Characterization of Discrete Scale Invariant

Markov Sequences

Abstract

By considering special sampling of discrete scale invariant (DSI) processes we provide a sequence which is in correspondence

to multi-dimensional self-similar process.

By imposing Markov property we show that the covariance functions of such discrete scale invariant Markov (DSIM) sequences

are characterized by variance, and covariance of adjacent samples in the first scale interval.

We also provide a theoretical method for estimating spectral density matrix of corresponding multi-dimensional self-similar Markov process.

Some examples such as simple Brownian motion with drift and scale invariant autoregressive model of order one are presented and these

properties are investigated. By simulating DSIM sequences we provide visualization of their behavior and investigate these results.

Finally we present a new method to estimate Hurst parameter of DSI processes and show that it has much better performance than maximum likelihood method for simulated data.

AMS 2010 Subject Classification: 60G18, 60J05, 60G12.

Keywords: Discrete scale invariance; Wide sense Markov; Multi-dimensional self-similar.

1 Introduction

The notion of scale invariance or self-similarity is used as a fundamental property to handle and interpret many natural phenomena,

like textures in geophysics, turbulence of fluids, data of network traffic and image processing, etc [2]. The idea is that a

function is scale invariant if it is identical to any of its rescaled functions, up to some suitable renormalization of its

amplitude.

Discrete scale invariance (DSI) is a property which requires invariance by dilation for certain preferred scaling factors [14].

It is known that DSI leads to log-periodic corrections to scaling. Log-periodic oscillations have been used to predict price trends,

turbulent time series, multi-fractal measures and crashes on financial markets [16].

Burnecki et al. [5] studied -stable and self-similar processes and established the uniqueness of such process by

implementing Lamperti transform. They also present a natural construction of two distinct -stable Ornstein-uhlenbeck

processes via this transformation.

Borgnat et. al. [3] have studied the property of DSI and its relation to periodically correlated (PC) by means of the

Lamperti transformation too.

Gray and Zhang proposed geometrically sampling of non-stationary self-similar processes, and implied

it to study Euler-Cauchy processes [7]. Vidacs and Virtamo considered geometric

sequence of sampling points in order to study the scaling behavior of the fractional Brownian motion traffic with fewer

samples [15]. They considered such sampling to obtain Maximum Likelihood estimator of the Hurst parameter of such models.

Current authors [8] considered some special geometric sampling to provide a correspondence multi-dimensional discrete

time self-similar process, and provided spectral representation and spectral density function of such

processes.

Continuous time DSI process in real life usually have some scale which is not necessarily integer, so our special geometric sampling scheme is to obtain a sequence with DSI property.

Current authors [9] improved the efficiency of DSI sequence and considered some flexible sampling of a continuous time DSI process. They presented the spectral representation and spectral density of such sampled process and implied this method to determine the structure of SP500 data for some special period.

We consider a DSI process with some scale and get our samples at points , where , and

is the number of samples in each scale.

One of the advantages of such sampling is to provide a multi-dimensional self-similar process in correspondence to the geometrically sampled DSI sequence.

This provides an appropriate platform to study discrete scale

invariant processes. In this paper we study discrete scale invariant Markov (DSIM) sequences which have DSI property and are Markov in the wide sense.

We investigate the properties of such DSIM sequences and show that its covariance function is characterized by elements , where is the covariance function of th and th element of this sequence.

We also present a theoretical estimation method for the spectral density matrix of corresponding multi-dimensional self similar Markov process and present a new method for estimation of Hurst parameter of DSI processes and implement the method for simulated data.

The paper is organized as follows. In section 2, we present definitions and some preliminary properties of discrete time DSI and self-similar processes, and also Markov processes in

the wide sense.

In section 3, we present a characterization theorem for the covariance function of the DSIM sequences by applying the variance and covariance functions of the adjacent samples in the first scale interval.

By introducing discrete scale invariant autoregressive sequence of order , DSIAR(p), with time varying coefficients and discrete

time simple Brownian motion we justify this result. Using quasi Lamperti transform, we show that DSIAR(1) is the counterpart of a

periodically correlated autoregressive, PCAR(1), process and obtain covariance function of it in this section.

