On the consistent separation of scale and variance for Gaussian random fields

Abstract

We present fixed domain asymptotic results that establish consistent estimates of the variance and scale parameters for a Gaussian random field with a geometric anisotropic Matérn autocovariance in dimension . When this is impossible due to the mutual absolute continuity of Matérn Gaussian random fields with different scale and variance (see Zhang [33]). Informally, when , we show that one can estimate the coefficient on the principle irregular term accurately enough to get a consistent estimate of the coefficient on the second irregular term. These two coefficients can then be used to separate the scale and variance. We extend our results to the general problem of estimating a variance and geometric anisotropy for more general autocovariance functions. Our results illustrate the interaction between the accuracy of estimation, the smoothness of the random field, the dimension of the observation space, and the number of increments used for estimation. As a corollary, our results establish the orthogonality of Matérn Gaussian random fields with different parameters when . The case is still open.

keywords:

[class=AMS]keywords:

1 Introduction

A common situation in spatial statistics is when one has observations on a single realization of a random field at a large number of spatial points within some bounded region . One is then is faced with the problem of predicting some quantity that depends on at unobserved points in . For example, one may want to predict or the derivative where is an unobserved point in . A common technique is to first estimate the covariance structure of , then predict using the estimated covariance. Typically, fully nonparametric estimation of the covariance is difficult since the observations are from one realization of the random field. In this case, it is common to consider a class of covariance structures indexed by a finite number of parameters which are then estimated from the observations (see [12] or [9] for an introduction to spatial statistical techniques).

Two common parameters found in many covariance models are an overall scale and an overall variance . The simplest example of this model stipulates that the random field is a scale and amplitude chance by an unknown and of a known random field . In particular, for a spatial domain , is modeled as

| (1) |

where denotes equality of the finite dimensional distributions. In this case, is an overall amplitude (in units of ) and is an overall spatial scale (in units of ). For a nice discussion of the roll of and in the Matérn autocovariance see Section 6.5 in [28].

A fundamental question is whether or not and are consistently estimable when the number of the observations in grows to infinity. Indeed, the answer is no in general. This is immediate from the existence of self similar random fields that satisfy for any where is a fixed constant. For these self-similar processes, any two pairs and that satisfy give the same model in (1). This problem can also be present when is not self similar. For example, suppose is an isotropic Ornstein-Uhlenbeck process in dimension (see Figure 1). In this case, if (i.e. ) the two models for yield mutually absolutely continuous measures (when see [19], [32], when see [33], [28]) and therefore are impossible to discern with probability one when observing one realization of . We shall see, however, that in some cases it is possible to consistently estimate and . Moreover, it will depend on dimension: typically the larger the dimension the more information there is to separate from . Before we continue, we mention the work of Stein (see [25],[26]) which establishes that even if two models are mutually absolutely continuous, using the wrong model to make predictions may still yield asymptotically optimal estimates. In fact, this phenomenon can also occur for orthogonal measures when restricting to predictors that are linear combinations of the observations (see [27]).

To understand the condition one can look at what is called the principle irregular term of the autocovariance function (see [28]). Suppose, for exposition, that there exist constants such that the covariance structure of satisfies

| (2) |

where is an even polynomial and both are not even integers. This model is not as restrictive as it seems and includes the Ornstein-Uhlenbeck process, the exponential autocovariance function and the Matérn autocovariance function (see below). The term is often referred to as the principle irregular term and is instrumental in determining the smoothness of . The second term, , is less influential but can have an observable effect depending on dimension and the magnitude of . Now, if we model by (1) and (2) we get

| (3) |

Therefore for two pairs of parameters and , the condition ensures that the covariance models for have the same principle irregular term. This explains the importance of the quantity . In addition, if one can estimate both coefficients and then it is possible to get separate estimates of and . In what follows we develop consistent estimators of these two coefficients which allow consistent estimation of and .

The majority of this paper focuses on the case when is a mean zero, isotropic Gaussian random field which has a Matérn autocovariance. The reasons are twofold. First, the Matérn autocovariance has been used extensively in spatial statistics so that results on the Matérn autocovariance are of intrinsic interest alone. The second reason is that once one establishes the results for the Matérn it is relatively easy to see how to extend to other covariance functions. In Section 3, we give two examples that illustrate these extensions. Our Matérn assumption stipulates the existence of a known such that

| (4) |

for all where denotes Euclidean distance and is the modified Bessel function of the second kind of order (see [1]). The parameter controls the mean square smoothness of the process: larger corresponds to smoother . The flexibility provided by the smoothness parameter along with the fact that it is positive definite in any dimension leads to its widespread use in spatial statistics.

