A Discussion on Mean Excess Plots

Abstract.

A widely used tool in the study of risk, insurance and extreme values is the mean excess plot. One use is for validating a generalized Pareto model for the excess distribution. This paper investigates some theoretical and practical aspects of the use of the mean excess plot.

1. Introduction

The distribution of the excess over a threshold for a random variable with distribution function is defined as

| (1.1) |

This excess distribution is the foundation for peaks over threshold (POT) modeling (Embrechts et al., 1997; Coles, 2001) which fits appropriate distributions to data of excesses. The use of peaks over threshold modeling is widespread and applications include:

Peaks over threshold modeling is based on the generalized Pareto class of distributions being appropriate for describing statistical properties of excesses. A random variable has a generalized Pareto distribution (GPD) if it has a cumulative distribution function of the form

| (1.2) |

where , and when and if . The parameters and are referred to as the shape and scale parameters respectively. For a Pareto distribution, the tail index is just the reciprocal of when . A special case is when and in this case the GPD is the same as the exponential distribution with mean .

The Pickands-Balkema-de Haan Theorem (Embrechts et al., 2005, Theorem 7.20, page 277) provides the theoretical justification for the centrality of the GPD class of distributions for peaks over threshold modeling. This result shows that for a large class of distributions (those distributions in a maximal domain of attraction of the extreme value laws), the excess distribution is asymptotically equivalent to a GPD law , as the threshold appropaches the right endpoint of the distribution . Here the asymptotic shape parameter is fixed but the scale may depend on . More precise statements are given below in Theorems 3.1, 3.6, and 3.9. For this reason the GPD is a natural candidate for modeling peaks over a threshold.

The choice of the extreme threshold , where the GPD model provides a suitable approximation to the excess distribution is critical in applications. The mean excess (ME) function is a popular tool used to aide this choice of and also to determine the adequacy of the GPD model in practice. The ME function of a random variable is defined as:

| (1.3) |

provided and is also known as the mean residual life function, especially in survival analysis. It has been studied as early as Benktander and Segerdahl (1960). See Hall and Wellner (1981) for a discussion of properties of mean excess functions. Table 3.4.7 in (Embrechts et al., 1997, p.161) gives the mean excess function for some standard distributions.

Given an independent and identically distributed (iid) sample from , a natural estimate of is the empirical ME function defined as

| (1.4) |

Yang (1978) suggested the use of the empirical ME function and established the uniform strong consistency of over compact -sets; that is, for any

| (1.5) |

In the context of extremes, however, (1.5) is not especially informative since what is of interest is the behavior of in a neighborhood of the right end point of , which could be . In this case the GPD plays a pivotal role. For a random variable , we have iff and in this case, the ME function of is linear in :

| (1.6) |

where if and if . In fact, the linearity of the mean excess function characterizes the GPD class. See Embrechts et al. (2005, 1997). Davison and Smith (1990) used this property to devise a simple graphical check that data conforms to a GPD model; their method is based on the ME plot which is the plot of the points , where are the order statistics of the data. If the ME plot is close to linear for high values of the threshold then there is no evidence against use of a GPD model. See also Embrechts et al. (1997) and Hogg and Klugman (1984) for the implementation of this plot in practice.

In this paper we establish the asymptotic behavior of the ME plots for large thresholds. We assume is in the maximal domain of attraction of an extreme value law with shape parameter . When we show that, as expected, for high thresholds the ME plot viewed as a random closed set converges in the Fell topology to a straight line. A novel aspect of our study is we also consider the ME plot in the case , the case where the ME function does not exist, and show that the ME plot converges to a random curve. This also holds in the more delicate case after suitable rescaling. These results show that the ME plot is inconsistent when and emphasizes that knowledge of a finite mean is required.

It is tempting to argue that consistency of the ME plot should imply, by a continuity argument, the consistency of the estimator of obtained from computing the slope of the line fit to the ME plot. However, this slope functional is not necessarily continuous as discussed in Das and Resnick (2008). So consistency of the slope function requires further work and is an ongoing investigation.

The paper is arranged as follows. In Section 2 we briefly discuss required background on convergence of random closed sets and then study the ME plot in Section 3. In Section 4 we discuss advantages and disadvantages of the mean excess plot and how this tool compares with other techniques of extreme value theory such as the Hill estimator, the Pickands estimator and the QQ plot. We illustrate the behavior of the empirical mean excess plot for some simulated data sets in Section 5 and in Section 6 we analyze three real data sets obtained from different subject areas and also compare different tools.

2. Background

2.1. Topology on closed sets of

Before we start any discussion on whether a mean excess plot is a reasonable diagnostic tool we need to understand what it means to talk about convergence of plots. So we discuss the topology on a set containing the plots.

We denote the collection of closed subsets of by . We consider a hit and miss topology on called the Fell topology. The Fell topology is generated by the families and where for any set

So and are collections of closed sets which miss and hit the set , respectively. This is why such topologies are called hit and miss topologies. In the Fell topology a sequence of closed sets converges to if and only if the following two conditions hold:

-

•

hits an open set implies there exists such that for all , hits .

-

•

misses a compact set implies there exists such that for all , misses .

The Fell topology on the closed sets of is metrizable and we indicate convergence in this topology of a sequence of closed sets to a limit closed set by . Sometimes, rather than work with the topology, it is easier to deal with the following characterization of convergence.

Lemma 2.1.

A sequence converges to in the Fell topology if and only if the following two conditions hold:

-

(1)

For any there exists such that

-

(2)

If for some subsequence , converges, then .

See Theorem 1-2-2 in (Matheron, 1975, p.6) for a proof of this Lemma. Since the topology is metrizable, the definition of convergence in probability is obvious. The following result is a well-known and helpful characterization for convergence in probability of random variables and it holds for random sets as well; see Theorem 6.21 in (Molchanov, 2005, p.92).

Lemma 2.2.

A sequence of random sets in converges in probability to a random set if and only if for every subsequence of there exists a further subsequence of such that -a.s.

