route is proportional to the sum of the dual variables along the route.

We also indicate an extension of the product form result to the situation where document sizes are finite mixtures of exponential distributions. Under this extension, the formal approximation for the joint stationary distribution for the number of flows present on different routes is insensitive: that is, the approximation does not depend on the distributions of document sizes, other than through the means of these distributions, provided that the distributions are finite mixtures of exponentials. This result complements the known result BM , BP , RM that, for proportional fair sharing and a small class of topologies and parameters, the stationary distribution for the number of flows present on different routes is exactly insensitive: that is, the stationary distribution does not depend on the distributions of document sizes, other than through the means of these distributions.

Finally, we indicate a relation to more general models with routing. There is considerable interest in multi-path routing in the Internet and rate control schemes generalizing TCP have been proposed HSHST , KV . It is known that the stability region for the flow-level model may be strictly increased if multi-path routing is allowed HSHST , KM . We show that our results on diffusion approximations under proportional fair sharing extend to the multi-path case. The local traffic condition becomes more difficult to verify in this setting, but if it is satisfied, then our results suggest a simple approximation for the stationary distribution of the numbers of source–destination flows in terms of independently distributed dual variables, one for each generalized cut constraint.

1.2 Notation and terminology

For each positive integer , will denote -dimensional Euclidean space and the positive orthant in this space will be denoted by When , we sometimes write instead of , and instead of . The Euclidean norm of will be denoted by . Vectors in will be assumed to be column vectors unless specifically indicated otherwise. The transpose of a vector or matrix will be denoted by the use of a superscript “′”. Inequalities between vectors in will be interpreted componentwise. That is, for is equivalent to for For each and each set , the distance between and is denoted by

For , . For each , denotes the largest integer less than or equal to . Given a vector , the diagonal matrix with the entries of on its diagonal will be denoted by diag(). For positive integers and , the norm of a matrix will be given by

The set of nonnegative integers will be denoted by and the set of points in with all integer coordinates will be denoted by . A sum over an empty set of indices will be taken to have a value of zero. The cardinality of a finite set will be denoted by . For , any integer and any bounded function , let and when , let .

All stochastic processes in this paper will be assumed to have sample paths that are right-continuous with finite left limits (r.c.l.l.). We denote by the space of r.c.l.l. functions from into and we endow this space with the usual Skorokhod -topology. We denote by the space of continuous functions from into . The Borel -algebra on either or will be denoted by . Consider each of which is a -dimensional process (possibly defined on different probability spaces). The sequence is said to be tight if the probability measures induced by the on the measurable space form a tight sequence, that is, they form a weakly relatively compact sequence in the space of probability measures on . The notation “” will mean that as , the sequence of probability measures induced on by converges weakly to the probability measure induced on the same space by . We shall describe this in words by saying that converges weakly (or in distribution) to as . The sequence of processes is called C-tight if it is tight and if each weak limit point, obtained as a weak limit along a subsequence, almost surely has sample paths in .

2 Flow-level model

2.1 Network structure

We consider a network with finitely many resources labeled by . A route is a nonempty subset of (interpreted as the set of resources used by route ). We are given a finite, nonempty set of allowed routes. Let , the total number of resources, and , the total number of routes. Let be the incidence matrix which contains only zeros and ones, defined such that if resource is used by route and otherwise. We assume that has rank so that it has full row rank. We further assume that resource (bandwidth) capacities are given and that these are all strictly positive and finite.

2.2 Stochastic primitives

An active flow on route corresponds to the continuous transmission of a document through the resources used by route . Transmission is assumed to occur simultaneously through all resources on route . It is assumed that a new document arrives to route at each jump time of a Poisson process that has rate parameter and that each such document has an exponentially distributed size with mean , where . These document sizes are assumed to be independent of one another and to be independent of all arrival times of documents. The number of documents on route at time zero is assumed to be independent of the remaining sizes of those documents and these sizes are assumed to be independent and exponentially distributed with mean . Initial numbers and sizes of documents, arrival times of new documents and their sizes for different routes are assumed to be mutually independent.

2.3 Bandwidth sharing policy

Bandwidth capacity is allocated dynamically to the routes according to the following bandwidth sharing policy which was first introduced by Mo and Walrand MW . The bandwidth for a route is shared equally among all of the documents currently being transmitted over that route. Given a fixed parameter and strictly positive weights , if denotes the (random) number of flows on route at time for each and , then the bandwidth allocated to route at time is given by and this bandwidth is shared equally among all of the flows on route , where the function is defined as follows (we define it on all of as we shall later apply it to rescaled versions of ).

Let be defined such that for each , for , and when is nonempty, is the unique value of that solves the optimization problem

| (1) | |||

where for and ,

| (2) |

and the value of the right member above is taken to be if and for some . The resulting bandwidth allocation is called a weighted -fair allocation.

The properties of the function are summarized in the following proposition. This proposition is proved in the Appendix of Kelly and Williams KW .

Proposition 2.1.

For each , {longlist}

for each ;

for each ;

is continuous at for those such that ;

there exists at least one , depending on , such that

| (3) |

where

| (4) |

The are Lagrange multipliers (or dual variables) for the optimization problem, where there is one multiplier for each of the capacity constraints.

2.4 Stochastic process description

The flow count process is a Markov process with state space . We use the following (equivalent in distribution) representation for and the cumulative unused capacity process :

| (5) | |||||

| (6) |

where is a Poisson process with rate , is a Poisson process with rate , is the cumulative amount of bandwidth allocated to route up to time and

| (7) |

We assume that for each , and are represented by

| (8) |

and

| (9) |

respectively, where is a sequence of i.i.d. exponential random variables with mean and is a sequence of i.i.d. exponential random variables with mean . It is assumed that , for , are mutually independent. We define an (average) workload process by

| (10) |

where is the diagonal matrix with the entries of on its diagonal.

3 Sequence of systems and scaling

Consider an increasing sequence of positive scale parameters which converges to infinity. To ease the notation, we shall simply write in place of , where it is understood that increases to infinity through a sequence. We consider a sequence of flow-level models indexed by , where the network structure with parameters and , and bandwidth sharing policy with parameters and do not vary with . Each member of the sequence is a stochastic system, as described in the previous section. We append a superscript of to any process, sequence of random variables or parameter associated with the th system that depends on . Thus, we have processes , sequences of random variables and for , parameters and , and matrices . Let for each . We shall henceforth assume that the following heavy traffic condition holds.

Assumption 3.1 ((Heavy traffic)).

There exist and such that and for all ,

| (11) | |||||

| (12) |

Remark 3.1.

