A Prediction Market for Toxic Assets Prices††thanks: This author is an Enterprise Ireland Principal Investigator (grant number PC/2008/0367).

Abstract

We propose the development of a prediction market for forecasting prices for “toxic assets” to be transferred from Irish banks to the National Asset Management Agency (NAMA). Such a market allows market participants to assume a stake in a security whose value is tied to a future event. We propose that securities are created whose value hinges on the transfer amount paid for loans from NAMA to a bank. In essence, bets are accepted on whether the price is higher or lower than a certain quoted figure. The prices of the securities represent transfer prices for toxic assets increases or decreases in line with market opinion. Prediction markets offer a proven means of aggregating distributed knowledge pertaining to fair market values in a scalable and transparent manner. They are incentive compatible (i.e. induce truthful reporting) and robust to strategic manipulation. We propose that a prediction market is run in parallel with the pricing procedure recommended by the European Commission. This procedure need not necessarily take heed of the prediction markets view in all cases but it may offer guidance and a means of anomaly detection. An online prediction market would offer everybody an opportunity to “have their say” in an open and transparent manner.

1 Introduction

The Irish Government has recently decided to set up a National Asset Management Agency whose objective is to acquire “toxic assets” from Irish banks on a mandatory basis so that they are removed from the balance sheet of at an agreed price. These assets are impaired loans that were given to developers so they could purchase land or fund construction projects. There are four key challenges associated with this approach.

-

1.

It is necessary to determine a fair price for these assets in the absence of a liquid property market and price signals in a clear and transparent manner.

-

2.

Determining the optimal basket of toxic assets to acquire given a finite budget, estimated fair prices and a multi-criteria objective function that seeks to maximize returns to the tax-payer, minimize asset management duration and allow recapitalization of the banks on the open market.

-

3.

The problem of establishing a scalable solution that can expedite the asset transfer process. Given the large number of properties that are dispersed across Ireland and many other countries that require valuation, it is imperative that any suggested approach can be rapidly expanded to deal with the enormous volume of troubled loans.

-

4.

The pricing and optimisation mechanisms need to be transparent so that it is clear to all tax-payers that no preferential treatment is being offered to any party and the process does not suffer from political interference.

In order to address these challenges, we suggest that a prediction market be initiated so that distributed knowledge among property experts (and even non-experts) can be capitalised on in a manner that incentives truthful reporting of valuations. Invited participants in the market will be offered an opportunity to wager on the transfer prices of toxic assets. This offers a means of leveraging “the wisdom of crowds” and improving the accuracy of fair price predictions in the absence of a liquid property market. Such an automated mechanism for price prediction offer scalability and a clear incentive for NAMA to determine prices that are aligned with public/market opinion. This addresses many of the criticisms leveled at NAMA by various commentators [2, 5].

The prediction market could be operated on a public-access basis or available only to registered experts in property valuation. We assume in this work that it is open to anybody (over the age of 18) who wishes to participate. Given the ease with which scalability can be provided, it is difficult to justify any argument in favour of excluding the general public. It is more politically acceptable and also improves the accuracy and robustness of the results.

We also briefly describe an extension that could enhance this approach. It involves determining dependencies between assets and finding super- or sub-additive valuations. We briefly outline a method that seeks to optimise the value of a portfolio Section 5 concludes.

2 Key Benefits of Prediction Markets

The quest to predict the future is pervades all aspects of society. According to Bragues, “A potential solution to this epistemological conundrum has emerged through mass collaboration” [1]. Prediction markets allow participants to purchase a stake in a security whose value is tied to a future event. The fluctuating prices offer a continuously updated probability estimate of the likely outcome of the event. A key advantage of prediction markets over other approaches to information aggregation (e.g. surveys) is that they provide incentives for truthful revelation of beliefs [6]. If prediction markets are used as inputs into future decisions, this may provide a countervailing incentive to trade dishonestly to manipulate market prices. However, Hanson and Oprea demonstrated that such attempts at manipulation are destined to fail because other participants have a greater incentive to counteract such efforts [3]. An important role for prediction markets is that potential profits offer an incentive for information discovery. The aggregated finding of all such efforts at information discovery would provide a strong indication to the NAMA as to the markets expectation regarding the fair price that will be paid. Some of the other benefits are listed below.

-

1.

Responsiveness: it has been shown that prediction markets respond quickly to new information [4].

-

2.

Arbitrage opportunities tend to be fleeting thus indicating market efficiency.

-

3.

Improved accuracy: the incentive compatibility removes some of the behavioural anomalies that are witnessed in surveys. Prediction markets for events such as political elections are widely regarded as more accurate than survey techniques.

-

4.

Versatility: they can be adopted in a wide variety of settings. For example, Hewlett Packard yielded more accurate sales forecasts than the firms internal experts.

3 Implementation Considerations

We present a prototype prediction market and we invite the reader to visit https://nama.inklingmarkets.com to see how this market operates for just a single property.