We use the following notation: For a real number and a set , .

2.2. Miscellany.

Throughout this paper we will take to be a sequence increasing to infinity such that . For a distribution function we write for the tail and the quantile function is

A function is regularly varying with index , written , if

We denote the space of nonnegative Radon measures on metrized by the vague metric by . Point measures are written as a function of their points by See, for example, (Resnick, 1987, Chapter 3).

We will use the following notations to denote different classes of functions: For

-

(i)

: Right-continuous functions with finite left limits defined on .

-

(ii)

: Left-continuous functions with finite right limits defined on .

We will assume that these spaces are equipped with the Skorokhod topology and the distance function. In some cases we will also consider product spaces of functions and then the topology will be the product topology. For example, will denote the class of 2-dimensional functions on . The classes of functions defined on the sets or will have the obvious notation.

3. Mean Excess Plots

As discussed in the introduction, a random variable having distribution with has a linear ME function given by (1.6) where the slope is positive negative or . We consider these three cases separately.

3.1. Positive Slope

In this subsection we concentrate on the case where . A finite mean for is guaranteed when and we also investigate what happens when .

The following Theorem is a combination of Theorem 3.3.7 and Theorem 3.4.13(b) in Embrechts et al. (1997).

Theorem 3.1.

Assume . The following are equivalent for a cumulative distribution function :

-

(1)

, i.e., for every

-

(2)

is in the maximal domain of attraction of a Frechet distribution with parameter , i.e.,

where .

-

(3)

There exists a positive measurable function such that

(3.1)

Theorem 3.1(3) is one case of the Pickands-Balkema-de Haan theorem. It guarantees the existence of a measurable function for which (3.1) holds but does not construct this function. However, can be obtained from Karamata’s representation of a regular varying function (Bingham et al., 1989), namely if , there exists such that

where and as . An easy computation shows as ,

This means that if is a random variable having distribution then for large ,

and is a choice for the scale parameter in (3.1). Hence we get that as by the convergence to types theorem (Resnick, 1987).

Consider the ME plot for iid random variables having common distribution which satisfies for some . Since the excess distribution is well approximated by the GPD for high thresholds, we expect that for , the ME function will look similar to that of the GPD for high thresholds and therefore seek evidence of linearity in the plot. We first consider the ME plot when and will discuss the case separately. Furthermore, we see that for each , the mean excess plot, being a finite set of -valued random variables, is measurable and a random closed set. It follows from the definition of random sets; see Definition 1.1 in (Molchanov, 2005, p. 2).

3.1.1. Heavy tail with a finite mean; .

The scaled and thresholded ME plot converges to a deterministic line.

Theorem 3.2.

If are iid observations with distribution satisfying with , then in

| (3.2) |

Remark 3.3.

Roughly, this result implies

The plot of the points is a little different from the original ME plot. In practice, people plot of the points but our result restricts attention to the higher order statistics corresponding to This restriction is natural and corresponds to looking at observations over high thresholds. One imagines zooming into the area of interest in the complete ME plot.

This result scales the points by . Since both co-ordinates of the points in the plot are scaled, we do not change the structure or appearance of the plot but only the scale of the axes. Hence we may still estimate the slope of the line if we want to estimate by this method (Davison and Smith, 1990). The scaling is important because the points are moving to infinity and the Fell topology is not equipped to handle sets which are moving out to infinity. Furthermore, the regular variation assumption on the tail of involves a ratio condition and thus it is natural that the random set convergence uses scaling.

A central assumption in Theorem 3.2 is that the random variables are iid. The proof of the theorem below will explain that an important tool is the convergence of the tail empirical measure in (3.4). By Proposition 2.1 in Resnick and Starica (1998), we know that the iid assumption of the random variables is not a necessary condition for the convergence of the tail empirical measure. We believe as long as the tail empirical measure converges, our result should hold.

Proof.

We show that for every subsequence of integers there exists a further subsequence of such that

| (3.3) |

Define the tail empirical measure as a random element of by

| (3.4) |

Following (4.21) in (Resnick, 2007, p.83) we get that

| (3.5) |

where Now consider

as random elements in .We will show that in , where

We already know the result for the first component of , i.e., in ; see (Resnick, 2007, p.82). Since the limits are non-random it suffices to prove the convergence of the second component of . Observe that the empirical mean excess function can be obtained from the tail empirical measure:

Consider the maps and from to defined by

We understand if is not integrable. We will show that . The function is obviously continuous and therefore in . In order to prove that it suffices to show that for any

where is the supnorm on . To verify this claim, note that

and the rest is proved easily following the arguments used in the step 3 of the proof of Theorem 4.2 in (Resnick, 2007, p.81).

Suppose is the subspace of consisting only of functions which are never less than 1. Consider the random element in the space ,

From what we have obtained so far it is easy to check that , where

The map defined by

is continuous if and are continuous and therefore

This finally shows the convergence of the second component of and hence we get that

Next we have to convert this result to that of convergence of the random sets . This argument is similar to the one used to prove Lemma 2.1.3 in Das and Resnick (2008). Choose any subsequence of integers. Since we have in . So there exists a subsequence of such that a.s. Now the final step is to use this to prove (3.3) and for that we will use Lemma 2.1 . Take any point in of the form for some . Set and observe that and . This proves condition of Lemma 2.1 and we next prove condition . Suppose for some subsequence of , converges to . Since is strictly monotone we get that the must be some such that as . Now, since and is a continuous we get that . That completes the proof. ∎

3.1.2. Case ; limit sets are random.

The following theorem describes the asymptotic behavior of the ME plot when . Reminder: guarantees an infinite mean.

Theorem 3.4.

Assume are i.i.d. observations with distribution satisfying :

-

(i)

If , then

(3.6) in , where and is the positive stable random variable with index which satisfies for

(3.7) -

(ii)

If and satisfies , , and

(3.8) then

(3.9) in , where

and is a positively skewed stable random variable satisfying

Remark 3.5.

