Christoph Hummel

Secquaero Advisors111Weinbergstr. 10,

CH-8807 Freienbach, Switzerland, christoph.hummel@secquaero.com

Abstract

We introduce a family of copulas which are locally piecewise uniform

in the interior of the unit cube of any given dimension.

Within that family, the simultaneous control of tail dependencies of all

projections to faces of the cube is possible and we give an efficient sampling algorithm.

The combination of these two properties may be appealing to

risk modellers.

1 Introduction

Copulas have become an accepted tool for modelling dependencies in the financial industry;

an overview from an applications point of view is given by

P. Embrechts in [2] together with a comprehensive

list of references. One reason why risk modellers have become more used to working with copulas

is the fact that copulas allow the creation of models with increasing dependencies in the

tails of the marginal distributions.

We deal with two shortcomings of some of the currently used copula models.

Firstly, practical algorithms

for generating independent random samples of copulas efficiently, particularly in

higher dimensions, are relatively scarce (refer to A. McNeil et al. [6]

and A. McNeil [5] for various simulation algorithms).

Secondly, the parameters of the most prominent copulas such as the t-copulas,

archimedean copulas (for instance Clayton and Gumbel)

or nested archimedean copulas are related to pairwise dependencies of the

marginal distributions so that a copula in the

corresponding family is uniquely determined by the projections onto the

-dimensional faces.

In this paper we give a general construction principle, which we call

tail nesting, for copulas in any dimension .

The characteristics of the tails can be shaped

by prescribing the tail dependencies in a very flexible manner.

The resulting copulas have efficient simulation algorithms.

A copula corresponds to a Borel probability measure on the -cube ,

which, when projected to any -dimensional face, yields the uniform probability measure.

The correspondence between and is given via for

and . In the context of this paper, working directly with the measure

turns out to be more convenient and we call as well a copula or a copula measure.

We refer to [6] or R. Nelsen [9] for an introduction to copulas.

Our main result is summarised below in this section. Some readers may prefer to read first the

motivating examples in Section 2 and then return to the paragraph below.

To begin with, we define the notion of tail dependency in higher dimensions which we

work with. It is motivated by Example 2.3, and the definition of

lower tail dependency in [6].

Definition 1.1.

For as above, we define the tail degree of ,

(1)

Its tail coefficient in case is

(2)

where . We observe that for . Formally, we set if and define the

tail characteristic of as the function

on the set of front faces of by

, .

Here denotes the push forward measure of to with respect to the

canonical projection . Front faces of are those faces which

contain the origin. Hence the tail characteristic is the collection of all tail coefficients

and tail degrees of the projections of to the front faces of .

We say that a copula on has tail dependence of degree

if its tail degree satisfies ; otherwise it has no tail dependence.

Example 1.2.

The Clayton copula given by

with parameter

has

for with .

The Gumbel copula

,

for parameter satisfies

for .

Hence the Gumbel copula has tail dependence of degree provided .

This must not be confused with the tail dependencies at the opposite vertex .

For convenience and without loss of generality

we work exclusively with tail dependencies at the origin.

For , lower tail dependence in [6] implies tail dependence of degree and

tail coefficient for the face .

We refer to A. Charpentier & J. Segers [1] who have investigated the tails of

archimedean copulas in a very general setting.

We consider now a face and a face of .

As projecting the copula first to and the result to is the same as projecting

the copula directly to we see that is a non-decreasing map in the following sense:

If are two faces of and , then .

We call a map with for

non-decreasing and increasing if the strict inequality holds for any .

Main Results.

Let

denote maps on the faces of such that for those

with . Let be non-decreasing.

(i)

If is increasing we construct a copula measure with . The copula is locally piecewise uniform in .

(ii)

If is not increasing, we give necessary conditions for such that for some copula . We investigate special cases where is not increasing.

(iii)

The construction for the proof generalises naturally to copulas of order , i.e.,

measures on the unit cube which project to any face of dimension to the uniform probability measure.

(iv)

Tail characteristics for risks could be defined via the transformations of the to uniform random variables. The construction works just as well with

any other transformation.

(v)

The construction comes along with an efficient simulation algorithm.

Finally we remark that the construction is elementary and contributes to the understanding of dependence patterns for random variables. We can imagine many applications for risk modelling.

Some of them we are going to discuss elsewhere.

The paper is organised as follows. We illustrate and motivate the copula construction principle

in order to prove the main results by means of two simple examples in the next section.

In Section 3 we introduce some notation and

in Section 4 we study the spaces of the most simple non-trivial

copulas in any dimension. They are the building blocks in the construction of our main result.

We introduce the construction technique of nesting in Section 5. We explore

it in Section 6 for shaping the tail characteristics and eventually

state Theorem 6.5 about tail nesting. We derive some corollaries in Section 7

and discuss the construction further in Section 8.

Acknowledgement.

I thank my colleague Guido Grützner for helpful discussions and the entire Secquaero team for their support.

2 Motivation

This section illustrates some of the ideas and observations in this paper

in a very elementary fashion.

The reader may find the descriptions in this section helpful when going through

the construction in any dimension.

