Analysis of a network structure of the foreign currency exchange market

Abstract

We analyze structure of the world foreign currency exchange (FX) market viewed as a network of interacting currencies. We analyze daily time series of FX data for a set of 63 currencies, including gold, silver and platinum. We group together all the exchange rates with a common base currency and study each group separately. By applying the methods of filtered correlation matrix we identify clusters of closely related currencies. The clusters are formed typically according to the economical and geographical factors. We also study topology of weighted minimal spanning trees for different network representations (i.e., for different base currencies) and find that in a majority of representations the network has a hierarchical scale-free structure. In addition, we analyze the temporal evolution of the network and detect that its structure is not stable over time. A medium-term trend can be identified which affects the USD node by decreasing its centrality. Our analysis shows also an increasing role of euro in the world’s currency market.

Keywords:

Foreign exchange market Correlation matrix Networks Minimal Spanning Tree1 Introduction

There are at least two reasons for analyzing the global foreign exchange (FX) market. First, this is the world’s largest and most important financial market, completely decentralized, extending over all the countries, with the highest daily trading volume reaching trillions of US dollars. Second, the FX market’s dynamics seems to be more complex than any other market’s. The absence of an independent reference frame makes the absolute currency pricing difficult or even impossible: one has to express a given currency’s value by means of some other currency which, in turn, is also denominated only in currencies. Moreover, apart from its internal dynamics, the global nature of the FX market implies sensitivity to current situation on other markets in all parts of the world. These properties together with the triangle rule aiba02 which links mutual exchange rates of three currencies are among the factors responsible for a highly correlated structure of Forex.

Correlations allow one to view the FX market’s structure as a network of interacting exchange rates. In this case the exchange rates are treated as network nodes and are linked with their neighbours via edges with weights proportional to the coupling strength. And although the exact nature of these interactions remains unexplained, it is justified to assume that they are strongly nonlinear. This indicates that the FX market may actually constitute a complex network.

An analysis of the currency exchange network can provide us with knowledge of the structure of the market and about a role played in it by each particular currency. We put stress on quantification of a currency’s importance in the world financial system and on tracking its subtle changes as the market evolves in time. We achieve this by employing the well-known methods of correlation matrix (CM) and minimal spanning trees (MST). However, one has to be aware that both these methods, although simple and effective, are linear and thus they detect only a part of interactions between the exchange rates; nonlinear contributions to the internode couplings are neglected.

An exchange rate assigns value to a currency X by expressing it in terms of a base currency B. In general, each currency can be a base for all other ones. Since different currencies may have different internal dynamics related to domestic economy, inflation, and sensitivity to events in other countries and markets, behaviour of the exchange rates is strongly dependent on a particular choice of the base. What follows, there is no absolute correlation structure of the FX network; its structure depends largely on the base currency.

2 Methodology and Results

2.1 Data and nomenclature

We analyze daily data sauder for a 63-element set comprising 60 actual currencies and 3 precious metals: gold, silver, and platinum. We consider the inclusion of these metals in our analysis as justified due to the two following reasons: First, gold and other precious metals are historically closely related to the currency system (silver and gold coins, the gold standard etc.). Even if at present there is no explicit relation between the official monetary system and the precious metals, they are still perceived by many as a convenient alternative to real currencies in times of high inflation or deep crises. Second, we prefer to include the precious metals also because they, if treated as a reference frame, can allow us to look at the actual currency market from outside. In this context the precious metals can serve as a benchmark of being decoupled from the market.

For denoting the currencies we adopted the ISO 4217 standard using three-letter codes (CHF, GBP, USD etc.). Our data spans the time period of 9.5 years from 1 January 1999 to 30 June 2008. At a time instant , the exchange rate B/X is . We conventionally define the exchange rate returns as the logarithmic exchange rate increments over an interval day. From our basket of currencies we obtained time series of length . All time series were preprocessed in order to eliminate artifacts and too extreme data points that can misleadingly dominate the outcomes; no points that deviate more than 10 standard deviations from the mean were allowed. Owing to a high quality of data, only a few data points in total were modified accordingly.

Dealing with all the available exchange rates for 63 currencies simultaneously would be rather inefficient due to information overload and would lead to results whose interpreting might be cumbersome. Attempts in this direction can be found elsewhere - for example, in ref. mcdonald05 ; we prefer here a more selective approach. An indirect but useful way to get some insight into properties of an individual currency, if only a set of its exchange rates is available, is to single out those rates in which this currency serves as a base currency and apply a statistical approach to the data. By selecting the base currency one associates a reference frame with this currency. Thus, the evolution of all other currencies expressed by relevant exchange rates is the evolution in the frame in which the base currency “rests”. In this context, a statistical analysis of the exchange rates offers information on how the global FX market looks like from the perspective of the base currency or, conversely, how the base currency behaves in relation to the global market.

2.2 Correlation matrix formalism

Details of the basic correlation matrix formalism are as follows. For a set of exchange rates sharing the same base B we calculate an correlation matrix :

| (1) |

where is data matrix and the bar denotes matrix transpose. Each entry is the correlation coefficient calculated for a pair of the exchange rates B/X and B/Y. If the exchange rates are considered as network nodes, the correlation matrix is equivalent to the weights matrix collecting the weights of links between the nodes. The so-defined correlation matrix is a starting point for our further calculations.

