Disentangling collective trends from local dynamics

Abstract

A single social phenomenon (such as crime, unemployment or birth rate) can be observed through temporal series corresponding to units at different levels (cities, regions, countries…). Units at a given local level may follow a collective trend imposed by external conditions, but also may display fluctuations of purely local origin. The local behavior is usually computed as the difference between the local data and a global average (e.g. a national average), a view point which can be very misleading. We propose here a method for separating the local dynamics from the global trend in a collection of correlated time series. We take an independent component analysis approach in which we do not assume a small unbiased local contribution in contrast with previously proposed methods. We first test our method on synthetic series generated by correlated random walkers. We then consider crime rate series (in the US and France) and the evolution of obesity rate in the US, which are two important examples of societal measures. For crime rates, the separation between global and local policies is a major subject of debate. For the US, we observe large fluctuations in the transition period of mid-’s during which crime rates increased significantly, whereas since the ’s, the state crime rates are governed by external factors and the importance of local specificities being decreasing. In the case of obesity, our method shows that external factors dominate the evolution of obesity since 2000, and that different states can have different dynamical behavior even if their obesity prevalence is similar.

Classification: Physical sciences (Applied mathematics, Physics), Social sciences.

Keywords: Time series analysis, independent component analysis, financial time series, crime rates, obesity.

I Introduction

Large complex systems are composed of various interconnected components. The measure of the behavior of a single component thus results from the superimposition of different factors acting at different levels. Common factors such as global trends or external socio-economical conditions obviously play a role but usually different sub-units (such as users in the Internet, states or regions in a country) will react in different ways and add their local dynamics to the collective pattern. For example, the number of downloads on a website depends on factors such as the time of the day but one can also observe fluctuations from a user to another one Huberman . In the case of criminality, favorable socio-economical conditions will impose a global decreasing trend while local policies will affect the regional time series. In the case of financial series, the market imposes its own trend and some stocks respond to it more or less dramatically. In all these cases it is important to be able to distinguish if the stocks or regions are at the source of their fluctuations or if on the opposite, they just follow the collective trend.

Extracting local effects in a collection of time series is thus a crucial problem in assessing the efficiency of local policies and more generally, for the understanding of the causes of fluctuations. This problem is very general and as the availability of data is always increasing particularly in social sciences, it becomes always more important for the modeling Castellano:2008 and the understanding of these systems. There is obviously a huge literature on studying stochastic signals Kautz ranging from standard methods to more recents ones such as the detrended fluctuation analysis Peng , independent component analysis ica , and separation of external and internal variables Menezes:2004a ; Menezes:2004b . Most of these methods treat the internal dynamics as a small local perturbation with zero mean which is in contrast with the method proposed here.

In a first part we present the method. In a second part, we test it on synthetic series generated by correlated random walkers. We then apply the method to empirical data of crime rates in the US and France, and obesity rates in the US, for which, to our knowledge, no general quantitative method is known to provide such separation between global and local trends.

II Model and Method

In general, one has a set of time series where and we will assume that the number of units is large. The index refers to a particular unit on a specific scale such as a region, city, a country. The problem we address consists in extracting the collective trend and the effect of local contributions. One way to do so is to assume the signal to be of the form

| (1) |

where the ‘external’ part, , represents the impact on the region of a global trend, while the ‘internal’ part, , represents the contribution due to purely local factors. Usually, in order to discuss the impact of local policies, one compares a regional (local) curve to the average (the national average in case of regions of a country) computed as

| (2) |

(or if one has intensive variables and populations ). Although reasonable at first sight, this assumes that the local component is purely additive: local term. In this article, following Menezes:2004a ; Menezes:2004b , we will rather consider the possibility of having both multiplicative and additive contributions. More specifically, we assume

| (3) |

where is a collective trend common to all series, and which affects each region with a corresponding prefactor . These coefficients are assumed to depend weakly on the period considered, ie. to vary slowly with time. We thus write

| (4) |

We first note that the global trend is known up to a multiplicative factor only (one cannot distinguish from whatever ) and we will come back to this issue of scale later. Also, the purely additive case is recovered if the ’s are independent of . If on the contrary the ’s are different from one region to the other, the national average (2), , is then given by

| (5) |

Here and in the following we denote the sample average, that is the average over all units , by a bar, , and the temporal average by brackets . The ‘naive’ local contribution is then estimated by the difference with the national average

| (6) | |||||

The estimated local contribution can thus be very different from the original one, , and the difference will be very large at all times where is large (note that the conclusion would be the same by taking the national average as ). This demonstrates that comparing local time series with the naive average could in general be very misleading. Beside the correct computation of the external and internal contributions, the existence of both multiplicative and additive local contributions implies that the effect of local policies must be analyzed by considering both how the local unit follows the global trend () and how evolves the purely internal contribution ().

In a previous study Menezes:2004a , Menezes and Barabasi proposed a simple method to separate the two contributions, internal () and external ( written as ). They assume that the temporal average is zero, and compute the external and internal parts by writing

| (7) |

and . This method can be shown to be correct in very specific situations, such as the case where is the fluctuating number of random walkers at node in a network, but in many cases however, one can expect that the local contributions have a non zero sample average and the method of Menezes:2004a ; Menezes:2004b will yield incorrect results. Indeed, if the hypothesis Eq. (4) is exact, this method would give for the estimate , and in the limit for would lead to the estimates and , which are different from the exact results, except if .

