Optimal investment with counterparty risk:

a default-density modeling approach

Abstract

We consider a financial market with a stock exposed to a counterparty risk inducing a drop in the price, and which can still be traded after this default time. We use a default-density modeling approach, and address in this incomplete market context the expected utility maximization from terminal wealth. We show how this problem can be suitably decomposed in two optimization problems in complete market framework: an after-default utility maximization and a global before-default optimization problem involving the former one. These two optimization problems are solved explicitly, respectively by duality and dynamic programming approaches, and provide a fine understanding of the optimal strategy. We give some numerical results illustrating the impact of counterparty risk and the loss given default on optimal trading strategies, in particular with respect to the Merton portfolio selection problem.

Key words: Counterparty risk, density of default time, optimal investment, duality, dynamic programming, backward stochastic differential equation.

1 Introduction

In a financial market, the default of a firm has usually important influences on the other ones. This has been shown clearly by several recent default events. The impact of a counterparty default may arise in various contexts. In terms of credit spreads, one observes in general a positive “jump” of the default intensity, called the contagious jump and investigated firstly by Jarrow and Yu [5]. In terms of asset (or stock) values for a firm, the default of a counterparty will in general induce a drop of its value process. In this paper, we analyze the impact of this risk on the optimal investment problem. More precisely, we consider an agent, who invests in a risky asset exposed to a counterparty risk, and we are interested in the optimal trading strategy and the value function when taking into account the possibility of default of a counterparty, together with the instantaneous loss of the asset at the default time.

The global market information containing default is modeled by the progressive enlargement of a background filtration, denoted by , representing the default-free information. The default time is in general a totally inaccessible stopping time with respect to the enlarged filtration, but is not an -stopping time. We shall work with a density hypothesis of the conditional law of default given . This hypothesis has been introduced by Jacod [4] in the initial enlargement of filtrations, and has been adopted recently by El Karoui et al. [3] in the progressive enlargement setting for the credit risk analysis. The density approach is particularly suitable to study what goes on after the default, i.e., on . For the before-default analysis on , there exists an explicit relationship between the density approach and the widely used intensity approach.

The market model considered here is incomplete due to the jump induced by the default time. The general optimal investment problem in an incomplete market has been studied by Kramkov and Schachermayer [7] by duality methods. Recently, Lim and Quenez [8] addressed, by using dynamic programming, the utility maximization in a market with default. The key idea of our paper is to derive, by relying on the conditional density approach of default, a natural separation of the initial optimization problem into an after-default one and a global before-default one. Both problems are reduced to a complete market setting, and the solution of the latter one depends on the solution of the former one. These two optimization problems are solved by duality and dynamic programming approaches, and the main advantage is to give a better insight, and more explicit results than the incomplete market framework. The interesting feature of our decomposition is to provide a nice interpretation of optimal strategy switching at the default time . Moreover, the explicit solution (for the CRRA utility function) makes clear the roles played by the default time and the loss given default in the investment strategy, as shown by some numerical examples.

The outline of this article is organized as follows. In Section 2, we present the model and the investment problem, and introduce the default density hypothesis. We then explain in Section 3 how to decompose the optimal investment problem into the before-default and after-default ones. We solve these two optimization problems in Section 4, by using the duality approach for the after-default one and the dynamic programming approach for the global before-default one. We examine more in detail the popular case of CRRA utility function and finally, numerical results illustrate the impact of counterparty risk on optimal trading strategies, in particular with respect to the classical Merton portfolio selection problem.

2 The conditional density model for counterparty risk

We consider a financial market model with a riskless bond assumed for simplicity equal to one, and a stock subject to a counterparty risk: the dynamics of the risky asset is affected by another firm, the counterparty, which may default, inducing consequently a drop in the asset price. However, this stock still exists and can be traded after the default of the counterparty.

