A queueing theory description of fat-tailed price returns in imperfect financial markets

HARBIR LAMBA111Department of Mathematical Sciences, George Mason University, MS 3F2, 4400 University Drive, Fairfax, VA 22030 USA

Abstract

In a financial market, for agents with long investment horizons or at times of severe market stress, it is often changes in the asset price that act as the trigger for transactions or shifts in investment position. This suggests the use of price thresholds to simulate agent behavior over much longer timescales than are currently used in models of order-books.

We show that many phenomena, routinely ignored in efficient market theory, can be systematically introduced into an otherwise efficient market, resulting in models that robustly replicate the most important stylized facts.

We then demonstrate a close link between such threshold models and queueing

theory, with large price changes

corresponding to the busy periods of a single-server queue. The distribution

of the busy periods is known to have excess

kurtosis and non-exponential decay under various assumptions on the

queue parameters. Such an approach may

prove useful in the development of mathematical models for rapid

deleveraging and panics in financial markets, and the

stress-testing of financial institutions.

PACS numbers 89.65.Gh 89.75.Da

1 Introduction

Economists and physicists have uncovered seemingly universal statistical properties of real markets, many of which deviate from those predicted by assumptions of market efficiency. These are often referred to as the ‘stylized facts’ [9, 21] and there now exist many different heterogeneous agent models (HAMs) that can replicate the most important ones: the lack of correlations in the price-returns at all but the shortest timescales; apparent power-law decays for the frequency of large magnitude price changes ; and volatility clustering. It is not our intention to review the vast HAM literature here (a valuable overview can be found in [23]) but many of the models suffer from one or more of the following (related) problems.

Firstly, they tend to be constructed without due regard to the actual process by which agents arrive at their chosen course of action. This makes it difficult to argue why one model should be preferred over another which in turn makes it harder to convince orthodox economists to take any of them seriously.

Secondly, at the level of individuals, many of the recent findings of behavioral economics [18, 13, 17, 6] are ignored. Similarly, larger-scale market structures and institutions may have rational-but-complex motivations and perverse incentives that are also overlooked.

A third common problem is that agents are treated as Markovian in the sense that their recent past does not influence their future behavior. It occurs in those models that, for example, probabilistically switch agents between investment positions or trading strategies[2, 1].

Finally, many models are sensitive to the size of the system and when the number of agents some of the stylized facts, such as excess kurtosis, can even disappear altogether. A frequent cause of this modelling issue is related to the Markovian modelling of the agents mentioned above — the Central Limit Theorem and The Law of Large Numbers remove any endogenous fluctuations in the continuum limit.

Previous work [11, 10, 12, 20] has shown that the use of price thresholds to trigger agent activity bypasses these problems while allowing for the modelling of multiple real-world phenomena in a plausible and consistent manner. Furthermore, an efficient market (where the price follows a geometric Brownian Motion) exists as a special case within this framework which makes possible a systematic study of the ways in which irrational behavior and other ‘imperfections’ may perturb such hypothetical solutions.

The two main contributions of this paper are, firstly, to extend and better justify the moving threshold models first introduced in [20] and, secondly, to show that queueing theory [7] may provide both insights and analytical tools for studying the fat-tailed price returns generated by such threshold models. This is because the largest price changes are caused by cascades of buying or selling and their distribution can be reinterpreted as the distribution of the busy-period of a single-server queue — the length of time for which a queue exists after it has begun. There are various established results concerning the excess kurtosis and non-exponential decay of this random variable under very general assumptions on the arrival rate, departure rate and service time of customers. While none of these extant results from queueing theory apply precisely to the more complicated situation in market models, the correspondence is close enough to suggest a common underlying mathematical explanation for the presence of power-laws and fat-tails in both types of system.

