Recovering a time-homogeneous stock price process from perpetual option prices

Abstract

It is well known how to determine the price of perpetual American options if the underlying stock price is a time-homogeneous diffusion. In the present paper we consider the inverse problem, that is, given prices of perpetual American options for different strikes, we show how to construct a time-homogeneous stock price model which reproduces the given option prices.

doi:

10.1214/10-AAP720keywords:

[class=AMS] .keywords:

.and

1 Introduction

In the classical Black–Scholes model, there is a one-to-one correspondence between the price of an option and the volatility of the underlying stock. If the volatility is assumed to be given (e.g., by estimation from historical data), then the arbitrage free option price can be calculated using the Black–Scholes formula. Conversely, if an option price is given, then the implied volatility can be obtained as the unique that would produce this option price if inserted in the Black–Scholes formula. It has been well documented that if the implied volatility is inferred from real market data for option prices with the same maturity date but with different strike prices, then, typically, a nonconstant implied volatility is obtained. Since the implied volatility often resembles a smile if plotted against the strike price, this phenomenon is referred to as the smile effect. The smile effect is one indication that the Black–Scholes assumption of normally distributed log-returns is too simplistic.

A wealth of different stock price models have been proposed in order to overcome the shortcomings of the standard Black–Scholes model, of which the most popular are jump models and stochastic volatility models. Given a model, option prices can be determined as risk-neutral expectations. However, models are typically governed by a small number of parameters, and only in exceptional circumstances can they be calibrated to perfectly fit the full range of options data.

Instead, there is a growing literature which tries to reverse the procedure, using option prices to make inferences about the underlying price process. At one extreme, models exist which take a price surface as the initial value of a Markov process on a space of functions. In this way the Heath–Jarrow–Morton HJM interest rate models can be made to perfectly fit an initial term structure. Such ideas inspired Dupire Dup to introduce the local volatility model which calibrates perfectly to an initial volatility surface. For a local volatility model, Dupire derived the PDE

where is the European call option price, is time to maturity and is the strike price. Solving for the (unknown) local volatility gives a formula for the time-inhomogeneous local volatility in terms of derivatives of the observed European call option prices.

The local volatility model gives the unique martingale diffusion which is consistent with observed call prices (alternative, nondiffusion models also exist; see, e.g., Madan and Yor MY ). The recent literature (e.g., Schweizer and Wissel SW ) has included attempts to extend the theory to allow for a stochastic local volatility surface. However, it relies on the knowledge of a double continuum of option prices, which are smooth. In contrast, Hobson Hob constructs models which are consistent with a continuum of strikes, but at a single maturity, in which case there is no uniqueness.

In the current article we present a method to recover a time-homogeneous local volatility function from perpetual American option prices. More precisely, we assume that perpetual put option prices are observed for all different values of the strike price, and we derive a time-homogeneous stock price process for which theoretical option prices coincide with the observed ones.

No-arbitrage enforces some fundamental convexity and monotonicity conditions on the put prices, and if these fail, then no model can support the observed prices. If the observed put prices are smooth, then we can use the theory of differential equations to determine a diffusion process for which the theoretical perpetual put prices agree with the observed prices, and our key contribution in this case is to give an expression for the diffusion coefficient of the underlying model in terms of the put prices. It turns out that this expression uniquely determines the volatility coefficient at price levels below the current stock price, but there is some freedom in the choice of the volatility function above the current stock price level. The key idea is to construct a dual function to the perpetual put price, and then the diffusion coefficient can be easily found by taking derivatives of this dual.

The second contribution of this paper is to give time-homogeneous models which are consistent with a given set of perpetual put prices, even when those put prices are not twice differentiable or not strictly convex in the continuation region where it is not optimal to exercise immediately or not strictly convex in the continuation region. Again, the key is the dual function, coupled with a change of scale and a time change. We give a construction of a time-homogeneous process consistent with put prices, which we assume to satisfy the no-arbitrage conditions, but which otherwise has no regularity properties.

One should perhaps note that in reality, put prices are only given in the market for a discrete set of strike prices. Therefore, as a first step one needs to interpolate between the strikes. If a stock price is modeled as the solution to a stochastic differential equation with a continuous volatility function, then the perpetual put price exhibits certain regularity properties with respect to the strike price. Therefore, if one aims to recover a continuous volatility, then one has to use an interpolation method that produces option prices exhibiting this regularity. On the other hand, if a linear spline method is used, then a continuous volatility cannot be recovered. This is one of the motivations for searching for price processes which are consistent with a general perpetual put price function (which is convex, but may be neither strictly convex nor smooth).

While preparing this manuscript we came across a preprint by Alfonsi and Jourdain, now published as AJ08b . The aim of AJ08b , as in this article, is to construct a time-homogeneous process which is consistent with observed put prices. However, the method is different and considerably less direct. Alfonsi and Jourdain AJ08b construct a parallel model such that the put price function in the original model (expressed as a function of strike) becomes a call price function expressed as a function of the initial value of the stock. They then solve the perpetual pricing problem for this parallel model and, subject to solving a differential equation for the optimal exercise boundaries in this model, give an analytic formula for the volatility coefficient. In contrast, the approach in this paper is much simpler and, unlike the method of Alfonsi and Jourdain, extends to the irregular case.

2 The forward problem

Assume that the stock price process is modeled under the pricing measure as the solution to the stochastic differential equation

Here, the interest rate is a positive constant, the level-dependent volatility is a given continuous function and is a standard Brownian motion. We assume that the stock pays no dividends, and we let zero be an absorbing barrier for . If the current stock price is , then the price of a perpetual put option with strike price is

| (1) |

where the supremum is taken over random times that are stopping times with respect to the filtration generated by . From the boundedness, monotonicity and convexity of the payoff, we have the following.

