Exact corrections for finite-time drift and diffusion coefficients

C. Anteneodo

celia@fis.puc-rio.brR. Riera

rrif@fis.puc-rio.brDepartment of Physics, PUC-Rio and

National Institute of Science and Technology for Complex Systems,

CP 38071, 22452-970, Rio de Janeiro, Brazil

Abstract

Real data are constrained to finite sampling rates, which

calls for a suitable mathematical description of the corrections

to the finite-time estimations of the dynamic equations.

Often in the literature,

lower order discrete time approximations of the modeling

diffusion processes are considered.

On the other hand, there is a lack of simple estimating procedures based

on higher order approximations.

For standard diffusion models,

that include additive and multiplicative noise components,

we obtain the exact corrections to the empirical finite-time

drift and diffusion coefficients, based on Itô-Taylor expansions.

These results allow to reconstruct the real hidden coefficients from the empirical estimates.

We also derive higher-order finite-time expressions for the third and fourth

conditional moments, that furnish extra theoretical checks for that class of diffusive models.

The theoretical predictions are compared with the numerical outcomes of some representative

artificial time-series.

pacs:

05.10.Gg, 05.40.-a, 02.50.Ey,

I Introduction

Many fluctuating random phenomena, including turbulent diffusion,

polymer dynamics or asset price evolution,

can be modeled by an univariate Itô-stochastic differential equation (SDE)

of the form bellow, characterizing a diffusive model:

(1)

where is a Wiener process, is the coefficient of the slowly varying

component (called drift coefficient) and is the coefficient of the rapid

one (called diffusion coefficient).

For sufficiently smooth and bounded drift and diffusion coefficients,

the associated probability density function (PDF)

is governed by the corresponding Fokker-Planck equation risken

(2)

Here, we are concerned with the empirical access to unknown drift and diffusion coefficients

of stochastic processes.

For an ideal time series generated by Eq. (1) and sampled

with a sufficiently high resolution on a long time period, the original coefficients can be

perfectly reconstructed.

For stationary processes, the coefficients , with can be directly estimated

from the conditional moments risken as:

(3)

where

(4)

with denoting statistical average and

meaning that at time the stochastic variable assumes the value .

Conversely, for general Markovian stochastic processes, the time evolution of PDFs is

governed by a generalization of Eq. (2), namely

(5)

with coefficients given by Eqs. (3)-(4), for any integer .

For diffusive processes, Eq. (5) reduces to Eq. (2).

Therefore, processes governed by the Itô-Langevin Eq. (1) must furnish null

coefficients , for .

Pawula theorem risken simplifies this task by

stating that if is null, all other coefficients with are null as well.

The coefficient is then a key coefficient to be investigated,

in order to establish the validity of the modeling of data series by Eq. (1)-(2).

However, due to the finite sampling rate of real data, numerical estimations of can

not always be straightforwardly extrapolated to the limit in Eq. (3).

In such cases, one accesses only the finite- estimation of the coefficients

given by Eq. (4), which may significantly

differ from the true coefficients .

This is specially relevant when is large compared to the characteristic timescales

of the process.

Some authors friedrich4 have introduced finite sampling rate corrections

to the coefficients and ,

by deriving expansions for the conditional moments up to some specified

low order of , directly from the Fokker-Planck equations.

Applications of this approach have already been implemented for those coefficients

up to second order Julia .

The error in the finite- estimated coefficients can also be derived

from the stochastic

Itô-Taylor expansion book of the integrated form of Eq. (1).

Within this line, the first order expansion of drift and diffusion coefficients

was recently presented in Ref. sura .

However, low order corrections may be inappropriate

when the convergence of the limit in Eq. (3) is slow friedrich4 ; comment .

Moreover, there is no a priori knowledge of whether the

sampling rate is fine enough to justify the use of the lowest order approximation.

In the present work, we investigate those issues for diffusion models defined by Eq. (1)

with linear drift coefficient, namely, ,

representing an harmonic restoring mechanism, and quadratic state-dependent diffusion coefficient,

namely, .

This class encompasses some of the most common models of the theoretical literature.

