Stochastic Optimization for Markov Modulated Networks with Application to Delay Constrained Wireless Scheduling

Abstract

We consider a wireless system with a small number of delay constrained users and a larger number of users without delay constraints. We develop a scheduling algorithm that reacts to time varying channels and maximizes throughput utility (to within a desired proximity), stabilizes all queues, and satisfies the delay constraints. The problem is solved by reducing the constrained optimization to a set of weighted stochastic shortest path problems, which act as natural generalizations of max-weight policies to Markov decision networks. We also present approximation results for the corresponding shortest path problems, and discuss the additional complexity and delay incurred as compared to systems without delay constraints. The solution technique is general and applies to other constrained stochastic decision problems.

Index Terms:

Constrained Markov Decision Processes, Queueing Systems, Dynamic SchedulingI Introduction

This paper considers delay-aware scheduling in a multi-user wireless uplink or downlink with delay-constrained users and delay-unconstrained users, each with different transmission channels. The system operates in slotted time with normalized slots . Every slot, a random number of new packets arrive from each user. Packets are queued for eventual transmission, and every slot a scheduler looks at the queue backlog and the current channel states and chooses one channel to serve. The number of packets transmitted over that channel depends on its current channel state. The goal is to stabilize all queues, satisfy average delay constraints for the delay-constrained users, and drop as few packets as possible.

Without the delay constraints, this problem is a classical opportunistic scheduling problem, and can be solved with efficient max-weight algorithms based on Lyapunov drift and Lyapunov optimization (see [1] and references therein). The delay constraints make the problem a much more complex Markov Decision Problem (MDP). While general methods for solving MDPs exist (see, for example, [2][3][4]), they typically suffer from a curse of dimensionality. Specifically, the number of queue state vectors grows exponentially in the number of queues. Thus, a general problem with many queues has an intractably large state space. This creates non-polynomial implementation complexity for offline approaches such as linear programming [2][3], and non-polynomial complexity and/or learning time for online or quasi online/offline approaches such as -learning [5][6].

We do not solve this fundamental curse of dimensionality. Rather, we avoid this difficulty by focusing on the special structure that arises in a wireless network with a relatively small number of delay-constrained users (say, ), but with an arbitrarily large number of users without delay constraints (so that can be large). This is an important scenario, particularly in cases when the number of “best effort” users in a network is much larger than the number of delay-constrained users. We develop a solution that, on each slot, requires a computation that has a complexity that depends exponentially in , but only polynomially in . Further, the resulting convergence times and delays are fully polynomial in the total number of queues . Our solution uses a concept of forced renewals that introduces a deviation from optimality that can be made arbitrarily small with a corresponding polynomial tradeoff in convergence time. Finally, we show that a simple Robbins-Monro iteration can be used to approximate the required computations when channel and traffic statistics are unknown. Our methods are general and can be applied to other MDPs for networks with similar structure.

Related prior work on delay optimality for multi-user opportunistic scheduling under special symmetric assumptions is developed in [7][8][9], and single-queue delay optimization problems are treated in [10][11][12][13] using dynamic programming and Markov Decision theory. Approximate dynamic programming algorithms are applied to multi-queue switches in [14] and shown to perform well in simulation. Optimal asymptotic energy-delay tradeoffs are developed for single queue systems in [15], and optimal energy-delay and utility-delay tradeoffs for multi-queue systems are treated in [16][17]. The algorithms of [16][17] have very low complexity and provably converge quickly even for large networks, although the tradeoff-optimal delay guarantees they achieve do not necessarily optimize the coefficient multiplier in the delay expression.

Our approach in the present paper treats the MDP problem associated with delay constraints using Lyapunov drift and Lyapunov optimization theory [1]. This theory has been used to stabilize queueing networks [7] and provide utility optimization [18][19][20][21][1] via simple max-weight principles. We extend the max-weight principles to treat networks with Markov decisions, where the network costs depend on both the control actions taken and the current state (such as the queue state) the system is in. For each cost constraint we define a virtual queue, and show that the constrained MDP can be solved using Lyapunov drift theory implemented over a variable-length frame, where “max-weight” rules are replaced with weighted stochastic shortest path problems. This is similar to the Lagrange multiplier approaches used in the related works [12][13] that treat power minimization for single-queue wireless links with an average delay constraint. The work in [12] uses stochastic approximation with a 2-timescale argument and a limiting ordinary differential equation. The work in [13] treats a single-queue MIMO system using primal-dual updates [22]. Our virtual queues are similar to the Lagrange Multiplier updates in [12][13]. However, we treat multi-queue systems, and we use a different analytical approach that emphasizes stochastic shortest paths over variable length frames. Because of this, our approach can be used in conjunction with a variety of existing techniques for solving shortest path problems (see, for example, [5]). We use a Robbins-Monro technique that is adapted to this context, together with a delayed queue analysis to uncorrelate past samples from current queue states. Our resulting algorithm has an implementation complexity that grows exponentially in the number of delay-constrained queues , but polynomially in the number of delay-unconstrained queues . Further, we obtain polynomial bounds on convergence times and delays.

