Utility Function and Optimum Consumption in the models with Habit Formation and Catching up with the Joneses

This paper analyzes popular time-nonseparable utility functions that describe “habit formation” consumer preferences comparing current consumption with the time averaged past consumption of the same individual and “catching up with the Joneses” (CuJ) models comparing individual consumption with a cross-sectional average consumption level. Few of these models give reasonable optimum consumption time series. We introduce theoretically justified utility specifications leading to a plausible consumption behavior to show that habit formation preferences must be described by a power CRRA utility function different from the exponential CARA used for CuJ.

Keywords: Optimal Consumption, Habit Formation, Catching up with the Joneses

JEL codes:

3.006 C6 - Mathematical Methods and Programming;

4.001 D1 - Household Behavior;

5.002 E2 - Consumption, Saving, Production, Employment, and Investment.

1 Introduction

The main properties of the Morgenstern-von Neumann utility function are convexity () and time-separability meaning that utility is derived from the current consumption independent of the past. These simplifying assumptions have faced repeated theoretical criticism (?, ?) and lead to paradoxes when compared to the empirical data (?, ?).

Numerous attempts to resolve these problems within the expected utility approach can be classified (following ?) into two categories by the ways in which the time-nonseparable utility function is constructed. The first, external criterion, category considers the averaged consumption of the economy as a standard of living benchmark compared to which the current individual’s consumption preferences are computed. This “catching up with the Joneses” (CuJ) approach was introduced in ? and developed in ? and ?. The utility function typically has the form where is the per capita consumption in the economy (?, ?). The second, internal criterion, category uses individual’s own past consumption as a benchmark for the current consumption. This “habit formation” approach was initially proposed in ? and usually assumes that the current consumption is compared to the weighted aggregate or recent past consumption either additively () (?, ?, ?) or multiplicatively () (?, ?) in the utility function. The papers ?, ? and ? attempt to combine both habit formation and CuJ in a single utility function.

The present work examines some existing time-nonseparable utility specifications and discuss their feasibility. Qualitative analysis is also used to construct utility functions which satisfy both analytical requirements and empirical data.

2 Habit Formation

2.1 Critique of the short-memory utility function

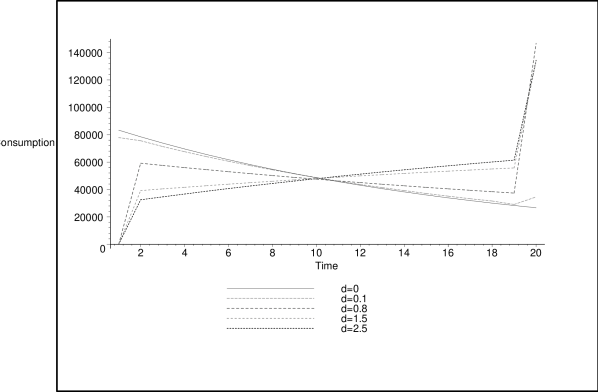

Consider a short-memory utility function in which the current consumption is compared to the past consumption during the last-period only, namely The typical form used in the literature (e.g. ?, ?) is where is a constant and has an isoelastic form with a constant relative risk aversion To see whether such a utility function leads to a plausible optimum policy for consumption, we maximize the life-time discounted utility

subject to

The direct optimization was carried out using the computer algebra software Maple 12, and the numerical results for risk aversion consumption period years, discount factor , initial wealth and inherited consumption =$100,000 are shown in Fig. 1.

The memory for one year only does make consumption grow with time for quite large but also creates huge jumps in consumption at the first and at the last year. In a particular case of the logarithmic utility (CRRA with ) with and the objective function simplifies to

and that it becomes optimal to wait until the end and consume all of the wealth in the last year, which is unrealistic.