In fact, this equation is frequently found in a diversity of processes, from turbulence

to finance turbulence ; turbfinance .

Moreover, the obtained results are also valid for another class of SDEs

with additive-multiplicative noises multiplicative1 ; multiplicative2 , given by

(6)

where are uncorrelated Wiener processes.

For discretely sampled data at intervals , we will

derive, from the stochastic Itô-Taylor expansion,

finite- expressions for the parameters ,

up to infinite order.

These exact expressions will allow us to reconstruct the true drift and

diffusion coefficients from

their empirical finite-time estimates.

As a corollary, one can determine up to which value of a given order of

truncation is reliable (within a fixed tolerance), or reciprocally,

which is the sufficient order for a given .

Furthermore, as empirical estimates suffer from finite- effects, one always gets

non-null . Therefore, the evaluation of the corrections for this coefficient is

crucial for a suitable probe of the diffusive modeling.

In this work, we also derive finite- expressions for coefficients and ,

which furnish extra theoretical tests of consistency for the diffusive models considered.

Our theoretical findings are corroborated by the outcomes of exemplary artificial

time-series generated by Eq. (1).

II Exact corrections for drift and diffusion coefficients

Let us consider the Itô formula book , for a given function of the stochastic

variable

(7)

and its integrated form

(8)

Let be the sampling interval of state space observations.

By applying Itô formula (8) to the functions and

in the integral form of Eq. (1):

(9)

one finds

(10)

After iterated applications of Itô formula,

one gets an expression for the increment of the

stochastic variable in terms of multiple stochastic integrals book :

(11)

where , with for all ,

and

are multiple stochastic integrals of the form

,

with and .

By inserting Eq. (11) into Eq. (4) and performing the averaging,

for , we achieve

analytical expressions for the finite- drift and diffusion

coefficients, up to arbitrary order in powers of .

The resulting expressions preserve the linear and quadratic

-dependence, respectively and can be written as:

(12)

Hence, we are led to the theoretical relation between the finite- coefficients

and the

true ones , namely,

(13)

(14)

(15)

Details of the derivation of Eqs. (13)-(15)

can be found in the Appendix.

By restricting the expansions (13)-(15) to some common finite power ,

one gets the respective th-order approximation.

This result extends previous findings of first sura and second Julia

order terms.

Notice that Eq. (13) is uncoupled, meaning that the estimated

harmonic stiffness is not affected by the exact noise components.

Moreover, from Eq. (15), the estimated multiplicative noise parameter

does not depend on the exact additive noise component.

Summing the series in Eqs. (13)-(15) up to infinite order,

and defining and ,

we find the exact finite- expressions:

(16)

Notice that

holds.

From Eqs. (16),

we obtain an invariant relation among the estimated and exact parameters, namely,

(17)

The meaning of this invariance can be drawn, for instance, from the stationary

PDF associated to the corresponding Fokker-Planck equation

given by Eq. (2). With the present choice of drift and diffusion coefficients,

for , , one has:

(18)

with a normalization constant.

This solution is of the -Gaussian form multiplicative1 , for which,

if , the variance is finite with value .

Hence, Eq. (17) represents the uphold of the data variance under

changes of sampling intervals.

For , one recovers the Gaussian stationary solution and its variance relation.

Notice also that, from Eqs. (13)-(15), Eq. (17)

still holds if one considers partial corrections of the parameters up to any

common order of truncation of the sums.

Let us remark that the results presented in Eqs. (12)-(16)

are valid even when the variance is infinite.

However, we will deal only with finite variance cases and

consider normalized data (with unitary variance),

which only implies a rescaling of .

Then,

(19)

Taking into account the constraint (19), from Eqs. (16),

the exact finite- expressions are:

(20)

(21)

Eqs. (20) and (21) can be readily inverted to extract the

true parameters from their finite- estimates:

(22)

(23)

Notice that (and also )

can not be greater than unit.

In what follows, we fix the timescale .

A different choice would simply lead to a rescaling of the parameters

.

