Long-term correlations and multifractal analysis of trading volumes for Chinese stocks

Abstract

We investigate the temporal correlations and multifractal nature of trading volume of 22 liquid stocks traded on the Shenzhen Stock Exchange in 2003. We find that the trading volume exhibits size-dependent non-universal long memory and multifractal nature. No crossover in the power-law dependence of the detrended fluctuation functions is observed. Our results show that the intraday pattern in the trading volume has negligible impact on the long memory and multifractality.

keywords:

Econophysics; Trading volume; Intraday pattern; Correlation; MultifractalityPACS:

89.65.Gh, 02.50.-r, 89.90.+n, , ,

1 Introduction

As implied by a well-known adage in the Wall Street that it takes volume to move stock prices, trading volume contains much information about the dynamics of price formation. For instance, the investigation of price-volume relationship has a long history in finance Karpoff-1987-JFQA , attracting more and more interest of physicists, and recently has been studied at the transaction level Chan-Fong-2000-JFE , Lillo-Farmer-Mantegna-2003-Nature , Lim-Coggins-2005-QF , Naes-Skjeltorp-2006-JFinM , Zhou-2007-XXX . In addition, the distributions of trading volumes at different time scales have been found to have power-law right tails for different stock markets Gopikrishnan-Plerou-Gabaix-Stanley-2000-PRE , Eisler-Kertesz-2006-EPJB , Eisler-Kertesz-2007-PA , Queiros-2005-EPL , deSouza-Moyano-Queiros-2006-EPJB , which can account at least partly the power-law tails of returns Gabaix-Gopikrishnan-Plerou-Stanley-2006-QJE , Gabaix-Gopikrishnan-Plerou-Stanley-2007-JEEA , Gabaix-Gopikrishnan-Plerou-Stanley-2008-JEDC , Zhou-2007-XXX . The distributions of trading volumes for Chinese stocks have also been reported to have power-law tails Mu-Chen-Kertesz-Zhou-2009-EPJB , Qiu-Zhong-Chen-2009-PA , Zhou-2007-XXX .

Another important feature of trading volumes is its long-range temporal correlation. Lobato and Velasco used a two-step semiparametric estimator in the frequency domain for the long-memory parameter of daily trading volume for 30 stocks composing DJIA from 1962 to 1994 and find that Lobato-Velasco-2000-JBES , which amount to the Hurst index . Gopikrishnan et al performed detrended fluctuation analyses of trading volume for 1000 largest US stocks over the two-year period 1994-1995 Gopikrishnan-Plerou-Gabaix-Stanley-2000-PRE . They found that, the trading volumes at different time scales (from 15 min to 390 min) show stronger correlations with . Bertram used the autocorrelation and variance plots to investigate the memory effect of high-frequency trading volumes for 200 most actively traded stocks on the Australian Stock Exchange spanning the period January 1993 - July 2002, and found that the average Hurst index is Bertram-2004-PA . Qiu et al conducted similar analysis on 18 liquid Chinese stocks from 2004 to 2006 and reported that , which does not depend on the intraday pattern Qiu-Zhong-Chen-2009-PA .

By investigating the TAQ data sets of 2674 stocks in the period 2000-2002, Eisler and Kertész found that the strength of correlations depends on the liquidity of stocks so that the Hurst index increases logarithmically with the average trading volume or the company size Eisler-Kertesz-2006-EPJB , Eisler-Kertesz-2006-PRE , Eisler-Kertesz-2006 , Eisler-Kertesz-2007-PA , Eisler-Bartos-Kertesz-2008-AP . There is also evidence showing that trading volumes possess multifractal nature in different markets, such as the high-frequency trading volumes of 30 DJIA constituent stocks Moyano-Souza-Queiros-2006-PA , of New York Stock Exchange stocks Eisler-Kertesz-2007-EPL and of the Korean stock index KOSPI Lee-Lee-2007-PA . These properties have not been studied for the Chinese market, which will be investigated in this work.

The paper is organized as follows. We give a brief description of the data in Section 2. The intraday pattern, temporal correlations and multifractal nature of trading volume are studied in Section 3, where we will show that the intraday pattern has negligible impact on the temporal correlations and multifractal nature. Section 4 concludes.

