Classification and categorical inputs with

treed Gaussian process models

Abstract

Recognizing the successes of treed Gaussian process (TGP) models as an interpretable and thrifty model for nonparametric regression, we seek to extend the model to classification. Both treed models and Gaussian processes (GPs) have, separately, enjoyed great success in application to classification problems. An example of the former is Bayesian CART. In the latter, real-valued GP output may be utilized for classification via latent variables, which provide classification rules by means of a softmax function. We formulate a Bayesian model averaging scheme to combine these two models and describe a Monte Carlo method for sampling from the full posterior distribution with joint proposals for the tree topology and the GP parameters corresponding to latent variables at the leaves. We concentrate on efficient sampling of the latent variables, which is important to obtain good mixing in the expanded parameter space. The tree structure is particularly helpful for this task and also for developing an efficient scheme for handling categorical predictors, which commonly arise in classification problems. Our proposed classification TGP (CTGP) methodology is illustrated on a collection of synthetic and real data sets. We assess performance relative to existing methods and thereby show how CTGP is highly flexible, offers tractable inference, produces rules that are easy to interpret, and performs well out of sample.

keywords: treed models, Gaussian process, Bayesian model averaging, latent variable

1 Introduction

A Gaussian process (GP) (e.g., Rasmussen and Williams,, 2006) is a popular nonparametric model for regression and classification that specifies a prior over functions. For ease of computation, typical priors often confine the functions to stationarity. While stationarity is a reasonable assumption for many data sets, still many more exhibit only local stationarity. In the latter case, a stationary model is inadequate, but a fully nonstationary model is undesirable as well. Inference can be difficult due to a nonstationary model’s complexity, much of which is unnecessary to obtain a good fit. A treed Gaussian process (TGP) (Gramacy and Lee,, 2008), in contrast, can take advantage of local trends more efficiently. It defines a treed partitioning process on the predictor space and fits distinct, but hierarchically related, stationary GPs to separate regions at the leaves. The treed form of the partition makes the model particularly interpretable. At the same time, the partitioning results in smaller matrices for inversion than would be required under a standard GP model and thereby provides a nonstationary model that actually facilitates faster inference.

Recognizing the successes of TGP for regression, we seek to extend the model to classification. Separately, both treed models and GPs have already been been successfully applied to classification. Bayesian methods in the first case outline a tree prior and series of proposals for tree manipulation in a Monte Carlo sampling framework, leading to Bayesian CART (Chipman et al.,, 1998)—extending the classical version due to Breiman et al., (1984). In the second case lies a method by which real-valued GP output may be utilized in a classification context (Neal,, 1998); for some number of classes, the real outputs of a commensurate number of GPs ( for classes) are taken as priors for latent variables that yield probabilities via a softmax function. This leads to two ways to combine trees with GPs for classification. The data may be partitioned once by the tree process, and then we may associate GPs to each region of the partition, or instead, separate full TGPs may be instantiated. We propose taking the latter route in the interests of faster mixing. We describe a Monte Carlo sampling scheme to summarize the posterior predictive distribution. The algorithm traverses the full space of classification TGPs using joint proposals for tree-topology modifications and the GP parameters at the leaves of the tree. We explore schemes for efficiently sampling the latent variables, which is important to obtain good mixing in the (significantly) expanded parameter space compared to the regression case.

The remainder of the paper is outlined as follows. We shall first review the GP model for regression and classification in Section 2. Section 3 begins with a review of the extension of GPs to nonstationary regression models by treed partitioning, covering the basics of inference and prediction with particular focus on the Monte Carlo methods used to integrate over the tree structure. We then discuss how categorical inputs may be dealt with efficiently in this framework. This discussion represents a new contribution to the regression literature and, we shall argue, is particularly relevant to our classification extensions; it is the categorical inputs that can most clearly benefit from the interpretation and speed features offered by treed partitioning. We are then able to describe the TGP model for classification in detail in Section 3.3. In Section 4 we illustrate our proposed methodology on a collection of synthetic and real data sets. We assess performance relative to existing methods and thereby demonstrate that this nonstationary classification model is highly flexible, offers tractable inference, produces rules that are easy to interpret, and (most importantly) performs well out of sample. Finally, in Section 5 we conclude with a short discussion.

2 Gaussian processes for regression and classification

Gaussian process (GP) models are highly flexible and nonlinear models that have been applied in regression and classification contexts for over a decade (e.g., Neal,, 1997, 1998; Rasmussen and Williams,, 2006). For real-valued -dimensional inputs, a GP is formally a prior on the space of functions such that the function values at any finite set of input points have a joint Gaussian distribution (Stein,, 1999). A particular GP is defined by its mean function and correlation function. The mean function is often constant or linear in the explanatory variable coordinates: , where . The correlation function is defined as .

We further assume that the correlation function can be decomposed into two components: an underlying strict correlation function and a noise term of constant and strictly positive size that is independently and identically distributed at the predictor points.

Here, is the Kronecker delta, and we call the nugget. In the model, the nugget term represents a source of measurement error. Writing the GP as , we have as the fixed mean function, as a zero-mean Gaussian random variable with correlation , and as an i.i.d. Gaussian noise process. Computationally, the nugget term helps ensure that remains nonsingular, allowing the frequent inversion of without concern for numerical instability that might otherwise plague efficient sampling from the Bayesian posterior as necessary for the analysis that follows.

Due to its simplicity, a popular choice for is the squared exponential correlation

where the strictly positive parameter describes the range (or length-scale) of the process. I.e., governs the rate of decay of correlation as the distance between locations and increases. The underlying (Gaussian) process that results with this choice of is both stationary and isotropic. It is easily extended to incorporate a vector-valued parameter so that correlation may decay at rates that differ depending on direction:

The resulting process is still stationary, but it is no longer isotropic. Further discussion of correlation structures for GPs can be found in Abrahamsen, (1997) or Stein, (1999). These structures include the popular Matérn class (Matérn,, 1986), which allows the smoothness of the process to be parameterized. The choice of correlation function is entirely up to the practitioner—the methods described herein apply generally for any .

The GP model, described above for the problem of regression, can be extended to classification by introducing latent variables (Neal,, 1997). In this case, the data consist of predictors and classes . Suppose there are data points and classes. We introduce sets of latent variables , one for each class. For a particular class , the generative model is a GP as before: . The class probabilities are now obtained from the latent variables via a softmax function

| (1) |

The generative model then specifies that the class at a point is drawn from a single-trial multinomial distribution with these probabilities. In practice, only GPs are required since we may fix the latent variables of the final class to zero without loss of generality.