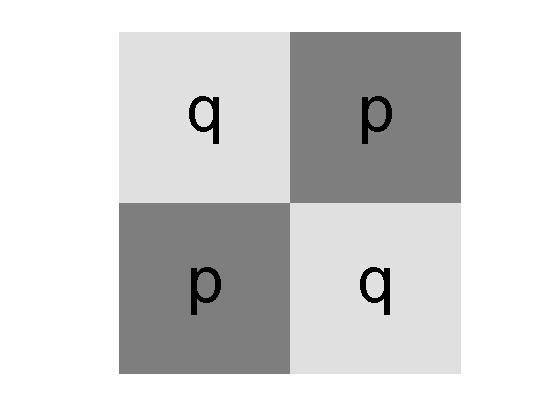

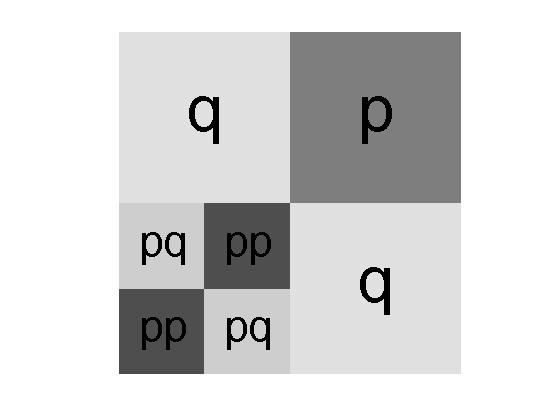

Example 2.1(Tail nesting in dimension ).

We decompose the unit -dimensional square into four boxes by splitting

each edge in the middle, i.e, into , for

and . Each of the four vertices corresponds to one of these

squares. Now we choose a probability measure on which has constant density in

each square. We describe this measure by the map which assigns

to each vertex the measure of the corresponding box in the decomposition. This measure is

a copula if it projects to the uniform measure on each of its edges. In choosing a copula

of that type we have only one degree of freedom. We can set the probability

equal to any . Then, due to the copula condition,

and thus . This is the most simple case of a

grid copula. The application of grid copulas in risk management was suggested

by D. Straßburger & D. Pfeifer [11].

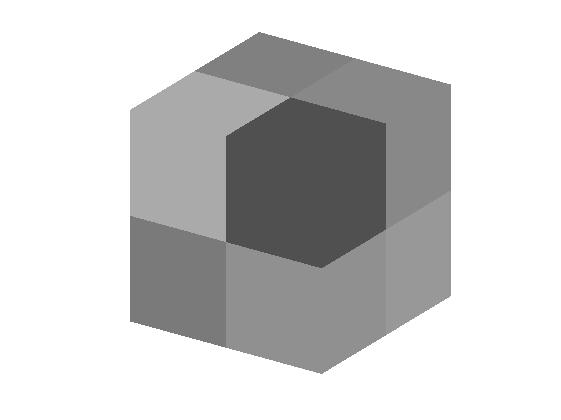

Figure 1: Nesting a -dimensional box copula into itself. Grey levels

according to the density of probability for some .

The following observation is simple, but crucial for the remainder of the paper:

We set as above. Then we nest into the square

of as follows: Decompose that square again into four equally

sized squares , for and and

modify on by ‘multiplying’ it with , in order to obtain

, as illustrated in Fig. 1.

In this construction we have refined the initial decomposition of . We call such

decompositions box decompositions. It can be verified immediately that is

again a copula. We call copulas of that type box copulas. Now we can repeat this

construction by nesting into the square of , in order

to obtain and so on, by recursively nesting into the square

of . The limit of this sequence of copulas exists and

is again a copula. Suppose we start with

and . Then and thus

as .

Remark 2.2.

Key observations when studying the simple example are:

(i)

The copulas are asymmetric and the probability density increases as

for .

(ii)

As ,the copula has zero

lower tail dependence222 is said to have lower tail dependence if

as , refer e.g. to [6] for details.

for .

(iii)

Nevertheless, given , we can choose such that

. Hence this copula family is still good enough for

sensitivity testing in risk modelling. Furthermore,

there is a simple recursive algorithm to generate samples of .

(iv)

We can further modify the tail behaviour by nesting in the -th step a copula

of the same type but with where is close to .

By choosing appropriate sequences we can not only control the

tail dependencies in the limit but also how the limit is approached

as .

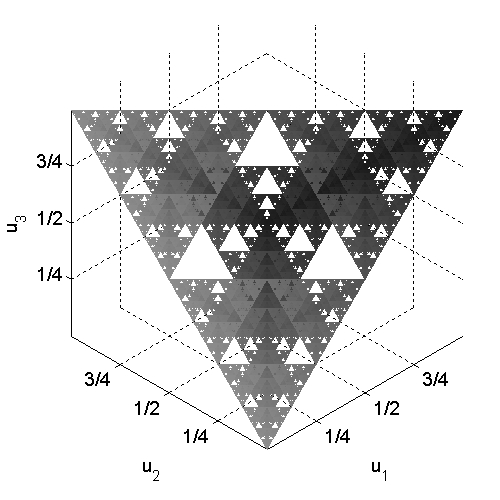

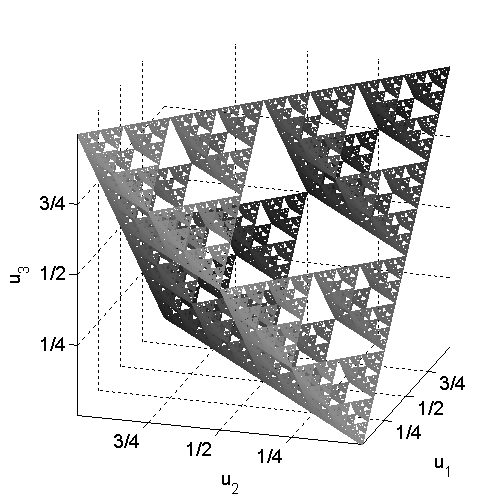

Example 2.3.