2 Data sets

We analyze an ultra-high-frequency database containing 22 Chinese stocks traded on the Shenzhen Stock Exchange in 2003. It records the sizes of all individual transactions. The 22 stocks investigated in this work cover a variety of industry sectors such as financials, real estate, conglomerates, metals & nonmetals, electronics, utilities, IT, transportation, petrochemicals, paper & printing and manufacturing. Our sample stocks were part of the 40 constituent stocks included in the Shenzhen Stock Exchange Component Index in 2003 Zhou-2007-XXX , Gu-Chen-Zhou-2007-EPJB , Mu-Chen-Kertesz-Zhou-2009-EPJB . The market started with an opening call auction period from 9:15 A.M. to 9:25 A.M. followed by a 5-min cooling period, and then the market entered the double continuous auction period Zhou-2007-XXX , Gu-Chen-Zhou-2007-EPJB , Mu-Chen-Kertesz-Zhou-2009-EPJB . We focus on the trades occurred in the double continuous auction period.

The tickers of the 22 stocks investigated are the following: 000001 (Shenzhen Development Bank Co. Ltd), 000002 (China Vanke Co. Ltd), 000009 (China Baoan Group Co. Ltd), 000012 (CSG holding Co. Ltd), 000016 (Konka Group Co. Ltd), 000021 (Shenzhen Kaifa Technology Co. Ltd), 000024 (China Merchants Property Development Co. Ltd), 000027 (Shenzhen Energy Investment Co. Ltd), 000063 (ZTE Corporation), 000066 (Great Wall Technology Co. Ltd), 000088 (Shenzhen Yan Tian Port Holdings Co. Ltd), 000089 (Shenzhen Airport Co. Ltd), 000429 (Jiangxi Ganyue Expressway Co. Ltd), 000488 (Shandong Chenming Paper Group Co. Ltd), 000539 (Guangdong Electric Power Development Co. Ltd), 000541 (Foshan Electrical and Lighting Co. Ltd), 000550 (Jiangling Motors Co. Ltd), 000581 (Weifu High-Technology Co. Ltd), 000625 (Chongqing Changan Automobile Co. Ltd), 000709 (Tangshan Iron and Steel Co. Ltd), 000720 (Shandong Luneng Taishan Cable Co. Ltd), and 000778 (Xinxing Ductile Iron Pipes Co. Ltd).

Let be the size of the -th trade for a given stock and the number of trades in a fixed time interval . Then the trading volume at time scale is

| (1) |

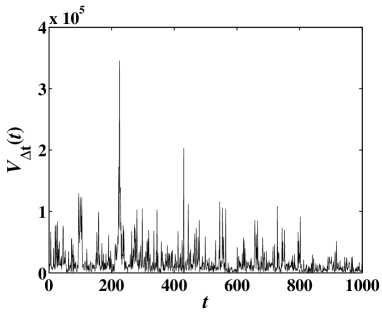

A segment of the time series of 1-min trading volume for stock 000001 is illustrated in Fig. 1.

3 Results

3.1 Intraday pattern

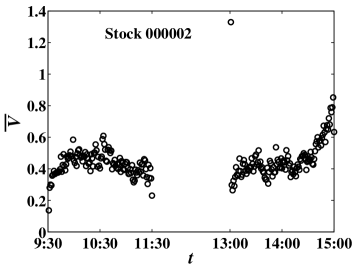

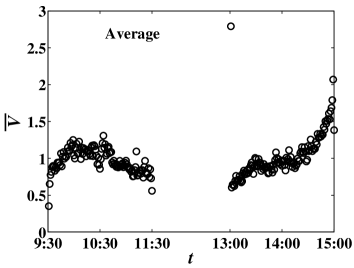

Many researches report that there exist intraday patterns in the trading volume but with different shapes Wood-McInish-Ord-1985-JF , Admati-Pfleiderer-1988-RFS , Stephan-Whaley-1990-JF , Gopikrishnan-Plerou-Gabaix-Stanley-2000-PRE , Lee-Fok-Liu-2001-JBFA , Qiu-Zhong-Chen-2009-PA . Figure 2 gives the intraday pattern of trading volume for stock 000002 and the average for all 22 stocks. The average trading volume increases and then decreases in the morning, with two mild peaks at about 10:00 and 11:00. At the first minute in the afternoon, there is a significant jump, which is simply due to the fact that orders submitted in the noon closing period are executed at 13:00. Afterwards, we see a monotonic increase in the average trading volume. Our result is quite similar to that in Refs. Lee-Fok-Liu-2001-JBFA , Qiu-Zhong-Chen-2009-PA , and the intraday pattern does not has a U-shape.