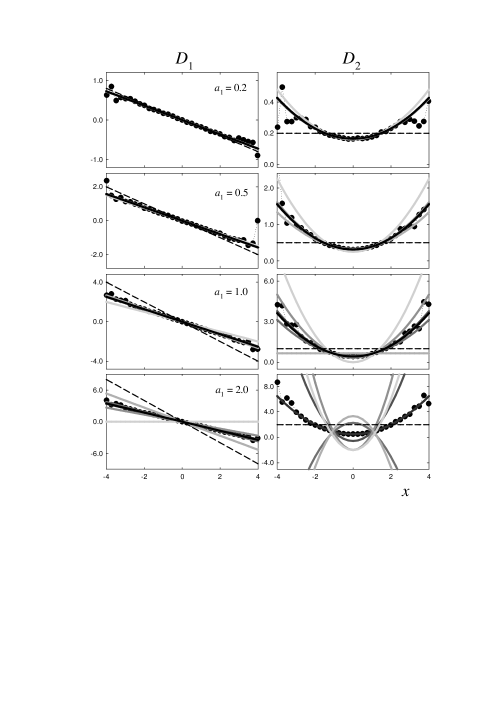

Figure 1: Drift and diffusion coefficients for the O-U process.

Symbols correspond to the numerical computation for artificial series ( data),

synthetized with the values of (, in accord with constraint

(19)) indicated on each panel.

Lines represent the coefficients given by Eqs. (12), using

the theoretical -expansions (13)-(15),

at different orders of truncation. The darker the color, the higher the order,

from first up to fifth order.

The infinite order (exact expression) is represented in thick black lines.

The zeroth order, corresponding to the true values, is plotted in dashed lines.

Now we investigate the importance of finite- effects for

discretely sampled realizations of representative known diffusive processes.

To this end, we generated artificial time-series through numerical integration of Eq. (1),

by means of an Euler algorithm with timestep ,

recording the data at each timesteps, in accord with our choice .

Our theoretical results for and will be compared

to the ones numerically computed from the time-series, through Eq. (4).

The particular case , corresponding to the Orstein-Uhlenbeck (O-U) process

and the general case with multiplicative component will be

investigated separately.

Fig. 1 shows the results

for the artificial series with known values of the parameters (),

together with our theoretical predictions.

The exact theoretical expressions reproduce the numerical (finite-time) outcomes.

Comparing the panels in Fig. 1, it is clear that,

the larger , the slower the convergence to the observed coefficients.

The results for also illustrate the entanglement one may find

in large- measurements, specifically, an oscillatory convergence of

and an alternating signal of .

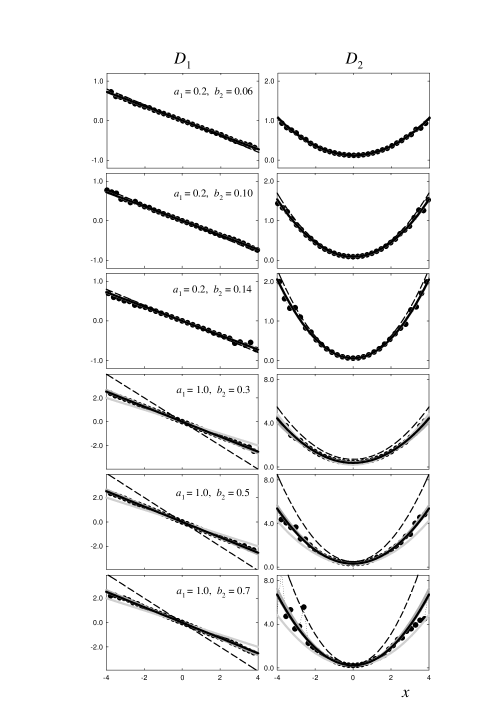

Figure 2: Drift and diffusion coefficients for the general process with multiplicative noise.

Symbols correspond to the numerical computation for artificial series ( data),

synthetized with the values of , in accord with constraint

(19)) and indicated on each panel.

Lines are as in Fig. 1.

In Fig. 2, we plot the numerical computations for

artificial time-series together with analytical predictions for .

Again, the theoretical approximations present slower convergence as

increases while the exact theoretical expressions agree with finite-time

estimates directly obtained from the time-series.