The paper is organized as follows. Section 2 provides a better motivation for the moving threshold models first introduced in [20]. In particular, a separation of timescales argument is used to justify the main modeling assumptions. It is then shown how the rules governing the threshold dynamics can mimic many phenomena that are neglected in efficient/rational market models. It is especially interesting to introduce those very simple rules and behaviors that induce coupling between agents’ trading strategies into an otherwise efficient market. Power-law fat-tailed price returns and volatility clustering consistent with the stylized facts are robustly generated.

The class of models in Section 2 assumes a separation of timescales and operates over long time periods. However, the fast cascade processes responsible for the largest price changes can also be viewed as a stand-alone model for very rapid price-deleveraging or market panics, say. Thus, in Section 3 we consider such cascades and, after a brief overview of queueing theory, demonstrate the very close connection between the two. Standard queueing theory results concerning the distribution of the busy-period of single-server queues then suggest a novel, but incomplete, explanation of the fat-tailed nature of price returns in financial markets.

2 A Threshold Model Over Long Timescales

2.1 A continuous-time model

We consider a market with asset or index price at (continuous) time and introduce a separation of timescales. Information arrives continuously and results in instantaneous price changes that are implemented by ‘fast’ agents who are primarily motivated by such new information rather than price (these agents will not be simulated directly in the time-discretized version since they operate over very small timescales). There are also, however, ‘slow’ agents, who are motivated primarily by price changes, and act over much longer timescales (typically weeks or months). Each of these agents can be either own (the state ) or not own (the state ) the asset at any given moment.

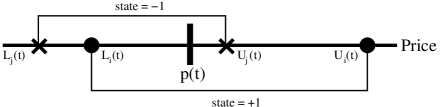

At time the slow agent is represented by its state, , and an interval where (see Figure 1). Whenever crosses either endpoint of this interval, agent is deemed to be no longer comfortable with her current investment position, switches states, and the interval is updated so that is again an interior point. Also, the action of switching causes a small jump in the price caused by the change in buy/sell pressure. Thus at time the system is represented by the price , the states of the agents, and closed intervals each of which includes the value .

We shall refer to the endpoints of the intervals as thresholds and the behavior of the system will be defined by rules governing both the dynamics of and the thresholds. Before describing the kinds of rules that can be incorporated into such a framework a few general remarks are in order.

The above model bears a resemblance to order-book models [24] that attempt to describe how trades are cleared. In such models, the price typically moves along the positive real line and potential buyers and sellers are matched when the price is acceptable to both parties. However, the differences are more profound than the similarities. Order-book models are concerned with very short timescales and how trades are executed. Here we are concerned with much longer timescales and why trades are placed — it is implicitly assumed that the market is liquid (the fast sellers provide the necessary pool of liquidity) and all trades can be executed without explicitly matching buyers and sellers.

2.2 A discrete-time version

We require time-discretized models that are suitable for computer simulations. First a timestep is chosen, typically less than one trading day. The state of the slow agent over the time interval is represented by . The price of the asset at the start of the time interval is and for simplicity the system is drift-free so that actually corresponds to the price relative to the risk-free interest rate plus equity-risk premium or the expected rate of return. We do not assume that agents are of uniform size (in terms of their trading positions) and thus weight the agent by its size and define . A key variable is the sentiment defined as the weighted average of the states of all of the investors

| (1) |

and .

The price evolves according to the rule

| (2) |

where and represents the exogenous information stream. Note that when and the price follows a geometric Brownian motion (the term is the drift correction required by Itô calculus). The function allows the effect of new information on the marketplace to vary and is discussed further below but note that if then the pricing formula (2) is simply a geometric Brownian motion modified by a linear supply/demand correction due to the sentiment of the slow agents.

The rules governing the dynamics of the thresholds are implemented as follows. The thresholds for each agent change (usually slowly) between switchings and correspond to that agent’s evolving strategy. If, at the end of a timestep, an agent’s interval is crossed by the price, then that agent switches and the corresponding change in will feed into the price at the next iteration. This choice of synchronous updating is made for two reasons — it is computationally convenient but also reflects the fact that even after a slow trader decides to react, there is likely to be some delay in effecting the trade (unlike the fast traders). In the simulations that follow, is chosen to correspond to 1/10 of a day and then the daily price returns are computed).