3.2 Size-dependent correlation in trading volume

We investigate the temporal correlations of trading volumes based on the detrended fluctuation analysis (DFA) Peng-Buldyrev-Havlin-Simons-Stanley-Goldberger-1994-PRE , Kantelhardt-Bunde-Rego-Havlin-Bunde-2001-PA which is a special case of the multifractal DFA method Kantelhardt-Zschiegner-Bunde-Havlin-Bunde-Stanley-2002-PA . If the time series are long-range power-law correlated, the detrended fluctuation function versus could be describe as follow,

| (2) |

where is the length of each segments (time window size) and is the variance of the detrended time series in a given segment after removing a linear trend, while is the generalized Hurst exponent. When , we have

| (3) |

which gives the well-known Hurst exponent .

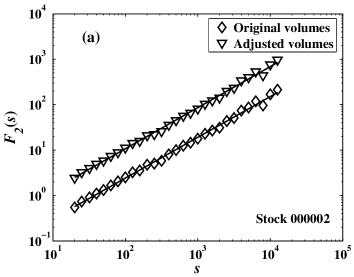

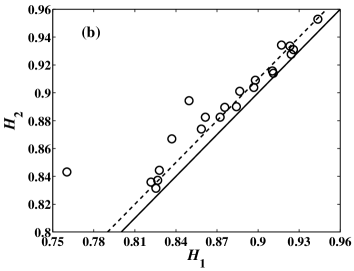

We perform DFA on the 1-min original trading volume data and the deseasonalized (or adjusted) data after removing the intraday pattern for each stock. Fig. 3(a) illustrates the power-law dependence of on for stock 000002. In addition, the two curves are almost parallel, indicating that the intraday pattern has negligible impact on the memory effect of trading volume. The results are similar for other stocks. The slopes of the best fitted linear lines in Fig. 3(a) give the estimates of the Hurst indexes for the original data () and the adjusted data (), which are presented in Table 1. The average Hurst indexes are and . We also plot against in Fig. 3(b) to show that . A careful scrutiny shows that is slightly greater than or equal to . We note that there is no crossover in the DFA plot of trading volume for Chinese stocks, which should be compared to the fact that there is no consensus for the presence of crossover Gopikrishnan-Plerou-Gabaix-Stanley-2000-PRE , Eisler-Kertesz-2007-PA .

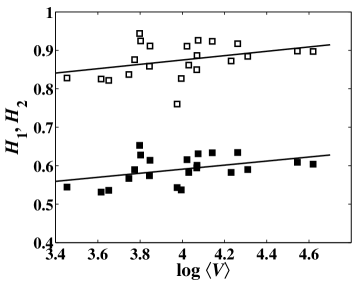

It is important to stress that the Hurst index varies from one stock to another, which depends on the company size or average trading volume of a stock. In Fig. 4, we present the dependence of the Hurst indexes of trading volumes on different logarithmic values of , the sample average of for individual stocks. We find that there is a linear relationship for both original and deseasonalized data:

| (4) |

where the base of log is 10, for the original data, and for the adjusted data. The relation (4) was first observed by Eisler and Kertész for the traded value (also called dollar volume or capital flow, defined by the trading volume times stock price), and they found that for NYSE stocks and for NASDAQ stocks Eisler-Kertesz-2006-PRE , Eisler-Kertesz-2006-EPJB , Eisler-Kertesz-2007-PA . Jiang et al verified the relationship for the traded values of about 1500 Chinese stocks and obtained that Jiang-Guo-Zhou-2007-EPJB . Since large average trading volume corresponds roughly to large company size (or capitalization), our results show that larger company has stronger correlation in the trading volume. We note that the relation (4) is observed for the first time for trading volume in this work.

3.3 Mean-variance analysis

We now conduct the mean-variance analysis on the time series of trading volume. For each stock, the mean and the variance are calculated for different time scales . Since is additive, the mean-variance analysis gives Taylor-1961-Nature