In what follows we extend the basic model (1) to the case when there is an unknown invertible matrix with determinant 1 (this class of matrices we denote by ) so that

| (5) |

The matrix is called a geometric anisotropy and is used to model a directional sheer of . The assumption that removes identifiability problems with the overall scale parameter . In Section 2, we construct estimates of , and . We show that the estimates of and are strongly consistent in any dimension and the estimate of is strongly consistent when .

There is a fair amount of literature on estimating for the Matérn autocovariance. In 1991, Ying [32] established strong consistency and the asymptotic distribution of the maximum likelihood estimate of for the Ornstein-Uhlenbeck process when (which has a Matérn autocovariance for ). In 2004, Zhang [33] established that the maximum likelihood estimate of (obtained by fixing and ) is strongly consistent when . In related work, Loh [23] shows that maximum likelihood estimates of scale and variance parameters in a non-isotropic multiplicative Matérn model are consistent when (similar results for the Gaussian autocovariance model can be found in [24]). In Section 6.7 of [28], Stein derives asymptotic properties of the maximum likelihood estimates of , and for a periodic version of the Matérn random field. For this periodic random field all the parameters are consistently estimable when . Our results confirm these findings for and with the non-periodic Matérn when . The case is still open.

Recent work by Kaufman et al. [8] and Du et al. [13] studies maximum likelihood estimates of using a tapered Matérn autocovariance when . The advantage gained by tapering is a reduction of the computational load for computing the likelihood and for computing kriging estimates. We will see that our estimates of the same quantity, , yield strongly consistent estimates in any dimension which are “root n” consistent and are easily computed with no maximization required. However, our estimates depend on the grid format of the observations whereas the maximum likelihood estimates are not confined to such restrictions. We also expect some loss of efficiency in our estimates as compared to the MLE. We hope that there is potential to combine the two estimation methods using a one-Newton-step tapered likelihood adjustment to the increment based estimate. Since our results can be easily extended, by a Lindeberg-Feller argument, to obtain the asymptotic normality of when , we believe this has the potential to mitigate any loss of efficiency and reduce the computational load for the maximum likelihood estimate.

Finally we mention the long tradition of using squared increments to estimate properties of random fields, beginning with the quadratic variation theorem of Lévy in 1940 ([22]). For example, increments have been used in [20] and [6] for identification of a local fractional index and in [11] to identify the singularity function of a fractional process. In [4] they are used to estimate a deformation of an isotropic random field. For more results on the convergence of quadratic variations see, [5], [15], [14], [21], [7], [30],[2], [6], [16], [10], [20].

2 The geometric anisotropic Matérn class

In this section we construct estimates of , and using increments of observed on a dense grid within . Using fixed domain asymptotics, we establish consistency of our estimates under assumptions (4) and (5) and provide bounds on the rate of variance decay as it depends on the number of increments used, the dimension of and the smoothness of measured by . These results will hold in any dimension. However, when the dimension is large enough (), the second term in (3) is influential enough so that can be estimated consistently.

If the observation region is an open subset of and the random field is modeled by (4) and (5), then is said to be a -dimensional geometric anisotropic Matérn random field with parameters . In this case, the covariance structure of is , where is defined as

| (6) |

for and . The function is the modified Bessel function of the second kind of order . Since for any orthogonal matrix , one can only identify up to left multiplication by an orthogonal matrix. To remove this identifiability problem we suppose that where denotes the orthogonal matrices in . In the theorems below, we write to mean that there exists a such that , and similarly for . Operationally, however, we estimate a representer of the cosets in given by the upper triangular matrices which have positive diagonal elements and determinant 1 (that this is a representer follows from the QR factorization, see [18]).

As discussed in the introduction, the principle irregular term is important in determining the sample path properties of the random field . The principle irregular term for the Matérn covariance function is

where is defined to be . Moreover,

| (7) |

where as and is an even polynomial. Notice that when is the identity matrix and , this gives the expansion (3) so that is the first principle irregular term and is the second term.

2.1 Estimating and in any dimension

Let be a bounded, open subset of and let . The idea is that we will be observing on a region, just a bit larger than , so that we can form the order increments of on . These will then be used to estimate and in any dimension and additionally , in dimension .

For a fixed nonzero vector define the increment in the direction by and the iterated directional increment . The following lemma establishes the relationship between the variance of these increments and the terms in (7) when the number of increments is sufficiently large.

Lemma 1.

Let be a mean zero, geometric anisotropic -dimensional Matérn Gaussian random field with parameters . If is a positive integer such that and is a non-zero vector, then

| (8) |

as where

| (9) | ||||

| (10) |

Now we are in a position to estimate the coefficient . Let denote the cardinality of the finite set and define

| (11) |

Notice that by equation (8), as . In addition, since is itself an average, one might hope that converges to . The following theorem shows that, indeed, this is the case. In addition, the theorem quantifies the decay of the variance of as a function of the number of increments, the smoothness of the random field and the dimension of the domain. The heuristic is that when the number of increments is large enough, there is sufficient decorrelation of the summands of to guarantee convergence as . Generally, more increments leads to more spatial decorrelation and hence a reduction in variance. However, this only holds up to a point, after which taking more increments no longer effects the rate of variance decay. Finally, the higher the dimension, the more increments one needs to take to get the best rate.