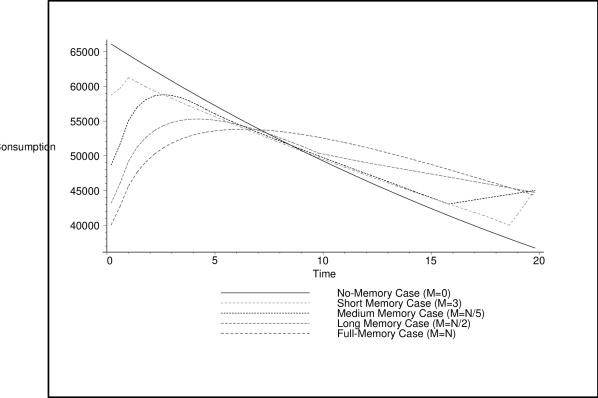

A similar phenomenon is observed with an -period utility for which the objective function takes the form ():

Numerical results for various memory lengths in Fig. 2 show

that the length of the consumer’s memory drastically changes his consumption in the first and last years, leaving intermediate consumption almost unchanged.

Avoiding abrupt changes in the optimum consumption behavior requires memory of every past period. Only in this case does the consumption become smooth and give plausible habit forming behavior — consumption increases as habits form, then becomes saturated and afterwards slowly decreases due to the discount factor . Therefore there is a tradeoff between habit formation and the consumer’s time preferences described by the discount factor.

The habit formation’s strength can be varied by introducing a parameter such that the utility function becomes where is the averaged past consumption

2.2 Critique of the additive utility function

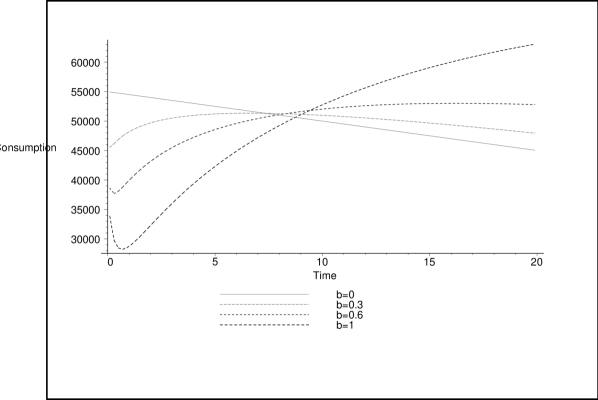

Another class of habit formation utility functions includes full memory about past consumption. Many authors (e.g. ?, ?, ?) consider the utility of the additive form where is the weighted aggregate past consumption. For the isoelastic utility this specification implies that consumption has to stay above or equal to As a result of this “additive=addictive” utility, the optimum consumption suffers from the pathological solution allowing “individual’s bankruptcy” for some This pathology remains, even if it is slightly reduced by replacing by the averaged consumption or its weighted analogue and simply stops working for quite high values of

One remedy might be to replace the CRRA utility by the constant absolute risk aversion (CARA) utility therefore allowing negative values of

To see whether this is the case, consider the problem of optimizing the objective function

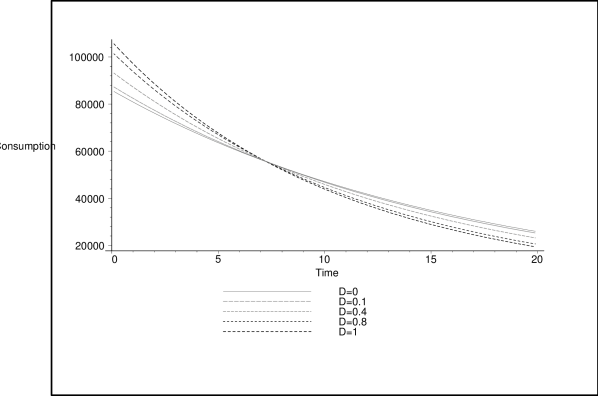

The optimum solution is shown in Fig. 3. This consumption path begins with an intuitively challenging initial trough. A better way to fix the problem was already mentioned in the previous section. The “multiplicative” utility is a good candidate for the habit formation both from a theoretical perspective as well as from the point of view of the optimum solution behavior. Numerical solutions for several parameters are shown in Fig. 4.