Assumption 3.1 thus implies that all resources are heavily loaded. We do not consider the case where some resources are underloaded; however, we conjecture that the diffusion approximation in this case would be as if these underloaded resources were deleted from the model.

We define fluid scaled processes as follows. For each and , let

| (13) | |||||

| (14) | |||||

| (15) |

We define diffusion scaled processes as follows. For each and , let

| (16) | |||||

| (17) | |||||

| (18) | |||||

| (19) | |||||

| (20) |

As , , are independent Poisson processes with parameters satisfying the convergence conditions , it follows that we have the following well-known functional central limit result Bi99 :

| (21) |

where and are independent -dimensional Brownian motions starting from the origin with zero drift and covariance matrices and , respectively.

Finally, we assume that, independent of (21), converges in distribution as to a -dimensional random variable.

4 Fluid model

In this section, we recall some definitions and results established in the prior work KW . These will be needed for our statement and proof of multiplicative state space collapse.

4.1 Fluid model solution

A fluid model solution can be thought of as a formal limit of the sequence as . In fact, if one assumes that converges in distribution as to a random variable taking values in , then one can show (see the Appendix of KW ) that is -tight and any weak limit point yields a fluid model solution a.s.

The following notions are used in the definition of a fluid model solution given below. A function is said to be absolutely continuous if each of its components , , is absolutely continuous. A regular point for an absolutely continuous function is a value of at which each component of is differentiable. [Since is absolutely continuous, almost every time is a regular point for . Furthermore, can be recovered by integration from its a.e. defined derivative.]

Definition 4.1.

A fluid model solution is an absolutely continuous function such that at each regular point for , we have, for each ,

| (22) |

and for each ,

| (23) |

where and .

Remark 4.1.

Note that we are not assuming uniqueness of fluid model solutions given the initial state.

4.2 Invariant manifold

Definition 4.2.

A state is called invariant (for the fluid model) if there is a fluid model solution such that for all . Let denote the set of all invariant states. We call the invariant manifold.

Remark 4.2.

Although is fixed throughout, we indicate the dependence of on explicitly here as it will be useful later on when we explain how the state space for the proposed workload diffusion approximation varies with .

Various characterizations of the invariant states were given in KW . We summarize these in Theorem 4.1 below. For this, we need the following definitions.

For each , define , to be given by

| (24) |

We call the workload associated with .

For each , define to be the unique value of that solves the following optimization problem:

| (25) | |||

where

| (26) |

(This function was introduced in BM as a Lyapunov function for the fluid model. In fact, it is a Lyapunov function for the original flow count process and can be used to show positive recurrence of when the average load on each resource is less than its capacity.) The function has the two properties stated in the next proposition.

Proposition 4.1.

The function is continuous. Furthermore, for each and ,

| (27) |

The first property is proved in Lemma 6.3 of KW . For the second property, note that for and , satisfies the constraints in (4.2) with in place of and so

| (28) |

On the other hand, by writing in place of in (28), we find that

and then, by replacing by and rearranging, we obtain

| (29) |

On combining (28) and (29), we conclude that

and by uniqueness of the solution to (4.2), we obtain the second property.

Theorem 4.1.

The following are equivalent for : {longlist}

is an invariant state (for the fluid model), that is, ;

for all ;

there exists some such that

| (30) |

.

This follows immediately from Lemma 5.1 and Theorems 5.1, 5.3 of KW .

Remark 4.3.

Note that if the conditions of Theorem 4.1 are satisfied, then satisfies conditions (3) and (4), and thus are dual variables for the optimization problem (2.3); note that we use the fact that for this. We have chosen to use to denote the dual variables associated with the invariant states, to distinguish them from the dual variables associated with arbitrary states . This distinction will be useful in our proof of convergence to a diffusion process (see Lemma 7.5), where we need to distinguish the dual variables associated with actual system states from the dual variables associated with nearby points on the invariant manifold. It is important to make this distinction because when a system state is near an invariant state and some component of the system state is near zero, it need not follow that the dual variables associated with the two states are close.

Proposition 4.2.

For each , , that is, is an invariant state.

4.3 Asymptotic properties of fluid model solutions

The next three propositions note some properties of fluid model solutions that follow from the analysis in KW and that are used in our proof of multiplicative state space collapse (see Theorem 5.1 below).

Proposition 4.3.

For each , there is a constant such that for any fluid model solution satisfying , we have for all .

The proof of this proposition is implicit in the proof of Theorem 5.2 in KW .

The next proposition states that fluid model solutions converge uniformly to the invariant manifold , where the uniformity applies across all fluid model solutions that start inside a compact subset of .

Proposition 4.4.

Fix and . There is a constant such that for each fluid model solution satisfying , we have

| (31) |

The content of this proposition is the same as that of Theorem 5.2 in KW .

Proposition 4.5.

For each and , there exists such that for any fluid model solution satisfying and , we have for all .

This proposition follows from the proof of Theorem 5.2 in KW . For completeness, we provide a few details. Fix and . By Proposition 4.3, there exists a compact set in such that for all for any fluid model solution satisfying . Let . As shown in KW , there is a continuous function that is zero on and strictly positive off such that is nonincreasing for each fluid model solution . Let . Then, and, by the properties of , there exists such that whenever is a fluid model solution satisfying and , we have . Since is a nonincreasing function, it then follows that for all . The latter implies that for all and so for all .

The following corollary shows that fluid model solutions starting on the invariant manifold stay at their starting points for all time. We note this for the reader’s interest. We do not use this corollary in our proofs.

Corollary 4.1.

Suppose that is a fluid model solution such that . Then, for all .

By Proposition 4.5, since , we have for all and hence for all . It follows from Theorem 4.1 that for each , for all such that . Then, by the fluid model dynamics (22), for each regular point of , we have

| (32) |

if and the last equality also holds if . It follows, since the absolutely continuous function can be recovered from its almost everywhere defined derivative, that for all .

5 Main results

In this section, we describe the main results of this paper. We begin with our result on multiplicative state space collapse. This is established using the asymptotic behavior of fluid model solutions described in Section 4.3. Loosely speaking, multiplicative state space collapse shows that an approximation for can be derived from one for via the continuous lifting map [see (4.2)–(26) for the definition of this map]. This lifting map can be nonlinear (for ). The multiplicative state space collapse result leads to a natural conjecture for a diffusion approximation to . In the case , assuming a mild local traffic condition and suitable initial conditions, we prove that the conjectured diffusion approximation is valid. (In Section 5.6, we indicate some of the challenges associated with establishing this conjecture for .) When and all of the weights for the bandwidth sharing policy are equal (proportional fair sharing), we use results of Harrison and Williams HaWi87 and Williams RSS to show that the diffusion has a product form invariant measure. When this measure has finite total mass, this result suggests an approximation for the stationary distribution of the flow count process which we are able to extend to the case where the document size distributions are finite mixtures of exponential distributions and to some models with multi-path routing. So as not to disrupt the flow of results and associated discussion, we defer the rather lengthy proofs of multiplicative state space collapse and of the diffusion approximation to Sections 6 and 7, respectively.