In this model, it remains to place priors, perhaps of a hierarchical nature, on the parameters of each GP. The challenge of efficiently sampling from the posterior of the latent variables also remains. Neal, (1997) suggests sampling the hyperparameters with a Gaussian random walk or by the hybrid Monte Carlo method. Our choice of hierarchical model, in contrast, allows almost entirely Gibbs sampling moves (Gramacy and Lee,, 2008). Neal suggests sampling the latent variables (individually) with adaptive rejection sampling (Gilks and Wild,, 1992). We prefer to use Metropolis–Hastings (MH) draws with a carefully chosen proposal distribution and consider block-sampling the latent variables (see Section 3.3.3).

The GP model, for both regression and classification, features some notable drawbacks. First, as mentioned above, the popular correlation functions are typically stationary whereas we may be interested in data which are at odds with the stationarity assumption. Second, the typical correlation functions are clumsy for binary or categorical inputs. Finally, the frequent inversions of a correlation matrix, an operation, are necessary for GP modeling, which makes these analyses computationally expensive.

3 Treed Gaussian processes

Partitioning the predictor space addresses all three of the potential drawbacks mentioned above and offers a natural blocking strategy (suggested by the data) for sampling the latent variables as required in the classification model. In particular, after partitioning the predictor space, we may fit different, independent models to the data in each partition. Doing so can account for nonstationarity across the full predictor space. Partitions can occur on categorical inputs; separating these inputs from the GP predictors allows them to be treated in classical CART fashion. Finally, partitions result in smaller local covariance matrices, which are more quickly inverted.

3.1 TGP for regression

CART (Breiman et al.,, 1984) and BCART (for Bayesian CART) (Chipman et al.,, 1998, 2002) for regression essentially use the same partitioning scheme as TGP but with simpler models fit to each partition described by the tree. More precisely, each branch of the tree—in any of these models—divides the predictor space in two. Consider predictors ; for some split dimension and split value , points with are assigned to the left branch, and points with are assigned to the right branch. Partitioning is recursive and may occur on any input dimension , so arbitrary axis-aligned regions in the predictor space may be defined. Conditional on a treed partition, models are fit in each of the leaf regions. In CART the underlying models are “constant” in that only the mean and standard deviation of the real-valued outputs are inferred. The underlying CART tree is “grown” according to one of many decision theoretic heuristics and may be “pruned” using cross-validation methods. In BCART, these models may be either constant (Chipman et al.,, 1998) or linear (Chipman et al.,, 2002) and, by contrast with CART, the partitioning structure is determined by Monte Carlo inference on the joint posterior of the tree and the models used at the leaves. In regression TGP (hereafter RTGP), the leaf models are GPs, but otherwise the setup is identical to BCART. Note that the constant and linear models are special cases of the GP model. Thus RTGPs encompass BCART for regression and may proceed according to a nearly identical Monte Carlo method, described shortly.

For implementation and inference in the RTGP model class, we take advantage of the open source tgp package (Gramacy and Taddy,, 2008) for R available on CRAN (R Development Core Team,, 2008). Details of the computing techniques, algorithms, default parameters, and illustrations are provided by Gramacy, (2007).

3.1.1 Hierarchical model

The hierarchical model for the RTGP begins with the tree prior. We define this prior recursively following Chipman et al., (1998). To assemble tree , start with a single (root) node. Form a queue with this root node. Recursively, for each node in the queue, decide to split with some probability . If splits, first choose a splitting rule for according to the distribution , and then put the new children of in the queue. It remains to define the distributions and . The choice , with and , includes a base probability of splitting and a penalty factor , which is exponential in the node depth in . A simple distribution over split-points is first uniform in the coordinates of the explanatory variable space and then uniform over splitting values that result in distinct data sets at the child nodes. When non-informative priors are used at the leaves of the tree it is sensible to have the tree prior enforce a minimum data requirement for each region of the partition(s). We take the tgp defaults in this respect, which automatically determine an appropriate minimum as a function of the predictor dimension .

Now let index the non-overlapping regions partitioned by the tree formed from the above procedure. In the regression problem, each region contains points of data: . is defined to be an extension to the predictor matrix with an intercept term: ; thus, has columns. A “constant mean” may be obtained with ; in this case, in Eq. (2) below. The generative model for the GP in region incorporates the multivariate normal (), inverse-gamma (), and Wishart () distributions as follows.

| (2) | ||||||

The hyperparameters are constant in the model, for which we take the tgp defaults.

3.1.2 Estimation

Our aim in this section is to approximate the joint distribution of the tree structure , the sets of GP parameters in each region depicted by , and GP hyperparameters (those variables in Eq. (2) that are not treated as constant but also not indexed by ). To do so, we sample from this distribution using Markov Chain Monte Carlo (MCMC). We sequentially draw , for each , and . All parameters (, ) and hyperparameters of the GPs can be sampled with Gibbs steps, with the exception of the covariance function parameters . Expressions are provided by Gramacy and Lee, (2008), and full derivations are provided by Gramacy, (2005), which are by now quite standard in the literature so they are not reproduced here.

Monte Carlo integration over tree space, conditional on the GP parameters , is, by contrast, more involved. Difficulties arise when we randomly draw a new tree structure from the distribution because it is possible that the new tree may have more leaf nodes (or fewer) than before. Changing the number of leaf nodes changes the dimension of , so simple MH draws are not sufficient for . Instead, reversible jump Markov Chain Monte Carlo (RJ-MCMC) allows a principled transition between models of different sizes (Richardson and Green,, 1997).

However, by choosing the GP parameters at the leaf nodes of the proposal tree carefully, the distinction between MH and RJ-MCMC can be effectively ignored. In the case where the number of leaf nodes does not change between the current tree state and the proposal tree, maintaining the same collection of allows us to ignore the RJ-MCMC Jacobian factor. In the case where the number of leaf nodes increases—and the increase will always be by exactly one leaf node—drawing the GP parameters from their priors similarly sets the Jacobian factor in the RJ-MCMC acceptance ratio to unity; this leaves just the usual MH acceptance ratio. Gramacy and Lee, (2008) describe proposals that facilitate moves throughout the space of possible trees and how these moves are made reversible. The moves are called grow, prune, change, and swap, where the final move has a special sub-case rotate to increase the resulting MCMC acceptance ratio. This list of four moves is largely the same as in the BCART model (Chipman et al.,, 1998), with the exception of rotate. During MCMC, the moves are chosen uniformly at random in each iteration.

