On the rates of convergence of simulation based optimization algorithms for optimal stopping problems

Abstract

In this paper we study simulation based optimization algorithms for solving discrete time optimal stopping problems. This type of algorithms became popular among practioneers working in the area of quantitative finance. Using large deviation theory for the increments of empirical processes, we derive optimal convergence rates and show that they can not be improved in general. The rates derived provide a guide to the choice of the number of simulated paths needed in optimization step, which is crucial for the good performance of any simulation based optimization algorithm. Finally, we present a numerical example of solving optimal stopping problem arising in option pricing that illustrates our theoretical findings.

Keywords: optimal stopping, simulation based algorithms, entropy with bracketing, increments of empirical processes

1 Introduction

The theory of optimal stopping is concerned with the problem of choosing a time to take a particular action, in order to maximise an expected reward or minimise an expected cost. Optimal stopping problems can be found in many areas of statistics, economics, and mathematical finance. They can often be written in the form of a Bellman equation, and are therefore often solved using dynamic programming. Results on optimal stopping were first developed in the discrete case. The formulation of optimal stopping problems for discrete stochastic processes was in sequential analysis, an area of mathematical statistics where the number of observations is not fixed in advance but is a random number determined by the behavior of the data being observed. Snell (1952) was the first person to come up with results on optimal stopping theory for stochastic processes in discrete time. We refer to the book of Peskir and Shiryaev (2006) for a comprehensive review on different aspects of optimal stopping problems.

A huge impetus to the development of optimal stopping theory was provided by option pricing theory, developed in the late 1960s and the 1970s. According to the modern financial theory, pricing an American option in a complete market is equivalent to solving an optimal stopping problem (with a corresponding generalization in incomplete markets), the optimal stopping time being the rational time for the option to be exercised. Due to the enormous importance of the early exercise feature in finance, this line of research has been intensively pursued in recent times. Solving the optimal stopping problem and hence pricing an American option is straightforward in low dimensions. However, many problems arising in practice have high dimensions, and these applications have motivated the development of Monte Carlo methods for pricing American option. Solving a high-dimensional optimal stopping problems or pricing American style derivatives with Monte Carlo is a challenging task because the determination of the optimal value function requires a backwards dynamic programming algorithm that appears to be incompatible with the forward nature of Monte Carlo simulation. Much research was focused on the development of fast methods to compute approximations to the optimal value function. Notable examples include mesh method of Broadie and Glasserman (1997), the regression-based approaches of Carriere (1996), Longstaff and Schwartz (2001), Tsitsiklis and Van Roy (1999) and Egloff (2005). All these methods aim at approximating the so called continuation values that can be used later to construct suboptimal strategies and to produce lower bounds for the optimal value function. The convergence analysis for this type of methods was performed in several papers including Egloff (2005), Egloff, Kohler and Todorovic (2007) and Belomestny (2009). An alternative to trying to approximate the continuation values is to find the best value function within a class of stopping rules. This reduces the optimal stopping problem to a much more tractable finite dimensional optimization problem. Such optimization problems appear naturally if one considers finite dimensional or parametric approximations for the corresponding stopping regions. The latter type of algorithms became particularly popular among practioneers (see e.g. Andersen (2000) or Garcia (2001)). However, the practical success of simulation-based optimization algorithms has not been yet fully explained by existing theory, and our analysis here represents a further step toward an improved understanding. The main goal of this work is to provide rigorous convergence analysis of simulation based optimization algorithms for discrete time optimal stopping problems.

Let us start with a general stochastic programming problem

| (1.1) |

where is a subset of , is a valued random variable on the probability space and Draw an i.i.d. sample from the distribution of and define

It is well known (see e.g. Shapiro (1993)) that under very mild conditions it holds In their pioneering work Shapiro and Homem-de-Mello (2000) (see also Kleywegt, Shapiro and Homem-de-Mello (2001)) showed that in the case of discrete random variable the convergence of to can be much faster than making Monte Carlo method particularly efficient in this situation. Turn now to the discrete time optimal stopping problem:

| (1.2) |

where is a stopping time taking values in the set and is a Markov chain. Since the random variable takes only discrete values, one can ask whether the simulation based methods in the case of discrete time optimal stopping problem (1.2) can be as efficient as in the case of (1.1) with discrete r.v. . In this work we give an affirmative answer to this question by deriving the optimal rates of convergence for the corresponding Monte Carlo estimate of based on paths and showing that these rates are usually faster than .

