Regularized Adaptive Long Autoregressive

Spectral Analysis

Abstract

This paper is devoted to adaptive long autoregressive spectral analysis when () very few data are available, () information does exist beforehand concerning the spectral smoothness and time continuity of the analyzed signals. The contribution is founded on two papers by Kitagawa & Gersch [1, 2]. The first one deals with spectral smoothness, in the regularization framework, while the second one is devoted to time continuity, in the Kalman formalism. The present paper proposes an original synthesis of the two contributions: a new regularized criterion is introduced that takes both information into account. The criterion is efficiently optimized by a Kalman smoother. One of the major features of the method is that it is entirely unsupervised: the problem of automatically adjusting the hyperparameters that balance data-based vs prior-based information is solved by maximum likelihood. The improvement is quantified in the filed of meteorological radar.

Index Terms:

Adaptive spectral analysis, long autoregressive model, spectral smoothness, time continuity, regularization, hyperparameter estimation, maximum likelihood, meteorological Doppler radar.I Introduction

Adaptive spectral analysis and time-frequency analysis are of major importance in fields as widely varied as speech processing [3], acoustical attenuation measurements [4, 5], ultrasonic Doppler velocimetry [6], or Doppler radars [7, 8, 9, 10, 11]. Reference [12] gives a synthesis of the various methods for these problems, and provides a number of bibliographical introductions.

The present paper focuses on short-time analysis: typically, for analysis of pulsed Doppler signals only 8 or 16 samples are available to estimate one spectrum, with possibly various shapes (multimodal or not, of large spectral width or not, mixed clutter, etc…). Under such circumstances, the construction of the sought spectra becomes extremely tricky on the sole basis of the samples. As a point of reference, let us recall that several hundred samples are usually needed to compute an averaged periodogram with a fair bias-variance compromise [13, 14]. So, parametric methods have generally been preferred, among which autoregressive (AR) play a central role. The AR coefficients estimation is usually tackled in the Least Squares (LS) framework [15, 16]. These methods often provide a solution at points where non-parametric methods are useless; but when the number of data is very low, these techniques become, in their turn, useless, especially if various spectral shapes are expected due to model order limitations.

In order to construct a reliable image, structural information about the sought spectrum sequence must be accounted for. Our investigation is therefore restricted to the cases in which two kinds of information are foreknown: spectral smoothness and time continuity. This a priori information is the foundation of the proposed construction.

In the framework of stationary AR analysis, Kitagawa & Gersch proposed a method integrating the idea of spectral smoothness [1] by which a high-order AR model can be robustly estimated, thereby getting around the difficult problem of order selection, and providing capability to estimate various spectral shapes. For the non-stationary case, and aside from [1], the same authors introduced in [2] a Markovian model for the regressor sequence in the Kalman formalism, in order to reflect time continuity. The present paper reviews [1] and [2] and makes an original synthesis suited to the special configuration of Doppler signals. A new Regularized Least Squares (RegLS) criterion simultaneously includes the spectral and time information and is optimized by a Kalman Smoother (KS).

One of the major features of the method is that it is entirely unsupervised: the adjustment of parameters that weight the relative contributions of the observation versus the a priori knowledge is automatically set by maximum likelihood (ML).

A comparative study is proposed in the context of pulsed Doppler radars. Special attention is payed to atmospheric and/or meteorological context imaging or identification: ground clutter, rain clutter, sea echos, etc… Adaptive spectral estimation of mixed clutter is achieved by means of several usual AR methods and the proposed one. The latter achieves qualitative and quantitative improvements w.r.t. usual methods.

The paper is organized as follows. Section II mainly introduces notations and problem statement. Section III focuses on usual LS methods and usual adaptive extensions. The proposed method is presented in Section IV and Section V deals with the KS. The problem of automatic parameter estimation is addressed in Section VI. Simulation results are presented in Section VII. Finally, conclusions and perspectives for future works are presented in Section VIII.