In Theorem 3.2 we considered the points of the mean excess plot normalized by . By scaling both coordinates by the same normalizing sequence, we did not change the structure of the plot. But in Theorem 3.4(i) we need different scaling in the two coordinates. This is simple to observe since and implies as . This means that in order to get a finite limit we need to normalize the second coordinate by a sequence increasing at a much faster rate than the normalizing sequence for the first coordinate. This is indeed changing the structure of the plot and even with this normalization the limiting set is random. The limit is a curve scaled in the second coordinate by the random quantity . Note that the limit is independent of the choice of the sequence as long as it satisfies the condition that and as . Another interesting outcome, as pointed out by a referee, is that in the log-log scale the limit set becomes

which is a straight line with slope and a random intercept term .

In Theorem 3.4(ii) along with we make the extra assumption (3.8). Under these assumptions we get that mean excess plot with some centering in the second coordinate converges to a random set. We could obtain result without (3.8) but then the centering becomes random and more complicated and difficult to interpret. The significance of (3.8) is as follows: The centering is of the form

where is in the de Haan class and has slowly varying auxiliary function ; see Resnick (2007), Bingham et al. (1989), de Haan (1976) and de Haan and Ferreira (2006). Condition (3.8) is the same as requiring to satisfy

Proof.

(i) We will first prove that

| (3.10) |

The two important facts that we will need for the proof are the following:

Since is non-random, in order to prove (3.10) it suffices to show that in (Resnick, 2007, Proposition 3.1, p.57). By Theorem 16.7 in (Billingsley, 1999, p.174) we need to show that in for every . So fix arbitrarily. By an abuse of notation we will use and as to denote their restrictions on as elements of .

Observe that and since we get as . Combining this with (B) we get that for any ,

| (3.12) |

Also observe that for any

| (3.13) |

Using (A), (3.12), (3.13) and Proposition 3.1 in (Resnick, 2007, p.57) we get that for any

| (3.14) |

This allows us to obtain the weak limit of :

By similar arguments we can also show that for any ,

From Billingsley (1999), Theorem 13.3, p.141, the proof of (3.10) will be complete if we show for any

where for any

Fix any and choose large enough such that and . Then for any

Therefore, using the form of the function we get

Hence we have proved (3.10).

Now we prove the statement of the theorem. By Proposition 6.10, page 87 in Molchanov (2005) it suffices to show that for any continuous function with a compact support

Suppose is a continuous function with compact support. By the Skorokhod representation theorem (see Theorem 6.7 in (Billingsley, 1999, p.70)) there exists a probability space and random elements and in such that and and in for every . Now observe that

Since is continuous we get

and since is bounded we apply the dominated convergence theorem to get

and that completes the proof of the theorem when .

(ii) Similar to the proof of part (i) we will first prove that in

| (3.15) |

We will use the following facts:

By the same arguments used in part (i) it suffices to prove that for any arbitrary

Observe that from (3.11) and the assumption that we get for any

| (3.16) |

The reason for this is that

where See (3.5) and (3.11). Now fix any and note that

We complete the proof using the same arguments as those in part (i). ∎

3.2. Negative Slope

The case when is characterized by the following theorem which is a combination of Theorems 3.3.12 and 3.4.13(b) in Embrechts et al. (1997):

Theorem 3.6.

If then the following are equivalent for a distribution function :

-

(1)

has a finite right end point and .

-

(2)

is in the maximal domain of attraction of a Weibull distribution with parameter , i.e.,

where .

-

(3)

There exists a measurable function such that

Here we again get a characterization of this class of distributions in terms of the behavior of the maxima of iid random variables and the excess distribution. Using Theorem 3.6(1) and Karamata’s Theorem (Bingham et al., 1989, Theorem 1.5.11, p.28) we get that as . We show that this behavior is observed empirically. The Pickands-Balkema-de Haan Theorem, part (3) of Theorem 3.6, does not explicitly construct the scale parameter but as in Remark 3.3 one can show that as .

Theorem 3.7.

Suppose are iid random variables with distribution which has a finite right end point and satisfies as for some . Then

in .

Remark 3.8.

As in Subsection 3.1 we look at a modified version of the mean excess plot. Here we scale and relocate the points of the plot near the right end point. We may interpret this result as

where .

Proof.

The proof is similar to that of Theorem 3.2. From Theorem 5.3(ii), p. 139 in Resnick (2007) we get

where for all and Following the arguments used in the proof of Theorem 4.2 in (Resnick, 2007, p.81) we also get

| (3.17) |

Here we can represent in terms of the empirical measure as

and taking the same route as in Theorem 3.2 we get

in . From this we get in the Fell topology

Finally, using the fact that

and the identity

we get the final result. ∎

3.3. Zero Slope

The next result follows from Theorems 3.3.26 and 3.4.13(b) in Embrechts et al. (1997) and Proposition 1.4 in Resnick (1987).

Theorem 3.9.

The following conditions are equivalent for a distribution function with right end point :

-

(1)

There exists such that has a representation

(3.18) where is a measurable function satisfying , , and is a positive, absolutely continuous function with density as .

-

(2)

is in the maximal domain of attraction of the Gumbel distribution, i.e.,

where and .

-

(3)

There exists a measurable function such that

Theorem 3.3.26 in Embrechts et al. (1997) also says that a possible choice of the auxiliary function in (3.18) is

and for this choice, the auxiliary function is the ME function, i.e., . Furthermore, we also know that as and this implies that as .

A prime example in this class is the exponential distribution for which the ME function is a constant. The domain of attraction of the Gumbel distribution is a very big class including distributions as diverse as the normal and the log-normal. It is indexed by auxiliary functions which only need to satisfy as . Since is a choice for the auxiliary function , the class of ME functions corresponding to the domain of attraction of the Gumbel distribution is very large.

Theorem 3.10.

Suppose are iid random variables with distribution which satisfies any one of the conditions in Theorem 3.9. Then in ,

Proof.

