Continuously monitored barrier options under Markov processes

Abstract.

In this paper we present an algorithm for pricing barrier options in one-dimensional Markov models. The approach rests on the construction of an approximating continuous-time Markov chain that closely follows the dynamics of the given Markov model. We illustrate the method by implementing it for a range of models, including a local Lévy process and a local volatility jump-diffusion. We also provide a convergence proof and error estimates for this algorithm.

1. Introduction

1.1. Background and motivation

Barrier options are among the most popular exotic derivatives. Such contracts form effective risk management tools, and are liquidly traded in the Foreign Exchange markets. The most liquid barrier options in FX markets are continuously monitored single- or double-no-touch options and knock-in or knock-out calls and puts (see e.g. Hakala and Wystup [28], Lipton [45], [46], Wystup [56]). The main challenge in the risk management of large portfolios of barrier options faced by trading desks that make a market in these securities is to be able to price and hedge the barrier products in models that are flexible enough to describe the observed option prices (i.e. calibrate to the vanilla market price quotes).

It is by now well established that the classical Black-Scholes model lacks the flexibility to fit accurately to observed option price data (see e.g. Gatheral [23] and the references therein). A variety of models have been proposed to provide an improved description of the dynamics of the price of the underlying that can more accurately describe the option surface. Parametric diffusion models like the CEV process [14] have additional flexibility to fit the vanilla skew at a single maturity for as many options as there are free parameters in the model. The seminal idea (developed by Dupire [18] and Gyöngy [26]) that allows one to construct a model that can describe the entire implied volatility surface (across all strikes and maturities) is that of local volatility models, where a non-parametric form of the local volatility function is constructed from the option price data. It has been shown that in practice such models imply unrealistic dynamics of the option prices (see the formula for the implied volatility in a local volatility model given in [27]). The ramification is an unrealistic amount of vega risk, which is expensive to hedge. Therefore, even though in a local volatility model barrier options can be priced using a PDE solver, this modelling framework alone is not suitable for the risk management of a large portfolio of barrier options.

At the other end of the spectrum are the jump processes with stationary and independent increments, which can fit very well the volatility smile at a single maturity (see e.g. [12] and the references therein). A variety of models in the exponential Lévy class have been proposed in the literature: CGMY [8], KoBoL [6], generalised hyperbolic [19], NIG [4] and Kou [37]. Exponential Lévy processes are simple examples of Markov processes whose law is uniquely determined by the distribution of the process at a single time. Since the set of call option prices at a fixed maturity for all strikes uniquely determines the marginal risk-neutral distribution at that maturity, calibration to option prices at multiple maturities in principle fixes the corresponding marginals. It has been reported (see e.g. [12]) that Lévy processes lack the flexibility of calibrating simultaneously across a range of strikes and maturities. Several generalisations within the one-dimensional Markov framework have been proposed.

If the stationarity assumption is relaxed while the property of independence of increments is retained, one arrives at the class of exponential additive processes, which have recently been shown to calibrate well to several maturities in equity markets. The Sato process introduced in Carr et al. [10] is an example of such an additive model used in financial modelling.

The independent increments property of a process implies that its transition probabilities are translation invariant in space, so that they only depend on the difference between the end and starting value of the process. It is well known that the distribution of a log-asset price depends in a non-linear way on the starting point (e.g. in equity markets it has been observed that if the current price is high, then the volatility is low and vice versa). To capture this effect one is led to consider Markov jump-processes whose increments are not independent. As a generalisation of local volatility models, the class of local Lévy processes introduced by Carr et al. [9] allows the modeller to modulate the intensity of the jumps as well as their distribution depending on where the underlying asset is trading. A local volatility jump-diffusion with similar structural properties was calibrated to the implied volatility surface in Andersen and Andreasen [2] and He et al. [29]. Due to the presence of jumps and the absence of stationarity and independence of increments, the problem of obtaining the first-passage probabilities for such a general class of processes is computationally less tractable.

There exists currently a good deal of literature on numerical methods for the pricing of barrier-type options. It is well known that in this case a straightforward Monte Carlo simulation algorithm will be time-consuming and yield unstable results for the prices and especially the sensitivities. The knock-in/out features in the barrier option payoffs lead to slower convergence of the Monte Carlo algorithm. To address this problem the following (semi-)analytical approaches have been developed for specific models:

- (a)

- (b)

The method (a) employs the explicit spectral decompositions for this class of diffusion models, whereas the approach (b) exploits the independence and stationarity of the increments of the Lévy process, and the so-called Wiener-Hopf factorisation. Since both of these approaches hinge on special structural properties of the underlying processes, it is not clear if and how they can be extended to more general Markovian models.

A different approach, pioneered by Kushner (see e.g. [41]), is the discrete time Markov chain approximation method. Originally developed for the numerical solution of stochastic optimal control problems in continuous time, this method consists of approximating the system of interest by a discrete time chain that closely follows its dynamics, and solving the problem of interest for this chain. An application to the pricing of American type options is given in Kushner [40]. Bally et al. [3] develop a quantization method to efficiently value American options on baskets of assets under a local volatility model. Using a discrete time Markov chain, Duan et al. [16] price a discretely monitored barrier option in the Black-Scholes and NGARCH models. Rogers and Stapleton [51] investigate an efficient binomial tree method for barrier option pricing (see also references therein for related methods). Related are PDE and PIDE finite difference discretization methods that have been investigated by various authors; Zvan et al. [57] consider barrier and related options in the Black-Scholes model; Tavella and Randall [55] present an overview of PDE finite difference methods for the pricing of financial instruments; Wang et al. [32] develop a robust scheme for American options under a CGMY model, and Cont and Voltchkova [13] follow a viscosity approach for the PIDEs connected to European and barrier option under Lévy models. Markov chains have also been employed to directly model the evolution of price processes; Albanese and Mijatović [1] model the stochasticity of risk reversals and carried out a calibration study in FX markets under a certain continuous-time Markov chain constructed to model the FX spot process.

1.2. Contribution of the current paper

In this paper we consider the problem of pricing barrier options in the setting of one-dimensional Markov processes, which in particular includes the case of local Lévy models as well as local volatility jump-diffusions and additive processes. The presented approach is probabilistic in nature and is based on the following two elementary observations: (i) given a Markov asset price process it is straightforward to construct a continuous-time Markov chain model whose law is close to that of , by approximating the generator of the process with an intensity matrix; (ii) the corresponding first-passage problem for a continuous-time Markov chain can be solved explicitly via a closed-form formula that only involves the generator matrix of the chain . More precisely, for a given Markov asset price model on the state-space with corresponding generator the algorithm for the pricing of any barrier product (including rebate options, which depend on the position at the moment of first-passage) consists of the following two steps:

-

(i)

Construct a finite state-space and a generator matrix for the chain that approximates the operator on .