Proposition 2.1

The function satisfies:

-

[(ii)]

-

(i)

for all ;

-

(ii)

is nondecreasing and convex.

If is constant, that is, if is a geometric Brownian motion, then

| (2) |

where and .

Intimately connected with the solution of the optimal stopping problem (1) is the ordinary differential equation

| (3) |

for . This equation has two linearly independent positive solutions which are uniquely determined (up to multiplication with positive constants) if one requires one of them to be increasing and the other decreasing; see, for example, Borodin and Salminen BS , page 18. We denote the increasing solution by and the decreasing one by . In the current setting, and are given by

and

| (4) |

for some arbitrary positive constants and . For simplicity, and without loss of generality, we choose

so that .

Lemma 2.2

The function is strictly decreasing and strictly convex.

Straightforward differentiation yields

| (5) |

so . Similarly,

so is strictly convex.

It is well known that with , we have

| (6) |

where the superindex denotes that the expected value is calculated using . [This result is easy to check by considering and which, since they involve solutions to (3), are local martingales.] Given the assumed time-homogeneity of the process , it is natural to consider stopping times in (1) that are hitting times. Define

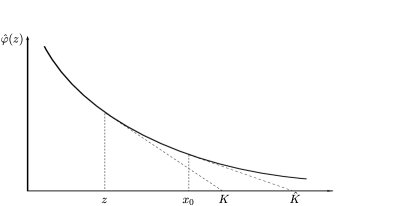

where the last equality follows from (6). Clearly , and, of course, as we show below, there is equality. Since the function is strictly convex, for each fixed there exists a unique for which the supremum in (2) is attained, that is,

| (8) |

Geometrically, is the unique value (less than or equal to ) which makes the negative slope of the line through and as large as possible; see Figure 1.

Define

From the strict convexity of it follows that if , then

and if , then

| (9) |

Moreover, for we have .

Lemma 2.3

The functions and coincide, that is,

| (10) |

As noted above, we clearly have since the supremum over all stopping times is at least as large as the supremum over first hitting times.

For the reverse implication, suppose first that . In that case , by (9). Further, is a nonnegative local martingale and hence a supermartingale. Thus, for any stopping time we have

Hence, .

Finally, let . It follows from the first part that , so Proposition 2.1 implies that , which completes the proof.

If is constant, that is, if is a geometric Brownian motion, then

where . Consequently, the put option price is given by

Straightforward differentiation shows that the supremum is attained for

if , and for if . Consequently, is given by (2).

Under our current assumptions it is not possible to rule out the case where the diffusion hits zero in finite time, although we then insist that zero is absorbing. Note that hits zero in finite time if and only if , in which case we set . When is finite we have and for , and . By the strict concavity of , .

Proposition 2.4

In addition to the properties described in Proposition 2.1, the following statements about the function hold:

-

[(iii)]

-

(i)

satisfies for all and for all ;

-

(ii)

is continuously differentiable on and twice continuously differentiable on ;

-

(iii)

is strictly increasing on with a strictly positive second derivative on .

Statement (i) follows from Lemma 2.3 and the fact that (i) is true for .

Next, consider . By (9) we have

for some . Since maximizes the quotient , we have

| (11) |

It follows from (11) and the implicit function theorem that is continuously differentiable for . Therefore, differentiating (8) gives

where the second equality follows from (11). Equation (2) shows that , so is at and, again, when we have so is also at . Moreover, since is and is away from , it follows that is on . In fact, for we have

where the second equality follows by differentiating (11). Thus, has a strictly positive second derivative on , which completes the proof.

Note that with equality if and only if .

We end this section by showing that can be recovered directly from the put option prices , at least on the domain . To do this, we define the function by

| (13) |

where is given by (10).

Lemma 2.5

[(b)]

Suppose is a nonnegative, decreasing convex function on with and . Define by

| (14) |

-

[(ii)]

-

(i)

is then a nonnegative, nondecreasing convex function with and for .

-

(ii)

and are self-dual in the sense that if, for we define

then on .

Similarly, assume that is a nonnegative, nondecreasing convex function with for all . Also, assume that there exists a point such that for and for . Define

for .

-

[(ii)]

-

(i)

is then a decreasing convex function with and .

-

(ii)

and are self-dual in the sense that if we define

then on .

See Appendix .5.

Corollary 2.6

The function coincides with the decreasing fundamental solution on .

3 The inverse problem: The regular case

We now consider the inverse problem. Let be observed perpetual put prices for all nonnegative values of the strike . The idea is that since satisfies the Black–Scholes equation (3), Corollary 2.6 provides a way to recover the volatility for from perpetual put prices. In this section we provide the details for the case where the observed put prices are sufficiently regular. We assume that the observed put option price satisfies the following conditions (cf. Propositions 2.1 and 2.4 above).

Hypothesis 3.1

-

[(iii)]

-

(i)

for all .

-

(ii)

There exists a strike price such that for all and for all .

-

(iii)

is continuously differentiable on and twice continuously differentiable on .

-

(iv)

is strictly increasing on with a strictly positive second derivative on . Moreover, exists and satisfies .

Motivated by Corollary 2.6, we define the function by

| (15) |

Proposition 3.2

The function can be recovered from by

This is a consequence of part (iii) of Lemma 2.5.

Proposition 3.3

The function is twice continuously differentiable with a positive second derivative, and it satisfies and .

