Random matrices:

The distribution of the smallest singular values

Abstract.

Let be a real-valued random variable of mean zero and variance . Let denote the random matrix whose entries are iid copies of and denote the least singular value of . The quantity is thus the least eigenvalue of the Wishart matrix .

We show that (under a finite moment assumption) the probability distribution is universal in the sense that it does not depend on the distribution of . In particular, it converges to the same limiting distribution as in the special case when is real gaussian. (The limiting distribution was computed explicitly in this case by Edelman.)

We also proved a similar result for complex-valued random variables of mean zero, with real and imaginary parts having variance and covariance zero. Similar results are also obtained for the joint distribution of the bottom singular values of for any fixed (or even for growing as a small power of ) and for rectangular matrices.

Our approach is motivated by the general idea of “property testing” from combinatorics and theoretical computer science. This seems to be a new approach in the study of spectra of random matrices and combines tools from various areas of mathematics.

1. Introduction

Let be a real or complex-valued random variable and denote the random matrix whose entries are i.i.d. copies of . In this paper, we always impose one of the following two normalizations on :

-

•

(-normalization) is real-valued with and .

-

•

(-normalization) is complex-valued with , , and .

Note in both cases has mean zero and variance one. A model example of a -normalized random variable is the real gaussian , while a model example of a -normalized random variable is the complex gaussian whose real and imaginary parts are iid copies of . Another -normalized random variable of interest is Bernoulli, in which equals or with an equal probability of each.

A basic problem in random matrix theory is to understand the distribution of singular values in the asymptotic limit . Given an matrix , let

denote the non-trivial singular values of . Our paper will be focused on the “hard edge” of this spectrum, and in particular on the least singular value , in the case of square matrices , but let us begin with a brief review of some known results for the rest of the spectrum.

There is a general belief that (under reasonable hypotheses) the limiting distributions concerning the spectrum of a large random matrix should be “universal”, in the sense that they should not depend too strongly on the distributions of the entries of the matrix. In particular, one usually expects that the asymptotic statistical properties that are known for matrices with (independent) gaussian entries should also hold for matrices with more general entries (such as Bernoulli). A well-known conjecture (now a theorem) of this type is the Circular Law conjecture (see [5, Chapter 10] and [47]). Another example is that of Dixon’s conjectures (see [26, Conjectures 1.2.1 and 1.2.2]).

Universality has been proved for several statistics concerning the random matrix model . As is well known, the bulk distribution of the singular values of is governed by the Marchenko-Pastur law. It has been shown that for any and any - or -normalized ,

as , both in the sense of probability and in the almost sure sense. For more details, we refer to [27, 31, 51, 5]. (In literature, very frequently one views as the eigenvalues of the sample covariance matrix and so it is more traditional to write down the limiting distributions in term of .)

The next objects to consider are the extremal singular values. The distribution of the largest singular value (and more generally, the joint distribution of the top singular values) was computed for the gaussian case by Johansson [18] and Johnstone [19]. This distribution is governed by the Tracy-Widom law (and more generally, the Airy kernel). In particular, one has

where denotes the Tracy-Widom distribution. More recently, Soshnikov [39] showed that the same result holds for all random matrices with normalized subgaussian entries.

Now we turn to the “hard edge” of the spectrum, and specifically to the least singular value . The problem of estimating the least singular value of a random matrix has a long history. It first surfaced in the work of von Neuman and Goldstein concerning numerical inversion of large matrices [30]. Later, Smale [38] made a specific conjecture about the magnitude of . Motivated by a question of Smale, Edelman computed the distrubition of for the real and complex gaussian cases [9]:

Theorem 1.1 (Limiting distributions for gaussian models).

For any fixed , we have

| (1) |

as well as the exact (!) formula

Both integrals can be computed explicitly. By change of variables, one can show

| (2) |

Furthermore, it is clear that

| (3) |

In fact, one can compute the joint distribution of the bottom singular values of or for any constant , as was done by Forrester[11]. The formula, which involves the Bessel kernel, is more complicated and is deferred to Section 6. In [33], a different approach was proposed by Rider and Ramirez, which lead to description that does not involve Bessel kernels directly. Ben Arous and Peche [8] generalized Forrester’s result to matrices whose entries are gaussian summable.

The error term in (1) is not explicitly stated in [9] (it relies on an asymptotic for the Tricomi function), but our Theorem 1.3 below will imply that it is of the form for some absolute constant .

The proofs of the above results relied on special algebraic properties of the gaussian models , (and in particular on various exact identities enjoyed by such models). For instance, Edelman’s proof used the exact joint distribution of the eigenvalues of , which are available in the gaussian case:

| (4) |

| (5) |

Here and are normalizing factors. It appears that this approach do not extend to the case of more general - or -normalized models , where the above formulae are not available.

In the general setting (and in particular in discrete cases such as Bernoulli), it is already not trivial to show that the probability that is positive tends to one with (this statement is, of course, obvious in the continuous case, such as gaussian, by a dimension argument). This was first done by Komlós [21, 22]. For more recent developments along this line we refer to [20, 46, 6]. These papers give better and better bounds on the rate of convergence (to one) of the probability in question, but do not give any quantitative estimate on .

In the last few years,we have seen considerable progresses in the problem of estimating and its tail distribution. In [43], the present authors proved an (almost sure) lower bound for the absolute value of the determinant of a random Bernoulli matrix. As the absolute value of the determinant is the product of the singular values, this result implies an (almost sure) lower bound of the form for the least singular value. A significant breakthrough was achieved by Rudelson [34], who established a polynomial lower bound for and also tail estimates for a certain range. Rudelson’s results were then extended by several authors [35], [36], [44], [45], [47], [48], [49], using the machinery of Inverse Littlewood-Offord theorems, introduced in [44]. For instance, under the assumption of bounded fourth moment , it was shown in [36] that

for all fixed , where goes to zero as ; similarly, in [35] it was shown that

for all fixed , where goes to zero as . Under the stronger assumption that is subgaussian, the lower tail estimate was improved in [36] to

| (6) |

for some constants and depending only on the subgaussian moments of . At the other extreme, with no moment assumptions on , the bound

was shown for any fixed in [48].

