Phase transition and information cascade

in

a voting model

Abstract

We introduce a voting model that is similar to a Keynesian beauty contest and analyze it from a mathematical point of view. There are two types of voters-copycat and independent-and two candidates. Our voting model is a binomial distribution (independent voters) doped in a beta binomial distribution (copycat voters). We find that the phase transition in this system is at the upper limit of , where is the time (or the number of the votes). Our model contains three phases. If copycats constitute a majority or even half of the total voters, the voting rate converges more slowly than it would in a binomial distribution. If independents constitute the majority of voters, the voting rate converges at the same rate as it would in a binomial distribution. We also study why it is difficult to estimate the conclusion of a Keynesian beauty contest when there is an information cascade.

*Standard and Poor’s, Marunouchi 1-6-5, Chiyoda-ku, Tokyo 100-0005, Japan

†Department of Physics, School of Science, Kitasato University, Kitasato 1-15-1

Sagamihara, Kanagawa 252-0373, Japan

1 Introduction

A Keynesian beauty contest is a popular concept used to explain price fluctuations in equity markets.[1] Keynes described the action of rational agents in a market using an analogy based on a fictional newspaper contest. In the contest, entrants are asked to choose a set of the six most beautiful faces from among photographs of different women. Those entrants who would select the most popular face would be then eligible for a prize. A naive strategy would be to choose the most beautiful face according to the opinion of the entrant. Entrants are known as employing such a strategy independent voters. A more sophisticated entrant, aiming to maximize his/her chances of winning a prize, would try to deduce the majority’s perception of beauty. This implies that the entrant would make a selection on the basis of some inference from his/her knowledge of public perception. Such voters are known as copycats. To estimate public perception, people observe the actions of other individuals; then, they make a choice similar to that of others. Because it is usually sensible to do what other people are doing, the phenomenon is assumed to be the result of a rational choice. Nevertheless, this approach can sometimes lead to arbitrary or even erroneous decisions. This phenomenon is called an information cascade. [2]

Collective herding phenomena in general pose quite interesting problems in statistical physics. To name a few examples, anomalous fluctuations in the financial market [3],[4] and opinion dynamics [5] have been related to percolation and random field Ising model. A recent agent-based model proposed by Curty and Marsili [6] focused on the limitations that herding imposed on the efficiency of information aggregation. Specifically, it was shown that when the fraction of herders in a population of agents increases, the probability that herding produces the correct forecast (i.e. that individual information bits are correctly aggregated) undergoes a transition to a state in which either all herders forecast rightly or no herder does.

We can observe super-diffusive behaviour in the sense that variance grows asymptotically faster than (where is the long memory) in several fields.[7],[8],[9],[10], [11] It is characterized by the variance when . When , the diffusion of the variance becomes a standard Brownian motion. For example, in the case of daily financial data, represents the time series of data. The past price affects the present price, and the diffusion becomes faster than Brownian motion. Such phenomena can be attributed to long-range positive correlations. We may observe dynamical phase transition (from normal to super-diffusive behaviour).[9] In such a phase transition, correlation plays an important role. Further our voting model shows a similar transition. The herders make long-range correlations and display super-diffusive behaviour. Therefore, a majority of voters reach the wrong conclusion.

In this paper, we discuss a voting model with two candidates and . As mentioned above, we set two types of voters-independent and copycat. Independent voters’ voting is based on their fundamental values; on the other hand, copycat voters’ voting is based on the number of votes. In our previous paper, we investigated the case wherein all the voters are copycats.[12] In such a case, the process is a Pólya process, and the voting rate converges to a beta distribution in a large time limit.[13] Our present model exhibits a scale-invariant behaviour. This behaviour is observed in the mixing of the binary candidates. Furthermore, the power law holds over the entire range in a double scaling limit. This paper is an extension of our previous works.