5.1 Multiplicative state space collapse

Definition 5.1 ((Multiplicative state space collapse)).

Multiplicativestate space collapse holds (for the sequence of flow-level models described in Section 3), if, for each ,

| (33) |

in probability as .

Remark 5.1.

We note here that in our form of multiplicative state space collapse, the normalization (in the denominator) is in terms of the flow count process, whereas in Bramson’s version for multiclass queueing networks BR , it is in terms of a workload process. Furthermore, the lifting maps in BR are all linear, whereas here, can be nonlinear (for ).

Remark 5.2.

If (33) holds without the factor in the denominator, then state space collapse is said to hold. Multiplicative state space collapse is more convenient for the purpose of verification and if (or ) satisfies a compact containment condition, then state space collapse follows from mutiplicative state space collapse. As was the case for open multiclass HL queueing networks Wi , in establishing our diffusion approximation result for under a mild local traffic condition, we will show for this case that multiplicative state space collapse implies state space collapse.

The following theorem is one of the main results of this paper. It is proved in Section 6.

Theorem 5.1.

Assume that

| (34) |

in probability as . Multiplicative state space collapse then holds.

5.2 Conjectured diffusion approximation

We are interested in obtaining a diffusion approximation for the scaled workload process . The multiplicative state space collapse result can then be used to obtain a diffusion approximation for the scaled flow count process .

For each , define the double fluid scaled bandwidth allocation process

| (35) |

Using (5)–(7) and (10) for the th system, the definitions of rescaled processes and (ii) of Proposition 2.1, after some simple manipulations, we obtain, for all ,

| (36) |

where

| (37) | |||||

| (38) | |||||

If we postulate that multiplicative state space collapse implies state space collapse, then, by formally (nonrigorously) passing to the limit in the expression (36) for , we can obtain a natural conjecture for a diffusion approximation to . Immediately below, we give an informal description of how one might arrive at this conjecture. Following that, we give a precise mathematical description of the diffusion process and of the conjecture.

For the following informal description, which is used to motivate the form of the conjectured diffusion approximation, we postulate that the sequence of processes converges in distribution to a 5-tuple of continuous processes . We also postulate that state space collapse (SSC) holds (not just multiplicative state space collapse). From the convergence of , SSC and continuity of the lifting map , it follows that converges in distribution to a continuous process that lives on the invariant manifold . The fact that will yield in the limit that . By the characterization of invariant states given in Theorem 4.1, it will then follow that for each and realization , there exists such that

| (40) |

Consequently, will live in the space

| (41) |

where

| (42) |

We call the workload cone. This is the state space for the conjectured diffusion approximation .

By the assumption made at the end of Section 3, we know that converges in distribution, independently of the primitive arrival and service processes. We denote the limit distribution of by . Under the postulated convergence of , will be concentrated on .

We now turn our attention to the term in the expression (36) for . Given the functional central limit theorem result (21) for the diffusion scaled arrival and service processes , and the heavy traffic Assumption 3.1, if we postulate that the double fluid scaled allocation processes achieve the nominal levels given by in the heavy traffic limit, then given by (37) will converge in distribution to the Brownian motion where for , for all and is defined in the heavy traffic Assumption 3.1. This Brownian motion starts from the origin, and has drift and covariance matrix , where we have used the facts that and for all to compute the second term in the diagonal part of the covariance matrix expression.

On examining the representation (36) for , we see that it remains to conjecture properties for the postulated limit of the scaled unused capacity process as . The limit will inherit the nondecreasing property from the . The main issue is to determine where each of the components of can increase. For the prelimit process, , to determine where its components increase, we see from (5.2) that it suffices to identify where each of the components of is strictly positive. From Proposition 2.1, if such that , then there is a Lagrange multiplier such that and

| (43) |

[For this, we note that both sides of (43) are zero if .] If is close to the nominal allocation , then, by (43), is near

the subset of obtained by setting equal to zero in (42), and then will be close to

| (45) |

which we refer to as the th face of the workload cone . Thus, one might conjecture that in the limit, can increase only when is on the face .

Combining all of the above considerations leads to the informal conjecture that converges in distribution to a -dimensional diffusion process of the form . The state space for is the workload cone and the initial distribution of is given by . In the interior of , the increments of are given by the increments of a Brownian motion with drift and covariance matrix

| (46) |

that starts from the origin. The process is confined to the cone by instantaneous “pushing” at the boundary of . The direction of push allowed when is on the boundary face is , the unit vector parallel to the positive th coordinate axis in , and the cumulative amount of push in that direction is given by the th component of the continuous nondecreasing process . (At the intersections of boundary faces, the combined effect of pushing on the individual boundary faces is a push in the direction of a convex combination of the pushing directions available from the intersecting boundary faces.) The direction of push on a given boundary face is usually called a direction of reflection, whereas it might be better thought of as a direction of regulation for the process. (The term “reflection” comes from the fact that in one dimension, when the drift is zero, the construction of such a regulated process from a Brownian motion can be achieved by a mirror reflection; although this type of construction does not generally apply in higher dimensions, the term “reflection” is still used.)

We now introduce a precise definition for the conjectured diffusion approximation to the workload process . (The delicate issue of existence and uniqueness for this process is discussed below.) This definition will be used in giving a precise statement of our conjecture. Here, is a vector in , is given by (46), is the unit vector parallel to the positive th coordinate axis and is a Borel probability measure on .

Definition 5.2.

A semimartingale reflecting Brownian motion that lives in the cone , has direction of reflection on the boundary face for each , has drift and covariance matrix , and has initial distribution on is an adapted, -dimensional process defined on some filtered probability space such that {longlist}

-a.s., for all ,

-a.s., has continuous paths, for all and has distribution ,

under , {longlist}

is a -dimensional Brownian motion starting from the origin with drift and covariance matrix ;

is a martingale,

for each , is an adapted, one-dimensional process such that -a.s., {longlist}

for all .

Remark 5.3.