In section 4, we present a characterization theorem which can be used to verify whether a process has DSIM property. We

also introduce a new method for the estimation of the covariance function which can be used to simply verify such property. This method enables us to estimate spectral density matrix of corresponding -dimensional self-similar Markov process too.

In section 5, we present simulation of simple Brownian motion with different scale and Hurst parameters to visualize the behavior of

such DSIM process. We investigate the characterization of the covariance function of DSIM sequences for the simulated data to verify such DSIM property. Finally we present a new method in this section for estimating Hurst parameters for DSI process and shows its efficiency by comparing

its performance with the maximum likelihood method of corresponding multi-dimensional self-similar process for

the simulated data.

2 Theoretical framework

In this section, we review the concepts of self-similar, DSI and wide sense self-similar processes in discrete time. We also present some characterizations of Markov processes in the wide sense.

2.1 Discrete time self-similar processes

A process is said to be stationary, if for any

| (2.1) |

where is the equality of all finite-dimensional distributions. If holds for some , the process is said to be periodically correlated (PC). The smallest of such is called period of the process. Also a process is said to be self-similar of index , if for any

| (2.2) |

The process is said to be DSI of index and scaling factor if holds for .

Definition 2.1

A process is called discrete time self-similar process with parameter space , any subset of distinct points of real line, if for any

| (2.3) |

The process is called DSI sequence with scale and parameter space , if for any , holds, see [8].

Remark 2.1

If the process is DSI with scale , then for any fixed , with parameter space is a discrete time self-similar process. If the process is DSI with scale , for some and , then for any fixed , with parameter space is a DSI sequence, with the same scale.

Based on the definition of wide sense self-similar process presented in [10], we present the following definition.

Definition 2.2

A random process is said to be discrete time self-similar in the wide sense with parameter

space for any , fixed and index , if the followings are satisfied

for every

,

,

.

If the above conditions hold for fixed , then the process is called DSI sequence in the wide sense with scale

. Another version of this definition is presented in [8].

Through this paper we are dealt with wide sense self-similar and wide sense scale invariant process, and for simplicity we omit the term ”in the wide sense” hereafter.

2.2 Markov processes in the wide sense

Let be a second order process of centered random variables, and .

Following Doob [6], a real valued second order process is Markov in the wide sense if, whenever

,

is satisfied with probability one, where stands for the linear projection (minimum variance estimator). If the process is

Gaussian, then is a version of the conditional expectation.

The following fact on the covariance of Markov processes in the wide sense, are essentially due to Doob [6]. The stochastic process

is Markov if and only , for where

is the covariance function of .

It follows that

for some functions and .

Borisov [4] completed the circle even for continuous time processes, namely, let be some function defined on

and suppose that everywhere on , where

is an interval. Then for to be the covariance function of a Gaussian Markov process with time space it

is necessary and sufficient that

| (2.4) |

where and are defined uniquely up to a constant multiple and the ratio is a positive nondecreasing function on

.

It should be noted that the Borisov result on Gaussian Markov processes can be easily derived in the discrete case for second

order Markov processes in the wide sense, by using Theorem 8.1 of Doob [6].

3 Covariance structure of the DSIM sequence

Let be a zero mean DSIM process with scale . If , we reduce the time scale, so that be greater than in the new scale. Now we consider to have samples in each scale. Our sampling scheme is to get samples at points where is obtained by equality . In this section we study the structure of the covariance function of DSIM sequence . We present a closed formula for the covariance function of DSIM sequence in Theorem 3.1. Discrete scale invariant autoregressive sequence of finite order , DSIAR(p), is introduced. The covariance function of DSIM sequence under some conditions is characterized in Theorem 3.2. Finally we justify our result by presenting two examples of DSIM sequences as discrete time simple Brownian motion and DSIAR(1).

Theorem 3.1

Let be a DSIM sequence with scale , , , then covariance function

| (3.1) |

where , , and is of the form

| (3.2) |

where ,

| (3.3) |

and Also

Proof: From the Markov property (2.4), for , satisfies

| (3.4) |

By substituting in the above relation and for we have

| (3.5) |

So . Thus by iteration

| (3.6) |

where As is a DSI sequence with parameter space and scale , by (3.1)

| (3.7) |

Thus for , by (3.3) and the convention we have

| (3.8) |

So by (3.5) for and (3.8)

| (3.9) |

for , and .

