Fractional Normal Inverse Gaussian Process

Arun Kumar and P. Vellaisamy

Department of Mathematics

Indian Institute of Technology Bombay, Mumbai-400076

India

Abstract

Normal inverse Gaussian (NIG) process was introduced by Barndorff-Nielsen (1997) by subordinating Brownian motion with drift to an inverse Gaussian process. Increments of NIG process are independent and stationary. In this paper, we introduce dependence between the increments of NIG process, by subordinating fractional Brownian motion to an inverse Gaussian process and call it fractional normal inverse Gaussian (FNIG) process. The basic properties of this process are discussed. Its marginal distributions are scale mixtures of normal laws, infinitely divisible for the Hurst parameter and are heavy tailed. First order increments of the process are stationary and possess long-range dependence (LRD) property. It is shown that they have persistence of signs LRD property also. A generalization of the FNIG process called n-FNIG process is also discussed which allows Hurst parameter in the interval . Possible applications to mathematical finance and hydraulics are also pointed out. Keywords: Fractional Brownian motion, Fractional normal inverse Gaussian process, infinite divisibility, inverse Gaussian distribution, long-range dependence, subordination

1 Introduction

In recent years, there has been a considerable interest on the study of subordinated processes, since they have wide applications in modeling of financial

time series and hydraulic conductivity in geophysics. Also, these processes have interesting probabilistic properties (Sato (2001)).

A subordinator is a one dimensional

Levy process with non-decreasing sample paths (a.s.) (Applebaum (2004) p. 49).

A subordinated process model formulation was originally considered by Mandelbrot and Taylor (1967).

They considered a one-sided stable law of index (with for the distribution of the subordinator with subordination

to a Brownian motion , which gives a

symmetric stable distribution of index for .

They interpreted the subordinator as trading volume (or number of transactions) upto time t. Clark (1973) used lognormal process

as a subordinator. Madan and Seneta (1990) considered gamma process as a subordinator and they called the

subordinated process variance gamma (VG) process. Barndorff-Nielsen (1997) introduced normal inverse Gaussian (NIG) process which is

obtained by subordinating Brownian motion with drift to an inverse Gaussian process for modeling of stochastic volatility. Heyde (2005) discussed

Student Levy process which is obtained by taking inverse gamma process as a subordinator.

The marginals of these subordinated processes are generally heavy tailed and are more peaked around the mode. The subordinated processes are useful for

modeling of the returns from financial assets (stocks). Indeed, log-returns from financial time series often exhibits a significant dependence

structure ( Shephard (1995)).

Subordinated processes, with subordination to Brownian motion have independent increments.

So, the above processes are limited in nature and may not be suitable for financial data which exhibits a dependence structure.

Recently, fractional Brownian motion (FBM) is used instead of Brownian motion for subordination, as its leads to LRD property,

that is, the covariance function = cov of the stationary time series decay so slowly such

that the series sum diverges (Beran (1994)). FBM is a natural

generalization of Brownian motion (Mandelbrot (1968)). The FBM with Hurst parameter is a centered Gaussian process with

and with covariance function

| (1.1) |

where Var(). Also, . The FBM has also the following integral representation (Mandelbrot (1968))

| (1.2) |

Its first order increments , called fractional Gaussian noise are stationary and exhibits LRD property, when . Mandelbrot (1997) considered , where is an FBM and the activity time process is a multifractal process with non-decreasing paths and stationary increments. Recently, Kozubowski et.al. (2006) introduced and studied fractional Laplace motion (FLM) by subordinating FBM to a gamma process. They have pointed out the applications of FLM to modeling of hydraulic conductivity in geophysics and financial time series. In the same spirit, we subordinate the FBM to in inverse Gaussian process to obtain FNIG process and study their probabilistic properties.