As general as the above framework is, it can be made more realistic by allowing agents to own differing amounts of the asset, and perhaps even shorting. This can be achieved by assigning an (evolving) weight value to each threshold (upper and lower, separately) such that when that threshold is breached the agent buys or sells so as to own that amount of stock. However useful this may prove to be in the future, it will not be considered here.

It is important to note that the model has two fundamental, and essentially separable, components — one governs the motion of the price , given by (2), and the other governs the motion of the thresholds. Or, equivalently, one set of rules describes the fast agents and the other describes the slow ones. We now discuss which phenomena can be incorporated into such a model.

Firstly, in the pricing formula (2) the law of supply and demand is reproduced for — increasing/decreasing causes the price to rise/fall. Its magnitude (relative to ) determines the extent to which price changes are determined by changes in sentiment versus the arrival of new information. If the function then the fast traders are accurately and instantly converting information into price changes. We posit, however, that this is not necessarily the case. For example during times of extreme sentiment may be greater, perhaps due to a surplus of speculators [8] or excessive attention being paid to information in an environment where market conditions are perceived to be due for a correction of some kind. This mechanism is undoubtedly too simplistic but nevertheless tying volatility to sentiment in this way results in realistic volatility clustering [20]. Or one can instead introduce an explicit dependence of upon to create changes in market conditions with time or to use a stochastic volatility model. And of course it is still being assumed that the information stream is Gaussian and uncorrelated with itself — weakening these highly unrealistic assumptions provides additional mechanisms for volatility clustering. In actual markets, all of these mechanisms are probably present to some degree or another, and will be considered in more detail elsewhere.

2.3 Introducing market ‘defects’ using thresholds

The focus of this paper is on the fat-tailed price returns, and previous results [11, 12, 20, 19] suggest that these are caused by the thresholds and their dynamics rather than the pricing mechanism.

Let us start by assuming that ; that the threshold distributions of the agents are perfectly mixed along the priceline at ; and that the threshold rules for agents in either state are identical and simply geometric Brownian motion. Then will not move away from zero since equal numbers of slow agents are switching between the two states and so reduces to a geometric Brownian process. Thus this special case corresponds to a weakly-efficient market [15] with no possibility of predicting future prices from prior ones.

This base model is also very closely related to the concept of rational expectations (in the sense of [22]) which relies upon the assumption that the predictions and expectations of all the agents are, on average, correct. In other words, there are no systemic biases or dependencies between agents’ strategies which are treated as Gaussian fluctuations around the ‘correct’ one222This assumption is used in macroeconomics to justify the use of a single ‘representative agent’ to model an entire economy.. Thus, interpreting the random motions of the slow agents’ thresholds in the above model as, in fact, being the result of arbitrarily complex computations to maximize individual utility functions gives a model that is, practically and philosophically, very close to the neoclassical paradigm.

But, by allowing for a wider range of threshold dynamics, we can replicate many different effects observed in real agents and real markets — and in doing so violate the above assumptions of independence and lack of systemic bias in agents’ strategies.

Suppose first that agent is perfectly rational then the values and represent the cumulative effect of rigorous market analysis and future expectations. Thus the price interval defines that agent’s (conscious, or algorithmic in the case of a trading program) strategy. Or in the case of a less-than-perfectly-rational individual the price interval still represents a de facto strategy, but one that the agent herself may not be fully aware of. The rules governing the dynamics of the threshold values may be as complicated as desired, simultaneously incorporating amongst many other things: rational strategies based upon optimization of utility functions or econometrics or technical analysis; past performance; adaptive heuristics; inductive learning; new information; tax issues; price data from alternative investment options; margin calls; perverse incentives; recent market volatility (perhaps then influencing future volatility); psychological effects; the weather; herding; imitation within a subset of closely-networked agents; and all the key findings of behavioral economics.

