* Faculty of Informatics, University of Debrecen,

Pf. 12, H–4010 Debrecen, Hungary.

Bolyai Institute, University of Szeged, Aradi vértanúk tere 1,

H–6720 Szeged, Hungary.

e–mails: barczy.matyas@inf.unideb.hu (M. Barczy),

ispany.marton@inf.unideb.hu (M. Ispány),

papgy@math.u-szeged.hu (G. Pap).

Corresponding author.

††2000 Mathematics Subject Classifications:

60J80, 60F99.††Key words and phrases:

unstable INAR() processes, squared Bessel processes, Boston armed robberies data set

Abstract

In this paper the asymptotic behavior of an unstable integer-valued

autoregressive model of order (INAR()) is described.

Under a natural assumption it is proved that the sequence of appropriately

scaled random step functions formed from an unstable INAR() process converges

weakly towards a squared Bessel process.

We note that this limit behavior is quite different from that of familiar unstable autoregressive

processes of order .

An application for Boston armed robberies data set is presented.

1 Introduction

Recently, there has been remarkable interest in integer-valued

time series models and a number of results are now available

in specialized monographs (e.g., MacDonald and Zucchini [47],

Cameron and Trivedi [12], and Steutel and van Harn [64])

and review papers (e.g., McKenzie [51],

Jung and Tremayne [37], and Weiß [68]).

Reasons to introduce discrete data models come from the need to account for

the discrete nature of certain data sets, often counts of events, objects or

individuals.

Examples of applications can be found in the analysis of time series of count

data on the area of financial mathematics by analyzing stock transactions

(Quoreshi [57]), insurance by modeling claim counts (Gouriéroux

and Jasiak [26]), medicine by investigating disease incidence (Cardinal

et al. [13]), neurobiology by change-point analysis of neuron

spike train data (Bélisle et al. [4]), optimal alarm systems

(Monteiro et al. [52]), psychometrics by treating longitudinal

count data (Böckenholt [7], [8]), environmetrics by analyzing rainfall

measurements (Thyregod et al. [65]), experimental biology (Zhou and

Basawa [69]), and queueing systems (Ahn et al. [1]

and Pickands III and Stine [56]).

Among the most successful integer-valued time series models proposed in the

literature we mention the INteger-valued AutoRegressive model of order

(INAR()). This model was first introduced by McKenzie [50]

and Al-Osh and Alzaid [2] for the case .

The INAR(1) model has been investigated by several authors.

Franke and Seligmann [22] analyzed maximum likelihood estimation

of parameters under Poisson innovation. Du and Li [19] and

Freeland and McCabe [24] derived the limit-distribution of the

conditional least squares estimator of the autoregressive parameter. Silva and Oliveira [60]

proposed a frequency domain based estimator, Brännäs and Hellström

[9] investigated generalized method of moment estimation, Silva and Silva [62] considered

a Yule-Walker estimator. Jung et al. [36] analyzed the finite sample

behavior of several estimators by a Monte Carlo study. Ispány et al.

[31], [32] derived asymptotic inference for nearly

unstable INAR(1) models which has been refined by Drost et al. [17]

later. A Poisson limit theorem has been proved for an inhomogeneous nearly

critical INAR(1) model by Györfi et al. [27].

The more general INAR() processes were first introduced by Al-Osh and Alzaid

[3].

In their setup the autocorrelation structure of the process corresponds to that of

an ARMA() process, see also Section 2.

Another definition of an INAR(p) process was proposed independently

by Du and Li [19] and by Gauthier and Latour [25] and Latour [44],

and is different from that of Alzaid and Al-Osh [3].

In Du and Li’s setup the autocorrelation structure

of an INAR() process is the same as that of an AR() process. The setup of Du and Li

[19] has been followed by most of the authors, and our approach will also be

the same, see Section 2.

The INAR() model has been investigated by several authors from different points of views.

Drost et al. [16] provided asymptotically efficient

estimator for the parameters.

Silva and Oliveira [61] described the higher order moments and cumulants

of INAR() processes, and Silva and Silva [62] derived asymptotic distribution of

the Yule-Walker estimator.

Drost et al. [18] considered semiparametric INAR() models and proposed efficient

estimation for the autoregression parameters and innovation distributions.

Recently, the so called -order Rounded INteger-valued AutoRegressive (RINAR()) time series model

was introduced and studied by Kachour and Yao [39] and Kachour [38].

The broad scope of the empirical literature in which INAR models are applied indicates its relevance.

Examples of such applications include Franke and Seligmann [22] (epileptic seizure counts),

Böckenholt [8] (longitudional count data), Thyregod et al. [65] (rainfall measurements),

Brännäs and Hellström [9] and Rudholm [59] (economics),

Brännäs and Shahiduzzaman [10] (finance), Gourieroux and Jasiak [26] (insurance),

Pavlopoulos and Karlis [54] (environmental studies)

and McCabe et al. [49] (finance and mortality).

An interesting problem, which has not yet been addressed for INAR()

models, is to investigate the asymptotic behavior of unstable INAR()

processes, i.e., when the characteristic polynomial has a unit root.

In this paper we give a complete description of this limit behavior.

In particular, it will turn out that an INAR() model is unstable if

and only if the sum of its autoregressive parameters equals 1, and in

this case the only unit root of the characteristic polynomial is 1 with

multiplicity one.

For the sake of convenience, we suppose that the process starts from zero.

Without loss of generality, we may suppose that the th autoregressive parameter is strictly positive and

that the greatest common divisor of the strictly positive autoregressive parameters is 1,

see Remark 2.2.

Under the assumption that the second moment of the innovation distribution is finite, we prove that

the sequence of appropriately scaled random step functions formed from

an unstable INAR() process converges weakly towards a squared Bessel process.

This limit process is a continuous branching process also known as square-root process or

Cox-Ingersoll-Ross process.

We remark that a similar theorem holds for critical, i.e., when the offspring mean is equal

to 1, branching processes with immigration, see Wei and Winnicki [66, Theorem 2.1].

We should also note that the asymptotic behavior of unstable INAR() models

is completely different from that of familiar (real-valued) unstable AR() models in at least

two senses.