We call a process satisfying the above properties an SRBM associated with the data . Here, “adapted” means adapted to the filtration . We note that this filtration need not be the one generated by —it can be larger. However, it can always be taken to be the filtration generated by . The martingale condition on is included here as we are using a “weak” definition of the process. This martingale property is needed in establishing uniqueness in law for an SRBM. The term “semimartingale” refers to the fact that is the sum of a continuous martingale and a continuous process that is locally of bounded variation. Condition (iv)(c) corresponds to the condition that can only increase when is on the boundary face .

We now give a precise statement of our conjecture.

Conjecture 5.1.

Suppose that the limit distribution of is , a probability distribution on endowed with the Borel -algebra, and suppose that

Then, converges in distribution as to a process that is an SRBM associated with the data .

We shall prove that Conjecture 5.1 holds when , provided that a mild local traffic condition holds. We state this result in the next subsection. In the remainder of the current subsection, we indicate some of the challenges associated with constructing a rigorous proof of the conjecture.

When (corresponding to weighted proportional fair sharing), we can express the cone in the simple form

| (47) |

where is an diagonal matrix with the th diagonal entry being . Thus, is a polyhedral cone. Since has full row rank and is a diagonal matrix with strictly positive diagonal entries, is a linear bijection between and . It follows from this that is a simple polyhedral cone. Necessary and sufficient conditions for the existence and uniqueness in law of SRBMs living in simple polyhedral domains have been given by Dai and Williams DW . Under these conditions, the SRBM is a diffusion, that is, a continuous strong Markov process. It will turn out that the conditions of DW are satisfied by our data when . For and , the workload cone is a wedge which is still a simple polyhedral cone. However, in general, for and , the workload cone is not a polyhedral cone (it has curved boundaries). In this case, we have some partial (unpublished) results on existence and uniqueness for SRBMs. The main impediment to obtaining a general result is that boundary faces can meet in cusp-like singularities, making it challenging to even determine whether the process can escape from the cusp and whether it can do so in a unique manner (see Section 5.6 for an example).

Even if one has existence and uniqueness of the SRBM, for any proof of the conjecture, there are a number of other challenges to overcome. First, one needs to establish -tightness of the sequence of triples . This is largely an issue of the -tightness of . One also needs to show that multiplicative state space collapse implies state space collapse. One of the most challenging aspects is to show that for any possible limit of the sequence , for each , the process can only increase when is on the boundary face . Indeed, in our informal use of (43) to arrive at our conjecture, we neglected the fact that need not be near when some component of is near zero [recall that need not be continuous when is zero]. Also, the notions of “nearness” and “closeness” used loosely in our informal description are not necessarily uniform. However, if is at or near zero when for an such that , then we can show that is near the boundary face . To take advantage of this observation, in the case when we prove the conjecture (), we will assume that a mild local traffic condition holds.

In summary, the main reasons that we are able to treat the case are that the existence and uniqueness theory for the limit diffusion process is in place DW and there is an associated invariance principle KaWi which, loosely speaking, is a perturbation result telling us that processes such as , that satisfy perturbed versions of the defining conditions for an SRBM, are close in distribution to an SRBM. In particular, for , the invariance principle of KaWi takes care of establishing the -tightness of and, in the presence of the uniqueness in law of the SRBM DW , it implies convergence in distribution of to an SRBM. In the case and , is a wedge (a polyhedral cone) and our proof for can be extended to this case. In as yet unpublished work, we have been able to establish uniqueness in law of the SRBM and to establish an invariance principle for some cases where and . However, some cases, especially when boundary faces meet in cusp-like singularities, are as yet unresolved. We summarize the situation for in Section 5.6. However, because of the partial nature of our results so far, we leave the description of these further developments to future work.

5.3 Diffusion approximation for weighted proportional fair sharing ()

The following condition is used in the next theorem. This condition can be interpreted as a local traffic assumption, under which each resource has at least one route that only uses that resource.

Assumption 5.1 ((Local traffic)).

For each , there exists at least one such that and for all .

The following theorem is proved in Section 7.

Theorem 5.2.

Assume that and that the local traffic Assumption 5.1 holds. Suppose that the limit distribution of as is (a probability measure on ) and that in probability as . Then, converges in distribution as to a continuous process , where is an SRBM with data and .

In the case , the lifting map is in fact a linear map on , given by

| (48) |

Indeed, for and , if and is given by the right-hand side of (48), then , by the definition of , and so that (30) holds. Then, by Theorem 4.1, we conclude that

and, hence, (48) holds. By the remark following Theorem 4.1, the defined above are dual variables for the optimization problem (2.3). It follows that we can associate a process of dual random variables with the SRBM of Theorem 5.2, as follows. Given as in Theorem 5.2, define

| (49) |

This process inherits an SRBM structure from . In fact, is a semimartingale reflecting Brownian motion living in , having the form

| (50) |

where the Brownian motion has drift and covariance matrix , and can increase only when is zero, . The direction of reflection on the boundary face of is defined by the th column of the matrix . The initial distribution of is obtained by applying the linear transformation to the distribution . (For the formal definition of such an SRBM, where reflection directions are not in general parallel to coordinate directions, see Wi98 .)

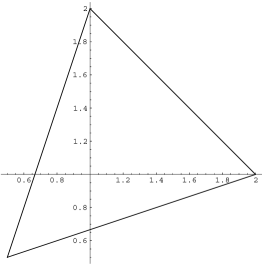

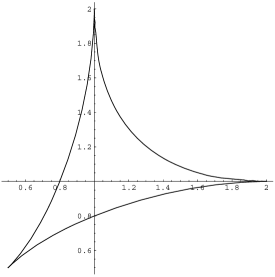

As an illustration of Theorem 5.2, consider a two-resource linear network operating under a weighted proportional fair sharing policy (). This network is depicted in Figure 1. It has two resources and three routes. Each resource has a route that passes only through that resource and there is also a route that passes through both resources.

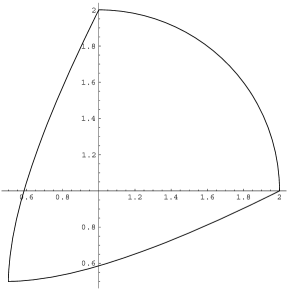

The workload cone in this case is a wedge in that has the following representation:

| (51) |

Let

It can be easily computed that the two boundary faces of the wedge have the following expressions:

and

The wedge is depicted in Figure 2. For a linear network, the local traffic condition holds automatically. Thus, the conclusion of Theorem 5.2 applies, provided converges in distribution to a random variable with distribution concentrated on and in probability as . For example, this holds if each of the systems indexed by starts empty and is the point mass at the origin in . The limiting SRBM lives in the wedge and is confined there by reflection (or pushing) at the boundary. Reflection occurs in the horizontal direction (corresponding to resource underutilizing capacity) on the bounding face where . The interpretation of this is that although there is no work for resource on route , there is work for this resource on route . However, congestion at resource , through the nature of the bandwidth sharing policy, is preventing resource from working at its full capacity. Similarly, vertical reflection (corresponding to resource underutilizing capacity) on the bounding face is interpreted to mean that congestion at resource is preventing resource from working at its full capacity. Thus, the shape of the workload space indicates the entrainment of resources, whereby congestion at some resources may prevent other resources from working at their full capacity. We note that when , the upper boundary of tends to the vertical axis and the lower boundary tends to the horizontal axis, hence the wedge expands to the whole quadrant, approaching the situation with full utilization of the resources.

