1. Introduction

Let be the short-rate (i.e. the rate offered by a bank) at

time . Assume that satisfies the following

stochastic differential equation

| (1) |

|

|

|

|

|

|

|

|

where is a one-dimensional Brownian motion defined on a

filtered probability space

.

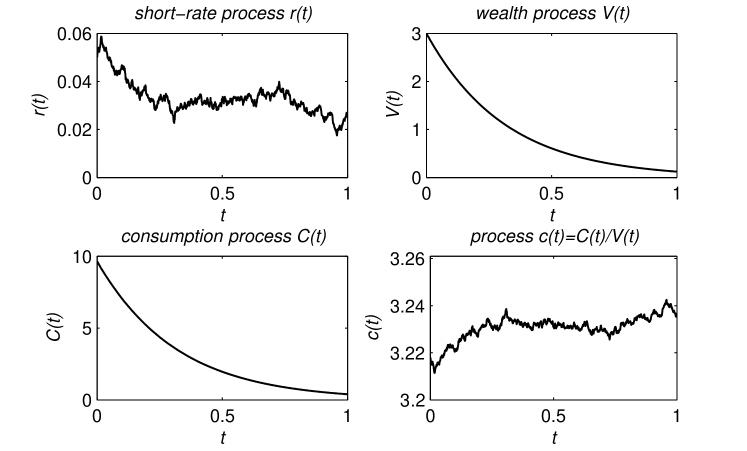

Let us denote by the capital at time of a

bank account owner whose consumption rate is and whose wealth

at time 0 is . Then

|

|

|

Let

| (2) |

|

|

|

be the bankruptcy time.

In the paper it is assumed that any consumption rate is

progressively measurable and non-negative. The space of all

consumption rates is denoted by .

Given a discount factor and an exponent of the power utility function, we are concerned with the

following problems:

Problem A Given and , find a consumption

rate which maximizes the

performance functional, that is,

|

|

|

where

| (3) |

|

|

|

, and is the conditional

expectation . A

solution to this problem is given in Proposition 1 and

Theorem 2 below.

Problem B It is reasonable to assume that one

keeps his money in the bank account as long as the interest rate

is positive. Under this assumption the performance

functional is given by

|

|

|

where , and .

Clearly, if , then . The goal is now to find

a consumption rate which maximizes (see Proposition

2 and Theorem 4).

Problem C Let be the price at

time of a zero-coupon bond that pays off at time .

If one may also invest in zero-coupon bonds then the wealth

dynamics is formally given by

| (4) |

|

|

|

|

|

|

|

|

|

|

|

|

where , is the density of the

distribution of investments in bonds with various terminal time

. The aim is to maximize the performance functional

given by (3) with .

Problems A, B and C defined above are particular cases of

an investor problem, various types of which has been investigating

since 1970’s (see [7] and [8]). However,

most of them are concerned with investment in a bank account

(usually on a constant rate) and a finite number of stocks. If one

can invest in a bank account and zero-coupon bonds, then the

investor problem is more difficult to solve. The reason is that

there can be an infinite number of bonds, since the time of

maturity can take an infinity of values. Furthermore, the

set of admissible strategies does not contain ”buy and hold”

strategy, i.e. one must convert bond to cash at maturity.

The type of an investor who can invest his money in bonds has been

recently studied in [1], [6] and

[11]. Contrary to our paper, authors of

[1], [6] and

[11] examined the portfolio problem without

possibility of consumption and with a finite time horizon. On the

other hand, in [1] and [11]

it is assumed that the dynamics of the instantaneous forward rate

is given and that the performance function is defined under a real

measure. More references can be find in the survey paper

[12].

In the paper we use the Hamilton–Jacobi–Bellman approach,

whereas in [1] and [11]

convex duality is used.

2. Preliminaries

In the paper, it is assumed that (1) defines a Markov family

on an open subinterval , which,

in particular, means that is invariant for

(1); that is, implies that for all . Moreover, it is assumed that

, , their

first derivatives are bounded on , and that the

diffusion is non-degenerate, i.e. for all .