On the one hand, the characteristic polynomial of a primitive (see Definition 2.2)

unstable INAR() model has only one unit root, namely 1, with multiplicity one,

whereas for an unstable AR() model it may have real or complex unit roots with various different multiplicities.

On the other hand, in the case of a primitive unstable INAR() model there is a limit process which is a squared

Bessel process, while in the case of an unstable AR() model in general there is no limit process,

only for appropriately transformed and scaled random step functions, see

Chan and Wei [14], Jeganathan [35] and van der Meer et al. [48, Theorem 3].

We remark that our result can be considered as the first step towards the comprehensive theory of

nonstationary integer-valued time series and investigation of the unit root problem of

econometrics in the integer-valued setup.

Nonstationary time series have been playing an important role in both econometric

theory and applications over the last 20 years, and a substantial literature

has been developed in this field. A detailed set of references is given in Phillips

and Xiao [55].

We note that Ling and Li [45], [46] considered an unstable ARMA model

with GARCH errors and an unstable fractionally integrated ARMA model.

Concerning relevance and practical applications of unstable INAR models we note that

empirical studies show importance of these kind of models.

Brännäs and Hellström [9] reported an INAR model with a coefficient

for the number of private schools, Rudholm [59] considered INAR models

with coefficients and , respectively for the number of Swedish

generic-pharmaceutical market.

Hellström [29] focused on the testing of unit root in INAR(1) models and provided

small sample distributions for the Dickey-Fuller test statistic under the null hypothesis

of unit root in an INAR(1) model with Poisson distributed innovations.

In this paper, we report that a subset INAR model is an adequate model for

Boston armed robberies data set published in Deutsch and Alt [15].

Our proposed model can be considered unstable since

the sum of the estimated (autoregressive) coefficients is 1.0317.

To our knowledge a unit root test for general INAR models is not known, and from

this point of view studying unstable INAR models is an important preliminary task.

The rest of the paper is organized as follows.

Section 2 provides a background description of

basic theoretical results related with INAR() models.

In Section 3 we describe the asymptotic behavior of unstable INAR() processes.

Under the assumption that the second moment of the innovation distribution is finite,

we prove that the sequence of appropriately scaled random step functions formed

from an unstable INAR() process converges weakly towards a squared Bessel process,

see Theorem 3.1.

Section 4 presents a real-life application of unstable

INAR models by investigating the Boston armed robberies time series.

Section 5 contains a proof of our main Theorem 3.1.

For the proof, we collect some properties of the first and second moments of

(not necessarily unstable) INAR() processes, we recall a useful functional martingale

limit theorem and an appropriate version of the continuous mapping theorem,

see Lemma 6.1, Corollary 6.1, Theorem 6.1

and Lemma 6.2 in Appendix, respectively.

2 The INAR() model

Let , , , and denote the set of non-negative integers,

positive integers, real numbers, non-negative real numbers and complex numbers, respectively.

For all , let us denote by the identity matrix.

Every random variable will be defined on a fixed probability space

.

One way to obtain models for integer-valued data is to replace multiplication

in the conventional ARMA models in such a way to ensure the integer

discreteness of the process and to adopt the terms of self-decomposability and

stability for integer-valued time series.

2.1 Definition.

Let be an independent and identically distributed

(i.i.d.) sequence of non-negative integer-valued random variables, and let

.

An INAR() time series model with coefficients

and innovations is a stochastic process

given by

(2.1)

where for all and ,

is a sequence of i.i.d. Bernoulli random variables with mean

such that these sequences are mutually independent and independent of the

sequence , and

, , …, are non-negative integer-valued random

variables independent of the sequences , ,

, and .

The INAR() model (2.1) can be written in another way using

the binomial thinning operator

(due to Steutel and van Harn [63]) which we recall now.

Let be a non-negative integer-valued random variable.

Let be a sequence of i.i.d. Bernoulli random variables

with mean .

We assume that the sequence is independent of .

The non-negative integer-valued random variable

is defined by

The sequence is called a counting sequence.

The INAR() model (2.1) takes the form

Note that the above form of the INAR() model is quite analogous with a usual AR()

process (another slight link between them is the similarity of some

conditional expectations, see (2.3)).

As we noted in the introduction, this definition of the INAR(p) process

was proposed independently by Du and Li [19] and by Gauthier and Latour [25]

and Latour [44],

and is different from that of Alzaid and Al-Osh [3], which assumes that the

conditional distribution of the vector

given

is multinomial with parameters and

is independent of the past history of the process.

The two different formulations imply different second-order structure for the processes:

under the first approach, the INAR() has the same second-order structure as an AR()

process, whereas under the second one, it has the same one as an ARMA

process.

An alternative representation of the INAR() process as a p-dimensional INAR(1)

process was obtained by Franke and Subba Rao [23] and see also Latour [43, formula (2.3)].

Accordingly, the INAR() process defined in (2.1) can be written as

where the -dimensional random vectors , and the -matrix

are defined by

(2.2)

and for a -dimensional random vector and

for a matrix

with entries satisfying , , the matricial binomial thinning operation

is defined as a -dimensional random vector whose -th component,

, is given by

where the counting sequences of all , , are assumed to be independent

of each other.

In what follows for the sake of simplicity we consider a zero start INAR() process,

that is we suppose .

The general case of nonzero initial values may be handled in a similar way, but we renounce

to consider it.

For nonzero initial values the first and second order moments of the sequence

have a more complicated form than in Lemma 6.1.

Further, for proving a corresponding version of our main result (see Theorem 3.1)

one needs to apply a more general version of Theorem 6.1 which is also valid

for random step functions not necessarily starting from .

In the sequel, we always assume that .

Let us denote the mean and variance of by and

, respectively.

For all , let us denote by the -algebra generated

by the random variables . (Note that , since .)

By (2.1),

(2.3)

Consequently,

This can also be written in the form

, , where

Consequently, we have

which implies

(2.4)

Hence the matrix plays a crucial role in the description of asymptotic behavior

of the sequence .

Let denote the spectral radius of , i.e.,

the maximum of the modulus of the eigenvalues of .

In what follows we collect some known facts about the matrix .

First we recall the notions of irreducibility and primitivity of a matrix.

A matrix is called reducible if and

, or if and there exist a permutation matrix

and an integer with

such that

where , ,

, and

is a null matrix.