Thus another working assumption is that all such effects are cumulative and can be applied to a single pair of thresholds — some effects will move a particular threshold inwards towards the current price (making it more likely that that threshold will be breached and the agent will switch) while others will move it outwards. In other words we are hypothesizing that a slow agent’s past experiences, present state and future expectations can be condensed into two price values, one on either side of the current price, together with the current state of the agent. Information about the agent’s state, threshold values and threshold dynamics are all carried over from one timestep to the next.

Thresholds are especially well-suited for incorporating some important aspects of agent behaviors and motivations in a very natural way. By ensuring that they are reset away from the current price after a switching, agents cannot switch arbitrarily often (which will be the case in the presence of non-negligible transaction costs). Similarly included is the ‘anchoring’ phenomenon whereby the price at which the agent last traded influences the value they place upon the asset and thus the price at which they next trade. In a similar vein, chartists and technical analysts have developed many observational rules to help them predict future market performance. A particularly simple kind concerns the existence of ‘resistance levels’ which, if breached, indicate a further price move in the same direction. If such an effect does indeed exist then it can be applied to the threshold dynamics of a subset of the agents (or it may even arise as a natural consequence of other rules). Taking this one step further, a subset of agents may be influenced by important-sounding numbers, such as 10000 on the DJIA, and consciously-or-not have a threshold at around that value333Or assume that other, less rational, agents will be affected by it (as in Keynes’ beauty contest) and so assign a significance to it themselves. In either case, the effect is the same!. As another (extreme but not uncommon) example consider an individual who bought a dot-com stock at the top of the tech-bubble and then held it all the way down to zero. In such a case, that agent’s lower threshold decreased (due to loss aversion) even faster than the price while the upper threshold didn’t decrease fast enough and so the stock was never sold. At the more rational end of the spectrum, a rational investor or computerized trading program (fundamentalist trader) that believes the current price to be too high, with no other complicating factors, will enter state (if necessary) and then can be mimicked by setting the lower threshold at some point below the appraised price level and the upper level arbitrarily high.

However the phenomenon that appears to be most important in the generation of fat-tails within threshold models is herding, whereby there is a tendency for (rational or otherwise) agents in the minority position to switch and join the majority. This can be incorporated into threshold dynamics in a very simple manner — agents in the minority position have their thresholds move inwards towards the current price thus making them more likely to switch and join the majority (unless the majority state changes first). Different agents have differing herding propensities that are reflected in the rate at which their thresholds move together.

Herding may be initiated, for example, by a widespread misconception about the present or the future (such as house prices never going down) or some systemic asymmetry444For example the perverse incentives induced by inappropriate fee structures, or the moral hazard that occurs when the risk of a certain investment position is reduced, removed or transferred. that causes agents to prefer one of the states over the other. Herding then provides a plausible positive-feedback mechanism. However, it must be emphasized that for many agents herding is a rational, not irrational, phenomenon. Indeed herding in the natural world is an effective survival strategy and the same is true in financial markets (as well as being a trading strategy in itself, often referred to as momentum trading). Professional investors risk losing their jobs, bonuses and/or investment capital if they deviate too far from the mean in what turns out to be the wrong direction. Thus there is a strong motivation to play safe and ‘chase the average’. This naturally (and rationally from the point of view of the agents themselves) also leads to herding.

2.4 Numerical Simulations

It is not the purpose of this paper to provide a detailed numerical investigation since results from a similar model (using two pairs of static thresholds for each agent) are compared against the stylized facts in [19] and further numerical results for a moving threshold model can be found in [20]. However, for completeness, we provide enough details for reproduction of the numerical results and highlight the main findings of previous studies.

The model is kept as simple as possible and so apart from including herding and a volatility function we assume that agents thresholds are reset after a switching from a specified random distribution.