The market global correlation structure, as it is viewed from B, can be described by the eigenspectrum of . Complete set of the corresponding eigenvectors and eigenvalues () can be obtained by solving the equation

| (2) |

For a stock market it is typical that the associated correlation matrix can be decomposed into three components:

| (3) |

The first component describes a collective (market) mode characterizing the average behaviour of the whole market. describes the sectored structure of the market and expresses independent behaviour of individual stocks. On a matrix level, has all its entries equal and its rank is 1, while is a random matrix drawn from the Wishart ensemble. The middle term in Eq. (3) is a matrix with a typical rank which contains the most interesting information on the stock market structure plerou02 ; utsugi04 ; kim05 .

2.3 Eigenspectra of CM for different base currencies

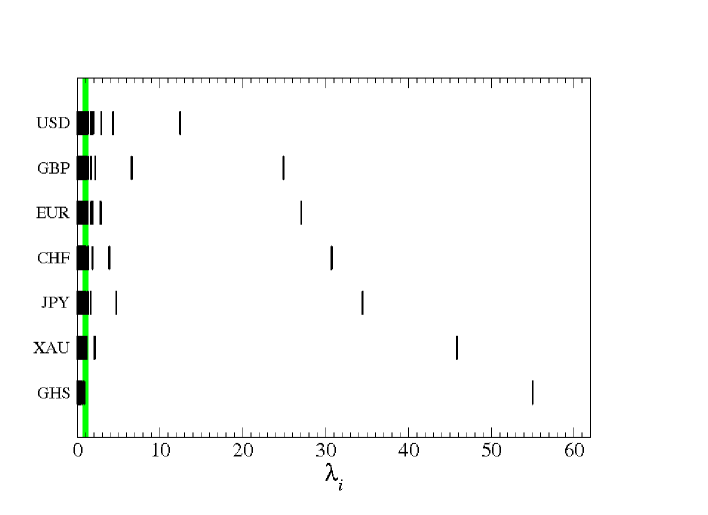

Taking outcomes of some earlier works mcdonald05 ; mizuno06 ; naylor07 ; drozdz07a into consideration we are justified to assume that also the FX market possesses similar correlation structure which can be decomposed into the analogous three levels of currency dependencies. To inspect this, we calculate the CMs and derived their eigenvalue spectra for all 63 base currencies. In each case the same scheme is reproduced: there is a collective mode represented by the largest eigenvalue with . Size of the gap between and is B-dependent. A few examples can be seen in Figure 1.

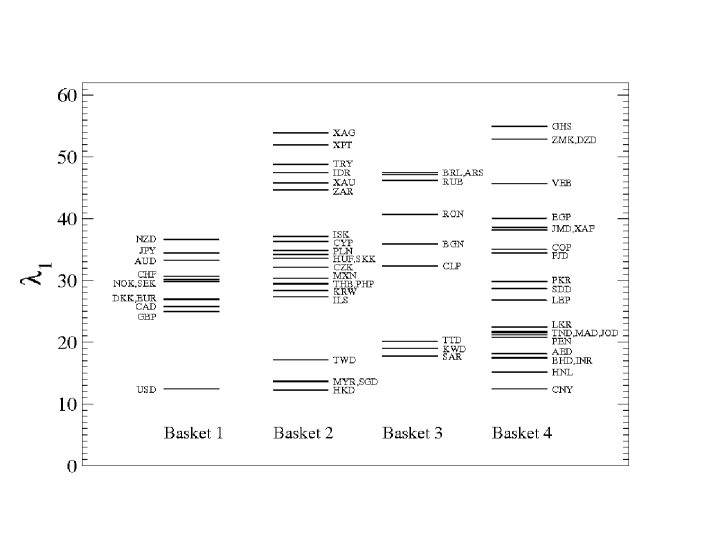

Magnitude of expresses how many exchange rates are correlated among themselves, i.e. how collective is the market. Properties of the matrix trace impose bounds on the magnitude of the largest eigenvalue: . In our case the range of the actual variability of is narrower: with the extrema reached for HKD and GHS, respectively. Figure 2 displays the corresponding for each B analyzed. The whole set of currencies has been divided there into four baskets with respect to liquidity of each currency. The most important and liquid currencies belong to Basket 1 and other liquid ones to Basket 2.

A straightforward interpretation of points out to the fact that the larger it is, the more coupled is behaviour of the underlying exchange rate sets. That is, for large comparable with , the global FX market evolves collectively in the reference frame of B. This actually means that the evolution of B is significantly decoupled and has its own independent dynamics not related to the global market. In such a case the influence of this currency on other currencies is marginal if at all. What is natural, the precious metals (XAG, XAU, XPT) as commodities qualify here, but, surprisingly, the same is true for a few actual currencies (e.g. GHS, DZD, ZAR, BRL). Reasons for this type of behaviour may comprise high inflation rate in the corresponding countries or a strong regulation of the market by local financial authorities (Basket 4). It is worth noting that no Basket 1 currency belongs to this group.

On the opposite pole (relatively small ) there is the US dollar and a few other currencies from different baskets (CNY, HKD, SGD etc.) In general, small values of are developed by the systems which do not display strong couplings among its elements. Hence, evolution of the exchange rates seen from the USD perspective must be rather decorrelated and many currencies enjoy large amounts of independence. Such a degree of independence is not observed for any other liquid, market-valued base currencies from Basket 1. Thus, by changing the base from one of those currencies to USD, many explicit satellites of USD and its more delicately related companions acquire a dose of freedom. This phenomenon is a manifestation of the leading role of USD in the global foreign exchange system.