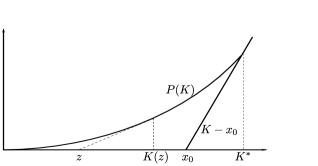

For each there exists a unique for which the supremum in (15) is attained. Geometrically, is the unique value which minimizes the slope of the line through and (cf. Figure 2). Clearly, satisfies the relation

| (16) |

Reasoning as in the proof of Proposition 2.4, one finds that is continuously differentiable on with

| (17) |

and . Differentiating (17) with respect to gives

| (18) |

where the second equality follows by differentiating (16). It follows that is continuous and positive, which completes the proof.

Next, we extend the function to the whole positive real axis so that is convex, strictly positive, twice continuously differentiable with a strictly positive second derivative and satisfies . We also define so that is a solution to the corresponding Black–Scholes equation, that is,

| (19) |

Now, given this volatility function , we are in the situation of Section 2 and can thus define to be the decreasing fundamental solution to the corresponding Black–Scholes equation scaled so that . Moreover, let be the corresponding perpetual put option price as given by (10).

Theorem 3.4

Since the decreasing fundamental solution is unique up to a multiplicative constant and , we have . Proposition 3.2 then yields

which completes the proof.

The inverse problem does not have a unique solution. Indeed, there is plenty of freedom when extending (and thereby also ) for . Note, however, that the volatility is completely determined by the given option prices for values below .

We next show how to calculate the volatility that solves the inverse problem directly from the observed option prices . To do that, note that for each fixed , the supremum in (15) is attained at some for which

| (20) |

| (21) |

and

| (22) |

[cf. (17) and (18)]. Since satisfies the Black–Scholes equation, we get

| (23) |

Consequently, to solve the inverse problem we first determine by

and then, for this we determines from (23).

4 The inverse problem: The irregular case

Again, suppose we are given perpetual put prices and a constant interest rate . Our goal is to construct a time-homogeneous process which is consistent with the given prices. Unlike in the regular case discussed in Section 3, we now impose no regularity assumptions on the function beyond the necessary conditions stated in Proposition 2.1 and condition (i) of Proposition 2.4. For a discussion of the necessity of condition (i) of Proposition 2.4, see Section 9.1.

Hypothesis 4.1

-

[(iii)]

-

(i)

For all we have .

-

(ii)

is nondecreasing and convex.

-

(iii)

There exists such that for and for .

Theorem 4.2

Given satisfying Hypothesis 4.1 and given , there exists a right-continuous (for ), time-homogeneous Markov process with such that

and such that is a local martingale.

Although we wish to work in the standard framework with right-continuous processes, in some circumstances we have to allow for an immediate jump. We do this by making the process right-continuous, except possibly at . At we allow a jump subject to the martingale condition .

Note that condition (iii) of Hypothesis 4.1 excludes the completely degenerate case where . If then, necessarily, to preclude arbitrage, and is consistent with the prices . In this case is an optimal stopping time for every .

Given satisfying Hypothesis 4.1, we define by

| (24) |

for . For some values of , the supremum in (24) may be infinite since may vanish on a nonempty interval , where . By Lemma 2.5, is a convex, decreasing, nonnegative function with . Further,

| (25) |

so . We define

and in the case where we see that for . In fact, if and only if , and it is then easy to see that these two quantities are equal.

We extend the definition of to in any way which is consistent with the convexity, monotonicity and nonnegativity properties and such that . It is convenient to use , for is then continuous at , and is twice continuously differentiable and positive on .

Given , define via

so that if is differentiable we have . Then, is a concave, increasing function, which is continuous on . (It will turn out that is the scale function, which explains the choice of label.) The function has a well-defined inverse , and if then we extend the definition of so that for . Note that is a convex, nondecreasing function with . Also, define . Then, is decreasing and convex with .

For geometric Brownian motion we have and if , and and if . Moreover,

and

for . If , then the corresponding formulae are , , , and .

Recall that a scale function is only determined up to a linear transformation. The choice is arbitrary, but extremely convenient, as it allows us to start the process , defined below, at zero. The choice is simple, but a case could be made for the alternative normalization for which . Multiplying by a constant has the effect of modifying the construction defined in the next section, but only by the introduction of a constant factor into the time changes. It is easy to check that this leaves the final model unchanged.

Our goal is to construct a time-homogeneous process which is consistent with observed put prices and such that is a (local) martingale. In the regular case we have seen how to construct a diffusion with these properties. We now have to allow for more general processes, perhaps processes which jump over intervals, or perhaps processes which have “sticky” points. One very powerful construction method for time-homogeneous, martingale diffusions is via a time change of Brownian motion, and it is this approach which we exploit.

5 Constructing time-homogeneous processes as time changes of Brownian motion

In this section we extend the construction in Rogers and Williams RW2 , Section V.47, of martingale diffusions as time changes of Brownian motion; see also Itô and McKean IM , Section 5.1. The difference from the classical setting is that the processes defined below may have “sticky” points and may jump over intervals. Since diffusions are continuous by definition, the resulting processes are not diffusions, but one might think of them as “generalized diffusions” (Kotani , or “gap diffusions” Knight ), and they are “as continuous as possible.”

Let be a Borel measure on and let be a filtration supporting a Brownian motion started at with local time process . Define to be the left-continuous increasing additive functional

| (26) |

and let be the right-continuous inverse of , that is,

Note that is a nondecreasing process, so is well defined, and is an -stopping time for each time . Set and, for set and . Note that is right-continuous, except possibly at . The process is a time-changed Brownian motion adapted to the filtration and subject to mild nondegeneracy conditions on (see Lemma 5.1 below), and the processes and are local martingales. Further, if then and , so that is a weak solution to , and is a diffusion in natural scale. Similarly, if in an interval, then solves in this interval. The measure is called the speed measure of , although, as pointed out by Rogers and Williams, is large when moves slowly.