3.1.3 Prediction

From the hierarchical model in Section 2, we can solve for the predictive distribution of the outputs . Conditional on the covariance structure, standard multivariate normal theory gives that the predicted value of ) is normally distributed with

| (3) |

| where | ||||||

Here, we have under the model with a linear mean, or under the constant mean. Further, is an -long vector with for all , and is given in closed form by Gramacy and Lee, (2008).

Conditional on a particular tree , the expressions in Eq. (3) betray that the predictive surface is discontinuous across the partition boundaries of . However, in the aggregate of samples collected from the joint posterior distribution of , the mean tends to smooth out near likely partition boundaries as the tree operations grow, prune, change, and swap integrate over trees and GPs with large posterior probability. Uncertainty in the posterior for translates into higher posterior predictive uncertainty near region boundaries. When the data actually indicate a non-smooth process, the treed GP retains the flexibility necessary to model discontinuities. When the data are consistent with a continuous process, the treed GP fits are almost indistinguishable from continuous (Gramacy and Lee,, 2008).

3.2 Categorical inputs

Classical treed methods, such as CART, can cope quite naturally with categorical, binary, and ordinal inputs. For example, categorical inputs can be encoded in binary, and splits can be proposed with rules such as . Once a split is made on a binary input, no further process is needed, marginally, in that dimension. Ordinal inputs can also be coded in binary, and thus treated as categorical, or treated as real-valued and handled in a default way. GP regression, however, handles such non-real-valued inputs less naturally, unless (perhaps) a custom and non-standard form of the covariance function is used (e.g., Qian et al.,, 2008). When inputs are scaled to lie in , binary-valued inputs are always a constant distance apart—at the largest possible distance in the range. When using a separable correlation function, parameterized by length-scale parameter , the likelihood will increase as gets large if the output does not vary with and will tend to zero if it does (in order to best approximate a step function correlation). Moreover, the binary encoding of even a few categorical variables (with several levels) would cause a proliferation of binary inputs which would each require a unique range parameter. Mixing in the high dimensional parameter space defining the GP correlation structure would consequently be poor. Clearly, this functionality is more parsimoniously achieved by partitioning, e.g., using a tree. However, trees with fancy regression models at the leaves pose other problems, as discussed below.

Rather than manipulate the GP correlation to handle categorical inputs, the tree presents a more natural mechanism for such binary indicators. That is, they can be included as candidates for treed partitioning but ignored when it comes to fitting the models at the leaves of the tree. They must be excluded from the GP model at the leaves since, if ever a Boolean indicator is partitioned upon, the design matrix (for the GP or LM) would contain a column of zeros or ones and therefore would not be of full rank. The benefits of removing the Booleans from the GP model(s) go beyond producing full-rank design matrices at the leaves of the tree. Loosely speaking, removing the Boolean indicators from the GP part of the treed GP gives a more parsimonious model. The tree is able to capture all of the dependence in the response as a function of the indicator input, and the GP is the appropriate non-linear model for accounting for the remaining relationship between the real-valued inputs and outputs. Further advantages to this approach include speed (a partitioned model gives smaller covariance matrices to invert) and improved mixing in the Markov chain when a separable covariance function is used since the size of the parameter space defining the correlation structure would remain manageable. Note that using a non-separable covariance function in the presence of indicators would result in a poor fit. Good range () settings for the indicators would not necessarily coincide with good range settings for the real-valued inputs. Finally, the treed model allows the practitioner to immediately ascertain whether the response is sensitive to a particular categorical input by tallying the proportion of time the Markov chain visited trees with splits on the corresponding binary indicator. A much more involved Monte Carlo technique (e.g., following Saltelli et al.,, 2008) would otherwise be required in the absence of the tree.

If it is known that, conditional on having a treed process for the binary inputs (encoding categories), the relationship between the remaining real-valued inputs and the response is stationary, then we can improve mixing in the Markov chain further by ignoring the real-valued inputs when proposing tree operations. In Section 4.1 we shall illustrate the benefit of the treed approach to categorical inputs in the regression context.

There is a possible drawback to allowing (only) the tree process to govern the relationship between the binary predictors and the response; any non-trivial treed partition would force the GP part of the model to relate the real-valued inputs and the response separately in distinct regions. By contrast, one global GP—with some mechanism for directly handling binary inputs—aggregates information over the entire predictor space. We can imagine a scenario where the correlation structure for the real-valued inputs is globally stationary, but the response still depends (in part) upon the setting of a categorical input. Then partitioning upon that categorical input could weaken the GP’s ability to learn the underlying stationary process governing the real-valued inputs. In this case, the approach described by Qian et al., (2008), which explicitly accounts for correlation in the response across different values of the categorical predictors, may be preferred. However, we shall argue in Section 3.3 that in the classification context this possibility is less of a worry because the GP part of the model is only a prior for the latent -values, and therefore its influence on the posterior is rather weak compared to the class labels . Such small influences take a back seat to the (by comparison) enormous speed and interpretability benefits that are offered by treed partitioning on binary inputs as illustrated empirically in Sections 4.2 and 4.3. These benefits are not enjoyed by the Qian et al., (2008) approach.

3.3 TGP for classification

Recall that in order to adapt the GP for classification (Section 2), we introduced sets of latent variables so that each predictor corresponds to latent variable values. The class then has a single-draw multinomial distribution with probabilities obtained via the softmax function (1) applied to these latent variables.

3.3.1 Possible model formulations

In the TGP case, however, it is not immediately clear how these latent variables fit into the tree structure. We can imagine at least two possibilities. First, recall that in the RTGP model, the tree partitions the predictor space into regions. In each region, we fit a GP. One latent variable extension to this model would be to fit a CGP at each leaf of the tree. Instead of a single GP, each leaf CGP consists of GPs. The output of these GPs would be the latent variable sets in that particular region. Together, the output over all regions would form the entire set of latent variables. Since this model features just one tree, we call it an OTGP.

Alternatively, we might not choose to generate a CGP at each leaf of a single tree. Rather, we could recall that the CGP amalgamates latent variables from real-valued models. Instead of the GPs of the CGP, then, we could generate independent, full TGP models. The output of the TGP would be the full set of latent variables for the class. Since this model features multiple, independent trees, we call it an MTGP. Note that in this latter case, the trees need not all have the same splits. We can imagine perfect copies of indexed by class. Then may be partitioned differently for each . In the OTGP case, on the other hand, is partitioned into exactly the same regions across all .