A common feature of the above mentioned results is that they give good upper and lower tail bounds on , but not the distributional law. In fact, many papers [35, 36, 45] are partially motivated by the following conjecture of Spielman and Teng [40, Conjecture 2].

Conjecture 1.2.

Let be the Bernoulli random variable. Then there is a constant such that for all

| (7) |

In this paper, we introduce a new method to study small singular values. This method is analytic in nature and enables us to prove the universality of the limiting distribution of .

Theorem 1.3 (Universality for the least singular value).

Let be - or -normalized, and suppose for some sufficiently large absolute constant . Then for all , we have

| (8) |

if is -normalized, and

if is -normalized, where is an absolute constant. The implied constants in the notation depend on but are uniform in .

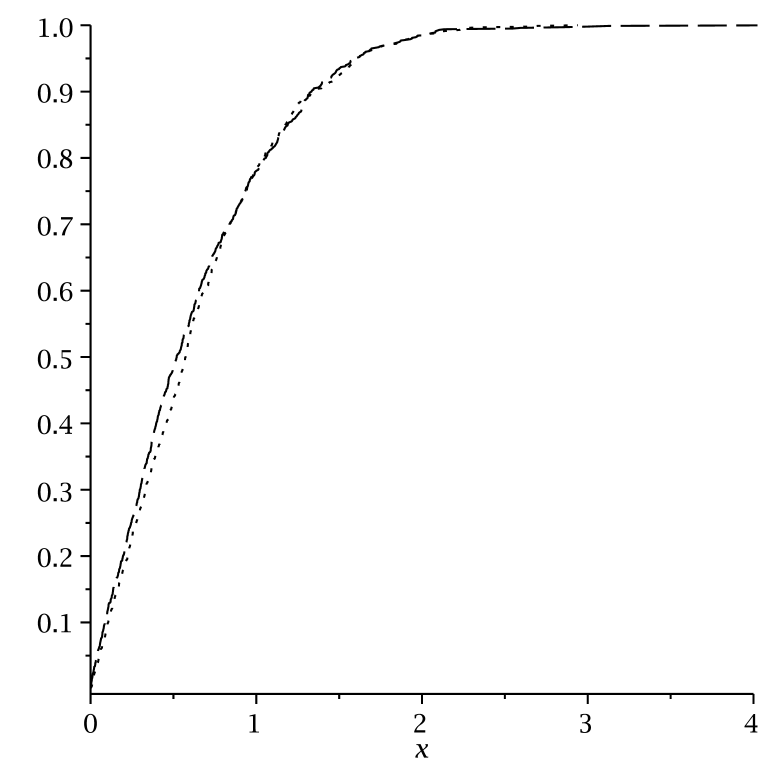

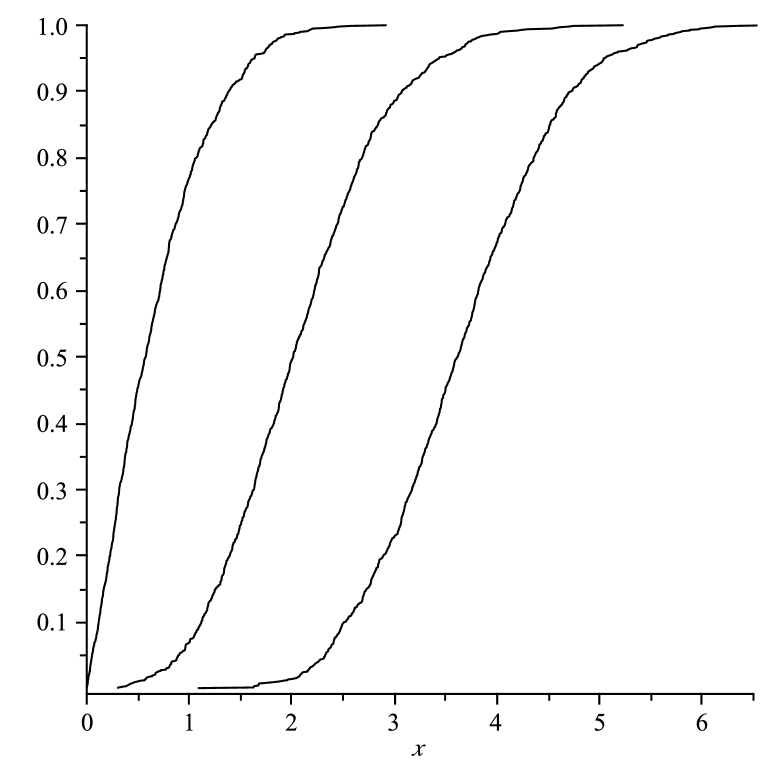

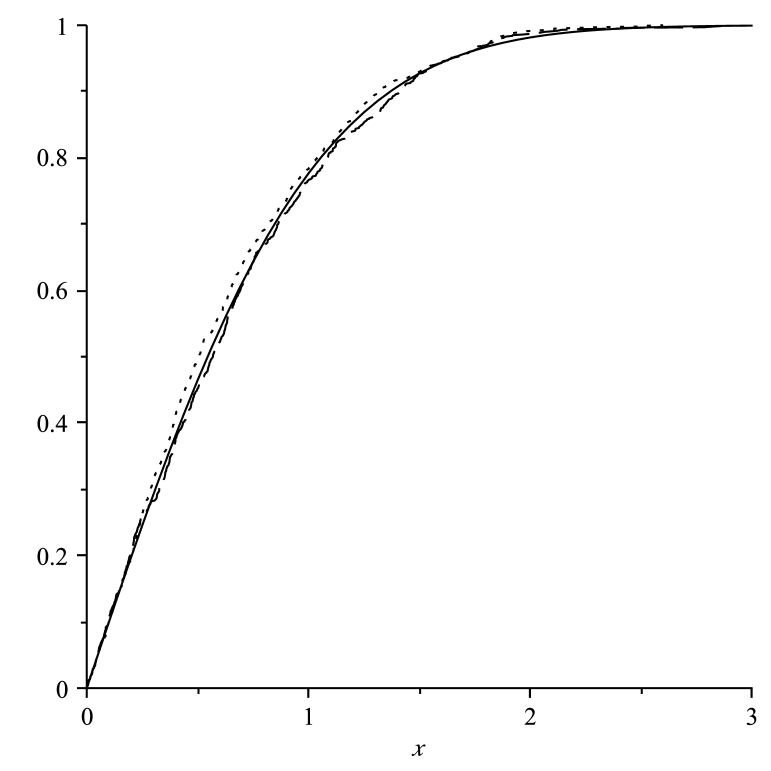

Figure 1 shows an empirical demonstration of the theorem above for Bernoulli and for gaussian distributions.

Very roughly speaking, we will show that one can swap with the appropriate gaussian distribution or , at which point one can basically apply Theorem 1.1 as a black box. In other words, we show that the law of is universal with respect to the choice of by a direct comparison to the gaussian models. The exact formulae and do not play any important role. This direct comparison (or coupling) approach is in the spirit of Lindeberg’s proof [24] of the central limit theorem, and was also recently applied in our proof of the circular law [49].