Moreover, the actual value of sets the convergence rate of .

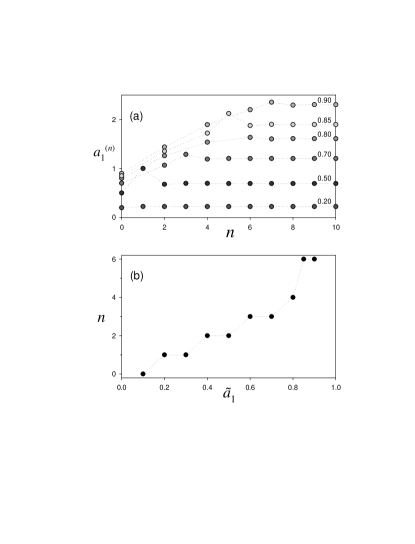

All these results raise a question about the domain of validity of lower order approximations

presented before in the literature. Let us investigate this issue quantitatively.

Given , obtained from numerical (finite-time) evaluation, the exact value of can

be recovered from Eq. (22).

Approximate values can be obtained by inversion of Eq. (13)

truncated at order .

Figure (3) illustrates as a function of

, for different values of .

Clearly, convergence to the true value is attained (within a given tolerance),

at different orders that depend on

the value of .

For instance, for , an order larger than two is required.

Convergence is faster for smaller , that is, as soon as 1/ becomes

large compared to the timescale .

For we obtained a very similar convergence scheme (not shown).

In Refs. sura ; Julia , the

fitness of low order expressions for O-U processes

results from the particular employment of .

However, this may not be the case when dealing with generic empirical data.

Figure 3: Dependence of on the order of the approximation given by

Eq. (13), for different values of (panel (a)). Dotted lines correspond to the

respective true values () and missing points denote

the absence of real solutions. Panel (b) exhibits the

order at which the limiting value is attained (within 5%) as a function of .

III Higher-order coefficients

Inserting the Itô-Taylor expansion Eq. (11) into Eq. (4) and

performing the average for , we also computed the

finite- expansion for and .

The resulting expressions are invariant functions of , namely:

(24)

(25)

For the particular case , we were able to derive the infinite order expansion for

the -parameters:

(26)

(27)

Notice that, ,

as expected, and that the relevant parameter for the rate of series convergence is .

Summing the series (26)-(27) up to infinite order, and

recalling that , one obtains

(28)

(29)

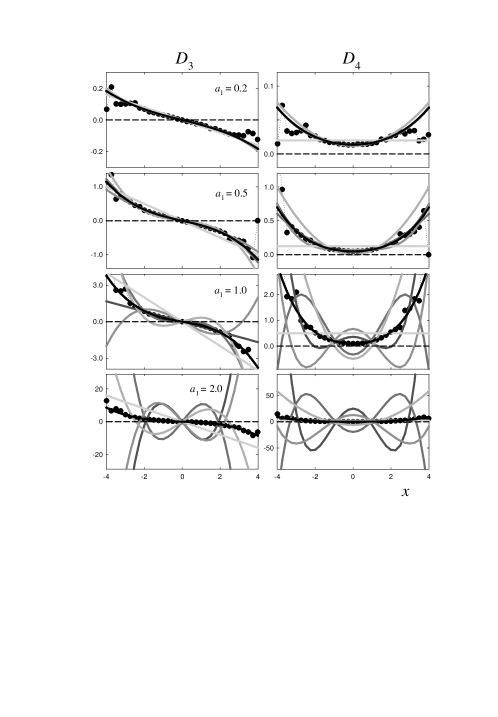

Fig. 4 shows the numerical computation of and

for the same artificial series as in Fig. 1.

For comparison, the theoretical estimates at different orders of truncation

of the series in Eqs. (26)-(27) are shown.

Notice that, although for the diffusive processes considered here,

their finite-time counterparts have cubic and quadratic forms.

Indeed, the exact theoretical expressions given by

Eqs. (28)-(29) reproduce the numerical outcomes,

validating our approach as furnishing meaningful tests for O-U models.