2 Main setup

Let us consider a Markov chain defined on a filtered probability space and taking values in a measurable space where for simplicity we assume that for some and is the Borel -algebra on It is assumed that the chain starts at under for some . We also assume that the mapping is measurable for each . Fix some natural number Given a set of measurable functions , satisfying

for all , we consider the optimal stopping problems

| (2.3) |

where for any the expectation in (2.3) is taken w.r.t. the measure such that under and the supremum is taken over all stopping times with respect to Introduce the stopping region with and

Introduce also the first entry times into by setting

It is well known that the value functions satisfy the so called Wald-Bellman equations

with by definition. Moreover, the stopping times are optimal in (2.3), i.e.

Let be independent processes with the same distribution as all starting from the point We can think of as a new process defined on the product probability space equipped with the product measure Let be a collection of sets from the product -algebra

that contains all sets of the form with Here we take into account the fact that the stopping set must coincide with Let be a subset of Define

The stopping rule

is generally suboptimal and therefore the corresponding Monte Carlo estimate

| (2.4) |

with

based on a new, independent of set of trajectories

fulfills

| (2.5) |

If the set is rich enough, then

and can serve as a good approximation for for large enough and In the next section we are going to study the question: how fast does converge to as ? We will show that the corresponding rates of convergence are always faster than usual rates This fact has a practical implication since it indicates that , the number of simulated paths used in the optimization step, can be taken much smaller than the number of paths used to compute the final estimate .

3 Main results

Definition

Let be a given number and be a pseudedistance between two elements of defined as

| (3.6) |

where and are subsets of Define be the smallest value for which there exist pairs of sets

such that for all and for any there exists for which

Then the value is called the -entropy with bracketing of for the pseudedistance .

Assumption

We assume that the family of stopping regions is such that

| (3.7) |

for some constant , any and some .

Example

Let , where is a class of subsets of with boundaries of Hölder smoothness defined as follows. For given and consider the functions having continuous partial derivatives of order , where is the maximal integer that is strictly less than . For such functions , we denote the Taylor polynomial of order at a point by . For a given , let be the class of functions such that

where stands for the Euclidean norm of Any function from determines a set

Define the class

| (3.8) |

It can be shown (see Dudley, 1999, Section 8.2) that the class fulfills

for some and all small enough. Now we are in the position to formulate the main result of our study.

Theorem 3.1.

Let be a subset of such that assumption (3.7) is fulfilled with some and

| (3.9) |

with and some constant Assume that all functions are uniformly bounded and the inequalities

| (3.10) |

hold for some , , and . Then for any and

| (3.11) |

with some constants , , and

Remark 3.2.

Remark 3.3.

The above convergence rates can not be in general improved as shown in the next theorem.

Proposition 3.4.

Consider the problem (2.3) with and two possible stopping dates, i.e. . Fix a pair of non-zero functions such that and on Fix some and and let be a class of pricing measures such that the condition (3.10) is fulfilled and for any the corresponding stopping set is in Then there exist a subset of and a constant such that for any , any stopping time measurable w.r.t.

Discussion

It follows from Theorem 3.1 that

as long as Using the decomposition

and the fact that for any , we conclude that

Hence, given , a reasonable choice of , the number of Monte Carlo paths used in the optimization step, can be defined as In the case when there exists a parametric family of stopping regions satisfying (3.9) (see Section 4 for some examples), one gets

| (3.12) |

since any parametric family of stopping regions with finite dimensional parameter set fulfills (3.7) for arbitrary small Let us also make a few remarks on the condition (3.10) and the parameter . If each function has a non-vanishing Jacobian in the vicinity of the stopping boundary and has continuous distribution, then (3.10) is fulfilled with In fact, it is not difficult to construct examples showing that the parameter can take any value from . If (the most common case) (3.12) simplifies to , the choice supported by our numerical example.