This is again similar to the proof of Theorem 3.2. Using Theorem 3.9(2) we get

Since we also get

and then Theorem 5.3(ii) in (Resnick, 2007, p.139) gives us

where for all . Following the arguments in the proof of Theorem 4.2 in (Resnick, 2007, p.81) we get

and then

Now, one can easily establish the identity between the empirical mean excess function and the empirical measure

From this fact it follows that

in and that in turn implies

Finally, using the fact that

we get the desired result. ∎

4. Comparison with Other Methods of Extreme Value Analysis

For iid random variables from a distribution in the maximal domain of attraction of the Frechet, Weibull or the Gumbel distributions, Theorems 3.2, 3.7 and 3.10 describe the asymptotic behavior of the ME plot for high thresholds. Linearity of the ME plot for high order statistics indicates there is no evidence against the hypothesis that the GPD model is a good fit for the thresholded data.

Furthermore, we obtain a natural estimate of by fitting a line to the linear part of the ME plot using least squares to get a slope estimate and then recovering . Although natural, convergence of the ME plot to a linear limit does not guarantee consistency of this estimate and this is still under consideration. Proposition 5.1.1 in Das and Resnick (2008) explains why the slope of the least squares line is not a continuous functional of finite random sets.

Davison and Smith (1990) give another method to estimate . They suggest a way to find a threshold using the ME plot and then fit a GPD to the points above the threshold using maximum likelihood estimation. For both this and the LS method, the ME plot obviously plays a central role. We analyze several simulation and real data sets in Sections 5 and 6 using only the LS method.

With any method, an important step is choice of threshold guided by the ME plot so that the plot is roughly linear above this threshold. Threshold choice can be challenging and parameter estimates can be sensitive to the threshold choice, especially when real data is analyzed.

The ME plot is only one of a suite of widely used tools for extreme value model selection. Other techniques are the Hill plot, the Pickands plot, the moment estimator plot and the QQ plot; cf. Chapter 4, Resnick (2007) and de Haan and Ferreira (2006). Some comparisons from the point of view of asymptotic bias and variance are in de Haan and Peng (1998). Here we review definitions and basic facts about several methods assuming that is an iid sample from a distribution in the maximal domain of attraction of an extreme value distribution. The asymptotics require , the number of upper order statistics used for estimation, to be a sequence increasing to such that .

-

(1)

The Hill estimator based on upper order statistics is

If then . The Hill plot is the plot of the points .

-

(2)

The Pickands estimator does not impose any restriction on the range of . The Pickands estimator,

is consistent for ; i.e., as . The Pickands plot is the plot of the points .

-

(3)

The QQ plot treats the case and separately. When , the QQ plot consists of the points where is a suitably chosen integer. Das and Resnick (2008) showed in equipped with the Fell topology. So the limit is a line with slope and the LS estimator is consistent (Das and Resnick, 2008; Kratz and Resnick, 1996).

In the case when then the QQ plot can be defined as the plot of the points , where is an estimate of based on upper order statistics.

- (4)

-

(5)

To complete this survey, recall that the ME plot converges to a nonrandom line when .

The Hill and QQ plots work best for and the ME plot requires knowledge that . Each plot requires the data be properly thresholded. The ME plot requires thresholding but also that be sufficiently large that proper averaging takes place.

5. Simulation

We divide this section into three subsections. In subsection 5.1 we show simulation results for mean excess plot of some standard distributions with well-behaved tails. In subsections 5.2 and 5.3 we discuss simulation results of some distributions with either difficult tail-behavior or infinite mean.

5.1. Standard Situations

5.1.1. Pareto distribution

The obvious first choice for a distribution function to simulate from is the GPD. For the GPD the ME plot should be roughly linear. We simulate 50000 random variables from the Pareto(2) distribution. This means that the parameters of the GPD are and .

Figure 1 shows the mean excess plot for this data set. Observe that in Figure 1(a) the first part of the plot is quite linear but it is scattered for very high order statistics. The reason behind this phenomenon is that the empirical mean excess function for high thresholds is the average of the excesses of a small number of upper order statistics. When averaging over few numbers, there is high variability and therefore, this part of the plot appears very non-linear and is uninformative. In Figure 1(b) we zoom into the plot by leaving out the top 250 points. We calculate using all the data but plot only the points . This restricted plot looks linear. We fit a least squares line to this plot and the estimate of the slope is Since the slope is we get the estimate of to be