In order to separate the two contributions we propose in this article a totally different approach, by taking an independent component analysis point of view in which we do not assume that the local contribution has a zero average (over time and/or over the regions). To express the idea that the ‘internal’ contribution is by definition what is specifically independent of the global trend, and that the correlations between regions exist essentially only through their dependence in the global trend, we impose that the global trend is statistically independent from local fluctuations

| (8) |

(we denote by the connected correlation ), and that these local fluctuations are essentially independent from region to region, that is for

| (9) |

where this statement will be made more precise below. We show that, for large , these constraints (8), (9) are sufficient to extract estimates of the global trend and of the ’s.

We denote by the average of and by its dispersion, so that we write

| (10) |

with and . If we denote by and , we have

| (11) |

with

| (12) |

Note that . If we now consider the correlations between these centered quantities, , we find

| (13) |

If we assume that for is negligible (of order ) compared to (which is what we mean by having small correlations between internal components, Eq. (9)), from this last expression we can show that at the dominant order in , we have

| (14) | |||||

| (15) |

These equations lead to

| (16) |

which is valid when . We note that our method has a meaning only if strong correlations exist between the different ’s and if it is not the case, the definition of a global trend makes no sense and the approximation used in our calculations are not valid.

In the Supporting Information (section SI1) we show that the factors ’s can also be computed as the components of the eigenvector corresponding to the largest eigenvalue of - a method which is valid under the weaker assumption of having a small number (compared to ) of non diagonal terms of the matrix which are not negligible.

Once the quantities are known, we can compute the global normalized pattern with the reasonable estimator given by ,

| (17) |

Indeed,

| (18) |

and since the quantity is a sum of independent variables with zero mean, we can expect it to behave as . We can show that this actually results from the initial assumptions. Indeed, by construction and the second moment is

| (19) |

By assumption we have if and we thus obtain .

The computation of the ’s and of is equivalent to an independent component analysis (ICA) ica with a single source (the global trend) and a large number of sensors. However, in contrast with the standard ICA, we are not interested in getting only the sources (here the trend ), but also the internal contributions (which, in a standard ICA framework, would be considered as noise terms, typically assumed to be small). We have already the ’s, and since has been calculated we can compute . We thus obtain at this stage

| (20) |

This is a set of equations for unknown ( and the ’s) and we are thus left with one free parameter, the ratio . Knowing its value would give the local averages, the ’s. Less importantly one may want also to fix the average (hence both and ) in order to fully determine the pattern : this will be of interest only for making a direct comparison between this pattern and the national average (2). This equation (20) suggests a statistical linear correlation between and , with a slope given by . We will indeed observe a linear correlation in the data sets (next section, Figure ). However, it could be that the ’s themselves are correlated with the s. Hence, and unfortunately, a linear regression cannot be used to get an unbiased estimate of the parameter . In the absence of additional information or hypothesis this parameter remains arbitrary. However one may compare the qualitative results obtained for different choices of : which properties are robust, and which ones are fragile. In particular one would like to be able to access how a given region is behaving, compared to another given region, and/or to the global trend. To do so, in the applications below we will in particular analyze: (i) the correlations between the two local terms, and ; (ii) the robustness of the rank given by the ’s; (iii) the sign of ; (iv) the quantitative and qualitative similarities between and the naive estimate .

We will focus on two particular scenarios. First, one may ask the global trend to fall ‘right in the middle’ of the series. There are different ways to quantify this. One way to do so is to note that, in the absence of internal contribution, would be equal to , hence would be equal to . Therefore we may compute by imposing

| (21) |

which is thus equivalent to impose An alternative is to ask the resulting to be as close as possible to the naive ones (Eq. (6)), by minimizing which gives

| (22) |

In both cases one may then fix from or by imposing for some arbitrary chosen . Finally, one may rather ask for a conservative comparison with the naive approach by minimizing the difference between and : either by writing (or ) and , or by minimizing , which gives

| (23) |

For is large, one can check that the results depend weakly on any one of these reasonable choices.

The second scenario considers the correlations between the ’s and the ’s. As we will see, the first hypothesis leads to a strictly negative correlation. An alternative is thus to explore the consequences of assuming no correlations, hence asking for

| (24) |

which implies that the slope of the observed linear correlation with gives the value of . As explained above, for each application below we will discuss the robustness of the results with respect to these choices of the parameter .

We can now summarize our method. It consists in (i) estimating the ’s using Eq. (16) (or using the eigenvector corresponding to the largest eigenvalue of the correlation matrix, section SI1), (ii) computing using Eq. (17), and finally (iii) comparing the results for different hypothesis on as discussed above. We propose to call this method the External Trend and Internal Component Analysis (ETICA). We note that if the hypothesis Eq. (4), (8), (9) are correct, the method gives estimates of , the s (hence of ) which become exact in the limit and large, and a good estimate of the full trend (hence of the ) whenever this trend, qualitatively, does fall ‘in the middle’ of the time series.

Once we have extracted with this method the local contribution , and the collective pattern together with its redistribution factor for each local series, we can study different quantities, as illustrated below on different applications of the method. In general, although this method gives a pattern very similar to the sample average , we will see that there is non trivial structure in the prefactors ’s leading to non trivial local contributions .