II Network Model

Consider a wireless queueing network that operates in discrete time with timeslots . The network has delay-constrained queues and stability-constrained queues, for a total of queues indexed by sets and . The queues store fixed-length packets for transmission over their wireless channels. Every timeslot, new packets randomly arrive to each queue, and we let represent the random packet arrival vector. The stability-constrained queues have an infinite buffer space. The delay-constrained queues have a finite buffer space that can store packets (for some positive integer ). The network channels can vary from slot to slot, and we let be the channel state vector on slot , representing conditions that affect transmission rates. We assume the stacked vector is independent and identically distributed (i.i.d.) over slots, with possibly correlated entries on the same slot.

Every slot , the network controller observes the channel states and chooses a transmission rate vector , being a vector of non-negative integers. The choice of is constrained to a set that depends on the current . A simple example is a system with ON/OFF channels where the controller can transmit a single packet over at most one ON channel per slot, as in [7]. In this example, is a binary vector of channel states, and restricts to be a binary vector with at most one non-zero entry and with whenever . We assume that for each possible channel state vector , the set has the property that for any , the vector is also in , where is formed from by setting one or more entries to . In addition to constraining to take values in every slot , we shall soon also restrict the values for the delay-constrained queues to be at most the current number of packets in queue . This is a natural restriction, although we do not place such a restriction on the stability-constrained queues . This is a technical detail that will be important later, when we show that the effective dimension of the resulting Markov decision problem is , independent of the number of stability-constrained queues .

Let represent the vector of current queue backlogs, and define . The queue dynamics for the stability-constrained queues are:111For simplicity of exposition later, we have allowed the stability-constrained queues to serve newly arriving data. This can be modified easily by introducing a delay by one slot, so that the “new arrivals” to the stability-constrained queues actually arrived one slot ago.

| (1) |

where the operation allows, in principle, a service variable to be independent of whether or not is empty.

The delay-constrained queues have a different queue dynamic. Because of the finite buffer, we must allow packet dropping. Let be the number of dropped packets on slot . The queue dynamics for the delay-constrained queues are given by:

| (2) |

Note that this does not have any operation, because we will force the and decisions to be such that we never serve or drop packets that we do not have. The precise constraints on these decision variables is given after the introduction of a forced renewal event, defined in the next subsection.

II-A Forced Renewals

To force the delay-constrained queues to repeatedly visit a renewal state of being simultaneously empty, at the end of every slot, with probability we independently drop all unserved packets in all delay constrained queues . The stability-constrained queues do not experience such forced drops. Specifically, let be an i.i.d. Bernoulli process that is with probability every slot , and otherwise. Assume is independent of . If , we say slot experiences a forced renewal event. The decision options for and for are then additionally constrained as follows: If , then:

so that during normal operation, we can serve at most packets from queue (so new arrivals cannot be served), and we can drop only new arrivals, necessarily dropping any new arrivals that would exceed the finite buffer capacity. However, if we have:

So that is constrained as before, but is then equal to the remaining packets (if any) at the end of the slot.

We shall optimize the system under the assumption that the forced renewal process is uncontrollable. This provides an analyzable system that lends itself to simple approximations, as shown in later parts of the paper. While these forced renewals create inefficiency in the system, the rate of dropped packets due to forced renewals is at most , which assumes the worst case of dropping a full buffer plus all new arrivals every renewal event. This value can be made arbitrarily small with a small choice of . For problems such as minimizing the average drop rate subject to delay constraints in the delay-constrained queues and stability in the stability-constrained queues, it can be shown that this term bounds the gap between system optimality without forced renewals and system optimality with forced renewals. Formally, this can be shown by a simple sample path argument: A system optimized without forced renewals has a performance that is no better than a system with forced renewals, but where all “drops” from forced renewals are counted as delivered throughput, and where all other decisions mimic those of the prior system. We omit a formal argument for brevity. In Theorem 1 we show the disadvantage of using a small value of is that our average queue bounds for the stability-constrained queues is .

Define a renewal frame as the sequence of slots starting just after a renewal event and ending at the next renewal event. Assume that , so that time starts the first renewal frame. Define , and let and for represent the sequence that marks the beginning of each renewal frame. For , define as the duration of the th renewal frame. Note that are i.i.d. geometric random variables with .

II-B Markov Decision Notation

Define as the observed arrivals and channels of the network on slot , and define the random network event . Then is i.i.d. over slots. We can summarize the control decision constraints of the previous section with the following simple notation: Let be the -dimensional state space for the delay-constrained queues, and let represent the current state of these queues. Every slot , the controller observes the random event and the queue state , and makes a control action , which determines all decision variables for and for , chosen in a set that depends on and . Note that, indeed, all of our decision variables as described in the previous subsection are constrained only in terms of and , and in particular the queue states for do not constrain our decisions.

Recall that . The , , together affect the vector through a deterministic function :

| (3) |

Further, , , together define the transition probabilities from to , defined for all states and in :

| (4) |

From the equation (2) we find that , so that next states are deterministic given , , . Finally, we define a general penalty vector , for some integer , where penalties are deterministic functions of , , :

| (5) |

For example, penalty can be defined as the total number of dropped packets on slot by defining , which is indeed a function of , , .