Also using (3.1) for

| (3.10) |

Remark 3.1

It follows from Theorem and relations and that ,

is fully specified

by the values of

3.1 Scale invariant autoregressive process

First we present periodically correlated autoregressive (PCAR) process of finite order, see [12], [13]. Then by introducing

discrete scale invariant autoregressive (DSIAR) sequence of order , we obtain the covariance function of such process.

A PC Process is called causal autoregressive of order , PCAR(), if

| (3.11) |

where is a periodic white noise with zero mean, variance and period and the coefficients are periodic with period , that is for . By causality, we have that is uncorrelated with . The PCAR(1) process is

| (3.12) |

where in (3.11), and . Then , where .

We remind that a stochastic process is said to be -ple Markov if for

| (3.13) |

The memory of this process extends units of time into the past. For the case of such a process is an ordinary Markov

process. Note that in the Gaussian case, the PC -ple Markov is equivalent to the PCAR().

Quasi Lamperti transform

Here we present an extension of Lamperti transform which we call quasi Lamperti that enable us to introduce flexible sampling of a continuous DSI process and provide a DSI sequence by the followings.

Definition 3.1

The quasi Lamperti transform with positive index and denoted by operates on a random process as

| (3.14) |

and inverse quasi Lamperti transform acts on process as

Corollary 3.1

If is DSI with scale and , then is its PC counterpart with period . Conversely if is PC with period then is DSI with scale .

Let be a DSI process with scale and index . We define discrete scale invariant autoregressive sequence of order , DSIAR(p), with parameter space and scale as

| (3.15) |

where is a white noise and has scale invariant property with scale , that is for . Then we have .

Remark 3.2

If is DSI with scale and for then is a self-similar autoregressive process of order .

Let be the PC counterpart of that by Corollary 3.1 we have

In addition we assume that and for , where and . So , where is a PCAR(p) counterpart of . If in (3.15) , is a DSIAR(1) process with parameter space and as

| (3.16) |

Then , where is defined by (3.1). So its covariance function for and can be written as

By a recursive method one can easily verify that . Since has scale invariant property, then

| (3.17) |

3.2 Characterization of the process

By the following theorem, the necessary conditions are given to show that, the covariance function , given by (3.2) characterizes a DSIM sequence.

Theorem 3.2

The function in relation characterize the covariance function of a DSIM sequence, if these functions satisfy the following condition

| (3.18) |

for and .

Proof: It is enough to show that every covariance function of the form (3.2) is the covariance function of a DSIM sequence.

For this, we show in (i) that the covariance function has scale invariance property

with scale .

We also prove in (ii) that is the covariance function of a wide sense Markov process, as it satisfies in the

relation .

(i) According to we have

where by and

and , therefore .

(ii) By (3.1), (3.2) and (3.8) we have that

where . Thus for , we have , that satisfies Borisov condition (2.4). So is the covariance function of a Markov process, provided is positive and nondecreasing. Positivity of is straight as

| (3.19) |

Now we prove that under condition (3.18) is nondecreasing function. So we show that . Let and , then we consider two cases, and . For , by (3.8) and (3.19) we have

As is DSI sequence with parameter space and scale , so by (3.1), . Therefore by (3.3)

Under condition for , , so is nondecreasing. For

By a similar method and under condition for , is nondecreasing.

3.3 Examples

We present two examples of DSIM sequence as discrete time simple Brownian motion with drift and DSIAR(1), then justify Theorem 3.1.

Example 3.1

A process is simple Brownian motion, with drift, and index , and scale as

where , are Brownian motion and indicator function respectively and is a real deterministic function.

Let , be disjoint sets. The expectation value and covariance function of the process for , and are

where and . Therefore by the condition , the above covariance is the covariance function of a Markov process. If and we have and

Then is DSI with scale .

By sampling of the process at points , , where , and

,

we provide a DSIM sequence and investigate the conditions of Theorem .

For where and we have

as . Also for when and , we have . Thus for , and

For , ,

and , , . Thus by (3.2)

Also by straight calculation we have the same result.