A matrix is called irreducible if it is not

reducible, see, e.g., Horn and Johnson [30, Definitions 6.2.21 and 6.2.22].

A matrix is called primitive if it is irreducible

and has only one eigenvalue of maximum modulus, see, e.g., Horn and Johnson [30, Definition 8.5.0].

By Horn and Johnson [30, Theorem 8.5.2], a matrix is primitive

if and only if there exists a positive integer such that all the entries of

the matrix are positive.

Let us denote by the characteristic polynomial of the matrix , i.e.,

2.1 Proposition.

For , , let us consider the matrix defined

in (2.2).

Then the following assertions hold:

(i)

The characteristic polynomial has just one positive root,

, the nonnegative matrix is irreducible,

is an eigenvalue of and

(2.5)

(2.6)

Further,

(2.7)

(ii)

If the greatest common divisor of the set

is equal to one, then is primitive,

is an eigenvalue of , the algebraic and geometric multiplicity of

equal 1 and the absolute value of the other eigenvalues of are

less than .

Corresponding to the eigenvalue there exists a unique vector

with positive coordinates such that

and the sum of the coordinates of is 1,

namely, takes the form

Further,

(2.8)

where is a unique vector with positive coordinates

such that and

, namely takes the form

with

for .

Moreover, there exist positive numbers and with

such that for all

(2.9)

where denotes the operator norm of a matrix

defined by

.

Proof.

(i): First we check that has just one positive root, which readily yields that

.

The function

is strictly decreasing and continuous on with

and

,

thus it takes the value 1 at exactly one positive point, which is the only

positive root of .

Now we turn to check that is irreducible.

By Brualdi and Cvetković [11, Definition 8.1.1 and Theorem 1.2.3], a nonnegative matrix

is irreducible provided

that its digraph (directed graph) (having vertices

labeled by the numbers and an edge from vertex to vertex provided )

is strongly connected (that is, for each pair and

of distinct vertices, there is a path from to and a

path from to ).

Now implies that contains a cycle

, hence is strongly

connected.

Using that is nonnegative and irreducible, by Horn and Johnson [30, Theorem 8.4.4],

we have is an eigenvalue of and hence

(ii):

By Brualdi and Cvetković [11, Definition 8.2.1 and Theorem 8.2.7], an irreducible

nonnegative matrix is primitive provided that the index of

imprimitivity of (the greatest common divisor of the lengths of

the cycles of its digraph ) equals .

Now the cycles of are

for all such that (not considering rotations).

Since such a cycle has length , we get the index of imprimitivity of

is , which yields that is primitive.

The other assertions of (ii) except the uniqueness of and

follows by the Frobenius-Perron theorem, see, e.g., Horn and Johnson [30, Theorems 8.2.11 and 8.5.1].

The uniqueness of follows by Horn and Johnson [30, Corollary 8.2.6] using that

for all .

The uniqueness of can be checked as follows.

Using that the irreducibility and primitivity of yields the irreducibility and primitivity

of (see, e.g., page 507 in Horn and Johnson [30]),

by Horn and Johnson [30, Theorems 8.2.11, 8.5.1 and Corollary 8.2.6] we get

is an eigenvalue of , the algebraic and

geometric multiplicity of equal 1, corresponding to the eigenvalue

there exists a unique vector with positive

coordinates such that and the sum of

the coordinates of is 1.

Further, by Horn and Johnson [30, page 501, Problem 1], we also have .

Using that the geometric multiplicity of equals 1,

we get is a unique vector

with positive coordinates such that and

.

The forms of and can be checked as follows.

Using that they are unique it remains to verify that the imposed conditions are satisfied

by the given forms.

We easily have has positive coordinates of which the sum is 1.

Further, with the notation ,

we get

where the last but one equality follows by (2.5).

Similarly, for , we get

Moreover, we easily have has positive coordinates and

where the last equality follows by (2.6).

With the notation

, we get

for all ,

Finally, using that , we get

2.1 Remark.

If , and , then the unique vectors

and defined in (ii) of Proposition 2.1

take the forms

with

and

2.2 Definition.

An INAR() process with coefficients

is called primitive if

(i)

,

(ii)

, where is the greatest common divisor of the set

.

2.2 Remark.

If and there exists such that ,

then is an INAR() process with coefficients

with , where

.

If , but , then the process takes the form

and hence the subsequences , , form independent

primitive INAR() processes with coefficients such that

.

Note also that in this case not all of the coefficients

are necessarily positive.

Finally, we remark that an INAR() process is primitive if and only if

its matrix defined in (2.2) is primitive.

Indeed, if is primitive, then part (ii) of Proposition 2.1

readily yields that is primitive.

Conversely (using the notations of the proof of Proposition 2.1), if is primitive,

then, by the proof of part (i) of Proposition 2.1, the digraph is strongly

connected.

This yields that , since otherwise there would be no path from to .

Further, the primitivity of yields that the index of imprimitivity of equals .

Using that the cycles of are

for all such that (not considering rotations)

and such a cycle has length , we get .

The next proposition is about the limit behavior of as .

This proposition can also be considered as a motivation for the classification of

INAR() processes, see later on.

2.2 Proposition.

Let be an INAR() process such that

and .

Then the following assertions hold:

(i)

If , then

(ii)

If , then

where is the characteristic polynomial of the matrix defined in

(2.2).

(iii)

If , then

for all , where is the greatest common divisor of the set

.

Proof.

If , then and , ,

which yields that , i.e., part (i) is satisfied

in the case of .

If not all of the coefficients are 0, then, by Remark 2.2,

is an INAR() process where

.

Hence in what follows we may and do suppose that the original process

is such that .

First we prove the proposition in the case of and , i.e.,

in the case of is primitive.

Proof of (i) in the case of and :

In this case we verify that

By (2.4), it is enough to prove that

if , then the series is convergent

and its sum is .

By (2.9), we have

since and .

One can give another proof for the convergence of .

Indeed, by Horn and Johnson [30, Corollary 5.6.14], we have

and hence

comparison test yields the assertion.