The value function for one of the listed above problems

is the maximum of the corresponding performance functional over

the set of admissible controls. We will show that the value

functions are very regular, namely in . Let

| (5) |

|

|

|

be the formal generator of the diffusion given by (1).

The results below have the form of the verification theorem for

stochastic control problems. For similar results see e.g.

[2], [9] or [10].

Proposition 1.

Let be such that

| (6) |

|

|

|

for every . Then is

the value function for Problem A, whenever for any and ,

| (7) |

|

|

|

where is given by (1), and . The optimal consumption

is given in the feedback form

| (8) |

|

|

|

Proof Taking into account the dynamics of

and the form of performance functional we see that

|

|

|

for a certain function . The Hamilton–Jacobi–Bellman equation

(see e.g. [2], [10]) for is

|

|

|

The supremum is attained at given by (8).

Hence, satisfies (6) and the HJB verification

theorem (see [9], [10]) gives us the

claim. □

In Problem B we have to assume that . If not, Problem B can

be reduced to Problem A. Let and .

With a similar proof as above we have the following proposition

concerning Problem B.

Proposition 2.

Let satisfy

(6). Then

|

|

|

is the value function for Problem B, whenever for any and ,

| (9) |

|

|

|

where , and . The optimal consumption is given in

the feedback form (8).

Note that satisfies a non-linear, non-Lipschitz second

order differential equation, but is not defined as a solution

to the Cauchy problem. The goal of the paper is to prove the

existence of the solution satisfying appropriate boundary

conditions and to find an approximating scheme for .

3. Solution to Problem C

In Problem C we assume that is a martingale measure.

Then

|

|

|

Since is a Markov process, is a function of and . Thus we

can rewrite (4) as follows

| (10) |

|

|

|

with , whenever is differentiable

with respect to .

In Problem C the performance function is given by (3), the

class of admissible controls consists of tuples

of progressively

measurable processes, such that is non-negative,

(10) is well defined and

|

|

|

Note that neither nor have to be non-negative.

Define

| (11) |

|

|

|

Then we can rewrite (10) in the form

| (12) |

|

|

|

Since we assumed that we are given dynamics of , and the

performance functional is under a martingale measure, we can treat

the investor portfolio as the one consisted of the bank account

and one other instrument with price given by

| (13) |

|

|

|

Note that given (12) and (13), we have

to assume that for any ,

|

|

|

Therefore the dynamics of the wealth of the investor is given by

|

|

|

which is equivalent to (4) and

(12). Thus the number of instruments is finite

and the same approach as in [5] can be taken.

Theorem 1 below, giving a solution to Problem C, was

formulated and proven in [5] under much weaken

conditions. Here we present another proof, based on Proposition

3 below. We restrict our attention to the value

function of the problem. We refer the reader to

[5] for details on the optimal control

(portfolio).

Proposition 3.

If satisfies

| (14) |

|

|

|

then is the value function for Problem C,

whenever for any and ,

| (15) |

|

|

|

where and .

The optimal consumption and the optimal factor defined in (11) are given by

| (16) |

|

|

|

Proof Again for a

certain function . The HJB equation for is

| (17) |

|

|

|

|

|

|

|

|

and the claim follows from the HJB verification theorem.

□

Since the value function is a

non-decreasing positive function of both arguments and ,

we see that is non-decreasing and positive. Then the optimal

in (16) is positive. Note that and whilst the short-selling is forbidden. Then

the condition

| (18) |

|

|

|

which holds e.g. in Vasicek and CIR models, implies that if the

short-selling is forbidden then necessarily and

given by (11) are non-positive. Thus the

supremum over in equation (17) is

attained at 0. Hence, if the short-selling is forbidden and

(18) holds, then Problem C reduces to Problem A.

It is worth mentioning that given we do not have

unambiguous solution to Problem C, i.e. we do not obtain

unambiguous pair . However we may choose arbitrary

such that and then we

derive an optimal from (11). For example we

may set for some .

The following result will be used to show the regularity of

the value function. Let

| (19) |

|

|

|

Proposition 4.