II Problem statement

The problem is that of processing pulsed Doppler signals from electronic scanning radars or ultrasound velocimeter. The reader may consult [7, 6] for a technological review. The pulsed Doppler systems are such that the observed signals do not occur in the usual form of time-frequency problems. So, neither the usual time-frequency methods nor the one proposed by Kitagawa & Gersch can be directly applied, and part of the presented work consists in constructing an appropriate method for the encountered configuration.

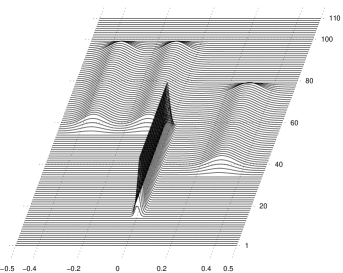

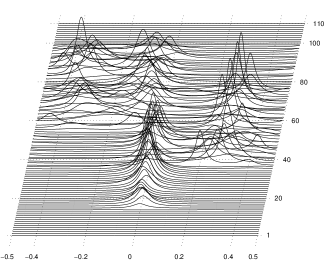

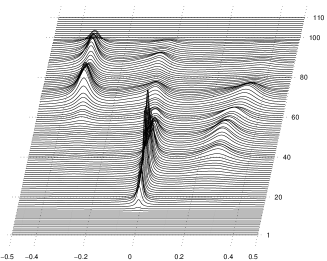

The measurements are available as a set of complex signals , depth-wise juxtaposed in range bins. It is assumed that each is a sample vector extracted from a zero-mean stationary process. Fig. 1 gives a Gaussian simulated example over bins for which samples are observed per bin. The successive regressors are denoted , where indicates the considered bin () and the order of the autoregression coefficient (). Let us note the collection of the whole set of coefficients. Let us also introduce and for signal and prediction error powers. The remainder of the paper is devoted to estimation of these quantities. The next section deals with the usual LS methods and their adaptive extension, and shows their inadequacy for the problem at stake.

III Review of classical methods

III-A Stationary spectral analysis

This subsection is devoted to spectral analysis applied to a single bin . Assuming a Gaussian distribution for the observed signal, the likelihood of the AR coefficients shows a special form [17, p. 82], but its maximization raises a difficult problem. A few authors [18, 19] have undertaken to solve it; but, firstly, the available algorithms cannot guarantee global maximization, and secondly, they are not computationally efficient for the applications under the scope of the paper. To remedy these disadvantages, the following approximation of the likelihood function is usually accepted [16, p. 185]:

| (1) |

involving the norm of the prediction error vector

| (2) |

i.e., a quadratic form w.r.t. the namely the LS criterion. The and are the vector and matrix designed according to some chosen windowing assumption [15, p. 217], [20, eq. (2)]. There are four possible forms: non-windowed (covariance method), pre-windowed, post-windowed, double-windowed i.e., pre- and post-windowed (autocorrelation method). Let us note the size of : , or , according to the chosen form. This choice is of importance since it strongly influences spectral resolution for short time analysis [15, p.225].

Whatever the chosen form, the maximization of (1) comes down to the minimization of (2) and yields:

| (3) |

As a prerequisite, the problem of choosing the model order must be tackled: has to be high enough to describe various PSD, and low enough to avoid spurious peaks, i.e., to ensure spectral smoothness. This compromise can usually be set by means of criteria such as FPE [21], AIC [22], CAT [23], or MDL [24], but, in the situation of prime interest here, they fail because the available amount of data is too small [25]. Actually, there exists no satisfying compromise in term of model order, since too few data are available to estimate DSPs with possibly complex structures.

III-B Adaptive spectral analysis

For the “multi range bin” analysis, the first idea consists in processing each bin independently: according to the LS approach, it amounts to minimize a global LS criterion:

| (4) |

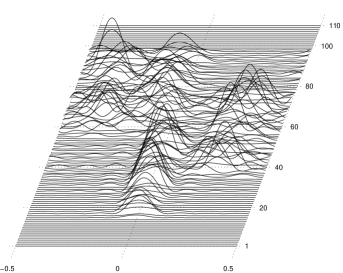

However, the resulting spectra hold unrealistic variations in the spatial direction (see Fig. 4). In order to remedy this problem, the Adaptive Least Squares (ALS) approach accounts for spatial continuity by processing the data from several bins, possibly in weighted form, to estimate each . A first approach uses a series of LS criteria including the data in a spatial window of length . A widely used alternative is the exponential decay memory which uses geometrically weighted LS criteria, with parameter . The latter is more popular because it is simpler: is merely incorporated into a standard recursive LS algorithm [15, p. 266]. In both cases, the degree of adaptivity, i.e., the spatial continuity is modulated by or .