5.4 Product form stationary distribution for proportional fair sharing

In this subsection, we prove a result which shows that when and for all (proportional fair sharing), an SRBM with the properties described in Theorem 5.2 has a product form invariant measure. (This is a result for SRBMs and so does not require the local traffic condition a priori.)

Theorem 5.3.

Suppose that and for all . Let be the measure on that is absolutely continuous with respect to Lebesgue measure with density given by

| (52) |

where

| (53) |

The product form measure is an invariant measure for the SRBM having state space , directions of reflection , drift and covariance matrix . This measure is integrable over if and only if for all and then, after normalization, it defines the unique stationary distribution for the SRBM.

Sufficient conditions for a reflecting Brownian motion in a simple polyhedral domain to have a product form invariant measure were determined by Williams in RSS , building on solutions of a related analytic problem obtained by Harrison and Williams in HaWi87 . In these works, the covariance matrix for the process is the identity matrix. In order to apply these results, we need to perform a linear transformation to transform an SRBM with covariance matrix into one whose covariance matrix is the identity matrix. We perform this transformation below; the computations are straightforward, though a little tedious, as we need to normalize the resulting directions of reflection to have inward normal components of unit length, to facilitate use of the results in RSS . Similar manipulations were carried out in the proof of Theorem 23 in HaWi87b , where the reflection directions had a special form.

Before introducing the transformation, we obtain an alternative representation for the simple convex polyhedron . By (47),

Here, since for all , we have that and, by (46), . Thus,

| (54) |

where we have used the fact that if and only if .

We now define the linear transformation to be applied to the SRBM. Let denote the diagonal matrix that has the same diagonal entries as . Let be the rotation matrix whose rows are the orthonormal eigenvectors of the covariance matrix and be the corresponding diagonal matrix of eigenvalues such that , where . Let be an SRBM with state space , drift , covariance matrix and directions of reflection given by , with a decomposition as in (i) of Definition 5.2. Let and define . Then, is an SRBM in the simple convex polyhedron

where, for each , is given by the th row of the matrix

| (55) |

and is the unit inward normal to the th face of . (The matrix is used to normalize the to be of unit length.) The process inherits the following decomposition from :

| (56) |

where , is the diagonal matrix with the same diagonal entries as and is a continuous, nondecreasing process that starts from zero and can increase only when is on the th face of . The columns of the matrix are the directions of reflection for on the faces of , normalized so that the inward normal component of each direction of reflection has unit length. (The matrix is used to achieve the normalization.) The matrix has the form

| (57) |

where is the matrix specified in (55) (whose rows are the inward unit normals to the faces of ) and is the matrix whose rows consist of the components of the (normalized) directions of reflection that are tangent to each of the faces of . In particular, the diagonal entries of are all zero. In this context, the sufficient condition given in RSS for existence of a product form invariant measure for is the so-called “skew symmetry condition,”

| (58) |

The vector form of (58) is

| (59) |

where, for each , is the inward unit normal to the th face of and is the tangential component of the (normalized) direction of reflection on that face. A geometric interpretation of the skew symmetry condition is provided in HaWi87 . We refer the reader to that paper, especially Section 9, for a full discussion. Briefly, for a simple convex polyhedron as we have here, the skew symmetry condition can be shown to be equivalent to a local condition. This local condition can be stated in words as requiring that near the intersection of any two distinct faces of , the component of the reflection vector on one face that is directed toward the intersection of the faces is balanced on the other face by the component of the direction of reflection for that second face which is of the same magnitude as the component on the first face, but it is directed away from the intersection of the faces. Indeed, under the skew symmetry condition, with probability one, the SRBM will not hit the intersection of any two faces when started away from that set, as is proved in RSS .

Thus, the skew symmetry condition (58) holds and it follows from Theorem 1.2 of RSS that the SRBM has a product form invariant measure with a density relative to Lebesgue measure that is proportional to , , where . Note, for this, that

where we have used the facts that and . Furthermore, by Corollary 1.1 of RSS , if the exponential density is integrable over , then, after normalization, it yields the unique stationary distribution for .

By inverting the linear transformation , we can transform this result back to one for . Noting that for ,

| (60) |

we conclude that (52) is an invariant density for the original SRBM and if this is integrable over , then, after normalization, it yields the unique stationary distribution for . Using the representation (54) for , we see that this density will be integrable over if and only if , is integrable over , which occurs if and only if for each .

Remark 5.4.

The product form invariant measure of Theorem 5.3 is remarkable, yet the proof of the result gives little insight into why the reflection directions and covariance matrix in the particular case for should allow the result to hold. We simply note here that the authors first suspected that a product form result might be found after observing that it is possible to describe a network of queues with a product form stationary distribution whose conjectured Brownian model approximation has the same directions of reflection and covariance matrix as the Brownian model approximation under study in this paper, provided that and for , that is, the case of proportional fair sharing. Earlier connections between product form queueing networks and proportional fairness have been explored by BP , MasRob2002 and the relationship between these several connections seems a rich area for further study.

The product form of the density (52) does not imply that, when for all , the components of the SRBM are independent under the stationary distribution for the SRBM since, in general, the cone is not an orthant. Independence can, however, be deduced for the components of the SRBM of dual variables.

Corollary 5.1.

Suppose that the assumptions of Theorem 5.2 hold, that for all and that for all . Let be the process identified in Theorem 5.2. The SRBM of dual variables then has a unique stationary distribution and this distribution has a density relative to Lebesgue measure that is proportional to , . Under this stationary distribution, the components of are independent and is exponentially distributed with parameter for each .

This result is immediate from Theorem 5.3 upon applying the linear transformation to transform into .