Although our model is very simple, it contains three phases. We believe that it is as adequate as the percolation and random field Ising models, and that it is useful for understanding phase transition in several fields. We discuss two specific issues: one is the distribution in votes that appears for a mixture of independent and copycat voters and the other is the change in the vote distributions over time. On the basis of these above mentioned points, we discuss phase transition for information cascade.

The organization of this paper is as follows. In section 2, we introduce our voting model and define the two types of voters-independent and copycat-mathematically. In section 3, we calculate the distribution functions strictly for the special cases-independent voters always vote for either of the two candidates; their behavior is not probabilistic. Then, we obtain a solution that is an extension of the solution given in [14]; in this case, there is no phase transition. In section 4, we discuss more general cases. We use a stochastic differential equation, the Fokker-Planck equation, and a numerical simulation. In this model, we can observe phase transition at the ratio of copycats to independents through the variance of the distributions. There are three phases. If copycats constitute a majority or number half of the total number of voters, the voting rate converges more slowly than it would in a binomial distribution. If independents constitute the majority of voters, the voting converges at the same rate as it would in a binomial distribution. This implies that the proportion of copycats influences the results of the voting. The last section presents the conclusions.

2 Model

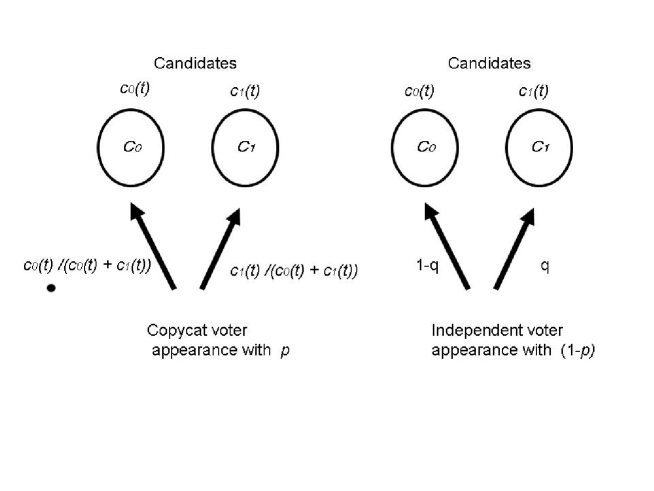

We model the voting of two candidates, and . At time , each candidate has and votes. At the beginning (), the two candidates, and , have and votes, respectively. Hereafter, we omit the time for the initial votes ( and ) and define . At each time step, one voter votes for one candidate. Voters are allowed see the number of votes for each candidate when they vote so that they have knowledge of public perception.

There are two types of voters-independent and copycat. Independent voters vote for and with probabilities and , respectively. Their votes are independent of others’ vote and depend on what they think their fundamental value is. Copycat voters vote for each candidate with the probabilities that are proportional to the candidates’ votes. If the number of votes are and at time , a copycat voter votes with probability for and for . Copycat voters’ votes are based on the number of votes.

Here, we set the ratio of independent voters to copycat voters as and , respectively. If we set , this system becomes a Pólya model with starting elements of type and starting elements of type . In this case, it is well known that the distribution of the voting rate is a beta distribution. As such, this system is a Pólya process doped with a binomial distribution.

The evolution equation for a candidate is

| (1) | |||||

is the distribution of the number of votes at time for candidate . The first and second terms of (1) denote the votes of the copycat voters; the third and fourth terms denote the votes of the independent voters. If we set as the distribution of the number of votes at time for candidate , we have the relation

| (2) |

The initial condition is . This is the relation between the back and front.

3 Exact solutions for (or )

In this section, we study the exact solution of (1) for a special case. For , we obtain the following master equation:

| (3) | |||||

At this limit, independent voters always vote for only one candidate, (if we set , independent voters vote only for ). The master equation has a simpler form:

| (4) |

When we substitute in the above equation, the last term of the RHS vanishes, and thus, the probability can be calculated easily:

| (5) |

For , we can prove (see Appendix A) that the following equality holds:

| (6) |

This is the distribution of the votes for the special case wherein the independent voters always vote for only one candidate, .