Example 3.2

We show that the covariance function of DSIAR(1) defined by satisfies the relation . By using and by the fact that we have

then according to , where .Therefore

which is the same as the straight computation of the covariance function in .

4 Spectral density estimation

In this section we assume that is a DSIM sequence with scale and present the characterization Theorem 4.1 for the covariance function of the associated T-dimensional discrete time self-similar Markov process. Then we report the spectral density matrix from [8], and present a dynamic method for estimation of the covariance function of DSIM process and spectral density matrix of its corresponding multi-dimensional self-similar process. The following definition, remark and theorem are reported from [8].

Definition 4.1

The process with parameter space , , and is a q-dimensional discrete time self-similar process in the wide sense, where

for all is discrete time self-similar process with parameter space .

For every

Remark 4.1

Corresponding to the DSIM sequence with scale , there exists a -dimensional discrete time self-similar Markov process with parameter space and

| (4.1) |

This remark is valid by the fact that for are discrete time self-similar process, and for

So assertions (a) and (b) of Definition 4.1 are satisfied.

Let be the covariance matrix of , then

Theorem 4.1

Let be a DSIM sequence with the covariance function and let , defined in , be its associated T-dimensional discrete time self-similar process with covariance function . Then

| (4.2) |

where is defined by and the matrix is given by , where , and the matrix is a diagonal matrix with diagonal elements , .

Current authors, showed that [8] if is a discrete time self-similar process with scale , then the spectral representation of the covariance function of the process is

| (4.3) |

where

| (4.4) |

and

| (4.5) |

for and .

Using Definition 4.1 they proved that the spectral density matrix of such -dimensional process is

, where

| (4.6) |

and is defined by (3.3). Thus we have the following result.

Remark 4.2

As the spectral density matrix of the multi-dimensional self-similar process , defined by is characterized by , relations reveal that the spectral density of the corresponding DSIM sequence is fully specified by .

Example 4.1

We present the T-dimensional DSIM sequence corresponding to the

DSIAR(1), defined by as

, where . Also we have

Thus the spectral density matrix of is obtained by substituting of in .

Estimation of covariance functions and spectral density matrix

Here we explain our method for estimation of the spectral density matrix of multi-dimensional self-similar Markov processes presented by (4.6).

For this, we need to estimate and

for and .

By the DSI property of the process, and have the same distribution,

so we evaluate these estimations by the followings. Let

Then we use following estimations to check the relation (3.2)

for .

for , and where

Also for , we have that

and

where and . By applying the above estimators in (4.6), the estimation of spectral density matrix is evaluated.

5 Simulation and Estimation

In this section first we present simulation of simple Brownian motion with different scale and Hurst parameters to visualize the behavior of such DSIM process in subsection 5.1. We verify the main results of the paper as Theorems 3.1 and 3.2, by simulating such process and estimating covariance and variance functions involve in relation (3.2). We use the scale invariant property of the process, with known scale parameter in subsection 5.2. So this study would be verification of Markov property of scale invariant processes. Finally in subsection 5.3, we present a new method for estimating Hurst parameters of DSI and self-similar processes.

5.1 Simulation

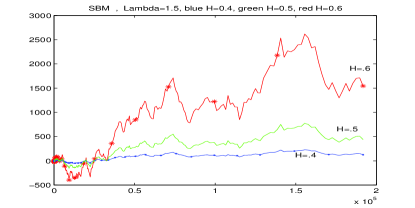

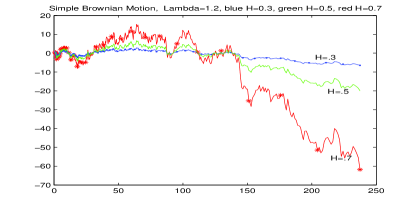

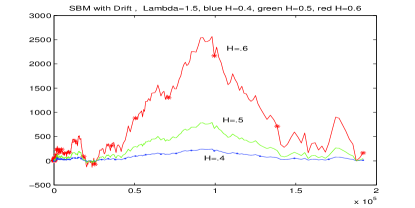

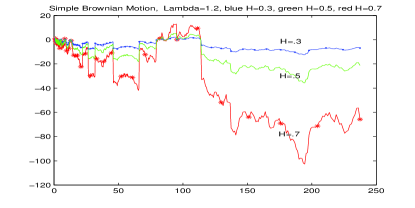

We present simulation of simple Brownian motion with drift which is defined in Example 3.1. For comparison it is interesting that when the drift is equal to zero, then we have simple Brownian motion with the same properties. We have simulated and plotted simple Brownian motion and also simple Brownian motion with drift for scales and and different Hurst indices which have been illustrated on the Figure 1 and Figure 2.

