Using Differential Equations to Obtain Joint Moments of First-Passage Times of Increasing Lévy Processes111Revised

Abstract

Let be a Lévy subordinator, that is, a non-decreasing process with stationary and independent increments and suppose that . We study the first-hitting time of the process , namely, the process , . The process is, in general, non-Markovian with non-stationary and non-independent increments. We derive a partial differential equation for the Laplace transform of the -time tail distribution function , and show that this PDE has a unique solution given natural boundary conditions. This PDE can be used to derive all -time moments of the process .

1 Introduction

Consider a non-decreasing Lévy Process , starting from , which is continuous from the right with left limits. Such a process is called a subordinator. It has stationary and independent increments and is characterized by its Laplace Transform

The function is called the Laplace exponent and is given by the Lévy-Khintchine formula:

| (1) |

where is the drift and is a measure on which satisfies (see [1], [7] or [8]).

We want to study the first-passage time of such a process, focusing on its finite-dimensional distributions. The first-passage time of a subordinator , is a new process , commonly called an inverse subordinator, and is defined as follows:

It is worth noting that in certain cases, the Lévy subordinator is itself a first passage time of another Lévy processes. For example, the -stable subordinator is the first passage time of standard Brownian motion, and the inverse Gaussian subordinator is the first passage time of standard Brownian motion with drift ([1], exercise 2.2.10). For these examples, is the “first-passage time of a first-passage time”.

Inverse subordinators appear in a variety of applications. For instance, they are used in the study of scaling limits of continuous-time random walks and fractional kinetics, [4], [5], [14], [17], [2]. Here, the time variable of a Markov process (typically Brownian motion), is replaced by an inverse -stable subordinator, with . This particular time change gives rise to anomalous diffusion, or sub-diffusion, where the variance of the process grows at a rate which is non-linear in time. The -stable subordinator is “fast” because all moments of order or less are infinite. An “ultrafast” subordinator introduced in [16] and [14] is a process which has, in general, no finite moments. While these subordinators have infinite moments, the moments of their inverses are finite. For the -stable subordinator, the first moment of its inverse subordinator, , grows as . For the ultrafast subordinator, the inverse is “ultraslow”, and can grow like a slowly varying function.

Our goal in this paper is to characterize the -point distribution function of a general inverse subordinator with a simple partial differential equation and to use this PDE to derive explicit expressions for joint moments. A PDE was derived (heuristically) by [4], [5] for the joint density function in the special case of -stable inverse subordinators and was used to obtain joint moments of these processes. To obtain precise results in the general case, we found it convenient to use suitable modified cumulative distribution functions instead of densities. An alternative approach, using Cox processes was followed by [15], who also obtains joint moments of increments of inverse subordinators. Our results are implemented in [19], where we develop algorithms for computing the moments numerically.

This paper is organized as follows: The -point distribution of is studied in Section 2, where we derive a PDE for the Laplace transform of the -point tail distribution function . In Section 3, we use this PDE to calculate the -point moments of a general inverse subordinator. The examples presented briefly in Section 4 are discussed in detail in the companion paper [19]. For convenience, we provide an appendix which contains key path properties of inverse subordinators.

2 PDE for the Multiple-time Distribution Function of Inverse Subordinators

Unlike the Lévy process , the inverse subordinator is often non-Markovian. Thus, we must consider all finite-dimensional distributions. For , define

| (2) |

To simplify notation, we will write . In the following, . Also, will denote the space of continuously differentiable functions on . The following theorem shows the Laplace transform,

of satisfies a PDE. Observe that since for . We let denote in (2) with and the other arguments unchanged.

Theorem 2.1

Let be a general Lévy subordinator and let be the inverse subordinator of . For , the Laplace Transform of the -point tail distribution of defined by (2) is the unique solution in to the following PDE

| (3) |

together with the boundary conditions

| (4) |

Proof.

From Proposition A.2, we have that

Let and fix . Calculating the Laplace transform in of , we have

Integrating by parts in , we obtain

Now rewrite the variables is an increasing order, , where and is a permutation of the integers . We add and subtract terms in the summation above and use the independence and stationarity of the increments of to obtain

| (5) | |||||

Differentiating with respect to , , we have that satisfies the system of PDEs

Adding these equations together gives

Since is simply a permutation of the integers , this is equivalent to (3).