Theorem 1.

Let be a mean zero, geometric anisotropic -dimensional Matérn Gaussian random field with parameters and let be a bounded, open subset of . If then

| (12) |

as . Moreover, there exists a constant such that

for all sufficiently large .

The above theorem establishes that consistently estimates (which depends on ). Now we show how these estimates can be used to recover and . As was mentioned above, we suppose is upper triangular with determinant one and positive diagonal elements. After renormalizing by known constants, the values of allow us to consistently estimate where for finitely many directions . We show by induction that these values are sufficient to recover each column of . Once this is established, the requirement gives and .

Let denote the element of and let denote the column of . Also let be the submatrix with elements for . For the first column of , notice that where denote the standard basis of . This follows since is upper triangular with positive diagonal. For the inductive step suppose the first columns are known. Taking and allows us to recover and for . By adding and subtracting appropriate terms we can then recover: , for all . Therefore where . This establishes the inductive step and therefore can be identified from observing at different vectors (let them be denoted by ).

Notice that as ranges over the set of upper triangular matrices with positive diagonal, the transformation sends an open subset of to . Since is a continuous map,

as .

2.2 Estimating , when

In this section we construct an estimate of when , which, in combination with and , allows us to consistently estimate . We start by noticing that by Lemma 1, for any

as . The term is significant because, for any positive integer

where is a known constant depending on and . In addition, Lemma 2 in the Appendix establishes that and for at least one . Moreover, doesn’t depend on the unknown parameters , and and therefore one can construct from the observed values of the random field . The following theorem quantifies how large and need to be for the almost sure convergence of to .

Theorem 2.

Let be a mean zero, geometric anisotropic -dimensional Matérn Gaussian random field with parameters and let be a bounded, open subset of . Suppose are positive integers such that and both are large enough so that and . Then

as .

Theorems 1 and 2 show that there exists strongly consistent estimates of , and . This, in turn, gives consistent estimates of , and . Notice that when this is impossible due to the mutual absolute continuity of Matérn Gaussian random fields with different scale and variance parameters (see Zhang [33]). Since Gaussian measures are either mutually absolutely continuous or orthogonal, the fact that we have strongly consistent estimates of , and gives the following corollary.

Corollary 3.

Let and be two, mean zero, geometric anisotropic -dimensional Matérn Gaussian random fields defined a bounded open set with parameters and where . If or then the Gaussian measures induced by the random fields and are orthogonal.

Remark: The strong consistency results for our estimates of , and all depend on knowledge of the true value of . However, our results can be extended when using an estimate so long as the error satisfies with probability one as . This follows since the ratio of the quadratic variation, , using the true , to the quadratic variation using the estimated , is which converges to if .

3 Beyond the Matérn

The previous section dealt exclusively with the Matérn autocovariance. Now we show how these results can be extended to other autocovariance functions. We choose two examples to illustrate how the methodology can be easily extended beyond the Matérn autocovariance function. The key components for showing extensions are establishing versions of Lemmas 1 and 4. Lemma 1 quantifies the expected value of the squared increments in terms of . Lemma 4 establishes that, in effect, derivatives of the covariance away from the origin are dominated by the derivatives of the principle irregular term. Once the analogs of these Lemmas are established all the subsequent arguments for versions of Theorems 1 and 2 follow almost immediately.

For our first example we consider the case when is a mean zero Gaussian random field on with generalized autocovariance function where and are known but and are unknown (it is tacitly assumed that the values of and give a conditionally positive definite function of order in , see [9]). In what follows we suppose and neither are even integers. The appropriate version of Lemma 1 says that when

| (13) |

where . Now is defined as in (11) with in place of . In this case, and therefore we set . Also, for an integer we have and after a renormalization one gets the estimate . The analog to Lemma 4 says that when and is a bounded open subset of there exists a constant such that

| (14) |

for all such that . Once (13) and (14) are established, versions of Lemma 6, Lemma 7, Lemma 8 and Theorem 1 following by replacing with . To establish Theorem 2, replace the term with in equation (47) and continue in an similar manner to establish the following theorem.

Theorem 4.

Suppose is a mean zero Gaussian random field on with generalized autocovariance function observed on where is a bounded open subset of and are known and not even integers. If then there exists integers such that and (defined above) converge with probability one to and (respectively) as .

There are different conditions on to guarantee convergence of versus . Generally, one only needs for consistent estimation of , which will hold in any dimension. However, in our case, we need the additional requirement that since we are working with a conditionally positive definite function of order . To get consistent estimation of we need the additional inequality . To relate this to our Matérn results in Section 2 set and so that the inequality becomes which appears in Theorem 2. Finally the analog to Lemma 2 guarantees there exits a such that is non-zero which allows us to define .