In some cases one may expect to have, in addition to the local contribution, a linear combination of several global trends (a small number of ’sources’): we leave for future work the extension of our method to several external trends.

III Applications: correlated random walkers, crime rates in the US and France, obesity in the US.

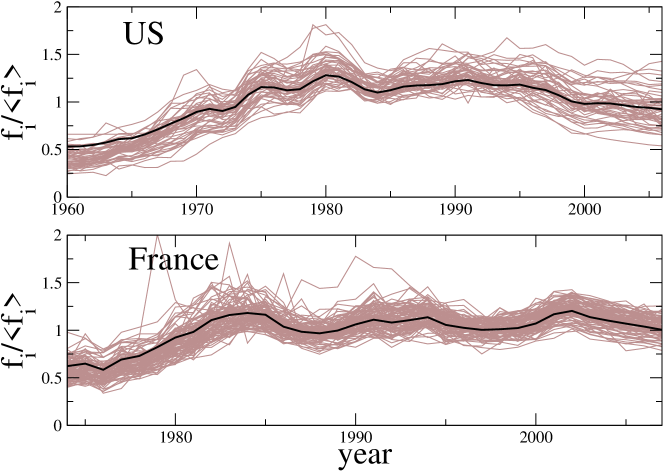

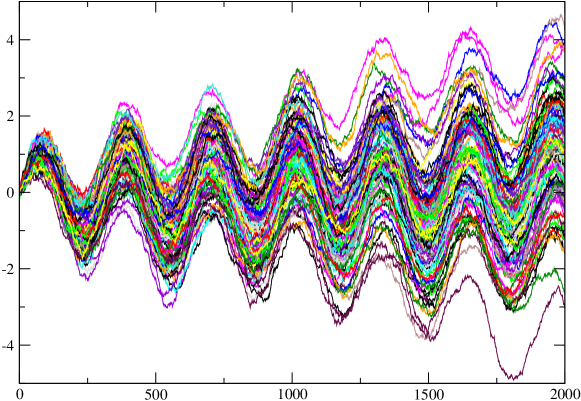

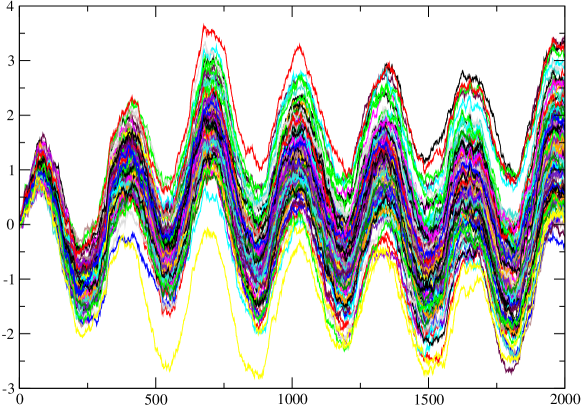

We first test our method on synthetic series and we then illustrate it on crime rate series (in the United States and in France) and on US obesity rate series. For the crime rates, a plot of the time series shows that obviously a common trend exists (Fig. 1).

|

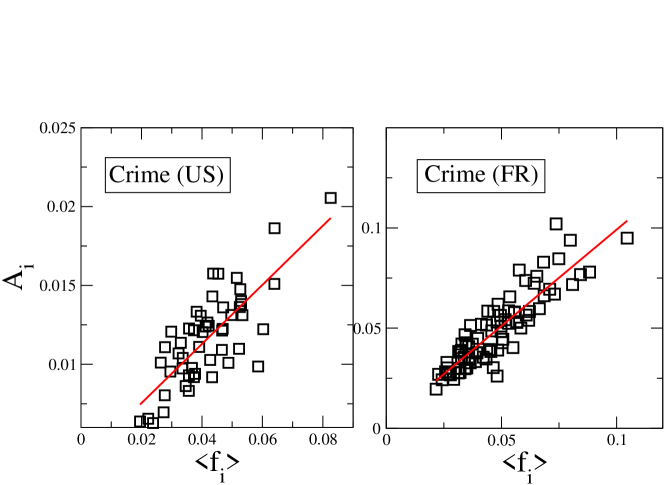

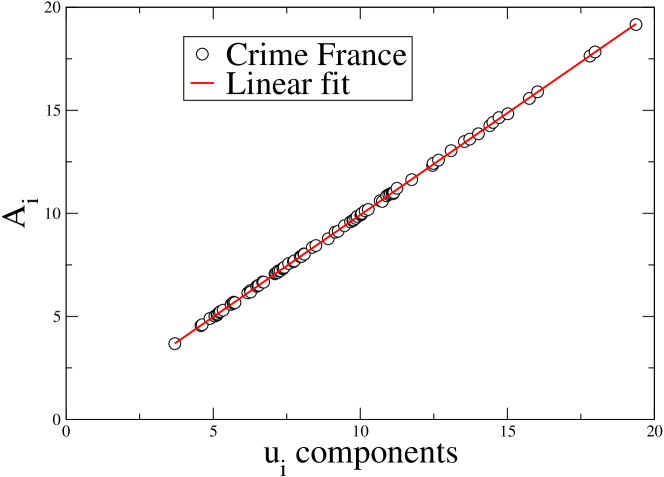

After computing the internal and external terms, we perform different tests in order to assess the validity of the approach. In particular, Figure shows a plot of the local factors s versus the data time-averages, the ’s.

|

One observes a statistical linear correlation in the four set of time series. We stress that the ’s are computed from the covariance matrix of the data, hence after removing the means from the time series. The fact that we do observe a linear correlation is thus a hint that our hypothesis on the data structure is reasonable (in contrast the very good linear correlation observed in Menezes:2004a ; Menezes:2004b can be shown to be an artefact of the method used in these works, leading to an exact proportionality independently of the data structure, (see the section SI2). We now discuss in more detail the synthetic series, each one of the crime rate data sets, and the obesity rate.