III-C Conclusion

Whatever the variant, the main disadvantage of these approaches has to do with the parameter settings.

-

–

From the spectral standpoint, smoothness is introduced in a roundabout fashion, via the model order (adjusted by ) and the compromise no longer exists when the amount of data is reduced.

-

–

From the spatial standpoint, continuity is also indirectly introduced (and tuned by or ) and no automatic method for adjusting this parameters is available.

These limitations are unavoidable in the simple LS formalism, and to alleviate this problem we resort to the regularization theory. In this framework, the proposed approach

-

•

includes the spectral smoothness and spatial continuity in the estimation criterion itself;

-

•

allows long-AR model to be robustly estimated, and then various spectra to be identified;

-

•

provides automatic parameter setting, i.e., an entirely unsupervised method.

IV Long AR – spatial continuity – spectral smoothness

IV-A Spatial continuity model

IV-B Spectral smoothness model

The spectral smoothness measure proposed by Kitagawa & Gersch in [2] (see also [26]), is easily deduced from (6) as the distance to a constant DSP

| (7) |

According to [1, 2], , but as well as (6) and (7) can be extended to .

Remark 1

— Strictly speaking, and are not spectral distances nor spectral smoothness measures since they are not functions of the PSD itself. However, they are quadratic and this has two advantages: it considerably simplifies regressor calculations (see Section V) as well as regularization parameter estimation (see Section VI).

IV-C Double smoothness

IV-D Regularized least squares

IV-E Optimization stage

Several options are available to compute (11). Since is quadratic, is the solution of a linear system. Moreover, since the involved matrix is sparse, direct inversion should be tractable but not recommendable here (, ). Another approach may be found in gradient or relaxation methods [28] since is differentiable and convex. But, given the depth-wise structure, another algorithm is preferred: Kalman Smoothing (KS). So, we resort to the initial viewpoint of Kitagawa & Gersch in [2]. However, it is noticeable that [2] does not mention the minimized criterion, where as our KS is designed to minimize (IV-D).

V Kalman smoothing

V-A State-space form

-

–

The successive prediction vectors are related by a first-order state equation:

(13) in which each is a complex, zero-mean, circular, vector with covariance matrix and the -sequence, is depth-wise white.

-

–

The full state model also brings in the initial mean and covariance: the null vector and , respectively.

-

–

The observation equation is the recurrence equation for the AR model in each bin, written in compact form as

(14) i.e., a generalized version of the one proposed in [2], adapted to depth-wise vectorial data. Each is a complex, zero-mean, circular, vector with covariance ; the -sequence, is also depth-wise white.

Remark 4

— [2] accounts for spatial continuity by means of a special case of Eq. (13): . The latter has two drawbacks, though. Firstly, it is introduced apart from the idea of spectral smoothness. Secondly, from a Bayesian point of view, this equation is interpreted as Brownian process with an increasing variance, which may cause drifts to appear in the estimated spectra. On the contrary, the new coefficients can be chosen in order to ensure stationarity of the model (13) or to minimize the homogeneous criterion (IV-D).

V-B Equivalence between parameter settings

V-B1 Homogeneous criterion

This section establishes the formal link between the parameters of the KS ( and ) and those of the regularized criterion (IV-D) ( and ). [29, p.150–158] states that the KS associated to (13)-(14) minimizes:

| (15) | |||||

Partial expansions yield identification of (IV-D) and (15) through the following count-down recursion.

with . These equations allow to precompute the coefficients of the KS in order to minimize (IV-D).