Before we continue, we mention a comment in Wahba’s book ([31], page 44) which argues in favor of using the generalized autocovariance over the model when . The reasoning is that the two models yield mutually absolutely continuous Gaussian measures, and therefore can not be consistently distinguished. We can see, however, that the dimension requirement is an integral component of this argument. When the dimension gets above , this reasoning no longer holds since the two models are orthogonal by the above theorem (setting and ).

For our second extension we show that the variance and scale can be separately estimated in the exponential autocovariance model when the dimension and . In this case, the appropriate version of Lemma 1 becomes

| (15) |

as when . From (15) one can now easily construct estimates of and . When a geometric anisotropy is present, the techniques of Section 2 are also sufficient to also construct . Notice that by direct differentiation, equation (14) holds when is replaced by . Using similar arguments for the previous theorem and extending to a geometric anisotropy the following theorem is obtained.

Theorem 5.

Let be a mean zero, Gaussian process on with autocovariance function observed on where is a bounded open subset of . Suppose is known, and are positive and is upper triangular with positive diagonal and determinant 1. If then and with probability one as . Moreover, if and then for any there exists such that and with probability one as .

Many other extensions are possible, including more general non-stationary random fields. In this case, both and depend on and will convergence to and similarly for . If one also needs pointwise convergence to or one can consider weighted local averaging of the terms in . This was the technique used in [4] when observing a deformed isotropic Gaussian random field that locally behaved like a fractional Brownian field. However, obtaining extensions in these cases are more difficult since one needs to consider rates of decay for a bandwidth parameter. That being said, this work leaves open the possibility of constructing consistent estimates of the two deformations when observing where and have generalized autocovariance functions and respectively. Finally we mention that since is constructed from increments, one can extend our results to random fields with a polynomial drift of known order.

4 Simulations

We finish with two simulations that illustrate (and hopefully compliment) our theoretical results. The first simulation shows how one can use directional increments to estimate and a geometric anisotropy using finitely many directions. The second simulation shows how to estimate the coefficient on the ‘second principle irregular term’ ( in equation (2)) and how it can be used to construct an unbiased estimate of the coefficient on the ‘first principle irregular term’ ( in equation (2)).