Under the assumptions of Corollary 5.1, from Theorem 5.2, (48) and the definition of , we have that

| (61) |

and it follows that the stationary distribution of can be expressed as a linear combination of independent exponential random variables. Thus, resource has associated with it a dual random variable , for (here, the superscript of signals that the random variable is associated with the stationary distribution). These dual variables are independent and exponentially distributed with parameters for and under its stationary distribution, the th component of is proportional to the sum of the dual variables associated with the resources used by route . This suggests the following simple approximation for the stationary distribution of the unscaled network, that is, the flow-level model of Section 2. The stationary approximation is

| (62) |

where , are independent and is exponentially distributed with parameter . We want to emphasize that (62) above is merely a formal approximation involving various implicit assumptions such as existence of a stationary distribution for and formal unraveling of the heavy traffic scaling and limit procedure. In particular, this involves an interchange of limits and the approximation in (62) involves errors that may be substantial (e.g., of order ). However, the following observation of Massoulié and Roberts RM , which yields an exact stationary distribution for an unscaled linear network, suggests that there is cause for optimism regarding the approximation (62).

Example 5.1.

Consider a linear network with resources, where the set of resources is . Let the set of routes be labeled , where we use the symbol for the route through every resource and, for , we use the symbol for the route through the single resource . The local traffic Assumption 5.1 thus holds and we assume and for all . Suppose that , and that . The stationary distribution for is then given by RM

| (63) |

where each run through the nonnegative integers. Summing this formula over and using the negative binomial expansion gives the marginal distribution for as

| (64) |

Thus, under the stationary distribution, are independent and is geometrically distributed with mean . This accords remarkably well with the approximation (62), under which would be approximated by an exponentially distributed random variable with the same mean.

For this particular example, as observed by RM , the Markov chain is reversible and, consequently, the stationary distribution for is insensitive to the document size distributions, depending only on their means. (For a description of general system structures to which such insensitivity results apply, see SCH and references therein.)

As a complement to the insensitivity result mentioned in the above example, we note that the stationary distribution result of Corollary 5.1 can be extended to the situation where the document sizes are finite mixtures of exponentials. Indeed, such a flow-level model may be realized by collapsing an extended (exponential) model. The extended model is obtained by splitting each route in the original model into finitely many “copies” so that each copy uses the same set of resources and has the same weights as the original route, but where each copy has its own Poisson arrival process and distinct exponential document size distribution. The relative arrival rates for the copies determine the proportions for the mixture of exponential distributions associated with the original route. More precisely, consider an extended (exponential) flow-level model in which, for each , routes identify finitely many identical routes (subsets of the resources in ) whose associated weights are also identical. In the following, parameters and processes associated with this extended model will have a superscript of † appended. In particular, will denote the flow count process.

Under the assumptions of Theorem 5.2 (heavy traffic, , local traffic condition and initial state space collapse) for the extended flow-level model, there is an SRBM approximation for the workload and an attendant approximation for the flow count process. Furthermore, there is an SRBM process of dual random variables. Under the additional assumptions of Corollary 5.1 (all of the weights are one and for each ), the stationary distribution of is such that the components are independent and is exponentially distributed with parameter for each . Thus, under the assumptions of Corollary 5.1, the stationary distribution of

| (65) |

can be expressed as a linear combination of exponential random variables.

For the extended model, the Poisson arrival rate for route is and the exponential service time parameter for this route is . Then, the -dimensional collapsed process defined by

| (66) |

has the same distribution as the flow count process in a flow-level model with routes, where the Poisson arrival rate for route is

| (67) |

and the document size distribution for route is a mixture of exponentials with parameters and proportions for . The mean of this document size distribution is , where is defined by

| (68) |

for . Let for .

Now, consider the exponential analog of the collapsed flow-level model where the finite mixture of exponential distributions for route is replaced by a single exponential distribution with parameter for . The nominal load placed on resource in the extended model is and this is the same as the nominal load placed on in the exponential analog. It follows that a sequence of extended flow-level models satisfying the assumptions of Corollary 5.1, where the limiting value in (12) of the heavy traffic Assumption 3.1 is denoted by , will have a parallel sequence of exponential analogs whose limiting value in (12) will be precisely the same as . Consequently, the stationary distribution of is the same as that for the process of dual random variables associated with the sequence of exponential analogs.

Then, combining (65) and (66), we obtain the following as an approximation for the collapsed flow count process:

that is, . Since the stationary distributions for and are the same, it follows that the stationary distribution for is the same, whether one considers the collapsed flow-level model (where document sizes are distributed as finite mixtures of exponentials) or the associated exponential analog (where document sizes are distributed as exponentials). Similarly, the formal approximation (62) for the unscaled network is the same for both. Note, however, that the stochastic processes , and , and, in particular, their covariance matrices are, in general, different from those associated with the exponential analog.

It is natural to conjecture an extension of the above insensitivity results to general document size distributions. However, even an extension to phase-type distributions would require generalization of the diffusion approximation results to flow-level models with feedback and treatment of more general distributions would appear to require a significantly more elaborate stochastic model (see growil06 ) to keep track of residual document sizes.

5.5 Multi-path routing

In this subsection, we describe a generalization of the earlier model that allows multi-path routing. In our initial description of the model, we shall use a different notation for the sets of routes and resources. This will allow our eventual results to be expressed in a notation consistent with that used elsewhere in the paper.

Suppose that we now interpret as a source–destination pair and let be the set of routes. Let and let . We suppose that is partitioned into nonempty subsets, each associated with a single source–destination pair. Let if route is associated with source–destination pair and let otherwise. Thus, is an matrix containing only zeros and ones, and for each .

There remain finitely many resources, but now labeled by , with capacities that are all strictly positive and finite. A route is a nonempty subset of (interpreted as the set of resources used by route ). We assume that and are both nonempty and finite. Let , the total number of resources. Let be the matrix containing only zeros and ones, defined such that if resource is used by route and otherwise. Our assumption that each route identifies a nonempty subset of implies that no column of is identically zero.

It is assumed that a new document arrives to source–destination pair at each jump time of a Poisson process that has rate parameter and that each such document has an exponentially distributed size with mean , where . These document sizes are assumed to be independent of one another and to be independent of all arrival times of documents. Let .

Given a fixed parameter and strictly positive weights , if denotes the (random) number of documents being transferred between source–destination pair at time for each and , then the bandwidth allocated to source–destination pair at time is given by and this bandwidth is shared equally among the transfers in progress between source–destination pair . The function is defined such that for each , for , and when is nonempty, is the unique value of that solves the optimization problem

| (69) | |||

where is again given by the definition (2).

Without loss of generality, we may assume that in the solution of (5.5), for those such that for all . With this convention, allocations , associated with the unique optimal value can be interpreted as bandwidth allocations for the routes which sum to give the bandwidth allocations to the source–destination pairs.

