Haar Wavelets-Based Approach for Quantifying Credit Portfolio Losses

Abstract

This paper proposes a new methodology to compute Value at Risk (VaR) for quantifying losses in credit portfolios. We approximate the cumulative distribution of the loss function by a finite combination of Haar wavelets basis functions and calculate the coefficients of the approximation by inverting its Laplace transform. In fact, we demonstrate that only a few coefficients of the approximation are needed, so VaR can be reached quickly. To test the methodology we consider the Vasicek one-factor portfolio credit loss model as our model framework. The Haar wavelets method is fast, accurate and robust to deal with small or concentrated portfolios, when the hypothesis of the Basel II formulas are violated.

1 Introduction

It is very important for a bank to manage the risks originated from its business activities. In

particular, the credit risk underlying the credit portfolio is often the largest risk in a bank. The measured

credit risk is then used to assign capital to absorb potential losses arising from its

credit portfolio.

The Vasicek model is the basis of the Basel II IRB approach. It is a Gaussian one factor model such that default

events are driven by a latent common factor that is assumed to follow a Gaussian distribution, also called

Asymptotic Single Risk Factor (ASRF) model. Under this model, loss only occurs when an obligor default in a

fixed time horizon. If we assume certain homogeneity conditions, this one factor model leads to a simple analytic

asymptotic approximation for the loss distribution and Value at Risk (VaR). This approximation works well

for a large number of small exposures but can underestimate risks in the presence of

exposure concentrations.

Concentration risks in credit portfolios arise from an unequal distribution of loans to single borrowers

(name concentration) or different industry or regional sectors (sector or country

concentration). Moreover, certain dependencies as, for example, direct business links between different

borrowers, can increase the credit risk in a portfolio since the default of one borrower can cause the default of

a dependent second borrower. This effect is called default contagion and is linked to both name and sector

concentration.

In credit risk management one is particularly interested in the portfolio loss distribution. Since the portfolio

loss is usually modeled as a sum of random variables, the main task is to evaluate the probability density

function (PDF) of such a sum. The PDF of a sum of random variables is equal to the convolution of the respective

PDFs of the individual asset loss distributions. The evaluation of this convolution is a difficult problem

analytically, is computationally very intensive and in full generality is impractical for any

realistically sized portfolio.

For all these reasons, several methods have been developed in the last years. The saddle point approximation due

to [Mar01a] gives an analytical approximation of the Laplace inversion of the moment generating function

(MGF). This method has been improved by [Mar06] based on conditional independence models.

[Gla07] applies the methodology developed by [Aba00] to the single-factor Merton model.

First, the Bromwich integral is approximated by an infinite series using the trapezoidal rule and second, the

convergence of the infinite series is accelerated by a method called Euler summation. They have shown that the

cumulative distribution function (CDF) is comparatively accurate in small loss region, whereas the accuracy

worsens in the tail region. This is because the infinite series obtained by the Euler summation is an alternating

series, each

term of which has a very large absolute value.

Another approach to numerically invert the Laplace transform has been studied by [Hoo82] and

[Ahn03] consisting in applying the Poisson algorithm to approximate the Bromwich integral by an infinite

series, as in [Aba00] and then use the quotient-difference (QD) algorithm to accelerate the slow

convergence of the infinite series. We will refer to this approach as

the Hoog algorithm. [Tak08]

has applied this methodology to the multi-factor Merton model. The numerical examples presented show that in

contrast with the Euler summation technique, de Hoog algorithm is quite efficient in measuring tail probabilities.

In this paper, we present a novel methodology for computing VaR through numerically inverting the Laplace

Transform of the CDF of the loss function once we have approximated it by a finite sum of Haar wavelets basis

functions. This kind of functions have compact support and so make them useful to study local properties of the

approximated function. Moreover, the CDF of

the loss function is discontinuous, making more suitable this way of approximation.

The remaining parts of the paper are organized as follows. In the next section we present the one-factor Gaussian copula model and we define VaR as the risk measure used to quantify losses in Basel II Accord. In section three we present the basic theory about Haar wavelets basis system used for the approximation detailed in section four. Finally, we show with numerical examples the speed and accuracy of the new method in section five and section six is devoted to conclusions.