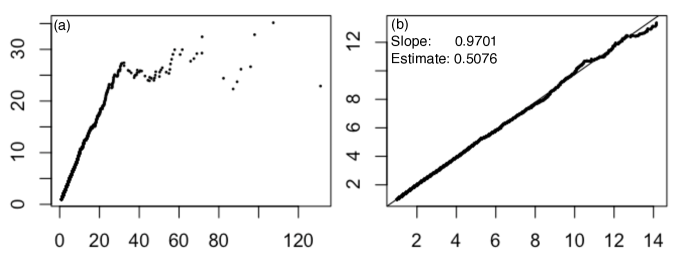

5.1.2. Right-skewed stable distribution

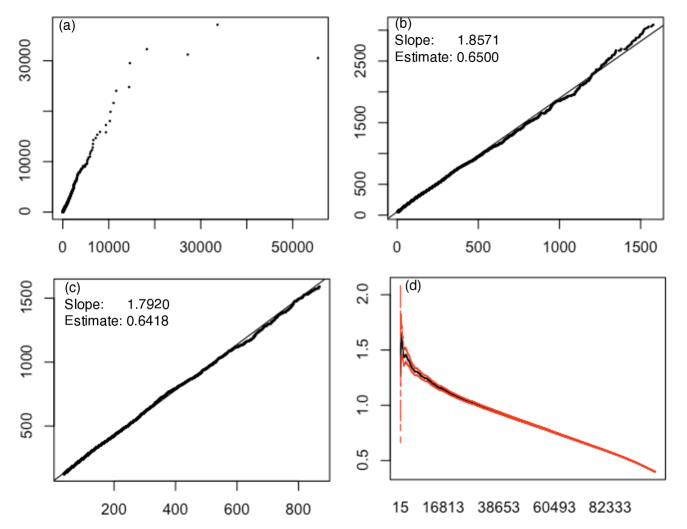

We next simulate 50000 random samples from a totally right skewed stable(1.5) distribution. So and then . Figure 2(a) is the ME plot obtained from this data set. This is not a sample from a GPD, but only from a distribution in the maximal domain of attraction of a GPD. The ME function is not exactly linear and for estimating we should concentrate on high thresholds. As we did for the last example we drop points in the plot for very high order statistics since they are the average of a very few values. Figures 2(b), 2(c) and 2(d) confines the plot to the order statistics 120-30000, 180-20000 and 270-10000 respectively, i.e., plots the points for in the specified range. As we restrict the plot more and more, the plot becomes increasingly linear. In Figure 2(d) the least squares estimate of the slope of the line is 1.763 and hence the estimate of is 0.638.

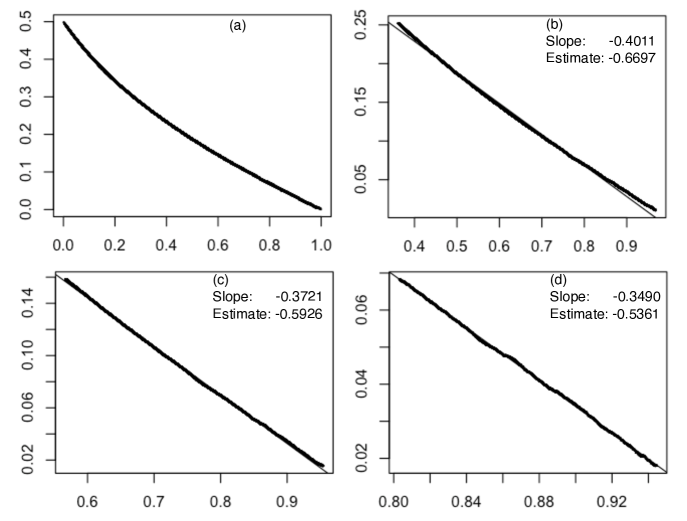

5.1.3. Beta distribution

Figure 3 gives the ME plot for 50000 random variables from the beta(2,2) distribution

which is in the maximal domain of the Weibull distribution with the parameter . Figure 3(a) is the entire ME plot and then Figures 3(b), 3(c) and 3(d) plot the empirical ME function for the order statistics 150-35000, 300-20000 and 450-5000 respectively. The last plot is quite linear and the estimate of is .

5.2. Difficult Cases

5.2.1. Lognormal distribution

The lognormal(0,1) distribution is in the maximal domain of attraction of the Gumbel and hence . The ME function of the log normal has the form

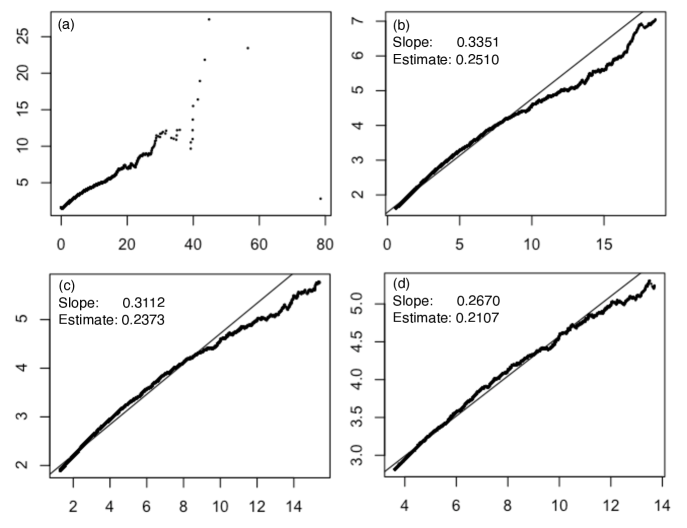

see Table 3.4.7 in (Embrechts et al., 1997, p.161). So is regularly varying of index but still . Figure 4(a) shows the ME plot obtained for a sample of size from the lognormal(0,1) distribution.

Figures 4(b), 4(c) and 4(d) show the empirical ME functions for the order statistics 150-70000, 300-40000 and 450-10000 respectively. The slopes of the least squares lines in Figures 4(b), 4(c) and 4(d) are 0.3351, 0.3112 and 0.267 respectively. The estimate of also decreases steadily as we zoom in towards the higher order statistics from 0.251 in 4(b) to 0.2107 in 4(d). Furthermore, a curve is evident in the plots and the slope of the curve is decreasing, albeit very slowly, as we look at higher and higher thresholds. At a first glance the ME function might seem to resemble that of a distribution in the maximal domain of attraction of the Frechet. The curve becomes evident only after a detailed analysis of the plot. That is possible because the data are simulated but in practice analysis would be difficult. For this example, the ME plot is not a very effective diagnostic for discerning the model.

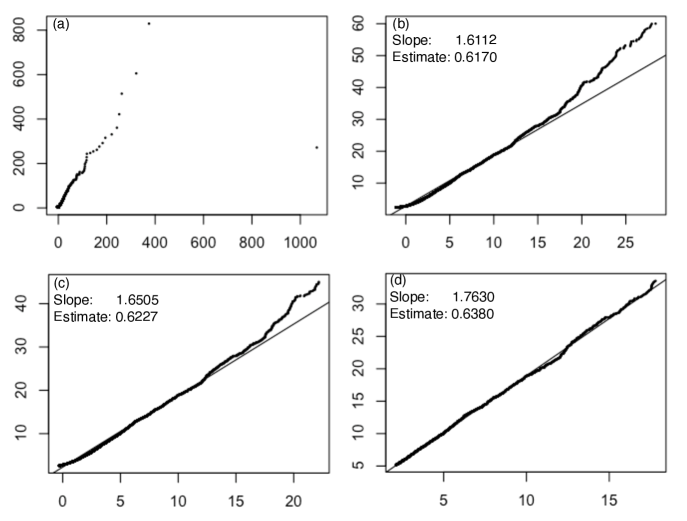

5.2.2. A non-standard distribution

We also try a non-standard distribution for which . This means that and therefore . The exact form of is given by

| (5.1) |

where is the Lambert W function satisfying for all . Observe that as and for . Furthermore,

and hence is a slowly varying function. This is therefore an example where the slowly varying term contributes significantly to . That was not the case in the Pareto or the stable examples.