V-B2 Limit model

This section is devoted to the asymptotic behavior of the -sequence. For the sake of notational simplicity, the sequence is rewritten in a count-up form:

| (16) |

It is clear that since . Let us introduce . It is straightforward that , so the entire -sequence remains in . Moreover, if it exists, the limit necessarily fulfills . Elementary algebra yields:

| (17) |

with . Finally, one can effortless see that we have , i.e., is a Lipschitz function with ratio in . Hence, the sequence effectively converges towards . It is also easy to see that the sequence is monotonous: increasing if and decreasing otherwise. In the present case, comparison of in (16) and in (17) shows that the -sequence is decreasing (in the count-up form), hence, is increasing.

Finally, since , the corresponding limit state power is given by:

| (18) |

V-B3 Associated stationary criterion

This section is devoted to the stationary limit model: the special case of Eq. (13), with and , i.e., a stationary first-order AR model for the -sequence. The initial power is denoted for notational coherence, even if it is not defined as a limit. It is actually defined according to and in order to ensure stationarity for the first-order AR model: .

Replacement of by in Eq. (15) yields the criterion minimized by the stationary KS:

where superscript “S” stands for stationary. Since we have: from Eq. (18) and from Eq. (17), one can effortless see that:

So, the stationary criterion and the initial homogeneous one are equal apart from the edge effects, i.e., two terms regarding the first and last regressors. As a consequence, the minimizer of and are practically equivalent and the latter is preferred since it does not require precomputation of the and .

V-C Kalman smoother equations

-

Initialization ()

(19) (20) -

Filtering phase (for )

-

–

Prediction step

(21) (22) -

–

Correction step

(23) (24) (25) (26) (27)

-

–

-

Smoothing count-down phase (for )

(28) (29) (30)

V-D Fast algorithm

Fast algorithms used to take a primordial position in the past decades, especially for real-time computations. More specifically, for adaptive spectral analysis of ultrasound Doppler signal, the Marasca algorithm [27] has been used in a real-time high-resolution velocimeter prototype. But, it has two drawbacks, resulting in a rigid spectral and spatial continuity tuning. On the one hand, it proceeds by blocks and incorporates spatial continuity by using the regressor of the current block as a prior mean for the next one; on the other hand, the fast version is developed only for the zero-order smoothness ().

To our knowledge, no fast algorithm exists for the KF in the configuration of interest, mainly because of the structures of the state equation and the smoothness matrix. However, fast algorithm may be developed on the basis of high-order displacement matrices [30]. More precisely, it is easy to see that the displacement matrix of order (if integer) is null for . Taking advantage of this property may result in a fast version of the proposed algorithm.

However, calculation time problems are now less crucial than they used. The standard KS algorithm only takes 111The proposed algorithm has been implemented using the computing environment matlab on a Personal Computer, Pentium III, with a 450 MHz CPU and 128 Mo of RAM. to process the entire data set of Fig. 1, so, real time computations can probably be achieved.

VI Hyperparameters estimation

The estimated -sequence and spectra sequence depend on hyperparameters: smoothness and AR orders and , power sequence , and two regularization parameters and .

VI-A Power parameters

The parameters are needed by the proposed RegLS method as well as the LS and ALS procedures and the same empirical estimates will be used for all of them. In the criterion (IV-D), parameters only act as weighting coefficients, so that the successive terms are of equivalent weight. The proposed empirical technique replaces the prediction error powers by the signal powers themselves. A simple empirical estimate could be used. However, since the estimation variance is high for , in practice, a more efficient technique consists in smoothing the sequence . Let us note that [2] proposes a scheme which is equivalent in principle.

VI-B Order parameters

The proposed framework allows to estimate long AR models to describe various spectral shapes. Moreover, by choosing the maximal order we get rid of the difficult problem of model order selection. In fact, as expected and confirmed in Section VII-C, as long as is large enough it does not affect significantly the spectral shape.

On the other hand, to our experience, the smoothness order does not affect the spectrum sequence provided that . So, the smoothness order is a priori tuned to , i.e., a first order derivative spectra penalization. Moreover, Section VII-C also provides a quantitative sensitivity study of the spectra sequence w.r.t. this parameter.