The measure may have atoms, and it may have intervals on which it places no mass. If there is an atom at then whenever , and then the time-changed process is “sticky” there. Conversely, if places no mass in then is constant on any time-periods that spends in this interval, and the inverse time change has a jump. In particular, spends no time in this interval. If then for any greater than the first hitting time by of level . In that case, so that if hits , then is absorbing for . The other possibility is that tends to this level without reaching it in finite time.

Define and via

The cases where or correspond to the degenerate case mentioned in the previous section, and we exclude them. The following lemma provides a guide to sufficient conditions for a time change of Brownian motion to be a local martingale and therefore provides insight into the constructions of local martingales via time change that we develop in the next section.

Lemma 5.1

Suppose that either or charges for each , and, further, that either or charges for each . Then, is a local martingale.

See Appendix .6.

6 Constructing the model

We now show how to choose the measure which gives the process we want. Define via

| (27) |

where is the measure defined by the second order distribution derivative of , and let for in the case where and . Similarly, in the case where we set for . Where is absolutely continuous it follows that has a density with respect to Lebesgue measure, but, more generally, (27) can be interpreted in a distributional sense.

Now, for this we can use the construction of the previous section to give a process . If we set , then, subject to the hypotheses of Lemma 5.1, is a local martingale, so that is a scale function for . The process is our candidate process for which the associated put prices are given by .

For geometric Brownian motion,

for . In the case this simplifies to

where . Then, , , for a Brownian motion and .

If the put price satisfies the regularity conditions of Hypothesis 3.1, then the scale function and its inverse are and satisfy

and

Moreover, so that

| (28) |

Consequently, the speed measure is given by

and the diffusion is the solution to the stochastic differential equation

Applying Itô’s formula to yields

where we use (28) for the final equality. We thus recover the diffusion model from the regular case described in Section 3.

Recall that and let be the first explosion time of . Note that by construction is continuous for and left-continuous at . Since is infinite outside the interval we also have the expression . The inverse scale function is convex on , but may have a jump (from a finite to an infinite value) at . In that case we take it to be left-continuous at so that we may have is finite.

For , define and .

Lemma 6.1

and are -local martingales.

Sketch of proof Suppose that is twice continuously differentiable with a positive second derivative. Then, is twice continuously differentiable. For , applying Itô’s formula to gives

But, by definition, , so is a local martingale, as required.

A similar argument can be provided for the process . For the general case, see the Appendix.

Since and are nonnegative local martingales on they converge almost surely to finite values, which we label and . In particular, if , then . However, if then there are several cases. The fact that a nonnegative local martingale converges means that we cannot have both and . Instead, if then and . If and , then , whereas if and , then typically has a nontrivial limit. Similar considerations apply to .

Recall that is the right-continuous inverse of and define the time-changed processes and . Note that these processes are adapted to and that, at least for , we have , and .

If then , and is defined for all .

If then we may have . In this case either , whence is defined for all as before, or . Then, and we set for all . It follows that for all , and 0 is an absorbing state.

Similarly, if then we may have . Then, either , whence is defined for all , or . In the latter case, if and then . We set for all , and it follows that for , . Thus, for , grows deterministically. An example of this situation is given in Example 8.4 below. (In fact, the case where , which depends on the behavior of the scale function to the right of , can always be avoided by a suitable choice of the extension to .)

We want to show how and inherit properties from . The key idea below is that, loosely speaking, a time change of a martingale is again a martingale. Of course, to make this statement precise we need strong control on the time change. (Without such control the resulting process can have arbitrary drift. Indeed, as Monroe Mon has shown, any semimartingale can be constructed from Brownian motion via a time change.) We have the following result, the proof of which is given in the Appendix.

Corollary 6.2

The process is a local martingale.

We can perform a similar analysis on and and use similar ideas to ensure that is defined on . The proof that is a local martingale mirrors that of Corollary 6.2.

Corollary 6.3

The process is a local martingale.

7 Determining the put prices for the candidate process

Recall the definitions of , and via , and . Suppose that is constructed from and a Brownian motion using the time change and construct the candidate price process via . By Corollary 6.2, the discounted price is a (local) martingale. To complete the proof of Theorem 4.2 we need to show that for the candidate process , the function

is such that for all .

Unlike the regular case, the process that we have constructed may have jumps. For this reason, for we modify the definition of the first hitting time so that .

Theorem 7.1

The perpetual put prices for are given by .

Fix . Suppose first that is such that is strictly increasing whenever the Brownian motion takes the value . Then, . More generally, the same is true whenever for every . By Corollary 6.3 we have that is a local martingale, and is bounded on so it follows that is a bounded martingale and . Hence,

Otherwise, fix and . It must be the case that is linear on , bounded on and

It follows that

| (29) |

[Clearly, if , then , so the supremum cannot be attained for such an .]

To prove the reverse inequality, we first claim that the left derivative of the convex function satisfies

| (30) |

To prove (30), first note that it follows from (25) that

Conversely, note that for each there exists a nonempty interval on which

| (31) |

To see this, let be small and draw the tangent line to that passes through the point . Let be the -coordinate of the point of intersection between the tangent line and the -axis. Then, for all we have that the line through and is below the graph of . Consequently, (31) holds. Therefore, for we have

Thus, since is arbitrary, so (30) follows.