A careful investigation of Figure 2 suggests that healthy, freely convertible currencies generally are associated with .

Going back to Figure 1, it is evident from the eigenspectra that the FX market might have a finer sectored structure similarly to the stock and the commodity markets sieczka08 . For most base currencies, apart from there are smaller eigenvalues which also do not coincide with the spectrum predicted for the Wishart matrix ensemble by the random matrix theory sengupta99 (see the shaded region in Figure 1). A possible way to extract information on a more subtle structure of the FX market would be removing the market component from the matrix , since it absorbs a significant fraction of the total variance of signals and suppresses other components. However, we prefer here an alternative approach, based on direct removing of specific exchange rates.

It is well known that due to strength of the associated economies and the investors confidence, the US dollar and euro are the most influential currencies. Their significant impact on other currencies is manifested in the network representation of the FX market by a key positions of the nodes representing the exchange rates involving at least one of these currencies mizuno06 ; naylor07 ; gorski08 . For all choices of B, satellite currencies of either USD or EUR have their exchange rates strongly correlated with B/USD or B/EUR. This implies that, from a point of view of a given base currency, the collective behaviour of the market expressed, e.g., in terms of the repelled is, at least in part, an effect of these correlations. In order to get more insight into subtle dependencies among the exchange rates, now masked by the USD- and EUR-induced correlations, these two groups of couplings have to be removed. This can be accomplished by subtracting the USD- and EUR-related components from each original signal B/X by least square fitting to (Y denotes either USD or EUR):

| (4) |

The residual component is just the exchange rate (B/X)’ linearly independent of B/Y.

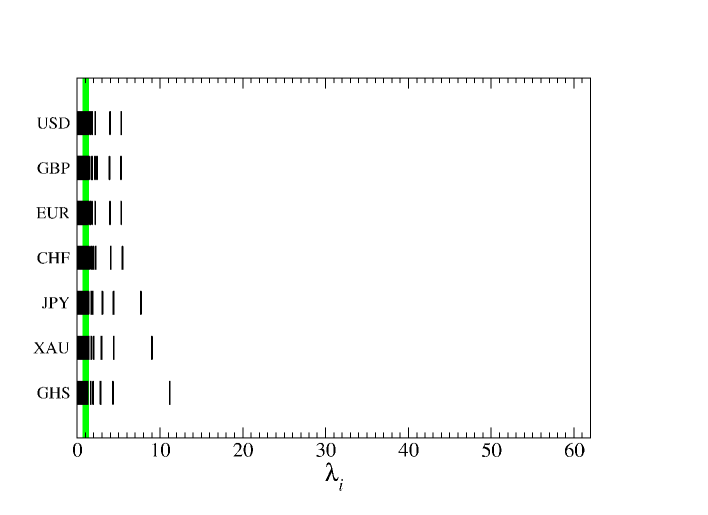

For a given B, we apply the above procedure to each exchange rate B/X twice: first for Y=USD, then for Y=EUR. Of course, if B=USD or B=EUR, Eq.(4) is applied only once, since the cases of the EUR/EUR and USD/USD rates are trivial. The correlation matrix constructed from the signals can again be diagonalized and its eigenspectrum can be calculated. Figure 3 shows the so-modified eigenspectra for the same base currencies as in Figure 1. Clearly, now there is no collective market mode for USD, EUR, GBP and CHF. This means that, for this group of base currencies, the entire collectivity of the market, as seen in the corresponding values of in Figure 2, stems from the couplings between USD and its satellites and between EUR and its satellites. No other factor contributes here. The eigenspectra with some eigenvalues which still do not fit into the predicted range for the random matrices do not show any considerable differences between different base currencies. This observation, however, is not valid for JPY, XAU and GHS (Figure 3). Here the largest eigenvalue deviates more from the rest of the spectrum, although not so strongly as in Figure 1. This residual collective behaviour can be explained by the existence of a significantly populated cluster of currencies which survived the process of removing the B/USD and B/EUR.