III.1 Synthetic series: correlated random walkers.

We can illustrate our method on the case of correlated random walkers described by the equation

| (25) |

where is the global trend imposed to all walkers and the are gaussian noises but with possible correlations between different walkers where and are tunable parameters (see the supporting section SI3). For , the random noises are independent and our method is very accurate: we choose for example a sinusoidal trend and we plot in the figure the original signal, the exact local contribution and the local contribution computed with our method.

|

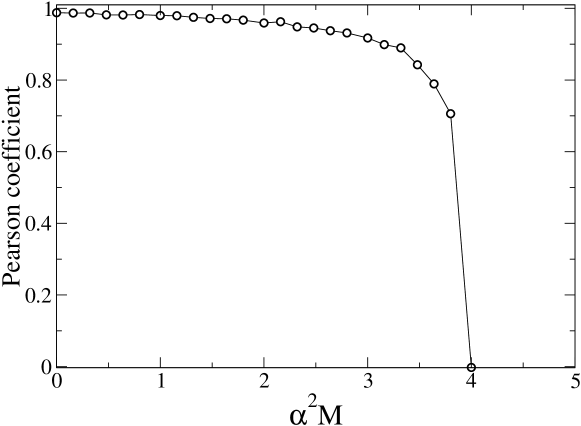

When the correlation between walkers is increasing we study the Pearson correlation coefficient between the original local contribution and the estimate provided by our method, and we observe that our method is indeed accurate as long as the correlations between the ’s are not too large, which corresponds here to the condition .

III.2 Crime rates in the US and France.

In criminology an essential question concerns the impact of local policies, a subject of much debate dMR04 ; Zimring:2007 . In order to assess these local effects (at the level of a state or a region), most authors consider the difference of a state evolution with the national average. As we noticed above this may lead to incorrect predictions. In this second part of applications, we thus illustrate our method on the analysis of the series of crime rates in states in the US refcrimeUS for the period , and about départements of France refcrimeFR for the period . On Fig. we represent these time series normalized by their time average. The observed data collapse confirms the existence of a collective pattern (we also show on this plot the collective pattern obtained with our method). For the French case, we have withdrawn outliers which do not satisfy our initial assumptions. The series of these départements are indeed uncorrelated with the rest of crime rates and cannot be incorporated in the calculation of the collective pattern. We apply our method to these data and extract , the ’s and . As already mentioned, we plot on Fig. the ’s vs. the averages , exhibiting a statistical linear correlation. We can check a posteriori that all conditions assumed in our calculation are fulfilled (zero and small , see SI1). Also, we checked that the coefficients do not vary too much the period considered, which is an important condition for our method (see the discussion on different datasets in the SI4).

In order to assess quantitatively the importance of local versus external fluctuations, we study in particular the ratio of dispersions defined by

| (26) |

where the external contribution is the standard deviation of , that is , and the internal one is given by . Note that these quantities , being based on fluctuations, does not depend on . This quantity is found in both cases in France and in the US larger than one. This indicates that external factors always dominate over local fluctuations, while local policies seem to play a minor role. In the case of crime, these external effects might be socio-economical factors such as unemployment, density, etc.