2 FNIG Process

The density function of an inverse Gaussian distribution with parameters and denoted by , is given by

| (2.1) |

The inverse Gaussian (IG) subordinator with parameters and is defined by (Applebaum (2004), p.51)

| (2.2) |

where and . Here, denotes the first time when Brownian motion with drift hits the barrier . Another interpretation of IG subordinator is that it is a Levy process such that the increment has inverse Gaussian distribution. We call as IG process with parameters and . Barndorff-Nielsen (1997) introduced and studied the subordination of Brownian motion with drift to an IG subordinator. Let IG, where and . Specifically, he studied the process , where and called NIG process with parameters and , denoted by NIG. The process is a Levy process and its marginals have heavier tails than Gaussian distribution. Since NIG process is a Levy process its increments do not possess LRD property. Our aim here is to introduce dependence between the increments by taking FBM instead of Brownian motion. Let be an FBM and let be an IG process with parameters and . Also, we assume , when We now define a new process , by subordinating FBM to an IG process:

| (2.3) |

where stands for equality of finite dimensional distributions. We call fractional normal inverse Gaussian (FNIG) process with parameters . Note that is a variance mixture of normal distribution with mean zero. Consequently, for all , can be represented as

| (2.4) |

where is a standard normal variable and is independent of having an inverse Gaussian IG distribution.

Remark 2.1.

In the representation (2.3), the distribution of and determine each other, i.e.,

| (2.5) |

The proof is as follows.

The step above the last one follows by the uniqueness of the Laplace transform.

Remark 2.2.

Since , we have

| (2.6) |

Also, by the law of large numbers for the subordinator (see Bertoin (1996), p.92),

Using the result that, iff for every bounded continuous function and taking , we have from (2.6)

2.1 Basic Properties of FNIG Process

We first obtain the density of one-dimensional distributions.

Proposition 2.1.

Let be an FNIG process with parameter vector . Then the density function of is given by

| (2.7) |

which is clearly symmetric about origin.

Proof. Since

we have

| (2.8) | |||||

the result follows.

Remark 2.3.

When and ,

and so represents a Cauchy process (see Feller 1971, p. 348).

Let is the modified Bessel function of third kind with index . An integral representation of (Jrgensen (1982), p. 170) is

| (2.9) |

Barndorff-Nielsen (1997) considered the NIG distribution with density

where

| (2.10) |

and is modified Bessel function of third kind and index 1. When , we have from (2.7)

| (2.11) |

which is same as the distribution of NIG.

We have the following result concerning the moments of FNIG process.

Proposition 2.2.

If is the FNIG process with parameters and , then

| (2.12) |

where

Proof. Using (2.4),

since and are independent. The r-th moment of IG() distribution (Jrgensen (1982), p. 13) is given by

| (2.13) |

Using (Jrgensen (1982), p. 170), we now obtain

The result follows by using the fact that = for a standard normal variate .

Remark 2.4.

Note that for large , (Jrgensen (1982) p. 171) which shows that, , as . This implies the increments of the FNIG process behave like the increments of FBM, as the lag .

Remark 2.5.

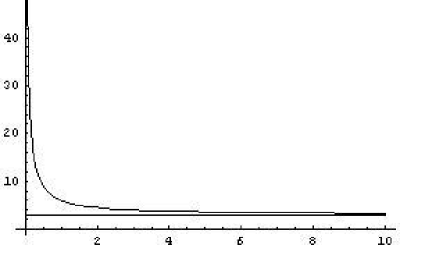

Let be the FNIG process with parameter . Using (2.12), the kurtosis of is given by,

A plot of against shows that is a decreasing function in t. This implies that the marginals of

(having for all ) have heavier tails and a larger degree of peakedness as compared to the Gaussian distribution. Since