Analogously to the decomposition in Example 2.1, we decompose now the unit

-dimensional cube into cubes, each isometric to . Each of these

cubes contains exactly one of the vertices . We assign to the ‘even’

cubes (i.e., those with ) the uniform measure with

total probability equal to . The ‘odd’ cubes get probability zero.

When projected to any -dimensional face, the resulting probability measure

is the uniform probability measure. In particular, is a copula.

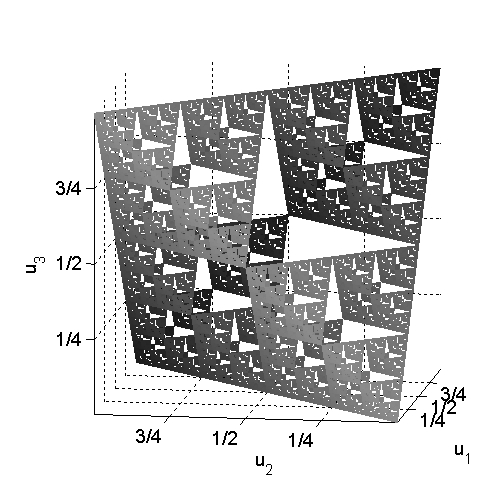

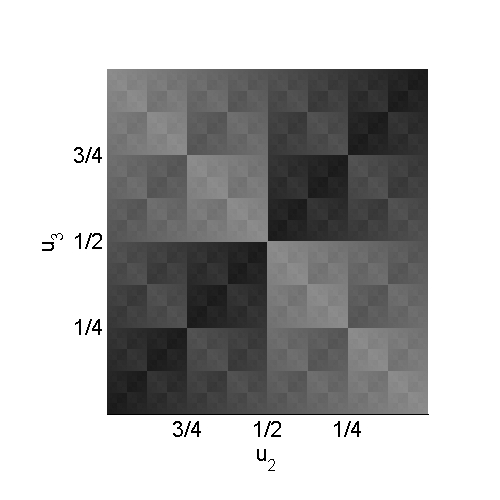

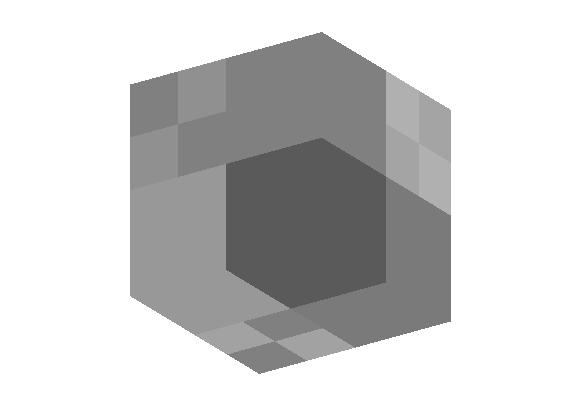

Figure 2: Illustration of from Example 2.3.

The pictures were generated by plotting one point in the centre of each of the

‘even’ cubes. The grey level of a point is given by .

The view in the left picture is along a diagonal. From left to right

it is stepwise rotated around the third coordinate axis. The points in the

picture on the right are uniformly distributed in the -plane.

Their grey level is merely an indication of the -level.

Now set and nest into the even cubes of the

decomposition underlying . In this way the even cubes decompose again into cubes,

each isometric to ; four are again ‘even’ and the others are odd.

We obtain a copula on , its support consisting of cubes,

each with uniform measure and probability equal to . Observe now that

still projects to the uniform measure on each of the -dimensional faces of .

We can continue this nesting and obtain a limit measure .

The projection of the limit measure to any -face of is again the uniform measure

and thus is in particular a copula. It is not difficult to see that

the limit measure is, up to scaling, the -dimensional Hausdorff measure of the support

of . The latter is the intersection of all the ‘even’ cubes obtained during the

recursive definitions of the .

Remark 2.4.

We summarise the main observations from the above example. To this end assume

that we have three risks whose dependence structure is given by ,

i.e., where is the quantile function.

(i)

Even if risks are pairwise independent, they can be heavily dependent overall.

For the univariate margins of the above copula the third margin is a function of

the other two.

(ii)

The probability that all three risks are worse than their -Quantile is

.

A measure for tail dependencies in higher dimensions should show that

has some tail dependence. This is one motivation for Definition 1.1.

It has become more and more common that risk modellers focus on tail dependencies when modelling

a portfolio. This example demonstrates nicely that in calibrating the corresponding dependence

models it is not sufficient to focus on the estimation of pairwise dependencies alone.

The construction for shaping the tails of copulas in Section 6 is as in

Example 2.1, but generalised to any dimension .

Roughly speaking, we can shape the projections to any lower dimensional faces,

which are also of this type, simultaneously so that we can achieve any tail characteristic

which is consistent with the condition for probability measures.

Before describing this aspect, we need to define some notation related to cubes, their vertices

and faces in Section 3. Then we study maps , the

equivalents of those maps for in Example 2.1,

which define copulas in Section 4.

3 Notation and basic definitions

By we denote usually points in where .

The unit -cube is . The set of its

vertices is

We use the letters exclusively for elements of .

There is a one-to-one correspondence between front faces

of the -cube and the vertices given by

(3)

We set and .

and denote by

the reflection with .