Finally, by Lemma 5.6.10 and Corollary 5.6.16 in Horn and Johnson [30],

we have , and hence,

by Cramer’s rule,

Proof of (ii) in the case of and :

In this case we verify that

Using also (2.6) and (2.10), this concludes (iii) in the case

of and .

Now we turn to give a proof in the case of and .

In this case, by Proposition 2.1, is irreducible, and,

by Remark 2.2, the subsequences , , form

independent primitive INAR() processes with coefficients

such that .

Let us introduce the matrix

and its characteristic polynomial

Since the greatest common divisor of the set

is 1, by Proposition 2.1,

we have is primitive.

We check that .

Since , , we get

.

By Proposition 2.1, and is an eigenvalue

of .

Hence is an eigenvalue of , which implies that

or equivalently .

If , then and using that part (i) has already been proved for

primitive matrices (i.e., in the case of and ) we have for all

,

This yields that exists with the given limit in (i).

If , then and using that part (ii) has already been proved for

primitive matrices we have for all ,

This yields that exists with given limit in (ii).

If , then and using that part (iii) has already been proved for

primitive matrices we have for all ,

Based on the asymptotic behavior of as described in Proposition 2.2,

we distinguish three cases.

The case is called stable or

asymptotically stationary,

whereas the cases and are called

unstable and explosive, respectively.

Note also that, if , then, by (2.7) of Proposition 2.1,

, and are equivalent

with , and

, respectively.

3 Convergence of unstable INAR() processes

A function is called càdlàg if it is right

continuous with left limits.

Let and denote the space of all

real-valued càdlàg and continuous functions on , respectively.

Let denote the Borel -field in

for the metric defined in (16.4) in Billingsley [5]

(with this metric is a complete and separable metric space).

For stochastic processes and ,

, with càdlàg paths we write if the

distribution of on the space converges weakly to

the distribution of on the space as .

For each , consider the random step processes

where denotes the integer part of a real number .

The positive part of will be denoted by .

3.1 Theorem.

Let be a primitive INAR() process with coefficients

such that

(hence it is unstable).

Suppose that and .

Then

(3.1)

where is the unique strong solution of the stochastic differential

equation (SDE)

(3.2)

with initial value , where

and is a standard Wiener process.

(Here is the characteristic polynomial of the matrix defined in

(2.2).)

3.1 Remark.

Note that under the conditions Theorem 3.1, if , then ,

and if , then .

Indeed, if , then , since otherwise

and hence the greatest common divisor of would be , which is a contradiction.

Since, by our assumption , we get . If , then , and hence .

Remark also that in the case of we have and hence

, , , and then

the limit process in Theorem 3.1

is deterministic, namely , .

To describe the asymptotic behavior of an unstable INAR process one has to go one step further and

one has to investigate the fluctuation limit.

By Donsker’s theorem (see, e.g., Billingsley [5, Theorem 8.2]), we have

as , where is

a standard Wiener process.

For completeness, we remark that Ispány, Pap and Zuijlen [31, Proposition 4.1]

describes the fluctuation limit behavior of nearly unstable INAR() processes.

3.2 Remark.

The SDE (3.2) has a unique strong solution for all

initial values .

Indeed, since , ,

the coefficient functions

and

satisfy

conditions of part (ii) of Theorem 3.5 in Chapter IX in Revuz and Yor [58]

or the conditions of Proposition 5.2.13 in Karatzas and Shreve [41].

Further, by the comparison theorem (see, e.g., Revuz and Yor [58, Theorem 3.7, Chapter IX]),

if the initial value is nonnegative, then is nonnegative

for all with probability one.

Hence may be replaced by under the square root in (3.2).

The unique strong solution of the SDE (3.2) is known as a squared Bessel process,

a squared-root process or a Cox-Ingersoll-Ross (CIR) process.

3.3 Remark.

If the matrix is not primitive but unstable, then we can suppose that

, since otherwise it is an unstable INAR() process with

(note that there exists

an such that because of the unstability of ).

If and , then, by Remark 2.2, the subsequences

, , form independent primitive unstable INAR()

processes with coefficients such that

.

Hence one can use Theorem 3.1 for these subsequences.

With the notations

by Theorem 3.1, as , where

is the unique strong solution of the SDE

with initial value and , ,

are independent standard Wiener processes.

We note that if and , then

does not converge in general as .

By giving a counterexample, we show that even the 2-dimensional distributions do not converge in general.

Let , , .

Then and using that as , ,

we have

(3.3)

as , and

(3.4)

as , where is the unique strong solution of the SDE

and that the subsequences and are

independent, by (3.3) and (3.4), we get

Since the random variables

do not have the same distributions (the coordinates of the first one are dependent,

however the coordinates of the second one are independent), we get (3.5).

For proving Theorem 3.1, let us introduce the sequence

(3.6)

of martingale differences with respect to the filtration

, and the random step processes

First we will verify convergence

(3.7)

where is the unique strong solution of the SDE

(3.8)

with initial value .

The proof of (3.7) can be found in Section 5.

3.4 Remark.

If is a strong solution of (3.2) with initial value

, then, by Itô’s formula, ,

, is a strong solution of (3.8) with initial value . On the other hand, if is a strong solution of

(3.8) with initial value , then, again by Itô’s formula,

(3.9)

is a strong solution of (3.2) with initial value .

Hence, by Remark 3.2, the SDE (3.8) has a unique strong solution

for all initial values .

Further, if the initial value is nonnegative, then

is nonnegative for all with probability one.

Hence may be replaced by

under the square root in (3.8).

which can be written in the form

, .

Consequently,

implying

(3.11)

In Section 5, we show that the statement (3.1) will follow

from (3.7) and (3.11) using a version of the continuous mapping theorem

(see Appendix).

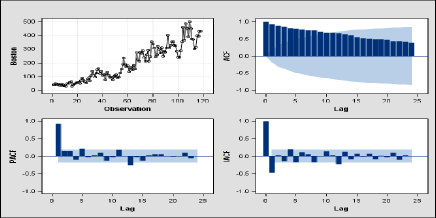

4 Application to Boston armed robberies data set

This data set consists of 118 counts of monthly armed robberies in Boston from

January 1966 to October 1975 (Fig. 1). The data were originally

published in Deutsch and Alt [15], see also the time series 6.10 in O’Donovan

[53, Appendix A.3].