We choose to focus on the MTGP in the following analysis as we expect it to exhibit better mixing than the OTGP when the number of classes is greater than two. For a particular choice of prior and hierarchical model, the OTGP may be thought of as an MTGP where the trees are all constrained to split on the same variable–value pairs. The MTGP may thus more easily model natural splits in a set of data since each tree can be different. Imagine a data set where class 1 occurs predominantly in region 1, class 2 occurs predominantly in region 2, and class 3 in region 3. As we will see in Section 4.2, a single split in each of the two MTGP trees may be sufficient to capture these divisions. For OTGPs, however, the overarching tree in the same case would require two splits to represent the partition. But a greater number of splits is less likely under the given tree prior (Section 3.1.1).

Moreover, the final splits in the MTGP are more interpretable since we immediately see which class label was relevant for a given split. In the OTGP, a split may be primarily relevant to a particular class label or set of class labels, but it will still be applied across all class labels. Along similar lines, when a grow or change move is proposed in the tree, evidence from all of the GPs of the OTGP accumulates for or against the move. Thus it is less likely that the acceptance probability will be high enough for such a move to take place in the OTGP. But for the MTGP, only the latent variables of class directly influence the proposal probability of grows or changes in the th tree. So it is easier for the MTGP trees to grow and thereby take advantage of the tree structure in the model.

Finally, as a practical consideration, the MTGP is more directly implemented as an extension of the RTGP. The combination of tree and latent variable sets for each class can be essentially the same—depending on hierarchical model choice in the classification case—as the existing RTGP formulation with the latent variables as the outputs. Thus, the MTGP model may be coded by making minor modifications to the the tgp package. Since we henceforth use only the MTGP, we will refer to it as a CTGP (TGP for classification) in analogy to the acronym RTGP.

3.3.2 Hierarchical model

The hierarchical model for the CTGP model is straightforward. Given data , we introduce latent variables . There is one set for each class or, equivalently, one set for each tree. Each of the trees divides the space into an independent region set of cardinality . And each tree has its own, independent, RTGP prior where the hyperparameters, parameters, and latent variable values—for fixed class index —are generated as in Eq. (2). While this full model is identical to the RTGP case, we prefer a constant mean for the classification task as the linear mean incorporates extra degrees of freedom with less of a clear benefit in modeling flexibility. Finally, the generative model for the class labels incorporates the latent variables from all trees. The softmax function appears just as in the CGP case (1). Figure 1 summarizes the full model via a plate diagram. The devil is, of course in the details, which follow.

3.3.3 Estimation

To approximate the joint distribution of the TGPs, we sample with MCMC as in Section 3.1.2 to a large extent. Sampling is accomplished by visiting each tree in turn. For the class, we sequentially draw , for each region of , , and finally the latent variables for each . The first three draws are the same as for the RTGP, although they may be modified as described below. The latent variable draw is the step unique to the CTGP.

One possible extension to the tree moves introduced in Section 3.1.2, and described in full detail in Gramacy and Lee, (2008), is to propose new latent variables along with each move. In this formulation, we would accept or reject the new partition along with the newly proposed set of latent variables and, possibly, newly proposed GP parameters (c.f. grow). A difficulty with these tree moves in classification problems is that the class data does not play a direct role; indeed, it is used only in defining the acceptance probability of the latent variable draws (see below). It is tempting to try to incorporate more directly into determining the tree structure by adding latent variable moves to grow, prune, change, and swap (but not rotate). We could, for instance, propose from its prior. Then the class data would appear in the posterior probability factor of the MH acceptance ratio. The tree operations themselves are no different whether the latent variables are proposed or not.

However, some experimental trials with this modification suggested that the resultant mixing in tree space is poor. Intuition seems to corroborate this finding. Incorporating many new random variables into a proposal will, generally, decrease the acceptance ratio for that proposal. Certainly, when the are all proposed simultaneously in each leaf from their GP prior, it is unlikely that they will predominantly arrange themselves to be in close correspondence with the class labels. Even when a blocking mechanism is used, all of the latent variables must be accepted or rejected together—along with the proposed tree move. Instead of handicapping the tree moves in this way, we therefore separate out the latent variable proposals. Moreover, we suspect that the tree will be most helpful for categorical inputs, which are not dealt with in a parsimonious way by the existing CGP model. Indeed, the latent variables have enough flexibility to capture the relationship between the real-valued inputs and the class labels in most cases.

3.3.4 Class latent variables given the class tree and parameters

While we cannot sample directly from to obtain a Gibbs sampling draw, a particular factorization of the full conditional for some subset of suggests a reasonable proposal distribution for MH. More specifically, the posterior is proportional to a product of two factors: (a) the probability of the class given the latent variables at its predictor(s) and (b) the probability of the latent variable(s) given the current GP and other latent variables in its region . Here is an index set over the predictors , and as usual labels the region within a particular class; is the index set of points in region of class that are not in . The latter distribution is multivariate normal, with dimension equal to the size of the latent variable set being proposed, . To condense notation in Eq. (4), let (similarly for and ), and let . Then we have

| (4) | |||||

The above is essentially a condensation and slight generalization of the predictive distribution for the real-valued output of an RTGP (3). To complete the description, we again slightly generalize the previous definitions of and (Gramacy and Lee,, 2008). Here, and are defined by their role in the distribution . The explicit formulas are as follows.

We sample from the latent variable distribution with MH steps. Such a step begins with a proposal of new latents from the prior for conditional on the GP parameters, i.e., following Eq. (4). Since the prior cancels with the proposal probability in the acceptance ratio, the new latent variables are accepted with probability equal to the likelihood ratio, where the unprimed represents the current latent variable values. This leaves:

It is not necessary to propose all of the latent variables in a region at once. We may employ a blocking scheme whereby we propose some subset of the latent variables in region conditioned on the rest; we keep proposing for different (mutually exclusive) blocks until we have iterated over all of the region’s latent variables, in each step conditioning on the accepted/rejected latents from the previously processed blocks and those yet to be proposed (i.e., having the values obtained in the previous iteration of MCMC). There is a natural trade-off in block size. Proposing all at once leads to a small acceptance ratio and poor mixing. But proposing each individually may result in only small, incremental changes. An advantage of the treed partition is that it yields a natural blocking scheme for updating the latent variables by making latents in a particular region independent of those in other regions. While it may be sensible to block further within a leaf, the automatic blocking provided by the treed partition is a step forward from the CGP.