If we set , all voters are copycats, and we obtain the following reduction:

| (9) | |||||

| (12) |

This is a beta binomial distribution. At the limit , the above equation becomes a beta distribution. Note that to obtain (12), we use the identity

In [12], we discussed the physical characteristic of this model. In the limit and with fixed, the scale invariance holds over the entire range.

Here, we can calculate the momentum of these distributions to analyze them. The momentum is given by

| (13) |

We introduce quasi-momentum as

| (14) |

We can prove (see Appendix B) that the quasi-momentum can have the following form:

| (15) |

If we set , we get the average vote

| (16) |

We study . The coefficients of master equation (3) do not contain the initial votes for ; given by . If we set , the master equation does not depend on the initial conditions. Therefore, for a large limit, the behaviour of the moment does not depend on the initial conditions , and . We can also observe this in (22) and (23) in the next section. Here, we set for the representative case. Direct calculation using (15) is difficult. Hence, we study as . In the above case, distribution (6) becomes a constant distribution with cut-off . The cut-off implies a fast decay for larger values (). If we set , we get a constant distribution. Using (6), we get

| (17) |

For large time values, the only time dependent term is . In the case of , we can assume that only the first term of the summation is non-negligible. Therefore,

| (18) |

Cut-off is the inflection point of . Using (17), we can obtain . Then, the momentum is

| (19) |

(19) is a continuous function of . Hence, there is no phase transition throughout. In the next section, we study the general case in the continuous limit.

4 Asymptotic cases

To investigate long-ranged correlations, we analyze in the limit . We can rewrite (3) as

We define with the initial condition . We change the notation from to for convenience. Then, we have . The support for the law of is thus . Given , we obtain a random walk model

Let . We now consider

| (21) |

where and . Approaching the continuous limit, we can obtain the Fokker-Plank diffusion equation for this process (see Appendix C):

| (22) |

We can also obtain such that it obeys a diffusion equation with small additive noise:

| (23) |

Though (22) and (23) are equivalent, hereafter, we only deal with (23) for simplicity. Assume is random or deterministic. Let

| (24) |

be the variance of . If is Gaussian or deterministic , the law of ensures that the Gaussian is in accordance with density

| (25) |

where is the expected value of and is its variance. If is the logarithm of the characteristic function of the law of , we have

| (26) |

and

| (27) |

Identifying the real and imaginary parts of , we obtain the dynamics of the mean of as

| (28) |

The solution for is

| (29) |

Since we are interested in the voting rate obtained, we introduce a new scaled variable:

The solution for is

| (30) |

When , . This implies that the average percentage of ’s votes againt the total poll is . When , . This agrees with our assertion that the scaled distribution of votes becomes a beta distribution when is large. In this case, the mean value does not change.

From the above discussion, we can infer that the distribution becomes similar to a delta function. The question of how this distribution converges to a delta function constitutes the next problem. To investigate this, we analyze the dynamics of the variance. The dynamics of are given by the Riccati equation

| (31) |

If , we get

| (32) | |||||

If , we get

| (33) |

Now, we can summarize the temporal behaviour of the variance as

| (34) |

| (35) |

| (36) |

Here, we introduce rescaled variables

The solution for is

| (37) |

| (38) |

| (39) |

If , becomes . This agrees with our assertion that the distribution of votes becomes a beta distribution. If or , candidate gathers of all the votes in the scaled distributions, but the voting rate converges more slowly than that in a binomial distribution. If , the voting rate becomes , and the distribution converges as it would in a binomial distribution. Hence, if independent voters form a majority, the distribution of votes becomes similar to a delta function and the convergence is at the same rate as that in a binomial distribution. If copycat voters form the majority, the distribution remains the same but the convergence is at a rate slower than that in a binomial distribution. In this phase, it is difficult to ascertain the causes for the delay of the convergence. Similar phenomena can be seen in several fields. In daily financial data, the motion of the price does not represent a Markov process, and it is difficult to forecast the future price. [10] In fact, it has been pointed out that the motion of price is super-diffusive behaviour and the stochastic differential equation for price is similar to (23).[9] When all voters are copycats, the distribution becomes a beta distribution and does not converges.