- (ii)

The form of the generators of Markov processes that commonly arise in pricing theory (including the local Lévy class) is well known from general theory (and are reviewed in Section 2). The state-space in step (i) is taken to be non-uniform with a higher density of points in the relevant areas such as spot and barrier levels. Subsequently, the generator matrix is defined by matching the instantaneous moments of the Markov processes and the chain on the state-space . This criterion implies in particular that the chain has the same average drift as the asset price process . Step (ii) of the algorithm consists of the evaluation of the closed-form formulas for the first-passage probabilities that can be derived employing continuous-time Markov chain theory (see Theorem 1 below). The evaluation of this formula consists of exponentiation of either the matrix or , which can be performed using the Padé approximation algorithm that is implemented in standard packages such as Matlab (see also [30]). The outputs of the algorithm yield arbitrage-free prices in a certain continuous time Markov chain model for the risky asset price process. This feature is a consequence of the fact that the algorithm is based on the construction of an approximate stochastic model. This property is not shared by many other numerical methods used in practice that are based on purely analytical considerations.

We implemented this algorithm for a number of models that include the features of local volatility as well as jumps. We obtained an accurate match with the numerical results under diffusion and Lévy models that were considered elsewhere in the literature (see Section 6). We prove that by refining the grid the prices generated by this approach converge to those of the limiting model. We also establish, under additional regularity assumptions, an error bound that is linear in the spatial mesh size and the truncation error (see Section 5). We showed that an additional logarithmic factor may arise in this error bound when the Lévy density has a pole of order two at the origin. Numerical experiments (reported in Section 6) appear to suggest that, for a number of models, the error actually decays quadratically in the spatial mesh size. An extension to the case of time-dependent characteristics is presented in an unabridged version of this paper [49], which also includes extra numerical examples, as well as some sample code.

There is good deal of literature devoted to the study of the (weak) convergence of Markov chains to limiting processes. However the (sharp) rates of convergence of prices generated by the Markov chain approximation to those of the limiting model are rarely available, especially for barrier options. For discrete time Markov chains some explicit rates have been established (see e.g. Broadie et al. [7] and Gobet and Menozzi [25]). Establishing the sharp rates of convergence for specific models remains an open question, left for future research.

The remainder of the paper is organized as follows. In Section 2 we define the class of models and barrier option contracts that is considered, and state some preliminary results about Markov processes. Section 3 presents the formulas for the first-passage quantities of the continuous-time Markov chains. In Section 4 we describe the discretization algorithm to construct the intensity matrix of the chain . Section 5 states the convergence results, which are proved in Appendix A. Numerical results are presented in Section 6 and Section 7 concludes the paper.

2. Problem setting: Barrier options for Markov processes

The problem under consideration is that of the valuation of general barrier options, which can be formulated as follows. Given a random process modelling the price evolution of a risky asset, non-negative payoff and rebate functions and , and a set specifying the range of values for which the contract ‘knocks out’, it is of interest to evaluate the expected discounted value of the random cash flow associated to a general barrier option contract

| (2.1) |

where denotes the indicator of a set and

is the first time that enters the set . Furthermore, it is relevant to quantify the sensitivities of this value with respect to different parameters such as the spot value . The cash flow in (2.1) consists of a payment in the case the contract has not knocked out by the time , and a rebate if it has. Examples of commonly traded options included in this setting are the down-and-out, up-and-out and double knock-out options. In particular, by taking we retrieve the case of a standard European claim with payoff at maturity .

We will consider this valuation problem in a Markovian setting, assuming that the underlying is a Markov process with state-space defined on some filtered probability space , where denotes the standard filtration generated by . Thus, takes values in and satisfies the Markov property:

| (2.2) |

for all and bounded Borel functions , where denotes the expectation under the probability measure and is given by

| (2.3) |

By taking expectations in (2.2) we see that the family forms a semigroup:

Informally, these conditions state that the expected value of the random cash flow occurring at time conditional on the available information up to time depends on the past via the value only. Setting the rate of discounting equal to a non-negative constant , for any pair of non-negative Borel functions and the expected discounted value of the barrier cash flow (2.1) at the epoch , the earlier of maturity and the first entrance time , is given by

| (2.4) |

If represents the price of a tradeable asset, is the risk-free rate, is the dividend yield and the process is a martingale, standard arbitrage arguments imply that no arbitrage is introduced if expression (2.4) is used as the current price of the option with payoff (2.1).

Before proceeding we review some key concepts of the standard Markovian setup that will be needed in the sequel. For background on the (general) theory of Markov processes we refer to the classical works Chung and Walsh [11], Ethier and Kurtz [20], Itô and McKean [33] and Rogers and Williams [52] (the latter two in particular treat the case of Markov processes with continuous sample paths). In what follows we will restrict to be in a subclass of Markov processes for which, if the function is continuous and tends to zero at infinity, the expected payoff has the following properties: it depends continuously on the spot and on expiry and also decays to zero when tends to infinity. More precisely, denoting by the set of continuous functions on that tend to zero at infinity, we make the following assumption:

Assumption 1.

is a Feller process on , that is, for any , the family , with defined in (2.3), satisfies:

-

(i)

for any ;

-

(ii)

for any .

The Feller property guarantees that there exists a version of the process with càdlàg paths satisfying the strong Markov property. In particular, a Feller process is a Hunt process.

Throughout the paper we will take the knock-out set to be of the form

| (2.5) |

which includes the cases of double and single barrier options—the latter by taking or To rule out degeneracies we will make the following assumption on the behaviour of at the boundary points and :

Assumption 2.

For every we have where .

This assumption states that the first entrance times into and its interior coincide almost surely, if the spot is equal to . If , a sufficient condition for Assumption 2 to be satisfied is for ; that is, when started at or , the process immediately enters .

The class of Feller processes satisfying Assumption 2 includes many of the models employed in quantitative finance such as (Feller-)diffusions, jump-diffusions with non-generate diffusion coefficient and Lévy processes whose Lévy measure admits a density.

The family is determined by its infinitesimal generator that is defined as

| (2.6) |

for any function for which the right-hand side of (2.6) converges in the strong sense.111That is, the convergence is with respect to the norm of the Banach space . The set of such functions is called the domain of the operator and is dense in . These fundamental facts about semigroups and their generators can be found in [20, Ch. 1].

We next give a few examples of Feller processes with their generators.

Example 1.

A diffusion asset price model evolves under a risk-neutral measure according to the stochastic differential equation (SDE)

| (2.7) |

where is the initial price, and is a given measurable function. To guarantee the absence of arbitrage we assume that is chosen such that the discounted process is a martingale, If, in addition, infinity is not entrance222 See Itô and McKean [33] for an explicit criterion in terms of and for this to be the case. for and is a continuous function, then is a Feller process, and its infinitesimal generator acts on 333 denotes the set of functions with compact support in . as

| (2.8) |

where denotes the derivative of with respect to (see [20, Sec. 8.1]).

Example 2.