3.1 Prototype

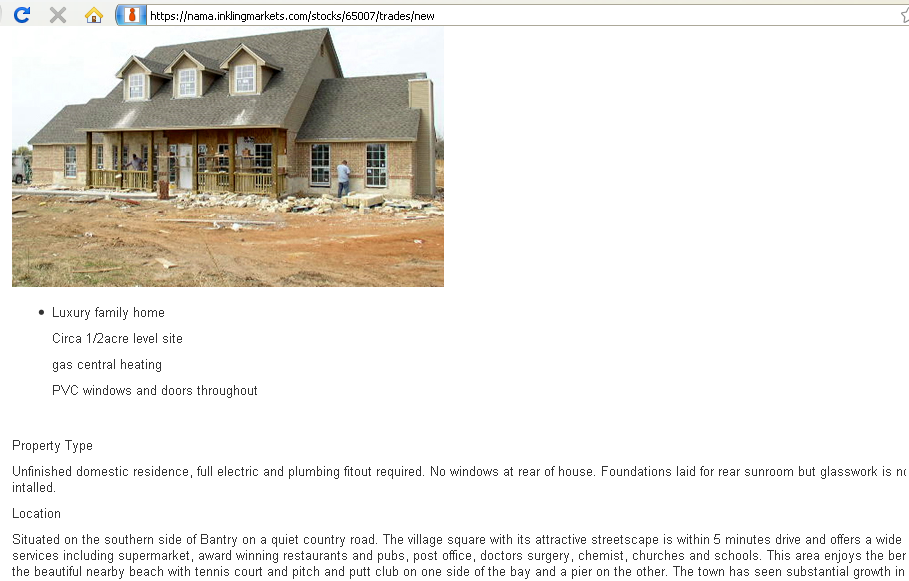

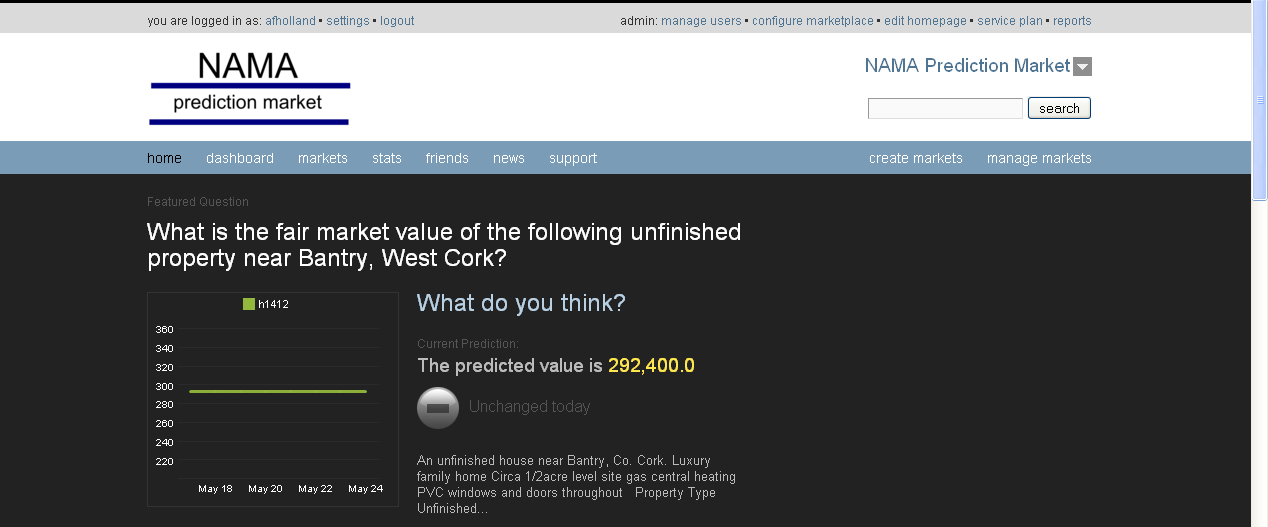

The author has prepared a prototype model of a prediction marketplace111See https://nama.inklingmarkets.com/. using a tool developed by Inkling Inc. It involves a single fictional unfinished property in Bantry, Co. Cork (Fig 1).