| (5) |

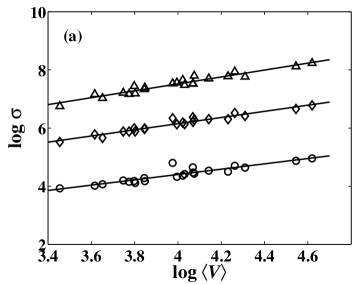

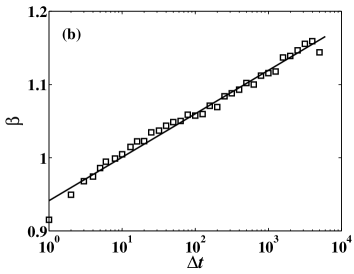

where denotes time averaging. Fig. 5(a) illustrates the power-law dependence of with respect to in double logarithmic coordinates for three time windows 1 min, 0.5 trading day (120 min) and 20 trading days and for the original data. For the deseasonalized data, so that the mean-variance does not apply. The slopes of the best linear fits give the estimates of at different time scales . Fig. 5(b) plots as a function of for the original trading volume data, which has a logarithmic trend,

| (6) |

where . We find that the following relation holds

| (7) |

which has been well verified for the traded values for different stock markets including developed Eisler-Kertesz-2006-EPJB , Eisler-Kertesz-2006-PRE and emerging stock markets Jiang-Guo-Zhou-2007-EPJB .

3.4 Multifractal analysis

In this section, we employ the MF-DFA method Kantelhardt-Zschiegner-Bunde-Havlin-Bunde-Stanley-2002-PA to investigate the multifractal nature of trading volumes. In this procedure, the -th order fluctuation function versus is analyzed for different . We vary the value of in the range from to ( is the length of a series), since becomes statistically unreliable for very large scales , and systematic deviations will be involved for very small scales . The relationship between and the mass scaling exponents in the conventional multifractal formalism based on the partition functions Halsey-Jensen-Kadanoff-Procaccia-Shraiman-1986-PRA , Kantelhardt-Zschiegner-Bunde-Havlin-Bunde-Stanley-2002-PA is formalized as follows,

| (8) |

where is the fractal dimension of the geometric support of the multifractal measure (in our case = 1). According to the Legendre transform Halsey-Jensen-Kadanoff-Procaccia-Shraiman-1986-PRA , we have

| (9) |

providing the estimation of strength of singularity and its spectrum .

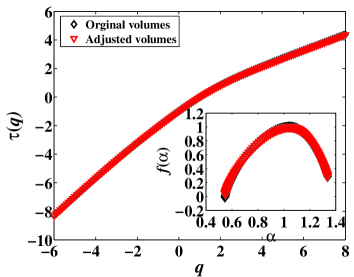

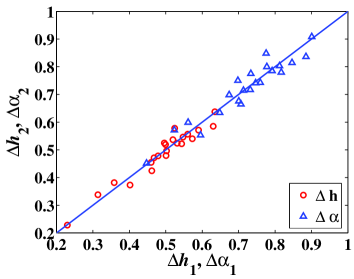

Fig. 6 illustrates an example the multifractal analysis for stock 000002. It is evidence from Fig. 6(a) that is a non-linear function of , which is a hallmark for the presence of multifractality. There is no remarked discrepancy observed between the original and adjusted data of trading volumes. To further clarify the negligible influence of the intraday pattern on the multifractal nature of trading volumes, we calculate two characteristic values and respectively for each time series. The results of and are listed in Table 1. The results are presented in Fig. 6(b). We see that and , indicating that the intraday pattern in the trading volume has negligible impact on the multifractal nature.

4 Conclusion

We have studied the temporal correlations and multifractal nature of trading volume for 22 most actively traded Chines stocks on the Shenzhen Stock Exchange. Detrended fluctuation analysis shows that the trading volumes at different time scales possess non-universal long memory, whose Hurst index depends logarithmically on the average trading volume as . The mean-variance unveils that the scaling exponent depends logarithmically on the time scale as . Empirical evidence shows that , consistent with the theoretical derivation. The investigation of the size-dependent non-universal correlation in trading volume has not been conducted before. Multifractal detrended fluctuation analysis confirms that the trading volume exhibits multifractal nature. Comparing the results obtained from the original trading volume data and the adjusted data after removing the intraday pattern, we conclude that the intraday pattern has negligible impact on the temporal correlations and multifractal nature of trading volumes.

In general, the results obtained for the Shenzhen Stock Exchange in this paper are qualitatively the same as other emerging and developed markets. However, there are some differences. There are studies showing that there is a crossover phenomenon in the power-law relation between the detrended fluctuation function and the scale for some markets, which is not observed for the Shenzhen Stock Exchange. Also, the multifractal spectra differ from one market to another with different singularity width, which is usually determined by the distribution and the correlation structure of the time series showing the idiosyncracy of different markets.