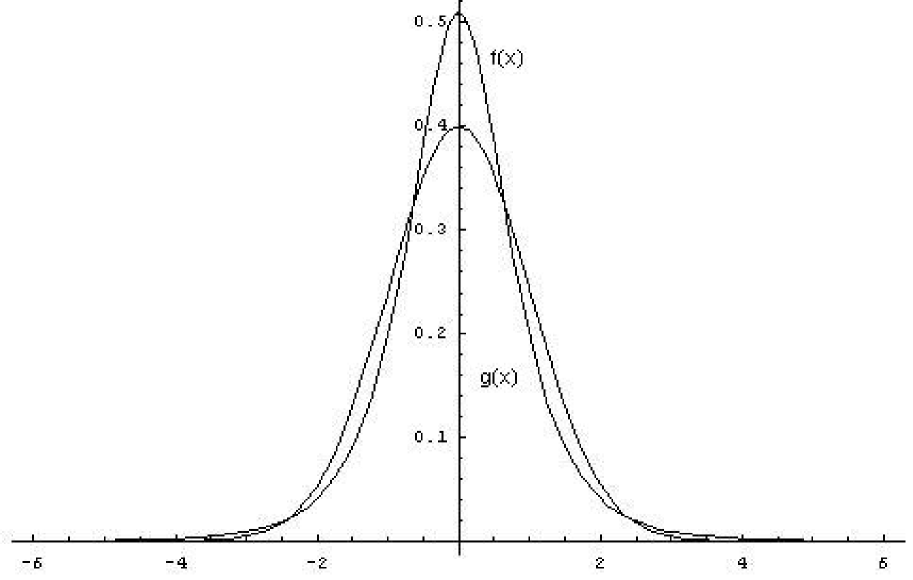

as , the process becomes Gaussian with an increasing lag. Observe from Figure 2 that the

density of the standardized (variance unity) random variable , denoted by have higher degree of peakedness and heavier tails than standard

normal density denoted by . Also, the density of tends to a normal density for large values of .

2.2 The Covariance Structure

The following result concerning the covariance function of FNIG process, follows using the fact and using (2.12).

Proposition 2.3.

The covariance function of FNIG process for , is given by

| (2.14) | |||||

Proposition 2.4.

For , as and

Proof. Without loss of generality, consider the case

, where with . Let . We discuss the following

three cases.

Case1. Let . Then , and from (1.1),

. Hence, using (2.14),

Case 2. Suppose that for some , so that , as In this case, we have

Hence,

Case 3. Suppose that so that . In this case,

| (2.15) |

An asymptotic expansion for for large (see equation A.9 of Jørgensen (1982), p.171) is

| (2.16) |

where Using the above result, we get , and

| (2.17) | |||||

which follows by using binomial series expansion for , and then allowing such that The result now follows from (2.15) and (2.17).

2.3 FNIG noise

Let be an FNIG process. Then the first-order increment process

| (2.18) |

for a lag is stationary.

We have the following result on persistence of signs LRD introduced by Heyde (2002). A process is said to have persistence of signs LRD property if LRD holds for (see Heyde (2002)), where

| (2.22) |

Proposition 2.5.

The increment process has persistence of signs LRD property, when .

Proof.

Note that has the same finite dimensional distribution as that of ,

which has persistence of signs LRD property (see Proposition 1 of Heyde(2002)).

We call the process

| (2.23) |

FNIG noise. Next result on the covariance function of FNIG noise directly follows from (2.14) and Proposition (2.2).

Proposition 2.6.

The next result shows the asymptotic behavior of the covariance function of .

Proposition 2.7.

Let be fixed. Then as

| (2.25) |

Proof. Using the asymptotic expansion for given in (2.16), we have,

| (2.26) | |||||

The last equality follows by using binomial series expansion of and . From (2.26),

| (2.27) |

since .

Corollary 2.1.

FNIG noise process has LRD property for .

Proof. The covariance function of can easily be obtained from (2.24) as

for

Further, we have

| (2.28) |

From (2.28), we have , for .

Remark 2.6.

Observe that when and , FNIG noise behaves like fractional Gaussian noise with an increasing lag . Also, the covariances (and correlations) are positive when and negative when , as in the case of FBM.