However, for , rich pictures for the low order approximations of

and arise, which hinder the asymptotic estimation.

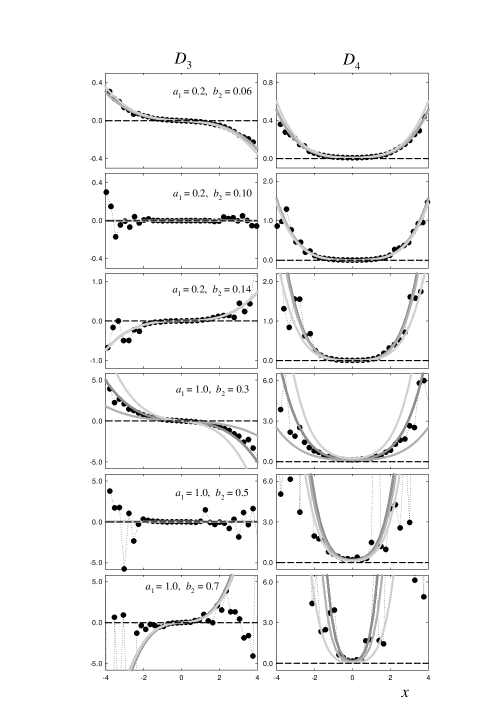

Figure 4: Third and fourth order coefficients for the O-U process.

Symbols correspond to the numerical computation for the same artificial series of

Fig. 1.

Lines represent the coefficients given by Eqs. (24)-(25), using

the theoretical -expansions (26)-(27),

at different orders of truncation. Colors as in Fig. 1.

For the general case with , we computed the third-order -expansions

for and .

Each power of of order has pre-factor denoted by

and respectively. We find, for :

(30)

where . At all orders, vanishes if .

Figure 5: Third and fourth order coefficients for the general process with multiplicative noise.

Symbols correspond to the numerical computation for the same artificial series of

Fig. 2.

Lines represent the coefficients given by Eqs. (24)-(25), using

the theoretical -expansions (30)-(31),

at different orders of truncation up to third order. Colors as in previous figures.

For , we have:

(31)

In Fig. 5, we show the numerical computation of

and for the same artificial series as in Fig. 2.

According to our theoretical results, is a threshold between positive and

negative slopes of , as illustrated in Fig. 5.

For comparison, we also show up to the third order theoretical estimates

and ,

according to Eqs. (30)-(31).

Coefficientes and provide further tests of validity of the diffusive modeling.

From Fig. 2, third order estimates

furnish suitable forecast of the numerical finite- measurements for small enough .

In such cases, once obtained from Eqs. (22)-(23), these values can be used in

theoretical equations for and , to check if the corresponding

non-null coefficients can be attributed to finite- effects.

IV Summary and final comments

For an important class of diffusion models with additive-multiplicative noise,

we have derived exact formulas that connect the empirical

discrete-time estimates with the actual

values of the parameters of drift and diffusion coefficients.

Additionally, we also provided theoretical expressions for higher-order coefficients which serve as a

further probe for the validity of this class of diffusive models.

Our results allow to access the generating stochastic process.

A possible procedure to identify it and its parameters can be summarized as follows.

When numerical computation of the coefficients from a real timeseries

yields linear and quadratic forms for and (which is a frequent outcome),

the values of can be obtained from curve fitting.

The present model (with or without multiplicative component) would be adequate when

i) and ii) ().

For the second order correction would be enough to recover ,

otherwise larger order corrections

should be considered. Once and are known,

Eqs. (22) and (23), allow to obtain,

exactly, the original parameters , hence also .

Values such that (hence, ) point to a simple O-U process,

otherwise a multiplicative term may be also present.

In both cases, a further check consists in the analysis of higher order coefficients, e.g.,

to see whether a non-null can be attributed to finite-time corrections.

By analyzing the O-U process, we also found that a low sampling rate would

significantly affect the diffusion coefficient estimate, by adding an extra

quadratic term.

Thus, the detection of a quadratic does not imply the existence of

multiplicative components in the actual process.

Moreover, estimations of and from low-order approximations would lead to

results inconsistent with the empirical outcomes.