If for every and

| (20) |

|

|

|

then and

| (21) |

|

|

|

Proof Let , where and . Then, by (20),

|

|

|

is a solution to the boundary problem

|

|

|

where

|

|

|

and . Since we assumed that is invariant for

(1), then for

any and consequently . Thus is a weak solution (see Definition

1 in Section 5) to (21), and

by Lemma 1, . Hence, it is a

strong solution to (21). □

The result below says that the function appearing in the

identity for the value function equals

.

Theorem 1.

Let assumptions of Proposition 4 hold. Assume

additionally that for any and ,

| (22) |

|

|

|

where and .

Then is the value

function for Problem C.

Proof By elementary calculus, (21) is

equivalent to (14) for .

Condition (22) implies (15) and we

conclude by Proposition 3. □

4. Solution to Problem A

This section contains one of the main result of the paper. It

provides the existence and approximating scheme for the solution

to the HJB equation (6) for Problem A. In its

formulation is a Banach space of continuous

functions on .

We will need the following hypotheses:

(H.1) For any fixed , , and

any sequence of stopping times, the sequences of

random variables

|

|

|

are uniformly integrable with respect to .

(H.2) For any Lipschitz continuous

bounded function and for

any non-negative , one has .

(H.3) The family of linear

operators

| (23) |

|

|

|

forms a -semigroup on .

We note that condition (H.1) will be needed only in the

proof of the inclusion .

Recall that is a function defined by (19). The following

hypothesis will be needed in the proof that is a

supersolution to the HJB equation (6), such that

and satisfies the boundary condition

(7). For more details see Definition 2 and

Remark 5.

(H.4)

For any ,

| (25) |

|

|

|

and for any stopping time ,

| (26) |

|

|

|

is uniformly integrable, where .

Moreover, and , where is defined by (24).

For any , define

| (27) |

|

|

|

Recall that is the generator of the semigroup

. We denote by the resolvent

set of . The proof of the following theorem is

postponed to Section 7.

Theorem 2.

Assume that (H.1), (H.2), (H.3) and

(H.4) are fulfilled. Then there is a solution to

(6) with condition (7). Moreover, , . Finally, for any

sequence such

that for any ,

| (28) |

|

|

|

one has

|

|

|

where is a non-decreasing sequence of both and

, defined as follows

|

|

|

|

|

|

|

|

5. Analytical tools

This section provides some useful analytical tools. Let us

consider a second order differential operator

|

|

|

with and in . We denote by

|

|

|

the formally adjoint operator. We denote by the space of all locally integrable functions on .

Definition 1.

Let . We call a weak

solution to the equation if

|

|

|

Let be an open subset of . The following

result holds only in dimension . For a counterexample in case

of see

[3].

Lemma 1.

Assume that is a

continuous function and such that

, is a weak solution to

| (30) |

|

|

|

Then , i.e. is a strong solution to (30).

Proof We may rewrite (30) in the form

| (31) |

|

|

|

where we skip argument and all derivatives of are in the

weak sense. We can use the following fact. Assume that is a

distribution whose derivative is a function . Then is a function and

|

|

|

for some finite and .

Applying this observation to (31) we obtain

|

|

|

where the r.h.s. is continuous, since integrand is locally

integrable. Thus

|

|

|

and . Using the same argument

again we have

|

|

|

and , since integrand is locally integrable. Having shown

that , we see that the integrand is

continuous, which implies . Now we

conclude that integrand is of class and consequently . □

Recall that is a differential operator given by (24). We

denote by the generator

of the -semigroup defined by (23) on the Banach

space , see (H.3).

Lemma 2.

We have

|

|

|

and for all .

Proof Write .

Step 1. Here we will show that . Let . First we

will show that for any . We have

|

|

|

|

|

|

|

|

where is a transition density function of process

, which exists due to the non-degeneration of the diffusion

coefficient. Hence

|

|

|

|

|

|

|

|

|

|

|

|

and since the transition density function satisfies backward

parabolic equation, it follows that

|

|

|

where subscript denotes that the operator acts on

as a function of with and fixed. Thus we

have

|

|

|

|

|

|

|

|

|

|

|

|

Thus is a weak solution to . By Lemma 1, and

is a strong solution to . Hence and .