5.2 Characterization of the covariance function

For visualizing the Theorem 3.1 in recognizing wide sense Markov property for DSI Processes, we simulated 3000 samples of the following process

with Hurst index and scale where at points , , where is the standard Brownian motion. So we consider samples of scale intervals with samples, by such geometric sampling, in each scale interval. Then we estimate left hand side of (3.2) as for some different and , say and , and the right hand side of it to examine such equality which guarantees wide sense Markov property for such DSI process. By applying the method, presented at the end of section 4, and by considering samples with the above values for the parameters, we find the corresponding value for the left hand side and right hand side of (3.2) as and respectively, where the true value theoretically is .

5.3 Estimation of Hurst parameter

We present a new method for estimating Hurst parameters of DSI processes.

First we need to determine the scale of the process.

There are some practical methods for estimating of scale parameter in Balasis et al. [1].

Also Rezakhah et al. [11] have considered a theoretical method in this regard, and obtained an estimation

method for scale parameter and Hurst index of semi-selfsimilar or DSI processes. They introduced a two-stage method for

estimation of Hurst index which is based on an equally spaced sampling scheme. In their first stage the estimation was

effected by a possible self-similar behavior of the process inside each scale interval.

In this paper we consider a combination of equally spaced and geometric sampling scheme that, after determining scale intervals,

samples inside each scale interval are equally spaced but sample points in each scale interval are times of the sample

points in the previous scale interval. This sampling scheme enables our estimation method that explicitly determine the Hurst

index.

Estimation method

Our sampling scheme is to consider samples at the first scale interval as equally spaced samples where and sample points in the rest scale intervals are defined as , where is the scale of the DSI process. So if we denote sample points with , then . Also we have samples of consecutive scale intervals. We consider first and second order variation of observations inside each scale interval as , and . Then for we evaluate

| (5.7) |

Finally we provide two estimate of the Hurst index as

for .

Simulation method

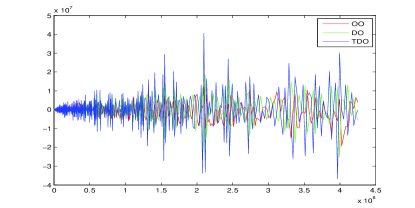

For simulation we consider simple Brownian motion with random drift as

where is the Brownian motion and are independent random variable with standard normal distribution. In Figure 3,

we have plotted the process and difference of order one and order two of lag one.

Abbreviations are, Original Observations (OO),

Differenced Observations (DO) and Twice Differenced Observations (TDO).

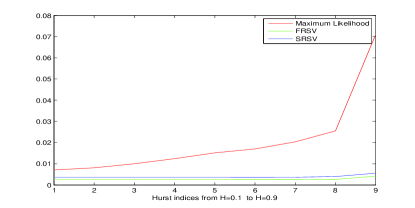

In Figure 4,

we have applied our estimation method and relation (5.7) for estimations of different Hurst indices by considering scale interval

and equally spaced samples in each scale and repetitions in each simulation and have plotted mean absolute

error (MAE) for different Hurst indices in Figure 4.

We also applied Maximum Likelihood method for corresponding multidimensional self-similar which has the same Hurst indices as the corresponding DSI Process and estimated Hurst indices and plotted their MAE to compare our estimation method with this Maximum Likelihood one which based on Vidas et all [15] present good estimate for Hurst index via geometric sampling.

As it is shown in Figure 5, MAE of estimations based on first order variation has less MAE and the MAE’s of estimation by second order variations are close to it, but estimation by Maximum likelihood method has much greater MAE and are going to increase by increasing the Hurst indices.