Finally, we would like to mention an interesting methodological connection between our analysis and the analysis of statistical discrimination problem performed in Mammen and Tsybakov (1999) (see also Devroye, Györfi and Lugosi (1996)). In particular, we need similar results form the theory of empirical processes and the condition (3.10) formally resembles the so called “margin” condition often encountered in the literature on discrimination analysis.

4 Applications

In this section we illustrate our theoretical results by some financial applications. Namely, we consider the problem of pricing Bermudan options. The pricing of American-style options is one of the most challenging problems in computational finance, particularly when more than one factor affects the option values. Simulation based methods have become increasingly attractive compared to other numerical methods as the dimension of the problem increases. The reason for this is that the convergence rates of simulation based methods are generally independent of the number of state variables. In the context of our paper we consider the so called parametric approximation algorithms (see Glasserman, 2003, Section 8.2). In essence, these algorithms represent the optimal stopping sets by a finite numbers of parameters and then find the Bermudan option price by maximizing, over the parameter space, a Monte Carlo approximation of the corresponding value function. The important question here is wether on can parametrize the optimal stopping region by a finite dimensional set of parameters, i.e. where is a compact finite dimensional set. It turns out that that this is possible in many situations (see Garcia (2001)). The assumption (3.7) and (3.9) are then automatically fulfilled with arbitrary small

4.1 Numerical example: Bermudan max call

This is a benchmark example studied in Broadie and Glasserman (1997) and Glasserman (2003) among others. Specifically, the model with identically distributed assets is considered, where each underlying has dividend yield . The risk-neutral dynamic of the asset is given by

where , are independent one-dimensional Brownian motions and are constants. At any time the holder of the option may exercise it and receive the payoff

where for We take , , , , , and , with as in Glasserman (2003, Chapter 8).

To describe the optimal early exercise region at date one can divide into three different connected sets: one exercise region and two continuation regions (see Broadie and Detemple (1997) for more details). All these regions can be parameterized by using two functions depending on two dimensional parameter Making use of this characterization, we define a parametric family of stopping regions as in Garcia (2001) via

where and is a compact subset of Furthermore, we simplify the corresponding optimization problem by setting This will introduce an additional bias and hence may increase the left hand side of (3.9) (see Remark 3.2). However, this bias turns out to be rather small in practice. In order to implement and analyze the simulation based optimization based algorithm in this situation, we perform the following steps:

-

•

Simulate independent sets of trajectories of the process each of the size :