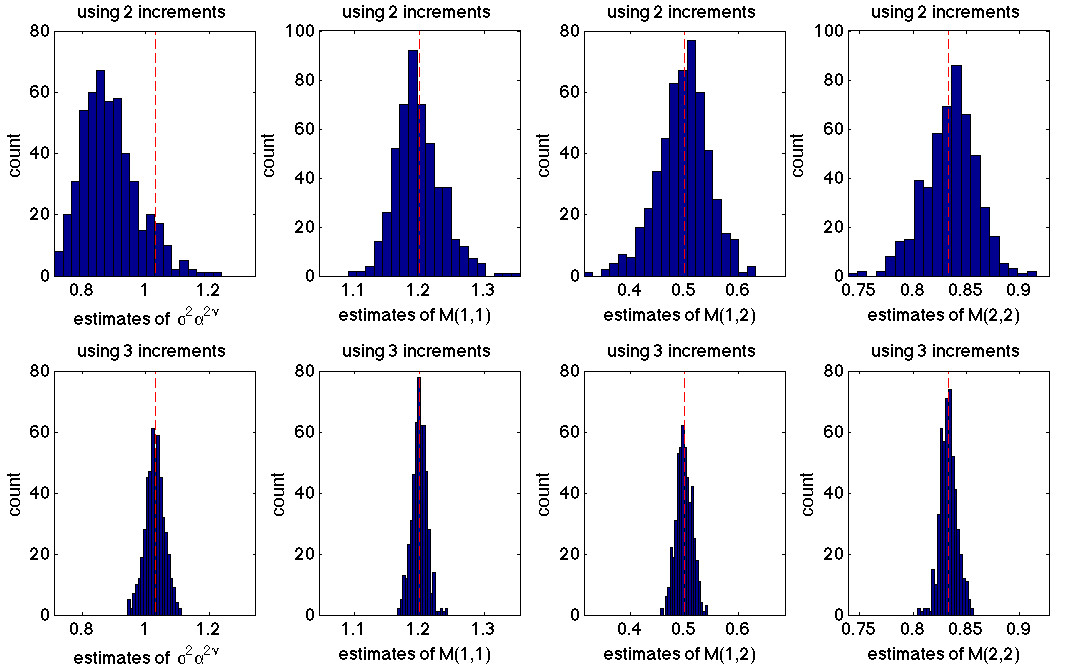

In our first example, we simulated 500 independent realizations of a Matérn random field with parameters , , , , , and observed on a square grid in with spacing . On each realization we estimated and using , and horizontal, vertical and diagonal increments. Notice that since , this random field is once, but not twice, mean square differentiable. Intuitively, we therefore need at least two increments for sufficient de-correlation of the terms in the quadratic variation sum (2). Table 1 displays the root mean squared error (RMSE) for estimating , the true value is approximately , and the elements of . Figure 2 plots histograms of the estimates for and increments. It is immediately clear that there is a large reduction in RMSE when using increments as compared to increments (and an additional bias reduction when estimating ). Indeed, by Theorem 1, more increments leads to more spatial decorrelation and hence a reduction in variance. In this case, so that the estimate based on increments is guaranteed to be consistent but the variance decays at a sub-optimal rate. Since , the variance of the estimate based on increments decays at the optimal rate. However, Theorem 1 also says that this variance reduction only holds up to a point, after which taking more increments no longer effects the rate of variance decay. Indeed, it is seen in Table 1 that taking 4 increments do not improve the RMSE nearly as much.

| 2 increments | 3 increments | 4 increments | |

|---|---|---|---|

| 0.1664 | 0.0300 | 0.0289 | |

| 0.0360 | 0.0114 | 0.0113 | |

| 0.0475 | 0.0147 | 0.0147 | |

| 0.0248 | 0.0079 | 0.0079 |

Our second simulation uses the results of Section 3 to estimate and when observing on at pixel locations where , and is independent of . The random field has autocovariance and has autocovariance which is positive definite on (see [29] for a proof). Our estimates of and are defined by

| (16) | ||||

| (17) |

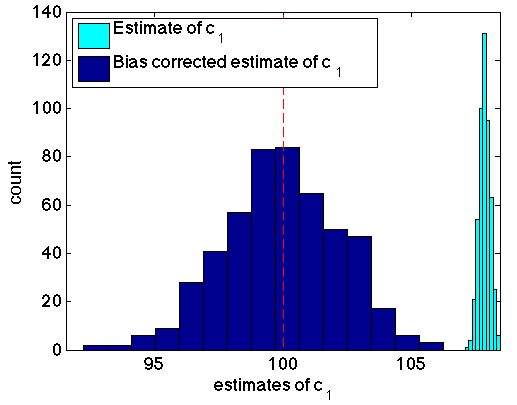

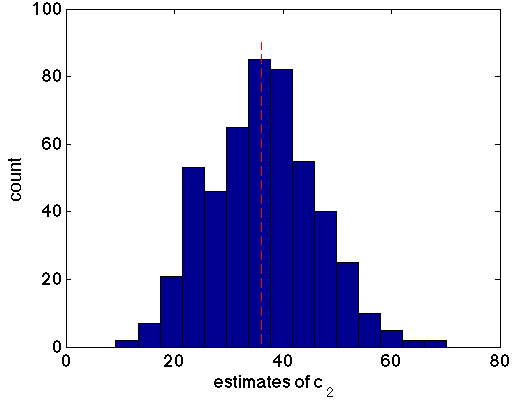

where , , , and . This example was chosen to illustrate the duality when estimating and : the smaller (in relation to the dimension ) the smaller the variance of and but the larger the bias of . In fact, as the dimension grows, the variance decreases at a faster rate (proportional to when using enough increments) but the bias decreases at the same asymptotic rate for any (proportional to ). In our example, since (so the quadratic term vanishes), we can explicitly compute the bias using equation (13) so that . Notice that using our estimate of we can now correct the bias in . The left plot of Figure 3 shows two histograms of the estimate and the bias corrected estimate on the 500 simulated realizations. The right plot of Figure 3 shows the histogram of the estimate . We can see that not only is it possible to get an estimate of , but using it to correct the bias in reduces the RMSE for estimating (from down to ).

Appendix A Proofs

We start with some notation. For a function of two variables let where acts on the variable and acts on the variable . Define to be the directional derivative in the direction and where acts on the variable and acts on .

Let be real valued functions defined on some set and let . We write for all if there there exists a positive constant such that for all . Notice that this definition also works for a sequence of functions by considering the variable as an argument and replacing by .

Proof of Lemma 1.

We suppose and is the identity matrix, then rescale for the general case. First note two immediate facts about the directional increment operator : for any function the -increment of can be computed where ; The -increment annihilates monomials of degree less than so that for all . Therefore, by the expansions given on page 375 of [1] we have

where as . Now for a fixed

where

| (18) | ||||

| (19) | ||||

| (20) |

Notice that . This is obviously true with . It also holds when since

| (21) |

and (since and ). Similar arguments can be applied to when which gives . Finally, notice that implies that . This establishes the claim when and is the identity matrix. The general result when and is then established by an easy rescaling argument (using equation (21) when ). ∎

Lemma 2.

Proof.