The above optimization problem reduces to the earlier problem (2.3) in the case where and is the identity matrix, that is, the case of a single route for each source–destination pair. More generally, the following proposition allows us to reduce to the optimization problem (2.3), even in the multi-path case. This observation was previously made in KEL , Section 3.3.

Let

Proposition 5.1.

There exists a representation

| (70) |

where , and can be chosen so that has positive elements, has nonnegative elements and no column of is identically zero.

The set is the intersection of the half-spaces , , and the nonnegative orthant, . Since no column of is identically zero, the set is bounded and is thus the convex hull of a finite number of extreme points. Hence, is the convex hull of a finite number of extreme points or, equivalently, the bounded intersection of a finite set of half-spaces.

Next, we explore further the geometry of . First, since the elements of are nonnegative. Also, since . Indeed, for positive and small enough, for all , , since for positive and small enough, for all , , and no row of is identically zero. Thus, is bounded by the hyperplanes bounding the nonnegative orthant, plus finitely many other hyperplanes, none of which contains the origin. Thus, there exists a representation of the form (70) for some choice of , and . Since , the elements of are nonnegative. Choose a minimal representation, where the set is of minimal cardinality. Then, the intersection of the hyperplane

| (71) |

with must have a nonempty interior relative to the hyperplane, for each .

Next, we show that if and , then . Let be such that and, for each , let be the unique index such that . Let for . Then, and , so .

We have seen that the intersection of the hyperplane (71) with has a nonempty interior relative to the hyperplane. Choose a point in this relative interior. Then, for . Fix and choose so that , with for . Then, , so . Hence, the hyperplane (71) must have .

Finally, note that for since the hyperplane (71) does not contain the origin, and no column of is identically zero since is bounded.

The represention (70) of allows us to elide the variables from the optimization definition of and to deduce that the unique solution to the optimization problem (5.5) is also the unique solution to the optimization problem (2.3). With this generalization to multi-path routing, the matrix may no longer only contain zeros and ones. However, the proofs of Theorem 5.2 and Corollary 5.1 still go through in this enhanced generality, provided that the local traffic condition is satisfied.

As an illustration, consider the network depicted in Figure 3, operating under the proportional fair sharing policy ( for all ), where the labeled resource capacities satisfy . It has three source–destination pairs, four resources and five routes. The matrices and can then be chosen as

These matrices may be viewed as expressing the generalized cut constraints

| (72) | |||||

| (73) |

apparent from Figure 3. In the first of these constraints, the capacities of the first and second resources are pooled. Resource pooling subject to generalized cut constraints is a common phenomenon in stochastic processing networks with routing LAWS . Theorem 3.1 of LAWS provides an alternative form of the representation (70) and provides references to algorithms to calculate matrices and .

In the above example, we have been able to construct the matrix so that a subset of its columns forms the identity matrix and thus the local traffic Assumption 5.1 holds. However, in general, it is more difficult to verify the local traffic condition for networks with multi-path routing than for networks without routing choices.

Suppose that the local traffic Assumption 5.1 holds for the matrix . Define heavy traffic as in Assumption 3.1 and assume that for . Corollary 5.1 then applies directly. We can illustrate the formal approximation (62) for the example shown in Figure 3: under the approximation, and , the random dual variables associated with constraints (72) and (73), respectively, are independent and exponentially distributed, with parameter and with parameter .

5.6 Discussion of the conjecture for

Consider the two-resource linear network depicted in Figure 1, operating under a weighted -fair bandwidth sharing policy for . Then, the workload cone is still a wedge in that has the following representation:

| (74) |

The two boundary faces of this wedge have the following expressions:

and

In this case, since the two-dimensional wedge is still a polyhedral cone, the proof of Theorem 5.2 can be easily modified to apply for , with used in place of there. When the weights are all equal, the wedge does not depend on . However, when the ’s are not all equal, the wedge does depend on . However, as goes to infinity, the quotients involving the weights in the expressions for , tend to one and there is a limiting wedge which is the same as that obtained when the are all equal. On the other hand, as tends to zero, the limit of the upper boundary depends on whether (tends to the vertical axis) or (tends to the 45 degree ray from the origin). Similarly, for the lower boundary, if , it tends to the horizontal axis and if , it tends to the 45 degree ray from the origin. Hence, as tends to zero, if , the wedge expands to the whole quadrant and if , the wedge contracts to the 45 degree ray from the origin. Note that even when the wedge expands to the whole quadrant, the components of the diffusion workload do not become independent as the covariance matrix , which does not depend on or , is not diagonal.

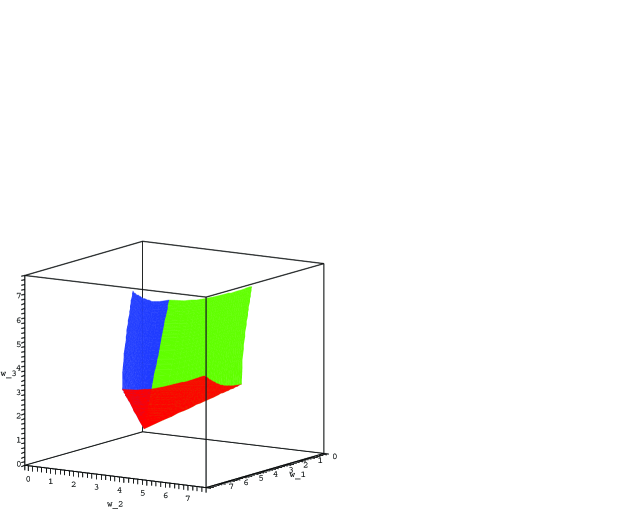

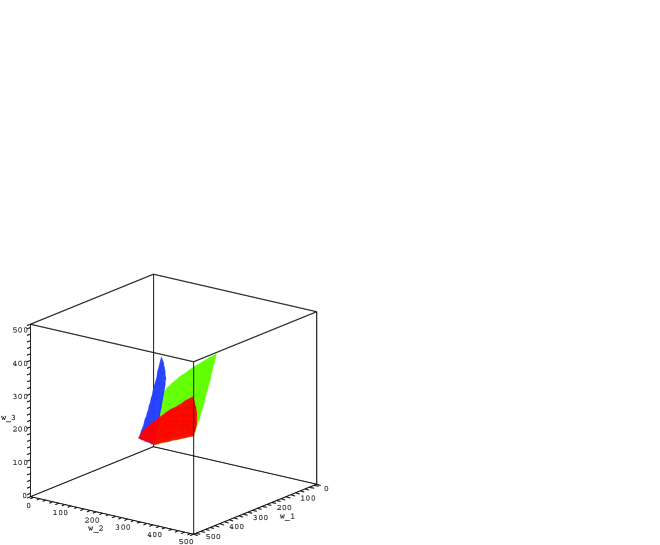

In general, for with higher-dimensional workloads, that is, , the shape of the workload cone depends on , as well as on , , and . This relationship appears to be quite complicated. We are investigating Conjecture 5.1 in this case. At this time, we only have some partial results. The main difficulty in establishing the validity of the conjecture concerns proving -tightness of and establishing uniqueness in law for any weak limit point. To illustrate some of the difficulties involved, we consider a linear network with three resources and four routes. Although this is a particular example, it exemplifies the challenges presented by the geometric data in establishing existence, uniqueness and an invariance principle for the SRBM. For this example, each of the three resources has a route that only goes through that resource and there is one additional route that goes through all three resources. Here, the workload cone is contained in the three-dimensional positive orthant. When for all , we depict the associated workload cone and one of its cross-sections, for , and in Figures 4–9.