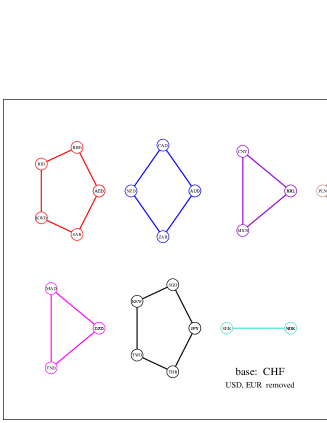

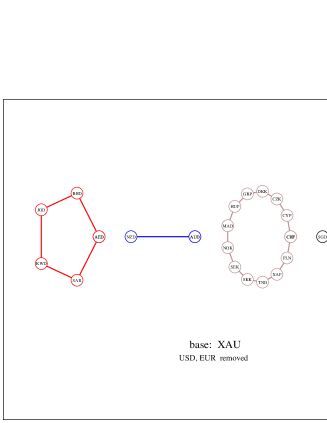

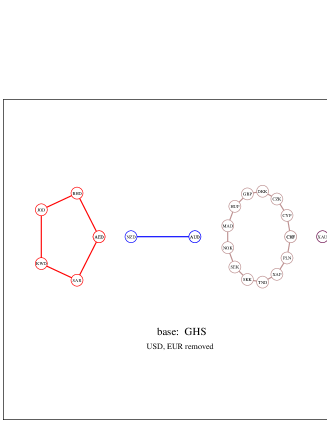

2.4 Cluster structure of the FX market

The residual correlations which develop the non-random structure of the CM eigenspectra in Figure 3 lead to the existence of currency clusters which previously were masked by the dominating nodes of USD and EUR. Identification of these clusters can be carried out with help of a simple method of discriminating threshold applied to CM entries kim05 . The procedure is as follows: we stepwise change the threshold from its maximal value down to 0 or even below 0. For each value of we preserve only those matrix entries that obey the inequality and substitute zeros otherwise. Then we count the clusters of at least two exchange rates. We define clusters as the disjoint sets of all residual exchange rates (B/X)’ that are linked by a non-zero matrix entries to at least one cross-rate (B/Z)’, ZX.

Obviously, for there is no cluster and for sufficiently small there is exactly one cluster comprising all exchange rates. On the other hand, for the intermediate values of the number of clusters varies and may exceed 1. In order to identify the finest possible cluster structure of the market and to identify the exchange rates that form each cluster, we fix the threshold at for which the number of clusters is stable and close to a maximum.

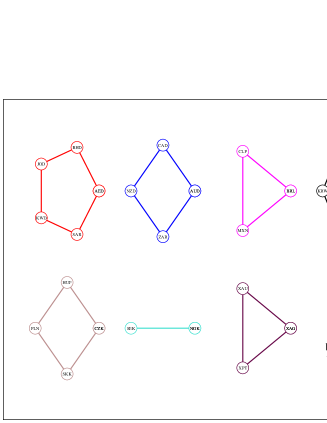

Figure 4 shows the clusters that have been found for the same six base currencies as in Figures 1 and 3 (in all Figures we label nodes, i.e., the exchange rates B/X, only with the term currency X, dropping the base B, since B is common to all exchange rates in a particular network representation). The cluster structure of the FX network is considerably stable. There are clusters, like the Middle East cluster AED-BHD-JOD-KWD-SAR and the commodity-trade-related cluster AUD-NZD-(CAD)-(ZAR), which are present in all network representations, there are also ones which can be found only in some representations (e.g. the Central European cluster CZK-HUF-PLN-SKK, the Scandinavian cluster NOK-SEK, and the precious metals cluster XAG-XAU-XPT). In general, among the analyzed network representations there are two dominating patterns of the cluster structure: the first one for CHF, EUR, GBP and USD, and the second one for JPY, XAU and GHS. This overlaps with the two different patterns of the eigenvalue spectra shown in Figure 3. Our results show that the currencies group together primarily according to geographical factors, but sometimes also according to other factors like, for example, the commodity trade.

2.5 Minimal spanning tree

A useful tool in analysis of the structure of a network is the minimal spanning tree method (MST), which allows one to describe and show the most important features of the network structure graphically in a compact form. For example, the B-based currency network is a fully connected undirected network with nodes and connections; the minimal spanning tree graph in this case has the same number of nodes but only connections.

The method is based on a metric defined on the entries of the correlation matrix by the formula:

| (5) |

In our case this quantity measures the distance between two exchange rates B/X and B/Y. For completely correlated signals and for completely anticorrelated ones . MST is then constructed by sorting the list of distances calculated for all pairs (X,Y) and by connecting the closest nodes with respect to in such a manner that each pair of nodes is connected exactly via one path. Each edge represents a link between this node and its closest neighbour. Detailed instructions can be found e.g. in mantegna99 . MST assigns to each node a measure of its importance in a hierarchy of nodes: a node is more significant if it has a higher degree , i.e. has more edges attached to it or, in a case of weighted networks, has edges with high weights.

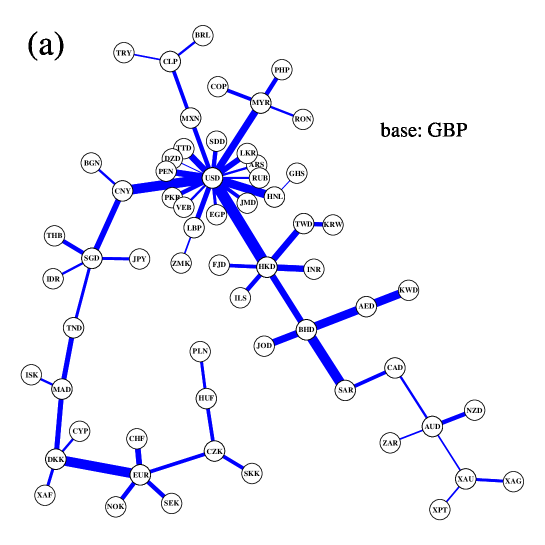

The complete minimal spanning tree for the GBP-based network is plotted in Figure 5(a). This choice of B allows us to observe the most complete cluster structure (see Figure 4(b)). In agreement with our remark from the previous section, the most important node is the node related to USD with a degree (it is directly linked to 28% of nodes). Other important nodes are HKD (), SGD and EUR (), as well as BHD, AUD, DKK and MYR (). Some edges are particularly strong (heavy lines in Figure 5) which typically indicates that one of the associated currencies is artificially pegged to the other. This is the case, for instance, of DKK-EUR, HKD-USD, MYR-USD and so on. Pegs lead to a situation in which certain nodes, in fact primarily coupled to EUR or USD, are effectively connected to less important currencies as DKK or HKD. This is why HKD has a larger multiplicity in Figure 5(a) than EUR, and a few other nodes have significant degrees even if they do not belong to the group of major currencies (BHD is a striking example here). Without this effect both USD and EUR would have a much larger value of .