6 Conclusion

By considering our special geometric sampling for discrete scale invariant (DSI) process we have provided a sequence of such DSI process with a correspondence multi-dimensional self-similar process. Imposing Markov property for such DSI sequences, we have shown that the covariance function of such DSIM process is characterized by variance and covariance of adjacent samples in the first scale interval through an explicit formula. We have investigated this result theoretically for two examples of DSIM process as simple Brownian motion and scale invariant autoregressive model of order one. By verifying this characterization formula for covariance function of simulated data we find that these estimations are very close to each other. We have presented an efficient estimation method for the covariance function and spectral density matrix of corresponding multi-dimensional self-similar process as well. Also we have proposed a new method for estimating the Hurst parameter of DSI processes by considering the ratio of sample variation of successive scale intervals. Comparing our estimation method for simulated data with maximum likelihood one for Hurst parameter of corresponding multi-dimensional self-similar process, reveals that our estimation method performs much better. This paper could initiate further research in the study of DSI process by providing such connection to the multi-dimensional processes, and also has the potential to be applied for DSIM process for estimating covariance structure and spectral density matrix of corresponding multi-dimensional process.

References

- [1] G. Balasis, C. Papadimitriou (2011) I.A. Daglis, Signatures of discrete scale invariance in Dst time series, Geophysical Research Letters, Vol. 38, doi:10.1029/2011GL048019.

- [2] P. Borgnat, P.O. Amblard, P. Flandrin (2005) Scale invariances and Lamperti transformations for stochastic processes, J. Phys A: Mathematical and General, Vol.38, pp.2081-2101.

- [3] P. Borgnat, P. Flandrin, P.O. Amblard (2002) Stochastic discrete scale invariance, IEEE Signal Process, Lett.9, pp.181-184.

- [4] I.S. Borisov (1982) On a criterion for Gaussian random processes to be Markovian, Theory Probab. Appl., No.27, pp.863-865.

- [5] K. Burnecki, M. Maejima, A. Weron (1997) The Lamperti transformation for self-similar processes, Yokohama Math. J., Vol.44, pp.25-42.

- [6] J.L. Doob (1953) Stochastic Processes, Wiley, New York.

- [7] H.L. Gray, N.F. Zhang (1988) On a class of nonstationary processes, Journal of Time Series Analysis, Vol.9, No.2, pp.133-154.

- [8] N. Modarresi, S. Rezakhah (2010) Spectral analysis of Multi-dimensional self-similar Markov processes, J. Phys A: Mathematical and Theoretical, Vol.43, No.12, 125004 (14pp).

- [9] N. Modarresi, S. Rezakhah (2013) A new structure for analyzing discrete scale invariant processes: Covariance and Spectra, Journal of Statistical Physics, Vol.152(6), 15pp, DOI: 10.1007/s10955-013-0799-4.

- [10] C.J. Nuzman, H.V. Poor (2000) Linear estimation of self-similar processes via Lamperti s transformation, Journal of Applied Probability, No.37(2).

- [11] S. Rezakhah, A. Philippe, N. Modarresi (2013) Estimation of Scale and Hurst Parameters of Semi-Selfsimilar Processes, http://arxiv.org/pdf/1207.2450v1.pdf.

- [12] Q. Shao and R.B. Lund (2004) Computation and characterization of autocorrelations and partial autocorrelations in periodic ARMA models, J. Time Series Analysis, 25, No.3, 359-372.

- [13] Z. Shishebor, A.R. Nematollahi, A.R. Soltani (2006) On covariance generating functions and spectral densities of periodically correlated autoregressive processes, Journal of applied mathematics and stochastic analysis, pp.1-17.

- [14] D. Sornette (1998) Discrete scale invariance and complex dimensions, Phys. Rep., No.297, pp.239-270.

- [15] A. Vidacs, J. Virtamo (1999) ML estimation of the parameters of fBm traffic with geometrical sampling, IFIP TC6, Int. Conf. on Broadband communications 99, Hong-Kong.

- [16] W.X. Zhou, D. Sornette (2004) Discrete scale invariance in fractals and multifractal measures, Phys. Rev., 0407600, Vol.27.