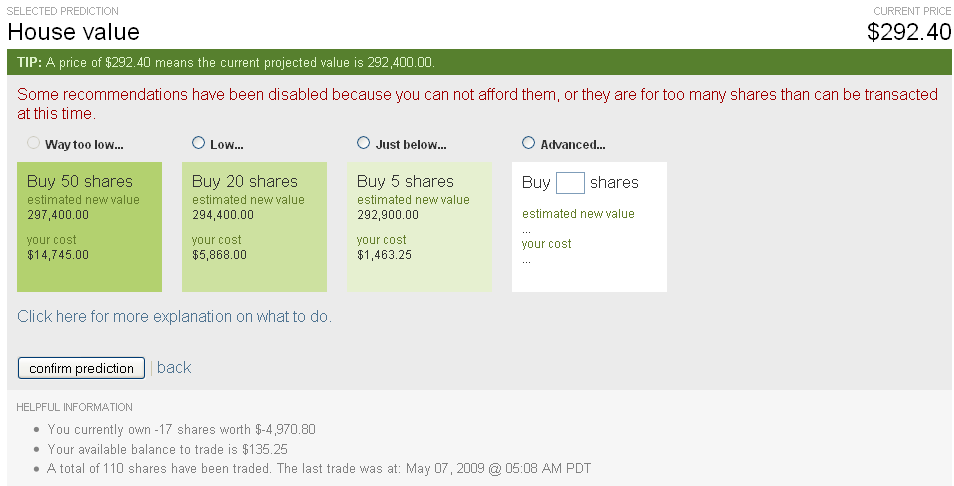

Market participants can choose whether to wager on the agreed price being higher or lower than the current threshold (Fig. 2). They can also choose how much to invest in that decision, Figures 3 and 4. We would envisage that each participant is limited in what they can wager on any single market. To encourage liquidity, it may be necessary to offer starting balances that can be topped up so that users have an incentive to engage initially and learn how the market works. From that point onwards, participants would have an incentive to enter markets pertaining to securities about which they were most knowledgeable. This would probably involve studying assets in their vicinity. In this manner, knowledge aggregation on a grand scale would be automated and trustworthy.

3.2 Software System

It is important that a software system that would host such a market is secure, scales well and provides a rich set of features. For this reason it may be preferable to utilise existing systems from experienced providers. Two obvious possibilities include the following.

- Inkling Markets:

-

Inkling provides a hosted software solution that could host such a prediction market(http://inklingmarkets.com/). Their customers include Cisco, CNN and Procter & Gamble.

- Intrade:

-

Alternatively, Intrade Ltd is one of the world’s largest prediction market makers and is based in Dublin222The author has had no contacts with either company and is not acting on their behalf. This may offer an excellent opportunity in terms of access to the necessary software engineering expertise for rapid deployment and/or customisation of a bespoke solution.

A desirable bespoke element of a tailored solution would include geographical browsing of assets that are close to a participants location. Other desiderata include a complete specification of the European Commission guidelines for estimating asset values. This would aid participants understanding of the goals of the NAMA in price determination. Of course it may be possible for the NAMA to condition it’s final value on the prediction markets view. This may serve to slow convergence to an outcome but this is a decision that should be taken in light of the liquidity of that market.

The immediate scalability depends largely upon the format and content of data regarding the underlying assets that were acquired by property developers. If all data is held in electronic form and conforms to a set of schema detailing the semantics of this information then transferal to an online database is relatively straightforward. If, however, the relevant data is unstructured or not held electronically then the data aggregation phase would be slower. Temporal aspects are also important for the correct functioning of the market. It is necessary for market participants to know a cut-off date by which it will become public knowledge how much was paid for certain assets.

The prediction market relies on open and transparent access to data so the legitimacy of information disclosure and potential privacy breaches would need further study.

4 Combinatorial Prediction Markets and Portfolio Optimisation

It is possible to set up more complex contracts that depend on the outcome of more than one event. This offers insight into the dependencies or correlation between events. For example, when valuing properties there are often super- or sub-additive valuations ascribed to collections of properties. The value may be enhanced if the assets complement one another. For example, adjacent properties may offer access to a road or other resources that increase the overall value of the combination. In the case where assets are substitutes, it may be desirable to acquire just one of them.

In order to optimise values, it is necessary to elicit information regarding dependencies. The necessary queries (i.e. combinatorial markets) will need to be decided using heuristics based on proximity or adjacency. The problem of optimising combined asset value minus the sum of the values of the individual assets can be modelled as a Mixed Integer Program. The computational problem is complex but efficient solvers exist for problems with tens of thousands of variables. Ultimately, this approach would need to be investigated but is of secondary importance compared to the valuation of stand-alone properties.

5 Conclusion

This proposal highlights the possibility of a complementary online market that offers indicative prices for toxic assets. A prediction market would improve the accuracy, speed and scalability of pricing toxic assets. It would also offer transparency and a voice to the general public who wish to have an input in this matter. There is little to lose but much to gain in adopting this approach that can run in parallel with existing pricing mechanisms in a seamless manner.

References

- [1] George Bragues. Prediction markets: The practical and normative possibilities for the social production of knowledge. Episteme, 6:91–106, Feb 2009.

- [2] Constantin Gurdgiev and Brian Lucey. What’s wrong with NAMA. http://trueeconomics.blogspot.com/2009/04/whats-wrong-with-nama.html, April 2009. Unedited version of article in Business and Finance (April 23).

- [3] Robin Hanson and Ryan Oprea. Manipulators increase information market accuracy. mimeo, George Mason University, 2005.

- [4] Erik Snowberg, Justin Wolfers, and Eric Zitzewitz. Partisan impacts on the stockmarket: Evidence from prediction markets and close elections. mimeo, University of Pennsylvania, 2006.

- [5] Karl Whelan. Panel discussion. RTE Primetime, 30 April 2009.

- [6] Justin Wolfers and Eric Zitzewitz. prediction markets. In Steven N. Durlauf and Lawrence E. Blume, editors, The New Palgrave Dictionary of Economics. Palgrave Macmillan, Basingstoke, 2008.