Let us fix a probability space equipped with a brownian motion over a finite horizon , and denote by the natural filtration of . We are given a nonnegative and finite random variable , representing the default time, on . Before the default time , the filtration represents the information accessible to the investors. When the default occurs, the investors add this new information to the reference filtration . We then introduce , , the filtration generated by this jump process, and the enlarged progressive filtration , representing the structure of information available for the investors over .

The stock price process is governed by the dynamics:

| (2.1) |

where , and are -predictable processes. At this stage, without any further condition on the default time , we do not know yet that is a -semimartingale (see Remark 2.1), and the meaning of the sde (2.1) is the following. Recall (cf. [9]) that any -predictable process can be written in the form: , , where is -adapted, and is measurable w.r.t. , for all . The dynamics (2.1) is then written as:

| (2.2) | |||||

| (2.3) | |||||

| (2.4) |

where , , are -adapted processes, and , are -measurables functions for all . The nonnegative process represents the (proportional) loss on the stock price induced by the default of the counterparty, and we may assume that is a stopped process at , i.e. . By misuse of notation, we shall thus identify in (2.1) with the -adapted process in (2.3). When the counterparty defaults, the drift and diffusion coefficients of the stock price switch from , to , and the after-default coefficients may depend on the default time . We assume that , , the following integrability conditions are satisfied:

| (2.5) |

and

| (2.6) |

which ensure that the dynamics of the asset price process is well-defined, and the stock price remains (strictly) positive over (once the initial stock price ), and locally bounded.

Consider now an investor who can trade continuously in this financial market by holding a positive wealth at any time. This is mathematically quantified by a -predictable process , called trading strategy and representing the proportion of wealth invested in the stock, and the associated wealth process with dynamics:

| (2.7) |

By writing the -predictable process in the form: , , where is -adapted and is -measurable, and in view of (2.2)-(2.3)-(2.4), the wealth process evolves as

| (2.8) | |||||

| (2.9) | |||||

| (2.10) |

We say that a trading strategy is admissible, and we denote , if

| and |

This ensures that the dynamics of the wealth process is well-defined with a positive wealth at any time (once starting from a positive initial capital ).

In the sequel, we shall make the standing assumption, called density hypothesis, on the default time of the counterparty. For any , the conditional distribution of given admits a density with respect to the Lebesgue measure, i.e. there exists a family of -measurable positive functions such that:

We note that for any , the process is a -martingale.

Remark 2.1

Such a hypothesis is usual in the theory of initial enlargement of filtration, and was introduced by Jacod [4]. The (DH) Hypothesis was recently adopted by El Karoui et al. [3] in the progressive enlargement of filtration for credit risk modeling. Notice that in the particular case where the family of densities satisfies for all , we have . This corresponds to the so-called immersion hypothesis (or the H-hypothesis), which is a familiar condition in credit risk analysis, and means equivalently that any square-integrable -martingale is a square-integrable -martingale. The H-hypothesis appears natural for the analysis on before-default events when , but is actually restrictive when it concerns after-default events on , see [3] for a more detailed discussion. By considering here the whole family , we obtain additional information for the analysis of after-default events, which is crucial for our purpose.

Let us also mention that the classical intensity of default can be expressed in an explicit way by means of the density. Indeed, the -predictable compensator of is given by , where is the conditional survival probability. In other words, the process is a -martingale. Thus, by observing from the martingale property of that , we recover completely the intensity process from the knowledge of the process . However, given the intensity , we can only obtain some part of the density family, namely for .