We next claim that for each fixed we have

| (32) |

for all . Clearly, this holds for and for . Similarly, if , then it follows from (30) and the convexity of that

It follows from (32) and Corollary 6.3 that for any stopping rule we have

Hence, for and, in view of (29), .

For it follows from , the convexity of and Hypothesis 4.1 that , which completes the proof.

8 Examples

The following examples illustrate the construction of the previous sections. The list of examples is not intended to be exhaustive, but rather indicative of the types of behavior that can arise. In each example we assume .

8.1 The smooth case

We have studied the case of exponential Brownian motion throughout. It is very easy to generate other examples, for example, by choosing a smooth decreasing convex function [with and ] and defining other quantities from .

8.2 Kinks in

If the first derivative of is not continuous, then we find that is linear over an interval , say. Then, is constant on this interval and is linear over the interval . It follows that does not charge this interval, so is constant whenever , and has a jump. then jumps over the interval , and spends no time in .

Example 8.2.

Using (24) we find that

(strictly speaking, there is some freedom in the choice of for , but the power function is a natural choice). Over the region is given by linear interpolation. The corresponding scale function is linear on and in the construction of , assigns no mass to . The process is a generalized diffusion with diffusion coefficient given by for , for and for .

8.3 Linear parts to

In this case, the derivative of is discontinuous at a point say. Then, is also discontinuous at this point, and is discontinuous at . It follows that has a point mass at , and that includes a multiple of the local time at .

Example 8.3.

Suppose that satisfying Hypothesis 4.1 is given by

is then convex, but is linear on the interval . We have

where we have chosen to extend the definition of to in the natural way. Then, for and otherwise. It follows that is everywhere convex, but has a discontinuous first derivative at , and that the corresponding measure has a positive density with respect to Lebesgue measure and an atom of size at . In the terminology of stochastic processes, the process is “sticky” at this point; for a discussion of sticky Brownian motion, see Amit Ami or, for the one-sided case, see Warren War .

If is piecewise linear (e.g., if is obtained by linear interpolation from a finite number of options), then is piecewise linear, is piecewise linear, is piecewise linear and consists of a series of atoms. As a consequence the process is a continuous-time Markov process on a countable state space [at least while ], in which transitions are to nearest neighbors only. Holding times in states are exponential and the jump probabilities are such that is a martingale.

In turn this means that is a continuous-time Markov process on a countable set of points (at least while ).

Example 8.4.

Suppose

This is consistent with a situation in which only two perpetual American put options trade, with strikes and and prices and , in which case we may assume that we have extrapolated from the traded prices to a put pricing function which is consistent with the traded prices. The function

is a possible choice of . Then,

The inverse of is given by

The corresponding measure assigns no mass to the intervals and but has a point mass of size at . The corresponding process has state space and is such that:

-

•

at , jumps to or 2 with probabilities and , respectively;

-

•

if ever then thereafter;

-

•

zero is an absorbing state for .

To examine what happens if ever reaches , note that and (where the superscript denotes local time at rather than an inverse) and then

where we have used the known density of (cf. page 213 in BS ). This implies that if ever reaches , then it stays there for an exponential length of time, rate , and jumps to 2 with probability and zero with probability .

Note that for the continuous-time Markov process , conditional on we have

Also, for this process

so we recover the put price function given at the start of the example.

8.4 Positive gradient of at zero [i.e., ]

In this case. It follows that and the resulting diffusion can hit zero in finite time. Recall that the diffusion is constructed so that 0 is an absorbing endpoint.

Example 8.5.

Suppose that

Then, and so that .

The following example covers the case of mixed linear and smooth parts of and shows an example where reflection, local times and jumps all form part of the construction.

Example 8.6.

Suppose satisfies

Note that has a jump at . We have for and for . We assume this formula also applies on . Then,

and

Consequently, for , no mass is assigned to the interval and for . It follows that for we have , and then

| (33) |

at least until the first hitting time of . To allow for behavior at the general construction includes a local time reflection and a compensating downward jump are added at instants when . The jump takes the process to zero, where it is absorbed.

Alternatively, the process can be formalized as follows. Let be the infimum process given by . By Skorokhod’s lemma, is then a reflected Brownian motion [reflected at the level ] and .

Let be a Poisson process with rate , independent of , and let be the first event time. The compensated Poisson process and the compensated Poisson process stopped at the first jump are then martingales. The time change is also a martingale.

Take and define via and

Note that at the first jump time of the time-changed Poisson process, jumps from to zero.

By construction, is a martingale.

8.5 is zero on an interval

Now, consider the case where for . We then find that for , where . Depending on whether the right derivative is zero or positive, may be infinite or finite. In the former case we have that does not reach in finite time. In the latter case does hit in finite time.

The first example is typical of the case where or, equivalently, where there is smooth fit of at .

Example 8.7.

Suppose and that solves

is then continuous and for we have . We also have for . As usual, there is some freedom when extending to , but for definiteness we assume that the formula applies there as well.

It follows that . Note that since we have that (the first hitting time of ) is infinite. Hence,

is consistent with the observed put prices, and since the process never hits it is not necessary to describe it beyond .

Now, consider the other case where .

Example 8.8.

Suppose and that solves

then has a jump at .

We have for and for , and we assume that this formula also applies on . Then, for , and

Then, for , and for . Consequently, the time change is a linear combination of and , where is the amount of time spent by the Brownian motion above before time .

It follows that for , . As before we have

| (34) |

It is easy to check using Itô’s formula that is a martingale in this case. The process is “sticky” at (this time in the sense of a one-sided sticky Brownian motion; see Warren War ) and this property is inherited by .