Curty and Marsili [6] recently introduced a model about information cascade. Their model is based on game theory. They showed that when the fraction of herders in a population of agents increases, the probability that herding produces the correct forecast undergoes a transition to a state in which either all herders forecast rightly or no herder does. Their model is similar to the limitation of our model in the case wherein voters are unable to see the votes of all the voters but can only see the votes of previous voters. However, there is a significant difference between our model and their model with respect to the behaviour of copy cats. In their model, copycats always select the majority of votes, which is visible to them. Thus, the behaviour becomes digital (discontinuous). We aim to carry out an analysis of the influence of this behaviour in the future.

We now consider the correlation. For a beta binominal distribution, we can define the parameter .[13] This parameter represents the strength of following a decision. If we set , everyone votes for the candidate who received the first voter’s vote. On the other hand, when , copycats become independent. It should be noted that our conclusion does not depend on except when . For large , convergence is not related to , but is related to , the appearance probability of independent voters.

Here we discuss the solution in the previous section. If we set ( is the same as relation(2)), (LABEL:pd) becomes for large . This is because independent voters’ votes become deterministic. Hence, in (22), the diffusion term disappears. In (31), the noise term disappears, and the dynamics of are given by

| (40) |

Then, phase transition disappears, and the behaviour of is continuous

| (41) |

This result is acceptable, following the discussion in the previous section and that (15) is continuous with respect to . (See (19).) If there is a consensus about the fundamental value, copycat voters affect the convergence in proportion to their ratio. Further, in this case, the convergence does not depend on correlation .

In order to confirm the analytical results pertaining to the asymptotic behaviour, we perform numerical simulations. We use the master equation (5) directly.