The price process in an exponential Lévy model given by

| (2.9) |

where and are constants representing the interest rate and dividend yield and is a Lévy process, such that for all . By construction, is a martingale. Further, if and only if the Lévy measure integrates at infinity, that is,

| (2.10) |

The law of is determined by its characteristic exponent , which is related to the characteristic function of by and which, under condition (2.10), has the Lévy-Khintchine representation

where is the characteristic triplet, with and the Lévy measure, which satisfies the integrability condition . The process is a Feller process with an infinitesimal generator acting on as (cf. Sato [53, Thm. 31.5])

where

Example 3.

More generally, one may specify the price process by directly prescribing its generator to act on sufficiently regular functions as

| (2.11) |

where is given in (2.8) and

where for every , is a (Lévy) measure with support in such that

The discounted process is a local martingale. Sufficient conditions on and to guarantee the existence of a Feller process corresponding to this generator were established in Kolokoltsov [36, Thm. 1.1].

A key step in solving the barrier valuation problems is the observation that the expected values of knock-out options and general barrier options can be expressed in terms of the marginal distributions of two Markov processes associated to . Given a Markov process the processes that have the same dynamics as before entering , but are stopped or jump to the graveyard state upon entering the set , respectively, are themselves Markov processes. Let denote the killed process and the process killed at rate that is stopped upon entering the set . Then the value of the barrier options can be expressed as

where we assume that and the function is defined as . To calculate the value-functions of barrier options written on the underlying price process we thus need to identify and . This can be achieved by employing the infinitesimal generators of the semigroups and associated to the Markov processes and which are explicitly expressed in terms of the generator as follows:

Lemma 1.

(i) For any , where is the domain of the generator , we have

| (2.12) |

where the convergence is pointwise. If is a Feller process, and

| (2.13) |

then , where is the infinitesimal generator of the semigroup .

(ii) Let and assume that satisfies

| (2.14) |

Then

| (2.15) |

where the convergence is pointwise. If is a Feller process and

then , where is the infinitesimal generator of the semigroup .

Lemma 1 is a straightforward consequence of the definition of the infinitesimal generator and the Hille-Yosida theorem, see e.g. [53, Lemma 31.7] (see [49] for the complete proof of Lemma 1). If and are themselves Feller processes, the relations between and , and between and can formally be expressed as follows:

| (2.16) |

Equation (2.16) can be given a precise meaning if, for example, and can be defined as a self-adjoint operator on a separable Hilbert space (see e.g. Ch. XII in Dunford and Schwarz [17], or Hille and Philips [31]). By determining the spectral decompositions of and one can construct spectral expansions of and , which in the case of a discrete spectrum reduces to a series expansion. See Linetsky [42, 43, 44] for a development of this spectral expansion approach for one-dimensional diffusion models in finance, and an overview of related literature.

When (asymmetric) jumps are present, the operator is non-local and not self-adjoint, and the spectral theory has been less well developed, with fewer explicit results. Here we will follow a different approach: we will approximate by a finite state Markov chain, and show that for the approximating chain a matrix analog of the identities (2.12)–(2.16) holds true, where the infinitesimal generators and can be easily obtained from . We give a self-contained development of this approach in Section 3.

3. Exit probabilities for continuous-time Markov chains

Given a Markov price process of interest, the idea is to construct a continuous-time finite state Markov chain whose dynamics are “close” to those of , and to calculate the relevant expectations for this approximating chain. In this section we will focus on the latter; we will return to the question of how to construct such a chain in Section 4. Assume therefore we are given a finite state continuous-time Markov chain . From Markov chain theory it is well known that the chain is completely specified by its state-space (or grid) and its generator matrix , which is an square matrix with zero row sums and non-positive diagonal elements, if has elements. Given the generator matrix the family of transition matrices of , defined by for , is given by

In particular, the expexted discounted pay-off at maturity is then given by

| (3.1) |

for and any function . Here and throughout the paper we will identify any square matrix and any vector in with functions

where the vectors denote the corresponding standard basis vectors of and ′ stands for transposition.

The generator can be retrieved from the family of matrices defined above by differentiation at , that is,

In order for itself to form a pricing model, defined under a martingale measure, we will suppose in addition that is non-negative and that the discounted process is a martingale; more precisely we assume that is a martingale where

| (3.2) |

with the hitting time of the “boundary” which consists of the smallest and largest elements of the state space , and . The Markov property of implies that the process given in (3.2) is a martingale precisely if

| (3.3) |

where the function is given by . Below we will show how to express the exit probabilities of the chain using matrix exponentiation in a way that is identical in form to the expected value (3.1) of a European pay-off. To that end, we partition into a ‘continuation’ set and a ‘knock-out’ set , where

| (3.4) |

and define the first exit time of from by

| (3.5) |

where we use the convention and where we will take the set as in (2.5).

The value of a general barrier knock-out option with a rebate depends on the joint distribution of the exit time from and the positions of the underlying at maturity and at the moment of exit. The corresponding quantities for the chain can be expressed in terms of two transformations of , namely the chain that is killed upon exiting and the chain that is absorbed at that instance, respectively. Correspondingly, we associate to the generator matrix , two matrices: the matrix , where , and the matrix , defined by

| (3.6) | |||||

| (3.7) |

We can now state the key result of this section:

Theorem 1.

For any , and and any function it holds that

| (3.8) |

In particular, for and with for we have that

| (3.9) | |||||

| (3.10) | |||||

| (3.11) |

where , the restriction of to .

Formulas (3.9)–(3.11) give a simple way of computing barrier option prices by a single matrix exponentiation. The expectation in (3.9) can be obtained by computing the spectral decomposition of the matrix and applying the formula . The powerful Padé approximation method for matrix exponentiation, described in [30], can also be used to compute efficiently the matrix exponentials in Theorem 1. Since the state-space is finite, Theorem 1 is a corollary of Lemma 1. We present next a direct probabilistic derivation.

Proof. To prove equation (3.8), we will verify that the expected value of an Arrow-Debreu barrier security that pays 1 precisely if is in the state at the earlier of the maturity and the knock-out time is given by

| (3.12) |

For a given time grid with denote by the expected value of the corresponding discretely monitored Arrow-Debreu security and let

be the corresponding time at which the barrier is crossed. Since the paths of the chain are piecewise constant, it follows that and as tends to infinity. Hence the expected values of the discretely monitored Arrow-Debreu securities converge to the expected value of the continuously monitored one,

Clearly, since is the knock-out set, it holds for all that

where is a square matrix of size with if and zero else. Further, for an application of the Markov property of shows that

Combining the two cases, iterating the argument and using the differentiability of at shows that

since . When tends to zero, this expression converges to , which completes the proof of (3.12) and hence implies (3.8). Equation (3.11) follows then directly by applying (3.8) to . Noting that for any and any we have

we get that

which yields (3.9). Finally, (3.10) is a direct consequence of (3.1), (3.9) and the fact that a European option with pay-off is equal to the sum of a knock-out barrier option and a knock-in barrier option with the same pay-off and same knock-out/knock-in levels.