In order to avoid this spurious phenomenon of absorbing a fraction of centrality of the major currencies by their satellites, we single out only those exchange rates GBP/X which involve independent currencies, i.e. such currencies which, in the analyzed interval of time, were not explicitely pegged to other monetary units. Figure 6 shows the corresponding MST comprising 41 nodes. Now the tree looks different. The USD node is even more central (, direct links with 40% of nodes) than for the full set of currencies in Figure 5(a), and it is followed by EUR (), SGD () and AUD (). This better reflects the role played by USD, EUR and AUD in the world’s currency system. SGD, which is here the least important unit, owes its localization in the MST to its specific basket-oriented regulation.

Figures 5(a) and 6 show that the currency network has a hierarchical structure, which supports earlier findings mizuno06 ; naylor07 ; gorski08 . These graphs, however, do not allow to observe the clustered structure discussed in the previous section. However, by neglecting the influence of the GBP/USD and GBP/EUR exchange rates (Eq.(4)), most clusters can easily be revealed. Indeed, in Figure 5(b) the cluster of AUD-CAD-NZD, as well as the ones of the Maghreb currencies, the Central European currencies, the Middle East currencies, the South-East Asian currencies, and the precious metals are identifiable. The hierarchical structure of the original network is lost here, however: the incomplete network of Figure 5(b) resembles rather a random graph.

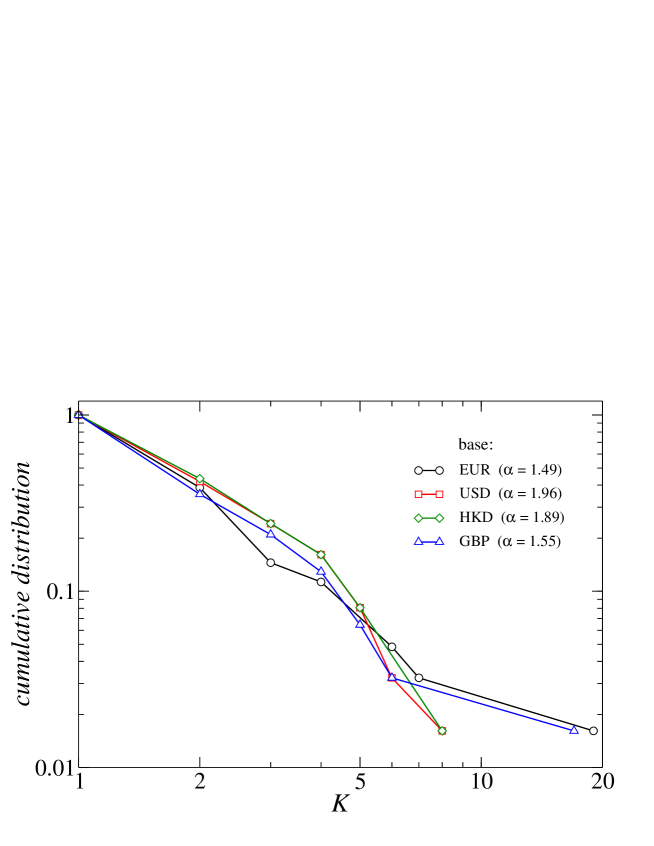

In order to be able to say something more on the MST topology, we calculate a distribution of the node degrees for the GBP-based network from Figure 5(a). We count the number of nodes of the same degree and calculate the cumulative distribution function for this quantity. This empirical distribution resembles the scale-free power-law behaviour, thus we attempt to fit the power function and evaluate the scaling exponent . For the GBP-based MST .