Step 2. We will show that . Let . Then

from Itô’s formula

|

|

|

where and

|

|

|

is a martingale. Taking expectations and next passing to limit

with , thanks condition (H.1), we obtain

|

|

|

which means that . Therefore by the mean-value theorem

|

|

|

which means that and

. □

6. Lipschitz modification of the HJB equation

In this section we will find a twice continuously differentiable solution to

the equation

| (32) |

|

|

|

where is given by (27).

Define and . Note that (32) can be written

as

| (33) |

|

|

|

Definition 2.

We call a subsolution to

(33) if

|

|

|

We call a supersolution if

|

|

|

Theorem 3.

Let and

be a subsolution and

a supersolution to (33), respectively. Assume that

. Define and as

| (34) |

|

|

|

where is such that (28) holds. Then

defined as a pointwise limit of , i.e.

| (35) |

|

|

|

belongs to and is a strong solution to (33).

Moreover, for all .

Proof From

|

|

|

we get . Since and consequently for every . It follows that .

Now we show that is a subsolution. From (28) and

(34) we have

|

|

|

which, with help of Lemma 2, implies that

is a subsolution to (33). Hence, by induction, and is a subsolution for all .

Now we show, by induction, that for

all . By definition . Assume that

. Then from (34) and (28)

we have

|

|

|

Hence,

|

|

|

implies that , and we obtain .

Summing up, we have

|

|

|

Therefore given by (35) exists for all . Since

is continuous,

|

|

|

and from (34) we have

|

|

|

for any test function . By

Lemma 2,

|

|

|

Let . By the dominated convergence theorem, we get

| (36) |

|

|

|

Since and is

continuous, then is locally bounded. Hence, is a weak

solution to (33), and we conclude by Lemma 1.

□

7. Proof of Theorem 2

Let be the sequence constructed in the previous section.

By (25) and (26) the function

satisfies

(7). So does . Hence, Remark

5 and Theorem 3 guarantee that

satisfies (7).

Therefore, by Remark 4, is the value

function for Problem A with constraint . Hence,

is a non-decreasing sequence and the function

|

|

|

is well defined. Note that in . Indeed, from

the continuity of we have ,

-a.s. for all and , which

implies , and therefore

|

|

|

is strictly positive in . Since , we have . Thus,

in particular, is well defined, where , for every .

We will show that is a weak solution to

| (37) |

|

|

|

To do this define

|

|

|

Clearly for all . Since

for every , we have

|

|

|

which implies, from continuity of , that for any ,

| (38) |

|

|

|

Now we show that (38) holds for any . To

do this note that .

Indeed, since for any , then for any there is such , that

|

|

|

and hence .

Note that for any and we have

|

|

|

Let in (36). By the inequality above

and the dominated convergence theorem, we get

|

|

|

which means that is a weak solution to (37), whenever

is locally integrable. Since , we have and from continuity of

, the function is locally bounded. By Lemma

1, is a strong solution to (37).

By (25) and (26), satisfies the boundary condition (7).

8. Solution to Problem B

This section provides the existence and approximating scheme for

the solution to the HJB equation (6) for Problem B.

Let be a Banach space of

continuous functions on .

Recall that . For

all we define the following functions:

|

|

|

and

|

|

|

Let for all and let .

We denote by ,

and the

equivalents to (H.1), (H.2) and (H.3)

respectively, where , and and are

replaced by and .

Clearly, , and the following hypothesis is needed to

show that the boundary condition (9) holds for any

continuous function satisfying in

.

For any ,

| (39) |

|

|

|

whenever , and for any

stopping time ,

| (40) |

|

|

|

is uniformly integrable, where . Moreover, and

, where , and .

Note that if holds, then it holds

simultaneously for both processes and .

For any , one has .

By , is a subsolution to

(32). It is easy to see that under assumptions of

Proposition 4, satisfies (21);

it is enough to take in the proof. Thus is a

supersolution to (32). Hence, by ,

|

|

|

|

|

|

|

|

and is also a supersolution.

Since , then from the fact that (see Theorem 4 below) we have a condition

, which with help of (39) and

(40) implies (9). Furthermore,

the value function for any . The proof of the following result

is analogous to that of Theorem 2 and is left to the

reader.

Theorem 4.

Assume that –

are fulfilled. Then there is a

solution to (6) with condition (9).