2 Portfolio Loss and Value at Risk

To represent the uncertainty about future events, we specify a

probability space with sample space , -algebra ,

probability measure and with filtration satisfying the usual conditions.

We fix a time horizon . Usually equals

one year.

Consider a credit portfolio consisting of obligors. Any obligor can be characterized by three parameters: the exposure at default , the loss given default which without loss of generality we assume to be and the probability of default , assuming that each of them can be estimated from empirical default data. The exposure at default of an obligor denotes the portion of the exposure to the obligor which is lost in case of default. Let be the default indicator of obligor taking the following values

Let be the portfolio loss given by:

where .

To test our methodology we consider the Vasicek one-factor Gaussian copula model as our model framework. The Vasicek model is a one period default model, i.e., loss only occurs when an obligor defaults in a fixed time horizon. Based on Merton‘s firm-value model, to describe the obligor’s default and its correlation structure, we assign each obligor a random variable called firm-value. The firm-value of obligor is represented by a common, standard normally distributed factor component and an idiosyncratic standard normal noise component . The factor is the state of the world or business cycle, usually called systematic factor.

where and , are i.i.d. standard

normally distributed.

In case that for all , the parameter is called the common asset correlation. The

important point is that conditional on the realization of the systematic factor , the

firm’s values and the defaults are independent. From now on, we assume to be constant.

Let us explain in detail the meaning of systematic and idiosyncratic risk. The first one can be viewed as the

macro-economic conditions and affect the credit-worthiness of all obligors simultaneously. The second one represent

conditions inherent to each obligor and this is why they are assumed to be

independent of each other.

In the Merton model, each obligor defaults if its firm-value falls below the threshold level defined by where is the standard normal cumulative distribution function and denotes its inverse function. The probability of obligor ’s default conditional on a realization of is given by

Consequently, the conditional probability of default depends on the systematic factor, reflecting the fact that

the business cycle

affect the possibility of an obligor’s default.

Let be the cumulative distribution function of . Without loss of generality, we can assume and consider

for a certain defined in .

Let be a given confidence level, the -quantile of the loss distribution of in this context is called Value at Risk (VaR). Thus,

Usually the of interest is very close to 1. This is the measure chosen in the Basel II Accord for the

computation of capital requirement, which means a bank that manages its risks with Basel II must to reserve

capital by an amount of

to cover extreme losses.

3 The Haar Basis Wavelets System

Consider the space . For simplicity, we can view this set as a set of functions which

get small in magnitude fast enough as goes to plus and minus infinity.

A general structure for wavelets in is called a Multi-resolution Analysis (MRA). We start with a family of closed nested subspaces

in where

and

If these conditions are met, then there exists a function such that is an orthonormal basis of , where

In other words, the function , called the father function, will generate an orthonormal basis for

each subspace.

Then we define such that . This says that is the space of functions in but not in , and so, . Then (see [Dau92]) there exists a function such that is an orthonormal basis of , and is a wavelets basis of , where

The function is called the mother function, and the are the wavelets functions.

For any function a projection map of onto ,

is defined by

| (1) |

where are the wavelets coefficients and the

are the scaling coefficients. The first part in

(1) is a truncated wavelets series. If were allowed to go to infinity, we would have the full

wavelets summation. The second part in (1) gives an equivalent sum in terms of the scaling functions

. Considering higher values, meaning that more terms are used,

the truncated series representation of our function improves.

To develop our work, we have used Haar wavelets (see [Dau92]). For these wavelets, the space is the set of all functions which are constant on each interval of the form for all integers . Then

and

The unique thing about using wavelets as opposed to Fourier series is that the wavelets can be moved (by the value), stretched or compressed (by the value) to accurately represent a function local properties. Moreover, is nonzero only inside the interval . These facts will be used later to compute the VaR without the need of knowing the whole distribution of the loss function.

|

|

4 Haar wavelets approximation

Let us mention an issue regarding the CDF defined above. Since the loss can take only a finite number of discrete values ( at most) the PDF of the loss function is a sum of Dirac delta functions and then, the CDF is a discontinuous function. Moreover, the stepped form of the CDF makes the Haar wavelets a natural and very well-suited way of approximation.