VI-C Regularization parameters

The problem of regularization parameter estimation within the proposed framework is a delicate one. It has been extensively studied and several techniques have been proposed and compared [31, 32, 33, 34, 35, 26]. The ML approach is often chosen within the Bayesian framework, mentioned in Remarks 2 and 3. The Gaussian likelihood function (1) and the Gaussian prior (9) together yield a Gaussian marginal law for the observed samples , i.e., the regularization parameter likelihood. The Hyperparameter-Co-Log-Likelihood (HCLL) is easily computed, for a given hyperparameter set, as a function of innovation vectors and covariances , i.e., two of the KF sub-products:

ignoring constant coefficients. This expression is the generalization of a more conventional identity, available for scalar observations [2]. The error covariance matrix is an matrix, possibly ranging from to , according to the windowing form and model order. Since is selected in the presented computations, no specific algorithm has been developed for inversion nor determinant calculations.

The ML estimate:

| (31) |

can be computed by means of several algorithms: coordinate/gradient descent algorithm [28] or EM algorithms [36, 37], but none of them can ensure global optimization. Here, the optimization stage is tackled by means of a coordinate descent algorithm with a golden section line search [28]. Since is a function of two variables only, the optimization stage only requires about 10 .

VII Simulation results and comparisons

The present section assesses the effectiveness of the proposed method, compared to the usual ones by processing the example shown in Fig. 1.

VII-A Quantitative comparison criterion

Since the true spectrum sequence is known in the presented simulations, quantitative criteria are computable on the basis of distances between estimated spectra and true ones , accumulated over the bins. Normalized distances:

with and have been computed. The normalization is chosen so that a null estimated spectrum results in a 100% error. Practically, the integrals are approximated by discrete summation over the frequency domain with .

VII-B Tuning parameters

VII-B1 Usual methods

Since no automatic parameters tuning is available for usual methods, these parameters have been chosen in order to produce the best distance. Moreover, we have checked that such a quantitative procedure finds itself in good agreement with the visual appreciation.

-

–

First of all, it is noticeable that, even for a short model, the non-windowed and pre-windowed methods systematically yield numerous spurious peaks. The best results have been obtained with the post-windowed form222A possible explanation for this rather counterintuitive fact, is that the post-windowed form is somewhat ”self penalizing”, i.e., the corresponding criterion incorporates quadratic penalization terms: , where only depends upon the data. (double-windowed behaves similarly) so, the estimated spectra are of poor resolution [15, p.225].

-

–

As expected, since the true spectra show up to three modes, the best results have been obtained with for both LS and ALS.

-

–

Finally, as far as the ALS method is concerned, has been selected.

VII-B2 Regularized method

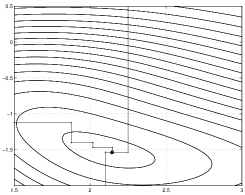

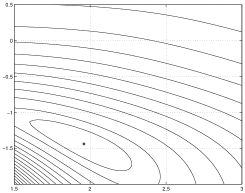

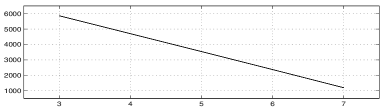

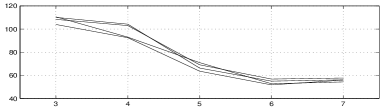

The HCLL function has been computed on a fine discrete grid of values between and for and between and for . The result is the HCLL sheet shown in Fig. 2-lhs. It is fairly regular, and exhibits a single minimum at and . Moreover, Fig. 2-rhs shows the corresponding distances and the strikingly similar behavior of and is a strong argument in favor of the likelihood as a criterion for parameters tuning.

However, it must be mentioned that a variation of on decade on or entails a nearly imperceptible variation in the estimated spectra and a fraction of percent error. This point is especially important for qualifying the robustness of the proposed method. Contrary to the choice of model order in the usual AR analysis, which is critical, the choice of offers broad leeway and can be made reliably.

Practically, the adjustment is set using the coordinate descent algorithm and Fig. 2-lhs illustrates its convergence, from three different starting points.