There is a third case, where , but .

Example 8.9.

Suppose for [and for ]. Equivalently,

For we then have

It follows that although can hit , the volatility at this level is zero, and the drift alone is sufficient to keep .

8.6 Kink in at : and

In this case is constant on an interval . This case is analogous to the one discussed in Section 8.2.

9 Extensions

9.1 No options exercised immediately

In Hypothesis 4.1, in addition to (i) and (ii), which are enforceable by no-arbitrage considerations, we also assumed (iii) that there exists a finite strike such that for all strikes the put option is exercised immediately. Since is equivalent to it is apparent from the expression in (5) that provided is finite on some interval where or, equivalently, gives mass to some interval where , this property will hold. However, it is interesting to consider what happens when this fails.

Suppose that for all and that . Then, , but is strictly decreasing on . The measure places no mass on , the process spends no time on and never takes values above . In particular, is reflected (downward) at . The resulting model is consistent with observed option prices, but not with the assumption that the discounted price process is a (local) martingale. However, by allowing nonzero dividend rates, we can find a model for which the ex-dividend price process is a martingale and for which the model prices are given by ; see Section 9.3 below.

Now, suppose . If then and we have an extreme example which falls into this setting. For as specified above we have that on . The measure places no mass on and on this region. Except for time 0, the process spends no time in and jumps instantly to , and thereafter spends no time above this point. Alternatively, if is not specified, then this case can be reduced to the previous case by assuming .

9.2 Nonzero dividend processes

Until now, we have assumed that dividend rates are zero. However, if dividend rates are a prespecified function of the asset price, then our method adapts in a straightforward manner.

Given put prices we recover exactly as before from the representation (15). The unknown volatility and are then related via the modified version of (3):

| (35) |

where denotes the dividend rate. [We are assuming that under the pricing measure, is governed by the stochastic differential equation , where is a known function.] The candidate is then given by

| (36) |

at least where this quantity exists.

Since is convex by construction, a necessary condition for the prices to be consistent with some model with dividend rate is that . Then, in smooth cases, where the existence of the diffusion with volatility can be guaranteed, the analysis is complete. However, if is not strictly convex and twice differentiable, then some care may be needed to define the diffusion associated with the candidate given in (36).

In keeping with our analysis in the previous sections, the most natural approach for defining the (potentially generalized) one-dimensional diffusion is via scale and speed. Note that if is sufficiently regular and is the operator

then . Moreover, we can find a second linearly independent solution of by the ansatz . This leads to the ODE

which gives the unknown and its derivative in terms of and and which has solution

Note that the last expression is in terms of the dual function and does not involve directly.

It is easily checked that the derivative of the scale function is given by the Wronskian, so . As before, the scale function can be used to determine the inverse scale function and measure . In turn, can be used to determine the time change and is given by the formula where is inverse to . Thus, in principle, the methods of this article extend directly to the case with dividends, even in the irregular case [although further work is necessary if is not strictly convex below , whence is not continuous, and the integral in (9.2) is not well defined]. However, we will not complete the analysis in this case and instead will just make a remark and give a couple of examples.

Whereas when dividends are zero we have (e.g., from Lemma 2.2) that is convex, this is not always the case when dividends are positive. This means that the duality between and is more subtle. A convex will lead to a convex and thence to a model which is consistent with the perpetual put prices . However, starting with a model for which is not convex, we can still derive option prices from expressions such as (2), but if we now try to recover the model from those prices, the duality lemma will lead to a function . Expressed differently, in the case with dividends it is possible to have many time-homogeneous diffusion models for which put prices are identical.

Example 9.1.

Suppose dividends are proportional so that with . Suppose further that and is given by

| (38) |

where for some positive .

Then, . It follows that . In this case it is clear that is exponential Brownian motion and it is not necessary to calculate the scale function. However, a scale function can easily be computed and is given by , where .

Example 9.2.

Suppose that, as in Example 8.2, and is given by

This time, however, we assume that there are proportional dividends with constant of proportionality (with ). As in Example 8.2, we find that (with )

Then, from and (9.2) we find that is linear over and, more generally, a choice of can be obtained by integrating

where now and .

9.3 Time-homogeneous processes with known volatility and unknown interest rate or unknown dividend processes

In the main body of the paper we have assumed that the interest rate is a given positive constant, that dividend rates are zero and that is a function to be determined. In the last section we generalized this analysis to allow for a known, nonzero, dividend rate. We will now argue that the same ideas can be used to find other time-homogeneous models consistent with observed perpetual put prices, whereby the volatility function is given, and either a state-dependent dividend rate or a state-dependent interest rate is inferred.

Suppose has dynamics . Given put prices as before, define via . The relationship between and the characteristics of the price process are then such that solves , where is given by

Note that we now allow for any of , or to depend on . Until now we have assumed that is constant and is zero (except in the last section, where was known but nonzero) and solved for , but we can alternatively assume that is a given function and is a positive constant, and solve for , or assume that and are given, and solve for .

For example, if and are given constants, then the dividend rate process is given by

If is negative, this should be thought of as a convenience yield.

By allowing for dividend processes which are singular with respect to calendar time and which are instead related to the local time of at level , it is possible to construct candidate price processes which spend no time above . For example, if is the local time at of , and if

then reflects at 1, and if for , then . This gives an example of a model consistent with the class of option prices described in Section 9.1.

9.4 Recovering the model from perpetual calls

The perpetual American call price function must be nonincreasing and convex as a function of the strike , and must satisfy the no-arbitrage bounds .