The timestep is defined in terms of the variance of the external information stream. A daily variance in price returns of 0.6–0.7% implies that of 0.000004 should correspond to approximately 1/10 of a trading day. The results of 10 consecutive timesteps are then combined to give the daily price return.

The parameter and all agents have equal weight. The reset thresholds after a switching at price are where are each chosen from the uniform distribution on the interval , corresponding to price moves in the range 5–25%. The model is very robust to changes in these parameters and in the absence of further information they are chosen to be as simple as possible.

The thresholds of all agents are subject to a random, driftless, component governed by a quantity . Herding is introduced by supposing that for agents in the minority position only

while for those in the majority

Note that the drift in the position of the thresholds is proportional to the length of the timestep and the magnitude of the sentiment. The constant of proportionality is different, but fixed, for each agent and chosen from the uniform distribution on . This range of parameters corresponds to a herding tendency that operates over a timescale of a few months or longer.

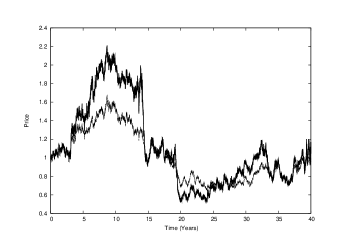

Figure 2 shows the price output of the model (the more volatile curve) against the ‘efficient’ pricing (less volatile) obtained from (2) by setting and with .

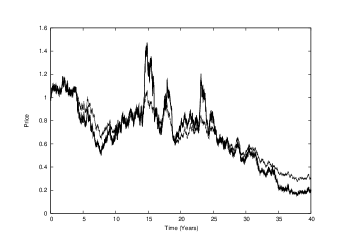

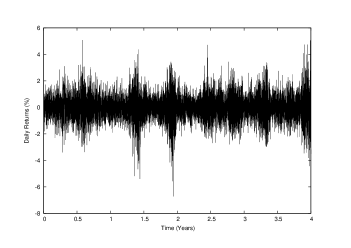

Figure 3 shows a simulation with but all other parameters unchanged, emphasizing that the results do not depend critically upon the system size while Figure 4 shows the daily percentage returns for the simulation in Figure 2.

Measurements of power-law exponents, similar to those carried out in [19], provided estimates close to those observed in analyses of price data from real markets for the tail of the price returns and the decay of the volatility autocorrelation function, typically in the range .

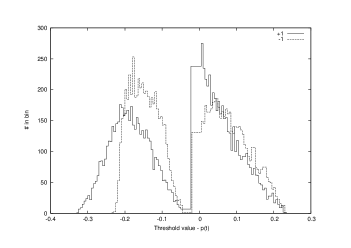

In the absence of herding, i.e. when , then, provided that the initial states of the agents are sufficiently mixed, and always remains close to the efficient market price. Such a model is both practically and philosophically recognizable as the neoclassical notion of an efficient market — agents trade due to differing expectations but the averaging procedure inherent in the rational expectations assumption is valid and no mispricing occurs. However, Figure 5 is a snapshot of the system for the simulation of Figure 2 (herding included) at a point in time when . The two displayed histograms are the density of thresholds for agents in the two states and plotted separately. The main point to note is the discrepancy between the two density functions which indicates that as the system evolves and the price fluctuates, will move away from 0 because the agent thresholds are not perfectly mixed.

Finally we note that in the above simulation there are different causal mechanisms for the volatility clustering and fat-tails. If (i.e. the fast agents are correctly interpreting new Gaussian information) then herding induces fat-tails but there is no volatility clustering. Thus the systemic bias of the slow agents cause fat-tails while the imperfect interpretation of information by the fast agents results in volatility clustering555However, more sophisticated threshold dynamics for the slow agents that are also functions of recent price volatility may provide a further mechnism for volatility clustering.