Under (DH) Hypothesis, a -brownian motion is a -semimartingale and admits an explicit decomposition in terms of the density given by (see [9], [6], [3]):

where is a -brownian motion, and is a finite variation -adapted process. Moreover, by the Itô martingale representation theorem for brownian filtration , is written in the form for some -adapted process . Let us then define the -adapted process

and consider the Doléans-Dade exponential local martingale: , . By assuming that is a -martingale (which is satisfied e.g. under the Novikov criterion: ), this defines a probability measure equivalent to on with Radon-Nikodym density:

under which, by Girsanov’s theorem (see [1] Ch.5.2), is a -Brownian motion, is a -martingale, so that the dynamics of follows a -local martingale:

We thus have the “no-arbitrage” condition

| (2.11) |

3 Decomposition of the utility maximization problem

We are given an utility function defined on , strictly increasing, strictly concave and on , and satisfying the Inada conditions , . The performance of an admissible trading strategy associated to a wealth process solution to (2.7) and starting at time from , is measured over the finite horizon by:

and the optimal investment problem is formulated as:

| (3.1) |

Problem (3.1) is a maximization problem of expected utility from terminal wealth in an incomplete market due to the jump of the risky asset. This optimization problem can be studied by convex duality methods. Actually, under the condition that

| (3.2) |

which is satisfied under (2.11) once

where , and under the so-called condition of reasonable asymptotic elasticity:

we know from the general results of Kramkov and Schachermayer [7] that there exists a solution to (3.1). We also have a dual characterization of the solution, but this does not lead to explicit results due to the incompleteness of the market, i.e. the infinite cardinality of . One can also deal with problem (3.1) by dynamic programming methods as done recently in Lim and Quenez [8] under (H) hypothesis, but again, except for the logarithmic utility function, this does not yield explicit characterization of the optimal strategy. We provide here an alternative approach by making use of the specific feature of the jump of the stock induced by the default time under the density hypothesis. The main idea is to separate the problem in two portfolio optimization problems in complete markets: the after-default and before-default maximization problems. This gives a better understanding of the optimal strategy and allows us to derive explicit results in some particular cases of interest.

The derivation starts as follows. First notice that any , thus in the form: , , can be identified with a pair where is the set of admissible trading strategies in absence of defaults, i.e. the set of -adapted processes s.t.

| and | (3.3) |

and is the set of admissible trading strategies after default at time , i.e. the set of Borel family of -adapted processes parametrized by s.t.

Hence, for any , we observe by (2.8)-(2.9)-(2.10) that the terminal wealth is written as:

where is the wealth process in absence of default, governed by:

| (3.4) |

starting from , and is the wealth process after default occuring at , governed by:

| (3.5) | |||||

| (3.6) |

Therefore, under the density hypothesis (DH), and by the law of iterated conditional expectations, the performance measure may be written as:

| (3.7) | |||||

where .

Let us introduce the value-function process of the “after-default” optimization problem:

| (3.8) | |||||

where is the set of -adapted processes satisfying a.s., and is the solution to (3.5) controlled by , starting from at time . Thus, is the value-function process of an optimal investment problem in a market model after default. Notice that the coefficients of the model depend on the initial time when the maximization is performed, and the utility function in the criterion is weighted by . We shall see in the next section how to deal with these peculiarities for solving (3.8) and proving the existence and characterization of an optimal strategy.

The main result of this section is to show that the original problem (3.1) can be split into the above after-default optimization problem, and a global optimization problem in a before-default market.

Theorem 3.1

Assume that a.s. for all . Then, we have:

| (3.9) |

Proof. Given , we have the relation (3.7) for under (DH). Furthermore, by Fubini’s theorem, the law of iterated conditional expectations, we then obtain:

by definitions of , and . This proves the inequality: .

To prove the converse inequality, fix an arbitrary . By definition of , for any , , and , there exists , which is an -optimal control for at . By a measurable selection result (see e.g. [10]), one can find s.t. , a.e., and so

By denoting , and using again (3), we then get:

From the arbitrariness of in and , we obtain the required inequality and so the result.