For the case depicted in Figures 4–5, and Theorem 5.2 applies to justify the diffusion approximation. The proof of this theorem uses the uniqueness of the diffusion process DW and the invariance principle developed in KaWi . For the case depicted in Figures 6–7, and the workload cone has boundary faces that curve outward. Away from the origin, the boundary and directions of reflection for the proposed diffusion approximation locally satisfy conditions required by the invariance principle given in KaWi . However, the workload cone has a “singular point” at the origin where the conditions in KaWi fail to be satisfied. However, since this is an isolated point, the invariance principle in KaWi and the proof of uniqueness starting in DW can be adapted to establish the SRBM diffusion approximation in this case. For higher-dimensional analogs of this case, we anticipate that a valid diffusion approximation can be established. However, as the dimension increases, it becomes more difficult to compute the inward normals to all boundary faces and, as yet, we do not have a systematic way to verify geometric sufficient conditions for uniqueness in law and a valid invariance principle. For the case depicted in Figures 8–9, where , the situation is more complex. Here, the workload cone has boundary faces that curve inward and any two faces meet in a cusp, that is, the inward normals to any two boundary faces point toward one another at the intersection of the faces. At present, we do not have an existence and uniqueness result, nor an invariance principle, to treat this case because of the singular geometry at the intersections of faces. In particular, it has not been established that the diffusion process can escape from the tip of a cusp or that there is uniqueness in law for a diffusion process starting there.

In a recent work, Shah and Wischik SW have proven multiplicative state space collapse for a class of “switched” networks operating under a family of scheduling policies related to the maximum weight algorithm introduced by Tassiulas and Ephremides TE . Based on this, Shah and Wischik have conjectured natural diffusion approximations for the workload processes in these models. These diffusions are SRBMs living in cones with piecewise smooth boundaries. While these cones have some characteristics in common with those found for the bandwidth sharing model considered here, there are also some new features. Depending on a parameter associated with the family of scheduling policies, the cones of SW include nonsimple convex polyhedrons as well as cones with curved boundaries where boundary faces can meet smoothly. The validity of these conjectured diffusion approximations for input-queued packet switches operating under a maximum weight algorithm is being explored in KaWiS .

6 Proof of multiplicative state space collapse

In this section, we prove the multiplicative state space collapse result, Theorem 5.1. Our proof follows a general line of argument pioneered by Bramson in BR , where open multiclass queueing networks operating under certain head-of-the-line (HL) service disciplines are treated. However, there are some differences from BR . Here, we have the more general structure of a stochastic processing network with simultaneous resource possession and our service discipline is not work-conserving. On the other hand, we have exponential interarrival and document size distributions (rather than general distributions), which lead to some simplifications in our proofs. A particularly interesting aspect here is that, in contrast to prior results on state space collapse for open multiclass queueing networks, our lifting map can be nonlinear (for ). In addition, unlike Assumption 3.1 in BR , we do not require an exponential rate of convergence of fluid model solutions toward points on the invariant manifold; we only use uniform convergence of fluid model solutions toward the invariant manifold (starting in a compact set). Despite these differences, our main line of argument follows that of Bramson BR .

We first provide some preliminary results in Section 6.1. Our proof of multiplicative state space collapse is then given in Section 6.2.

We note (for the extension to multi-path routing described in Section 5.5) that the proofs in this and the next section use the fact that the entries in the matrix are nonnegative, rather than the stronger condition that they are zeros or ones.

6.1 Crucial estimates for fluid scaled processes

Recall the definition of fluid scaled processes from Section 3. For each and , let

| (75) |

and define shifted and scaled processes as follows. For , and ,

| (76) | |||||

| (77) | |||||

| (78) | |||||

| (79) | |||||

| (80) | |||||

| (81) |

The additional scaling by used here is to ensure that the starting values of all lie in a single compact set, namely the unit ball in . This facilitates use of the properties of fluid model solutions described in Section 4. It is easy to check using (5)–(6), (13)–(15) and the scaling property of that for each , and ,

| (82) | |||||

| (83) | |||||

| (84) |

The following theorem summarizes essential properties of the above processes needed for our proof of multiplicative state space collapse. The proof of this uses arguments very similar to those in Sections 4, 5 and 6 of Bramson BR .

Theorem 6.1.

Let

| (85) |

Fix . For each , there exists a sequence of measurable sets and a family of positive constants such that for each and , {longlist}

;

for each and ,

| (86) |

and there is a fluid model solution satisfying

| (87) |

Note that we have not indicated explicit dependence on in the above as will always be fixed in the application of this result. Also, to simplify notation, we have omitted explicit indication of the dependence of on , , , and .

Before proving this theorem, we establish the following preliminary lemma. For this lemma and the proof of Theorem 6.1, let .

Lemma 6.1.

Fix . For each , there exists a sequence of measurable sets and a family of positive constants such that for each and , we have

| (88) |

and on , for ,

| (89) | |||||

| (90) |

where , and , for all and .

Fix . Note that since the bandwidth allocations given by are bounded by , for each and , is Lipschitz continuous with Lipschitz constant . Since this property is unchanged by the (fluid) scaling in (78), we have that is also Lipschitz continuous with the same Lipschitz constant. It follows from this that On combining this with Assumption 3.1, the fact that the interarrival times and document sizes are exponential and the memoryless property of the associated Poisson processes, by an argument similar to that used in verifying (5.19) of Proposition 5.1 in Bramson BR , we have that as ,

| (91) |

It follows that there exists a sequence satisfying , for each integer , such that for each ,

For , define

and

Then, since as , for each , there exists such that for all . Combining the above, we conclude that for all ,

| (92) |