We simulated random variables from this distribution. Figure 5(a) gives the entire ME plot from this data set. Figures 5(b) and 5(c) plots the ME function for the order statistics 150-70000 and 400-20000 respectively. In Figure 5(c) the estimate of is 0.6418 which is a somewhat disappointing estimate given that the sample size was . Figure 5(d) is the Hill Plot from this data set using the QRMlib package in R. It plots the estimate of obtained by choosing different values of . It is evident from this that the Hill estimator does not perform well here. For none of the values of is the Hill estimator even close to the true value of which is 2. We conclude, not surprisingly, that a slowly varying function increasing to infinity can fool both the ME plot and the Hill plot. See Degen et al. (2007) for a discussion on the behavior of the ME plot for a sample simulated from the g-and-h distribution and Resnick (2007) for Hill horror plots.

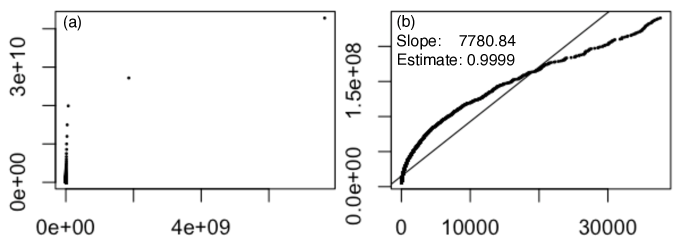

5.3. Infinite Mean: Pareto with .

This simulation

sheds light on the behavior of the ME plot when . In this case the ME function does not exist but the empirical ME plot does. Figure 6 displays the ME plot of for 50000 random variables simulated from Pareto(0.5) distribution. The plot is certainly far from linear even for high order statistics and the least squares line has slope 7780.84 which gives an estimate of to be 0.9999. This certainly gives an indication that the ME plot is not a good diagnostic in this case.

6. ME Plots for Real Data

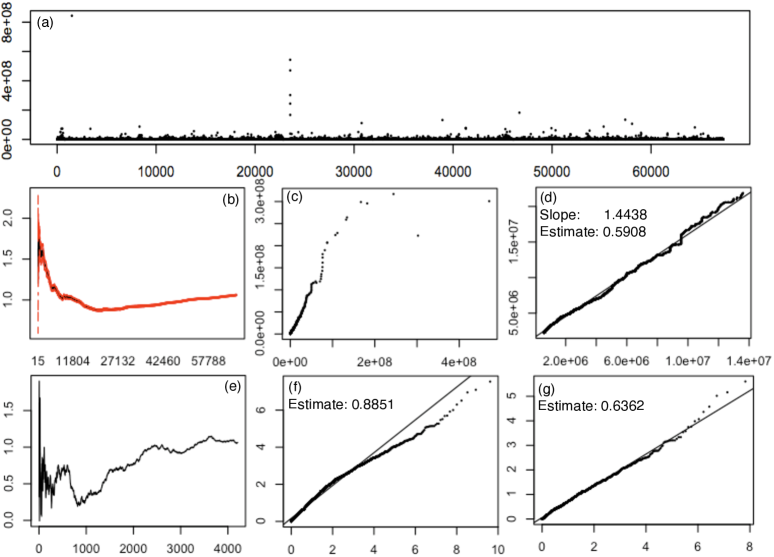

6.1. Size of Internet Response

This data set consists of Internet response sizes corresponding to user requests. The sizes are thresholded to be at least 100KB. The data set a part of a bigger set collected in April 2000 at the University of North Carolina at Chapel Hill.

Figure 7 contains various plots of the data. Figures 7(b) and Figure 7(e) are the Hill plot (estimating ) and the Pickands plot respectively. It is difficult to infer anything from these plots though superficially they appear stable.

Figures 7(c) and 7(d) are the entire ME plot and the ME plot restricted for order statistics 300-12500. The second plot does seem to be very linear and gives an estimate of to be 0.5908. Figures 7(f) and 7(g) are the QQ plots for the data for and (as explained in Section 4). The estimate of in these two plots are 0.8851 and 0.6362. The estimates of obtained from the QQ plot 7(d) and the ME plot 7(g) are close and the plots are also linear. So we believe that this is a reasonable estimate of .