Acknowledgments:

This work was partly supported by the National Natural Science Foundation of China (70501011 and 70502007), the Shanghai Educational Development Foundation (2008SG29), the China Scholarship Council (2008674017), and the Program for New Century Excellent Talents in University (NCET-07-0288).

References

- [1] J. M. Karpoff, The relation between price changes and trading volume: A survey, J. Financ. Quart. Anal. 22 (1987) 109–126.

- [2] K. Chan, W. M. Fong, Trade size, order imbalance, and the volatility-volume relation, J. Financ. Econ. 57 (2000) 247–273.

- [3] F. Lillo, J. D. Farmer, R. Mantegna, Master curve for price impact function, Nature 421 (2003) 129–130.

- [4] M. Lim, R. Coggins, The immediate price impact of trades on the Australian Stock Exchange, Quant. Financ. 5 (2005) 365–377.

- [5] R. Næs, J. A. Skjeltorp, Order book characteristics and the volume-volatility relation: Empirical evidence from a limit order market, J. Financ. Markets 9 (2006) 408–432.

- [6] W.-X. Zhou, Universal price impact functions of individual trades in an order-driven market, http://arxiv.org/abs/0708.3198v2 (2007).

- [7] P. Gopikrishnan, V. Plerou, X. Gabaix, H. E. Stanley, Statistical properties of share volume traded in financial markets, Phys. Rev. E 62 (2000) R4493–R4496.

- [8] Z. Eisler, J. Kertész, Size matters: Some stylized facts of the stock market revisited, Eur. Phys. J. B 51 (2006) 145–154.

- [9] Z. Eisler, J. Kertész, The dynamics of traded value revisited, Physica A 382 (2007) 66–72.

- [10] S. M. D. Queiros, On the emergence of a generalised Gamma distribution: Application to traded volume in financial markets, Europhys. Lett. 71 (2005) 339–345.

- [11] J. de Souza, L. G. Moyano, S. M. D. Queiros, On statistical properties of traded volume in financial markets, Eur. Phys. J. B 50 (2006) 165–168.

- [12] X. Gabaix, P. Gopikrishnan, V. Plerou, H. E. Stanley, Institutional investors and stock market volatility, Quart. J. Econ. 121 (2006) 461–504.

- [13] X. Gabaix, P. Gopikrishnan, V. Plerou, H. E. Stanley, A theory of limited liquidity and large investors causing spikes in stock market volatility and trading volume, J. Eur. Econ. Assoc. 4 (2007) 564–573.

- [14] X. Gabaix, P. Gopikrishnan, V. Plerou, H. E. Stanley, Quantifying and understanding the economics of large financial movements, J. Econ. Dyn. Control 32 (2008) 303–319.

- [15] G.-H. Mu, W. Chen, J. Kertész, W.-X. Zhou, Preferred numbers and the distributions of trade sizes and trading volumes in the Chinese stock market, Eur. Phys. J. B 68 (2009) 145–152.

- [16] T. Qiu, L.-X. Zhong, G. Chen, Statistical properties of trading volume of Chinese stocks, Physica A 388 (2009) in press.

- [17] I. N. Lobato, C. Velasco, Long memory in stock-market trading volume, J. Bus. Econ. Stat. 18 (2000) 410–427.

- [18] W. K. Bertram, An empirical investigation of Australian Stock Exchange data, Physica A 341 (2004) 533–546.

- [19] Z. Eisler, J. Kertész, Scaling theory of temporal correlation and size-dependent fluctuations in the traded value of stocks, Phys. Rev. E 73 (2006) 046109.

- [20] Z. Eisler, J. Kertész, Why do Hurst exponents of traded value increase as the logarithm of company size?, in: A. Chatterjee, B. K. Chakrabarti (Eds.), Econophysics of Stock and Other Markets (Proceedings of the Econophys-Kolkata II), Springer, Berlin, 2006, pp. 49–58.

- [21] Z. Eisler, I. Bartos, J. Kertész, Fluctuation scaling in complex systems: Taylor's law and beyond, Ann. Phys. 57 (2008) 89–142.

- [22] L. G. Moyana, J. de Souza, S. M. D. Queiros, Multi-fractal structure of traded volume in financial markers, Physica A 371 (2006) 118–121.

- [23] Z. Eisler, J. Kertész, Liquidity and the multiscaling properties of the volume traded on the stock market, Europhys. Lett. 77 (2007) 28001.