4. Construction of the Markov chain

The Markov chain approximation algorithm for homogeneous Feller processes can now be described as follows:

-

(1)

Construct an approximating Markov chain:

-

(a)

specify a (non-uniform) grid ;

-

(b)

define a generator matrix of a Markov chain with state-space .

-

(a)

- (2)

A suitable choice of the grid in step (1a) is essential for the effectiveness of the above pricing algorithm. The construction of an optimal grid (according to some criterion) is a topic of separate study, which will not be pursued further in this paper. One of the features of a good grid is that it has sufficient resolution in regions of interest, such as the current spot value and the barrier levels, which is a necessary condition for constructing a Markov chain market model that approximates well the dynamics of the given price process. Another desirable feature is that the grid “covers” a sufficiently large part of the state space, which is needed to control the truncation error that arises when approximating an infinite state space by a finite state space. To employ a uniform grid that satisfies these conditions would be computationally expensive. The use of adaptive meshes for option pricing was proposed in Figlewski and Gao [21]. Here we employ the following procedure for generating a suitable non-uniform grid , based on an algorithm from [55]:

-

(1)

Pick and the density parameters , , and the smallest and largest values of the grid , where .

-

(2)

Define GenerateSubGrid, for , where .

-

(3)

Set ,

where the subgrid is generated by the following procedure:

GenerateSubGrid

-

(1)

Compute , .

-

(2)

Define the lower part of the grid by the formula for . Note that .

-

(3)

Define the upper part of the grid using the formula for . Note that .

Return

The non-uniform state-space for the Markov chain is constructed by concatenating the three subgrids that are generated by specifying lower, middle and upper points and density parameters and . A smaller density corresponds to a grid that is more concentrated around the middle point . Observe that the algorithm above places the current spot and the barrier levels on the grid and that the resolution of the grid around and can be controlled by the density parameters ,. A Matlab implementation of this grid generator can be downloaded from [48]. The remainder of this section will be devoted to step (1b) in the algorithm described above.

4.1. Jump processes with state-dependent characteristics

The construction of the generator matrix of the approximating Markov chain is now carried out in two steps: we first define the jump matrix , which corresponds to the discretization of the jump measure , and then characterize a tri-diagonal generator matrix by stipulating that the Markov chain with the generator has the same instantaneous moments as the process .

We start by building the state-space with elements using the algorithm described in the beginnig of this section. Define the sets

where the “boundary” consist of the smallest (i.e. ) and largest (i.e. ) elements in and the “interior” is the complement of the boundary. For any given we associate to the set defined by

The set consists of the relative jump sizes of jumps starting from and arriving at any other point in . The -th row of the jump part of the generator of is obtained by discretizing the jump measure on the set . In particular let and define a function such that

| (4.1) |

where . A possible natural choice for would be the mid-point of the interval

We can now define the jump part of the generator as

| (4.2) |

where and

| (4.3) |

Note that the function generates a partititon of . The jump intensities of the chain, defined in formula (4.2), are obtaiend by integrating the Lévy measure over the corresponding part of the partition. For we set for all . It is clear that the matrix constructed in this way is a generator matrix.

In the second step we match the first and second instantaneous moments of the asset price process . In other words the chain must satisfy conditions

| (4.4) |

for all starting states . Note that condition (4.4) implicitly assumes that the second instantaneous moment of exists. This is the case if the jump measure satisfies the following condition

| (4.5) |

which we now assume to hold.

The task now is to find a tri-diagonal generator matrix such that the chain generated by the sum satisfes (4.4). The tri-diagonal matrix therefore has to satisfy the following conditions

| (4.6) | |||||

| (4.7) | |||||

| (4.8) |

for all , where are the instantaneous interest rate and dividend yield respectively and is the local volatility function in (2.11). The right-hand side of equation (4.7) is the difference of the risk-neutral drift and the drift induced by the presence of jumps. Similarly the right-hand side of the linear equation in (4.8) consists of the difference of the instantaneous second moments of the asset price process (computed directly from its generator (2.11)) and the chain that corresponds to the jump generator . As usual we assume the absorbing boundary condition for all .

The linear system in (4.6)–(4.8) can typically be satisfied by a tri-diagonal generator matrix if is strictly positive. Once we find we define the generator matrix of the approximating chain by

Remark 1.

In the case that is a diffusion time-changed by an independent Lévy subordinator, there is an alternative approach to constructing the approximating continuous-time Markov chain , based on the Phillips theorem. For the details of this construction see [49].

5. Convergence and error estimates

5.1. Convergence of barrier option prices

Consider a sequence of finite-state continuous-time Markov chains approximating a given Feller price process . For to replicate as closely as possible the dynamics of one chooses the generator matrix with the corresponding state-space such that it is uniformly close to the infinitesimal generator of , in the sense that the distance between the generators is small for a sufficiently large class of regular test functions , where

where equals without the smallest and the largest elements and is the restriction of to . More specifically, if tends to zero as tends to infinity for in the class and the probability that the chain exits before time tends to zero, then the sequence of processes converges weakly to the process . This weak convergence on the level of the process implies in particular that the marginal distributions of will converge to those of , and therefore the values of European options converge, that is,

for , maturity , and continuous bounded functions .

The payoff of the barrier option can be described in terms of the first-passage time of and the position of at that moment, which are both functionals of the path . For the weak convergence of to to carry over to convergence of barrier-type payoffs, continuity (in the Skorokhod topology) is required of these two functionals, which is guaranteed to hold under Assumption 2. In view of the fact that the payoff of a barrier option is typically a discontinuous function, an additional condition is needed to ensure the convergence of the barrier option prices; we will assume that and are such that

| (5.1) |

Most models used in mathematical finance satisfy this condition. Even if (5.1) is not satisfied, this does not constitute a limitation in practice, since for any given process the condition is satisfied for all but countably many pairs . The statement of the convergence is made precise in the following theorem.

Theorem 2.

Let be a Feller process with state-space and infinitesimal generator that does not vanish at zero and infinity.444The set where the generator does not vanish is defined to be the set of all with the following property: for every open interval in that contains (if then takes the form for some ) there exists a function with compact support in such that the function is not identically equal to zero. Let be a sequence of Markov chains with generator matrices such that the rows corresponding to the smallest and the largest elements in are equal to zero. Assume further that the following two conditions are satisfied for any function in a core of :555A core of the operator is a subspace of the domain of that is (i) dense in and (ii) there exists such that the set is dense in .

| (5.2) | |||

| (5.3) |

where for any set we define . If (5.1) holds, then, as ,

for any bounded continuous functions .

Remark 2.