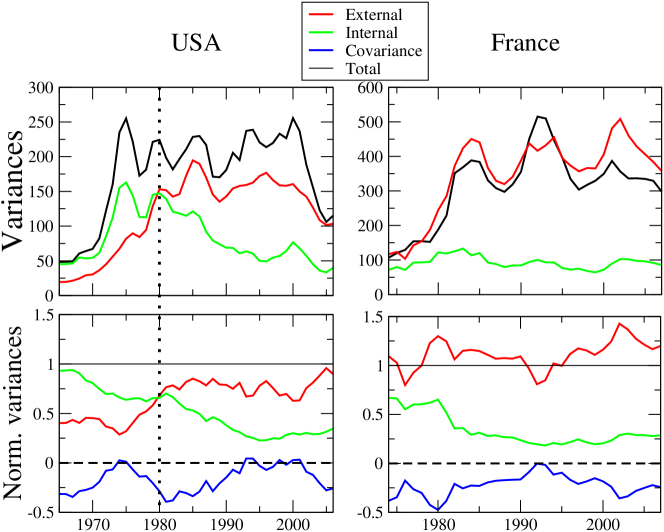

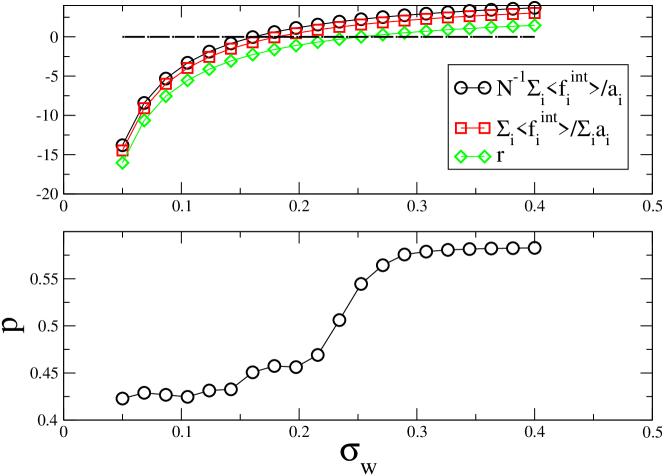

In addition to compute the average of the ’s, we can also observe the time evolution of the heterogeneity defined by the sample variances of the different components. We first observe on Fig. that large fluctuations are observed in the transition period of mid-’s during which crime rates increased significantly.

|

We also observe for the USA that until , fluctuations were essentially governed by local effects but that this trend is inverted and increases in the period post-’s. In particular during the period during which one observes a decline of crime rates Zimring:2007 , it is the collective trend which determines the fluctuations.

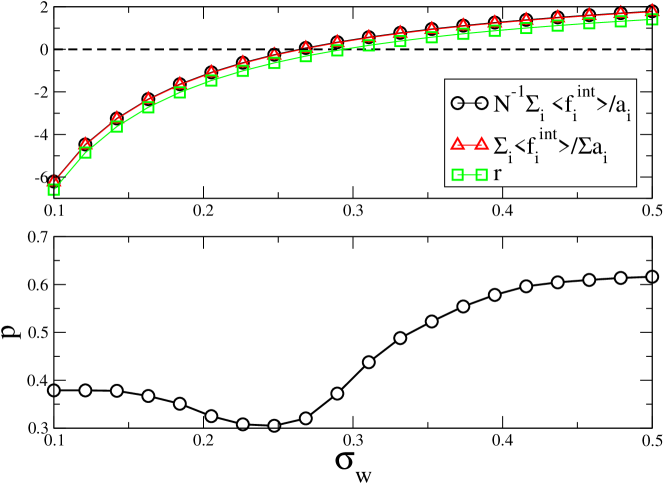

Even we have presented results for reasonable choices of the parameter (in the following we make the harmless choice ), one can ask the question of the robustness of different observed properties. First, we can compare the predictions for obtained for the different assumptions used in this paper. In the upper panels for Figs. and we show for the US (France), the quantities , and .

|

We see on these figures that these quantities are zero for values of which are very close. We also compute the fraction of time for which and the naive calculation have different signs.

|

We plot in the lower panels of Figs. and , the quantity showing a that for this range of , the signs of and are the same for about of the time period. We can also study the sign versus and we can observe some robustness. In particular, in the US case, approximately states (CA, NV, MO, MI, NY, AZ) have a positive local contribution (in the range while states have always a negative local contribution (VT, GA, LA, NH, CT, MS). In these cases we can reasonably imagine that local policies have a noticeable effect.

Finally, we can also analyze the ranking of the local contributions versus by studying Kendall’s for the two consecutive series and . In both cases (France and US) we observe a larger than for the range chose (the control case for a random permutation being less than ) indicating a large robustness of the ranking. This means that independently of the assumption used to compute we can rank the different regions according to the importance of their local contribution.

III.3 Obesity in the US.

The prevalence of obesity (defined as a body max index - BMI, which is the ratio of the body mass to the square of the height - larger than ) is rapidly increasing in the world James:2001 and reached epidemic proportion in the US and is now a major public health concern Mokdad:1999 ; Ogden:2006 .

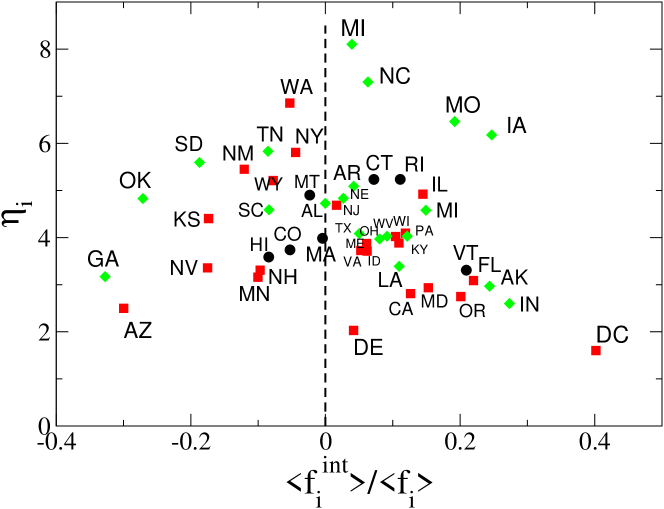

Disparities by sex and between ethnic groups have been observed in the prevalence of obesity Beydoun:2007 , but few studies focus on the effect of local factors and policies on the obesity rate. We thus apply our method to data from the CDC nccd which describe the percentage of the population which is obese for each states in the US and for the period 1995-2008. As in the crime rate case, we can compare the variances for the internal and external contributions (see SI5) and we observe that the external contribution is dominating since the year . This result means that the global trend is the major cause of the evolution of obesity in different states. We can get more detailed information about the specific behavior of the states by studying the ratio defined in Eq. (26) and the ratio of the fraction of the time average local contribution to the total signal . We represent these two quantities in a plane (see figure ) and we first note that for all states which means that fluctuations are mainly governed by the global trend.