3.3.5 Prediction

The most likely class label at a particular predictor value corresponds to the smallest—or most negative—of the latent variables obtained at that predictor; this observation follows from the softmax generative model for the class labels given in Eq. (1). Recall that the latent is fixed at zero. We predict the class labels by keeping a record of the predicted class labels at each round of the Monte Carlo run and then take a majority vote upon completion. We may furthermore summarize the posterior multinomial distribution over the labels by recording the proportion of times each class label had the lowest latent value over the entire Markov chain, obtaining a full accounting of our predictive uncertainty in a true and fully Bayesian fashion.

4 Illustrations and empirical results

Before illustrating the CTGP algorithm and comparing it to CGP on real and synthetic data, we shall illustrate the use of categorical inputs in the regression context. Two examples without categorical inputs then follow in order to illustrate and benchmark CTGP against CGP when the inputs are real-valued. We conclude the section with a real data set involving credit card applications and exhibiting both types of inputs. One aim there will be to further highlight how an appropriate handling of categorical inputs via trees facilitates faster and more accurate Bayesian inference. But we also show how this approach aids in identification of a particular categorical feature to which the response (credit card approval) is sensitive. This last type of output would have been difficult to elicit in the classical CGP setup.

4.1 Categorical inputs for regression TGP

Consider the following modification of the Friedman data (Friedman,, 1991; see also Section 3.5 of Gramacy,, 2007). Augment 10 real-valued covariates in the data () with one categorical indicator that can be encoded in binary as

Now let the function that describes the responses (), observed with standard normal noise, have a mean

| (5) |

that depends on the indicator . Notice that when the original Friedman data is recovered, but with the first five inputs in reverse order. Irrespective of , the response depends only upon , thus combining nonlinear, linear, and irrelevant effects. When the response is linear in . In the experiments that follow we observe with i.i.d. noise.

Note that the encoding above precludes splits of the indicator variable with exactly two values on each side. As has been noted previously in the context of CART (Hastie et al.,, 2001), a full enumeration of non-ordinal, categorical predictor splits is exponential in the range of categorical predictor values. The encoding above—which generalizes to an arbitrary number of predictor values—is more limited; the growth in the number of splits is linear in the number of predictor values. Observe that the full and restricted encodings differ only for predictor ranges of size at least four. Arbitrary groupings of predictor values are still achievable—although the remaining values will not necessarily form a single, opposing group.

| method | bcart | btlm | btlm2 | btgp | btgp2 | btgp3 |

|---|---|---|---|---|---|---|

| 95% | 3.24 | 2.86 | 1.82 | 1.33 | 1.16 | 1.00 |

| mean | 2.83 | 2.69 | 1.70 | 1.15 | 0.66 | 0.56 |

| median | 2.79 | 2.69 | 1.68 | 1.15 | 0.53 | 0.49 |

| 5% | 2.52 | 2.54 | 1.54 | 0.93 | 0.41 | 0.40 |

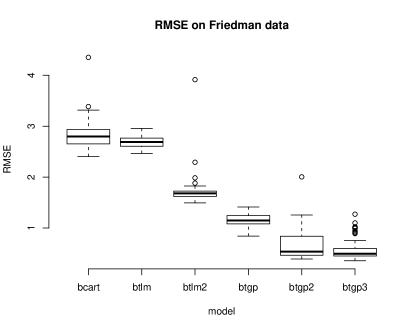

Figure 2 compares boxplots and summaries of the root mean squared error (RMSE) obtained for various regression algorithms (in the TGP class) when trained on 500 points from (5) sampled uniformly at random in and tested on a similarly obtained hold-out test set of size 1000. The results and behavior of the various methods are discussed below.

One naïve approach to fitting this data would be to fit a treed GP model ignoring the categorical inputs. But this model can only account for the noise, giving high RMSE on a hold-out test set, and so is not illustrated here. Clearly, the indicators must be included. One simple way to do so would be to posit a Bayesian CART model (bcart in the Figure). In this case the indicators are treated as indicators (as is appropriate) but in some sense so are the real-valued inputs since only constant models are fit at the leaves of the tree. As expected, the tree does indeed partition on the indicators and the other inputs.

One might hope for a much better fit from a treed linear model (btlm) to the data since the response is linear in some of its inputs. Unfortunately, this is not the case. When a linear model with an improper prior (the tgp default) is used at the leaves of the tree, the Boolean indicators could not be partitioned upon because such a proposal would cause the design matrices at the two new leaves to become rank-deficient (they would each, respectively, have a column of all zeros or all ones). A treed GP would have the same problem. While such models offer a more parsimonious representation of a smoothly varying response (i.e., not piecewise constant) compared to CART, a penalty is paid by the inability to partition; improvements in modeling the real-valued predictors (via, for instance, the linear model) balance against the cost of sacrificing the categorical predictors. Ultimately, the net result of these two effects translates into only marginal improvements in predictive performance over Bayesian CART.

One possible remedy is to employ a proper prior at the leaves. But that has its own drawbacks. Instead, consider including the Boolean indicators as candidates for treed partitioning, but ignoring them when it comes to fitting the models at the leaves of the tree. This way, whenever the Boolean indicators are partitioned upon, the design matrix (for the GP or LM) will not contain the corresponding Boolean column and therefore will be of full rank. To implement this scheme, and similar ones to follow, we use the basemax argument to the b* functions in tgp as described by Gramacy and Taddy, (2009). Consider the treed linear model again (btlm2) under this new treatment. In this case the MAP tree does indeed partition on the indicators in an appropriate way—as well as on some other real-valued inputs—and the result is the lower RMSE we desire.

A more high-powered approach would be to treat all inputs as real-valued by fitting a GP at the leaves of the tree (btgp). Binary partitions are allowed on all inputs, and . As in a direct application of the BCART linear model, treating the Boolean indicators as real-valued is implicit in a direct application of the TGP for regression. However, we have already seen that this representation is inappropriate since it is known that the process does not vary smoothly over the and settings of the four Boolean indicators representing the categorical input . Since the design matrices would become rank-deficient if the Boolean indicators were partitioned upon, there is no partitioning on these predictors. As there are large covariance matrices to invert, the MCMC inference is very slow. Still, the resulting fit (obtained with much patience) is better than the Bayesian CART and treed LM ones, as indicated by the RMSE.