Remark 3.1

The relation (3.9) can be viewed as a dynamic programming type relation. Indeed, as in dynamic programming principle (DPP), we look for a relation on the value function by varying the initial states. However, instead of taking two consecutive dates as in the usual DPP, the original feature here is to derive the equation by considering the value function between the initial time and the default time conditionnally on the terminal information, leading to the introduction of an “after-default” and a global before-default optimization problem, the latter involving the former. Each of these optimization problems are performed in complete market models driven by the brownian motion and with coefficients adapted with respect to the brownian filtration. The main advantage of this approach is then to reduce the problem to the resolution of two optimization problems in complete markets, which are simpler to deal with, and give more explicit results than the incomplete market framework studied by the “classical” dynamic programming approach or the convex duality method.

Furthermore, a careful look at the arguments for deriving the relation (3.9) shows that in the decomposition of the optimal trading strategy for the original problem (3.1) which is known to exist a priori under (2.11):

is an optimal control to (3.9), and is an optimal control to with , and is the wealth process governed by . In other words, the optimal trading strategy is to follow the trading strategy before default time , and then to change to the after-default trading strategy , which depends on the time where default occurs. In the next section, we focus on the resolution of these two optimization problems.

4 Solution to the optimal investment problem

In this section, we focus on the resolution of the two optimization problems arising from the decomposition of the initial utility maximization problem. We first study the after-default optimal invesment problem, and then the global before-default optimization problem.

4.1 The after-default utility maximization problem

Problem (3.8) is an optimal investment problem in a complete market model after default. A specific feature of this model is the dependence of the coefficients on the initial time when the maximization is performed. This makes the optimization problem time-inconsistent, and the classical dynamic programming method can not be applied. Another peculiarity in the criterion is the presence of the density term weighting the utility function .

We adapt the convex duality method for solving (3.8). We have to extend this martingale method (in complete market) in a dynamic framework, since we want to compute the value-function process at any time . Let us denote by:

the (local) martingale density in the market model (2.4) after default. We assume that for all , there exists some -measurable strictly positive random variable s.t.

| (4.1) |

This assumption is similar to the one imposed in the classical (static) convex duality method for ensuring that the dual problem is well-defined and finite.

Theorem 4.1

Proof. First observe, similarly as in Theorem 2.2 in [7], that under , the validity of (4.1) for some or for all -measurable strictly positive random variable, is equivalent. By definition of and Itô’s formula, the process is a nonnegative -local martingale, hence a supermartingale, for any , and so . Denote . Then, by definition of , we have for all -measurable strictly positive random variable, and :

| (4.3) | |||||

which proves in particular that is finite a.s. Now, we recall that under the Inada conditions, the supremum in the definition of is attained at , i.e. . From (4.3), this implies

| (4.4) | |||||

Now, under the Inada conditions, (4.1) and , for any , , the function is a strictly decreasing one-to-one continuous function from into . Hence, there exists a unique s.t. . Moreover, since is -measurable, this value can be chosen, by a measurable selection argument, as -measurable. With this choice of , and by setting , the inequality (4.4) yields:

| (4.5) |

Consider now the process defined in (4.2) leading to at time . By definition, the process is a strictly positive -martingale. From the martingale representation theorem for brownian motion filtration, there exists an -adapted process satisfying a.s., and such that

Thus, by setting , we see that , and by Itô’s formula, satisfies the wealth equation (3.5) controlled by . Moreover, by construction of , we have:

Recalling (4.5), this proves that is an optimal solution to (3.8), with corresponding optimal wealth process .

Remark 4.1

Under the (H) hypothesis, is -measurable. In this case, the optimal wealth process to (3.8) is given by:

where is the strictly positive -measurable random variable satisfying . Hence, the optimal strategy after-default does not depend on the density of the default time.

We illustrate the above results in the case of Constant Relative Risk Aversion (CRRA) utility functions.