Our arguments are completely effective, and give an explicit value for ; for instance, certainly suffices. Clearly, one should be able to lower significantly (we have made no attempt to optimize in , in order to simplify the exposition), but we will not explore this issue here.

Theorem 1.3 can be extended in several directions, with simple modifications of the proof. For example, we can prove a similar universality result involving the joint distribution of the bottom singular values of , for bounded (and even some results when is a small power of ). Next, we can also consider rectangular matrixes where the difference between the two dimensions is not too large. Finally, all results hold if we drop the condition that the entries have identical distribution. (It is important that they are all normalized, independent and their -moments are uniformly bounded.) For precise statements, see Section 6.

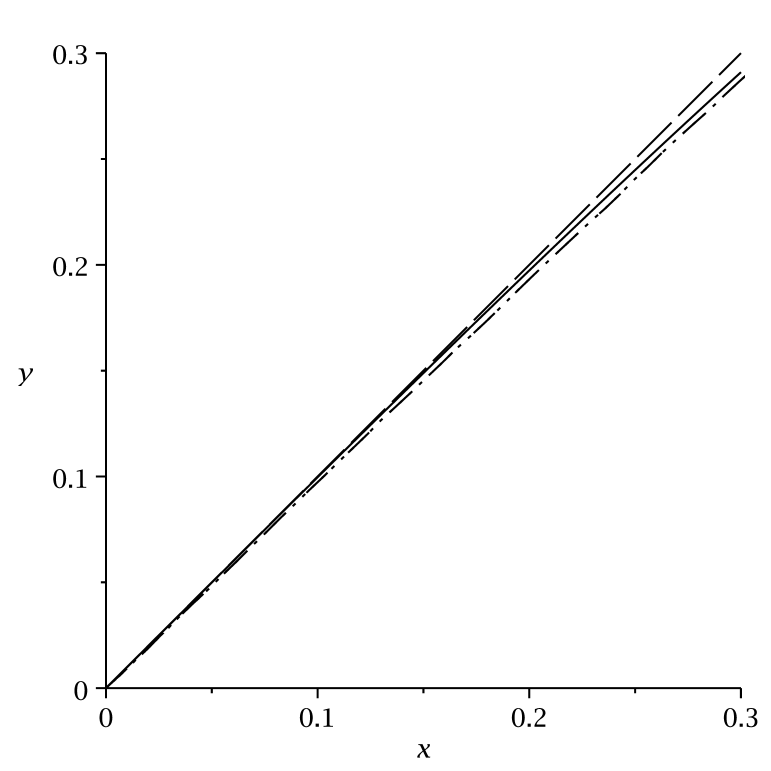

It is clear that one can use Theorem 1.3 to address Conjecture 1.2. By Theorem 1.3 and (2), the left hand side of (7) is

Since for any , we conclude that Conjecture 1.2 holds for any , for some positive constant . More importantly, it shows that the main term on the right hand side of (7) is only a (first order) approximation of the truth and could certainly be improved. For example, for sufficiently small , Taylor expansion gives