We assume throughout that all of the above deterministic functions are bounded, so that there is a finite constant such that for all , all , and all slots we have:

| (6) |

II-C The Optimization Problems

A control policy is a method for choosing actions over slots . We restrict to causal policies that make decisions with knowledge of the past but without knowledge of the future. Suppose a particular control policy is given. Define time averages and for and by:

Our goal is to design a control policy to solve the following stochastic optimization problem:

| Minimize: | (7) | ||||

| Subject to: | (8) | ||||

| (9) | |||||

| (10) |

That is, we desire to minimize the time average of the penalty, subject to time average constraints on the other penalties, and subject to queue stability (called strong stability) for all stability-constrained queues. The general structure (7)-(10) fits a variety of network optimization problems. For example, if we define as the sum packet drops , define , and define for all (for some positive constant ), then the problem (7)-(10) seeks to minimize the total packet drop rate, subject to an average backlog of at most in all delay-constrained queues , and subject to stability of all stability-constrained queues .

Alternatively, to enforce an average delay constraint at all queues (for some positive number ), we can define penalties:

Note that the time average of is the number , the average arrival rate of (non-dropped) packets to queue . Hence, the constraint is equivalent to:

However, by Little’s theorem [23] we have , where is the average delay for queue , and so the constraint ensures (assuming ).

In the following, we develop a dynamic algorithm that can come arbitrarily close to solving the problem (7)-(10). Our solution is general and applies to any other discrete time Markov decision problem on a general finite state space , random events (for forced renewal process ), control actions in a general set , queue equations (1) with given in the form (3), transition probabilities in the form (4), and penalties in the form (5).

II-D Slackness Assumptions

Suppose the problem (7)-(10) is feasible, so that there exists a policy that satisfies the constraints. It can be shown that the constraint implies that [24], and so the following modified problem is feasible whenever the original one is:

| Minimize: | (11) | ||||

| Subject to: | (12) | ||||

| (13) | |||||

| (14) |

Define as the infimum of for the problem (11)-(14), necessarily being less than or equal to the corresponding infimum of the original problem (7)-(10).222Recall that is defined assuming forced renewals of probability . Thus, is within a gap of of the minimum cost without such forced renewals. We show in Theorem 1 that, under a suitable slackness condition, the value of can be approached arbitrarily closely while maintaining for all queues . Thus, under that slackness condition, is also the infimum of for the original problem (7)-(10).

The problem (11)-(14) is a constrained Markov decision problem (MDP) with state . Under mild assumptions (such as this state space being finite, and the action space being finite for each ) the MDP has an optimal stationary policy that chooses actions every slot as a stationary and possibly randomized function of the state only. We call such policies -only policies. Because this system experiences regular renewals, the performance of any -only policy can be characterized by ratios of expectations over one renewal frame. Thus, we make the following assumption.

Assumption 1: There is an -only policy that satisfies the following over any renewal frame:

| (15) | |||||

| (16) | |||||

| (17) |

where is the size of the renewal frame, with , and , are values under the policy on slot of the renewal frame.

We emphasize that Assumption 1 is mild and holds whenever the problem (11)-(14) is feasible and has an optimal stationary policy (i.e., an optimal -only policy). We now make the following stronger assumption that there exists an -only policy that can meet the constraints (16)-(17) with “-slackness,” without caring what average value of this policy generates. This assumption is related to standard “Slater-type” assumptions in optimization theory [22].

Assumption 2: There is a value and an -only policy (typically different from policy in Assumption 1) that satisfies the following over any renewal frame:

| (18) | |||||

| (19) |

We show in Theorem 1 that systems that satisfy Assumption 2 with larger values of can operate with smaller average queue sizes in the stability-constrained queues.

III The Dynamic Control Algorithm

To solve the problem (7)-(10), we extend the framework of [1] to a case of variable length frames. Specifically, for each of the penalty constraints , we define a virtual queue that is initialized to zero and that has dynamic update equation:

| (20) |

where is the th penalty incurred on slot by a particular action . The intuition is that if the virtual queue is stable, then the time average of must be non-positive. This turns the time average constraint into a simple queue stability problem.

III-A Lyapunov Drift

Define as a vector of all virtual queues for . Define as the combined vector of all virtual queues and all stability-constrained queues:

Assume all queues are initially empty, so that . Define the following quadratic function:

Let be the start of a renewal frame, with duration . Define the frame-based conditional Lyapunov drift as follows:

| (21) |

Note that is a function of the initial state and the policy implemented during the frame, where expectations are with respect to the random events that can take place and the possibly random control actions made. The explicit conditioning on in (21) will be suppressed in the remainder of this paper, as this conditioning is implied given that starts a renewal frame.

It is important to note the following subtlety: The implemented policy may not be stationary and/or may depend on the queue values (which can be different on each renewal interval), and so actual system events are not necessarily i.i.d. over different renewal frames. However, these frames are useful because we will analytically compare the Lyapunov drift of the actual implemented policy over a frame to the corresponding drifts of the -only policies of Assumptions 1 and 2.

Lemma 1

(Lyapunov Drift) Under any network control policy that chooses for all slots during a renewal frame , and for any initial queue values , we have:

| (22) |

where is defined:

| (23) | |||||

and where is a finite constant defined:

where we recall is the bound in (6).