Example 4.1

The case of CRRA Utility function

We consider utility functions in the form

In this case, we easily compute the optimal wealth process in (4.2):

where . The optimal value process is then given for all by:

| (4.6) |

Notice that the case of logarithmic utility function: , , can be either computed directly, or derived as the limiting case of power utility function case: as goes to zero. The optimal wealth process is given by:

and the optimal value process for all , is equal to:

4.2 The global before-default optimization problem

In this paragraph, we focus on the resolution of the optimization problem (3.9). We already know the existence of an optimal strategy to this problem, see Remark 3.1, and our main concern is to provide an explicit characterization of the optimal control.

We use a dynamic programming approach. For any , , let us consider the set of controls coinciding with until time :

Under the standing condition that , we then introduce the dynamic version of the optimization problem (3.9) by considering the family of -adapted processes:

so that for any . In the above expression, is the wealth process of dynamics (3.4), controlled by , and starting from . We also denote the wealth process of dynamics (3.4), controlled by , starting from , so that it coincides with until time , i.e. . From the dynamic programming principle (see El Karoui [2]), the process can be chosen in its càd-làg version, and is such that for any :

| is a | (4.7) |

Moreover, the optimal strategy to problem , is characterized by the martingale property:

| is a | (4.8) |

In the sequel, we shall exploit this dynamic programming properties in the particular important case of constant relative risk aversion (CRRA) utility functions. We then consider utility functions in the form

and we set . Notice that we deal with the relevant economic case when , i.e. the degree of risk aversion is strictly larger than . This will induce some additional technical difficulties with respect to the case . For CRRA utility function, is also of the same power type, see (4.6):

and we assume that is finite a.s. for all . The value of the optimization problem (3.9) is written as

In the above equality, we may without loss of generality take supremum over , the set of elements such that:

| (4.9) |

and by misuse of notation, we write . For any with corresponding wealth process governed by (3.4) with control , and starting from , we notice that the càd-làg -adapted process defined by:

does not depend on . It lies in the set of nonnegative càd-làg -adapted processes. Let us also denote by the set of -adapted process s.t. a.s.

We have the following preliminary properties on this process .

Lemma 4.1

The process in (4.2) is strictly positive, i.e. . Moreover, for all , the process

| (4.11) |

is bounded from below by a martingale.

Proof. (1) We first consider the case . Then,

by taking in (4.2) the control process defined by . Moreover, since is nonnegative, the process is nonnegative, hence trivially bounded from below by the zero martingale.

(2) We next consider the case . Then,

Notice that the process can be chosen in its càd-làg modification. Let us show that for any , the infimum in is attained. Fix , and consider, by a measurable selection argument, a minimizing sequence to , i.e.

| (4.14) |

Here denotes the wealth process of dynamics (3.4) governed by . Consider the (local) martingale density process

By definition of and Itô’s formula, the process is a nonnegative -local martingale, hence a supermartingale, and so . By Komlòs Lemma applied to the sequence of nonnegative -measurable random variable , there exists a convex combination conv such that converges a.s. to some nonnegative -measurable random variable . By Fatou’s lemma, we have . Moreover, by convexity of , and Fatou’s lemma, it follows from (4.14) that

| (4.15) |

Now, since , , and a.s., we deduce that , and so a.s. Consider the process , . Then, is a strictly positive -martingale, and by the martingale representation theorem for brownian filtration, using same arguments as in the end of proof of Theorem 4.1, we obtain the existence of an -adapted process satisfying , such that satisfies the wealth process dynamics (3.4) with portfolio on , and starting from . By considering the portfolio process defined by , for , and denoting by the corresponding wealth process, it follows that for , and in particular a.s. From (4.15), the nonincreasing property of , and definition of , we deduce that

| (4.16) |

and as a byproduct that . The equality (4.16) means that the process is a modification of the process . Since, and are càd-làg, they are then indistinguishable, i.e. . We deduce that the process , and consequently , inherit the strict positivity of the process .

From (4.2), we have for all , ,

by taking in (4.2) the control process . The negative process is an integrable (recall (4.9)) martingale, and the assertions of the Lemma are proved.