where

-

•

Compute estimates via

-

•

Simulate a new set of trajectories of size independent of

-

•

Compute estimates for the optimal value function as follows

with

Denote by the standard deviation computed from the sample and set

-

•

Compute

By the law of large numbers

| (4.13) | |||||

| (4.14) |

where

The difference with

can be decomposed into the sum of three terms

| (4.15) |

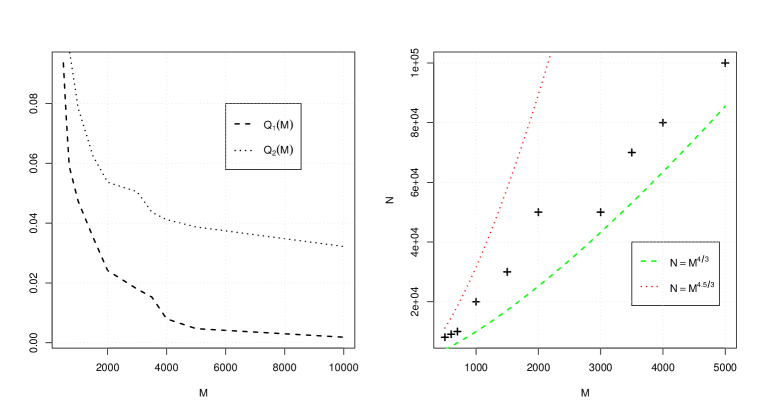

The first term in (4.15) is deterministic and can be approximated by with large enough , and The variability of the second, zero mean, stochastic term can be measured by which in turn can be estimated by , due to (4.14). The standard deviation of for any can be approximated by . In our simulation study we take and obtain (note that according to Glasserman (2003)). In the left-hand side of Figure 1 we plot both quantities and as functions of Note that dominates , especially for large Hence, by comparing with and approximately solving the equation in , one can infer on the optimal relation between and . In Figure 1 (on the right-hand side) the resulting empirical relation is depicted by crosses. Additionally, we plotted two benchmark curves and . As one can see the choice is likely to be sufficient in this situation since it always leads to the inequality for any As a consequence, for and any , lies with high probability in the interval provided that is large enough.

5 Proof of main results

5.1 Proof of Theorem 3.1

Define

and for any Since

with probability , it holds

| (5.16) |

with Set then

Define

and set for Note that under assumption (3.7) the condition (6.17) of Theorem 6.1 is fulfilled with due to Corollary 6.3. Hence Theorem 6.1 yields Denote

for any Since and , we get on

with . Combining Corollary 6.3 with Corollary 6.4 leads to the inequality

which holds on the set where and are defined in Corollary 6.4. Denote

with some It then holds on

and therefore

with Let us now estimate Using Corollary 6.4, we get

with Furthermore, due to (5.16)

for large enough Theorem 6.1 implies

with some constants and Applying Theorem 6.1 to and using the fact that for all we finally obtain the inequality

which holds for all and with some constant depending on

5.2 Proof of Proposition 3.4

For simplicity, we give the proof only for the case (an extension to higher dimensions is straightforward). In the case of two exercise dates the corresponding optimal stopping problem is completely specified by the distribution of the vector Because of a digital structure of the distribution of would be completely determined if the marginal distribution of and the probability are defined. Taking into account this, we now construct a family of distributions for indexed by elements of the set First, the marginal distribution of is supposed to be the same for all and posseses a density satisfying

Let us now construct a family of conditional distributions , To this end let be an infinitely many times differentiable function on with the following properties: for for all and For put

with some For vectors of elements and for any define

Put for any and any

where is a positive constant. Due to our assumptions on , there are constants such that

Hence, the constant can be chosen in such a way that remains positive and strictly less than on for any The stopping set

belongs to since for small enough. Moreover, for any

and the condition (3.10) is fulfilled. Let be a stopping time w.r.t. , then the identity (see Lemma 6.2)

leads to

with . By conditioning on we get

Using now a well known Birgé’s or Huber’s lemma, (see, e.g. Devroye, Györfi and Lugosi, 1996, p. 243), we get

where and is a Kullback-Leibler distance between two measures and . Since for any two measures and from with

with some constant for small enough , and , we get

with some constant Hence,

provided that for small enough real number . In this case

with

6 Auxiliary results

We have

with functions defined as

Denote Obviously is a class of uniformly bounded functions provided that all functions are uniformly bounded.

Definition

Let be the smallest value of for which there exist pairs of functions such that for all and such that for each there is such that

Then is called the entropy with bracketing of . The following theorem follows directly from Theorem 5.11 in Van de Geer (2000).

Theorem 6.1.

Assume that there exists a constant such that

| (6.17) |

for any and some , where is the -entropy with bracketing of Fix some then for any

for all and where and are two positive constants. Moreover, for any

with some positive constant .

Let us define a pseudedistance between any two sets in the following way

It obviously holds for the pseudodistance defined in The following Lemma will be frequently used in the sequel.

Lemma 6.2.

For any it holds with probability one

| (6.18) |

and

| (6.19) |

for .

Proof.

We prove (6.19) by induction. The inequality (6.18) can be proved in a similar way. For we get

| (6.20) |

since events and are measurable w.r.t. and on the set Thus, (6.19) holds with . Suppose that (6.19) holds with . Let us prove it for . Consider a decomposition

| (6.21) |

with

Using the fact that if for any , we get

and

with probability one. Hence

since on the set Our induction assumption implies now that

and hence (6.19) holds with . ∎

Corollary 6.3.