3 A Queueing Theory Description of Price Cascades over Short Timescales

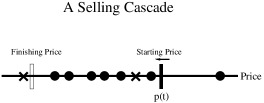

We are interested primarily in the tail-distribution of price returns. Since the information stream is modelled as Gaussian, extreme price moves are due to cascades of buying or selling affecting (2) with . Without loss of generality we shall consider a selling cascade. Figure 6 shows the start of such a possible selling cascade within the threshold model of Section 2. The circles and crosses to the left of the current price indicate the positions of the lower thresholds of the slow agents.

There are four points to consider before proceeding. Firstly, Figure 6 can act as a stand-alone model of a rapid deleveraging process. As the price falls and passes the lower thresholds of agents who are in the state, they switch to the state pushing the price down further (if ) and triggering other agents to sell and so on (note that these lower thresholds may in reality be the pricing points at which margin calls are activated). Secondly, under the most extreme market conditions, the distinction between fast and slow agents made in Section 2 may be invalid as the amount of new information entering the system is negligible and all the agents are motivated by price changes. In this case will be equal to the total number of agents, not just the number of slow ones, and the model more closely resembles an order book. Thus the link to queueing theory outlined below may also be useful in the context of those models.

Thirdly, as shown in Figure 5, the distribution of thresholds is a result of the evolution of the system over a long period of time and will in general be highly non-uniform over the positive real line. Finally, although we are supposing that the cascade/relaxation process is instantaneous, in practice this is certainly not the case and agents’ thresholds may move significantly between the start of the cascade and the end.

We consider the continuous-time version of the model outlined at the start of Section 2 and it will also be convenient to introduce the log-price . At the start of the cascade the price is fluctuating due to the arrival of new information and the action of the fast traders. Then at some value it equals one of the thresholds of agent who is in the state. We now consider the cascade to be a relaxation process that occurs instantaneously. The log-price jumps downwards by an amount as the agent switches and its thresholds jump to a non-zero distance away. If there is no other agent with its lower threshold in the interval then the cascade stops immediately. If there is such an agent, or agents, then the cascade continues. During the relaxation process, there may be agents in the opposite state caught in the cascade whose switching will act in the opposite price direction and help to bring the cascade to an end. Once the cascade is over, time restarts and evolves under the action of the information stream until another threshold is met.

Now consider the following scenario from queueing theory [7]. A customer, named , arrives at an empty single-server queue. If she is served before another customer arrives then the busy period of the queue, defined to be the length of time it is in existence, is simply the time taken to serve her, call it . If on the other hand other customers arrive before she is served then the queue continues until they are all served. However, we must also allow for the possibility that some people in the queue may decide to leave it before being served — this is referred to in the queueing theory literature as reneging.

There exists an almost exact correspondence between these two situations. Price in the market model corresponds to time in the queueing problem, the size of the trade the agent wishes to make corresponds to the length of time taken to serve that customer, and the overall price change during the cascade maps to the busy period of the queue. Agents in the opposite state caught up in the cascade act as ‘anti-customers’ whose arrival in the queue causes them to cancel out with an agent, or agents, of the same total weight/service time. This is of course equivalent to those agents deciding to renege and leave the queue. A subtle, but negligible, difference is that in the market cascade an agent in the opposite state getting caught up in the process should correspond to a customer, or customers, of the same total ‘size’ reneging from the queue. But if is sufficiently large then there may not be enough total weight in the queue for this to happen (i.e. at the end of a selling cascade a small ‘bounce’ may occur in the price but customers who have already been served cannot leave a queue).

Queueing theory has a standard notation for describing queues. A queue (without reneging) is where describes the distribution of arrivals, the serving times and is the number of servers. Below we shall only consider cases where or and . corresponds to exponentially-distributed arrival or service times generated by a Poisson process while is a general distribution, usually under some assumption of finite moments. In the case of an queue the Poisson parameters for and are and respectively.

We now state some results from queueing theory concerning the distribution of the busy period under progressively weaker assumptions. While none of these results apply directly to price cascades under all circumstances, they may be indicative of an underlying explanation for the apparent universality of sub-exponential decays in price returns [21].