Notice first that where is an intrinsic random function on observed on with generalized covariance (since annihilates polynomials of order , and , see [28]). The same reasoning establishes that when .

For the last part of the lemma we show that there exists such that

We will argue by contradiction and suppose that for all ,

| (22) |

By a spectral representation of (see [28] page 36) and an easy induction establishes that and . Notice also that . Let and be two probability measures on defined by

Our assumption (22) then becomes

| (23) |

for all . Notice that the variances and serve as the normalizing constants so that and have total mass one. In what follows we show that the normalizing constants satisfy both and to establish the desired contradiction.

By the equalities in (23), the random variables and have the same moments when and . In addition, and so that the moment generating functions are both finite in a non-empty radius of the origin. Therefore , where denotes equality in law. This gives , for example. However

by the fact that . Therefore

| (24) |

To show the contradicting inequality let’s start by computing the density of these two random variables. The idea is to show that the non-normalized (i.e. without the term ) density of is strictly smaller than the non-normalized density of in a positive neighborhood of . In particular, the density of can be written as where the ’s are the different positive branches of the inverse and is the density of . This simplifies to

for . Notice that as and as for all . Therefore the term dominates the sum when is small. In particular for all sufficiently small we have

| (25) | ||||

| (26) |

Since and have the same integrate integrals over Borel subsets of , we must have . This contradicts (24) and therefore establishes the lemma. ∎

Lemma 3.

For any , ,

as ranges in the interval where is the modified Bessel function of the second kind of order .

Proof.

Using the expansions for found in [1] (page 375) we can write

| (27) |

where the ’s are of the form where the ’s decay fast enough so that the series converges absolutely for all and all it’s derivatives exist and are bounded on . This immediately establishes that when , for all since both and are continuous and bounded on .

When and we have that as ranges in the bounded interval . Similarly, when and we have

Finally, when , . The lemma now follows by equation (27) and the fact that the derivative of a product satisfies .

∎

Lemma 4.

Suppose is the isotropic Matérn autocovariance function defined in (6) for fixed parameters . Then for any integer , nonzero vector , matrix and bounded set

| (28) |

for all such that .

Proof.

First notice that it is sufficient to show the claim when is the identity matrix and (extending to general and follows by the chain rule for derivatives). Define and so that . Also let denote a generic directional derivative on either the variable or . By generic I mean that denotes for some and where each could be with respect to or . Now by successive application of the directional derivatives we get that

| (29) |

where each is uniformly bounded on . The functions are uniformly bounded by the nice fact that on when .

We will bound the terms of the sum (29) when , , and separately. Notice first that since we have that

| (30) |

This implies, by Lemma 3, that the terms in the sum (29), for which , are bounded. When

where the inequality holds for all such that (note that we use the fact that is bounded implies for some ). For the last case, , a similar argument establishes

for all such that . Therefore for all such that . ∎

Lemma 5.

Let be a nonzero vector in , and be the matrix defined by

| (31) |

If is a positive integer greater than then

for all positive integers and such that .

Proof.

First notice that . Now for any , positive integer and such that , we have

The last line follows from the assumption that which implies . Therefore

∎

Lemma 6.

Let be a mean zero, geometric anisotropic -dimensional Matérn Gaussian random field with parameters and let be a bounded, open subset of . Fix a positive integer and a non-zero vector . Let to be the covariance matrix of the increments as ranges in the set so that

| (32) |

for all . Then there exists an such that

| (33) |

for all , and such that . Moreover,

| (34) |

for all and such that .

Proof.

First notice that where is the isotropic Matérn autocovariance function defined in (6). To simplify the notation let and be the by matrix defined in (31). An induction argument on establishes that when we can express directional increments as integrals of directional derivatives so that

Therefore

for all , such that . On the other hand when

| (35) |

where the last inequality is by Lemma 1. Actually, a direct application of Lemma 1 only establishes (35) when . However, a small adjustment of the proof of Lemma 1 establishes that as when . This is then is sufficient to establish (35). ∎

Lemma 7.

Proof.

First note that by symmetry, , where is the maximum of the row norms and is the maximum of the column norms. To bound the row norms, we bound the terms of the sum when and separately. For the off-diagonal terms we use Lemma 6 to ensure the existence of an such that for all

| (36) | ||||

| (37) |

The last inequality, (37), follows by the fact that for any constant and open set which is bounded and contains the origin, one has

| (38) |

as (for details see [3], Lemma 3, page 41). In addition, by Lemma 6

| (39) |

for all . This establishes the proof by noticing that the sum of the last terms in (37) and (39) bound . ∎

Lemma 8.

Under the same assumptions as in Lemma 6 there exits an such that

for all where is a constant and denotes the Frobenious matrix norm.

Proof.