|

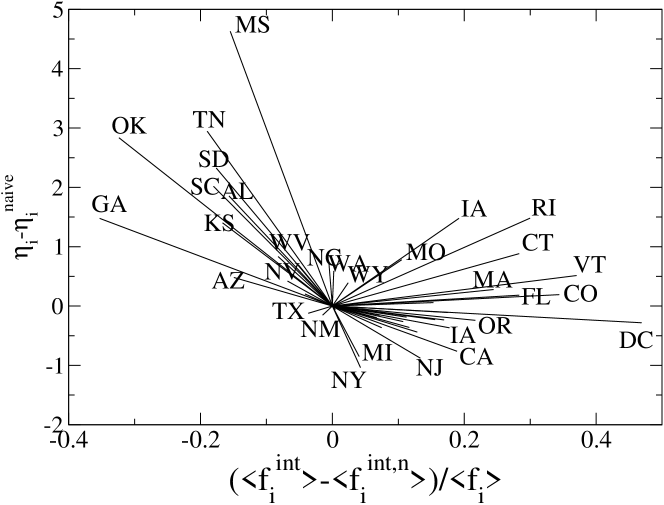

We can also divide the states into two groups (with and ). For large and positive , the states have a small which means that these states are the less susceptible to the global trend, while in the opposite case, the states are governed by the global trend. Within each group we can then distinguish the states according to their level of fluctuations ( close to or much larger than one). The states Arizona, Georgia, and Oklahoma for example have very little local contribution and their variations is dominated by the global trend. In this respect, states such as DC, Indiana are very different from the first group. More generally, we can see on this figure that states with large prevalence display very different values of . This result points toward the fact that describing states by their prevalence only can be very misleading and can hide important dynamical behaviors. Finally, we also computed the quantities and using the ‘naive’ local contribution using the national average defined in Eq. (2) by . We represent in figure the difference as vectors of components given by and we can see on this figure that for roughly half of the states the naive calculation of the local contribution can be very misleading.

|

IV Discussion.

In this article we adressed the crucial problem of extracting the local components of a system governed by a global trend. In this case, comparing the local signal to the average is very misleading and can lead to wrong conclusions. We applied this method to the example of crime rates series in the US and France and our analysis revealed surprising facts. The important result is about the importance of fluctuations which after the ’s in the US are governed by external factors. This result suggest that understanding the evolution of crime rates relies mostly on the identification of global socio-economical behavior and not on local effects such as state policies etc. In particular, this result could also help in understanding the decreasing trend observed in the US and which so far remains a puzzle Zimring:2007 ; Levitt . In the case of obesity, we show that since the year , external factors dominate, and maybe more importantly that states with the same level of prevalence have very different dynamical behaviors, thus calling for the need of a detailled study state by state.

However one may expect an even better signal analysis by assuming that there are several independent external trends: it will be interesting to see if our approach, combined with the more standard ICA techniques, can be generalized to the case of several global trends (a small number of ’sources’). The recent availability of large amounts of data in social systems call for the need of tools able to analyze them and to extract meaningful information and we hope that our present contribution will help in the understanding of these systems where the local dynamics is superimposed to collective trends.

Acknowledgements: We thank the anonymous referees for constructive remarks, in particular about the applicability conditions of our method. This work is part of the project “DyXi” supported by the French National Research Agency, the ANR (grant ANR-08-SYSC-008).

References

- (1) Huberman, B.A. (2001) The laws of the Web (MIT Press, Cambridge).

- (2) Castellano, C., Fortunato, S., Loreto, V. (2009) Statistical physics of social dynamics. Reviews of Modern Physics, 81, 591-646.

- (3) Kautz, H., Schreiber, T. (1997) Nonlinear time series analysis (Cambridge University Press, Cambridge).

- (4) Peng. C.K. et al. (1994) Mosaic organization of DNA nucleotides Physical Review E 49:1685-1689.

- (5) Comon P. (1994) Independent Component Analysis: a new concept? Signal Processing, 36(3):287–314; Cardoso, J.-F. (1997) Statistical principles of source separation, Proc. of SYSID’97 (11th IFAC symposium on system identification, Fukuoka, Japan) pp. 1837-1844; Hyvärinen A., J. Karhunen J. and Oja E. (2001) Independent Component Analysis, New York: Wiley.

- (6) de Menezes, M.A., Barabasi, A.-L. (2004) Fluctuations in network dynamics. Phys. Rev. Lett. 92:028701.

- (7) de Menezes, M.A., Barabasi, A.-L. (2004) Separating internal and external dynamics of complex systems. Phys. Rev. Lett. 93:068701.

- (8) James, P.T., Leach, R., Kalamara, E., Shayeghi, M. (2001) The Worldwide Obesity Epidemic. Obesity Research, 9:228S-233S.

- (9) A.H. Mokdad et al. (1999) The spread of obesity epidemic in the United States, 1991-1998. Journal of the American Medical Association 282: 1519-1522.

- (10) Ogden, C.L., et al. (2006) Prevalence of Overweight and Obesity in the United States, 1999-2004. Journal of the American Medical Association, 295:1549-1555. Hedley, A.A., et al. (2004) Prevalence of Overweight and Obesity Among US Children, Adolescents, and Adults, 1999-2002. Journal of the American Medical Association, 291:2847-2850.