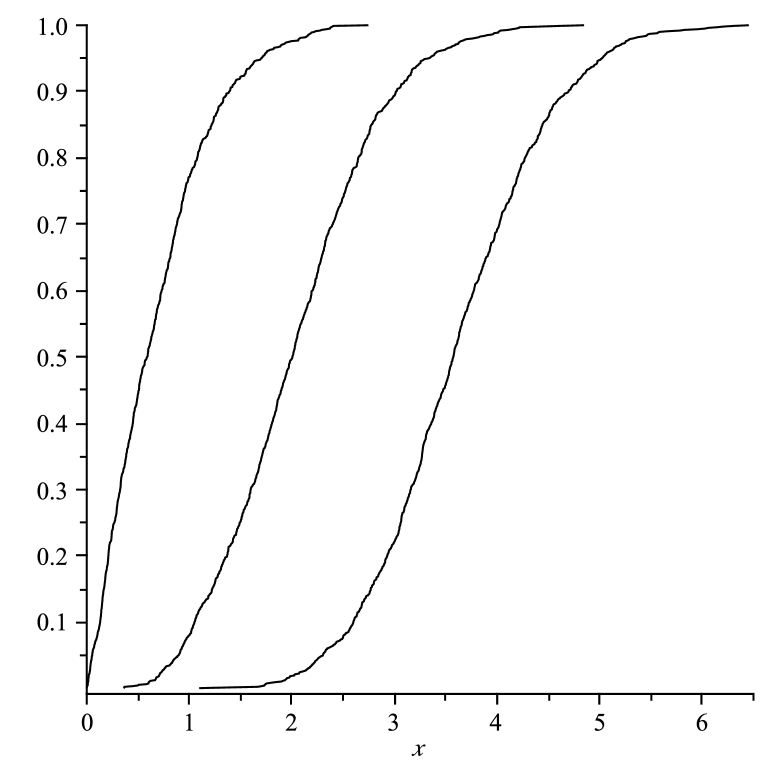

Figure 2 provides empirical evidence that for the Bernoulli and gaussian cases.

The rest of the paper is organized as follows. In the next section, we describe our proof strategy. In Section 3, we turn this high-level strategy into a rigorous proof, using many technical lemmas from various areas of mathematics (linear algebra, theoretical computer science, probability and high dimensional geometry). Many of these lemmas may have some independent interest. For instance, Corollary 5.2 shows that the distance from a random vector (in ) to a hyperplane spanned by other random vectors has (asymptotically) gaussian distribution. This is obvious in the case when the coordinates of the vector in question are iid gaussian, but is not so when they are Bernoulli. (See also [36] for some related results in this spirit.)

Notation. We consider as an asymptotic parameter tending to infinity. We use , , , or to denote the bound for all sufficiently large and for some which can depend on fixed parameters (such as or ) but is independent of .

The Frobenius norm of a matrix is defined as . Note that this bounds the operator norm of the same matrix.

For a random variable , is the expectation of . If is real, we denote by its median, namely a number such that both and are at least . (If is not unique, choose one arbitrarily.)

For an event , is its indicator function, taking value 1 if holds and 0 otherwise. Clearly .

2. The main idea and the proof strategy

We now discuss our main idea and the strategy behind Theorem 1.3. A formal version of this argument is given in Section 3, though for various minor technical reasons, the presentation there will be rearranged slightly from the one given here.

Let us first reveal our main idea. To start, we are going to view as the (reciprocal of the) largest singular value of . One of the most popular methods to study the largest singular value is the moment method, which enables one to control on (of a random matrix ) if one can have good estimates on for very large . The moment method was used successfully by Sosnhikov [39] to study . However, it is important in the applications of this method that the entries of are independent and their distributions well-understood. Unfortunately, the entries of are highly correlated and not much is known about their distributions.

We have found a new approach, motivated by the general idea of “property testing”, a topics popular in theoretical computer science and combinatorics. The general setting of a property testing problem is as follows. Given a large, complex, structure , we would like to study some parameter of . It has been observed that quite often one can obtain good estimates about by just looking at the small substructure of , sampled randomly. In our situation, the large structure is the matrix , and the parameter in question is its largest singular value. It has turned out that this largest singular value can be estimated quite precisely (with high probability) by sampling a few rows (say ) from and considering the submatrix formed by these rows. The heart of the proof then consists of two observations: (1) The singular values of can be computed from a matrix obtained by projecting the rows of onto a subspace of dimension and (2) Such a projection has a central limit theorem effect. All these together allow us to compare the least singular value of with the least singular value of (properly normalized), proving the universality.

Let us now be a little more specific. For sake of discussion we discuss the -normalized case (8). Our goal is to show

| (9) |

where we will be deliberately vague111Roughly speaking, means that the distributions of the random variables and are close in some appropriately normalized Lévy distance, where the appropriate normalization may change from line to line. as to what the symbol means in this non-rigorous discussion. The -normalized case will of course be very similar.

We have

| (10) |

(From existing results, e.g. [20, 48], it is known that is invertible with very high probability.) We now wish to show that

Let denote the rows of , and let for some small absolute constant . To estimate the largest singular value of the matrix formed by the rows , we use random sampling. More precisely, we create the submatrix formed by selecting of these rows at random. Actually, since the joint distribution of is easily seen to be invariant under relabeling of the indices, we may just take to be the matrix with rows . An application of the second moment method (see Lemma 3.1 and its proof) will give us the relationship

| (11) |

provided that we have some reasonable bound on the magnitude of the rows (see Proposition 3.2); of course we expect the same statement to be true with replaced by . Assuming it for now, we are now (morally) reduced to establishing a relationship of the form

The next step is to use some elementary linear algebra to replace the matrix with an matrix , defined as follows. Let be the columns of ; observe that these iid random variables are the dual basis of , thus for , where is the Kronecker delta.