Since condition (5.2) is required to hold for all in a core of , it follows that will eventually ‘fill up’ the part of the state-space where the generator does not vanish. Indeed, if there were to exist an open interval that does not intersect for large , then condition (5.2) would not hold for functions with compact support in this open interval satisfying , as . In particular, condition (5.2) implies that and when with if the generator does not vanish in a neighbourhood of zero and infinity.

Remark 3.

Note that, since is by definition an element in for any in the domain of , it holds that as and that is well defined and equal to . Assume that does not vanish at zero and infinity and that the rows corresponding to the smallest and the largest elements in of the generator matrices are equal to zero. Then, if conditions (5.2) and (5.3)(i) are satisfied, we have

| (5.4) |

Remark 4.

In practice the condition of boundedness of the payoff is not restrictive as it is always possible to consider the truncation for large constants without losing noticeable accuracy. Further, under additional regularity properties on the parameters of the process , the convergence in Theorem 2 also holds true for barrier call options. To see why this is the case note that

| (5.5) |

where denotes the expectation under the measure given by . Under the process remains a Markov process, and, under additional regularity properties is still a Feller process. The convergence then follows from Theorem 2 as the pay-off function on the right-hand side of (5.5) is bounded.

5.2. Error estimates

In this section we quantify the speed at which the algorithm converges by providing error estimates for a specific choice of a sequence of approximating Markov chains, assuming sufficient smoothness of the value-function of the barrier option. Consider a Feller process with infinitesimal generator acting on with compact support as

| (5.6) | |||||

| (5.7) | |||||

| (5.8) |

where ′ denotes differentiation with respect to , ( and are the instantaneous interest rate and dividend yield respectively) and is a nonnegative locally bounded function such that

where .

We next describe the sub-class of Markov processes that we will consider.

Definition 1.

The process is called uniformly of bounded jump-variation if the jump-density satisfies the integrability condition

| (5.9) |

where

| (5.10) |

Definition 2.

The process is called locally of stable type on if there exist constants and such that for all

| (5.11) | |||||

| (5.12) |

We will consider three different cases:

-

•

Case O: is uniformly of bounded jump-variation.

-

•

Case I: is locally of stable type with or .

-

•

Case II: is locally of stable type with .

Case I can be considered to be a boundary case separating cases O and II, as is uniformly of bounded jump-variation if it is of stable type with . The class of processes of uniformly bounded jump-variation (case O) contains processes whose jump-part forms a compound Poisson process (such as the Kou model [37]), as well as the Lévy models of bounded variation such as for example the VG model. Examples of processes satisfying the condition in cases I and II are the Generalised Hyperbolic Lévy models and CGMY models with , respectively. More generally, the class of processes that are locally of stable type contains the class of regular Lévy processes of exponential type studied in Boyarchenko and Levendorskii [6].

We will impose in addition the following regularity conditions:

Assumption 3.

There exists a constant such that for all

Assumption 4.

The pay-off function is Lipschitz-continuous666A function is Lipschitz continuous if there exists a constant such that for all . and has compact support. The barrier option value-function is .

Remark 6.

In the strictly elliptic case ( for ) with a jump-part that is uniformly of bounded variation, explicit sufficient conditions on the data and guaranteeing the smoothness of required in Assumption 4 follow from classical existence and uniqueness results for Cauchy-Dirichlet problems associated to second order partial-integro differential operators. Specifically, Theorem II.3.3 in Garroni & Menaldi [22] implies that if, for some , the following conditions are satisfied: (a) has compact support in and 777 is the set of functions that are times continuously differentiable with the th derivative -Hölder continuous., (b) and (c) is with bounded derivatives, uniformly over . Note that (c) implies that the in (5.8) is if is .

Throughout the rest of this section we take

and consider the spatial grid given by

| (5.13) |

We will denote by

| (5.14) |

the mesh of the spatial grid, and by

| (5.15) |

the tail mass of the jump-measure, where and

are the relative jump-sizes from to the one-but-largest and one-but-smallest elements and of the state-space . We approximate by a sequence of Markov chains with infinitesimal generators . An explicit description of is given in Appendix A.1.

Theorem 3.

Let Assumptions 3 and 4 hold, and consider cases O, I or II. Assume also that the sequences of grids satisfies

Then there exist constants , , independent of and , given in (5.14) and (5.15), such that for all sufficiently large and

where , and

| (5.16) |

The proof of Theorem 3 is given in Appendix A.2. The logarithmic factor in the error bound (5.16) in case I is due to the form (5.11)–(5.12) of the singularity of the jump measure at zero in this case (see the proof for details). Note that the discontinuous part of a process satisfying case I is of infinite variation, but has zero -variation for every .

Numerical experiments, reported in Section 6, suggest that in several pricing models of interest the error of the Markov generator (MG) algorithm described in Section 4 is actually of order . A further theoretical investigation of error bounds and sharp rates of convergence of the algorithm, is left for future research.

6. Numerical examples

In this section the Markov chain algorithm is examined numerically in a variety of contexts. Subsection 6.1 contains a numerical examples for the geometric Brownian motion model and a comparison with a binomial tree method for the pricing of barrier options. In subsection 6.2 the algorithm is applied to two cases of Lévy driven SDEs. Further numerical examples, including comparisons of computational times of the various algorithms, can be found in [49].

6.1. Geometric Brownian motion

The model is given by SDE (2.7) where the volatility function is constant and the drift equals , where is the risk free rate and is the dividend yield. We now compare our algorithm (MG), based on the Markov generator of the approximating chain , with the results obtained in Geman and Yor [24] and Kunitomo and Ikeda [39]. The numerical results are contained in Table 1.

| GY | KI | MG | GY | KI | MG | GY | KI | MG |

| 0.0411 | 0.041089 | 0.041082 | 0.0178 | 0.017856 | 0.017856 | 0.07615 | 0.076172 | 0.076165 |

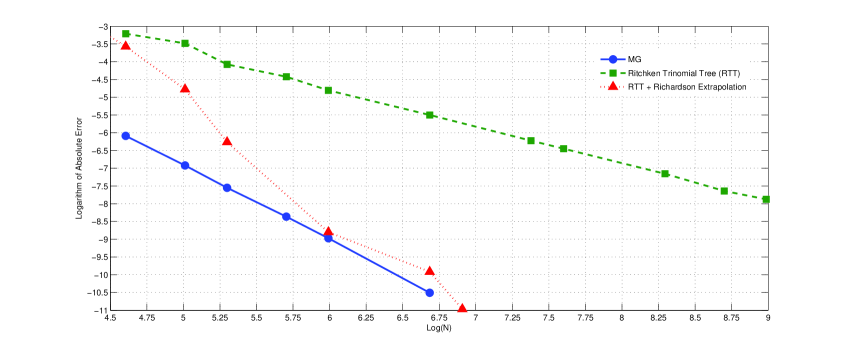

In Figure 3 the errors and computation times of the Markov generator algorithm (MG) and a trinomial tree are plotted against the number of points, for the computation of the price of a double knock-out barrier call option. Note that the graph of the logarithm of the absolute pricing error for the MG algorithm given in Figure 3 is approximately linear in with slope , which implies that the error itself is approximately quadratic in . The pricing algorithm, given in Ritchken [50, Ex. 7], is based on the trinomial tree and it appears to converge at the rate . Figure 3 shows that when the trinomial tree algorithm of Ritchken [50, Ex. 7] is combined with the second order Richardson extrapolation, the convergence appears to be of higher order than in the MG algorithm.