- (11) Wang, Y., Beydoun, M.A. (2007) The Obesity Epidemic in the United States—Gender, Age, Socioeconomic, Racial/Ethnic, and Geographic Characteristics: A Systematic Review and Meta-Regression Analysis. Epidemiol Rev, 29:6–28.

- (12) Center for Disease Control and Prevention http://apps.nccd.cdc.gov/brfss/.

- (13) de Maillard J. and Roché S. (2004) Crime and Justice in France: Time Trends, Policies and Political Debate European Journal of Criminology 1:111-151

- (14) Zimring, F. (2007) The Great American Crime Decline (Oxford University Press, Oxford).

- (15) United States: Uniform Crime Report – State Statistics from http://www.disastercenter.com/crime/

- (16) France: Institut National des Hautes Etudes de Sécurité (http://www.inhes.interieur.gouv.fr/Bulletin-annuel-112.html); La Documentation française: Criminalité et délinquance constatées en France - Tome I : données générales, nationales, régionales et départementales (http://www.ladocumentationfrancaise.fr/rapports-publics/084000201/)

- (17) Levitt, S.D. (2004) Understanding Why Crime Fell in the 1990s: Four Factors that Explain the Decline and Six that Do Not. Journal of Economic Perspectives 18:163-190.

V Supporting information 1. Determining the ’s by using eigenvectors of the correlation matrix

The data correlation matrix is known to provide useful information, in particular for the analysis of financial time series or in other fields, e.g. in protein structure analysis . The first, largest, eigenvalue is related to a global trend, and usually one is interested in the small number of intermediate eigenvalues: the associated eigenvectors give the relevant correlations in the data – e.g. allows to extract the sectors in financial time series. Here, making explicit use of our hypotheses, we extract from the first eigenvector of the correlation matrix the factors which give how the global trend is amplified or reduced at the local level.

We have

| (27) |

where . If is a normalized eigenvector () of with eigenvalue : , we have

| (28) |

We can have which implies that is also eigenvector for which in general is unlikely (there are no reasons that eigenvectors of are orthogonal to ). If we then obtain

| (29) |

and

| (30) |

For the largest eigenvalue, we will neglect at first order the second term of the rhs of this last equation, which leads to . Since is normalized, we obtain

| (31) |

This approximation is justified if is small compared to and thus

| (32) |

Since , this approximation is justified if is of order and not of order . This is correct if is diagonal (which means that the external components are not correlated ), but also if the number of non-zero terms of is finite compared to , or in other words if is a sparse matrix.

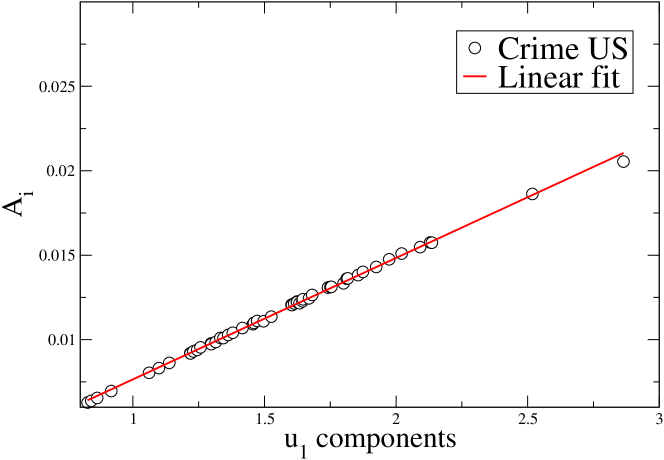

We compared the values of computed with the method exposed in the text and with the eigenvector method. Results are reported in the figures (9,10,11).

|

|

|

We see that indeed for the crime rates in the US and in France, is indeed negligible which demonstrate that the correlations of the internal contributions between different states in the US are negligible. This is not the case for the stocks in the where we can observe (small) discrepancies between the two methods, a result which supports the idea of sectors in the .

VI Supporting information 2: Scaling

We show that the scaling observed by de Menezes and Barabasi in is actually built in the method proposed by these authors: it is a direct consequence of their definitions of the internal and external parts, and it does not depend on the data structure.

Indeed, let be an arbitrary data set such that . For , following define by

| (33) |

and by

| (34) |

Then, from these definitions and without any hypothesis or constraint on the data other than , one has

| (35) |

and

| (36) |

Hence

| (37) |

with

| (38) |

Hence, one has always

| (39) |

The dispersion of the external component, if defined from (33) and (34), is thus exactly proportionnal to the mean value of the local data.

VII Supporting information 3. Synthetic series: correlated random walkers

We considered the case where the external trend is

| (40) |

The gaussian noises are given by

| (41) |

where the and are independent, uniform random variable of zero mean and variance equal to . In this case, the correlation between different noises are governed by the parameters and

| (42) |

When , the variables and are independent (for ) and we can monitor the correlations by increasing the value of . We plot in figure , random walkers in the usual uncorrelated case and in presence of correlations.

|

|

In this simple case the exact result is given by , , and . The important condition for the validity of the method is given by and is given here by

| (43) |

For , the random noises are independent and our method is very accurate as shown in the main text.