First consider an queue without reneging. Using standard arguments [7], if then the busy period of the queue is finite with probability 1 and the entire distribution is given by

| (3) |

where is the first modified Bessel function of the first kind. Furthermore explicit formulae exist for the moments and

| (4) |

(generalizations for queues with various reneging assumptions

can be found in [16]).

In fact (4) holds for

queues without reneging if . The generalization

of (3) to queues is provided by the

Takacs Equation:

if is the Laplace-Stieltjes transform of the cumulative

density function of then

satisfies

| (5) |

This functional equation establishes close connections between the tail of the service times and the tail of the busy period distribution [14] (see also [26, 5, 16]). In particular, the tails of the service time distribution (ie. the distribution of agent sizes) and the tails of the busy period (price changes) obey the relationship

where and is subexponential with for some slowly-varying function . Such results are of interest because of the observed power-law distributions of sizes in many socio-economic and financial systems. However it should be noted that threshold models can produce approximate power laws even when the agents are all of uniform size [20] and so a general explanation of power-law price returns may not require a power-law distribution for the agents’ sizes.

The above results for queues without reneging may be directly applicable to smaller and intermediate-size cascades where the presence of reneging (agents who are switching in the opposing direction) can be approximated by modifying the service time distribution and, in particular, decreasing . However, especially for larger cascades, the assumptions of constant arrival and reneging rates are not appropriate. As an extreme case, consider a selling cascade that initially has arrival rates corresponding to a supercritical process (and a queue that would become infinitely long with non-zero probability). Then the mechanism that ultimately stops the cascade is the re-arrival of agents who have already been through the cascade once. For example, an agent who was fortunate (or smart) enough to sell at the start of a selling cascade may eventually re-enter the process but making the opposite trade, thus reaping an actual as opposed to hypothetical profit, and acting as a brake rather than an accelerator. Thus financial cascades have a propensity to be self-limiting. Similar situations within queueing theory arise by considering the arrival and reneging rates to be functions of time and/or queue length [25, 3, 4] but few general results exist concerning the busy-period distribution.

We end by commenting that price-return tails are an aggregate of many different cascades that almost certainly have differing queueing parameters. Thus a precise analysis of the busy-period distributions may not be necessary to explain the observed functional forms of the tails.

4 Conclusions

Even very simple threshold models appear to be capable of capturing the most important statistical aspects of financial markets. They also better reflect the incremental and history-dependent nature of decision-making processes. Furthermore, since a (weakly) efficient market exists as a special case, it is possible to systematically study the ways in which removing various efficient market assumptions, as reflected in the model, change the global behavior of the system. In this sense, the framework presented in Section 2 can be considered as a set of thought experiments that can be used to query the assumptions behind much of modern finance and economics.

The numerics in Section 2.4 focussed upon herding as the principle cause of deviation from an otherwise efficient market. This is because many important real-world factors such as psychology, bonus/commission criteria and other compensation practices, and moral hazard all produce a similar effect; namely, that one side of a trade or market position becomes more attractive than the other and then herding provides a positive feedback mechanism.

It was then demonstrated that queueing theory can potentially be applied to threshold models. It is unlikely that the cited results, concerning the kurtosis and tail-distribution of the busy periods of single-server queues, can be accurately applied to any real market cascade. However, the analytical methods of queueing theory may provide an explanation for the universality seen in the tail statistics. Queueing theory may also be useful for analyzing order-books and modelling market panics and deleveraging cascades.

Finally, in this paper the attention has been on the slow traders and hence the threshold dynamics. However, such threshold models can be fused, in a very intuitive way, with order-book models. The resulting models would be computationally very intensive, since they must simulate the fast traders as well as the slow ones, but should be able to mimic many different real-world effects across multiple timescales.

References

- [1] S. Alfarano, T. Lux, and F. Wagner. Time variation of higher moments in a financial market with heterogeneous agents: An analytical approach. J. Econ. Dyn. Cont., 32:101–136, 2008.