6.2. Lévy and local Lévy models

6.2.1. The CGMY/KoBoL process

In this section we assume that the price is again an exponential Lévy process given by (2.9), where the Lévy processes is a CGMY process [8] with Lévy density given by the formula

| (6.1) |

The inequality is induced by the integrability condition on the Lévy measure at zero and the condition implies the exponential moment condition (2.10).

Madan and Yor [47] show that the CGMY process has the same law as the time-changed Brownian motion with and Lévy subordinator that is independent of and that has Laplace exponent given by

| (6.2) |

where denotes the Gamma function and the functions , are given by the formulae

We compare our numerical results with those obtained in Boyarchenko and Levendorskii [5] using a Fourier method (see Table 2).

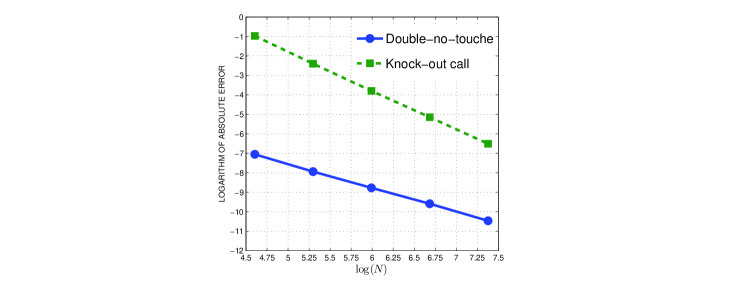

In Figure 4 the error and computation times are plotted of the prices of double-no-touch and double knock-out put options as a function of the grid size. As the true values we took the outcomes of the algorithm for . The figure appears to suggest that the error is approximately proportional to and , respectively, where is the number of point in the grid.

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

6.2.2. A local Lévy model

The following Lévy driven SDE specifies a Markov process with local volatility and double-exponential jumps,

| (6.3) | |||||

| (6.4) |

The special case of this model for was introduced into the mathematical finance literature by Kou [37]. The random variables , , are independent of both the Brownian motion and the Poisson process with intensity and are distributed according to the double exponential density

The parameter is given by

If the process has positive probability of hitting zero in finite time, in which case we take 0 to be absorbing.

It is clear that the model described by (6.3) and (6.4) has a generator of the form given in (2.11) with and . The jump measure in representation (2.11) is supported in and in our case by (6.2.2) takes the explicit form

| (6.6) |

Representation (6.6) of the jump measure of the asset price process can now be used to construct the “jump” generator defined in equations (4.2) and (4.3). Furthermore it is clear from (6.6) that the instantaneous variance term caused by the jumps of the process in (4.8) is of the form

Note that in the present model the instantaneous variance is finite (cf. condition (4.5)) if which is a condition that is typically satisfied in applications. The numerical results of the MG algorithm applied to an up-and-in call option are contained in Table 3, and are compared in the case with the corresponding results of Kou and Wang [38] (see Table 3 in [38]).

| Local Lévy model | MG: | MG: | MG: | KW | |

|---|---|---|---|---|---|

| 10.0528 | 10.0530 | 10.0530 | 10.05307 | ||

| 9.2768 | 9.2771 | 9.2772 | 9.27724 | ||

| 9.7685 | 9.7688 | 9.7688 | N/A | ||

| 8.9572 | 8.9575 | 8.9575 | N/A | ||

| 9.0185 | 9.0187 | 9.0188 | N/A | ||

| 8.0855 | 8.0858 | 8.0858 | N/A | ||

Figure 5 presents the pricing error for the up and in call option described in Table 3. The error of the pricing algorithm is plotted on a log-log-scale against the number of points in the state-space, for the parameter values and . Unlike in the case of double knock-out options where a truncation error can be avoided, a truncation error will be present when pricing a single up-and-in option, as in the example above. To ensure that the truncation error is sufficiently small we ran the algorithm for an increasing sequence of values of , the largest point in the state-space of the chain, and observed that the outcomes did not change up to the required accuracy. The slope of the line in Figure 5 is equal to -2, which suggests that also in this case the algorithm is of order in the mesh size.

7. Conclusion

In this paper we presented an algorithm for pricing barrier options in one-dimensional Markovian models based on an approximation by continuous-time Markov chains. The generator of the approximating chain is constructed by the matching of instantaneous moments of the infinitesimal generator of the Markov process in question, on a suitable non-uniform grid. The approximate barrier option prices are then obtained by calculating the corresponding first-passage distributions for the approximating Markov chain.

To illustrate the flexibility of the method we implemented the algorithm for a number of models, including local volatility models with jumps and models with time-dependent jump-distributions (see [49]). In the cases of the diffusion and jump-diffusion models where results had been obtained before in the literature, the algorithm produced outcomes that accurately matched those results, and we numerically investigated the order of decay of the error.

We provided a mathematical proof of the convergence of the outcomes of the algorithm to the true prices and derived error estimates under additional regularity assumptions. We derived a theoretical upper bound for the error of the outcomes produced by the algorithm that is linear in the spatial mesh size and the truncation error. We showed that an additional logarithmic factor may arise in this error bound when the Lévy density has a pole of order two at the origin. In addition, this bound is also linear in the time mesh size if the model is time-inhomogeneous (see [49]). Numerical experiments suggest that for a number of models the error of the outcomes generated by the algorithm actually decays quadratically in the spatial mesh-size. It would be of interest to establish error bounds under weaker regularity assumptions, and obtain sharp rates of convergence for the specific models, which is a topic left for future research.

Although in principle the method also applies to higher-dimensional Markov processes, the size of the generator matrix would make straightforward application of the algorithm computationally infeasible. The investigation of efficient extensions of the approach to Markov processes of moderate dimension is another topic left for future research.

Appendix A Proofs

A.1. Explicit construction of the generator matrices

Recall that the generator matrix is of the form . The action of , which discretizes the operator (5.7), on a function is described by

| (A.1) |

where and is defined in (5.13). We write instead of and will do so in all that follows. We denote by and the first and second order difference operators given by

| (A.2) | |||||

| (A.3) | |||||

| (A.4) |

with and defined by

where and are as in (5.6). Note that the discretization in (A.1) defines a birth-death process also in the case that .

The jump part of the generator, given in (5.8), can be rewritten as follows

Note that , defined in (5.10), is either finite for all or infinite for all because we are assuming that the process we are approximating falls into one of the categories O, I, II. The representation (A.1) has a natural discretization, which we will now describe, because the second integral in (A.1) is an integral of a continuous function against a finite measure.