Now we claim that with the boundary conditions (4), the tail probability is the unique solution to the PDE (3) in . Suppose is another solution in to (3) with the boundary conditions (4). Define . By linearity, is also a solution to (3) with boundary conditions

| (6) |

Fix , and WLOG, assume (if not we can simply re-index as before). Proceeding by the method of characteristics ([12], section 3.2), we define the function

| (7) |

Observe that (6) can now be written as

| (8) |

Differentiating (7) with respect to and using the definition of , we have

| (9) |

Since satisfies the PDE (3), equation (9) implies that satisfies the ODE

Now, using as a initial condition and using (8), we have

Thus, for is a solution to this initial value problem, and by standard uniqueness theory of ODEs ([9], chapter 2), this is the unique solution. Hence

implying is the unique solution to (3) with the boundary conditions (4).

-

Remark.

The boundary conditions (4) are natural ones, since they imply that the -dimensional distribution function can be reduced to the dimensional distribution function when for some .

-

Remark.

One might wonder why a PDE for the -time Laplace transform of is useful when in fact we can write down its solution (5) in closed form. It is, because:

-

–

It simplifies the calculation of the moments of , which we demonstrate in Section 3.

-

–

Understanding the dynamics of is useful in the study of more complicated processes. For example, in [5], the PDE (3) in the case of the -stable process (where ) is used to derive equations corresponding to the -time distribution functions of the so-called fractional kinetic process , where is Brownian motion and is an inverse -stable subordinator. This process appears as a scaling limits for various trap models, [2]. Thus, the PDE (3) can extend this analysis done in [5] to a larger class of processes.

-

–

3 Moments of Inverse Subordinators

In this section we use Theorem 2.1 to calculate moments of a general inverse subordinator. The utility of the PDE (3) will become clear in that it will simplify many of the following computations.

Before we calculate moments, we first argue that all moments of an inverse subordinator are finite. Notice that, for any , we can bound the tail distribution of using (31) from the proof of Proposition A.2 and Markov’s inequality:

| (10) |

which implies that for any .

The Laplace transform of with has a simple form:

| (12) |

where we have used integration by parts to calculate . Of particular importance is the mean of . Let . From (12) has Laplace transform given by

| (13) |

We will see in the following that characterizes all finite-dimensional distributions of the process . While the Laplace transform of is easy to express in terms of , calculating the inverse is, in general, not always an easy task. In [19], a numerical method is given for computing for general .

-

Remark.

Although the subordinator is, in general, different from a renewal process, it has some of its characteristics. For example, it satisfies the so called renewal theorem, which states that if the mean of the subordinator is finite, then , as . This was proven using various methods in [15], [8] and [11]. This fact can be easily seen from the Laplace transform of given above. Indeed, if has finite mean, then from the Lévy-Khintchine formula,

(14) and thus as . From (13), as and the Tauberian theorem ([7], page 10) implies the renewal theorem:

(15) Thus, for subordinators with finite mean, their mean first-passage time will exhibit a non-linear transient behavior for small times, followed by a linear behavior for large times.

As an application of the differential equation given in Theorem 2.1, we obtain expressions of the Laplace transforms for the -time integer moments of in terms of Laplace transforms of lower-order moments.

Theorem 3.1

Let be a general Lévy subordinator with Lévy exponent and let be the inverse subordinator of . For positive integers , let

| (16) |

In the special case , we will simply write . The -time Laplace Transform of is given in terms of strictly lower order moments by

| (17) |

Proof.

We first write in terms of the tail probability ,

where . Taking the Laplace transform in and rearranging the order of integration yields

| (18) |

Now multiply through by and apply Theorem 2.1 to obtain

| (19) |

| (20) |

Let us now focus on the inner-most integral above. If , we have

| (21) | |||||

Above we have used the fact that exponentially as , which follows from (5), and that from (4).

If , we integrate by parts and get

| (22) |

-

Remark.

Theorem 3.1 is equivalent to Theorem 2.1 in [15]. There, the result gives the joint moments of increments of the inverse subordinator: , where , and are positive integers, and expresses them with an integral expression. The formulas given here, which are obtained using different methods, give directly and have the added advantage of expressing higher order moments in terms of lower order ones. Also, out results give the Laplace transform of all -time moments.

Recursion: Theorem 3.1 gives expressions for the Laplace transform of all -time moments of a general inverse subordinator. In theory, these -dimensional Laplace transforms can be inverted, however doing so directly can be a formidable task. As an alternative, we take advantage of the recursive nature of equation (17). Let be the order of the moment , i.e. . Observe that equation (17) implies that moments of order can be calculated using a linear combination of convolutions involving moments of order and the inverse Laplace transform of the function , which we address below. Thus, if one has , then all moments can be obtained inductively using this method.