First note that . As in the proof of Lemma 8 we bound the near-diagonal terms of separately from the off-diagonal terms. By Lemma 6 there exists an such that

| (40) | ||||

| (41) |

for all . Notice that the last inequality is a slight variation on (38). For the near diagonal terms we also use Lemma 6 to get

| (42) |

Proof of Theorem 1.

Define the random vector to be the vector of -increments, the components of which are indexed by (in any order), so that

| (43) |

Now we can write , where (note that is defined in (32)). Therefore and by Lemma 8

for all sufficiently large . This establishes the variance rates.

For the almost sure convergence result let where is the component-wise absolute value of . The Hanson and Wright bound in [17] then gives

| (44) |

for all , where are positive constants not depending on or . First notice that by Lemma 7 we get

| (45) | ||||

| (46) |

for sufficiently large . Also notice that this implies that for sufficiently large . Therefore for sufficiently small , . Now the rates in (46) and the Borel-Cantelli Lemma are sufficient to establish that , with probability one as . By Lemma 1, (a slight adjustment also proves the case when rather than ) which establishes the theorem. ∎

Proof of Theorem 2.

First notice that when

| (47) |

as by Lemma 1. To get almost sure convergence notice

| (48) | ||||

| (49) |

We can again use the Hanson and Wright bound ([17]) and the rates derived in Theorem 1 to get

| (50) |

for all sufficiently small where is a positive constant that doesn’t depend on or . By inspection of the rates in (46) the Borel-Cantelli Lemma can be applied when so that with probability one as . A similar result holds for the second term in (49) using the fact that both and are non-zero by Lemma 2. This, combined with convergence of the expectation in (47), completes the proof. ∎

Proof of Theorem 4.

First notice that for any

| (51) | ||||

| (52) |

where . This follows since is an intrinsic random function of order with generalized autocovariance function and is an allowable linear combination of order (see [9]). Now is defined as in (11) with in place of so that

For any integer we have that and . By a proof similar to Lemma 2 one can show that for any there exists a such that and (this uses the fact that , are not even integers). This motivates the following definition

| (53) | ||||

| (54) |

In what follows we show that implies as . Moreover if then there exists a such that .

We start by letting for all and where is the component-wise absolute value of . The Hanson and Wright bound in [17] gives

| (55) |

for all , where are positive constants not depending on or . Later in the proof we will show that when

| (56) |

for all sufficiently large . First, however, we show this is sufficient for the almost sure convergence result. Equations (55) and (56) immediately establishes that when since by Borel-Cantelli and . To see that notice that

| (57) |

for all sufficiently small and sufficiently large . Therefore, by inspection of the rates in (56), one can show that whenever and . Since , this is sufficient to establish that there exists a such that as when and .

Now to finish the proof we need to establish (56). We start by noticing that for any there exists a constant such that

for all such that where is a positive constant. Following the proofs of Lemma 6 we can then derive that there exists an such that for any

for all , and such that . Moreover,

for all and such that . Now by direct analogs to Lemma 7, Lemma 8 (by replacing with ) we have

| (58) | ||||

| (59) |

where , are positive constants. These equations hold when and are sufficient to establish (56). This completes the proof. ∎

Proof of Theorem 5.

First notice that since one can show that for any

| (60) | ||||

| (61) |

where . This follows by a proof exactly similar to that of Lemma 1.

Now is defined as in (11) with in place of so that

Therefore

| (62) |

and

| (63) |

By a proof similar to Lemma 2 one can show that for any one has that and if, additionally, there exists a such that and (this uses the fact that is not an even integer). This motivates the following definition

| (64) | ||||

| (65) |

In what follows we show that for any we have that as . Moreover, if and (this is required to guarantee that ) there exists a such that and . Notice that this is sufficient to prove the theorem since and together imply that and .

We start by letting for all and where is the component-wise absolute value of . The Hanson and Wright bound in [17] gives

| (66) |

for all , where are positive constants not depending on or . Later in the proof we will show that

| (67) |

for all sufficiently large . First, however, we show this is sufficient for the almost sure convergence result. Equations (66) and (67) immediately establishes that since by Borel-Cantelli and . To see that notice that equations (66) and (67) imply

| (68) |

for all sufficiently small and sufficiently large . Therefore whenever . Since , this is sufficient to establish a so that .

Now to finish the proof we need to establish (67). We start by noticing that for any there exists a constant such that

for all such that where is a positive constant. Following the proofs of Lemma 6 we can then derive that there exists an such that for any

for all , and such that . Moreover,

for all and such that . Now by direct analogs to Lemma 7, Lemma 8 (by replacing with ) we have

| (69) | ||||

| (70) |

where , are positive constants. These equations hold when and establish (67). This completes the proof. ∎

References

- [1] M. Abramowitz and I. Stegun. Handbook of Mathematical Functions. ninth ed. Dover, New York, 1965.

- [2] R. J. Adler and R. Pyke. Uniform quadratic variation for Gaussian processes. Stoch. Proc. Appl., 48:191–209, 1993.