Moreover, , .

Finally, for any sequence satisfying (28) for any , one has

|

|

|

where is a non-decreasing sequence of both and

, defined as follows

|

|

|

|

|

|

|

|

9. Vasicek model

Let us recall that in the so-called Vasicek model

is given by

| (41) |

|

|

|

with . Let

| (42) |

|

|

|

and

|

|

|

Theorem 5.

The assumptions of Theorem 2 are satisfied, whenever

| (43) |

|

|

|

where

|

|

|

Proof Notice that for any stopping time ,

|

|

|

|

|

|

|

|

and, by Fernique’s theorem, the r.h.s. is integrable for any fixed

. We similarly obtain

|

|

|

Therefore (H.1) is satisfied.

It is easy to check that satisfies

(H.2). Assume that is given by (41) and

that is given by (23). In Appendix it is shown

that is a -semigroup on , and hence hypothesis

(H.3) is satisfied. Therefore we have to show

(H.4). We split a verification of (H.4) into

several steps.

Step 1.

First we show that for any . From

(41) we obtain

| (44) |

|

|

|

where

| (45) |

|

|

|

and its distribution does not depend on . In what follows we

denote by the law (distribution) of a random

variable . Note that

| (46) |

|

|

|

Therefore, we have

|

|

|

|

|

|

|

|

|

|

|

|

and by Fubini’s theorem

| (47) |

|

|

|

which implies that

| (48) |

|

|

|

Thus

|

|

|

|

|

|

|

|

|

|

|

|

by (43). Analogously we can show that by

(43), condition (20) holds.

Step 2. Here we show (25). We have

just shown that

| (49) |

|

|

|

where

|

|

|

is positive by (43). Then to prove (25)

it is enough to show that

|

|

|

From Hölder’s inequality

|

|

|

and we easily compute that

|

|

|

Note that given with distribution , it

is easy to show that

| (50) |

|

|

|

Therefore, the expression in the second bracket above is dominated

by , which is finite for every . Thus (25) holds.

Step 3. Here we show that the family in

(26) is uniformly integrable. By the de la Vallée

Poussin theorem (see e.g. [9], p. 241), it is enough

to show that

| (51) |

|

|

|

for some . Here we take .

By (49) we obtain

|

|

|

|

|

|

|

|

where

|

|

|

and is defined by (45). Let and

. Then

|

|

|

By Itô’s formula

|

|

|

where

|

|

|

and

|

|

|

Note that and . Therefore by the Novikov

condition is a martingale, and . By (43) there is a such that

|

|

|

Then

|

|

|

and it is enough to show that

|

|

|

We have

|

|

|

|

|

|

|

|

where the last estimate holds due to Doob’s inequality. Since , where

is a martingale of the same form as , but with

constant instead of , then

|

|

|

Step 4. Here we show that . By Proposition 4, . To show that we have to

prove that

|

|

|

It is easy to see that

|

|

|

The condition

|

|

|

amounts to

|

|

|

which clearly holds.

Step 5. Finally, we need to show . By the definition of (see (24)) and

the previous step of the proof, we know that . Thus we need to verify the condition

|

|

|

By (21) we have

|

|

|

Since

|

|

|

where is, by Step 1, a strictly positive integrable

function, then is positive and increasing. Furthermore,

|

|

|

Hence,

|

|

|

and, since , the limit above is equal to zero.

□

Note that the condition assures the finiteness

of for any and that assumption

(20) holds, and the condition is needed for uniform integrability of the family in

(26).

Let and let

|

|

|

be equipped with the norm

|

|

|

Then we have the following result.

Theorem 6.

The assumptions of Theorem 4 are fulfilled in the

Vasicek model (41), whenever (43) holds.

Proof Verification of

, and

is left to the reader, as it is

similar to verification of (H.1), (H.2) and

(H.3). Here we verify only

and . To show

define a sequence of functions

, such that

|

|

|

Then, by (43),

|

|

|

where and . Furthermore, for any test

function ,

|

|

|

which implies that

|

|

|

Under the following conditions,

|

|

|

|

|

|

|

|

|

|

|

|

which we will verify below, we have and the convergence is almost uniform. Thus,

|

|

|

and it holds for any . By

Lemma 1, .