For different levels of activity of the purely discontinuous part of , quantified by whether or not defined in (5.10) is finite, the matrix is defined in the following way. Let

where the levels and are given by

| (A.6) |

with the spatial mesh size and

| (A.7) |

where , and are the constants given in (5.11) and (5.12), and

| (A.8) |

We can then define

Finally we define the discretized version of the generator as

| (A.9) | |||||

If is finite is given by

| (A.10) |

where

| (A.11) |

If is equal to infinity we have

| (A.12) | |||||

Here is the (central) difference operator given by

| (A.13) |

Clearly, the first part in the expression in (A.9) defines the generator matrix of a Markov chain taking values in . Similarly the expression in (A.10) yields a generator of a Markov chain. In (A.12) the levels and are chosen so as to ensure that defined in (A.9) is in fact a generator.

To verify that (A.12) defines a Markov jump process we need to show that in the matrix defined in (A.9) all off-diagonal elements are positive. It follows from the definitions of and that this is the case if the following condition holds for all :

| (A.14) | |||||

| (A.15) |

For sufficiently small it is easily checked from the definition of that

which implies that (A.14) is satisfied if, for any ,

This condition is satisfied if, for any , the following two conditions hold for sufficiently small

| (A.16) | |||||

| (A.17) |

In view of (5.11) it follows that (A.16) holds if the following inequality is satisfied

The latter holds for all sufficiently small if

Clearly, , defined in (A.7), satisfies this condition. The fact that Condition (A.17) is satisfied follows by a similar line of reasoning.

A.2. Proof of error estimates

The following lemma is an important auxiliary result for the development of error-estimates. It formalises the intuition that two semi-groups should be “close” if the corresponding infinitesimal generators are “close”.

Suppose that is a Feller process on the state-space with associated semigroup and corresponding infinitesimal generator , and let be a sequence of Markov chains with state-spaces , semigroups and corresponding generator matrices . For any , the domain of , consider the following error measure

| (A.18) |

where we write and with and

| (A.19) |

for any . Then the following estimate holds true:

Lemma 2.

Let and , and suppose that there exists a function and a function such that for all and

Then it holds that

Proof.

The proof closely follows that of Lemma 6.2 in Ethier and Kurtz [20]. Note first that

| (A.20) | |||||

as and commute. Since the function in (A.20) is continuous in , the fundamental theorem of calculus and the fact that imply that

Thus, the triangle inequality yields that

for any , as is non-negative.

Before we proceed we introduce some further notation. The integral part of the infinitesimal generator, and its approximation will be denoted by

| (A.21) | |||||

| (A.22) |

where , ′ denotes the derivative with respect to and

Furthermore, we define

| (A.23) | |||||

| (A.24) |

where, for ,

where is defined in (A.11), with

and

Proof of Theorem 3. In view of Assumption 4, it follows that the stopped and discounted process is a Feller process. The infinitesimal generator of the stopped semi-group corresponding to is denoted by . The process is approximated by the Markov chains with infinitesimal generators , where is described above and is obtained from by setting the rows of corresponding to equal to zero and subtracting on the diagonal elements of the rows corresponding to , as in (3.6).

For any satisfying Assumption 4, has compact support as for all (recall we take ). Furthermore also by Assumptions 3 and 4 and the form of the Feller process under consideration is contained in the domain of the infinitesimal generator . Since

is a martingale, Dynkin’s lemma implies that

so that in particular condition (2.13) holds true with replaced by . From Lemma 1 and Assumption 4 we find that is given by (2.12). Recall that, in the case under consideration, is of the form (2.11).

The form of the approximation and the triangle inequality imply that, for , , the distance between and can be estimated as

where is defined in (5.10). The norm was defined in (A.19) and we wrote for the supremum over all the points in the grid that lie between the barriers. The functions and are given by and where . The operator is equal to defined in (A.4) and is given by or in (A.3) and (A.2) according to whether the constant is positive or negative, as in (A.1). We denote by the derivative of with respect to .

Writing

Assumptions 3 and 4 and second and third order Taylor expansions yield that

Furthermore, the triangle inequality and Assumptions 3 and 4 yield that, for sufficiently small, we have

where is given in Assumption 3, , and and are the spatial mesh size and tail-mass defined in (5.14) and (5.15), and const is a bound for on . In case O the triangle inequality yields that, for sufficiently large,

for some positive constant . Indeed,

In view of Assumptions 3 and 4 the three terms in (A.2) can be estimated as follows:

using that , by a Taylor expansion. Furthermore, for sufficiently small, we have

where we used that for , , by a Taylor expansion.

References

- [1] C. Albanese and A. Mijatović. A stochastic volatility model for risk-reversals in foreign exchange. International Journal of Theoretical and Applied Finance, 12:877–899, 2009.

- [2] L. Andersen and J. Andreasen. Jump-diffusion processes: Volatility smile fitting and numerical methods for option pricing. Review of Derivatives Research, pages 231–262, 2000.

- [3] V. Bally, G. Pagés, and J. Printems. A quantization tree method for pricing and hedging multidimensional American options. Math. Finance, 15(1):119–168, 2005.

- [4] O. E. Barndorff-Nielsen. Processes of normal inverse Gaussian type. Finance and Stochastics, 2:41–68, 1998.

- [5] M. Boyarchenko and S. Z. Levendorskii. Valuation of continuously monitored double barrier options and related securities. Preprint, 2008.

- [6] S.I. Boyarchenko and S.Z. Levendorskii. Non-Gaussian Merton-Black-Scholes Theory. World Scientific, 2002.

- [7] M. Broadie, P. Glasserman, and S. Kou. A continuity correction for discrete barrier options. Math. Finance, 7:325–349, 1997.

- [8] P. Carr, D. Madan, H. Geman, and M. Yor. The fine structure of asset returns: an empirical investigation. Journal of Business, 75(2):305–332, 2002.

- [9] P. Carr, D. Madan, H. Geman, and M. Yor. From local volatility to local Lévy models. Quantitative Finance, 4(5):581–588, 2004.

- [10] P. Carr, D. Madan, H. Geman, and M. Yor. Self-decomposability and option pricing. Mathematical Finance, 17(1):31–57, 2007.

- [11] K.L. Chung and J.B. Walsh. Markov processes, Brownian motion, and time symmetry. Springer, 2005.

- [12] R. Cont and P. Tankov. Financial Modelling With Jump Processes. Chapman & Hall, 2003.

- [13] R. Cont and E. Voltchkova. Integro-differential equations for option prices in exponential Lévy models. Fin. Stoch., 9(3):299–325, 2005.

- [14] J. Cox. Notes on option pricing I: Constant elasticity of variance diffusions. Journal of Portfolio Management, 22:15–17, 1996.