- [3] E. Anderes. Estimating Deformations of Isotropic Gaussian Random Fields. PhD thesis, University of Chicago, 2005.

- [4] E. Anderes and S. Chatterjee. Consistent estimates of deformed isotropic gaussian random fields on the plane. Ann. Stat. To appear.

- [5] G. Baxter. A strong limit theorem for Gaussian processes. Proc. Amer. Math. Soc., 7:522–527, 1956.

- [6] A. Benassi, S. Cohen, J. Istas, and S. Jaffard. Identification of filtered white noises. Stoch. Proc. Appl., 75:31–49, 1998.

- [7] S. M. Berman. A version of the Lévy-Baxter theorem for the increments of Brownian motion of several parameters. Proc. Amer. Math. Soc., 18:1051–1055, 1967.

- [8] D. Nychka C. Kaufman, M. Schervish. Covariance tapering for likelihood-based estimation in large spatial datasets. J. Amer. Stat. Assoc. To appear.

- [9] J. Chilès and P. Delfiner. Geostatistics: Modeling Spatial Uncertainty. Wiley series in probability and statistics, 1999.

- [10] S. Cohen, X. Guyon, O. Perrin, and M. Pontier. Identification of an isometric transformation of the standard brownian sheet. J. of Stat. Planning and Inference., 136:1317–1330, 2006.

- [11] S. Cohen, X. Guyon, O. Perrin, and M. Pontier. Singularity functions for fractional processes: application to the fractional brownian sheet. Ann. Inst. Henri Poincaré, PR 42:187–205, 2006.

- [12] N. Cressie. Statistics for Spatial Data, revised ed. Wiley, New York, 1993.

- [13] J. Du, H. Zhang, and V. Mandrekar. Fixed-domain asymptotic properties of tapered maximum likelihood estimators. Ann. Stat. To appear.

- [14] R. M. Dudley. Sample functions of the Gaussian process. Ann. Probability, 1:66–103, 1973.

- [15] E. G. Gladyshev. A new limit theorem for stochastic processes with Gaussian increments. Theor. Probability Appl., 6:52–61, 1961.

- [16] X. Guyon and G. Leon. Convergence en loi des h-variations d’un processus gaussien stationnaire. Ann. Inst. Henri Poincaré, 25:265–282, 1989.

- [17] D.L. Hanson and F.T. Wright. A bound on tail probabilities for quadratic form in independent random variables. Ann. Math. Stat., 42:1079–1083, 1971.

- [18] R. Horn and C. Johnson. Matrix Analysis. Cambridge University Press, 2007.

- [19] I. A. Ibragimov and Y. A. Rozanov. Gaussian Random Processes. Springer, New York, 1978.

- [20] J. Istas and G. Lang. Quadratic variations and estimation of the local Hölder index of a Gaussian process. Ann. Inst. Henri Poincaré, 33:407–436, 1997.

- [21] R. Klein and E. Gine. On quadratic variation of processes with Gaussian increments. Ann. Probability, 3:716–721, 1975.

- [22] P. Lévy. Le mouvement brownien plan. Amer. J. Math., 62:487–550, 1940.

- [23] W.-L. Loh. Fixed-domain asymptotics for a subclass of matérn-type gaussian random fields. Ann. Stat., 33:2344–2394, 2005.

- [24] W.-L. Loh and T.-K. Lam. Estimating structured correlation matrices in smooth gaussian random field models. Ann. Stat., 28:880–904, 2000.

- [25] M. L. Stein. Asymptotically efficient prediction of a random field with a misspecified covariance function. Ann. Stat., 16:55–63, 1988.

- [26] M. L. Stein. Uniform asymptotic optimality of linear predictions of a random field using an incorrect second-order structure. Ann. Stat., 18:850–872, 1990.

- [27] M. L. Stein. A simple condition for asymptotic optimality of linear predictions of random fields. Statistics and Probability Letters, 17:399–404, 1993.

- [28] M. L. Stein. Interpolation of Spatial Data: Some Theory for Kriging. Springer, New York, 1999.

- [29] M. L. Stein. Fast and exact simulation of fractional Brownian surfaces. J. of Comput. and Graph. Stat., 11:587–599, 2002.

- [30] P. T. Strait. On Berman’s version of the Lévy-Baxter theorem. Proc. Amer. Math. Soc., 23:91–93, 1969.

- [31] G. Wahba. Spline Models for Observational Data. SIAM, Philadelphia, 1990.

- [32] Z. Ying. Asymptotic properties of a maximum likelihood estimator with data from a gaussian process. J. of Multi. Analysis, 36:280–296, 1991.

- [33] H. Zhang. Inconsistent estimation and asymptotically equal interpolations in model-based geostatistics. J. Amer. Stat. Assoc., 99:250–261, 2004.