3.1 Getting the inverse Laplace transform

To calculate moments of inverse subordinators, we must be able to invert Laplace transforms of the form , where the function is known. Hence, we must first obtain the inverse Laplace transform of the function . Following [7], section III.1, define the renewal measure to be the Borel measure whose distribution function is given by . From this we see that for a.e. ,

| (23) | |||||

By approximating with step functions, this can be extended to where is a continuous function. Choosing , we get that the Laplace transform of the renewal measure is given by

Thus, for an arbitrary function , the inverse Laplace transform of is given by the convolution of with the renewal measure, i.e.

| (24) |

This can be generalized to dimensions. For ease of notation, write , where is interpreted as a generalized function(since might contain jumps). If , then

This follows from standard rules of Laplace transforms (see for example [18], page 169). This can be understood by writing and then computing by viewing as a shift. Using the fact that , the above reduces to

| (25) | |||||

Using from Theorem 3.1, equation (25) lets one compute any order moments by successive convolutions. As an application, we give a general expression for the covariance of an inverse subordinator in terms of and .

Corollary 3.2

Let be a Lévy subordinator with Lévy exponent , and let be the inverse subordinator of . For , the covariance , of is given by

| (26) |

Proof.

We have

| (27) | |||||

| (28) |

where we have used the notation (16). From Theorem 3.1, the Laplace transform of is

Now, (25) gives

- Remark.

Let be a strictly increasing Lévy subordinator with inverse . Then using Corollary 3.2, one can show that has stationary and uncorrelated increments if and only if for some constant .

4 Examples

Examples are discussed in [19]. We focus there on the following three important families of subordinators:

-

•

Poisson and Compound Poisson processes. Their Lévy exponent is given by

where is a finite measure on .

-

•

“Mixed” -stable processes. Their Lévy exponent is given by

Here is some probability measure on . Notice the -stable subordinator corresponds to the choice .

-

•

Generalized Inverse Gaussian Lévy processes, which are Lévy processes whose time 1 distribution is given by the Generalized inverse Gaussian distribution. This family of distributions was shown to be infinitely divisible in [3] and its Lévy-Khintchine representation is derived in [10]. This family includes the gamma process, inverse Gaussian process and the reciprocal gamma process.

In some cases, an analytic expression for the mean first-hitting time can be given for the above processes, however, this is usually not the case. In [19], we give numerical methods for inverting the Laplace transform . We test these methods in cases where can be computed explicitly. We then study the three examples above in detail, focusing in each case on the asymptotic behavior of and on computing and higher order moments numerically.

Appendix A Appendix: Path Properties of Inverse Subordinators

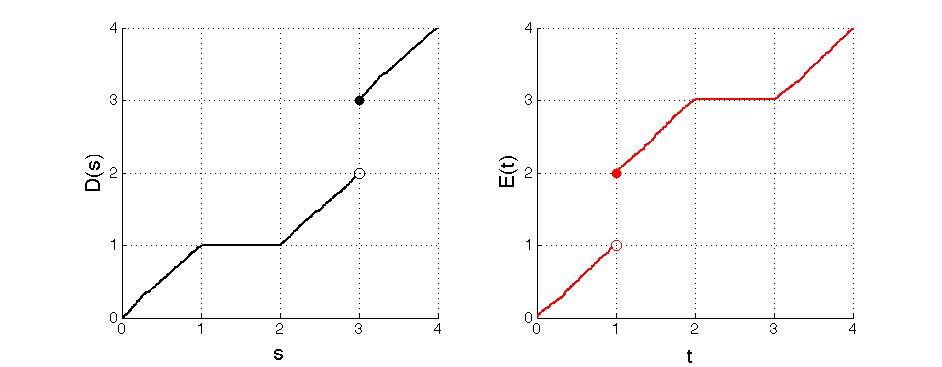

We describe here the path of the inverse subordinator. Figure 1 illustrates the relationship between a subordinator, , , and its inverse, , . Observe that both , and , are right continuous.

The following proposition provides additional details. We provide a proof for the convenience of the reader.

Proposition A.1

The sample paths of the inverse subordinator are non-decreasing and are right continuous with left limits. The sample paths of moreover, are continuous if and only if is strictly increasing222Sometimes, the inverse is defined as . This process will have all of the same properties as the inverse defined here, with the exception that it will be left continuous as opposed to right continuous..

Proof.

We start by proving that increasing implies that is non-decreasing and has cadlag sample paths (right continuous with left limits). Indeed, if , then , meaning . To prove the sample paths are cadlag, note that the left limits follow from the fact that is non-decreasing. To see right continuity, observe that

since is non-decreasing. Thus, taking inf’s,

Thus, , implying right continuity.