For a front face the corresponding back face is and

the complementary front face . We observe that the front face complementary

to is .

We can identify each face naturally with .

Other faces of are of the form for .

Given a front face of we denote by

(4)

the canonical projection along to its complement .

An interval in is an -fold product of intervals in . We call a

compact interval in with non-empty interior an -box in .

Hence -boxes are of the form with

for each . A box decomposition of an -box is a collection of finite -boxes

such that their union is and their non-trivial intersections are of

lower dimensions, i.e., and

for all .

Given an - and -box and with box decompositions and , respectively,

we can form the product box in which inherits a natural box decomposition

, the product decomposition. If a box decomposition of a box is the product of box

decompositions of its -dimensional faces we call it a grid decomposition

or simply a grid.

Given an -box we denote by the canonical affine transformation from

the unit -cube to ,

(5)

Via this transformation we define the corresponding faces of and projections to faces of .

Observe that maps box decompositions of to box decompositions of .

Definition 3.1(Box measure).

Let be a box decomposition of and .

We view elements , i.e., maps , as signed measures on such that

is a uniform measure, i.e., proportional to the Lebesgue measure of .

Let be a box decomposition of . The canonical transformations

induces a canonical vector space isomorphism

by pushing forward the measures.

In the same way we can push forward box measures using the

canonical projections along faces.

In case is not a grid decomposition, the elements of do not define a

box decomposition of (see e.g., Fig. 1).

In this case, we denote by the projection of some refinement

of into a grid. In this way, we can push forward box measures in to

box measures on and obtain a linear map

(6)

Our ultimate goal is to construct copulas in satisfying some given conditions,

such as a certain behaviour near the the origin .

To this end the following notion turns out to be quite useful.

Definition 3.2.

Let be a box decomposition of .

Then define the following linear subspaces of for ,

(7)

and set .

Observe that is the set of those box measures which project onto each face

of dimension to the zero measure. Thus it does not depend on the choice

of in (6). Furthermore, we obtain a filtration of

linear subspaces of ,

(8)

We let denote the element which corresponds to the

uniform probability measure on .

Definition 3.3.

For we define the following subsets of :

(9)

The set of probability measures in is and

the subset of copulas is , the box copulas in .

We call elements of box copulas of order . We observe that

for . The sets are convex in . We call elements of

copula generators of order for .

The limits of sequences of box copulas we work with later on are not

box copulas. We extend some notions from above to Borel measures

on such as the property of being a

copula of order in the obvious way.

We call a probability measure on

locally piecewise uniform on if for each

there exists a neigbourhood of in such that

is equal to some box measure restricted to .

Remark 3.4.

Note that by construction each box copula corresponds to a probability measure

on such that the projection to any edge yields the uniform

probability measure. The notion of a box copula differs from the notion

of a grid-type copula [11] or simply grid copula

only by the underlying decomposition.

We already made use of the fact that any box decomposition can be

refined into a grid decomposition when defining projections.

One reason for introducing the notion of a box copula is that it is

useful when designing efficient simulation algorithms for nested copulas

(see Algorithm 6.4). For that purpose, we may want to describe

the measure with the smallest possible number of boxes

(see Fig. 1 for an illustration).

Example 3.5(Box copulas).

It is not difficult to construct box copulas:

(i)

The copulas , , from Example 2.3

are box copulas of order .

(ii)

Take any copula on , select some and

let be the -measure of , .

Then . The finer , the better the

approximation of by .

(iii)

Given some copula generator , some

, then

for and sufficiently small.

This follows from the convexity of .

Remark 3.6(Copula surgery).

If is an -box, and

the canonical map, then

can be viewed as a copula generator on with support

contained in and with respect to any box decomposition which extends .

Observe that we can now build the sum as signed measures for .

Provided is appropriate, e.g., sufficiently small for each ,

is a copula of order .

It is indeed a box copula for any common refinement of and .

This construction can be iterated with appropriate sequences of generators.

The reader may wish to compare this with some of the methods

for the construction of copulas in [9].

Nesting and tail nesting which we introduce later on are special cases of ‘copula surgery’.

In order to explore the range of such constructions,

a detailed study of the vector spaces for certain turns out to be helpful.

This is the subject of the next section.

4 Vertex decompositions and their copulas

In this section we will describe the box copula spaces for the most

simple box decompositions. A point induces a decomposition

of the -th edge, namely . The product of these

decompositions is a box decomposition . Each box of this

decomposition contains exactly one vertex of . In this way,

we identify

via . We call these decompositions vertex decompositions and corresponding

box measures vertex measures. Vertex measures are defined by together

with a map , i.e, by an element of .

We denote the canonical basis of by .

Observe that the linear spaces do not depend on ; but the copula spaces

do.

We also point out that vertex decompositions project to

vertex decompositions along the faces via the corresponding map

.

Given a subset we view naturally as the linear subspace of .

In this way a map is extended to a map on by mapping

elements in to zero. The canonical projection

corresponds to restricting maps onto , denoted by .

We decompose into disjoint sets

(10)

with . We write

(11)

and likewise or and so forth. Accordingly, we decompose the set of

front faces of into

(12)

where is the set of front faces of codimension .

Observe that and . We denote by

the set of front faces of dimension . We also write along the lines of (11).

Remark 4.1.

We summarise some observations for later purposes333Drawing pictures for

may provide helpful illustrations..

(i)

The map map , given by is compatible with the

above decompositions. It defines bijections , .

For we have that and .

In the same way, the map defines bijections .