Since any Ornstein–Uhlenbeck process is recurrent, then

holds. Condition is implied by the continuity of

trajectories. To show , note that due to Step 3 of the

proof of Theorem 5 the sequence of random variables in

the second expression below is uniformly integrable, which

justifies the first equality, and the constant does not

depend on . Thus,

|

|

|

|

|

|

|

|

|

|

|

|

where is given by (47).

We proceed to show that holds. Since

condition above holds, then we do not have to verify

(39).

Note that . Therefore, by Theorem

5, the sequence in (40) is uniformly

integrable whenever uniformly integrable is the sequence

|

|

|

By the strong Markov property it is equivalent to the uniform

integrability of

|

|

|

which is fulfilled whenever

|

|

|

This holds, since as and

|

|

|

is uniformly integrable (see Step 3 of the proof of Theorem

5).

Here we will show that . Since

then and it is enough

to show that . By the similar argumentation to

that in verification of in the previous step of the proof,

we have

|

|

|

|

|

|

|

|

|

|

|

|

Now we will show that ,

which will imply that . Since,

by condition (43), satisfies

| (52) |

|

|

|

then , and consequently . Furthermore, , since

|

|

|

Analogously, for any

, and consequently for any .

In order to prove that , note

that by (52), we have

|

|

|

We need the following result.

Lemma 3.

Let and . Then for any .

Proof Since for any , one has , then

|

|

|

|

|

|

|

|

where . Since , then is finite. □

Going back to the proof of Theorem 6 note that we can

rewrite (52) as follows

|

|

|

which implies that the l.h.s. belongs to , and by

the lemma above, for any . Since , then . Hence, for any and , we get

|

|

|

|

|

|

|

|

It is easy to verify that is increasing, which implies

that for any . Thus, the limit above is equal

to zero. □

10. Invariant interval model

Here we assume that the short-rate dynamics is given by (1),

, where and

is equipped with the supremum norm.

The sufficient condition for interval invariance is (see

[4])

|

|

|

where

|

|

|

for a fixed .

It is easy to show that the conditions above holds in the model

| (53) |

|

|

|

with .

Theorem 7.

The assumptions of Theorem 2 hold in the invariant

interval model (53).

Proof Notice that for any stopping time

and any fixed ,

|

|

|

and similarly

|

|

|

which means that (H.1) is satisfied. One may easily check

that the space satisfies (H.2). Assume

that is given by (23). In Appendix it is shown

that is a -semigroup on , and hence hypothesis

(H.3) is satisfied. Thus we have to verify

(H.4).

Given , we have

|

|

|

and

|

|

|

Thus and (25) holds. In the same manner we

can see that (20) holds.

Recall that (51) implies uniform integrability of the family

in (26). Let . Then (51)

holds, since we have

|

|

|

By Proposition 4, one has . Note that is bounded, i.e.

|

|

|

Since is also increasing and continuous, then there exist

finite limits and . Thus . By (21), we have

|

|

|

Hence, . Since for all

, and

|

|

|

is finite, then necessarily .

Analogously we get . Thus there

exist limits and , which implies that . □

11. Models with infinite value function

We will show here that if is either a Brownian motion or a

geometric Brownian motion, then the value function in Problem A

is infinite.

Let us observe first that we may assume that optimal consumption is of the proportional form , where

|

|

|

for given by (2) and is well defined. Also

in this case the HJB equation and the optimal consumption

have the form (6) and (8) respectively.

Moreover,

|

|

|

and consequently

|

|

|

which implies that

|

|

|

Thus from now on, we assume that our consumption is of the

proportional form and

| (54) |

|

|

|

with for every .

Lemma 4.

Assume . Then:

If , then there is a consumption

rate such that for all .

If , then

| (55) |

|

|

|

|

|

|

|

|

Proof of i) Whenever ,

then (54) gives us the claim with . □

Proof of ii) Since now , we have

and

|

|

|

instead of (6). If , then

|

|

|

Now we formulate necessary and sufficient conditions for

finiteness of value function . Set .

Lemma 5.