- [24] K. E. Lee, J. W. Lee, Probability distribution function and multiscaling properties in the Korean stock market, Physica A 383 (2007) 65–70.

- [25] G.-F. Gu, W. Chen, W.-X. Zhou, Quantifying bid-ask spreads in the Chinese stock market using limit-order book data: Intraday pattern, probability distribution, long memory, and multifractal nature, Eur. Phys. J. B 57 (2007) 81–87.

- [26] R. A. Wood, T. H. McInish, J. K. Ord, An investigation of transactions data for NYSE stocks, J. Financ. 40 (1985) 723–739.

- [27] A. R. Admati, P. Pfleiderer, A theory of intraday patterns: Volume and price variability, Rev. Financ. Stud. 1 (1988) 3–40.

- [28] J. A. Stephan, R. E. Whaley, Intraday price change and trading volume relations in the stock and stock option markets, J. Financ. 45 (1990) 191–220.

- [29] Y. T. Lee, R. C. W. Fok, Y. J. Liu, Explaining intraday pattern of trading volume from the order flow data, J. Business Financ. Accounting 28 (2001) 199–230.

- [30] C.-K. Peng, S. V. Buldyrev, S. Havlin, M. Simons, H. E. Stanley, A. L. Goldberger, Mosaic organization of DNA nucleotides, Phys. Rev. E 49 (1994) 1685–1689.

- [31] J. W. Kantelhardt, E. Koscielny-Bunde, H. H. A. Rego, S. Havlin, A. Bunde, Detecting long-range correlations with detrended fluctuation analysis, Physica A 295 (2001) 441–454.

- [32] J. W. Kantelhardt, S. A. Zschiegner, E. Koscielny-Bunde, S. Havlin, A. Bunde, H. E. Stanley, Multifractal detrended fluctuation analysis of nonstationary time series, Physica A 316 (2002) 87–114.

- [33] Z.-Q. Jiang, L. Guo, W.-X. Zhou, Endogenous and exogenous dynamics in the fluctuations of capital fluxes: An empirical analysis of the Chinese stock market, Eur. Phys. J. B 57 (2007) 347–355.

- [34] L. R. Taylor, Aggregation, variance and the mean, Nature 189 (1961) 732–735.

- [35] T. C. Halsey, M. H. Jensen, L. P. Kadanoff, I. Procaccia, B. I. Shraiman, Fractal measures and their singularities: The characterization of strange sets, Phys. Rev. A 33 (1986) 1141–1151.

5 Appendix

| Stock code | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| 000001 | 0.40 | 0.37 | 0.60 | 0.55 | |||||

| 000002 | 0.55 | 0.55 | 0.79 | 0.78 | |||||

| 000009 | 0.56 | 0.56 | 0.81 | 0.80 | |||||

| 000012 | 0.46 | 0.45 | 0.65 | 0.63 | |||||

| 000016 | 0.36 | 0.38 | 0.56 | 0.60 | |||||

| 000021 | 0.52 | 0.58 | 0.78 | 0.85 | |||||

| 000024 | 0.50 | 0.52 | 0.70 | 0.75 | |||||

| 000027 | 0.46 | 0.42 | 0.71 | 0.67 | |||||

| 000063 | 0.57 | 0.54 | 0.82 | 0.78 | |||||

| 000066 | 0.50 | 0.50 | 0.73 | 0.72 | |||||

| 000088 | 0.54 | 0.52 | 0.76 | 0.74 | |||||

| 000089 | 0.63 | 0.64 | 0.90 | 0.91 | |||||

| 000429 | 0.23 | 0.23 | 0.45 | 0.45 | |||||

| 000488 | 0.47 | 0.47 | 0.67 | 0.70 | |||||

| 000539 | 0.63 | 0.59 | 0.88 | 0.84 | |||||

| 000541 | 0.48 | 0.48 | 0.71 | 0.71 | |||||

| 000550 | 0.50 | 0.52 | 0.73 | 0.78 | |||||

| 000581 | 0.52 | 0.54 | 0.78 | 0.80 | |||||

| 000625 | 0.59 | 0.57 | 0.85 | 0.81 | |||||

| 000709 | 0.31 | 0.34 | 0.52 | 0.57 | |||||

| 000720 | 0.50 | 0.48 | 0.70 | 0.68 | |||||

| 000778 | 0.53 | 0.52 | 0.75 | 0.74 |