Let be the -dimensional subspace of defined as the orthogonal complement of the -dimensional space spanned by the columns . We select an orthonormal basis on arbitrarily (e.g. uniformly at random, and independently of the columns ), thus identifying with the standard -dimensional space . The orthogonal projection from to can now be thought of as a partial isometry . Let be the matrix whose columns are . In Lemma 3.3 we will establish the simple identity

thus reducing our task to that of showing that

| (12) |

The relation (12) looks very similar to our original relation (9) (indeed, when , (12) collapses back to (9)). However, the critical gain here is that (12) becomes much easier to prove than (9) when is only a small power of , because the projection will act to average out the random variable into (approximately) a gaussian variable (essentially thanks to the central limit theorem). Indeed, by using a variant of the Berry-Esséen central limit theorem (Proposition 3.4), together with some non-degeneracy (or “delocalization”) properties of (Proposition 3.5), we will be able to establish a relation of the form

and similarly

(indeed, it is not hard to see that and in fact have an identical distribution). The claim (12) will then follow from the Lipschitz properties of , which is a consequence of the Hoefmann-Weilandt theorem (see Lemma B.1).

3. The rigorous proof

We now implement the strategy sketched out in Section 2 to give a rigorous proof of Theorem 1.3. This proof will rely on several key propositions which are proven in later sections or in the appendices.

Let be either the real field or the complex field , and fix an -normalized random variable . We assume to be a sufficiently large constant to be chosen later (e.g. certainly suffices). All implied constants are allowed to depend on and . In all arguments, we assume to be large depending on these parameters. Fix , and write if or if . Our task is to show that

| (13) |

We first make a simple reduction. By hypothesis, . Hence by Markov’s inequality, we see that . Thus, by the union bound, we see that with probability at least , all coefficients of are . If we remove the tail event from , and readjust slightly to restore the -normalization conditions (using (36) to absorb the error, and using the continuity of ), we may thus reduce to the case when

| (14) |

with probability one. This is a standard truncation and re-normalization process, used frequently in random matrix literature (see, for instance, [5]). We omit the (routine, but somewhat tedious) details.

For minor technical reasons, it is also convenient to assume to be a continuous random variable (in particular, this implies that is invertible with probability one). However, we emphasise that the bounds in our arguments do not explicitly depend on the continuity properties of , and instead depend only on the moment of for any fixed . Since one can express any discrete random variable with finite moment (and obeying (14)) as the limit of a sequence of continuous random variables with uniformly bounded moment (and also obeying (14)), we see that the discrete case of the theorem can be recovered from the continuous one by a standard limiting argument (keeping fixed during this process, and using (36) as necessary).

Applying (10), we have

Let denote the rows of . Since the columns of are exchangeable (i.e. exchanging any two columns of does not affect the distribution), we see that is row-exchangeable.

Our first step is motivated by the observation that in certain cases the largest singular values of a matrix can be well approximated by sampling. This fact is well-known in theoretical computer science and numerical analysis. In particular, the lemma below is a special case of more general results from [14, 7].

Lemma 3.1 (Random sampling).

Let be integers. be an real or complex matrix with rows . Let be selected independently and uniformly at random, and let be the matrix with rows . Then

In order to apply Lemma 3.1, we need to bound the right hand side. This is done in the following proposition.

Proposition 3.2 (Tail bound on ).

Let be the rows of . Then

We will prove this important proposition in Section 5.

To continue, let denote the event

| (15) |

By Proposition 3.2, we have

| (16) |

Set

| (17) |

Sample a matrix from the distribution . Let be the submatrix formed by random rows of . If the rows of satisfies , then by Lemma 3.1 and the definition of , we have

By Markov’s inequality,

(The expectation and probability in the last two estimates are with respect to the random choice of the rows; the matrix is fixed and satisfies .)

Let be the event that

Finally, let be the event that

We are going to view both as events in the product space generated by and the random choice of the rows. A simple calculation shows that if hold, then

It follows that

Arguing similarly, we have

Our next tool is a linear algebraic lemma that connects the submatrices of to matrices obtained by projecting the row vectors of onto a subspace.

Lemma 3.3 (Projection lemma).

Let be integers, let be the real or complex field, let be an -valued invertible matrix with columns , and let denote the rows of . Let be the matrix with rows . Let be the -dimensional subspace of formed as the orthogonal complement of the span of , which we identify with via an orthonormal basis, and let be the orthogonal projection to . Let be the matrix with columns . Then is invertible, and we have

In particular, we have

for all .

We prove this lemma in Appendix B.

For any fixed value of the rows , we choose a projection as above. The exact choice of is not terribly important so long as it is made independently of the rows ; for instance, one could pick uniformly at random with respect to the Haar measure on all such available projections, independently of .

Applying Lemma 3.3 twice, and noticing that since the rows of have identical distribution, we can rewrite the inequalities in question as

and

respectively, where

(with the convention that if ) and

and is the matrix with rows , and is the orthogonal projection to the -dimensional space orthogonal to the columns of , where we identify with via some orthonormal basis of , chosen in some fashion independent of first columns .

The final, and key, point in the proof is to show that the distribution of is very close to that of . We are going to need the following high-dimensional generalization of the classical Berry-Esseen central limit theorem, which we will prove in Appendix D.

Proposition 3.4 (Berry-Esséen-type central limit theorem for frames).

Let , let be the real or complex field, and let be -normalized and have finite third moment . Let be a normalized tight frame for , or in other words

| (18) |

where is the identity matrix on . Let denote the random variable

where are iid copies of . Similarly, let be formed from iid copies of . Then for any measurable set and any , one has

where

is the topological boundary of , and and is the distance using the metric on . The implied constant depends on the third moment of .

In order to apply this result, we need to ensure non-degeneracy of the subspace . This is done in the following proposition, which we will proved in Section 4.

Proposition 3.5 ( is non-degenerate).

Let denote the event that there does not exist a unit vector in such that . If is a sufficiently small absolute constant, then

An important point here is that does not depend on . For instance, we will be able to take .