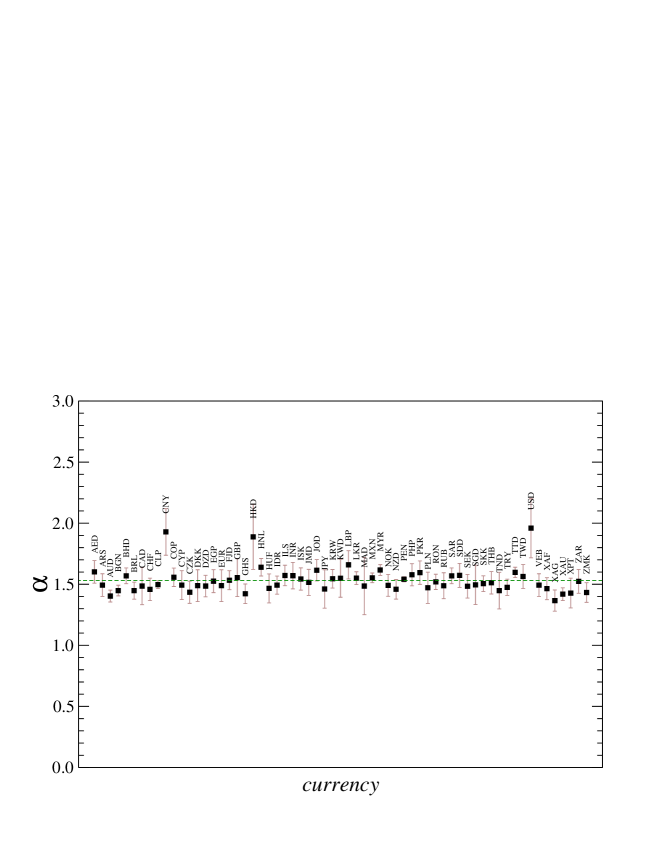

It is worthwhile to compare the scaling exponents for the cumulative distributions of the node degrees using different base currencies. Typically, the scaling relations exhibited by the c.d.f.s are of statistical significance and the corresponding scaling exponents can be estimated with only a small error gorski08 . The exponents have values in the range but a vast majority of values do not exceed 1.66. Only for five base currencies : this happens for USD (), CNY (), and HKD (). In all these cases the scaling quality is also poor, as the significant statistical errors indicate. Both HKD and CNY are tied to USD and therefore they mimic its evolution. Moreover, they develop a small collective eigenvalue (Figure 2), which is also a property inherited from the US dollar. This result suggests that the base currencies with high values of are associated with the network representations that are more random than typical hierarchical networks. It occurs that the exponent averaged over all base currencies , in agreement with the theoretically derived value of 1.61 for a hierarchical network of the same size ravasz03 ; noh03 . The above results are displayed in Figure 7.

2.6 Temporal stability of the market structure

Earlier works showed that the currency networks, expressed by the MST graphs, are sensitive to current market situation - for instance, to which currencies are most active at the moment mcdonald05 ; naylor07 . However, despite this fact a majority of network edges were reported to be rather stable.

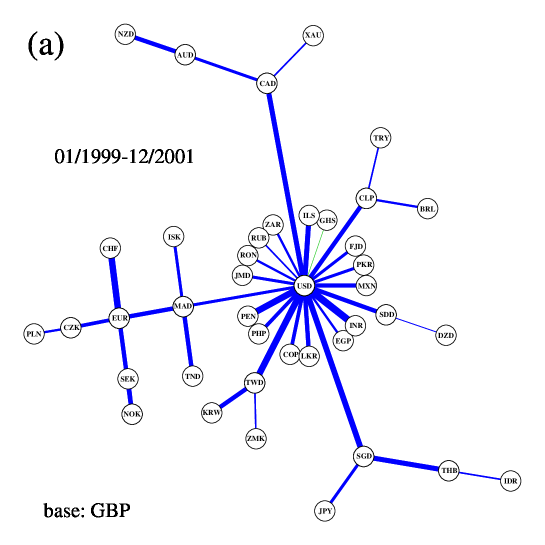

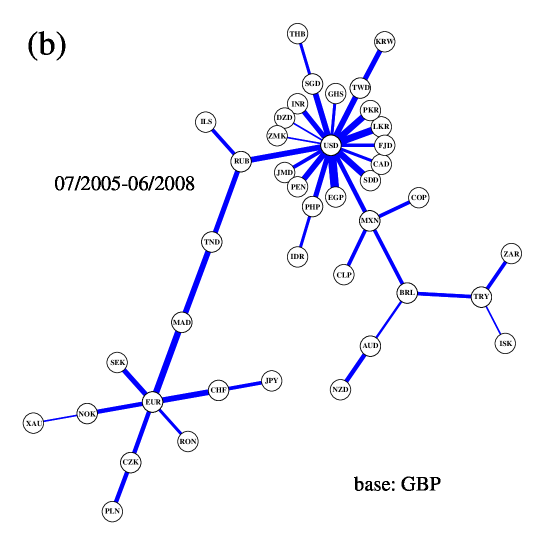

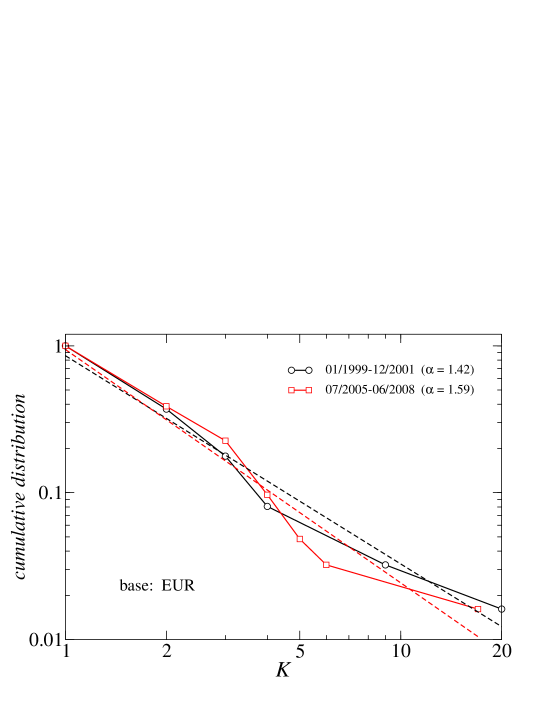

As an example of the MST variability, in Figure 8 we present the exemplary GBP-based trees for the two disjoint and mutually distant time intervals of three years: 01/1999-12/2001 (Interval 1) and 07/2005-06/2008 (Interval 2). To eliminate the spurious wandering of nodes between the major currencies and their satellites, we restricted the network to 41 independent exchange rates (as it was the case for the entire period in Figure 6). In fact, the structure of MSTs in both panels of Figure 5 is different. In the more recent Interval 2 (Figure 5(b)) the USD node has smaller centrality than in the earlier Interval 1 (Figure 5(a)); its degree dropped from to . In addition, the tree in Figure 5(b) has more extended branches than its counterpart in Figure 5(a). However, neither of the trees lacks the overall hierarchical structure, which seems to be a stable property of the network under study.