If with some constant , then

for any

Proof.

Follows directly from (6.18) since a.s. for any stopping time taking values in ∎

Corollary 6.4.

Assume that (3.10) holds for , then there exist constants and such that

| (6.22) |

for all satisfying . Moreover it holds

| (6.23) |

for any

References

- Andersen (2000) L. Andersen (2000). A simple approach to the pricing of Bermudan swaptions in the multi-factor Libor Market Model. Journal of Computational Finance, 3, 5-32.

- Belomestny (2009) D. Belomestny (2009). Pricing Bermudan options using nonparametric regression: optimal rates of convergence for lower estimates, http://arxiv.org/abs/0907.5599, forthcoming in Finance and Stochastics.

- Broadie and Glasserman (1997) M. Broadie and P. Glasserman (1997). Pricing American-style securities using simulation. J. of Economic Dynamics and Control, 21, 1323-1352.

- Broadie and Detemple (1997) M. Broadie and J. Detemple (1997). The valuation of American options on multiple assets. Mathematical Finance, 7(3), 241-286.

- Carriere (1996) J. Carriere (1996). Valuation of early-exercise price of options using simulations and nonparametric regression. Insuarance: Mathematics and Economics, 19, 19-30.

- Devroye, Györfi and Lugosi (1996) L. Devroye, L. Györfi and G. Lugosi (1996). A probabilistic theory of pattern recognition. Application of Mathematics (New York), 31, Springer.

- Dudley (1999) R.M. Dudley (1999). Uniform central limit theorems. Cambridge University Press.

- Egloff (2005) D. Egloff (2005). Monte Carlo algorithms for optimal stopping and statistical learning. Ann. Appl. Probab., 15, 1396-1432.

- Egloff, Kohler and Todorovic (2007) D. Egloff, M. Kohler and N. Todorovic (2007). A dynamic look-ahead Monte Carlo algorithm for pricing Bermudan options, Ann. Appl. Probab., 17, 1138-1171.

- Garcia (2001) D. Garcia (2001). Convergence and biases of Monte Carlo estimates of American option prices using a parametric exercise rule. Working paper.

- Glasserman (2003) P. Glasserman (2003). Monte Carlo Methods in Financial Engineering. Springer.

- Kleywegt, Shapiro and Homem-de-Mello (2001) A.J. Kleywegt, A. Shapiro and T. Homem-de-Mello (2001). The sample average approximation method for stochastic discrete optimization, SIAM J. Optim., 12, 479-502.

- Longstaff and Schwartz (2001) F. Longstaff and E. Schwartz (2001). Valuing American options by simulation: a simple least-squares approach. Review of Financial Studies, 14, 113-147.

- Mammen and Tsybakov (1999) E. Mammen and A. Tsybakov (1999). Smooth discrimination analysis. Ann. Statist., 27, 1808-1829.

- Peskir and Shiryaev (2006) G. Peskir and A. Shiryaev (2006). Optimal Stopping and Free-Boundary Problems. LM - Lectures in Mathematics ETH Z rich.

- Shapiro (1993) A. Shapiro (1993). Asymptotic behavior of optimal solutions in stochastic programming, Math. Oper. Res., 18, 829-845.

- Shapiro and Homem-de-Mello (2000) A. Shapiro and T. Homem-de-Mello (2000). On the rate of convergence of optimal solutions of Monte Carlo approximations of stochastic programs. SIAM J. Optim., 11(1), 70-86.

- Snell (1952) J. L. Snell (1952). Applications of martingale system theorems. Trans. Amer. Math. Soc. 73, 293–312.

- Tsitsiklis and Van Roy (1999) J. Tsitsiklis and B. Van Roy (1999). Regression methods for pricing complex American style options. IEEE Trans. Neural. Net., 12, 694-703.

- Van de Geer (2000) S. Van de Geer (2000). Applications of Empirical Process Theory. Cambridge Univ. Press.