In the sequel, we denote by the set of processes in , such that for all , the process is bounded from below by a martingale. The next result gives a characterization of the process in terms of backward stochastic differential equation (BSDE) and of the optimal strategy to problem (3.9).

Theorem 4.2

When (resp. ), the process in (4.2) is the smallest (resp. largest) solution in to the BSDE:

| (4.18) |

for some , and where

| (4.19) |

The optimal strategy to problem (3.9) attains the supremum in (4.19). Moreover, under the integrability condition: a.s., the supremum in (4.19) can be taken pointwise, i.e.

while the optimal strategy is given by:

and satisfies the estimates:

| (4.20) |

where

Proof. By Lemma 4.1, the process lies in . From (4.7), we know that for any , the process is a -supermartingale. In particular, by taking , we see that the process is a -supermartingale. From the Doob-Meyer decomposition, and the (local) martingale representation theorem for brownian motion filtration, we get the existence of , and a finite variation -adapted process such that:

| (4.21) |

From (3.4) and Itô’s formula, we deduce that the finite variation process in the decomposition of the -supermartingale , , is given by with

Now, by the supermartingale property of , , which means that is nondecreasing, and the martingale property of , i.e. , this implies:

Observing from (4.2) that , this proves together with (4.21) that solves the BSDE (4.18). In particular, the process is continuous.

Consider now another solution to the BSDE (4.18), and define the family of nonnegative -adapted processes , , by:

| (4.22) |

By Itô’s formula, we see by the same calculations as above that: , where is a nondecreasing -adapted process, and is a local -martingale as a stochastic integral with respect to the brownian motion . By Fatou’s lemma under the condition , this implies that the process is a -supermartingale, for any . Recalling that , we deduce that for all

If (resp. ), then by dividing the above inequalities by , which is positive (resp. negative), we deduce by definition of (see (4.2) and (4.2)), and arbitrariness of , that (resp. ) , . This shows that is the smallest (resp. largest) solution to the BSDE (4.18).

Next, we make the additional integrability condition:

| (4.23) |

Let us consider the function defined on by:

(As usual, we omit the dependence of in ). By definition, we clearly have almost surely

| (4.24) |

Let us prove the converse inequality. Observe that, almost surely, for all , the function is strictly concave (recall that the process is strictly positive), on , with:

and satisfies:

We deduce that almost surely, for all , the function attains its maximum at some point , which satisfies:

By a measurable selection argument, this defines an -adapted process . In order to prove the equality in (4.24), it suffices to show that such lies in , and this will be checked under the condition (4.23). For this, consider the -adapted processes and defined by:

When , we have:

and so by strict concavity of in : . When , and since , we get: . Consequently, we have the upperbound: , for all . Notice that by (2.5), continuity of the path of , and since , we have: a.s. Moreover, since , we have , and thus lies in . Next, consider the -adapted process defined by:

for some -adapted nonnegative process to be determined. When , we have

| (4.25) | |||||

When , the inequality (4.25) also holds true. Hence, by choosing such that the r.h.s. of (4.25) vanishes, i.e.

we obtain almost surely: , , and so by strict concavity of in : . Finally, under (4.23), and recalling that is continuous, , we easily see that satisfies the integrability condition: a.s., and so lies in . Therefore, we have proved that lies in , and satisfies the estimates (4.20).

Remark 4.2

The driver of the BSDE (4.18) is in general not Lipschitz in the arguments in , and we are not able to prove by standard arguments that there exists a unique solution to this BSDE.