If there are no dividends (and if is a martingale), then the perpetual call prices are given by the trivial function .

So, suppose instead that the (proportional) dividend rate is positive. Let be the increasing positive solution to

normalized so that . Then, for , , and call prices in a model where are given by

Suppose solves with . Then, where and

Note that since we have . Note also that .

The corresponding call prices are given by

which for gives , and for gives

The example discusses the forward problem, but the discussion of the inverse problem is similar to that in the put case. Given perpetual call prices , for we can define via and then construct a triple so that

By combining information from put and call prices, it is possible to determine a candidate model which simultaneously matches both puts and calls. The information contained in the perpetual puts determines the volatility below and the information contained in the perpetual calls determines the volatility above . However, for this candidate model to return the put and call prices, there is an additional consistency condition. For a discussion of this condition in the smooth case, see Alfonsi and Jourdain AJ08b , Proposition 4.6.

Appendix: Proofs

.5 Duality

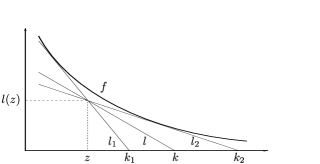

{pf*}Proof of Lemma 2.5 It is clear that is nonnegative and nondecreasing since is positive and nonincreasing. The lower bound on follows from choosing in (14), and the upper bound follows since is nonincreasing. To show that is convex, first note that is minus the reciprocal of the slope of the tangent of the function which passes through the point .

For two given points and with , let and be the corresponding tangent lines. Let for some , and let be the line through the point and the intersection point of and (cf. Figure 3).

If the intersection point is denoted , then the convexity of guarantees that

which proves that is convex.

To prove the self-duality, let . By the definition of we have that for all . Consequently,

For the reverse inequality, let and let be a tangent line to through the point (such a tangent is not necessarily unique if has a kink at ). Assume that the point where intersects the -axis is given by . Then, , so

which completes the proof of (ii). The proof of (b) can be constructed along the same lines.

.6 Time changes of local martingales

Proposition .1

Suppose is a martingale with respect to the filtration , and is an increasing process such that is a finite stopping time with respect to for each . Define and . In general is not a martingale. However, if is a bounded martingale, then is a bounded martingale.

Given a Brownian motion , for , let be the first hitting time of level . Then, defined via is not a martingale.

However, if is bounded, then , by optional sampling.

Suppose now that we are in the setting of Section 5, where is constructed from the Brownian motion . In particular, is an increasing additive functional of , and is the right-continuous inverse to .

Proof of Lemma 5.1 Intuitively, a time change of Brownian motion is a local martingale, but if the additive functional is constant when is in then the resulting process spends no time above and reflects there. To maintain the local martingale property we need either that the time-changed process never gets to , or that there are arbitrarily large values at which is strictly increasing.

If is a bounded interval, then and is a bounded martingale, by Proposition .1.

Now, suppose and suppose that for each , assigns mass to every set and .

We have with equality when is strictly increasing at . Let and be two sequences converging to and , respectively, so that assigns mass to any neighborhood of and , and set . Then, is strictly increasing at . Set . Then, . Note that increases to infinity almost surely, and hence . Under our hypothesis, given by

is a bounded martingale. Hence, is a localization sequence for .

The mixed case can be treated similarly.

Proof of Lemma 6.1 For , set and write . If is not differentiable at then we take the right derivative, which exists since is convex. (We use a similar convention for , and defined below.) Then,

and, as usual, for . Note that in the case where is not twice differentiable, we have so that exists in a distributional sense.

We have and

Let be the first explosion time of . Then, by the Itô–Tanaka formula (e.g., Revuz and Yor RY , Theorem VI.1.5), for ,

Thus, , where denotes the Doléans exponential, and is a local martingale. It follows that is a local martingale.

Now, define and

Again, exists in the distributional sense, even if is not continuous. By exactly the same argument as above, we find that and is a local martingale.

It remains to show that . Define so that is continuous and right-differentiable. [We write for this right-derivative when the derivative is not well defined.] Then, and

We have that is (right-) differentiable, even if separately and are not, and

Finally, since is a bounded continuous function with compact support for each fixed , we conclude that .

Proof of Corollary 6.2 Recall that in our setting, defined via (26) grows without bound and is continuous, at least until hits or . Thus, if denotes the first explosion time of , then the inverse function is defined for every and for . Then, using the extension of the definition of beyond as necessary, we have

Recall that is extended to in such a way that . Therefore, either and assigns infinite mass to all points , or and there exists a sequence such that assigns mass to any neighborhood of .

Suppose that the second case obtains. If then , otherwise . On , is strictly increasing at and . Set

| (39) |

where the second line is redundant if . Then, is such that and is a reducing sequence for .

Now, suppose and . Choose such that assigns mass to any neighborhood of . Then, on , we have, by the argument after Lemma 6.1, that almost surely, and the argument proceeds as before with given by (39) being a reducing sequence.

Finally, suppose and . Then, is bounded by and is a martingale.

Acknowledgments

We thank Eberhard Mayerhofer and an anonymous referee for their careful reading.