Proof:

For any and any we have by squaring (20):

where the final inequality holds because the change in on any slot is at most , as is the magnitude of . Summing the above over and dividing by yields:

where (III-A) uses the identity:

Similarly, it can be shown for any :

| (26) | |||||

Summing (LABEL:eq:driftlem1) and (26) over , , taking conditional expectations, and noting that the second moment of a geometric random variable with success probability is given by proves the result. ∎

III-B The Frame-Based Drift-Plus-Penalty Algorithm

Let be a non-negative parameter that we use to affect proximity to the optimal solution. Our dynamic algorithm initializes all virtual and actual queue states to 0, and designates as the start of the first renewal frame. Then:

-

•

For each frame , observe the vector of virtual and actual queues and implement a policy over the course of the frame to minimize the following “drift-plus-penalty” expression:

(27) - •

The decision rule (27) generalizes the drift-plus-penalty rule in [1][25] to a variable frame system. The problem of designing a policy to minimize (27) is a weighted stochastic shortest path problem, where weights are virtual and actual queue backlogs at the start of the frame. Finding such a policy is non-trivial, and often can only be done in an approximate context. In the next sub-section, we present the performance of the algorithm, under the assumption that we have an algorithm to approximate (27). In Section IV we consider various such approximation methods.

III-C Performance Theorem

For constants , , define a -approximation of (27) to be a policy for choosing over a frame (consisting of slots ) that yields a total drift-plus-penalty that is less than or equal to that of any other policy, plus an error term parameterized by and :

| (28) |

where and represent (23) and (5), respectively, under any alternative algorithm that can be implemented during the slots of the frame. Note that an exact minimization of the stochastic shortest path problem (27) is a -approximation for .

Theorem 1

Suppose Assumptions 1 and 2 hold for a given . Fix , , , and suppose we use a -approximation every frame. If , then all virtual and actual queues are strongly stable, and so all desired constraints (8)-(10) are satisfied. In particular, for all positive integers , the average queue sizes satisfy:

| (29) |

Further, the time average penalty satisfies:

| (30) |

Suppose our implementation of the stochastic shortest path problem every frame is accurate enough to ensure . Then from (30) and (29), the time average of can be made arbitrarily close to (or below) as is increased, with a tradeoff in average queue size that is linear in . The dependence on the parameter is also apparent: While we desire to be small to minimize the disruptions due to forced renewals, a small value of implies a larger value of in (30) and (29). Note also that the average size of each stability-constrained queue affects its average delay, and the average size of each virtual queue affects the convergence time required for its constraint to be closely met.

III-D Proof of Theorem 1

Proof:

(Theorem 1 part 1—Queue Bounds) Let be the start of a renewal time. From (28) and (22) we have:

| (31) |

where and are for any alternative policy . Using the fact that for all , and , we have:

| (32) |

Now consider the -only policy from Assumption 2, which makes decisions independent of to yield (using the definition of in (23)):

Substituting the above into the right-hand-side of (32) gives:

| (33) |

Taking expectations of the above and using the definition of gives:

Summing the above over (for some positive integer ), dividing by , and using the fact that gives:

Rearranging terms and using and proves (29). While (29) samples only at the start of renewal frames, it can easily be used to show all queues are strongly stable (recall that the maximum queue change over any slot is bounded, and frame sizes are geometrically distributed with average ). Hence, by stability theory in [24] we know all desired inequality constraints are met. ∎

Proof:

(Theorem 1 part 2 — Performance Bound) Define probability . This is a valid probability because by assumption. We consider a new policy implemented over the frame . The policy is a randomized mixture of the -only policies from Assumptions 1 and 2: At the start of the frame, independently flip a biased coin with probabilities and , and carry out one of the two following policies for the full duration of the renewal interval:

- •

- •

Note that this policy is independent of . With , from (15) we have:

| (34) |

We also have from (16)-(17) and (18)-(19):

| (35) |

Plugging (34)-(35) into (31) yields:

Taking expectations gives:

Summing over and dividing by gives the following for all :

Using shows the right-hand-side of the above inequality is the same as the right-hand-side of the desired inequality (30). Finally, because for all , and are i.i.d. geometric random variables with mean , it can be shown that (see Appendix A):

∎

IV Approximating the Stochastic Shortest Path Problem

Consider now the stochastic shortest path problem (27). Here we describe several approximation options. For simplicity, assume the state space is finite, and the action space is finite for all . Without loss of generality, assume we start at time and have (possibly non-zero) backlogs . Let be the renewal interval size. For every step , define as the incurred cost assuming that the queue state at the beginning of the renewal is :

| (36) | |||||

Let denote the optimal control action on slot for solving the stochastic shortest path problem, given that the controller first observes and . Define , where we have added a new state “” to represent the renewal state, which is the termination state of the stochastic shortest path problem. Appropriately adjust the transition probabilities to account for this new state [26][5]. Define as a vector of optimal costs, where is the minimum expected sum cost to the renewal state given that we start in state , and . By basic dynamic programming theory [26][5], the optimal control action on each slot (given and ) is:

| (37) |

This policy is easily implemented provided that the values are known. It is well known that the vector satisfies the following vector dynamic programming equation:333One can also derive (38) by defining a value function , writing the Bellman equation in terms of , taking an expectation with respect to the i.i.d. , , and defining .

| (38) |

where we have used an entry-wise min (possibly with different actions being used for minimizing each entry ). Further, is defined as a vector with entries , and is the matrix of transition probabilities for and control action . The expectation in (38) is over the distribution of the i.i.d. process . Because has the structure , where is the random outcome for slot and is an independent Bernoulli process that has forced renewals with probability , we can re-write the above vector equation as:

| (39) |

where:

We assume the transition probabilities are known (recall that these are indeed known binary values as described in the model of Section II-B). We next show how to compute an approximation of based on random samples of and using a classic Robbins-Monro iteration.