A stochastic process is said to be self-similar with Hurst parameter if for any , we have

| (2.29) |

A stationary process is related to a self-similar process by the Lamperti transformation defined by

| (2.30) |

(see Lamperti (1962)). The process , is self-similar with exponent . The process may or may not have strictly stationary increments. If we apply the Lamperti transformation (2.30) to defined in (2.18), we obtain self-similar process that do not have strictly stationary increments. In fact, its covariance function for , is given by

| (2.31) | |||||

2.4 Infinite Divisibility

The generalized gamma convolutions (g.g.c.) were introduced by Thorin (1978a). They have turned out to be a powerful tool in proving infinite divisibility of various distributions (Bondesson (1979)). A distribution on is said to be a g.g.c. if it is the weak limit of finite convolutions of gamma distributions (see Steutel and Van Harn (2004), p.349). Bondesson (1979) proved that any density on of the form

| (2.32) |

with all the parameters strictly positive, and , are g.g.c.’s; consequently all densities (distributions) which are weak limit of densities of the form (2.32) are g.g.c.’s and thus infinitely divisible. Also, if has a density of the form (2.32), the weak limit possibilities included, then the density of , is also a g.g.c. (Bondesson (1979)) and hence infinitely divisible.

Proposition 2.8.

When , the marginal distributions of FNIG process are infinitely divisible.

Proof: It is known that inverse Gaussian distributions or more generally generalized inverse Gaussian (GIG) distributions are g.g.c.’s (Halgreen (1979)) and hence infinitely divisible. Using Bondesson (1979) result, we conclude that the stochastic variance has a distribution which is a g.g.c., when . Since , and is a variance mixture of normal distribution, it is infinitely divisible (Kelker (1971)), when .

Remark 2.7.

(i)Kelker (1971) discussed by an example that the variance mixtures of normal distributions can be infinitely divisible, even when the

stochastic variance is not.

However, we have not been able to establish infinite divisibility of FNIG process for .

(ii) Halgreen (1979) showed that variance mixtures of normal distribution are self-decomposable,

if the stochastic variance is a g.g.c. So, the marginals of FNIG process are self-decomposable, when .

2.5 Small Deviation Probabilities

Small deviation probability (in the logarithmic level) for a stochastic process deals with the asymptotic behavior of

For the inverse Gaussian subordinator , the Laplace exponent , defined by is given by

We have

The following results on the small deviation probabilities for FNIG process , follows immediately by Theorem 2.1 of

Linde and Shi (2004).

(a) The quenched case (conditional probability :

(b) The annealed case (product probability):

where , means, and is the -norm.

3 nth-Order Fractional Normal Inverse Gaussian (n-FNIG) Process

A generalization of FBM called nth-order FBM, is discussed by Perrin et.al. (2001). This generalization allows the Hurst parameter in the range . Note that n-FBM is obtained by subtracting terms upto the nth-order of the limit expansion of the kernel from (1.2), leading to the definition of extended FBM:

Definition 3.1.

The nth-order fractional Brownian motion (n-FBM) is defined by

| (3.1) | |||||

The covariance function of n-FBM is given by

| (3.4) |

where

| (3.5) |

Also, the variance of is

| (3.8) |

To allow Hurst parameter in the range , we study nth-order FNIG process by subordinating inverse Gaussian process with nth-order fractional Brownian motion (n-FBM). We define n-FNIG process as

| (3.9) |

All the properties of marginals of n-FNIG process follow similar to that of FNIG process by replacing by . We can find the covariance function of n-FNIG process with the help of (3.4) s.t.

| (3.13) | |||||

Also, we have

| (3.16) | |||||

| (3.19) | |||||

| (3.23) | |||||

The last statement follows by using (2.13). The covariance function of n-FNIG process can be put in explicit form by using (3.16) and (2.13) that is given by

| (3.29) | |||||

For , the covariance function of n-FNIG process becomes covariance function of FNIG process. Similar to Proposition (2.4) we can show that as and

3.1 nth-Order Fractional Normal Inverse Gaussian Noise

For a function , we denote the kth-order increments by

| (3.30) |

Perrin et.al. (2001) showed that nth-order increments of n-FBM are stationary and hence are called nth-order fractional Gaussian noise. Covariance function of nth-order fractional Gaussian noise is given by (see Perrin et.al. (2001))

| (3.33) |

where . The nth-order increments of n-FNIG process are stationary and the associated noise is obtained by taking nth-order increments of the n-FNIG process. If is an n-FNIG process, then, for any

| (3.34) |

is a stationary process. We call the process

| (3.35) |

an nth-order fractional inverse Gaussian noise (n-FNIGN). Using (3.33), we find the covariance function of n-FNIGN process.