Figure 9 shows cumulative distributions of the node degrees for two different network representations and for the same two intervals of time. A difference of the MST structures can be seen for both Bs. For Interval 1 the cumulative distribution has fatter tails while for Interval 2 the c.d.f. decreases more quickly and develops thinner tails. It is debatable whether we observe any scaling behaviour of the tails, but, nevertheless, in order to describe the different shapes of the distributions we calculate the optimal scaling exponents. For Interval 1 we obtain and , while the analogous numbers for Interval 2 are equal to 1.54 and 1.59, respectively. In both representations there is a clear increase of the scaling exponent’s value.

Quantitative characterization of the changes in the MST network structure with time can also be possible by observing the temporal variability of the largest eigenvalue for different choices of B. We divide our 9.5-years-long time interval into shorter annual periods of approximately 250 trading days (with an exception for the last period of 2008, which is only 6 months long) and calculate the correlation matrices and their eigenspectra for each period and for each base currency. Results are shown in Figure 10. While the upper edge of the eigenvalue ladders remains almost unchanged over time with for one or more base currencies approaching 60, their lower ends reveal a systematic tendency to increase from in 1999 to in 2008. This means that from the perspective of USD, occupying one of the lowermost rungs of the ladder, the global market is nowadays more collective than it used to be 7-9 years ago. This, in turn, means that the set of currencies which previously were tightly related to the US dollar, now seems to be less populated. Interestingly, although USD permanently remains at the bottom of the ladder, sometimes it loses its extreme position to the advantage of other currencies like HKD or SGD. However, even then USD remains the currency with the lowest among all the major ones from Basket 1.

Since during the analyzed period both and significantly changed their values indicating a lack of stability of the network in different representations (Figure 10), it is worthwhile to inspect the behaviour of the largest eigenvalue for these and other base currencies with a better temporal resolution. We improved it by applying a moving window of length of about 6 months (126 trading days) which was shifted by 1 month (21 trading days).

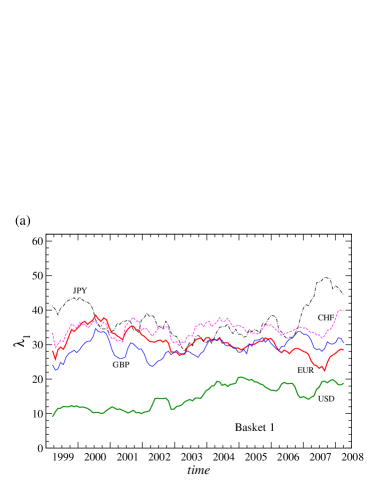

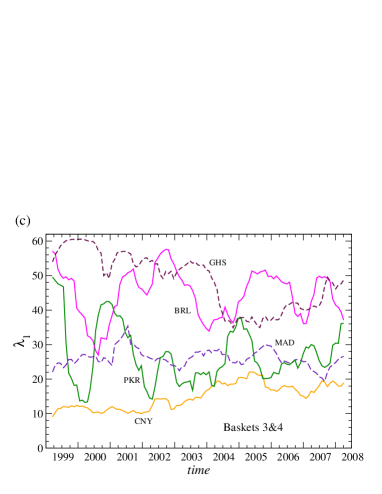

The corresponding behaviour of for 15 exemplary currencies representing different baskets is presented in three panels of Figure 11. The most interesting observation is that a distance gradually decreases (Figure 11(a)). This effect is caused predominantly by a systematically decreasing value of , which from a magnitude of 38 in 2000 reached a level of 23 at the end of 2007. At the same time , after a significant increase between 2002 and 2004, presently oscillates without any systematic trend between 14 and 20. On the other hand, the two other European major currencies: CHF and GBP, while sometimes closely mimicking the transient short-term behaviour of , do not follow its long term evolution. JPY is a rather different case: after a decreasing trend of between 1999 and 2003 and after a period of stabilization in 2004-2006, JPY now displays strong oscillations which elevated its largest eigenvalue to a level typical for less influential currencies (Baskets 2-4) that are decoupled from the global market. Figures 11(b)-(c) show for a few liquid and illiquid currencies from Baskets 2, 3 and 4. A characteristic property of this group of currencies is strong short-term variability of the largest eigenvalue which can be seen for almost all choices of B except SGD and CNY.

3 Summary

We presented outcomes of a study of the FX network structure based on daily data collected for the interval 01/1999-06/2008. These outcomes allow us to draw the following principal conclusions:

(i) The currency network structure depends on a choice of base currency and the associated reference frame. On one hand, a network based on a currency which is decoupled from the rest of the currencies and display an independent behaviour shows a highly correlated, rigid structure. On the other hand, a network viewed from the USD perspective (or the perspectives of its satellites) has a richer structure with less correlations and more noise. For typical currencies the networks has intermediate structure that can be classified between these two extremes. However, for a vast majority of currencies, the MST graphs share the same topology quantified in terms of the node degree distribution. We found that these networks show a signature of scale free networks. An extreme opposite case are the USD-based, CNY-based and HKD-based networks which have topology deviating from scale-free in direction of a random network.