It can also be obtained from the Time Series Data Library:

http://robjhyndman.com/tsdldata/data/mccleary5.dat.

Deutsch and Alt [15] used this time series to illustrate the method of intervention analysis

developed by Box and Tiao [6].

They assessed the impact of a 1975 Massachusetts gun control law on armed robbery in Boston.

The correlation analysis for this series, shown in Fig. 1, and preliminary ARIMA model

fitting clearly indicate unstability.

Figure 1: Boston armed robberies, time series (top left),

autocorrelation function (top right), partial autocorrelation function

(bottom left), inverse autocorrelation function (bottom right).

For preliminary fitting, subset ARIMA (Model 1) and ARIMA (Model 2) models are applied. Here and in the sequel,

ARIMA denotes a seasonal ARIMA model with period

and orders , where capital letters

denote the seasonal orders. We use the following approach to characterize

the unstability of an ARIMA model. Let and be the

autoregressive and seasonal autoregressive polynomial of the model, respectively,

where denotes the backshift operator. We suppose that these

polynomials are stable, i.e., the roots are all lie outside the complex unit circle.

Define the coefficients , ,

by . Then, we characterize the unstability of the model by the sum

. Clearly, if an ARIMA model is unstable

(nonstationary), i.e., or , and hence its characteristic

polynomial has unit root 1, then .

Since Model 1 is unstable and Model 2 is nearly unstable, see Table 1, Deutsch and Alt

[15] suggested first order differencing and seasonal differencing getting an

ARIMA model (Model 3).

Model

Fitted model

Standard error

1

1

39.55

2

0.9841

40.39

3

1

38.66

4

1

0.1954

5

1.0189

526.8

6

1.0317

26.18

Table 1: Fitted models for Boston armed robberies data set with and

standard error.

In contrast, Hay and McCleary

[28] claimed that Deutsch and Alt had misspecified the stochastic component for

this time series and they proposed only first order differencing getting an

ARIMA model (Model 4) after logarithmic transformation

of the time series. Hay and McCleary reported that this alternative model

has better statistical properties and there is no intervention into the

time series (i.e., the parameters of the model do not vary in time),

thus there is inconclusive evidence for the effect claimed by Deutsch and Alt.

They argued for the need of logarithmic transformation to eliminate the “variance”

nonstationarity of the time series.

The following was reported by Hay and McCleary [28]:

“We conducted several analyses to obtain supporting evidence for our hypothesis of

variance nonstationarity. First, we divided the series into equal length segments

and calculated the mean and standard deviation for each segment. Both statistics

showed a nearly monotonic increase over time and were highly intercorrelated. Two

tests of homogeneity of variance (Cochran’s C and the Bartlett and Box’s F) also

indicated that the segment variances were not homogeneous.”

Based on the foregoing it is evident that the Boston armed robberies data set

possesses the following properties: it is integer–valued, heteroscedastic,

and unstable. Our aim here is to fit an appropriate INAR(p) model for this data set

using the method of conditional least squares (CLS) and to compare our model with

the previously mentioned ones. The CLS estimators , ,

and of the parameters , , and of an INAR

model based on the observations are given by minimizing the residual

sum of squares in (3.10). This technique has

been suggested by Klimko and Nelson [42] for general stochastic processes,

and it has been applied for INAR models by Du and Li [19, Theorem 4.2]

proving the asymptotic normality of these estimators in the stable case.

The correlation analysis (Fig. 1) shows that there are significant

dependences between and , and, due to the seasonal effect, between

and . Thus, we fit a subset INAR model where the strictly

positive coefficients are and , and we estimate these

(autoregressive) parameters and the mean . By solving the normal equations

we have Model 5, see Table 1, where

is the centered innovation.

Similarly to ARIMA models we characterize the unstability of an INAR model

by the sum (the classification of INAR(p) models is based

on this sum, see the end of Section 2).

Then the fitted Model 5 appears to be unstable since . For the goodness–of–fit of ARIMA

and INAR models the standard error (the square root of the mean square error) is applied which is

defined by , where

, , are the estimated

residuals and denotes the number of estimated parameters. The standard error is

relatively high for Model 5 () comparing with that of Deutsch and Alt’s

model (Model 3) because the “error” terms fluctuate to much in (3.10)

if the INAR model is unstable.

(We note that the model of Hay and McCleary (Model 4) is uncomparable with the other ones

using the standard error because of the logarithmic transformation has changed the scale.)

To stabilize the fluctuation of let us introduce the weighted martingale differences

Since , the conditional variance of the “weighted error” terms would

not fluctuate too much even if is unbounded.

Moreover, we have almost surely as

and almost surely, where denotes the cardinality of the set

. Hence, the weighted error terms are

asymptotically homogeneous in the stable and the unstable cases as well.

The weighted conditional least squares

(WCLS) estimation is given by minimizing the weighted residual sum of squares

. This technique has been suggested by Wei and Winnicki

[67] for branching processes with immigration to derive a unified estimation

procedure for the offspring mean. By solving the normal equations we have Model 6 which

appears to be unstable again, see Table 1. Defining the standard error

for Model 6 as , this

subset INAR(12) model possesses the smallest standard error among the fitted models except

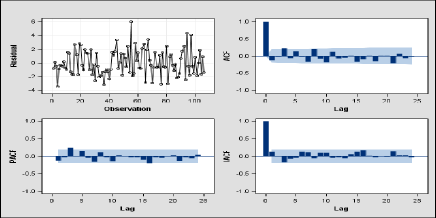

that of Hay and McCleary. The correlation analysis of estimated weighted residuals

, see Fig. 2, shows that they form a white noise time series.

Figure 2: Residual analysis of Model 6, residual series (top left),

autocorrelation function (top right), partial autocorrelation function

(bottom left), inverse autocorrelation function (bottom right).

In summary, Model 6 is an adequate model for Boston armed robberies times series

since its coefficients can be considered significant, it has minimum number of parameters

and minimal residual variance (among the fitted models), and the residuals form a white noise.

We note that the asymptotic theory of CLS and WCLS estimation of INAR models in the

unstable case has not yet been developed now, this is a task for the future.

Finally, we would like to call attention to other possible estimation methods which may also

work in the unstable case.