4.1 Laplace Transform Inversion

Due to the fact that and according to the theory of MRA, we can approximate in by a sum of scaling functions,

| (2) |

and

Recall that in the one-factor model framework, if the systematic factor is fixed, default occurs independently because the only remaining uncertainty is the idiosyncratic risk. The MGF conditional on is thus given by the product of each obligor’s MGF as

Notice that we are assuming non stochastic LGD. Taking the expectation value of this conditional MGF yields the unconditional MGF,

But if is the probability density function of the loss function then the unconditional MGF is also the Laplace transform of :

| (3) |

As we have noticed before,

| (4) |

where is the Dirac delta at that can be thought as a density distribution of a unit of mass concentrated in the point (i.e. , for every test function ). Probabilistically, a distribution, such as (4), corresponds to a situation where only the scenarios are feasible with respective probabilities . Of course these probabilities must be positive and sum up 1, this is,

As it is also well known, in the context of generalized functions, the derivative of the Heaviside step function is a Dirac delta. In this context (and of course in the context of regular functions) we can integrate by parts the expression (3) and using the approximation (2) to conclude that,

| (5) |

where

is the Laplace transform of the basis function .

Observing that and making the change of variable , the expression (5) is the same as

| (6) |

Where we note that for , is analytic inside the disc of the complex plane , since the singularity in is avoidable. Then, given the generating function , we can obtain expressions for the coefficients by means of the Cauchy’s integral formula. This is,

where is a circle about the origin of radius , .

Making the change of variable , ,

| (7) |

Finally, we can calculate the integral in (7) approximately by

means of the trapezoidal rule to obtain the coefficients.

4.2 VaR computation

It can be easily proved that

and

VaR can now be calculated quickly with at most coefficients for each fixed level of resolution of the approximation, due to the compact support of the basis functions. Observe that

Thus, we can simply start searching computing with any bisection like method. If then we compute , otherwise we compute , and so on. Finally, observe that VaR lies between and for a certain .

5 Numerical Examples

In this section we present a comparative study to calculate VaR between the

Wavelet Approximation (WA) method and Monte Carlo (MC).

As it is well known, MC has a strong dependence between the size of the

portfolio and the computational time. As the size increases, MC becomes a

big time consuming method.

The real situation in some financial companies show us that there are strong concentrations in their credit

portfolios. Basel II formulas to calculate VaR are supported under unrealistic hypothesis, such as infinite number

of obligors with small exposures.

For these reasons, we test our methodology with concentrated portfolios. We consider four portfolios ranging from

100 to 10000 obligors with the main numerical results displayed in Table 1. The Wavelet Approximation

with provides accurate results in a few seconds of computational time111Computations have been

implemented in C under a PC with Intel CPU 280 GHz and 496 MB RAM., since the

maximum relative error

in portfolios P1, P2 and P3 is only 0.5%, 1% and 0.7% respectively. The

relative error in portfolio P4 may look somewhat greater than expected (2.5%).

But in this case, performing MC simulations we find that the

VaR obtained is 0.160, being the maximum relative error of 1.2% and showing

again the fast convergence of the WA methodology.