Proposition 3.1.

Let be the n-FNIGN process . Then, for any , where , we have

where .

4 Simulation

The sample paths of FNIG process can be simulated by subordinating a discretized IG process with fractional Brownian motion. We first simulate a discretized IG process on equally spaced intervals. Then we simulate , which conditionally on the values of is a second order Gaussian process with the explicit covariance function of FBM evaluated at the values of the IG process. Using Choleski decomposition of the covariance function of the random vector . Then , where , a multivariate normal vector. The algorithm is given below.

-

(i)

Choose a finite interval say our aim to have simulated values at .

-

(ii)

Generate n IG variates , where , by using the algorithm given by Michael, Schucany and Hass (see Cont and Tankov (2004), p.182).

-

(iii)

Form the matrix , where .

-

(iv)

Using Cholesky decomposition find such that .

-

(v)

Generate a n-dimensional standard normal vector .

-

(iv)

Compute . Then denotes n-simulated values from FNIG process.

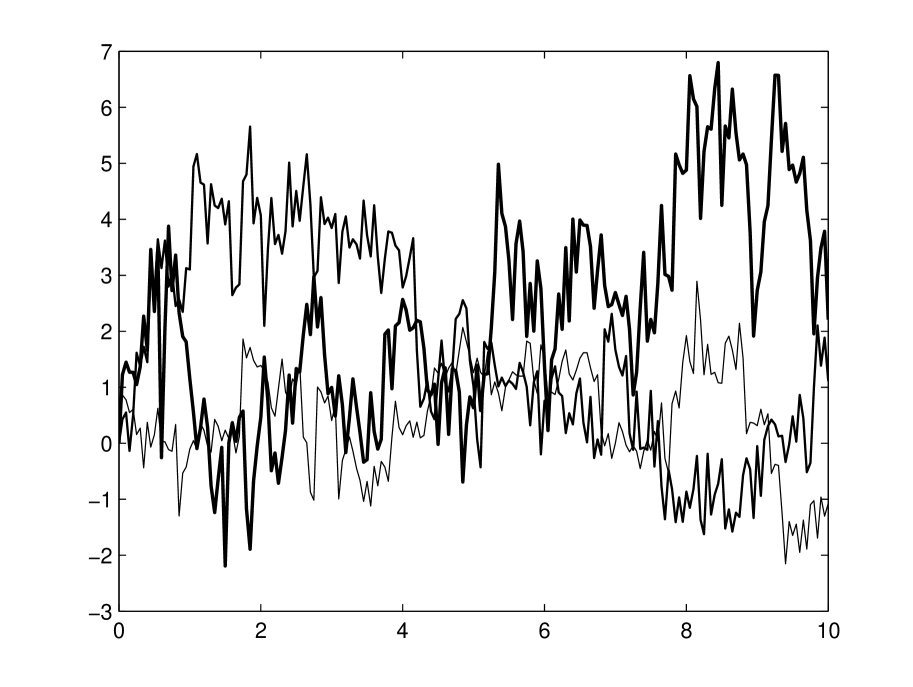

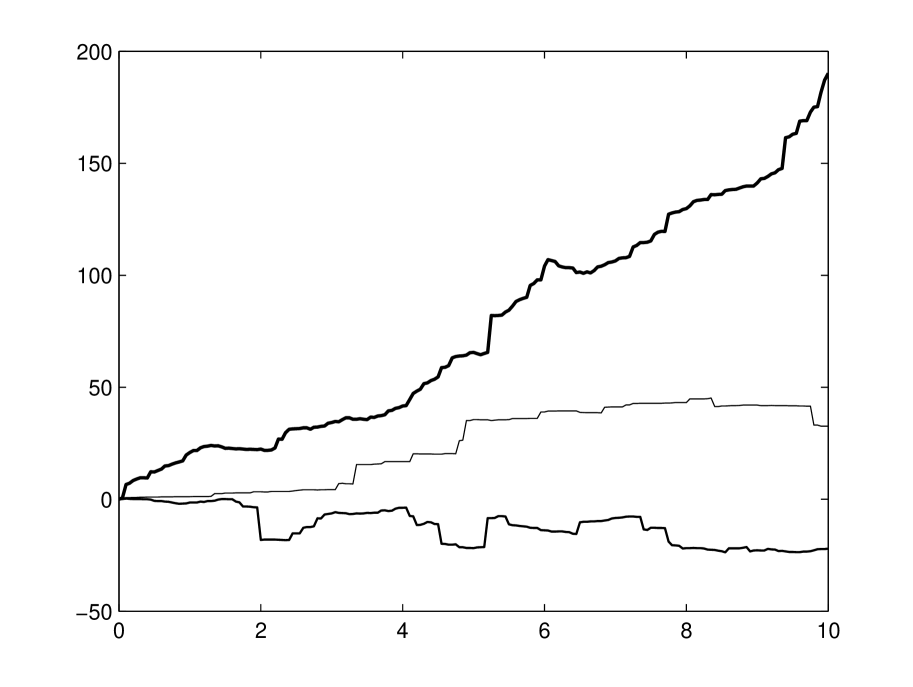

Figures 3 and 4 give the simulated sample paths of FNIG process for the case , and for the choices (thin lines), (medium thick lines) and (thick lines). Note that sample paths for the case (Figure 4) have less fluctuations, compared to the case when (Figure 3). This is because of the persistence of signs LRD property of the FNIG process for .

5 Applications

Recently, subordinated processes have been found useful models in finance and geophysics. Most common processes in literature include variance gamma (Madan and Seneta (1990)), normal inverse Gaussian (Barndorff-Nielsen (1997)), FATGBM model (Heyde (1999)), multifractal model (Mandelbrot et.al. (1997)), Student processes (Heyde and Leonenko (2005)) and FLM (Kozubowski et.al. (2006)). Let denote the value of a stock at time . Heyde (1999) considered the model

| (5.37) |

where is an increasing process with LRD property and having stationary increments and heavy tails. Also, is independent of . Then the log-return

is an uncorrelated process having heavy tails. Mandelbrot et.al. (1997) considered the model