6.2. Volume of Water in the Hudson River

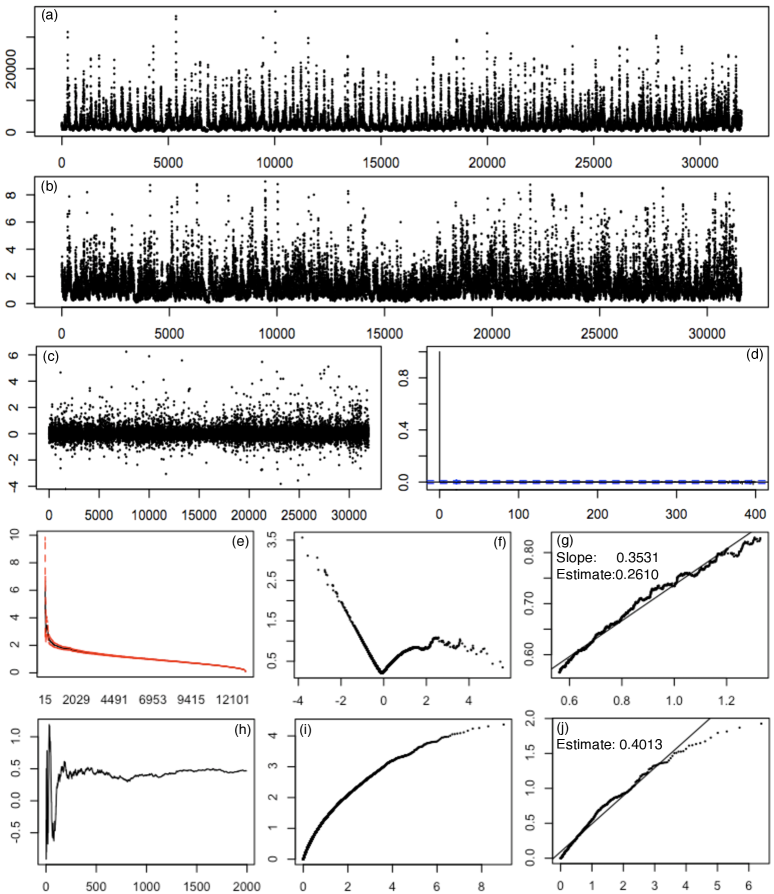

We now analyze data on the average daily discharge of water (in cubic feet per second) in the Hudson river measured at the U.S. Geological Survey site number 01318500 near Hadley, NY. The range of the data is from July 15, 1921 to December 31, 2008 for a total of 31946 data points.

Figure 8(a) is the time series plot of the original data and it shows the presence of periodicity in the data. The volume of water is typically much higher in April and May than the rest of the year which possibly is due to snow melt. We ‘homoscedasticize’ the data in the following way. We compute the standard deviation of the average discharge of water for every day of the year and then divide each data point by the standard deviation corresponding to that day. If the original data is say then we transform it to , where is the standard deviation of the data points obtained on July 15 in the different years in the range of the data and similarly is the same for December 31. The plot of the transformed points is given in 8(b). We then fit an AR(33) model to this data using the function ar in the stats package in R. The lag was chosen based on the AIC criterion. Figures 8(c) and (d) show the residuals and their ACF plot respectively. This encourages us to assume that there no linear dependence in the residuals.

We now apply the tools for extreme value analysis on the residuals. Figure 8(e) is the Hill plot and it is difficult to draw any inference from this plot in this case. Figures 8(f) and 8(g) are the entire ME plot and the ME plot restricted to the order statistics 300-1300. From 8(g) we get an estimate of to be 0.261. The Pickands plot in 8(h) and the QQ plots in 8(i) and 8(j) suggest an estimate of around 0.4. A definite curve is visible in the QQ plot even for . But the slope of the least squares line fitting the QQ plot supports the estimate suggested by the Pickands plot and the ME plot. We see that it is difficult to reach a conclusion about the range of . Still we infer that 0.4 is a reasonable estimate of for this data since that is being suggested by two different methods.

6.3. Ozone level in New York City

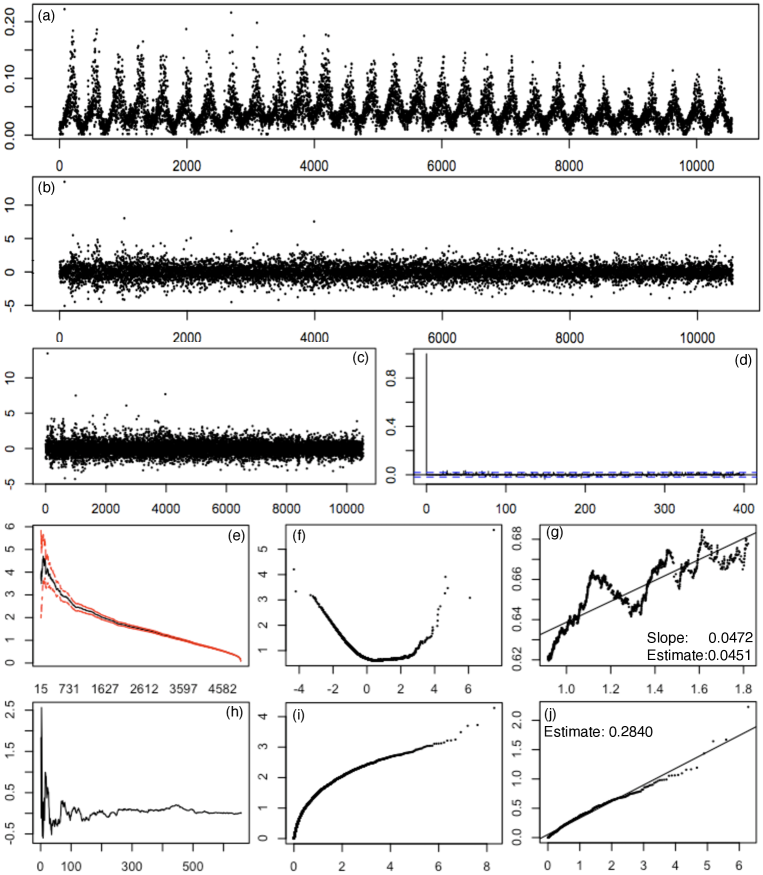

We also apply the methods to a data set obtained from http://www.epa.gov/ttn/airs/aqsdatamart. This is the data on daily maxima of level of Ozone (in parts per million) in New York City on measurements closest to the ground level observed between January 1, 1980 and December 31, 2008.

Figure 9(a) is the time series plot of the data. This data set also showed a seasonal component which accounted for high values during the summer months. We transform the data set to a homoscedastic series (Figure 9(b)) using the same technique as explained in Subsection 6.2. Fitting an AR(16) model we get the residuals which are uncorrelated; see Figures 9(c) and 9(d).