(ii) From a perspective of a typical currency, the FX network is dominated by two strong clusters of nodes related to USD and to EUR. The former comprises usually the Latin American and the South-East Asian currencies, while the latter consists of the European and the Maghreb ones. There are also other smaller groups of nodes forming clusters related to geographical or economical factors, but normally they are masked by the dominating two clusters and can be seen in full detail only after removing the USD and EUR nodes from the network. Among those secondary clusters we distinguish the cluster of Middle East currencies, the cluster of Canadian, Australian and New Zealand dollars (sometimes accompanied by the South African rand, which couples currencies involved in trade of various commodities), the cluster of Central European currencies, and the cluster of precious metals. Weaker links couple also the Scandinavian currencies, the Latin American currencies, and the South-East Asian currencies.

(iii) We found that the FX network is not stable in time. Over a few past years the currency network underwent a significant change of its structure with the main activity observed in the neighbourhood of USD and EUR. The USD-related cluster released its ties, allowing some nodes to acquire more independence. At the same time the USD-based network becomes more correlated, what is a different manifestation of the same phenomenon. On the other hand, the EUR node now attracts more nodes than before and, complimentarily, the EUR-based network reveals decreasing strength of couplings. This might be a quantitative evidence that after a transient period in which the FX market actors treated the new European currency with a little of suspense, now more and more of them start to rely upon it. These findings open an interesting topic for future research.

References

- (1) Y. Aiba, N. Hatano, H. Takayasu, K. Marumo, T. Shimizu, Triangular arbitrage as an interaction among foreign exchange rates, Physica A 310, 467-479 (2002)

- (2) Sauder School of Business, Pacific Exchange Rate System, http://fx.sauder.ubc.ca/data.html (2008)

- (3) M. McDonald, O. Suleman, S. Williams, S. Howison, N.F. Johnson, Detecting a currency’s dominance or dependence using foreign exchange network trees, Phys.Rev.E 72, 046106 (2005)

- (4) V. Plerou, P. Gopikrishnan, B. Rosenow, L.A.N. Amaral, T. Guhr, H.E. Stanley, Random matrix approach to cross correlations in financial data, Phys. Rev. E 65, 066126 (2002)

- (5) A. Utsugi, K. Ino, M. Oshikawa, Random matrix theory analysis of cross correlations in financial markets, Phys. Rev. E 70, 026110 (2004)

- (6) D.-H. Kim, H. Jeong, Systematic analysis of group identification in stock markets, Phys. Rev. E 72, 046133 (2005)

- (7) T. Mizuno, H. Takayasu, M. Takayasu, Correlation networks among currencies, Physica A 364, 336-342 (2006)

- (8) M.J. Naylor, L.C. Rose, B.J.Moyle, Topology of foreign exchange markets using hierarchical structure methods, Physica A 382, 199-208 (2007)

- (9) S. Drożdż, A.Z. Górski, J. Kwapień, World currency exchange rate cross-correlations, Eur. Phys. J. B 58, 499 (2007)

- (10) P. Sieczka, J.A. Hołyst, Correlations in commodity markets, preprint arXiv:0803.3884 (2008)

- (11) A.M. Sengupta, P. Mitra, Distributions of singular values for some random matrices, Phys. Rev. E 60, 3389 (1999)

- (12) A.Z. Górski, S. Drożdż, J. Kwapień, Scale free effects in world currency exchange network, Eur. Phys. J. B (2008)

- (13) R.N. Mantegna, Hierarchical structure in financial markets, Eur. Phys. J. B 11, 193-197 (1999)

- (14) G. Bonanno, F. Lillo, R.N. Mantegna, High-frequency cross-correlation in a set of stocks, Quant. Finance 1, 96-104 (2001)

- (15) G. Bonanno, G. Caldarelli, F. Lillo, R.N. Mantegna, Topology of correlation-based minimal spanning trees in real and model markets, Phys. Rev. E 68, 046130 (2003)

- (16) G. Bonanno, G. Caldarelli, F. Lillo, C. Miccichè, N. Vandewalle, R.N. Mantegna, Networks of equities in financial markets, Eur. Phys. J. B 38, 363-371 (2004)

- (17) J.-P. Onnela, K. Kaski, J. Kertesz, Clustering and information in correlation based financial networks, Eur. Phys. J. B 38, 353-362 (2004)

- (18) M. Tumminello, C. Coronnello, F. Lillo, S. Miccichè, R.N. Mantegna, Spanning Trees and bootstrap reliability estimation in correlation based networks, Int. J. Bif. Chaos 17, 2319-2329 (2007)

- (19) R. Coelho, P. Richmond, S. Hutzler, B. Lucey, Study of the correlations between stocks of different markets, preprint arXiv:0710.5140 (2007)

- (20) E. Ravasz, A.-L. Barabási, Hierarchical organization in complex networks, Phys. Rev. E 67, 026112 (2003)

- (21) J.-D. Noh, Exact scaling properties of a hierarchical network model, Phys. Rev. E 67, 045103(R) (2003)

- (22) S. Drożdż, J. Kwapień, F. Grümmer, J. Speth, Are the contemporary financial fluctuations sooner converging to normal?, Acta Phys. Pol. B 34, 4293-4306 (2003)

- (23) S. Drożdż, M. Forczek, J. Kwapień, P. Oświȩcimka, R. Rak, Stock market return distributions: from past to present, Physica A 383, 59-64 (2007)

- (24) J. Kwapień, S. Drożdż, J. Speth, Time scales involved in market emergence, Physica A 337, 231-242 (2004)