References

- (1) {barticle}[mr] \bauthor\bsnmAlfonsi, \bfnmAurélien\binitsA. and \bauthor\bsnmJourdain, \bfnmBenjamin\binitsB. (\byear2009). \btitleExact volatility calibration based on a Dupire-type call-put duality for perpetual American options. \bjournalNoDEA Nonlinear Differential Equations Appl. \bvolume16 \bpages523–554. \biddoi=10.1007/s00030-009-0027-8, mr=2525515 \endbibitem

- (2) {barticle}[mr] \bauthor\bsnmAmir, \bfnmMadjid\binitsM. (\byear1991). \btitleSticky Brownian motion as the strong limit of a sequence of random walks. \bjournalStochastic Process. Appl. \bvolume39 \bpages221–237. \biddoi=10.1016/0304-4149(91)90080-V, mr=1136247 \endbibitem

- (3) {bbook}[vtex] \bauthor\bsnmBorodin, \bfnmAndrei N.\binitsA. N. and \bauthor\bsnmSalminen, \bfnmPaavo\binitsP. (\byear2002). \btitleHandbook of Brownian Motion—Facts and Formulae, \bedition2nd ed. \bseriesProbability and Its Applications. \bpublisherBirkhäuser, \baddressBasel. \bidmr=1912205 \endbibitem

- (4) {barticle}[vtex] \bauthor\bsnmDupire, \bfnmB.\binitsB. (\byear1994). \btitlePricing with a smile. \bjournalRisk \bvolume7 \bpages18–20. \endbibitem

- (5) {barticle}[vtex] \bauthor\bsnmHeath, \bfnmD.\binitsD., \bauthor\bsnmJarrow, \bfnmR.\binitsR. and \bauthor\bsnmMorton, \bfnmA.\binitsA. (\byear1992). \btitleBond pricing and the term structure of interest rates. \bjournalEconometrica \bvolume60 \bpages77–106. \endbibitem

- (6) {barticle}[vtex] \bauthor\bsnmHobson, \bfnmD.\binitsD. (\byear1998). \btitleRobust hedging of the lookback option. \bjournalFinance Stoch. \bvolume2 \bpages329–347. \endbibitem

- (7) {bbook}[vtex] \bauthor\bsnmItô, \bfnmKiyoshi\binitsK. and \bauthor\bsnmMcKean, \bfnmHenry P.\binitsH. P., \bsuffixJr. (\byear1965). \btitleDiffusion Processes and Their Sample Paths. \bseriesGrundlehren der Mathematischen Wissenschaften \bvolume125. \bpublisherAcademic Press, \baddressNew York. \bidmr=0199891 \endbibitem

- (8) {bincollection}[vtex] \bauthor\bsnmKnight, \bfnmFrank B.\binitsF. B. (\byear1981). \btitleCharacterization of the Levy measures of inverse local times of gap diffusion. In \bbooktitleSeminar on Stochastic Processes, 1981 (Evanston, Ill., 1981). \bseriesProgr. Prob. Statist. \bvolume1 \bpages53–78. \bpublisherBirkhäuser, \baddressBoston, MA. \bidmr=0647781 \endbibitem

- (9) {bincollection}[mr] \bauthor\bsnmKotani, \bfnmS.\binitsS. and \bauthor\bsnmWatanabe, \bfnmS.\binitsS. (\byear1982). \btitleKreĭn’s spectral theory of strings and generalized diffusion processes. In \bbooktitleFunctional Analysis in Markov Processes (Katata/Kyoto, 1981). \bseriesLecture Notes in Math. \bvolume923 \bpages235–259. \bpublisherSpringer, \baddressBerlin. \bidmr=0661628 \endbibitem

- (10) {barticle}[mr] \bauthor\bsnmMadan, \bfnmDilip B.\binitsD. B. and \bauthor\bsnmYor, \bfnmMarc\binitsM. (\byear2002). \btitleMaking Markov martingales meet marginals: With explicit constructions. \bjournalBernoulli \bvolume8 \bpages509–536. \bidmr=1914701 \endbibitem

- (11) {barticle}[vtex] \bauthor\bsnmMonroe, \bfnmItrel\binitsI. (\byear1978). \btitleProcesses that can be embedded in Brownian motion. \bjournalAnn. Probab. \bvolume6 \bpages42–56. \bidmr=0455113 \endbibitem

- (12) {bbook}[mr] \bauthor\bsnmRevuz, \bfnmDaniel\binitsD. and \bauthor\bsnmYor, \bfnmMarc\binitsM. (\byear1999). \btitleContinuous Martingales and Brownian Motion, \bedition3rd ed. \bseriesGrundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences] \bvolume293. \bpublisherSpringer, \baddressBerlin. \bidmr=1725357 \endbibitem

- (13) {bbook}[vtex] \bauthor\bsnmRogers, \bfnmL. C. G.\binitsL. C. G. and \bauthor\bsnmWilliams, \bfnmDavid\binitsD. (\byear2000). \btitleDiffusions, Markov Processes, and Martingales. Vol. 2: Itô calculus. \bpublisherCambridge Univ. Press, \baddressCambridge. \bidmr=1780932 \endbibitem

- (14) {barticle}[mr] \bauthor\bsnmSchweizer, \bfnmMartin\binitsM. and \bauthor\bsnmWissel, \bfnmJohannes\binitsJ. (\byear2008). \btitleArbitrage-free market models for option prices: The multi-strike case. \bjournalFinance Stoch. \bvolume12 \bpages469–505. \biddoi=10.1007/s00780-008-0068-6, mr=2447409 \endbibitem

- (15) {bincollection}[vtex] \bauthor\bsnmWarren, \bfnmJonathan\binitsJ. (\byear1997). \btitleBranching processes, the Ray–Knight theorem, and sticky Brownian motion. In \bbooktitleSéminaire de Probabilités, XXXI. \bseriesLecture Notes in Math. \bvolume1655 \bpages1–15. \bpublisherSpringer, \baddressBerlin. \biddoi=10.1007/BFb0119287, mr=1478711 \endbibitem