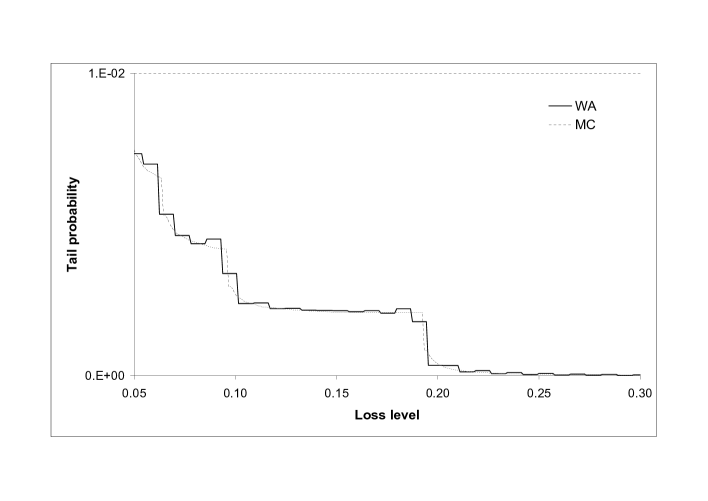

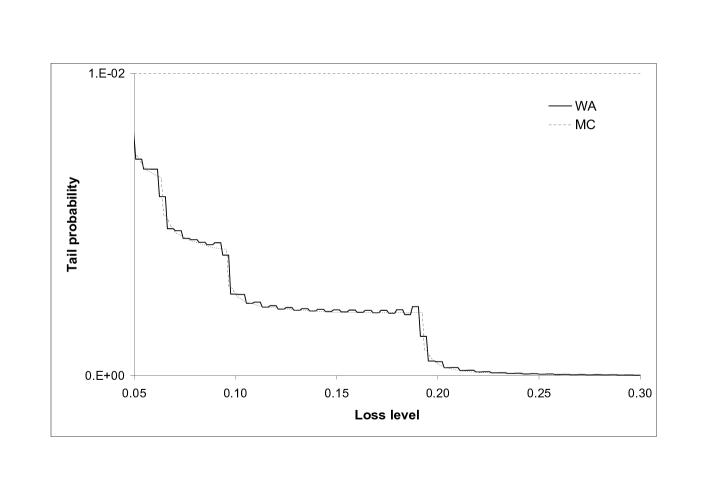

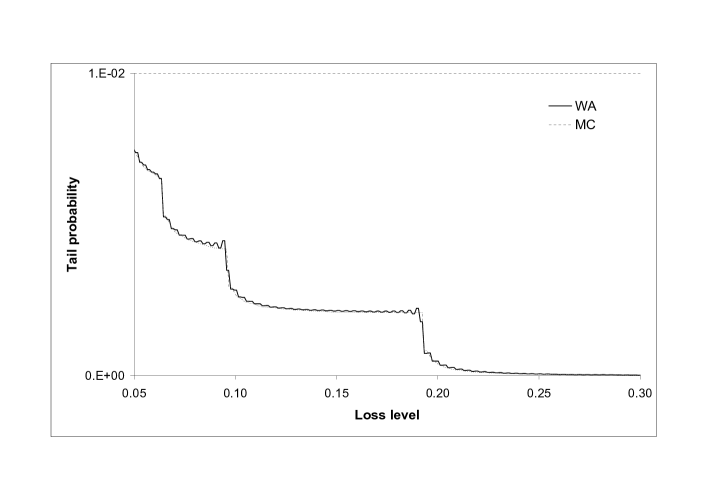

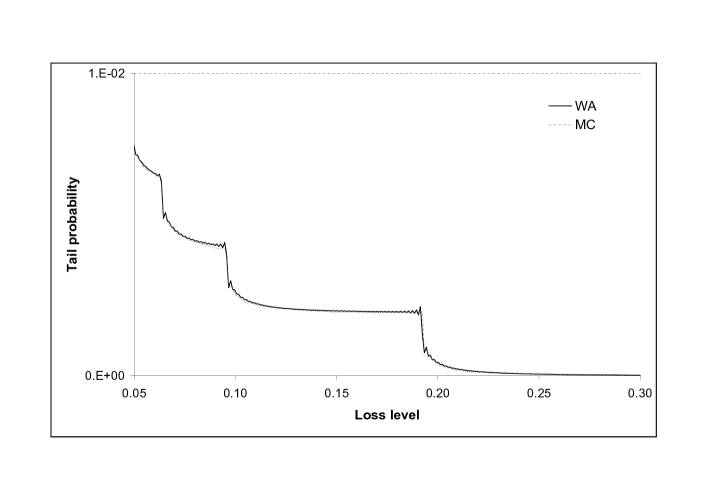

Finally, in order to display the accuracy of Wavelet Approximation, we have considered the tail probabilities of the loss function associated with portfolio P1 using different resolutions ( and 10). The results, compared again with Monte Carlo simulations, can be seen in figures 2,3,4 and 5 respectively. It is remarkable how the Haar wavelets are naturally capable of detecting jumps in the cumulative distribution, making the approximation very precise with not many terms.