VII-C Order sensitivity

This subsection assesses the sensitivity of the method w.r.t. the order parameters and . For to and for to (step .25), we have computed the ML estimate (31):

and the corresponding optimal likelihood and distance

They are plotted in Fig. 3, as a function of for the several values of .

As far as the likelihood is concerned,

-

•

is a decreasing (almost linear) function of model order : the ML selected order is the maximal one .

-

•

does not depend on (the four curves are over plotted) so that, given the triplet “over-parameterize” the likelihood and is indifferent.

As far as the is concerned, it still behaves similarly to the likelihood: it is roughly decreasing with and not depending upon . As a conclusion, the maximization of the likelihood w.r.t. and does not provide any improvement and the recommended scheme described in Section VI-B is an efficient one.

VII-D Qualitative evaluation

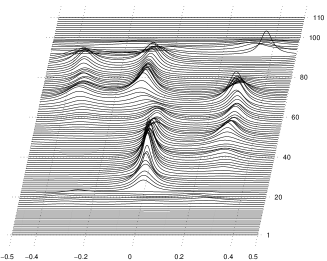

We have then compared the usual methods at their best (optimally adjusted parameters knowing the true spectra) with the proposed method (automatic selection of regularization parameters without knowledge of the true spectra). The results obtained by LS, ALS, and RegLS are presented in Fig. 4. A simple qualitative comparison with the reference Fig. 1 already leads to four conclusions.

-

–

The ML strategy provides a good value for the regularization parameters and the (and ) distance is in accordance with the qualitative assessment.

-

–

The effect of the regularization is obvious. Estimated spectra are in a much greater conformity with the true ones. The spectrum shapes are reproduced more precisely, in one, two or three modes. Their positions and their amplitudes are correctly estimated.

-

–

Moreover, the spectral resolution for the ground clutter is strongly enhanced. It is essentially due to the coherent accounting for spectral and spatial continuity resulting in a robust non-windowed form.

- –

| Method | ||

|---|---|---|

| Periodogram | 87.1% | 92.9% |

| Best LS | 76.6% | 85.4% |

| Best ALS | 66.4% | 75.5% |

| ML & RegLS | 57.9% | 69.2% |

VII-E Quantitative evaluation

In the non adaptive context, quantitative comparisons have previously been performed in [1, 26]. The adaptive extension originally proposed by Kitagawa & Gersch has also been quantitatively assessed in [2].

For the proposed method, quantitative comparison have been achieved by evaluating and distances between true and estimated spectra. The results are listed in Table I and show an improvement of about 10% form periodogram to best LS, 10% from best LS to best ALS and 10% from best ALS to the entirely automatic proposed method.

VIII Conclusion and perspectives

This paper tackles short-time adaptive AR spectral estimation within the regularization framework. It proposes a new regularized least squares criterion accounting for spectral smoothness and spatial continuity. The criterion is efficiently optimized by a special Kalman smoother. In this sense, the present study significantly deepens the contributions of [1, 2], given that the latter separately address spectral smoothness and spatial continuity. Moreover, the proposed method is entirely unsupervised and it is shown that maximum likelihood regularization parameters is both formally achievable and practically useful. Finally, a simulated comparison study is proposed in the field of Doppler radars. It shows an improvement of about 10%, comparing some usual methods at their best versus the entirely automatic proposed one.

Future works will be devoted to compensate for the over-smoothing character of quadratic regularization in the presence of spatial breaks. [41] accounts for spatial continuity while preserving breaks by way of a non-Gaussian state model and extended KF algorithms. In our mind, a preferable approach could be to introduce non-quadratic convex penalty terms and to minimize the resulting criterion using descent algorithms [38, 39, 42].

Acknowledgements

Jean-François Giovannelli is grateful to Mr Grün and Mrs Groen for their expert editorial assistance.

References

- [1] G. Kitagawa and W. Gersch, “A smoothness priors long AR model method for spectral estimation”, IEEE Trans. Automat. Contr., vol. AC-30, no. 1, pp. 57–65, January 1985.