The Hill plot in Figure 9(e) again fails to give a reasonable estimate of the tail index. The ME plots in Figures 9(e) and 9(g) are also very rough. Figure 9(g) is the plot of the points for and the least squares line fitting these points has slope 0.0472 which gives an estimate of to be 0.0451. This is consistent with the Pickands plot in 9(h). This suggests that the residuals may be in the domain of attraction of the Gumbel distribution.

7. Conclusion.

The ME plot may be used as a diagnostic to aid in tail or quantile estimation for risk management and other extreme value problems. However, some problems associated with its use certainly exist:

-

•

One needs to trim away for small values of where too few terms are averaged and also trim irrelevent terms for large values of which are governed by either the center of the distribution or the left tail. So two discretionary cuts to the data need be made whereas for other diagnostics only one threshold needs to be selected.

-

•

The analyst needs to be convinced since for random sets are the limits for the normalized ME plot. Such random limits could create misleading impressions. The Pickands and moment estimators place no such restriction on the range of . The QQ method works most easily when but can be extended to all . The Hill method requires .

-

•

Distributions not particularly close to GPD can fool the ME diagnostic. However, fairness requires pointing out that this is true of all the procedures in the extreme value catalogue. In particular, with heavy tail distributions, if a slowly varying factor is attached to a Pareto tail, diagnostics typically perform poorly.

The standing assumption for the proofs in this paper is that is iid. We believe most of the results on the ME plot hold under the assumption that the underlying sequence is stationary and the tail empirical measure is consistent for the limiting GPD distribution of the marginal distribution of . We intend to look into this further. Other open issues engaging our attention include converses to the consistency of the ME plot and if the slope of the least squares line through the ME plot is a consistent estimator.

We are thankful to the referees and the editors for their valuable and detailed comments.

References

- Benktander and Segerdahl (1960) Benktander, G., Segerdahl, C., 1960. On the analytical representation of claim distributions with special reference to excess of loss reinsurance. In: XVIth International Congress of Actuaries, Brussels.

- Billingsley (1999) Billingsley, P., 1999. Convergence of Probability Measures, 2nd Edition. John Wiley and Sons, New York.

- Bingham et al. (1989) Bingham, N. H., Goldie, C. M., Teugels, J. L., 1989. Regular Variation. Cambridge University Press.

- Coles (2001) Coles, S., 2001. An Introduction to Statistical Modeling of Extreme Values. Springer-Verlag, London.

- Csorgo and Mason (1986) Csorgo, S., Mason, D., 1986. The asymptotic distribution of sums of extreme values from a regularly varying distribution. The Annals of Probability 14 (3), 974–983.

- Das and Resnick (2008) Das, B., Resnick, S., 2008. Qq plots, random sets and data from a heavy tailed distribution. Stochastic Models 24 (1), 103–132.

- Davison and Smith (1990) Davison, A., Smith, R., 1990. Models for exceedances over high thresholds. Journal of the Royal Statistical Society Series B 52 (3), 393–42.

- de Haan (1976) de Haan, L., 1976. An Abel-Tauber theorem for Laplace transforms. Journal of the London Mathematical Society 13, 537–542.

- de Haan and Ferreira (2006) de Haan, L., Ferreira, A., 2006. Extreme Value Theory: An Introduction. Springer-Verlag, New York.

- de Haan and Peng (1998) de Haan, L., Peng, L., 1998. Comparison of tail index estimators. Statistica Neerlandica 52 (1), 60–70.

- Degen et al. (2007) Degen, M., Embrechts, P., Lambrigger, D. D., 2007. The quantitative modeling of operational risk: between g-and-h and evt. Astin Bulletin 37 (2), 265.

- Dekkers et al. (1989) Dekkers, A., Einmahl, J., de Haan, L., 1989. A moment estimator for the index of an extreme-value distribution. Ann. Statist. 17, 1833–1855.

- Embrechts et al. (1997) Embrechts, P., Klüppelberg, C., Mikosch, T., 1997. Modelling Extremal Events. Vol. 33 of Applications in Mathematics. Springer-Verlag, New York.

- Embrechts et al. (2005) Embrechts, P., McNeil, A. J., Frey, R., 2005. Quantitative Risk Management: Concepts, Techniques, and Tools. Princeton University Press.

- Guess and Proschan (1985) Guess, F., Proschan, F., 1985. Mean Residual Life: Theory and Applications. Defense Technical Information Center.

- Hall and Wellner (1981) Hall, W., Wellner, J., 1981. Mean residual life. Statistics and Related Topics, 169–184.

- Hogg and Klugman (1984) Hogg, R., Klugman, S., 1984. Loss Distributions. Wiley, New York.

- Kratz and Resnick (1996) Kratz, M., Resnick, S., 1996. The qq-estimator and heavy tails. Stochastic Models 12 (4), 699–724.

- Matheron (1975) Matheron, G., 1975. Random Sets and Integral Geometry. Wiley, New York.

- Molchanov (2005) Molchanov, I. S., 2005. Theory of Random Sets. Springer.

- Resnick (2007) Resnick, S., 2007. Heavy-Tail Phenomena: Probabilistic And Statistical Modeling. Springer.

- Resnick and Starica (1998) Resnick, S., Starica, C., 1998. Tail index estimation for dependent data. The Annals of Applied Probability, 1156–1183.

- Resnick (1987) Resnick, S. I., 1987. Extreme Values, Regular Variation and Point Processes. Springer-Verlag, Berlin, New York.

- Smith (1989) Smith, R., 1989. Extreme value analysis of environmental time series: an application to trend detection in ground-level ozone. Statistical Science 4 (4), 367–377.

- Todorovic and Rousselle (1971) Todorovic, P., Rousselle, J., 1971. Some problems of flood analysis. Water Resources Research 7 (5), 1144–1150.

- Todorovic and Zelenhasic (1970) Todorovic, P., Zelenhasic, E., 1970. A stochastic model for flood analysis. Water Resources Research 6 (6), 1641–1648.

- Yang (1978) Yang, G., 1978. Estimation of a biometric function. The Annals of Statistics 6 (1), 112–116.