IV-A Estimation Through Random i.i.d. Samples

Suppose we have an infinite sequence of random variables arranged in batches with batch size , with denoting the th sample of batch . All random variables are i.i.d. with probability distribution the same as , and all are independent of the queue state that is used for this stochastic shortest path problem. Consider the following two mappings and from a vector to another vector, where the second is implemented with respect to a particular batch :

| (40) | |||

| (41) |

where the min is entrywise over each vector entry. The expectation in (40) is implicitly conditioned on a given vector, and is with respect to the random , which is independent of . We note that both and are vectors with size determined by the size of the state space . For a system with delay-constrained queues, the size of is exponential in . Thus, any computation of the map or must update a number of entries that is exponential in . This is why we desire to be small, even though the number of stability-constrained queues can be large.

The mapping cannot be implemented without knowledge of the distribution of (so that the expectation can be computed), whereas the mapping can be implemented as a “simulation” over the random samples (assuming such samples can be generated or obtained). However, the expected value of is exactly equal to . Thus, given an initial vector for use in step , we can write , where is a zero-mean vector random variable. Specifically, the vector satisfies:

Thus, while the vector is not independent of , each entry is uncorrelated with any deterministic function of . That is, for each entry and any deterministic function we have via iterated expectations:

| (42) |

For we have the iteration:

| (43) |

This iteration is a classic Robbins-Monro stochastic approximation algorithm. It can be shown that the vector remains deterministically bounded for all (see Appendix B), and that and satisfy the requirements of Proposition 4.6 in Section 4.3.4 of [5]. Thus the above iteration is in the standard form for stochastic approximation theory, and ensures that:

where is the cost vector associated with the optimal stochastic shortest path problem, that is, it is the solution to (39) and thus satisfies . This holds for any batch size (including the simplest case ), although taking larger batches reduces the variance of the per-batch estimation and may improve overall convergence speed.

Unfortunately, the above does not specify how many iterations are needed to yield a close approximation to the value. The intuition is that we can run the iterations for a “large enough” time, and hope that we have obtained a close enough approximation to yield and values that can be used in Theorem 1. 444We note that an earlier version of this technical report attempted to overcome this challenge by analyzing error bounds for the following alternative recursion: While this can be shown to be a contraction under the norm , our results erroneously claimed (in Lemma 7 of the old technical report) that it was a contraction under the norm , where is treated as a random variable (the two norms are identical if is treated as a constant). The error was in: (i) erroneously passing expectations through max[] in a step that was skipped, and (ii) using a result that (which is correct for a fixed transition probability matrix ), where one actually would need , where can be a function of , and this latter inequality does not necessarily hold.

IV-B Recursive Methods for

Contraction results for general stochastic shortest path problems are given in [5]. The following is a related result with a simpler form that holds because of our forced renewal structure. For a given vector , define as the maximum absolute value of :

It is not difficult to show that for any vector and any probability matrix with rows that sum to 1, and with a number of columns equal to the size of , we have .

Lemma 2

For any vectors , of the same size as , we have:

Proof:

Note that for all and all we have:

Define vector by:

Therefore:

By switching the roles of and it can similarly be shown:

The result follows. ∎

This simple result yields the following approximation bounds for iterations of the map . Define as an initial guess of , and for define .

Lemma 3

For any initial vector and any we have:

Proof:

Recall that and . Then:

The result then follows easily by recursion. ∎

Because the renewal frame size is independent of the policy, and has average , it is not difficult to show that , where is the largest possible magnitude of of for slot in the frame (such a constant exists and is finite because of the boundedness assumptions). Therefore, defining and using Lemma 3 yields:

By the definition of in (36), it can be shown that is a sum of terms that are proportional to , , and . Further, in Appendix C it is shown that the deviation in the optimal cost when (37) is used with an approximate value , rather than , deviates from by at most:

Hence, the above two bounds can be used to compute a value that provides explicit approximation values for and for use in Theorem 1.

IV-C Recursive Methods for

The difficulty in iterating the map is that it requires full knowledge of the underlying probability distributions to compute the associated expectations. An approximation of this is to use from (41). Specifically, assume we have i.i.d. samples . Then the function is:

Define as any initial vector, and for define . Using the same proof technique as Lemmas 2 and 3, it is easy to show that for any , is also a contraction that satisfies for any and :

Thus, it has a unique fixed point satisfying , and for all we have:

The value is typically not the same as . It represents the optimal cost vector in a modified system where the vector is i.i.d. with the same distribution as the empirical average given over the samples. Intuitively, becomes a better approximation for when the number of samples is large.

IV-D Sampling From the Past and Delayed Queue Analysis

It remains to be seen how one can obtain the required i.i.d. samples without knowing the probability distribution for . In this subsection, we describe a technique that uses previous samples of the values.