Remark 4.3

We make some comments and interpretation on the form of the optimal before-default strategy. Let us consider a default-free stock market model with drift and volatility coefficients and , and an investor with CRRA utility function , looking for the optimal investment problem:

where is the wealth process in (3.4). In this context, , defined in (3.3) is interpreted as the set of trading strategies that are constrained to be upper-bounded (in proportion) by . In other words, is the Merton optimal investment problem under constrained strategies. By considering, similarly as in (4.2), the process

and arguing similarly as in Theorem 4.2, one can prove that is the smallest solution to the BSDE:

for some , where

while the optimal strategy for is given by:

Notice that when the coefficients , and are deterministic, then is also deterministic, i.e. , and is the positive solution to the ordinary differential equation:

with , and so: . Moreover, the optimal strategy is . In particular, when there is no constraint on trading strategies, i.e. , we recover the usual expression of the optimal Merton trading strategy: .

Here, in our default stock market model, the optimal before-default strategy satisfies the estimates (4.20), which have the following interpretation. The process has a similar form as the optimal Merton trading strategy described above, but includes further through the process and , the eventuality of a default of the stock price, inducing a drop of size , and then a switch of the coefficients of the stock price from to . The optimal trading strategy is upper-bounded by , and when the jump size goes to zero, it converges to , as expected since in this case the model behaves as a no-default market.

4.3 Example and numerical illustrations

We consider a special case where , , are constants, are only deterministic functions of , and the default time is independent of , so that is simply a known deterministic function of , and the survival probability is a deterministic function. We also choose a CRRA utility function , , , . Notice that with

Moreover, the optimal wealth process after-default does not depend on the default time density, and the optimal strategy after-default is given, similarly as in the Merton case, by:

On the other hand, from the above results and discussion, we know that in this Markovian case, the value function of the global before-default optimization problem is in the form with:

where is a deterministic function of time, solution to the first-order ordinary differential equation (ODE):

| (4.26) |

with

| (4.27) |

There is no explicit solutions to this ODE, and we shall give some numerical illustrations.

The following numerical results are based on the model parameters described below. We suppose that the survival probability follows the exponential distribution with constant default intensity, i.e. where , and thus the density function is . The functions and are supposed to be in the form

which have the following economic interpretation. The ratio between the after and before-default rate of return is smaller than one, and increases linearly with the default time: the after-default rate of return drops to zero, when the default time occurs near the initial date, and converges to the before-default rate of return, when the default time occurs near the finite investment horizon. We have a similar interpreation for the volatility but with symmetric relation: the ratio between the after and before-default volatility is larger than one, decreases linearly with the default time, converging to the double (resp. initial) value of the before-default volatility, when the default time goes to the initial (resp. terminal horizon) time.

To solve numerically the ODE (4.26), we apply the Howard algorithm, which consists in iterating in (4.27) the control value at each step of the ODE resolution. We initialize the algorithm by choosing the constrained Merton strategy

In the following Table 1, we show the impact of the loss given default on the optimal strategy . The numerical tests show that except in some extreme cases where both the default probability and the loss given default are large, the optimal strategy is quite invariant with respect to time in most cases we consider. So we give below the optimal strategy as its expected value on time. We perform numerical results for various degrees of risk aversion : smaller, close to and larger than one, and with , , and .

First, observe that, when we take into account the counterparty risk, the proportion invested in the stock is always smaller than the Merton strategy without conterparty risk. Secondly, the strategy is decreasing with respect to , which means that one should reduce the stock investment when the loss given default increases.

| PD | |||||||

|---|---|---|---|---|---|---|---|

| PD | |||||||

| PD | |||||||

| PD | |||||||

Next, we examine the role played by the default intensity . In Table 2, the column PD represents the default probability of the counterparty up to with the given intensity , i.e. PD . We see that the stock investment decreases rapidly when the default probability increases. Moreover, when both default probability of the counterparty and the loss given default of the stock are large, one should take short position on the stock in the portfolio investment strategy before the default of the counterparty. Then at the default time , the optimal strategy is switched to , which is always positive.