2.3 Utility function for habit formation

Another type of utility function of the form was also examined and found to be not suitable for the description of habit formation because it led to decreasing consumption paths. In summary, we found that there are two simple types of utility functions that seem to give feasible optimum solutions for consumption:

-

•

-

•

The latter form of utility is used by the authors ? and ?. However, they also include a second part that represents CuJ and seems to be misused for that purpose, as explained in the next section.

3 Catching Up with the Joneses

3.1 Critique of the multiplicative utility function

The “Catching up with the Joneses” (CuJ) idea introduces external preferences into the consumer’s behavior. An individual’s level of consumption is directly related to the whole economy through the per-capita consumption : if the economy grows, an individual will feel a need to increase his consumption to maintain his happiness. Therefore, one expects a positive change in the optimum consumption (relative to the standard time-separable solution) with a positive change in per-capita consumption. Unfortunately, some of the popular models of utility functions for CuJ lead, as we will see, to the opposite behavior.

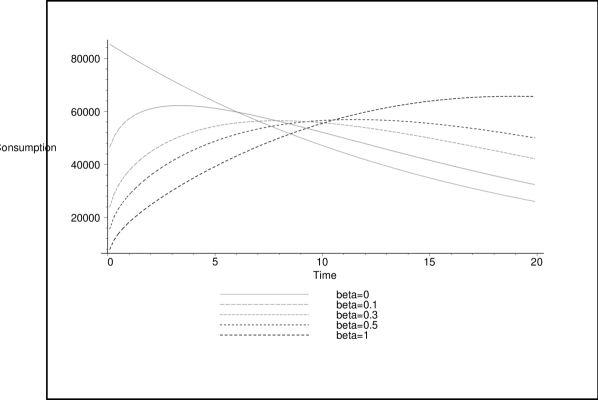

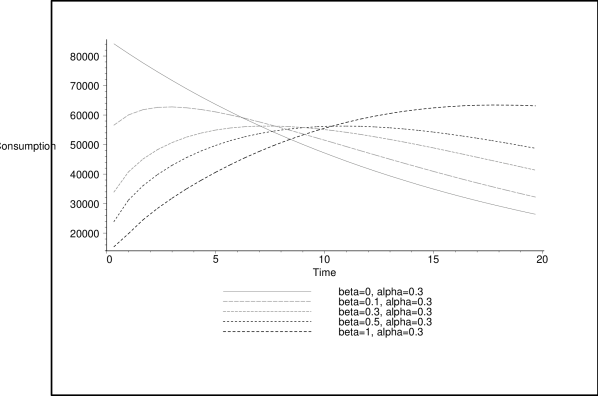

Following ? and ?, ? we consider the utility function of the form

where is a tunable constant. We also assume that the per-capita consumption is a linear function approximately doubling every 30 years (?). The numerical results are shown in Fig. 5.

We can see that the consumption decreases even faster with time than in the standard model with , opposite to the assumption of growing economy. This multiplicative utility type is therefore unsuitable for modeling CuJ. This result is easily extended to any growing function and is particularly obvious for exponentially increasing which imply, for any positive and isoelastic preferences, decreasing in time utility

equivalent to the utility without CuJ discounted, however, with a bigger factor . Moreover, even the case where is negative, equivalent to the utility function considered by ?, fails to predict increasing consumption.

3.2 Utility function for catching up with the Joneses

A hint on modelling CuJ comes from the empirical “Easterlin Paradox” result (see ?, ?) which shows that, despite sharp rises in per-capita GDP, average happiness has remained constant over time. Mathematically this behavior can be expressed as or

Empirical data suggest that which gives and assuming to be approximately linear (confirmed by Fig. 6.) yields a simple partial differential equation of the form

with a constant which is easily integrated giving

So the utility function for CuJ must be additive.

Further numerical analysis shows that, similar to the case of habit formation, the additive utility cannot be assumed isoelastic (as in ?) because of possible negative values of so must be of the CARA type. In Fig. 6. we present optimal consumption for

Two other types of utilities: and were also considered and found unsuitable for CuJ because the former led to decreasing consumption paths and the latter didn’t influence the optimum consumption at all ( separates from ).