We first obtain a collection of i.i.d. samples of . Consider a given renewal time , and suppose that the time is large enough so that we can obtain samples according to the following procedure: Let , , . Because is i.i.d. over slots (and because our renewal times are chosen randomly and independently), it is easy to see that form an i.i.d. sequence.

A subtlety now arises: Even though the sequence is i.i.d., these samples are not independent of the queue backlog at the beginning of the renewal. This is because these values have influenced the queue states. This makes it challenging to directly implement a Robbins-Monro iteration. Indeed, the expectation in (40) can be viewed as a conditional expectation given a certain queue backlog at the beginning of the renewal interval, which is for the th renewal. This conditioning does not affect (40) when is chosen independently of initial queue backlog, and so the random samples in (41) are also assumed to be chosen independent of the initial queue backlog, which is not the case if we sample from the past.

To avoid this difficulty and ensure the samples are both i.i.d. and independent of the queue states that form the weights in our stochastic shortest path problem, we use a delayed queue analysis as in [27]. Let denote the slot on which sample is taken, and let represent the queue backlogs at that time. It follows that the i.i.d. samples are also independent of . Hence, the bounds derived for the iteration technique in the previous section can be applied when the iterates use as the backlog vector. Let denote the optimal solution to the problem (38) for a queue backlog at the beginning of our renewal time , and let denote the corresponding optimal solution for a problem that starts with initial queue backlog . Then there are slots in between and . Because the maximum change in any queue on one slot is bounded by , we want to claim that an algorithm which computes the stochastic shortest path using the queue values gives a result that is within an additive constant of the algorithm which uses . Such an additive constant can be viewed as the constant in Theorem 1. This can be justified using the next lemma, which bounds the deviation of the optimal costs associated with two general queue backlog vectors.

Let and be two different queue backlog vectors, and let and represent the optimal frame costs corresponding to and , respectively. Define the constant as follows:

| (44) |

where is the vector, indexed by , with the th entry given by (36) using backlog vector . Note from (36) that is independent of (as the term in (36) cancels out in the subtraction), and is proportional to the maximum penalty value times the maximum difference in any queue backlog entry in and its corresponding entry in . Thus is also independent of the actual size of the backlog vectors, and depends only on their difference, being proportional to .

Lemma 4

For the vectors and , and for the value defined in (44), we have:

(a) The difference between and satisfies:

(b) Let denote the policy decisions at time under the policy that makes optimal decisions subject to queue backlogs , and define as the expected sum cost over a frame of a mismatched policy that incurs costs according to backlog vector but makes decisions according to (and hence has the same decisions as the optimal policy for ). Then:

where is a vector of all values with the same dimension as .

Proof:

Omitted for brevity (see Appendix D). ∎

V Simulation

In this section, we simulate the frame-based drift-plus-penalty algorithm in Section III-B for the simple network in Fig. 1. The algorithm utilizes the classic Robbins-Monro iteration, based on samples from the past, to approximate the weighted stochastic shortest path problem (39). This is because solving (39) exactly is computationally expensive, would require full probability knowledge, and may not be practical for implementation.

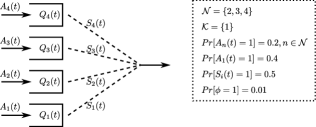

The network in Fig. 1 consists of one delay-constrained queue and three stability-constrained queues, so that and . The size of the delay-constrained queue is limited to packets. Random packet arrivals are i.i.d. Bernoulli processes with for and . Each network channel is a binary state and is active (ON-state) with probability for . The force renewal probability is .

In this simulation, we consider a problem of minimizing the average number of dropped packets. For the delay-constrained queue , the average backlog is limited to 1.5. Define and . Then an optimization for this simulation is

| minimize | ||||

| subject to | ||||

The simulation follows the frame-based drift-plus-penalty algorithm in Section III-B with the Robbins-Monro iteration (43). A batch size is set to be , so that we store the most recent samples (using less than 50 in the initial slots ). Note that the number of samples is half of the average frame size, . Every forced renewal slot , the algorithm uses the batch to approximate the mapping in (41), and then updates according to (43). After updating , every decision in frame is decided from the simple rule (37). Then all delay-constrained, stability-constrained, and virtual queues are updated as in (1), (2), and (20).

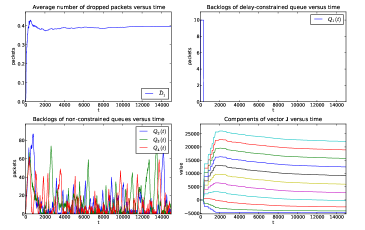

For a simple initial comparison, we use , so the algorithm puts no weight on minimizing and only attempts to satisfy the desired constraints. Results from the algorithm until slots are shown in Fig. 2. The system drops almost all packets in the delay-constrained queue (as expected), making its average queue size approach zero, as shown in the top graphs of Fig. 2. All stability-constrained queues are stable, which is shown in the bottom-right of Fig. 2. The bottom-left of Fig. 2 shows the convergence of . This illustrates that the algorithm yields a feasible solution.