- [15] D. Davydov and V. Linetsky. Pricing options on scalar difusions: an eigenfunction expansion approach. Operations Research, 51(2):185–209, 2003.

- [16] J.-C. Duan, E. Dudley, G. Gauthier, and J.-G. Simonato. Pricing discretely monitored barrier options by a Markov chain. Journal of Derivatives, pages 9–31, 2003.

- [17] N. Dunford and J.T. Schwartz. Linear operators. Part II. Wiley Classics Library. John Wiley & Sons Inc., New York, 1988. General theory, With the assistance of William G. Bade and Robert G. Bartle, Reprint of the 1958 original, A Wiley-Interscience Publication.

- [18] B. Dupire. Pricing with a smile. Risk, pages 18–20, 1994.

- [19] E. Eberlein and U. Keller. Hyperbolic distributions in finance. Bernoulli, 1:281–299, 1995.

- [20] S.N. Ethier and T.G. Kurtz. Markov Processes: Characterization and Convergence. Wiley Series in Probability and Statistics. Wiley, 2005.

- [21] S. Figlewski and B. Gao. The adaptive mesh model: a new approach to efficient option pricing. Journal of Financial Economics, 53:313–351, 1999.

- [22] M.G. Garroni and J.L. Menaldi. Green functions for second order parabolic integro-differential problems. Longman Scientific & Technical, 1992.

- [23] J. Gatheral. The volatility surface: a practitoner’s guide. John Wiley & Sons, Inc., 2006.

- [24] H. Geman and M. Yor. Pricing and hedging double barrier options: a probabilistic approach. Math. Finance, 6:365–378, 1996.

- [25] A. Gobet and S. Menozzi. Exact approximation rate of killed hypoelliptic diffusions using the discrete Euler scheme. Stoch. Proc. Appl., 112:210–223, 2004.

- [26] I. Gyöngy. Mimicking the one-dimensional marginal distributions of processes having an Itô differential. Probab. Th. Rel. Fields, 71:501–516, 1986.

- [27] P.S. Hagan and D.E. Woodward. Implied Black volatilities. Applied Mathematical Finance, 6:147–157, 1999.

- [28] J. Hakala and U. Wystup, editors. Foreign Exchange Risk: Models, Instruments and Strategies. Risk Publications, 2002.

- [29] C. He, J. Kennedy, T. Coleman, P. Forsyth, Y. Li, and K. Vetzal. Calibration and hedging under jump diffusion. Review of Derivatives Research, 9(1):1–35, 2006.

- [30] N.J. Higham. The scaling and squaring method for the matrix exponential revisited. SIAM J. Matrix Anal. Appl., 26(4):1179–1193, 2005.

- [31] E. Hille and R.S. Phillips. Functional analysis and semigroups. American Mathematical Society, Providence, R. I., 1974. Third printing of the revised edition of 1957, American Mathematical Society Colloquium Publications, Vol. XXXI.

- [32] J.W.I. Wan I.R. Wang and P.A. Forsyth. Robust numerical valuation of European and American options under the CGMY process. J. Comp. Finance, 10(4):31–69, 2007.

- [33] K. Itô and H.P. McKean. Diffusion Processes and Their Sample Paths. Springer, 1965.

- [34] J. Jacod and A.N. Shiryaev. Limit theorems for stochastic processes, volume 288 of A Series of Comprehensive Studies in Mathematics. Springer-Verlag, 2nd edition, 2003.

- [35] M. Jeannin and M. Pistorius. A transform approach to calculate prices and greeks of barrier options driven by a class of Lévy processes. Quantitative Finance, 10:629–644, 2010.

- [36] V. N. Kolokoltsov. The Lévy-Khintchine type operators with variable Lipschitz continuous coefficients generate linear or nonlinear Markov processes and semigroups. arxiv.org/abs/0911.5688v1, 2009.

- [37] S.G Kou. A jump-diffusion model for option pricing. Management science, 48(8):1086–1101, 2002.

- [38] S.G Kou and H. Wang. Option pricing under a double exponential jump diffusion model. Management science, 50(9):1178–1192, 2004.

- [39] N. Kunitomo and M. Ikeda. Pricing options with curved boundaries. Math. Finance, 2(4):275–298, 1992.

- [40] H.J. Kushner. Numerical methods for stochastic control problems in finance. In Mathematics of Derivative Securities, Publications of the Newton Institute 15, pages 504–527. Cambridge University Press, 1997.

- [41] H.J. Kushner and P.G. Dupuis. Numerical Methods for Stochastic Control Problems in Continuous Time. Springer, 2nd edition, 2000.

- [42] V. Linetsky. Lookback options and diffusion hitting times: a spectral expansion approach. Finance Stoch., 8(3):373–398, 2004.

- [43] V. Linetsky. The spectral decomposition of the option value. Int. J. Theor. Appl. Finance, 7(3):337–384, 2004.

- [44] V. Linetsky. Spectral expansions for Asian (average price) options. Oper. Res., 52(6):856–867, 2004.

- [45] A. Lipton. Mathematical Methods for Foreign Exchange. World Scientific, 2001.

- [46] A. Lipton. Universal barriers. Risk, pages 81–85, May 2002.

- [47] D. Madan and M. Yor. CGMY and Meixner subordinators are absolutely continuous with respect to one sided stable subordinators. Preprint, 2006.

- [48] A. Mijatović and M. Pistorius. Matlab code for the algorithm from “Continuously monitored barrier options under Markov processes”, 2009. see URL http://www.ma.ic.ac.uk/~amijatov/Abstracts/MarkovBar.html.

- [49] A. Mijatović and M. Pistorius. Continuously monitored barrier options under Markov processes - unabridged version, 2010. Available at SSRN: http://ssrn.com/abstract=1462822.

- [50] P. Ritchken. On pricing barrier options. The Journal of Derivatives, 3(2):19–28, 1995.

- [51] L.C.G. Rogers and E.J. Stapleton. Fast accurate binomial pricing. Fin. Stoch., 2:3–17, 1997.

- [52] L.C.G. Rogers and D. Williams. Diffusions, Markov processes and Martingales. Vols. I,II. Cambridge University Press, 2000.

- [53] K. Sato. Lévy processes and infinitely divisible distributions, volume 68 of Cambridge studies in advanced mathematics. CUP, 1999.

- [54] A. Sepp. Analytical pricing of double-barrier options under a double-exponential jump diffusion process: Applications of Laplace transform. International Journal of Theoretical and Applied Finance, 7(2):151–175, 2004.

- [55] D. Tavella and C. Randall. Pricing Financial Instruments: The Finite Difference Method. Wiley, 2000.

- [56] U. Wystup. FX Options and Structured Products. John Wiley & Sons, 2006.

- [57] R. Zvan, K. R. Vetzal, and P. A. Forsyth. PDE methods for pricing barrier options. J. Econ. Dyn. Con, 24:1563–1590, 1997.