The idea that normal vectors are non-degenerate was considered in [43] and has since then become an important part in several papers on the least singular value problem, e.g. [34], [35], [36], [37], [44], [45], [47], [48]. The notion of non-degeneracy here is, however, somewhat different from those considered before. In the above mentioned papers, it was typically required that no small set of coordinates (say coordinates) contains most of the mass of the vector (in other words, one cannot compress the vector into a much shorter one). In contrast, we require here that no individual coordinate can contain a significant (but not overwhelming) portion of the mass.

Let us take this proposition for granted for now, and condition on

so that holds; note that remain iid under this conditioning. We can then write

where the are iid copies of , and is the matrix with all rows vanishing except the row, which is equal to , where is the basis vector of . Since is a partial isometry, , which implies that

where we view identify the space of matrices with the vector space in the standard manner.

Now let be the set of all matrices such that , thus

Applying Proposition 3.4 (with ) and the definition of the event , we thus have

where is a parameter to be chosen later. But by (36) and the crude bound

for any matrix , we see that if is an matrix in , then

and thus

Setting (say), we see from construction of that , if is large enough depending on . Also, we can absorb the error into the main term by replacing by a slightly larger quantity, e.g.

Integrating over all obeying , and then using Proposition 3.5 and the above argument, we conclude that

| (19) |

A similar argument gives

| (20) |

where

At this point we could use Theorem 1.1 and obtain a qualitative version of Theorem 1.3. This would result in error terms rather than . However, one only needs a little more effort to obtain the full result. The estimates (19), (20) hold with replaced by ; adjusting appropriately (as well as the implied constants defining ), one obtains the bounds

| (21) |

and

| (22) |

This bound is established under the hypothesis (14), but as discussed at the beginning of the section, we may easily remove this hypothesis. In particular, the above bounds now hold for the gaussian distribution . Meanwhile, from Theorem 1.1 we have

| (23) |

Iterating222One way to interpret this iteration is to view (21), (22) as asserting that the random variables form a Cauchy sequence in the Lévy metric. (21), (22) and using (23) to pass to the limit (and adjusting the implied constants in the definition of , again), we conclude that

and

since is absolutely integrable and decays exponentially at infinity, we thus have

Inserting this bound (with replaced by ) into (19), (20) and using the continuity of again, we obtain (13), and Theorem 1.3.

Remark 3.6.

The above argument used the explicit limiting statistics for the hard edge of the gaussian random matrix spectrum in Theorem 1.1. If one refused to use this theorem, the best one could say using the above argument is that there exists a random variable taking values in the positive real line and independent of and such that

for any . (We can replace by by slightly changing the value of .) In other words, the random variables converge at some polynomial rate with respect to the Lévy metric to a universal limit depending only on the field . Theorem 1.1 can then be viewed as a computation as to what this universal limit is.

4. Non-degeneracy of normal vectors

In this section we prove Proposition 3.5. Let be a sufficiently small constant. By the union bound and symmetry, it suffices to show that

| (24) |

Let be such that the event in (24) occurs. Since , we have

where is the matrix with rows . We write , where is a column vector whose entries are iid copies of , and is a matrix whose entries are also iid copies of . We similarly write where . Then we have

| (25) |

Our first tool here is the following lemma, which asserts that with overwhelming probability, a random matrix has many small singular values. We will prove this lemma in Appendix F.

Lemma 4.1 (Many small singular values).

Let , and let be -normalized or -normalized, such that almost surely for some sufficiently small absolute constant . Then there are positive constants such that with probability , has at least singular values in the interval .

The next tool has a geometric flavor. It asserts that the orthogonal projection of a random vector onto a large subspace is strongly concentrated.

Lemma 4.2 (Concentration of the projection of a random vector).

Let be integers, let , let be the real or complex field, let be -normalised with almost surely, and let be a subspace of of dimension . Let , where are iid copies of . Suppose that for some sufficiently large absolute constant . Then

This lemma is an extension of the special case considered in [43], in which is Bernoulli. We are going to prove this lemma in Appendix E.

Applying Lemma 4.1 to an block of and using the interlacing law (Lemma B.2), we conclude (given that is sufficiently large) that with probability , has at least singular values of size , for some absolute constant . This implies the existence of a subspace of dimension such that , where is the orthogonal projection to . Let us condition on the event that this is the case (note that this event does not depend on ). Then we have

Combining this with (25) and the hypothesis , we conclude that

5. A lower bound for the distance between a random vector and a random hyperplane

In this section we prove Proposition 3.2. This type of result is somewhat related to the lower tail bounds on the lowest singular value in the literature (e.g. [25], [34], [36], [37], [44], [45], [48]). There are two basic means to obtain such bounds, namely via Littlewood-Offord theorems and via Berry-Esséen-type central limit theorems. We will rely solely on the second route (cf. [25], [36, Section 2.3]).

Let us begin with a simple lemma.

Lemma 5.1 (Distance from vector to hyperplane controls inverse).

Let , let be the real or complex field, let be an -valued invertible matrix with columns , and let denote the rows of . Then for any , we have

where is the hyperplane spanned by .

One can directly verify this lemma using the identity . It is also the special case of Lemma 3.3.

To start, we first study the distribution of . Let us temporarily condition on (i.e. freeze) the vectors , leaving random, and let be a unit normal vector to the hyperplane spanned by . Applying Proposition 3.5, we see that with probability , we have for some absolute constant . Suppose that this event occurs. If we write , where are iid copies of , then we have

Applying333When , one could also use the classical Berry-Esséen theorem, Proposition D.1. Proposition 3.4, we thus see that for any and , we have

setting we conclude

We can bound by (when , we have the stronger bound of , though we will not exploit this). By symmetry, we thus obtain the lower tail estimate

| (27) |

Notice that a slight modification of the above argument also yields the following corollary:

Corollary 5.2 (Random distance is gaussian).