(ii)

Choose and . Then with

(iii)

for each and any where

is defined. Indeed, given and

we observe that has codimension in . Hence

projects to zero along .

(iv)

We have that . Indeed, if is a front

face of codimension in , then is a face of

codimension in . Hence

for .

Next we are describing the spaces and the corresponding copula spaces.

Lemma 4.2.

The vector spaces have the following properties:

(13)

In other words, projects to the zero-measure along any face of codimension

if and only if the projection of along any face of codimension

is zero at the origin .

It is evident that is contained in the set on the right hand side of (13)

which we denote by . We argue by induction over the dimension . To this end we note

that the statement is trivial for . We assume that

for the vertices of cubes up to dimension and for all .

Suppose now that and . We need to show that .

We distinguish two cases.

Firstly, assume . Then we observe that

and by the induction hypothesis in as

. Note that as and hence .

Secondly, If we see from the definition of that restricted to any

is in and thus in .

Hence for .

It remains to show that . This follows by projecting

along the -dimensional front face to the zero-dimensional face

which yields as by assumption. Hence .

∎

The following proposition describes the degrees of freedom one has

in finding box copulas with prescribed properties for the tail.

Proposition 4.3.

There is a linear map with the following properties:

(i)

is an isomorphism between the vector space filtrations, i.e.,

the following diagram is commutative for :

(ii)

For and any we have .

is uniquely determined by (i) and (ii) and is given by

(14)

for where for any .

Eventually we are interested in the construction of copulas with prescribed tail properties.

The proposition will be instrumental for this.

If with properties (i) and (ii) existed, it would be unique as its inverse would be given by the previous remark. To prove existence, we just construct .

First we are going to define and it

is readily verified that . From the previous lemma we know that .

For any we denote by

the back face corresponding to .

Observe that and that corresponds naturally to

the origin in . Exactly as with before,

we define now to be the unique element in

having the required property,

and that is

(16)

Therefore we obtain a candidate for the isomorphism in question, namely

(17)

Now observe that if and only if and thus

where is as in (14). As is compatible with the filtration

on the basis , it is indeed compatible with the filtration. As it satisfies

for and

otherwise it satisfies by linearity.

By Lemma 4.2, restricts to isomorphisms .

∎

Remark 4.5.

For each there exists a unique map

such that for .

The map is a vector space isomorphism.

As we do not make use of this result, we leave the proof as an exercise.

Next we describe the vertex copulas for . We abbreviate

for any and where .

The uniform copula in corresponds to the element

which depends on . Observe that .

Therefore the proposition implies that

Corollary 4.6.

The vertex copulas of order with respect to are given by

with

(18)

Condition (18) is the condition for being a probability measure.

Proof.

A given element in is of the form with .

Using the proposition, choose such that and set .

Then and the statement follows from the proposition.

∎

Remark 4.7.

The reader may compare Condition (18) with the rectangle inequality

for a copula in [6], p. 185. We see from the corollary that in case of vertex measures

there is no need to check that property for every -box in .

5 Nesting box copulas

In this section we define formally the nesting constructions used in the

Examples 2.1 and 2.3.

Related techniques have been used by G. Fredricks et al. [3]

in dimension .

Definition 5.1(Nesting box copulas).

Suppose , are two box measures on and

is a box for . Let be

the canonical transformation. Then is the box measure

with and

(19)

In other words, is equal to outside of and

on , it is a copy of , scaled by .

We call the box measure obtained from nesting

into along .

If , we define to be the box measure

obtained by consecutively nesting into the elements of .

Note that this construction does not depend on the order of the different

nesting operations. We call

the box measure obtained from nesting into along .

Lemma 5.2.

Assume that , are box copulas of order .

Then is in where is as in the definition.

Proof.

The measure is

uniform.

The projections of along faces of up to codimension

is by assumption a constant times the euclidean volume of the face for the

corresponding dimension. The scale factor is arranged such that projections

of to these faces are equal to the projection of .

To this end note that

∎

Algorithm 5.3(for sampling nested box copulas).

Suppose that we have a simulation algorithm for drawing random samples

from copulas and as in the lemma, i.e., essentially an algorithm for

simulating multinomial distributed variates. Then the following is a

simulation algorithm for :

(i)

Draw a random variate from .

(ii)

If then return ,

(iii)

otherwise generate a random sample from . Return .

We can nest copulas iteratively. To this end we start with a box copula .

Then construct recursively. Suppose we have already constructed

. Then we choose a box copula , a subset

and set .

Remark 5.4.

Suppose that , , is a obtained from

consecutive nestings. Intuitively, the sequence of measures

converges as for , we have that for each .

Formally, given define

Arguing as in [8], p. 8, Eq. (1), we conclude that

is an outer measure where Borel sets are measurable.

Form the construction we see that for each .

It is evident that is a copula measure.

Note that in the interesting case where we have infinitely many non-trivial

nestings, the limit measure is not given by a box copula.

We choose the vertex decomposition of given by and

start with the vertex copula on ,

as in Proposition 4.3. This copula assigns to each vertex

with the probability and to the other

vertices the probability . Proceeding as above, we choose and

. The limit copula is, up to scaling,

equal to the -dimensional Hausdorff measure on the limiting

set .

We consider now the canonical projections

onto the -th coordinate and view it as a random variable

with probability measure given by . We write

with having values in . They are the digits for the

binary representation of .

It can be seen from the construction of that

where the summation is in . Hence is the

bitwise addition of the . Any subset of

with less than elements is independent.