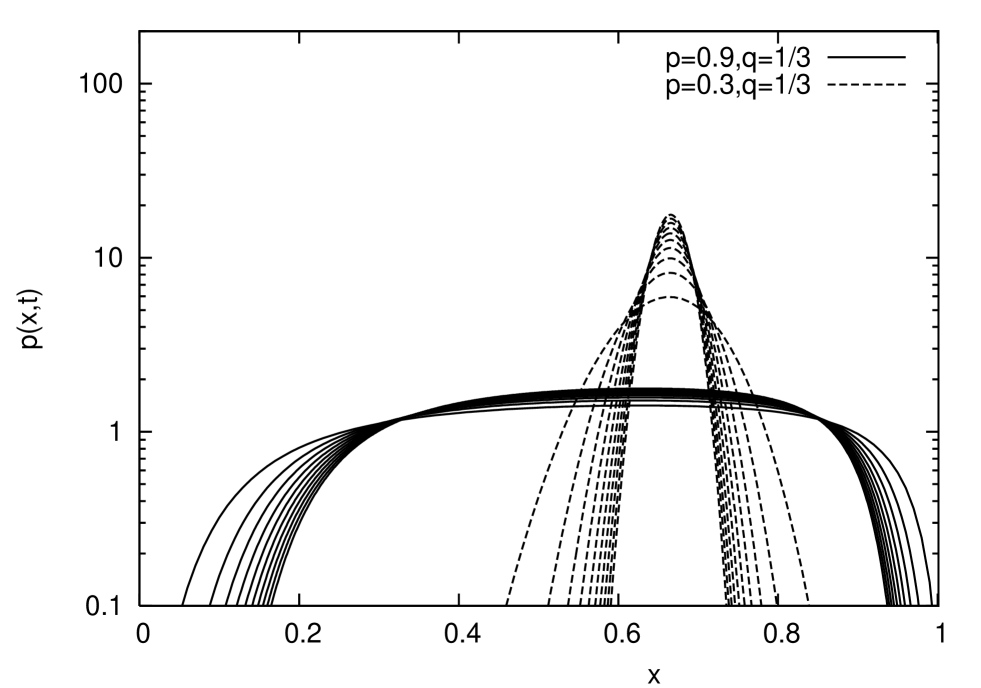

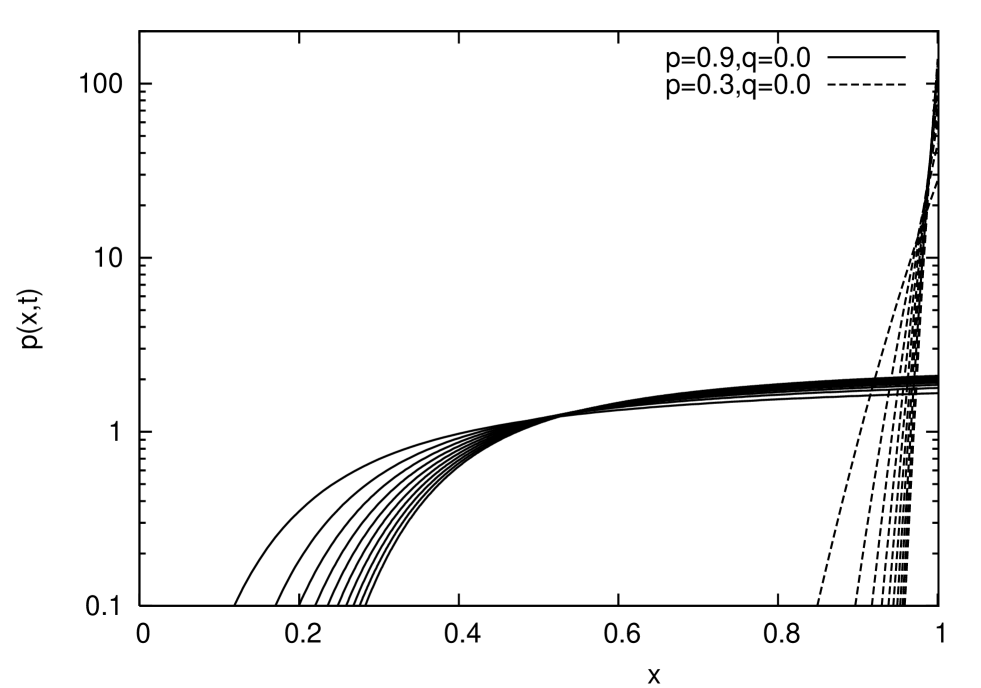

Figures 2 and 3 display the deformation of the distribution of votes for over time . Figure 2 is the case wherein the independent voters vote for with the probability , and Figure 3 is the case wherein the independent voters always vote for . We can see that the distribution converges to a delta function for the votes of the independent voters. If all voters are copycats (), the distribution becomes a beta binomial distribution. Because of the doped binomial distribution (independent voters), the distribution is deformed. For the case , we can obtain an exact solution in section 3.