- [2] G. Kitagawa and W. Gersch, “A smoothness priors time-varying ar coefficient modeling of nonstationary covariance time series”, IEEE Trans. Automat. Contr., vol. AC-30, no. 1, pp. 48–56, January 1985.

- [3] Y. Grenier, “Modèles arma à coefficients dépendant du temps”, Traitement du Signal, vol. 3, no. 4, pp. 219–233, 1986.

- [4] R. Kuc, “Employing spectral estimation procedures for characterizing diffuse liver disease”, in Tissue Characterization with Ultrasound, chapter 6, pp. 147–166. 1986.

- [5] J. Idier, J.-F. Giovannelli, and B. Querleux, “Bayesian time-varying ar spectral estimation for ultrasound attenuation measurement in biological tissues”, in Proceedings of the Section on Bayesian Statistical Science, Alicante, Spain, 1994, pp. 256–261, American Statistical Association.

- [6] P. Péronneau, Vélocimétrie Doppler. Application en pharmacologie cardiovasculaire animale et clinique., Édition INSERM, Paris, France, 1991.

- [7] D. K. Barton and S. Leonov, Radar Technology Encyclopedia, Artech House, Inc., Boston-London, 1997.

- [8] G. Le Foll, P. Larzabal, and H. Clergeot, “A new parametric approach for wind profiling with Doppler radar”, Radio Science, vol. 32, no. 4, pp. 1391–11408, July-August 1997.

- [9] J. M. B. Dias and J. M. N. Leitão, “Nonparametric estimation of mean Doppler and spectral width”, IEEE Trans. Geosci. Remote Sensing, vol. 38, no. 1, pp. 271–282, January 2000.

- [10] N. Allan, C. L. Trump, D. B. Trizna, and D. J. McLaughlin, “Dual-polarized Doppler radar measurements of oceanic fronts”, IEEE Trans. Geosci. Remote Sensing, vol. 37, no. 1, pp. 395–417, January 1999.

- [11] F. Barbaresco, “Turbulences estimation with new regularized super-resolution Doppler spectrum parameters”, in RADME, Rome, Italy, June 1998.

- [12] M. Basseville, N. Martin, and P. Flandrin, Méthodes temps-fréquence et segmentation de signaux, vol. 9 of Numéro spécial de Traitement du Signal, JOUVE, Paris, France, 1992.

- [13] J. B. Allen, “Short term spectral analysis, synthesis, and modification by discrete Fourier transform”, IEEE Trans. Acoust. Speech, Signal Processing, vol. ASSP-25, no. 3, pp. 235–238, June 1977.

- [14] J. B. Allen and L. R. Rabiner, “A unified approach to short-time Fourier analysis and synthesis”, Proc. IEEE, vol. 65, no. 11, pp. 1558–1564, 1977.

- [15] S. L. Marple, Digital Spectral Analysis with Applications, Prentice-Hall, Englewood Cliffs, nj, 1987.

- [16] S. M. Kay, Modern Spectral Estimation, Prentice-Hall, Englewood Cliffs, nj, 1988.

- [17] B. Picinbono, Éléments de probabilité, vol. 1127, Cours de supélec, Gif-sur-Yvette, France, 1991.

- [18] S. M. Kay, “Recursive maximum likelihood estimation of autoregressive processes”, IEEE Trans. Acoust. Speech, Signal Processing, vol. ASSP-21, pp. 56–65, 1983.

- [19] D. T. Pham, “Maximum likelihood estimation of the autoregressive model by relaxation on the reflection coefficients”, IEEE Trans. Signal Processing, vol. 36, no. 8, pp. 1363–1367, 1988.

- [20] S. M. Kay and S. L. Marple, “Spectrum analysis – a modern perpective”, Proc. IEEE, vol. 69, no. 11, pp. 1380–1419, November 1981.

- [21] H. Akaike, “Statistical predictor identification”, Ann. Inst. Stat. Math., vol. 22, pp. 207–217, 1970.

- [22] H. Akaike, “A new look at the statistical model identification”, IEEE Trans. Automat. Contr., vol. AC-19, no. 6, pp. 716–723, December 1974.