To prove the second part of the proposition, we will first show that if is continuous, then is strictly increasing. Suppose the opposite is true, that is, is not strictly increasing. If for with , then by the right continuity of , and , contradicting the continuity of .

We now show that strictly increasing implies that is continuous. Suppose that this is not that case, that is discontinuous at some point . From above, is continuous from the right, thus discontinuity implies that is not left-continuous at , meaning . Then, for any with , one has . Since is non-decreasing, for one has

thus . Letting proves that , contradicting that is strictly increasing. This finishes the proof.

The next proposition displays the inverse relationship between the Lévy subordinator and its first passage time.

Proposition A.2

Proof.

First, observe that we have the following set inclusions:

| (30) |

To see this, suppose that . Then by right continuity, for sufficiently close to . Thus, since is non-decreasing.

For the second inclusion, assume . If , then we would have , a contradiction. This verifies (30).

Thus, we have for all and , we have

| (31) |

Now, for fixed,

| (32) |

For each , let . Notice that each is at most a countable subset of , and hence is a set of Lebesgue measure . Thus, (32) implies that

To prove the second statement of the proposition, assume is strictly increasing. With this, the first inclusion in (30) is strengthened to equality:

| (33) |

To see this, we proceed by contra-positive. If , then since is strictly increasing, for all , hence . This, combined with (30) proves (33), thus for all .

References

- [1] D. Applebaum. Levy Processes and Stochastic Calculus. Cambridge University Press, Cambridge, UK, 2004.

- [2] G. B. Arous and J. Cerny. Scaling limits for trap models on . Annals of Probability, 35(6):2356–2384, 2007.

- [3] O. Barndorff-Nielsen. Infinite divisibility of the hyperbolic and generalized inverse Gaussian distributions. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete, 38:309–312, 1977.

- [4] A. Baule and R. Friedrich. Joint probability distributions for a class of non-Markovian processes. Physical Review E., 026101(71), 2005.

- [5] A. Baule and R. Friedrich. A fractional diffusion equation for two-point probability distributions of a continuous-time random walk. EPL, 77, 2007.

- [6] B.Baeumer and M. Meerschaert. Stochastic solutions for fractional Cauchy problems. Fractional Calculus Appl. Anal., 4:481–500, 2001.

- [7] J. Bertoin. Levy Processes. Cambridge University Press, Cambridge, UK, 1996.

- [8] J. Bertoin. Subordinators: Examples and Applications, in: Lecture Notes in Mathematics, volume 1717. Springer, Berlin, 1999.

- [9] R.H. Cole. Theory of Ordinary Differential Equations. Appleton-Century-Crofts, New York, 1968.

- [10] Ernst Eberlein and Ernst August v. Hammerstein. Generalized hyperbolic and inverse Gaussian distributions: limiting cases and approximation of processes. In Seminar on Stochastic Analysis, Random Fields and Applications IV, volume 58 of Progr. Probab., pages 221–264. Birkhäuser, Basel, 2004.

- [11] I. Eliazar and J. Klafter. On the first passage of one-sided Lévy motions. Physica A, 336:219–244, 2003.

- [12] L. C. Evans. Partial Differential Equations. American Mathematical Society, Rhode Island, 1998.

- [13] A. Gut. Probability: A Graduate Course. Springer, New York, USA, 2005.

- [14] M. Kovacs and M. Meerschaert. Ultrafast subordinators and their hitting times. Publications de L’Institut Mathematique, 94(71):193–206, 2006.

- [15] A. N. Lageras. A renewal-process-type expression for the moments of inverse subordinators. Journal of Applied Probability, 42:1134–1144, 2005.

- [16] M. Meerschaert and H. Scheffler. Stochastic model for ultraslow diffusion. Stochastic Processes and their Applications, 116(9):1213–1235, 2006.

- [17] M. Meerschaert and Hans-Peter Scheffler. Limit theorems for continuous-time random walks with infinite mean waiting times. J. Applied Probability, 41(3):623–638, 2004.

- [18] G. E. Roberts and H. Kaufman. Table of Laplace Transforms. W. B. Saunders Company, Philadelphia, USA, 1966.

- [19] M. Veillette and M. Taqqu. Numerical methods for computing first-passage times of increasing Lévy processes. Preprint, 2008.

Mark Veillette & Murad Taqqu

Dept. of Mathematics

Boston University

111 Cummington St.

Boston, MA 02215