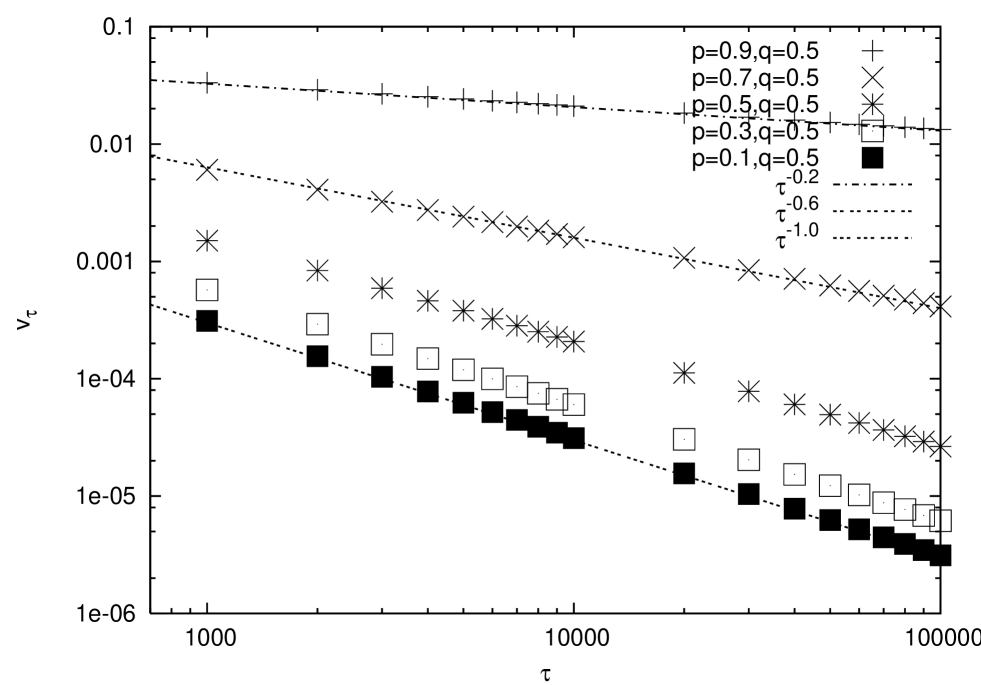

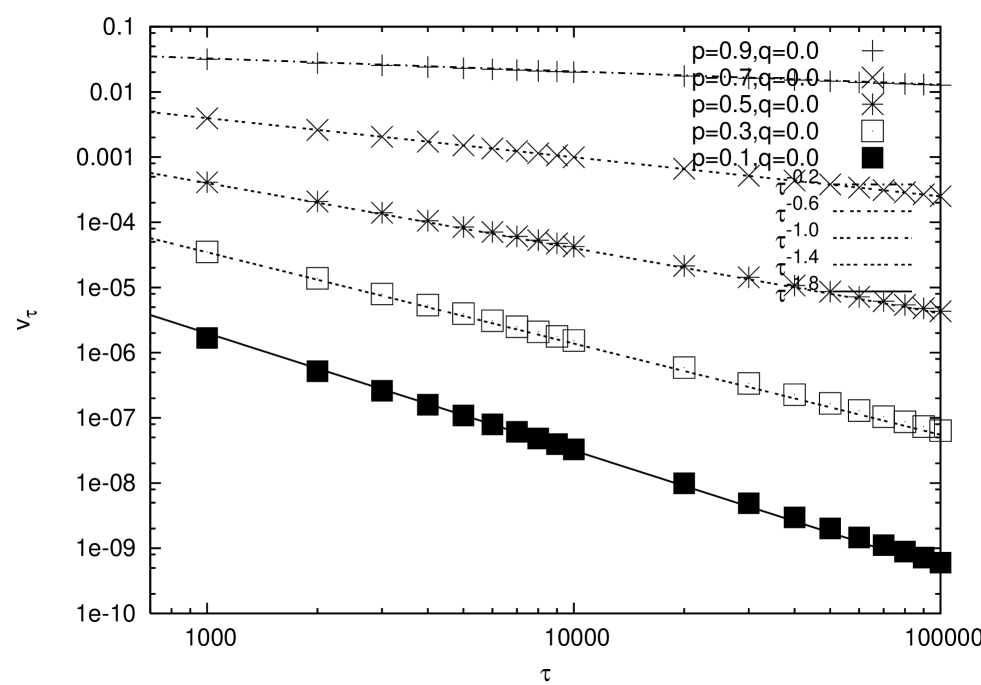

Figures 4 and 5 display the resulting scaled variance for different . The distribution converges to a delta function over time. However, there are differences between Figures 2 and 3 at . The difference is in the speed of the convergence that is characterized by the scaled variance . In the general case (), we can recognize the phase transition (Figure 4). If , the variance converges at the same rate as that in a binomial distribution (slope ). If or , super-diffusive behaviour is exhibited, and convergence is slower than that in a binomial distribution (slope ). The cases and represent two different phases.