We expect to get the best of both worlds if we allow partitioning on the indicators but guard against rank deficient design matrices by ignoring these Boolean indicators for the GP models at the leaves (btgp2). Indeed this is the case, as the indicators then become valid candidates for partitioning.

Finally it is known that, after conditioning on the indicators, the data sampled from Friedman function are well-modeled with a GP using a stationary covariance structure and linear mean. We can use this prior knowledge to build a more parsimonious model. Moreover, the MCMC inference for this reduced model would have lower Monte Carlo error, since it would bypass attempts to partition on the real-valued inputs. These features are facilitated by the splitmin argument to the b* functions, as described by Gramacy and Taddy, (2009). The lower RMSE results for this model (btgp3) corroborate the analysis above.

4.2 Classification TGP on synthetic data

4.2.1 Simple step data in 1d

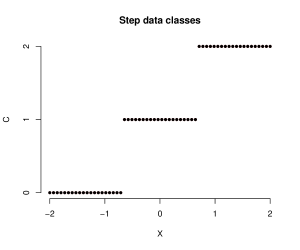

We begin with a trivial classification problem to illustrate the difference between the CTGP and CGP models. We consider a generative model that assigns points less than to class 0, points between and to class 1, and points greater than to class 2. The data set predictors are 60 points distributed evenly between and , inclusive.

This “step” data is depicted in Figure 3. Label the points in order from to . Clearly, we would expect CART and BCART to form a tree with one partition between and and another between and , perfectly dividing the classes and correctly predicting all points outside the data set that do not fall between these dividing points.

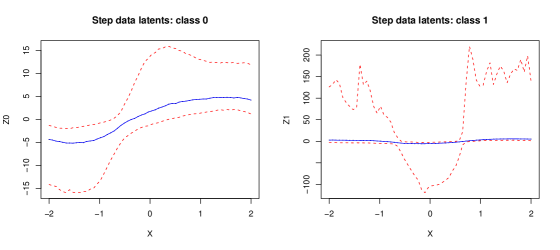

The CGP model likewise captures the pattern of the data but does so without the partition mechanism. In particular, running the CGP on this data returns two sets of latent variables, one set corresponding to class 0 and the other corresponding to class 1. Note that one class label—here class 2—will always be represented by latent variables that are fixed to zero. Otherwise, the model is overdetermined (Section 2).

For the first two classes in the CGP model, the latent variable values are depicted in Figure 4. As expected, the latent variable values, which follow a Gaussian process prior, vary smoothly across the predictor space. Since these values enter into a softmax function to determine class probabilities in the likelihood, smaller values roughly correspond to a higher posterior probability for a particular class. Thus, we see that the latent variables for class 0 mark out a negative-valued region corresponding to the training points in class 0. There is no real distinction, however, amongst the remaining latent variable values for this class. Likewise, the latent variable values for class 1 mark out a negative-valued region corresponding to the training points in class 1, and the remaining latent variable values—representing data in other classes—are all positive and of similar modulus.

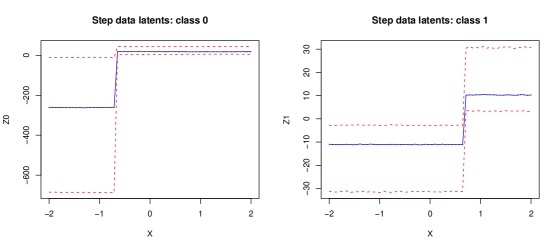

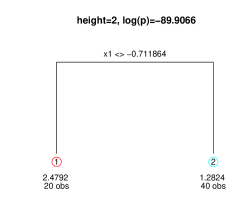

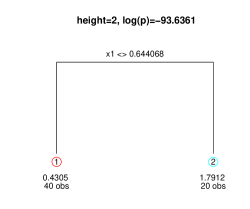

The CTGP model also captures the pattern of the data. But in this very simple example, it reduces almost exactly to BCART. Just as for CGP, there are two sets of latent variables—one set for class 0 and one set for class 1 (Figure 5). Unlike the smooth variation of the CGP latent variables, the CTGP takes advantage of the treed structure and limiting constant model. Thus, the latent variables in class 0 exhibit a sharp divide between and . This divide sets out a negative region for 0-labeled latent variables and sets the remaining latent values at a constant positive value. Similarly, the class 1 latent variables exhibit a sharp divide between and . In contrast to the CGP, the divide in class 1 latent variables here separates the data in classes 0 and 1 from the class 2 data and allows the divide in class 0 latent variables to take care of separating the class 0 data from classes 1 and 2. This difference likely arises from the prior penalty on larger trees. A partition that separates class 1 data from the other two classes would require a tree of height two; the existing tree of height one accomplishes the same task with a more parsimonious representation.

Indeed, we can plot the maximum a posteriori trees of height greater than one for both classes (Figure 6) to verify that the divisions here are (a) caused by treed partitioning and (b) in exactly the places we would expect given the training data. The figure demonstrates that both of these hypotheses are indeed true.

This example illustrates that the CTGP is capable of partitioning on continuous-valued data in practice as well as theory. Nonetheless, this data is rather contrived and simplistic; with noisier data, it is much less likely for real-valued partitioning to occur given our current prior. And the partitioning does not fundamentally change the predictive accuracy of the model. However, it does allow for a much clearer interpretation. The treed partitioning in this example has the same value for intuition as BCART trees whereas the CGP latent variables, while powerful for modeling, are opaque in meaning.

Finally, we see even in this small example the running-time benefits of the CTGP over the CGP. While the latter took seconds to run, the former elapsed only seconds, a speedup of roughly a factor of two.