For example, Enciso–Mora et al. [20] proposed a reversible jump MCMC algorithm which

even works well near the borders of the stationary region and has been successfully

applied to a simulated nearly unstable INAR(3) data set having as the sum of the (autoregressive) parameters.

For the proof we will use Corollary 6.1, Theorem 6.1

and Lemma 6.2 which can be found in Appendix.

First we prove (3.7), i.e., as .

We will apply Theorem 6.1 for , , ,

and for , .

By Remark 3.4, the SDE (3.8) has

a unique strong solution for all initial values , .

Now we show that conditions (i) and (ii) of Theorem 6.1 hold.

We have to check that for each ,

Hence, for all , the randomness of the difference in (5.1)

is via a linear combination of the random variables , .

Then, in order to show (5.1), it suffices to prove

First we prove (5.4).

Using that the random variables

are independent of the

-algebra for all , we get

where is given by

with

.

Consider the decomposition

where

where the sum is taken for ,

, with .

Consider the decompositions

where

where the sum is taken for and

with .

Using that

we have

where

In order to prove (5.4), it is enough to show that

(5.7)

as .

We have

where

as for all by the dominated convergence theorem.

Thus, by Corollary 6.1, we get with some constant ,

which yields .

Independence of and

implies

Here , ,

and, by Markov’s inequality,

Thus we get

Hence, by Cauchy-Schwarz’s inequality and Corollary 6.1, we get with some constant ,

which implies .

By Cauchy-Schwarz’s inequality,

where

Using the independence of and

for , we get

with some constant .

Further, by Markov’s inequality,

with some constant .

Hence

with some constant .

Using that

with some constant , we get, in order to show

(5.7), it suffices to prove

.

In fact,

since Corollary 6.1 implies

.

Thus we finished the proof of (5.4).

Now we turn to prove (5.5).

Using that for all the random variables

are independent of the -algebra , we get ,

where is given by

Using again the independence of

,

where by Markov’s inequality,

,

and

.

Hence, in order to show (5.5), it suffices to prove

.

In fact, by Corollary 6.1, .

Now we turn to prove (5.6).

By independence of and ,

thus we obtain (5.6).

Hence we get (5.2), and we conclude, by

Theorem 6.1, convergence .

Now we start to prove (3.1).

By (3.11), , where the mapping

is given by

for , , .

Further, , where, by (3.9), the mapping

is given by

We check that the mappings , , and are measurable.

Continuity of follows from the characterization of convergence in

, see, e.g., Ethier and Kurtz

[21, Proposition 3.5.3], thus we obtain measurability of .

Indeed, if , , and the sequence

converges in to , then for all

there exist continuous, increasing mappings , , from

onto such that

Since for all

we have for all ,

In order to prove measurability of , first we localize it.

For each , consider the stopped mapping

given by

for ,

, .

Obviously, in as

for all , since for all

and we have , ,

and hence as

.

Consequently, it suffices to show measurability of for all

.

We can write , where the

mappings and

are defined by

for , ,

, .

Measurability of follows from Ethier and Kurtz

[21, Proposition 3.7.1].

Next we show continuity of by checking

as

for all whenever in

.

This convergence follows from the estimates

since

.

We obtain measurability of both and , hence

we conclude measurability of .

The aim of the following discussion is to show that

there exists with and , where is defined in Appendix.

We check that satisfies the above mentioned

conditions.

First note that , where ,

.

Using that is a measurable subset of (see, e.g., Ethier and Kurtz [21, Problem 3.11.25])

and that is measurable (see, e.g., Ethier and Kurtz [21, Proposition 3.7.1]),

we have .

Fix a function and a sequence

in with , where is defined in Appendix.

By the definition of , we get .

Further, we can write

where is the modulus of continuity of

on , and we have since is

continuous (see, e.g., Jacod and Shiryaev [34, Chapter VI, 1.6]).

In a similar way, for all ,

Thus we conclude

Since and, by the definition of a strong solution

(see, e.g., Jacod and Shiryaev [34, Definition 2.24, Chapter III]), has

almost sure continuous sample paths, we have .

Consequently, by Lemma 6.2, we obtain

as .

6 Appendix

In the proof of Theorem 3.1 we will extensively use the following facts

about the first and second order moments of the sequences

and .

6.1 Lemma.

Let be an INAR() process defined by (2.1) such that

and .

Then, for all ,

(6.1)

(6.2)

Moreover,

(6.3)

(6.4)

Further,

(6.5)

(6.6)

Proof. We have already proved (6.1), see (2.4).

The equality clearly implies (6.3)

and (6.5).

By (2.1) and (3.6),

(6.7)

For all , the random variables

are independent of each other, independent of , and have

zero mean, thus in the case we conclude (6.4) and hence

(6.6).

If , then

by (6.3), and thus we obtain (6.4) and (6.6) in the case of

.

where is defined in Theorem 3.1.

Hence we obtain .

Next we recall a result about convergence of step processes towards a diffusion process,

see Ispány and Pap [33, Corollary 2.2].

This result is used for the proof of convergence (3.7).

6.1 Theorem.

Let be a continuous function.

Assume that uniqueness in the sense of probability law holds for the SDE

(6.9)

with initial value for all , where

is a standard Wiener process.

Let be a solution of (6.9) with initial value

.

For each , let be a sequence of random

variables adapted to a filtration .

Let

Suppose and

for all .

Suppose that for each ,

(i)

,

(ii)

for all ,

where denotes convergence in probability.

Then as .

In fact, this theorem is a corollary of a more general limit theorem, see Ispány and Pap

[33, Theorem 2.1].

Now we recall a version of the continuous mapping theorem.

For a function and for a sequence

in , we write if

converges to locally uniformly, i.e., if

as for all

.

For measurable mappings and

, , we will

denote by the set of all functions

such that and

whenever with

, .

For deriving convergence (3.1) from convergence (3.7) we will need

the following version of the continuous mapping theorem.

6.2 Lemma.

Let and , , be

stochastic processes with càdlàg paths such that as .

Let and

, , be

measurable mappings such that

there exists with

and .

Then as .

Lemma 6.2 can be considered as a consequence of Theorem 3.27 in Kallenberg [40],

and we note that a proof of this lemma can also be found in Ispány

and Pap [33, Lemma 3.1].