Let be random vectors whose entries are iid copies of . Then the distribution of the distance from to is approximately gaussian, in the sense that

A naive application of the union bound to (27) is clearly insufficient to establish (26), since we have distances to deal with. However, we can at least use that bound to show that

for any .

The key fact that enables us to overcome the ineffectiveness of the union bound is that the distances are correlated. They tend to be large or small at the same time. Quantitatively, we have

Lemma 5.3 (Correlation between distances).

Let , let be the real or complex field, let be an -valued invertible matrix with columns , and let denote the distance from to the hyperplane spanned by . Let , let denote the orthogonal complement of the span of , and let denote the orthogonal projection onto . Then

We are going to prove this lemma in Appendix C.

Fix and ; then (if is sufficiently large compared with ) we have

| (28) |

To control the other distances for , we use Lemma 5.3, which gives the lower bound

| (29) |

where is the orthogonal projection to the -dimensional space orthogonal to .

6. Extensions of Theorem 1.3

In this section, we describe several extension of Theorem 1.3, mentioned briefly at the end of the introduction. As an application, we show that our results determine the distribution of the condition number of , extending results of Edelman from [9].

6.1. Joint distribution of least singular values

The proof of Theorem 1.3 can be adapted to control the joint distribution of the bottom singular values of , for a small power of . More precisely, define to be the random variable

Then a routine modification of the proof of Theorem 1.3 gives

Theorem 6.2 (Universality for ).

Let be the real or complex field, let be -normalized, and suppose for some sufficiently large absolute constant . If is a sufficiently small absolute constant, then we have

for all and all measurable , where is the set of all points in which lie within (in norm) of the topological boundary of .

Indeed, one simply repeats the arguments for Theorem 1.3 (which is basically the case) but acquires losses of throughout the argument, which will be acceptable if we force to be a sufficiently small power of , and if one shrinks as necessary; we omit the details.

Now we focus on the case when is independent of , then Theorem 6.2 asserts that converges in the (-dimensional) Lévy metric to a limiting distribution on . The precise value of this limiting distribution is complicated to state, but can in principle be computed from the following asymptotics of Forrester [11] in the complex case :

Theorem 6.3 (Bessel kernel asymptotics at the hard edge, complex case).

[11] Let be an integer, and let be a symmetric function. Then the expression

converges as to the limit

where is the Bessel kernel

where is the Bessel function

In the real case , there is a similar formula, but is a now a matrix-valued kernel, also defined in terms of Bessel functions, which is somewhat more complicated to state; see [28] for details.

As mentioned above, these -point correlation asymptotics are, in principle, sufficient to reconstruct the asymptotic distribution of . For instance, this is done for in [12] (in particular, recovering the results in Theorem 1.1), and for and in [13]. However, the computations rapidly increase in complexity as increases, and a closed-form expression for the limit in the general case does not appear to currently be in the literature. On the other hand, one can apply Theorem 6.2 directly to results such as Theorem 6.3 to conclude that the same asymptotics are in fact valid for all -normalized (and similarly that the asymptotics in [28] are valid for all -normalized ); we omit the details.