4.2.2 2d Exponential data

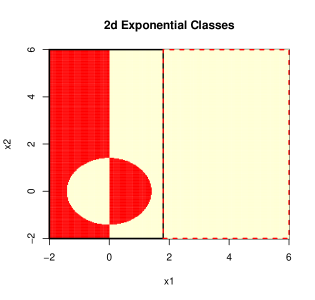

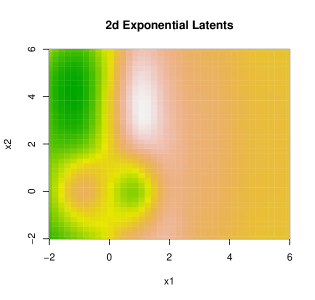

While the CTGP easily partitions categorical inputs, as illustrated with real data in Section 4.3, it can be difficult to manufacture non-trivial synthetic classification data sets that are obvious candidates for partitioning amongst the real-valued inputs. In contrast, it can be quite easy to manufacture regression data which requires a nonstationary GP model. Here we demonstrate how a simple Hessian calculation can convert nonstationary synthetic regression data into class labels that are likely to benefit from partitioning. Consider the synthetic 2d exponential data used to illustrate RTGP by Gramacy, (2007). The input space is , and the true response is given by

| (6) |

In the regression example a small amount of Gaussian noise (with sd ) is added. To convert the real-valued outputs to classification labels we calculate the Hessian:

Then, for a particular input we assign a class label based on the sign of the sum of the eigenvalues of , indicating the direction of concavity at that point. A function like the 2d exponential one (6) whose concavity changes more quickly in one region of the input space than in another (and is therefore well fit by an RTGP model) will similarly have class labels that change more quickly in one region than in another and will similarly require a treed process for the best possible fit.

Figure 7 shows the resulting class labels. Extensions to multiple class labels (up to of them) can be accommodated by a more general treatment of (the signs of) the components of the Hessian.

Overlaid on the plot in Figure 7 (left) is the maximum a posteriori tree—a single split—encountered in the trans-dimensional Markov chain sampling from the CTGP posterior. Here the tree is clearly separating the interesting part of the space, where class labels actually vary, from the relatively large area where the class is constant. As in the regression case, by partitioning, the CTGP is able to improve upon predictive performance as well as computational speed relative to the full CGP model. We trained the classifier(s) on data obtained by a maximum entropy design of size subsampled from a dense grid of 10000 points and calculated the misclassification rate on the remaining 9600 locations. The rate was 3.3% for CGP and 1.7% for CTGP, showing a relative improvement of roughly 50%. CTGP wins here because the relationship between response (class labels) and predictors is clearly nonstationary. That is, no single collection of range parameters is ideal for generating the latent -values that would best represent the class labels through the softmax. However, it is clear that two sets of parameters, for either side of as obtained by treed partitioning, would suffice. The speed improvements obtained by partitioning were even more dramatic. CGP took 21.5 hours to execute 15000 RJ-MCMC rounds whereas CTGP took 2.0 hours, an over 10-fold improvement.

4.3 Classification TGP on real data

The previous experiment illustrates, among other things, treed partitions on real-valued predictors in the classification context. However, a strength of the RTGP demonstrated in Section 4.1 is that it can offer a more natural handling of categorical predictors compared to a GP. With this observation in mind, we shall compare the CTGP to the CGP (as well as neural networks and recursive partitioning) on real data while restricting the treed partitions in the CTGP to the categorical inputs.

For this evaluation, we considered the Credit Approval data set from the UCI Machine Learning database (Asuncion and Newman,, 2007). The set consists of 690 instances grouped into two classes: credit card application approval (‘+’) and application failure (‘–’). The names and values of the fifteen predictors for each instance are confidential. However, aspects of these attributes relevant to our classification task are available. E.g., we know that six inputs are continuous, and nine are categorical. Among the categorical predictors, the number of distinct categories ranges from two to fourteen. After binarization, we have a data set of 6 continuous and 41 binary predictors. The CGP treats these all as continuous attributes. The CTGP forms GPs only over the six continuous attributes and partitions on (and only on) the 41 binary attributes.

We also considered two other standard classification algorithms. First, we used the neural networks (NN) algorithm as implemented by the nnet function available in the nnet library (Ripley,, 2009) in R. For each test, we used the tune function in the R library e1071 (Dimitriadou et al.,, 2010) to simultaneously tune the number of hidden layer units (2, 5, or 10) and the weight decay parameter (base ten logarithm equal to -3.0, -1.5, or 0) based on the training data. The tune function evaluates the classification error for each parameter-set value via a cross-validation on the training data and then selects the optimal parameters. All other settings for nnet parameters were kept at the default.

Second, we used recursive partitioning (RP) as implemented by the rpart function (Therneau and Atkinson,, 2010) in R. Again, for each test, we used the tune function to select the complexity parameter (0.01, 0.02, 0.05, 0.1, 0.2, or 0.5) based on the training data. All other settings were kept at the default.

| Method | Avg | Stddev |

|---|---|---|

| NN | 18.1 | 6.1 |

| RP | 15.2 | 3.8 |

| CGP | 14.6 | 4.0 |

| CTGP | 14.2 | 3.6 |

Our comparison consists of ten separate 10-fold cross-validations for a total of 100 folds. The results are summarized in Table 1. The CTGP offers a slight improvement over the CGP with an average misclassification rate of 14.2%, compared to 14.6%. Similarly, the standard deviation of CGP misclassification across folds was 4.0% while the CTGP exhibited slightly smaller variability with a standard deviation of 3.6%. More impressive is the speed-up offered by CTGP. The average CPU time per fold used by the CGP method was 5.52 hours; with an average CPU time per fold of 1.62 hours, the CTGP showed a more than three-fold improvement.

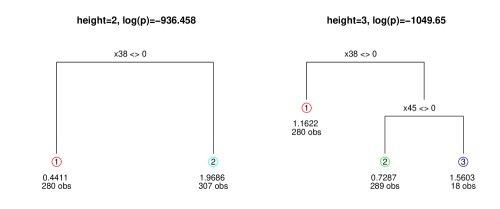

Finally, the interpretative aspect of the CTGP, with an appropriate (treed) handling of the categorical inputs, is worth highlighting. For a particular run of the algorithm on the Credit Analysis data, the MAP trees of different heights are shown in Figure 8. These trees, and others, feature principal splits on the binary predictor, which is a binarization of the two-valued categorical predictor. Therefore, the CTGP indicates, without additional work, the significance of this variable in predicting the success of a credit card application. To extract similar information from the CGP, one would have to devise and run some additional tests—no small feat given the running time of single CGP execution. The figure also shows that the Markov chain visited other trees, including one with a split on the binary predictor. However a comparison of log posteriors (shown in the Figure) and a trace of the heights of the trees encountered in the Markov chain (not shown) indicate that this split, and any others, had very low posterior probability.