Acknowledgements

Figures 1 and 2 were prepared with SAS Enterprise Guide 4.2.

The authors have been supported by the Hungarian Portuguese Intergovernmental S & T Cooperation

Programme for 2008–2009 under Grant No. PT–07/2007.

M. Barczy and G. Pap have been partially supported by the Hungarian Scientific Research Fund

under Grant No. OTKA T–079128.

M. Ispány has been partially supported by TÁMOP 4.2.1./B-09/1/KONV-2010-0007/IK/IT

project, which is implemented through the New Hungary Development Plan co–financed by the

European Social Fund and the European Regional Development Fund.

References

[1]S. Ahn, L. Gyemin and J. Jongwoo,

Analysis of the M/D/1-type queue based on an integer-valued

autoregressive process.

Operations Research Letters27, 235–241, (2000).

[2]M. A. Al-Osh and A. A. Alzaid,

First order integer-valued autoregressive INAR(1) process.

Journal of Time Series Analysis8(3), 261–275, (1987).

[3]M. A. Al-Osh and A. A. Alzaid,

An integer-valued th-order autoregressive structure

(INAR(p)) process. Journal of Applied Probability27(2), 314–324, (1990).

[4]P. Bélisle, L. Joseph, B. MacGibbon,

D. Wolfson and R. du Berger, Change-point

analysis of neuron spike train data. Biometrics54, 113–123, (1998).

[5]P. Billingsley,Convergence of Probability Measures, 2nd ed.

Wiley, 1999.

[6]G. E. P. Box and G. C. Tiao, Intervention analysis with applications

to economic and environmental problems.

Journal of the American Statistical Association70(349), 70–79, (1975).

[7]U. Böckenholt,

An INAR(1) negative multinomial regression model for longitudinal

count data. Psychometrika64, 53–67, (1999).

[8]U. Böckenholt,

Mixed INAR(1) Poisson regression models: analyzing heterogeneity and

serial dependencies in longitudinal count data.

Journal of Econometrics89, 317–338, (1999).

[9]K. Brännäs and J. Hellström,

Generalized integer-valued autoregression.

Econometric Reviews20, 425–443, (2001).

[10]K. Brännäs and Q. Shahiduzzaman,

Integer-valued moving average modelling of the number of transactions in stocks.

Umea Economic Studies637, University of Umeå, (2004).

[11]R. A. Brualdi and D. Cvetković,

A Combinatorial Approach to Matrix Theory and its Applications.

CRC Press, Boca Raton, FL, 2009.

[12]A. C. Cameron and P. Trivedi,

Regression Analysis of Count Data.

Cambridge University Press, Oxford, 1998.

[13]M. Cardinal, R. Roy and J. Lambert,

On the application of integer-valued time

series models for the analysis of disease incidence.

Statistics in Medicine18, 2025–2039, (1999).

[14]N. H. Chan and C. Z. Wei, Limiting

distributions of least squares estimates of unstable autoregressive

processes. The Annals of Statistics16, 367–401, (1988).

[15]S. J. Deutsch and F. B. Alt, The effect of

Massachusetts’ gun control law on gun–related crimes in the city of Boston.

Evaluation Quarterly1(4), 543–568, (1977).

[16]F. C. Drost, R. v. den Akker and B. J. M. Werker,

Local asymptotic normality and efficient estimation for INAR() models.

Journal of Time Series Analysis29(5), 783–801, (2008).

[17]F. C. Drost, R. v. den Akker and B. J. M. Werker,

The asymptotic structure of nearly unstable non-negative

integer-valued AR(1) models.

Bernoulli15(2), 297-324, (2009).

[18]F. C. Drost, R. v. den Akker and B. J. M. Werker,

Efficient estimation of autoregression parameters and innovation distributions

for semiparametric integer-valued AR() models.

Journal of the Royal Statistical Society: Series B

(Statistical Methodology)71(2), 467-485, (2009).

[19]J. G. Du and Y. Li, The integer valued

autoregressive (INAR(p)) model.

Journal of Time Series Analysis12(2), 129–142, (1991).

[20]V. Enciso–Mora, P. Neal and T. Subba Rao,

Efficient order selection algorithms for integer-valued ARMA processes.

Journal of Time Series Analysis30(1), 1–18, (2009).

[21]S. N. Ethier and T. G. Kurtz,

Markov Processes.

John Wiley & Sons, Inc., New York, 1986.

[22]J. Franke and T. Seligmann,

Conditional maximum-likelihood estimates for INAR(1)

processes and their applications to modelling epileptic seizure counts.

In: T. Subba Rao (Ed.), Developments in time series, pp. 310–330.

London: Chapman & Hall, (1993).

[23]J. Franke and T. Subba Rao,

Multivariate first order integer valued autoregressions.

Technical report. Math. Dep., UMIST, England (1995).

[24]R. Freeland and B. McCabe,

Asymptotic properties of CLS estimators in the Poisson

AR(1) model. Statistics & Probability Letters 73, 147–153, (2005).

[25]G. Gauthier and A. Latour,

Convergence forte des estimateurs des paramétres d’un processus GENAR.

Annales des Sciences Mathématiques du Québec 18(1), 49–71, (1994).

[26]C. Gourieroux and J. Jasiak,

Heterogeneous INAR(1) model with application to

car insurance. Insurance: Mathematics and Economics34,

177–192, (2004).

[27]L. Györfi, M. Ispány, G. Pap and K. Varga,

Poisson limit of an inhomogeneous nearly critical model.

Acta Universitatis Szegediensis. Acta Scientiarum Mathematicarum73(3-4), 789–815, (2007).

[28]R. Hay and R. McCleary, Box–Tiao times series models for impact assessment.

Evaluation Quarterly3(2), 277–314, (1979).

[29]J. Hellström,

Unit root testing in integer-valued AR(1) models.

Economics Letters70, 9–14, (2001).

[30]R. A. Horn and Ch. R. Johnson,Matrix Analysis.

Cambridge University Press, Cambridge, 1985.

[31]M. Ispány, G. Pap and M. C. A. van Zuijlen,

Asymptotic inference for nearly unstable INAR(1) models.

Journal of Applied Probability40(3), 750–765, (2003).