We conclude that empirical consumption growth evidence suggests a simple utility form which best describes consumption externalities should be exponential CARA type

4 Conclusions

This paper examines several widely-used utility specifications designed to describe internal consumer preferences that specify her consumption path based on past consumption (habit formation), and preference externalities (catching up with the Joneses). Few of these models lead to feasible patterns in the consumption path of the consumer. We recommend how to change the utility function to correctly reflect the consumer’s theoretical and empirical behavior.

The paper concludes that habit formation should be described by the isoelastic CRRA utility of the form

and that catching up with the Joneses should be described by the exponential CARA utility

These may be combined in a single utility function via the linear combination

The corresponds to pure habit formation and corresponds to pure catching up with the Joneses. The optimum consumption for an intermediate case is shown in Fig. 7.

References

- [1]

- [2] [] Abel, A., 1990, Asset prices under habit formation and catching up with the Joneses, American Economic Review, 80, 38–42.

- [3]

- [4] [] Alvarez-Cuadrado, F., G. Monteiro, and S. Turnovsky, 2004, Habit formation, catching up with the Joneses, and economic growth, Journal of Economic Growth, 9, 47–80.

- [5]

- [6] [] Clark, A., P. Frijters, and M. Shields, 2008, Relative income, happiness and utility: An explanation for the Easterlin paradox and other puzzles, Journal of Economic Literature, XLVI, 95–144.

- [7]

- [8] [] Constantinides, G., 1990, Habit formation: A resolution of the equity premium puzzle, The Journal of Political Economy, 98, 519–543.

- [9]

- [10] [] Duesenberry, J., 1949, Income, Saving and the Theory of Consumer Behavior, Cambridge, MA: Harward University Press.

- [11]

- [12] [] Easterlin, R., 1974, Does economic growth improve the human lot? Some empirical evidence, in R. David and R. Reder, eds., Nations and Households in Economic Growth: Essays in Honor of Moses Abramovitz, New York: Academic Press, 89–125.

- [13]

- [14] [] Fuhrer, J., 2000, Habit formation in consumption and its implications for monetary policy models, American Economic Review, 90, 367–390.

- [15]

- [16] [] Galí, J., 1990, Finite horizons, life-cycle savings, and time-series evidence on consumption, Journal of Monetary Economics, 26, 433–452.

- [17]

- [18] [] Galí, J., 1994, Keeping up with the Joneses: Consumption externalities, portfolio choice, and asset prices, Journal of Money, Credit and Banking, 26, 1–8.

- [19]

- [20] [] Gómez, M., 2007, Equilibrium efficiency in the Ramsey model with habit formation, Berkeley Electronic Press: Studies in Nonlinear Dynamics & Econometrics, 11, 1–32.

- [21]

- [22] [] Kahneman, D. and A. Tversky, 1979, Prospect theory: An analysis of decision under risk, Econometrica, 47, 263–291.

- [23]

- [24] [] Ljungqvist, L. and H. Uhlig, 2000, Tax policy and aggregate demand management under catching up with the Joneses, The American Economic Review, 90, 356–366.

- [25]

- [26] [] Mehra, R. and E. Prescott, 1985, The equity premium: A puzzle,” Journal of Monetary Economics, 15, 145–161.

- [27]

- [28] [] Ryder, H. and G. Heal, 1973, Optimal growth with intertemporally dependent preferences, The Review of Economic Studies, 40, 1–31.

- [29]

- [30] [] Shoemaker, P., 1982, The expected utility model: Its variants, purposes, evidence and limitations, Journal of Economic Literature, 20, 529–563.

- [31]

- [32] [] Smith, W., 2002, Consumption and saving with habit formation and durability, Economic Letters, 75, 369–375.

- [33]

- [34] [] Sundaresan, S., 1989, Intertemporally dependent preferences and the volatility of consumption and wealth, The Review of Financial Studies, 2, 73–89.

- [35]