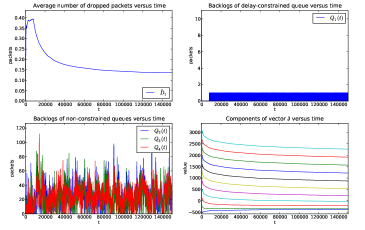

We next use , so the algorithm attempts to minimize dropping in queue 1. Behaviors in the system for the first slots are shown in Fig. 3. The figure shows the convergence of the algorithm. After slots, the average number of dropped packets is and the average backlog of the delay-constrained queue is . These values correspond to the data points plotted for in Figs. 4 and 5. Compared to the result from , the average number of dropped packets decreases, while the backlog increases as a result of more aggressive admission. In addition, the algorithm with takes more time slots to converge.

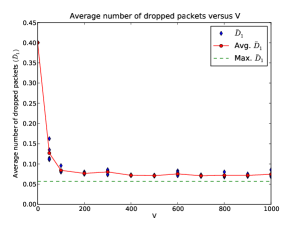

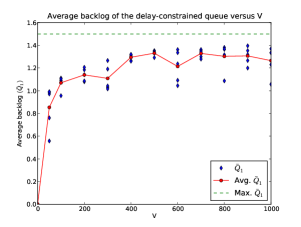

Finally, the system is simulated for in the range from to , as shown in Figs. 4 and 5. Each value of is simulated over 5 independent runs. As is increased, we expect the average drop rate to converge to optimality, with a corresponding increase in average queue sizes for the stability-constrained queues. This is exactly what happens. After slots, the average number of dropped packets and the average number of backlogs are recorded. Then the average of the five values for each is calculated. Also, the nearest optimal solution (when ) that we obtained is represented by dashed lines in both figures. In this case, the average number of dropped packets is , and the average number of backlog is . Note that in this case, the average queue size constraint is met with near equality, which is why the number of dropped packets can be pushed down so far. Fig. 4 illustrates the performance of the algorithm as varies.

VI Conclusions

We have developed an approach to the Markov Decision problems associated with a small number of delay-constrained wireless users and a (possibly large) number of stability-constrained queues. Our formulation allows optimization of general penalty functions subject to general penalty constraints, such as minimizing average packet drops subject to average backlog and/or average delay constraints at the delay-constrained queues, and subject to stability at the stability-constrained queues. Our approach uses a reduction to an online (unconstrained) weighted stochastic shortest path problem implemented over variable length frames. This generalizes the class of max-weight network control policies to networks with Markov decisions. The solution to the underlying stochastic shortest path problem has complexity that is exponential in the number of delay-constrained queues , but polynomial in the number of delay-unconstrained queues . A Robbins-Monro approximation technique was used to develop several approximation algorithms for the stochastic shortest path problem. The solution technique is general and extends to other network problems with stochastic decisions.

Appendix A

Here we show that if are i.i.d. geometric random variables with mean , and if for all (for some positive constant ), then:

| (45) |

This is used at the end of the proof of Theorem 1.

We have by the Law of Large Numbers:

First consider the case when with probability 1 for all , so that for all . Let be the number of renewal events that have occurred up to time (not counting the renewal at time ). Then with probability . Fix a value such that . Define the following event :

Define as the opposite event. Then as . If is true, then and so:

where we recall that is the time of the th renewal event. Now for any time we have:

where the final inequality holds because we have added the non-negative term:

Therefore:

Taking limits yields:

The above holds for all such that . Taking a limit as yields:

The reverse inequality can be proven similarly. This establishes (45) for the case when is a non-negative process.

For the case , but can take possibly negative values, we can define . Then we have for all . It follows that:

Subtracting from both sides of the above equality yields the result of (45).

Appendix B

Here we show that if we use iteration (43) starting with any initial vector , then the norms of all iterates are bounded, where we use the max-absolute value norm:

Consider the iteration:

where:

where is the map of (40), and is a sequence of zero mean vector random variables, where each entry of is uncorrelated with any deterministic function of . We show that and are deterministically bounded. Define as the maximum absolute value of any term of the or functions, under any . This maximum is finite by the boundedness assumptions. Define . We claim that if If , then:

Appendix C

We now show that an implementation that chooses over a frame according to (37), using the estimate instead of the optimal vector, results in an approximation to the stochastic shortest path problem that deviates by an amount that depends on .

Claim: Suppose we choose according to (37) over the course of a frame, using a vector rather than . Let represent the expected sum cost over the frame (given ). Then:

| (46) |

Proof:

Let represent the control decision on slot made using the vector, and let represent the decision that would be made under the vector. Then:

where the expectation is with respect to the random outcome. Thus:

| (47) |

Appendix D

Here we prove Lemma 4 of Section IV-D, restated below for convenience: For the vectors and , and for the value defined in (44), we have:

(a) The difference between and satisfies:

(b) Let denote the policy decisions at time under the policy that makes optimal decisions subject to queue backlogs , and define as the expected sum cost over a frame of a mismatched policy that incurs costs according to backlog vector but makes decisions according to (and hence has the same decisions as the optimal policy for ). Then:

where is a vector of all values with the same dimension as .

Proof:

By definition, we have (as is the minimum sum cost over any policy when penalties are incurred according to queue backlog). Consider any entry , and suppose we start in initial state .555Note that while all frames start with , and hence have optimal cost , is defined with entries indexed by general initial states . Then:

where the final inequality is due to the fact that the mean renewal time is , and from the fact that the value in (44) bounds the difference in the and components. This proves part (b).