[32]M. Ispány, G. Pap and M. C. A. van Zuijlen,

Asymptotic behaviour of estimators of the parameters of nearly unstable

INAR(1) models.

Foundations of statistical inference (Shoresh, 2000), 195–206,

Contributions to Statistics, Physica, Heidelberg, (2003).

[33]M. Ispány and G. Pap,

A note on weak convergence of step processes.

Acta Mathematica Hungarica126(4), 381–395, (2010).

[34]J. Jacod and A. N. Shiryaev,Limit Theorems for Stochastic Processes, 2nd ed.

Springer–Verlag, Berlin, 2003.

[35]P. Jeganathan, On the asymptotic behavior of

least squares estimators in AR time series with roots near the unit circle.

Economic Theory7, 269–306, (1991).

[36]R. C. Jung, G. Ronning and A. R. Tremayne,

Estimation in conditional first order autoregression with

discrete support. Statistical Papers46, 195–224, (2005).

[37]R. C. Jung and A. R. Tremayne,

Binomial thinning models for integer time series.

Statistical Modelling6, 81 -96, (2006).

[39]M. Kachour and J. F. Yao,

First-order rounded integer-valued autoregressive (RINAR(1)) process.

Preprint, University of Rennes 1, (2008).

[40]O. Kallenberg,

Foundations of Modern Probability.

Springer, New York, Berlin, Heidelberg, 1997.

[41]I. Karatzas and S. E. Shreve,

Brownian Motion and Stochastic Calculus, 2nd ed.

Springer, Berlin, 1991.

[42]L. A. Klimko and P. I. Nelson,

On conditional least squares estimation for stochastic processes.

The Annals of Statistics6(3), 629–642, (1978).

[43]A. Latour, The multivariate GINAR() process.

Advances in Applied Probability29, 228–248, (1997).

[44]A. Latour,

Existence and stochastic structure of a non-negative integer-valued

autoregressive processes.

Journal of Time Series Analysis19(4), 439–455, (1998).

[45]S. Ling and W. K. Li, Limiting distributions

of maximum likelihood estimators for unstable ARMA time

series with GARCH errors. The Annals of Statistics26, 84–125, (1998).

[46]S. Ling and W. K. Li, Asymptotic inference

of nonstationary fractional ARIMA models. Economic Theory17,

738–764, (2001).

[47]I. MacDonald and W. Zucchini,Hidden Markov and Other Models for Discrete-valued Time Series.

Chapman & Hall, London, 1997.

[48]T. van der Meer, G. Pap and

M. C. A. van Zuijlen, Asymptotic inference for nearly unstable AR() processes.

Economic Theory15, 184–217, (1999).

[49]B. P. M. McCabe, G. M. Martin and

D. Harris, Optimal probabilistic forecasts for counts.

Monash University, Working Paper 7/09, 2009.

[50]E. McKenzie,

Some simple models for discrete variate time series.

Water Resources Bulletin21, 645–650, (1985).

[51]E. McKenzie, Discrete variate time series.

In: Shanbhag D. N., Rao C. R. (eds) Handbook of Statistics.

Elsevier Science, 573–606, (2003).

[52]M. Monteiro, I. Pereira and M. G. Scotto,

Optimal alarm systems for count processes.

Communications in Statistics. Theory and Methods37, 3054–3076, (2008).

[53]T. M. O’Donovan, Short Term Forecasting: An Introduction to the

Box–Jenkins Approach. Wiley, New York, 1983.

[54]H. Pavlopoulos and D. Karlis,

INAR(1) modeling of overdispersed count series with an environmental application.

Environmetrics19, 369–393, (2008).

[55]P. C. B. Phillips and Z. Xiao, A primer on

unit root testing. J. Econom. Surv.12, 423–470, (1998), In:

M. McAleer, L. Oxley (Eds.), Practical Issues in Cointegration

Analysis, Blackwell, Oxford, 1999.

[56]J. Pickands III and R. Stine,

Estimation for an M/G/1 queue with incomplete

information. Biometrika84, 295–308, (1997).

[57]A. M. M. S. Quoreshi,

Bivariate time series modelling of financial count data.

Communications in Statistics. Theory and Methods35, 1343–1358, (2006).

[58]D. Revuz and M. Yor,

Continuous Martingales and Brownian Motion, 3rd ed.,

corrected 2nd printing. Springer-Verlag, Berlin, 2001.

[59]N. Rudholm,

Entry and the number of firms in the Swedish pharmaceuticals market.

Review of Industrial Organization19, 351–364, (2001).

[60]M. E. Silva and V. L. Oliveira,

Difference equations for the higher-order moments and cumulants of the

model.

Journal of Time Series Analysis25(3), 317–333, (2004).

[61]M. E. Silva and V. L. Oliveira,

Difference equations for the higher-order moments and cumulants of the

model.

Journal of Time Series Analysis26(1), 17–36, (2005).

[62]I. Silva and M. E. Silva,

Asymptotic distribution of the Yule-Walker estimator for

processes.

Statistics & Probability Letters76(15), 1655–1663, (2006).

[63]F. Steutel and K. van Harn,

Discrete analogues of self–decomposability and stability.

The Annals of Probability7, 893–899, (1979).

[64]F. W. Steutel and K. van Harn,Infinite Divisibility of Probability Distributions on the Real Line.

Dekker, New York, 2004.

[65]P. Thyregod, J. Carstensen, H. Madsen

and K. Arnbjerg-Nielsen, Integer valued autoregressive models

for tipping bucket rainfall measurements. Environmetrics10,

395–411, (1999).

[66]C. Z. Wei and J. Winnicki, Some asymptotic results for the branching

process with immigration. Stochastic Processes and their Applications31(2), 261–282, (1989).

[67]C. Z. Wei and J. Winnicki, Estimation of the means in the branching

process with immigration. The Annals of Statistics18(4), 1757–1773, (1990).

[68]C. H. Weiß,

Thinning operations for modelling time series of counts—a survey.

Advances in Statistical Analysis92(3), 319 -341, (2008).

[69]J. Zhou and I. V. Basawa,

Least-squared estimation for bifurcation autoregressive processes.

Statistics & Probability Letters74, 77–88, (2005).