where is a multifractal process with increasing sample paths and stationary increments. It is known that NIG distributions are more suitable than Gaussian or generalized hyperbolic distributions (see Barndroff-Nielsen(1997)). Shephard (1995) observed that log-returns often exhibits dependence structure. Also, the autocorrelations of asset returns are often insignificant, but this is not true for small time scales data (Cont and Tankov (2004)). Also, Heyde (2002) observed that the log-returns for a financial time series have persistence of signs LRD property, i.e., the process has the tendency to change signs more rarely than under independence or weak dependence. We have shown that FNIG process has LRD property and also have persistence of signs LRD property. Also, FNIG process is a non-stationary process with stationary increments, and reduces to Gaussian process, for sufficiently large lags, and hence could be useful for large-scale models based on fractional Brownian motion and non-Gaussian behavior on smaller scales. Processes with these properties were used by Molz and Bowman (1993) and Painter (1996) for analyzing hydraulic conductivity measurements. Also, Meerschaert et.al. (2004) used FLM to study the hydraulic conductivity measurements. Hence, we believe that FNIG process could serve a useful model in the area of finance, biology, geophysics and etc., where the dependence structure of increments and heavy tailedness of marginals play an important role. Acknowledgment The first author wishes to thank Council of Scientific and Industrial Research (CSIR), India, for the award of a research fellowship. References

-

Applebaum, D. (2004). Levy Processes and Stochastic Calculus (Cambridge Studies in Advanced Mathematics). Cambridge University Press, Cambridge.

-

Barndorff-Nielsen, O. E. (1997). Normal inverse Gaussian distributions and stochastic volatility modeling. Scand. J. Statist., 24, 1-13.

-

Beran, J. (1994). Statistics for Long-Memory Processes. Chapman & Hall, New York.

-

Bertoin, J. (1996). Levy Processes. Cambridge University Press, Cambridge.

-

Bondesson, L. (1979). A general result on infinite divisibility. Ann. Probab. 7(6), 965–979.