The obtained formulas also allow to quantify the errors induced by a finite

sampling rate in the numerically estimated coefficients.

The analytical results indicate that, in order to grasp the

true values of the parameters from the knowledge of the observed ones,

the required correction depends strongly on the (hidden) inverse time .

Our work shows that one should be careful when applying low-order finite-

corrections for diffusion models.

Furthermore, as shown in Fig. 3, our results provide a criterion,

from the knowledge of ,

to determine the required order , or equivalently, up to which value of the respective

approximation is reliable.

Acknoledgements:

We acknowledge Brazilian agencies Faperj and CNPq for partial financial support.

Appendix

Rewriting Eq. (4) according to the notation introduced in Eq. (11), one has

Only multiple stochastic integrals such that have non-null

average, being .

From the iterated application of Itô formula to Eq. (9),

.

These are general results independent of the particular form of and .

Noticing that, from Eq. (7), ,

and that is time-independent and linear in ,

then, . Finally,

which is of the same functional form of the true and can be identified

with , so that

From the definition of in Eq. (11),

if (then is constant),

only two classes of terms in Eq. (32) are non-null, those with:

i) and and

ii) and .

In those cases, the products take the values:

i) (with ),

ii) (with ).

In order to evaluate the averages of products of multiple stochastic

integrals, it is useful to recall that

and that

book .

Then, summing over all the pairs contributing to the order

, one obtains:

i) ,

ii) .

Finally, from Eq. (32), we arrive at

(33)

which can be cast in the form , allowing to

identify and with functions of the true parameters, as

(34)

For the general case , a similar but tricky derivation leads to

Eqs. (14)-(15) that generalize the expressions (34).

Proceeding with the third order, products of three multiple integrals appear. For ,

there are two types of products

contributing to :

i) , , and

ii) , , , with

pre-factors proportional to and

to , respectively.

Evaluating the averages of products of three multiple stochastic

integrals and summing over all the triplets contributing to the same

order in , as done for the second order coefficient,

one gets , as in Eq. (24).

Analogously, at fourth order, considering the relevant products of four

multiple integrals, for ,

three types of contributions appear,

yielding ,

as in Eq. (25).

Let us recall that the averages of products of multiple stochastic integrals appearing in

the -order term of the

coefficients can be expressed, in general, as multinomial terms, whose summation over all the products

has the form (with rational ) for the order in .

Moreover, products of multiple stochastic integrals can be readily simplified, by means of useful relations

between multiple Itô integrals book .

Then, although at the cost of increasing the number of indices, the number of factors can be reduced.

References

(1)

H. Risken, The Fokker-Planck Equation: Methods of Solution and Applications

(Springer-Verlag, Berlin, 1984).

(2)

R. Friedrich, Ch. Renner, M. Siefert, J. Peinke, Phys. Rev. Lett. 89, 149401 (2002).

(3) J. Gottschall, J. Peinke, New Journal of Physics. 10, 083034 (2008);

and references therein.

(4)

P.E. Kloeden, E. Platen, Numerical Solution of Stochastic Differential

Equations, (Springer- Verlag, 1992).

(5) P. Sura, J. Barsugli, Phys. Lett. A 305, 304 (2002).

(6) M. Ragwitz, H. Kantz, Phys. Rev. Lett. 87, 254501 (2001);

M. Ragwitz, H. Kantz, Phys. Rev. Lett. 89, 149402 (2002).

(7)

S. Ghashghaie, W. Breymann, J. Peinke, P. Talkner, Y. Dodge, Nature 381, 767 (1996);

A. Naert, R. Friedrich, J. Peinke, Phys. Rev E 56, 6719 (1997);

St. Lück, J. Peinke, R. Friedrich, Phys. Rev. Lett. 83, 5495 (1999).

(8)

S. Ghashghaie, W. Breymann, J. Peinke, P. Talkner, Y. Dodge, Nature 381, 767 (1996).

(9)

C. Anteneodo, C. Tsallis, J. Math. Phys. 44, 5194 (2003).

(10)

C. Anteneodo, R. Riera, Phys. Rev. E 72, 026106 (2005).