This example is well known, at least for finitely many digits

(where the are ‘cut off’ after the -th digit),

refer e.g., to J. Stoyanov [10]. The set of

can be enlarged by for any non-empty subset

where stands for bitwise addition as

described before. In this way we obtain a longer finite sequence of

pairwise independent random variables .

A similar construction works also for representations with respect to any base ,

i.e., with any . Just start with the

regular grid for which decomposes each edge into intervals

of length and assign to them the digits .

Define the starting box copula as above for the case by adding the digits assigned to the edges

in .

Finite versions of such constructions

have applications in computer science (see e.g., M. Luby & A. Wigderson [4]).

6 Tail nesting

In this section we define and investigate tail nesting which is a

specific way of nesting vertex copulas in order to shape tail dependencies.

Let be a grid decomposition of . The -box of

is the unique box in which contains the origin .

For we define the set of -boxes with respect to

as the set of all such that

is an -box of and

is not an -box of

for any . In this way we obtain a disjoint decomposition of ,

Thus elements in project to the -box in the decomposition of

and is the face of maximal dimension having that property.

Definition 6.1(Tail nesting for grid copulas).

Suppose that is a vertex copula of dimension and that is a grid copula

of order on with grid . Then is the grid copula

obtained from by nesting

successively for each the product measure of with the uniform copula

as an element of , that is

into . Thus is given by the consecutive nestings

(20)

The grid decomposition for is obtained from

by assigning to each box the vertex decomposition induced by the nesting.

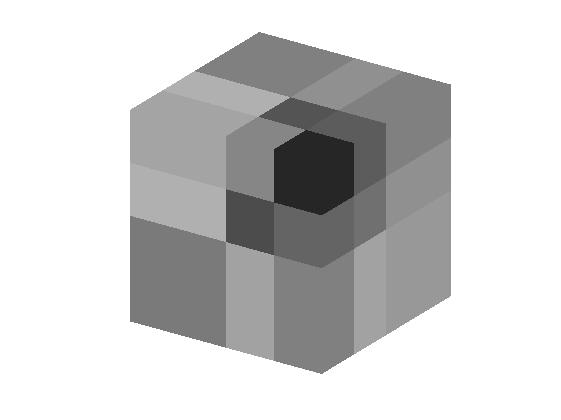

Figure 3: Illustration of tail nesting a -dimensional vertex copula

once into itself. The copula measure is pictured left. A front and back view of the

resulting box copula is illustrated middle and right, respectively.

The tail vertex is the upper front corner in the left and middle picture.

On the right hand side, the opposite vertex corresponds to the lower front corner.

Grey levels are set according to the density of probability.

Lemma 6.2.

In the setting of the above definition, is a grid copula of order .

Furthermore, tail-nesting commutes with projections along faces of ,

for the corresponding grid copulas.

Proof.

It is a direct consequence of Lemma 5.2 that is a

grid copula of order provided are of order .

We prove now the second part of the statement.

For any face we denote here by the uniform copula on with

grid decomposition .

Now let be a given face. Suppose that and .

Observe that . The elements in which project along to

are of the form , and in particular .

Observe that where with .

Therefore we obtain

This implies that

for a scaling factor . From the definition of nesting, .

∎

In analogy to Example 2.1, we can now investigate

iterated tail nestings in dimension .

We pick a sequence , with , for .

We define recursively grid copulas such that and

with grid decomposition . We denote the limit copula also by and observe that

is a copula of order . Lemma 6.2 implies that

(21)

Note that the -box of is with

(22)

The -box of in is denoted by

and given by

(23)

Remark 6.3.

Building a simulation algorithm for based on this definition and

Algorithm 5.3 is not efficient. Observe that the nestings for

do not change the measure and merely refine the decomposition. Including these

trivial nestings formally in the definition has advantages in stating and

proving properties of iterated tail nestings.

Algorithm 6.4(for sampling tail nested copulas).

Generate the samples based on Algorithm 5.3 and do the iterative nestings

only for -boxes with respect to . In the first iteration step one

obtains a box copula which is illustrated in Fig. 3. Then one needs to extend

the definition of -boxes to -boxes with respect to for the

resulting box decomposition, which is easy. Proceeding in that way yields the required

algorithm. In the first iteration, one ends up in the ‘otherwise’-routine of

Algorithm 5.3 with a probability of

and conditioned on that, with a probability of

in the ‘nested otherwise’-routine and so on. Hence generating samples of the

limit copula requires the sampling of approximately

random variates from a multinomial distribution for the

vertices444In each ‘otherwise-routine’, the number of vertices is , .

If we have an upper bound , then

and the algorithm converges. In practise, working with sufficiently

smaller than and with a finite sequence for shaping a desired

tail behaviour should be sufficient.

We can coarsen the box decomposition by building consecutively unions of two boxes,

starting with boxes in , if they share a common face of codimension and the

probability density of on these boxes is the same, irrespective of the choice of

probabilities , and . In this way we obtain the relevant

box decomposition for Algorithm 6.4 and denote it by .

We observe that each box in

(24)

is also contained in for and that restricted to

these boxes is equal to restricted to these boxes.

The theorem below summarises the main properties of iterated tail nestings

and demonstrates the flexibility one has when ‘shaping the tail’ of

by choosing appropriate with appropriate vertex decompositions given by .

The constraint is given by Corollary 4.6 and in particular

Condition (18) for the probability measure.

Theorem 6.5.

Let be the set of vertices of and denote the isomorphism given by (14).