-

Clark, P.K. (1973). A subordinated process model with finite variance for speculative prices. Econometrica, 41, 135-155.

-

Cont, R. and Tankov, P. (2004). Financial Modeling with Jump Processes. Chapman & Hall CRC Press, Boca Raton.

-

Devroye, L. (1986). Nonuniform Random Variate Generation. Springr, New York.

-

Feller, W. (1971). Introduction to Probability Theory and its Applications. Vol. . John Wiley, New York.

-

Halgreen, C. (1979). Self-decomposability of the generalized inverse Gaussian and hyperbolic distributions. Z. Wahrsch. Verw. Gebiete. 47, 13–17.

-

Heyde, C.C. (1999). A risky asset model with strong dependence through fractal activity time. J. Appl. Probab. 34(4), 1234-1239.

-

Heyde, C.C. (2002). On modes of long-range dependence. J. Appl. Probab. 39, 882-888.

-

Heyde, C.C. and Leonenko N. N. (2005). Student processes. Adv. Appl. Probab. 37, 342-365.

-

Kelker, D. (1971). Infinite divisibility and variance mixtures of the normal distribution. Ann. Math. Statist. 42, 802-808.

-

Kozubowski, T.J., Meerschaert, M.M., and Podgorski, K. (2006). Fractional Laplace motion. Adv. Appl. Prob. 38, 451-464.

-

Lamperti, J. W. (1962). Semi-stable stochastic processes . Trans. Amer. Math. Soc. 104, 62-78.

-

Linde, W. and Shi, Z. (2004). Evaluating the small deviation probabilities for subordinated Levy processes. Stochastic Process. Appl. 113, 273-287.

-

Madan, D.B., Carr, P. and Chang, E.C. (1998). The variance gamma process and option pricing. Europ. Finance Rev. 2, 74-105.

-

Madan, D.B. and Seneta, E. (1990) The variance gamma (V.G) model for share markets returns. J. Business 63, 511-524.

-

Mandelbrot, B.B. (2001). Scaling in financial prices: I. Tails and dependence. Quant. Finance 1, 113-123.

-

Mandelbrot, B.B., Fisher, A. and Calvet, L. (1997). A multifractal model of asset returns. Cowles Foundation Discussion Paper No. 1164.

-

Mandelbrot, B.B. and Taylor, H. (1967). On the distribution of stock price differences. Operat. Res. 15, 1057-1062.

-

Mandelbrot, B.B and Van Ness, J.W. (1968). Fractional Brownian motion, fractional noises and applications. SIAM Rev. 10, 422-438.

-

Meerschaert, M.M., Kozubowski, T.J., Molz, F.J., and Lu, S. (2004). Fractional Laplace model for hydraulic conductivity. Geophys. Res. Lett. 31, p. L08501.

-

Molz, F. J., and Bowman, G.K. (1993). A fractal-based stochastic interpolation scheme in subsurface hydrology. Water Resour. Res. 32, 1183-1195.

-

Painter, S. (1996). Evidence for non-Gaussian scaling behavior in heterogeneous sedimentary formations. Water Resour. Res. 32, 1183-1195.

-

Perrin, E., Harba, R., Berzin-Joseph, C., Iribarren, I. and Bonami, A. (2001). nth-Order fractional Brownian motion and fractional Gaussian noises. IEEE Trans. Sig. Proc. 49, 1049-1059.

-

Sato, K. (2001). Subordination and self-decomposability. Statist. Probab. Lett. 54 (3), 317–324.

-

Shephard, N. (1995). Statistical aspects of ARCH and stochastic volatility. In Time series models. In econometrics, finance and others fields (eds D.R. Cox, D.V. Hinkley & O.E. Barndorff-Nielsen), 1-67. Chapman & Hall, London.

-

Steutel, F.W. and Van Harn, K. (2004). Infinite Divisibility of Probability Distributions on the Real Line. Marcel Dekker, New York.

-

Thorin, O. (1978a). An extension of the notion of a generalized gamma convolution. Scand. Actur. J., 141-149.