- [2] S. Alfarano and M. Milaković. Should network structure matter in agent-based finance? University of Kiel, Economics Department Report.

- [3] C.J. Ancker and A.V. Gafarian. Some queueing problems with balking and reneging I. Operations Research, 11:88–100, 1963.

- [4] C.J. Ancker and A.V. Gafarian. Some queueing problems with balking and reneging II. Operations Research, 11:928–937, 1963.

- [5] A. Baltrunas, D.J. Daley, and C. Kluppelberg. Tail behaviour of the busy period of a GI/GI/1 queue with subexpoential service times. Stochastic processes and their applications, 111:237–258, 2004.

- [6] N. Barberis and R. Thaler. A survey of behavioral finance. In G.M. Constantinidos, M. Harris, and R. Stultz, editors, Handbook of Economics and Finance, pages 1053–1123. Elsevier Science, 2003.

- [7] P.P. Bocharov, C. D.Apice, A.V. Pechinkin, and S. Salerno. Queueing Theory. VSP Utrecht, 2004.

- [8] G.W. Brown. Volatility, sentiment and noise traders. Financial Analysts Journal, pages 82–90, 1999.

- [9] R. Cont. Empirical properties of asset returns: stylized facts and statistical issues. Quantitive Finance, 1:223–236, 2001.

- [10] R. Cross, M. Grinfeld, and H. Lamba. A mean-field model of investor behaviour. J. Phys. Conf. Ser., 55:55–62, 2006.

- [11] R. Cross, M. Grinfeld, H. Lamba, and T. Seaman. A threshold model of investor psychology. Phys. A, 354:463–478, 2005.

- [12] R. Cross, M. Grinfeld, H. Lamba, and T. Seaman. Stylized facts from a threshold-based heterogeneous agent model. Eur. J. Phys. B, 57:213–218, 2007.

- [13] R.H. Day and V.L. Smith. Experiments in Decision, Organization and Exchange. North-Holland, Amsterdam, 1993.

- [14] A. de Meyer and J.L. Teugels. On the asymptotic behaviour of the distributions of the busy period and service time in M/G/1. J. Appl. Prob., 17:802–813, 1980.

- [15] E.F. Fama. Efficient capital markets: A review of theory and empirical work. J. Finance, 25:383–417, 1970.

- [16] O. Jouini and Y. Dallery. Moments of first-passage times in general birth-death processes. Math. Meth. Oper. Res., 68:49–76, 2008.

- [17] J.H. Kagel and A.E. Roth (eds.). The Handbook of Experimental Economics. Princeton University Press, 1995.

- [18] D. Kahneman and A. Tversky. Judgement under uncertainty: Heuristics and biases. Science, 185(4157):1124–1131, 1974.

- [19] H. Lamba and T. Seaman. Market statistics of a psychology-based heterogeneous agent model. Int. J. Theor. Appl. Fin., 11:717–737, 2008.

- [20] H. Lamba and T. Seaman. Rational expectations, psychology and learning via moving thresholds. Phys. A, 387:3904–3909, 2008.

- [21] R. Mantegna and H. Stanley. An Introduction to Econophysics. CUP, 2000.

- [22] J.A. Muth. Rational expectations and the theory of price movements. Econometrica, 6, 1961.

- [23] E. Samanidou, E.Zschischang, D. Stauffer, and T. Lux. Agent-based models of financial markets. Rep. Prog. Phys., 70:409–450, 2007.

- [24] F. Slanina. Critical comparisons of several order-book models for stock-market fluctuations. Eur. Phys. J. B, 61:225–240, 2008.

- [25] H.M. Srivastava and B.R.K. Kashyap. Special functions in queueing theory and related stochastic processes. Academic Press, London, 1982.

- [26] A.P. Zwart. Tail asymptotics for the busy period in the GI/G/1 queue. Mathematics of Operations Research, 26:485–493, 2001.