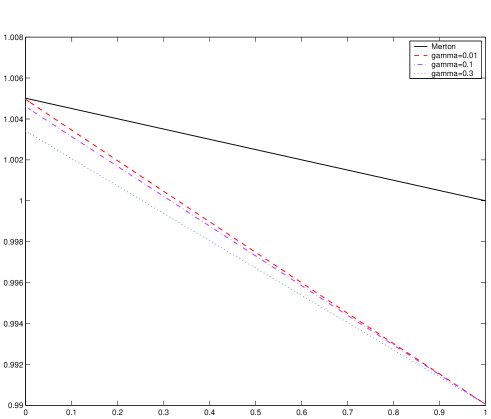

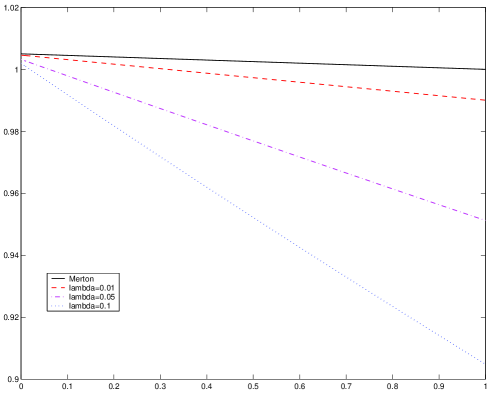

We also compare the value function obtained in our example to that in the classical Merton model, that is, the solution to the ODE (4.26) and the function deduced with and . In Figure 2, the curves represent different values of such that . The value function obtained with counterparty risk is always below the Merton one. It is decreasing on time and also decreasing w.r.t. the proportional loss . In addition, for a given default intensity , all curves converge at to . In Figure 2, the curves represent different values of . The value function is also decreasing w.r.t. the default intensity . However, the final value of each curve corresponds to different values of .

5 Conclusion

This paper studies an optimal investment problem under the presence of counterparty risk for the trading stock. By adopting a conditional density approach for the default time, we derive a suitable decomposition of the initial utility maximization problem into an after-default and a global default one, the solution to the latter depending on the former. This makes the resolution of the optimization problem more explicit, and provides a fine understanding of the optimal trading strategy emphasizing the impact of default time and loss given default. The density approach can be used for studying other optimal portfolio problems, like the pricing by indifference-utility, with counterparty risk. A further topic is the optimal investment problem with two assets (names) exposed both to bilateral counterparty risk, and the conditional density approach should be relevant for such study planned for future research.

References

- [1] Bielecki T. and M. Rutkowski (2002): Credit risk: Modeling, Valuation and Hedging, Springer Finance.

- [2] El Karoui N. (1981): Les aspects probabilistes du contrôle stochastique, Lect. Notes in Math. 816, Springer-Verlag.

- [3] El Karoui, N., M. Jeanblanc, and Y. Jiao (2009): “What happens after a default, the conditional density approach”, Working Paper.

- [4] Jacod, J. (1987): “Grossissement initial, Hypothèse (H’) et théorème de Girsanov”, in Séminaire de Calcul Stochastique, (1982/1983), vol. 1118, Lecture Notes in Mathematics, Springer.

- [5] Jarrow, R. and F. Yu (2001): “Counterparty risk and the pricing of defaultable securities”, Journal of Finance, 56(5), 1765–1799,

- [6] Jeanblanc, M. and Y. Le Cam (2008): “Progressive enlargement of filtration with initial times”, to appear in Stochastic Proc. and their Applic.

- [7] Kramkov D. and W. Schachermayer (1999): “The asymptotic elasticity of utility functions and optimal investment in incomplete markets”, Annals of Applied Probability, 9, 904-950.

- [8] Lim, T. and M.C. Quenez (2008): “Utility maximization in incomplete markets with default”, Preprint PMA, Universities Paris 6-Paris7.

- [9] Mansuy, R. and M. Yor (2005): Random times and enlargements of filtrations in a Brownian setting, Springer.

- [10] Wagner D. H. (1980): “Survey of measurable selection theorems: an update”, Lect. Notes in Math. 794, Springer-Verlag.