| Portfolio | N | WA | WA | MC | |

|---|---|---|---|---|---|

| P1 | 100 | 0.21% | 0.194 | ||

| P2 | 1000 | 1.00% | 0.194 | ||

| P3 | 1000 | 0.30% | 0.141 | ||

| P4 | 10000 | 1.00% | 0.158 |

6 Conclusions

We have presented a numerical approximation to the loss function based on Haar wavelets system. First of all, we

approximate the discontinuous distribution of the loss function by a finite sum of Haar scaling functions, and

then we calculate the coefficients of the approximation by inverting its Laplace transform. Due to the compact

support property of Haar system, only a few coefficients are needed for VaR computation.

We have shown the performance of the numerical approximation in four sample

portfolios. These results among other simulations, show that the

method is applicable to different sized portfolios and very accurate

with short time computations. Moreover, the Wavelet Approximation is robust

since the method is very stable under changes in the parameters of the model.

The stepped form of the approximated distribution makes the Haar wavelets

natural and very suitable for the approximation.

We also remark that the algorithm is valid for continuous cumulative distribution functions, and that it can be used in other financial models without making conceptual changes in the development. For instance, we can easily introduce stochastic loss given default (just changing a bit the unconditional moment generating function) and consider the multi-factor Merton model as the model framework as well.

References

- [Aba96] J. Abate, G.L. Choudhury and W. Whitt (2000). On the Laguerre method for numerically inverting Laplace transforms. Journal on Computing.

- [Aba00] J. Abate, G.L. Choudhury and W. Whitt (2000). An introduction to numerical transform inversion and its application to probability models. Computational Probability, ed. W.K. Grassman, Kluwer, Norwell, MA.

- [Ahn03] J. Ahn, S. Kang and Y. Kwon (2003). A flexible inverse Laplace transform algorithm and its application. Computing 71. 115-131.

- [Art97] P. Artzner, F. Delbaen, J.M. Eber, D. Heath (1997). Thinking coherently. RISK (November), 68-71.

- [Art99] P. Artzner, F. Delbaen, J.M. Eber, D. Heath (1999). Coherent measures of risk. Mathematical Finance 9 (3): 203-228.

- [Dau92] I. Daubechies (1992). Ten lectures on wavelets. CBMS-NSF Regional Conference Series in Applied Mathematics. SIAM.

- [Gie06] G. Giese (2006). A saddle for complex credit portfolio models. RISK (July), 84-89.

- [Gla05] P. Glasserman and J. Li (2005). Importance sampling for credit portfolios. Management Science, 51(11). 1643-1656.

- [Gla07] P. Glasserman and J. Ruiz-Mata (2007). Computing the credit loss distribution in the Gaussian copula model: a comparison of methods. Journal of Credit Risk 3. 33-66.

- [Hoo82] F. de Hoog, J. Knight and A. Stokes (1982). An improved method for numerical inversion of Laplace transforms. SIAM Journal on Scientific and Statistical Computing 3. 357-366.

- [Kal94] M. Kalkbrener (2004). Sensible and efficient capital allocation for credit portfolios. RISK (January), S19-S24.

- [Mar01a] R. Martin, K. Thompson and C. Browne (2001). Taking to the saddle. RISK (June), 91-94.

- [Mar01b] R. Martin, K. Thompson and C. Browne (2001). How dependent are defaults. RISK (July), 87-90.

- [Mar01c] R. Martin, K. Thompson and C. Browne (2001). VaR: who contributes and how much?. RISK (August), 99-102.

- [Mar04] R. Martin (2004). Credit portfolio modeling handbook. Credit Suisse First Boston Limited.

- [Mar06] R. Martin and R. Ordovás (2006). An indirect view from the saddle. RISK (October), 94-99.

- [Tak08] Y. Takano and J. Hashiba (2008). A novel methodology for credit portfolio analysis: numerical approximation approach. www.defaultrisk.com.