For other cases (), the slope changes continuously (Figure. 4).

5 Concluding Remarks

We investigated a voting model that is similar to a Keynesian beauty contest. Mathematically, our model is a binomial distribution (independent voters) doped in a beta binomial distribution (copycat voters). We calculated the exact solution for special cases and analyzed the general case using a stochastic differential equation. In the special cases, there is no phase transition. We will extend this function to the general in the future. We believe that the obtained solution is a useful clue to understand phase transitions clearly.

In general, , the correlation structure, exhibits a dramatic change at a critical value of the doping. If copycats constitutes a majority or number half of the total number of voters, the variance converges slower than it would in a binomial distributions. This implies that our conclusion is extremely volatile because the fundamental value becomes irrelevant, and it is difficult to estimate the conclusion of the vote.

We observed phase transition in the limit . However, the long memory is finite; therefore, this gives rise to the question of whether we can observe the phase transition. This question arises because in this case, voters are unable to see the votes of all the voters but can only see the votes of previous voters. This model is useful to understand the model introduced by Curty and Marsili.[6] We intend to address this issue in the future.

Acknowledgment

This work was supported by Grant-in-Aid for Challenging Exploratory Research 21654054 (SM).

Appendix Appendix A

We prove the assumption (47). Multiplying (3) by and summing over we get

| (42) | |||||

where We call the second and third terms of the RHS without the coefficient and , respectively. We can rewrite as

| (43) | |||||

We can rewrite as

| (44) | |||||

Then, is given by

| (45) |

Substituting (45) in (42), we can obtain the time evolution of the summation:

For , we can prove that the following equality holds:

| (47) |

The analytic form can be obtained by multiplying both sides with and summing over

| (48) |

Appendix Appendix B

Replacing the analytical form (14), we can obtain

Further,

| (50) |

and

| (51) |

the quasi-momentum can have the following form:

Appendix Appendix C

We use and , a standard iid Gaussian sequence; our objective is to identify the drift and variance such that

| (53) |

Given , using the transition probabilities of , we get

| (54) |

Then, the drift term is . Moreover,

| (55) |

such that In the continuous limit, we can obtain the Fokker-Plank diffusion equation for this process:

| (56) |

References

- [1] Keynes J M 1936 General Theory of Employment Interest and Money

- [2] Bikhchandani S, Hirshleifer D and Welch I 1992 Journal of Political Economy 100 992

- [3] Cont R and Bouchaud J 2000 Macroeconomic Dynamics 4 170

- [4] Eguíluz V and Zimmermann M 2003 Phys. Rev. Lett. 85 5659

- [5] Stauffer D 2002 Adv.Complex Syst. 7 55

- [6] Curty P and Marsili M 2006 JSTAT P03013

- [7] Kanter I and Kessler D F 1995 Phys. Rev. Lett. 74 4559

- [8] Schenkel A, Zhang J and Zhang Y C 1993 Fractals 1 47

- [9] Hod S and Keshet U 2004 Phys. Rev. E. 70 11006

- [10] Usatenko O V and Yampol’skii 2003 Phys. Rev. Lett 90 110601

- [11] Huillet T 2008 J. Phys. A 41 505005

- [12] Mori S and Hiskado M 2010 J.Phys.Soc.Jpn 79 034001

- [13] Hisakado M, Kitsukawa K and Mori S 2006 J. Phys. A. 39 15365

- [14] Kullmann L and Kertesz J 2001 Phys. Rev. E. 63 051112