Assume that is a sequence in such that is a sequence of vertex copulas of order . Then is a copula of order and satisfies

(25)

where for .

Furthermore, if as then is locally piecewise uniform

on .

Proof.

By Proposition 4.3, in particular (ii), and since commutes with , it is sufficient to show that (25) holds for , i.e., that

where . This follows immediately from the definition of nesting.

Now assume that as . As above, let be the grid decomposition for obtained in the process of iterated nestings.

Then, given , all elements of are contained in the -tube555The -tube around a set is the set of all points with distance to some point in . around for all , where is sufficiently large. Indeed, if the -tube is taken with respect to the maximum norm, we may choose such that for each .

We obtain for . Note that , , is piecewise uniform by (24). Therefore is locally piecewise uniform in .

∎

Remark 6.6.

We observe that (25) also holds for the limit copula obtained by nesting iteratively with .

Tail nesting avoids those nestings which are not relevant for shaping the tail characteristic. Formally, this is done in (20) by averaging over

those dimensions which do not matter for shaping the tail.

In this context we notice the following. Suppose we start with a grid copula of order . We refine possibly the corresponding grid before

‘tail-nesting’ a sequence of vertex copulas of order into the grid copula. In this way the original grid copula measure

is merely modified in an arbitrarily small neighbourhood of , provided the refinement of the original grid was fine enough.

7 Tail characteristics

Before we apply the theorem to construct copulas with certain tail characteristics, we investigate properties of any tail characteristic.

To this end we assume that is any copula measure of order , where , with and . We denote . For we write

(26)

The condition for probability measures (18) implies that

(27)

From this equation we obtain necessary condition for maps which are tail characteristics of copulas (see the remark below).

As an application of the theorem we are going to state sufficient conditions. We have already introduced the properties non-decreasing and increasing

for maps in the introduction.

We say is increasing at and eventually constant at

if and , respectively,

for each with and .

If is increasing and is an accumulation point of the corresponding maps

as ,

we can see that the dominating summand in (27)

is , provided .

Remark 7.1(Necessary conditions).

From the above we obtain the following necessary conditions for

maps

such that for some copula of order

and such that is an accumulation point of the corresponding maps

as .

(i)

is non-decreasing, i.e., for any ,

(ii)

for each .

(iii)

If is eventually constant at , then

.

If a pair satisfies (i)–(iii) for we say that

satisfies .

The tail characteristics of a copula restricted to the faces of dimension

provide a measure for tail dependencies of order .

Given a map as above we view it as well as a map

by composing it with the bijection .

Corollary 7.2.

Let , , satisfy for some . Suppose the sequence

converges to some . Assume in addition that is increasing.

Let be a sequence in with as . Then, after passing to common subsequences, again denoted by

, , there exists a sequence of vertex copulas of order , such that we have for that

(28)

Remark 7.3.

Let be any copula of order with increasing. Choosing , such that converges as where is as in (26).

Then the corollary states that after passing to a subsequence, .

For and we define open intervals

and .

We claim that there exists some and such that for any , any map

(29)

the following is true: For

with

we have

The idea for the proof of this claim if already laid out in Remark 7.1.

Indeed, we need to check the condition for vertex copulas of order in Corollary 4.6. Observe that and restricted to are such that provided Condition (18) for a probability measure is fulfilled. We estimate the respective expression

(30)

for from below and from above by

(31)

which is equivalent to

(32)

Since and for each by assumption on

this proves that Condition (18) holds for if is

small enough. Next observe that

provided is sufficiently small.

Now we choose such that the above claim holds.

Given the sequences and we choose the subsequences, again denoted by and such that

for any . Then we set

and observe that

Now the corollary follows from the theorem.

∎

Corollary 7.4.

Suppose satisfy the condition for some .

Assume further that

is increasing. Then there exists some and a sequence , such that

satisfies

.

Proof.

Given as in the Corollary, we choose and sufficiently small such that

(33)

We choose now a sequence , with for ,

such that

as . Then we set

for .

We calculate next the tail degree of . Given we determine

such that

We obtain for that

Applying the theorem yields

and therefore . A continuity argument shows that there exists an adequate sequence such that .

∎

Remark 7.5.

We make the following observation in the previous proof.

When nesting with where ,

in order to construct with ,

we can arrange that

, depending on . This enables us to obtain an upper bound for

depending only on . Here is determined from as in (26).

Furthermore, if we had , then as . In such a situation, the condition for the probability measure may become more difficult to control. Further below we will see that it can be easily controlled

if the tail degree is equal to .

In the next application we weaken the condition that is increasing.

Corollary 7.6.

Suppose that satisfy condition for some .

Assume that is increasing or eventually constant at every .

Then, given any sequence in converging to ,

there is a subsequence , a sequence of vertex copulas of order such that

for and

.

Proof.

We proceed exactly as in the proof of Corollary 7.2 with the originally given sequence and with . To begin with we obtain

the estimate (32) for those with increasing at by arguing as above.

Setting for , we choose and it remains to show that for those with eventually constant at .

Observe that for these , for each . As satisfies (iii)

by assumption we see that provided is sufficiently small.

Without loss of generality assume .

Next we set , , .

We claim that after passing to an appropriate subsequence . Indeed, suppose is eventually constant at and . Then we decompose the vertices of along the lines of (10) into and observe that

the number of elements in is . As

we see that . Hence satisfies the condition for a probability measure.

For , , we see that has the desired properties.