More generally, in order to assess quantitatively the efficiency of the method, we compute the Pearson correlation coefficient between the exact and the estimate computed with the method. We plot in figure this coefficient versus .

|

This figure confirms the fact that our method is valid and very precise provided that the correlations between local contributions are not too large (here ).

VIII Supporting information 4. Dependence of the on the time interval

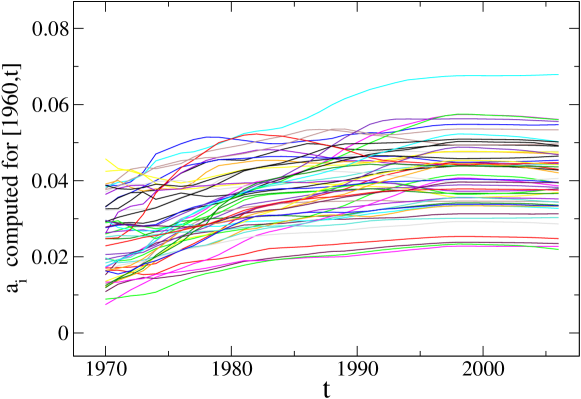

We can compute the quantities for the interval and by letting vary. We then obtain for the crime in the US (in the case of the crime rates in France, the dataset is not large enough) the figure (A).

|

|

This figure shows that in the case of the crime rate in the US, the converge to a stationary value, independent of the time interval, provided it is large enough. Our method will then lead to reliable results constant in time.

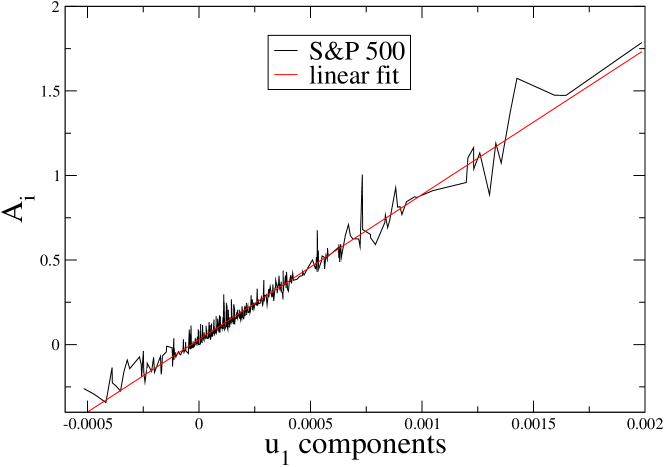

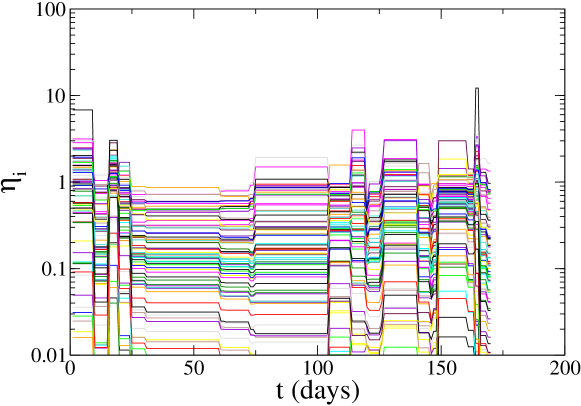

We also tested our method on the financial time series given by the 500 most important stocks in the US economy [1], and which composition leads to the index. Here the ‘local’ units are the individual stocks (), and the (naive) average - analogue to a national average - is precisely the index time serie. We study the time series for these stocks on the days of the period and we compute the global pattern , the coefficients , and the parameters (defined in the text) computed for the time window for varying from to . These quantities measure quantitatively the importance of local versus external fluctuations for the stock . The results for the ’s are shown in figure (B) and display large variations, particularly when we approach October, 2008, a period of financial crisis. It is therefore not completely surprising that the (and the ’s) in this case fluctuate a lot. In some sense, we can conclude that the ’s correspond to an average susceptibility to the global trend, are not invariable quantities and can vary for different periods. We thus see on this example, that it is important to check the stability of the coefficients which is an crucial assumption in our method. The variations of these coefficients is however interesting and further studies are needed in order to understand these variations.

[1] Historical Data for stocks http://biz.swcp.com/stocks/

IX Supporting information 5. Obesity in the US: variances for the external and internal contribution

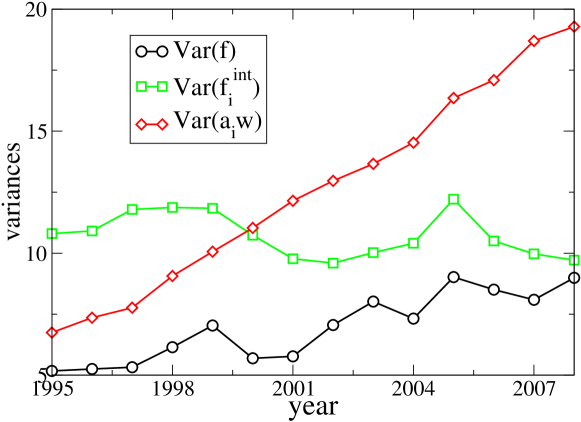

For the obesity rate series, we compare the variances of the internal () and the external () contributions. We observe on the figure that the variance of the external contribution became dominant after the year .

|