If is finite for all , then

| (56) |

|

|

|

If the performance functional is given by

(54) and

| (57) |

|

|

|

holds with , then is finite for all

.

Proof of i) Taking constant gives us the

claim. □

Proof of ii) Set . From (54) we have

|

|

|

and from Hölder’s inequality is dominated by

|

|

|

From Lemma 4 with , the expression in the

second bracket above is finite for every and such

that . Thus (57) gives us the claim. □

Proposition 5.

If is a drifted Brownian motion

|

|

|

or is a geometric Brownian motion

|

|

|

then (56) does not hold for any and consequently the

value function for Problem is infinite.

Proof Notice that , which implies

|

|

|

Thus if is a

drifted Brownian motion, then

|

|

|

|

|

|

|

|

for all . Hence, .

Notice that for all . Thus if

is a geometric Brownian motion, then we have

|

|

|

|

|

|

|

|

|

|

|

|

for all . Hence, . Moreover

, since in this case for every . □

Appendix - proof of -semigroup property of in case of Vasicek model

For any define

|

|

|

Note that , and for , where is given by

(42). We assume that and are given by

(41) and (23) respectively.

In the subsequent steps of the proof we need the following result.

Lemma 6.

For any and any ,

|

|

|

Proof Notice that we do not assume that

. This will be shown later. Let and

be given by (45) and (47) respectively. We have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 1. Denote by the space of all functions

, which are Lipschitz continuous. Here we show that

for any .

Define a sequence of continuous functions

|

|

|

Then

|

|

|

where

|

|

|

|

|

|

|

|

|

|

|

|

Now we show that . To this end write

|

|

|

and define a function as

|

|

|

which is Lipschitz continuous with constant , since both

and are Lipschitz continuous.

Denote by the value of with initial

condition . We have

|

|

|

where is the Euclidean norm.

Since

|

|

|

with and Lipschitz continuous, then

from the mean-square continuity of (see [9])

we have

|

|

|

for all .

Since we consider close to , it is now sufficient to show

that converges to , as , uniformly in for any . We obtain

|

|

|

and from the Schwarz inequality

|

|

|

By (50) and Chebyshev’s inequality,

|

|

|

|

|

|

|

|

as . In a similar way we show that

|

|

|

for every . Thus and the

convergence is uniform in .

Thus we have

|

|

|

Hence, is continuous for all and .

Step 2. We show that for any .

Let us fix a . As is dense in , there

exists an approximating sequence such that

and in .

Set . We have

|

|

|

|

|

|

|

|

|

|

|

|

and from Lemma 6

|

|

|

Furthermore, from Step 1, , i.e.

|

|

|

and therefore

|

|

|

Step 3. Here we show that . For any

write

|

|

|

We need to show that . From (44) and (47)

we have

|

|

|

|

|

|

|

|

and from the Schwarz inequality

|

|

|

Hence

|

|

|

where

|

|

|

Clearly for any fixed , by (48)

and (50).

Set . Since , then there exists a

such that

|

|

|

in a set and therefore

|

|

|

where is the supremum norm over

. Clearly for every

. From (44),

|

|

|

|

|

|

|

|

and

|

|

|

by (46) and (50). Hence, .

Step 4. Clearly and holds since is a Markov process. We need to show

strong continuity of , i.e

| (58) |

|

|

|

Taking into account Lemma 6 and the Banach–Steinhaus

theorem, it is enough to show (58) for . For such a we have

|

|

|

where

|

|

|

|

|

|

|

|

|

|

|

|

Since , then there exists a

such that

and

|

|

|

where

|

|

|

|

|

|

|

|

Since uniformly in ,

we easily verify that .

Set . Recall, that every continuous function on a

compact set is uniformly continuous. Thus there exists a such that

|

|

|

|

|

|

|

|

where is the supremum norm. Hence

|

|

|

|

|

|

|

|

where is a normal distribution function of

and

|

|

|

The supremum is attained at or , but with a possible infinite limit, i.e. . In all this cases we

obtain

|

|

|

Hence, taking , .

Finally, from the Schwartz inequality

|

|

|

where we can easily derive an analytic formula of . Then we take into consideration

all the possible realization of supremum , as above, and

we get .