In view of Remark 7.5 we can achieve . If the ratios

were not uniformly bounded from above we can enlarge the sequence by appropriate intermediate points in order to apply the arguments as in Remark 7.5.

∎

Recall that the Clayton copula has tail dependence of degree and

likewise the nested Clayton copulas which are described in [5].

We conclude this section by investigating necessary and sufficient conditions

for tail coefficients in case of tail degree .

Remark 7.7.

Suppose is a copula of order and as in Remark 7.1.

Then any accumulation point of satisfies condition (ii) and (iii) in that remark.

If has tail dependence of degree , then (iii) is equivalent to

(iii)’

is a probability measure for

with . Indeed, given choose with .

By assumption, for any face and

thus is eventually constant at any .

We recall that if and only if .

Given any in we see from (iii) that

As this shows that (iii)’

holds. The other direction is now evident as well.

Corollary 7.8.

Let with for . Assume that is a probability measure for any .

Then there exists a sequence of vertex copulas such that has tail dependence of degree and . Moreover,

In other words, by means of tail nesting we can achieve any possible tail coefficients in case of

tail degree . As the above limit exists, the copulas with have lower

tail dependence .

Proof.

Along the lines of the construction above, we set

with for and . By the assumptions on ,

provided is sufficiently small. Next we claim that

for any . As is constant on we need to verify only that

. And indeed,

for any .

Now choose , , such that and set

Then has the desired properties.

∎

Remark 7.9.

Other interesting examples of copulas with tail dependence of degree are

for appropriate with

and

In this way, we can

control how the limits are approached, starting at an arbitrary .

8 Change of coordinates

When studying tail characteristics for random variables ,

we could study for a given decreasing sequence and each

the asymptotic behaviour of

(34)

where is the quantile function of , i.e., the inverse of the cumulative distribution function .

We assume for simplicity that the are continuous and strictly increasing.

As an application of Theorem 6.5 we can use tail nesting in order to construct probability spaces with random variables where the asymptotic behaviour of all the functions in (34) can be prescribed.

The transformation to the uniform variables appearing in this context is just one of many possible transformation. One of the critical comments about the use of copulas is that

“ there is no particular mathematical or practical reason ”

(Th. Mikosch [7]) for selecting this transformation.

More generally one may wish to look at the asymptotic behaviour of

(35)

for a given sequence such that and strictly decreasing to .

As above, we can apply Theorem 6.5 in order construct probability spaces together with random variables where

(i)

the cumulative distribution function of is given, and

(ii)

the asymptotic behaviour of can be controlled simultaneously for all .

We can arrange the vertex copulas in Theorem 6.5 such that

where is as in (22). The sequence is determined by the sequence and we can choose subject

to the conditions in Corollary 4.6.

The transformation from to

gives merely a nice coordinate system to carry out the geometric construction of nesting.

Example 8.1.

Consider a collection of Pareto-distributions

with . Say we are choosing for some , i.e.,

we aim to control the asymptotic behaviour of the probabilities

As we see that

which does not depend on .

We define now by

where , for , , and

.

Furthermore, we require that

(36)

and

(37)

We observe next that ,

provided is sufficiently large.

We impose the condition on the right hand side of (37)

in order to ensure that the probabilities of -boxes as approaching the origin

are not smaller than in the case where the corresponding are independent.

Note that

for the upper and lower bound in (37)

are equal and their values consistent with the requirements in

Corollary 4.6 for copulas (of order ). For the probability measure on

and ,

we obtain

As in the previous section, we can weaken condition (36)

by dealing directly with constraints for imposed by Corollary 4.6.

Conclusion

The construction and examples described in this paper provide insights into

a variety of asymptotic dependence structures of random variables.

Tail nested copulas enable us to deal with tail dependencies of any order.

The behaviour of these copulas can be controlled along

a sequence inside the unit -cube which converges to the origin.

We believe that tail nested copulas are suitable for applications in risk management.

They allow the risk modeller not only to take those dependencies into account

which really matter in the specific application, but as well to generate

corresponding stochastic samples numerically in an efficient manner.

References

[1] A. Charpentier & J. Segers, Tails of Multivariate Archimedean Copulas, arXiv:0901.1521 [math.PR], Jan. 2009.

[2] P. Embrechts, Copulas: A personal view, Department of Mathematics, ETH Zürich, 2007, to appear in Journal of Risk and Insurance.

[3] G. Fredricks et al., Copulas with fractal supports, Insurance: Mathematics and Economics, 37 (2005), pp. 42–48.

[4] M. Luby & A. Wigderson, Pairwise Independence and Derandomization,

Foundation and Trends in Theoretical Computer Science, 1 (4), pp 237–301, 2005.

[5] A. McNeil, Sampling nested Archimedean copulas. Journal of Statistical Computation and Simulation, 78(6), 2008, pp. 567–581.

[6] A. McNeil, R. Frey & P. Embrechts, Quantitative Methods in Risk Management, Princeton Series in Finance, Princeton University Press, 2005.

[8] F. Morgan, Geometric Measure Theory: A Beginner’s Guide,

Academic Press, 1988.

[9] R. Nelsen, An Introduction to Copulas, Springer Verlag, 1999.

[10] J. Stoyanov, Counterexamples in Probability, Second Edition, John Wiley & Sons, 1987.

[11] D. Straßburger & D. Pfeifer, Dependence Matters!, Institut für Mathematik, Carl von Ossietzky Universität, Oldenburg, presented at 36. Internationales Astin-Kolloquium, ETH Zürich, Sep. 2005.