To prove part (a), note that part (b) implies:

However, switching the roles of and , we can similarly derive . This proves part (a). ∎

References

- [1] L. Georgiadis, M. J. Neely, and L. Tassiulas. Resource allocation and cross-layer control in wireless networks. Foundations and Trends in Networking, vol. 1, no. 1, pp. 1-149, 2006.

- [2] S. Ross. Introduction to Probability Models. Academic Press, 8th edition, Dec. 2002.

- [3] E. Altman. Constrained Markov Decision Processes. Boca Raton, FL, Chapman and Hall/CRC Press, 1999.

- [4] S. Meyn. Control Techniques for Complex Networks. Cambridge University Press, 2008.

- [5] D. P. Bertsekas and J. N. Tsitsiklis. Neuro-Dynamic Programming. Athena Scientific, Belmont, Mass, 1996.

- [6] J. Abounadi, D. Bertsekas, and V. S. Borkar. Learning algorithms for markov decision processes with average cost. SIAM Journal on Control and Optimization, vol. 20, pp. 681-698, 2001.

- [7] L. Tassiulas and A. Ephremides. Dynamic server allocation to parallel queues with randomly varying connectivity. IEEE Transactions on Information Theory, vol. 39, no. 2, pp. 466-478, March 1993.

- [8] E. M. Yeh. Multiaccess and Fading in Communication Networks. PhD thesis, Massachusetts Institute of Technology, Laboratory for Information and Decision Systems (LIDS), 2001.

- [9] A. Ganti, E. Modiano, and J. N. Tsitsiklis. Optimal transmission scheduling in symmetric communication models with intermittent connectivity. IEEE Transactions on Information Theory, vol. 53, no. 3, pp. 998-1008, March 2007.

- [10] A. Fu, E. Modiano, and J. Tsitsiklis. Optimal energy allocation for delay-constrained data transmission over a time-varying channel. Proc. IEEE INFOCOM, 2003.

- [11] M. Goyal, A. Kumar, and V. Sharma. Power constrained and delay optimal policies for scheduling transmission over a fading channel. Proc. IEEE INFOCOM, April 2003.

- [12] N. Salodkar, A. Bhorkar, A. Karandikar, and V. S. Borkar. An on-line learning algorithm for energy efficient delay constrained scheduling over a fading channel. IEEE Journal on Selected Areas in Communications, vol. 26, no. 4, pp. 732-742, May 2008.

- [13] D. V. Djonin and V. Krishnamurthy. -learning algorithms for constrained markov decision processes with randomized monotone policies: Application to mimo transmission control. IEEE Transactions on Signal Processing, vol. 55, no. 5, pp. 2170-2181, May 2007.

- [14] C. C. Moallemi, S. Kumar, and B. Van Roy. Approximate and data-driven dynamic programming for queuing networks. Submitted for publication, 2008.

- [15] R. Berry and R. Gallager. Communication over fading channels with delay constraints. IEEE Transactions on Information Theory, vol. 48, no. 5, pp. 1135-1149, May 2002.

- [16] M. J. Neely. Optimal energy and delay tradeoffs for multi-user wireless downlinks. IEEE Transactions on Information Theory, vol. 53, no. 9, pp. 3095-3113, Sept. 2007.

- [17] M. J. Neely. Super-fast delay tradeoffs for utility optimal fair scheduling in wireless networks. IEEE Journal on Selected Areas in Communications, Special Issue on Nonlinear Optimization of Communication Systems, vol. 24, no. 8, pp. 1489-1501, Aug. 2006.

- [18] M. J. Neely. Dynamic Power Allocation and Routing for Satellite and Wireless Networks with Time Varying Channels. PhD thesis, Massachusetts Institute of Technology, LIDS, 2003.

- [19] A. Stolyar. Maximizing queueing network utility subject to stability: Greedy primal-dual algorithm. Queueing Systems, vol. 50, no. 4, pp. 401-457, 2005.

- [20] A. Eryilmaz and R. Srikant. Fair resource allocation in wireless networks using queue-length-based scheduling and congestion control. IEEE/ACM Transactions on Networking, vol. 15, no. 6, pp. 1333-1344, Dec. 2007.

- [21] A. Eryilmaz and R. Srikant. Joint congestion control, routing, and mac for stability and fairness in wireless networks. IEEE Journal on Selected Areas in Communications, August 2006.

- [22] D. P. Bertsekas. Nonlinear Programming. Athena Scientific, Belmont, MA, 1995.

- [23] D. P. Bertsekas and R. Gallager. Data Networks. New Jersey: Prentice-Hall, Inc., 1992.

- [24] M. J. Neely. Stochastic Network Optimization with Application to Communication and Queueing Systems. Morgan & Claypool, 2010.

- [25] M. J. Neely. Energy optimal control for time varying wireless networks. IEEE Transactions on Information Theory, vol. 52, no. 7, pp. 2915-2934, July 2006.

- [26] D. P. Bertsekas. Dynamic Programming and Optimal Control, vols. 1 and 2. Athena Scientific, Belmont, Mass, 1995.

- [27] M. J. Neely. Max weight learning algorithms with application to scheduling in unknown environments. arXiv:0902.0630v1, Feb. 2009.