- [23] E. Parzen, “Some recent advances in time series modeling”, IEEE Trans. Automat. Contr., vol. AC-19, no. 6, pp. 723–730, December 1974.

- [24] J. Rissanen, “Modeling by shortest data description”, Automatica, vol. 14, pp. 465–471, 1978.

- [25] T. J. Ulrych and R. W. Clayton, “Time series modelling and maximum entropy”, Phys. Earth Planetary Interiors, vol. 12, pp. 188–200, 1976.

- [26] J.-F. Giovannelli, G. Demoment, and A. Herment, “A Bayesian method for long ar spectral estimation: a comparative study”, IEEE Trans. Ultrasonics Ferroelectrics Frequency Control, vol. 43, no. 2, pp. 220–233, March 1996.

- [27] A. Houacine and G. Demoment, A Bayesian method for adaptive spectrum estimation using high order autoregressive models, pp. 311–323, Mathematics in Signal Processing II. Clavendon Press, Oxford, uk, J.G. McWhirter edition, 1990.

- [28] D. P. Bertsekas, Nonlinear programming, Athena Scientific, Belmont, ma, 1995.

- [29] A. H. Jazwinski, Stochastic process and filtering theory, Academic Press, New York, ny, 1970.

- [30] A. H. Sayed and T. Kailath, “A state-space approach to adaptive RLS filtering”, IEEE Trans. Signal Processing Mag., pp. 18–60, July 1994.

- [31] G. H. Golub, M. Heath, and G. Wahba, “Generalized cross-validation as a method for choosing a good ridge parameter”, Technometrics, vol. 21, no. 2, pp. 215–223, May 1979.

- [32] D. M. Titterington, “Common structure of smoothing techniques in statistics”, Int. Statist. Rev., vol. 53, no. 2, pp. 141–170, 1985.

- [33] P. Hall and D. M. Titterington, “Common structure of techniques for choosing smoothing parameter in regression problems”, J. R. Statist. Soc. B, vol. 49, no. 2, pp. 184–198, 1987.

- [34] A. Thompson, J. C. Brown, J. W. Kay, and D. M. Titterington, “A study of methods of choosing the smoothing parameter in image restoration by regularization”, IEEE Trans. Pattern Anal. Mach. Intell., vol. PAMI-13, no. 4, pp. 326–339, April 1991.

- [35] N. Fortier, G. Demoment, and Y. Goussard, “gcv and ml methods of determining parameters in image restoration by regularization: Fast computation in the spatial domain and experimental comparison”, J. Visual Comm. Image Repres., vol. 4, no. 2, pp. 157–170, June 1993.

- [36] R. Shumway and D. Stoffer, “An approach to time series smoothing and forecasting using the em algorithm”, J. Time Series Analysis, pp. 253–264, 1982.

- [37] S. E. Levinson, L. R. Rabiner, and M. M. Sondhi, “An introduction to the application of the theory of probabilistic function of a Markov process to automatic speech processing”, Bell Syst. Tech. J., vol. 62, no. 4, pp. 1035–1074, April 1982.

- [38] C. A. Bouman and K. D. Sauer, “A generalized Gaussian image model for edge-preserving map estimation”, IEEE Trans. Image Processing, vol. 2, no. 3, pp. 296–310, July 1993.

- [39] P. J. Green, “Bayesian reconstructions from emission tomography data using a modified em algorithm”, IEEE Trans. Medical Imaging, vol. 9, no. 1, pp. 84–93, March 1990.

- [40] L. Rudin, S. Osher, and C. Fatemi, “Nonlinear total variation based noise removal algorithm”, Physica D, vol. 60, pp. 259–268, 1992.

- [41] G. Kitagawa, “Non-Gaussian state-space modeling of nonstationary time series”, J. of the American Statistical Association, Theory and Methods Section, vol. 82, no. 400, pp. 1032–1041, December 1987.

- [42] J. Idier, “Convex half-quadratic criteria and interacting auxiliary variables for image restoration”, IEEE Trans. Image Processing, vol. 10, no. 7, July 2001.