5 Discussion

In this paper we have illustrated how many of the benefits of the regression TGP model extend to classification. The components of TGP, i.e., treed models and GPs, have separately enjoyed a long tenure of success in application to classification problems. In the case of the GP, processes are each used as a prior for latent variables, which encode the classes via a softmax function. While the CGP is a powerful method that typically offers improvements over simpler approaches (including treed models), drawbacks include an implicit assumption of stationarity, clumsy handling of categorical inputs, and slow evaluation due to repeated large matrix decompositions. In contrast, the treed methods are thrifty, provide a divide-and-conquer approach to classification, and can naturally handle categorical inputs. Two possible ways of combining the GP with a tree process naturally suggest themselves for, first, partitioning up the input space and thus taking advantage of the divide-and-conquer approach to a nonstationary prior on the latent variables used for classification and, second, handling categorical inputs.

We argued that it is better to work with separate TGP models rather than deal with one treed model with GPs at each leaf. However, a drawback of this (MTGP) approach is that, when there are no (useful) real-valued predictors, then it will behave like BCART. But what results will be an inefficient implementation due to all of the latent variables involved—as the MCMC basically tries to integrate them out. So in this case, a direct implementation via BCART is preferred. However, when mixed categorical and real-valued inputs are present, the combined tree and GP approach allows the appropriate component of the model (tree in the case of categorical inputs, and GP in the case of real ones) to handle the marginal process in each input dimension. The result is a classification model that is speedy, interpretable, and highly accurate, combining the strengths of GP and treed models for classification.

Acknowledgments

This work was partially supported by Engineering and Physical Sciences Research Council Grant EP/D065704/1. TB’s research was supported by a Marshall Scholarship. We would like to thank three anonymous referees, whose many helpful comments improved the paper.

References

- Abrahamsen, (1997) Abrahamsen, P. (1997). “A Review of Gaussian Random Fields and Correlation Functions.” Tech. Rep. 917, Norwegian Computing Center, Box 114 Blindern, N-0314 Oslo, Norway.

- Asuncion and Newman, (2007) Asuncion, A. and Newman, D. (2007). “UCI Machine Learning Repository.”

- Breiman et al., (1984) Breiman, L., Friedman, J. H., Olshen, R., and Stone, C. (1984). Classification and Regression Trees. Belmont, CA: Wadsworth.

- Chipman et al., (1998) Chipman, H., George, E., and McCulloch, R. (1998). “Bayesian CART Model Search (with discussion).” Journal of the American Statistical Association, 93, 935–960.

- Chipman et al., (2002) — (2002). “Bayesian Treed Models.” Machine Learning, 48, 303–324.

- Dimitriadou et al., (2010) Dimitriadou, E., Hornik, K., Leisch, F., Meyer, D., and Weingessel, A. (2010). “e1071: Misc Functions of the Department of Statistics (e1071), TU Wien.” Version 1.5-24. CRAN repository. Maintained by Friedrich Leisch. Obtained from http://cran.r-project.org/web/packages/e1071/e1071.pdf.

- Friedman, (1991) Friedman, J. H. (1991). “Multivariate Adaptive Regression Splines.” Annals of Statistics, 19, No. 1, 1–67.

- Gilks and Wild, (1992) Gilks, W. R. and Wild, P. (1992). “Adaptive rejection sampling for Gibbs sampling.” Applied Statistics, 41, 337–348.

- Gramacy, (2005) Gramacy, R. B. (2005). “Bayesian Treed Gaussian Process Models.” Ph.D. thesis, University of California, Santa Cruz.

- Gramacy, (2007) — (2007). “tgp: An R Package for Bayesian Nonstationary, Semiparametric Nonlinear Regression and Design by Treed Gaussian Process Models.” Journal of Statistical Software, 19, 9.

- Gramacy and Lee, (2008) Gramacy, R. B. and Lee, H. K. H. (2008). “Bayesian treed Gaussian process models with an application to computer modeling.” Journal of the American Statistical Association, 103, 1119–1130.

- Gramacy and Taddy, (2008) Gramacy, R. B. and Taddy, M. A. (2008). tgp: Bayesian treed Gaussian process models. R package version 2.1-2.

- Gramacy and Taddy, (2009) — (2009). “Categorical inputs, sensitivity analysis, optimization and importance tempering with tgp version 2, an R package for treed Gaussian process models.” Tech. rep., University of Cambridge. Submitted to JSS.

- Hastie et al., (2001) Hastie, T., Tibshirani, R., and Friedman, J. (2001). The Elements of Statistical Learning. New York, NY: Springer-Verlag.

- Matérn, (1986) Matérn, B. (1986). Spatial Variation. 2nd ed. New York: Springer-Verlag.

- Neal, (1997) Neal, R. M. (1997). “Monte Carlo implementation of Gaussian process models for Bayesian regression and classification.” Tech. Rep. 9702, Deptartment of Statistics, University of Toronto.

- Neal, (1998) — (1998). “Regression and classification using Gaussian process priors (with discussion).” In Bayesian Statistics 6, ed. e. a. J. M. Bernardo, 476–501. Oxford University Press.

- Qian et al., (2008) Qian, Z., Wu, H., and Wu, C. (2008). “Gaussian process models for computer experiments with qualitative and quantitative factors.” Technometrics, 50, 383–396.

- Rasmussen and Williams, (2006) Rasmussen, C. E. and Williams, C. K. I. (2006). Gaussian Processes for Machine Learning. The MIT Press.

- Richardson and Green, (1997) Richardson, S. and Green, P. J. (1997). “On Bayesian Analysis of Mixtures With An Unknown Number of Components.” Journal of the Royal Statistical Society, Series B, Methodological, 59, 731–758.

- Ripley, (2009) Ripley, B. (2009). “Feed-forward Neural Networks and Multinomial Log-Linear Models.” Version 7.3-1. CRAN repository. Maintained by Brian Ripley. Obtained from http://cran.r-project.org/web/packages/nnet/nnet.pdf.

- Saltelli et al., (2008) Saltelli, A., Ratto, M., Andres, T., Campolongo, F., Cariboni, J., Gatelli, D., Saisana, M., and Tarantola, S. (2008). Global Sensitivity Analysis: The Primer. John Wiley & Sons.

- R Development Core Team, (2008) R Development Core Team (2008). R: A language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Aus. ISBN 3-900051-00-3.

- Stein, (1999) Stein, M. L. (1999). Interpolation of Spatial Data. New York, NY: Springer.

- Therneau and Atkinson, (2010) Therneau, T. M. and Atkinson, B. (2010). “rpart: Recursive Partitioning.” Version 3.1-46. CRAN repository. Maintained by Brian Ripley. Obtained from http://cran.r-project.org/web/packages/rpart/index.html.