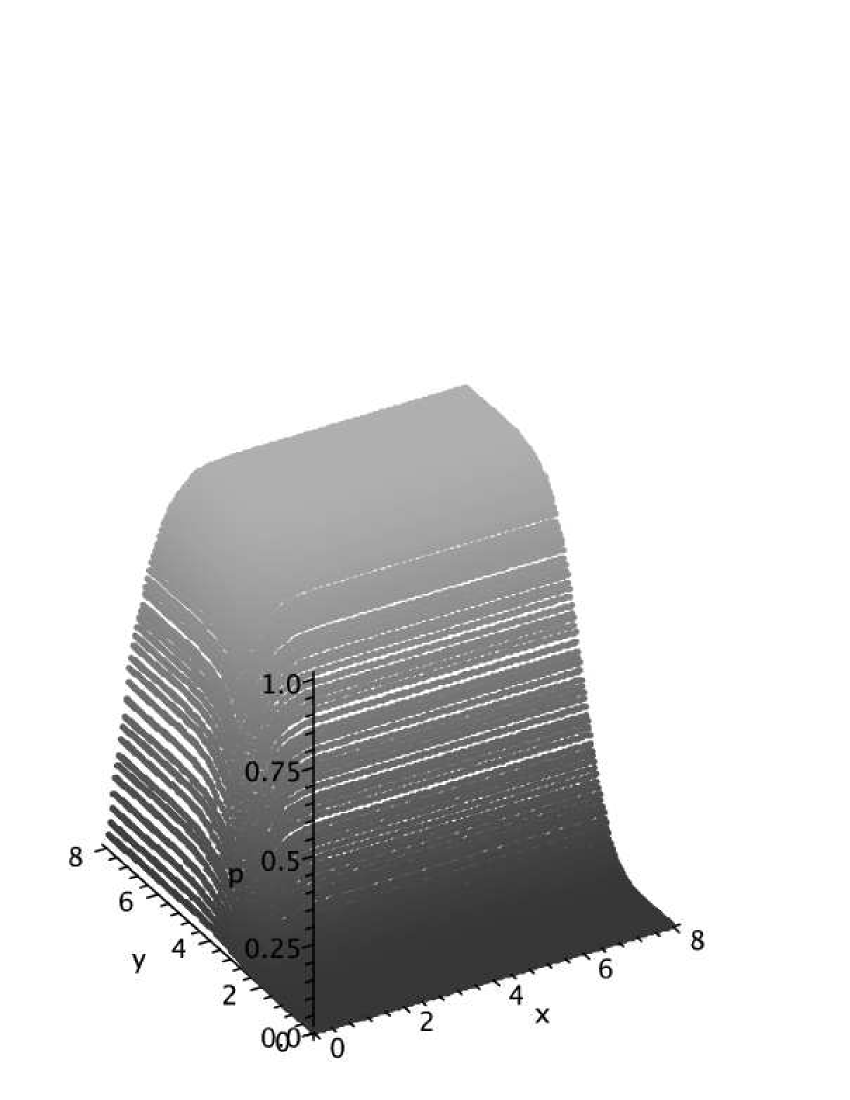

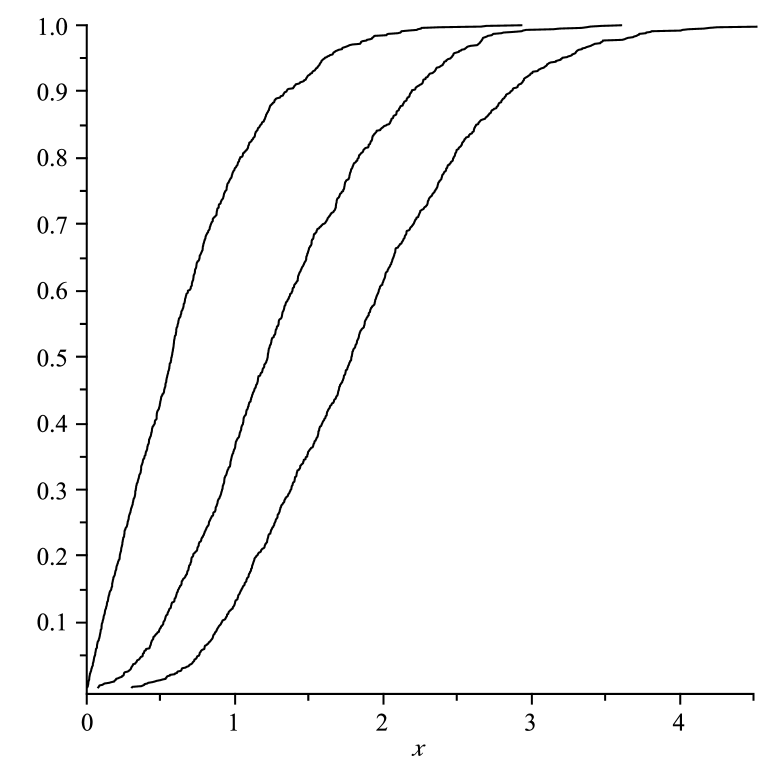

Bernoulli Gaussian

Figure 3 shows the joint distribution of the smallest two singular values for Bernoulli and gaussian distributions.

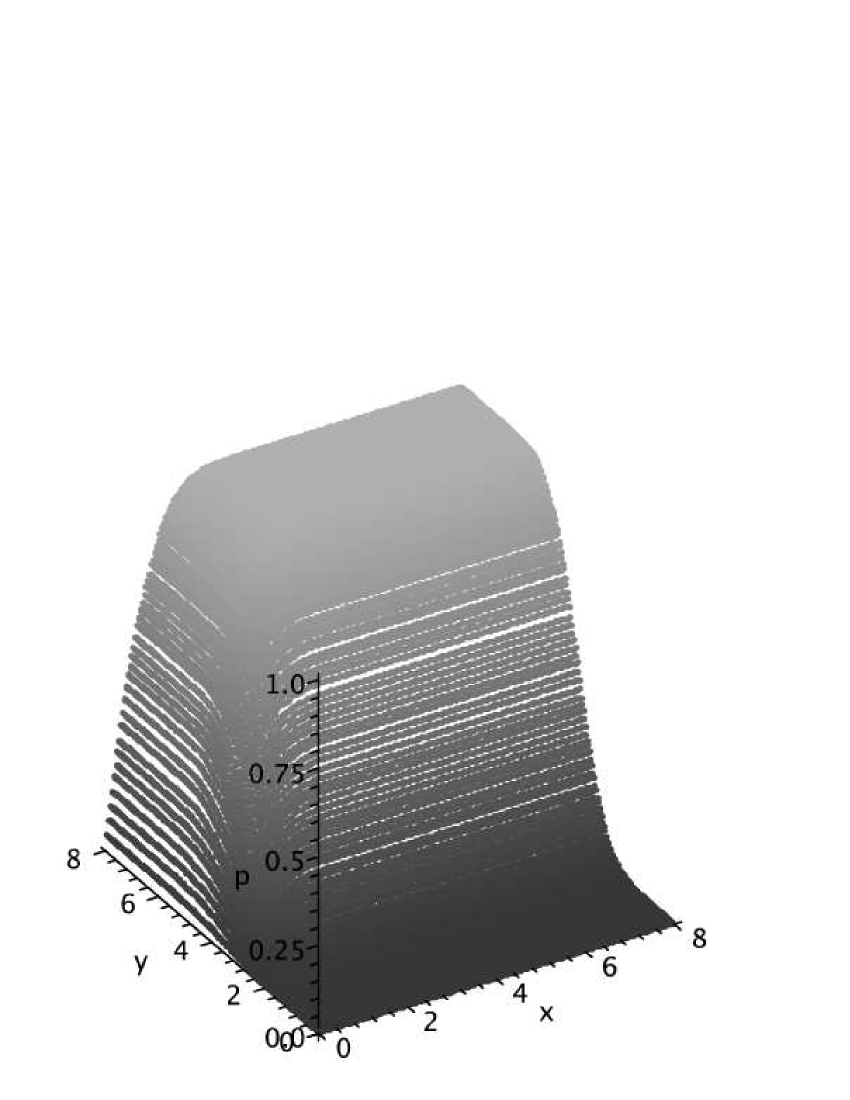

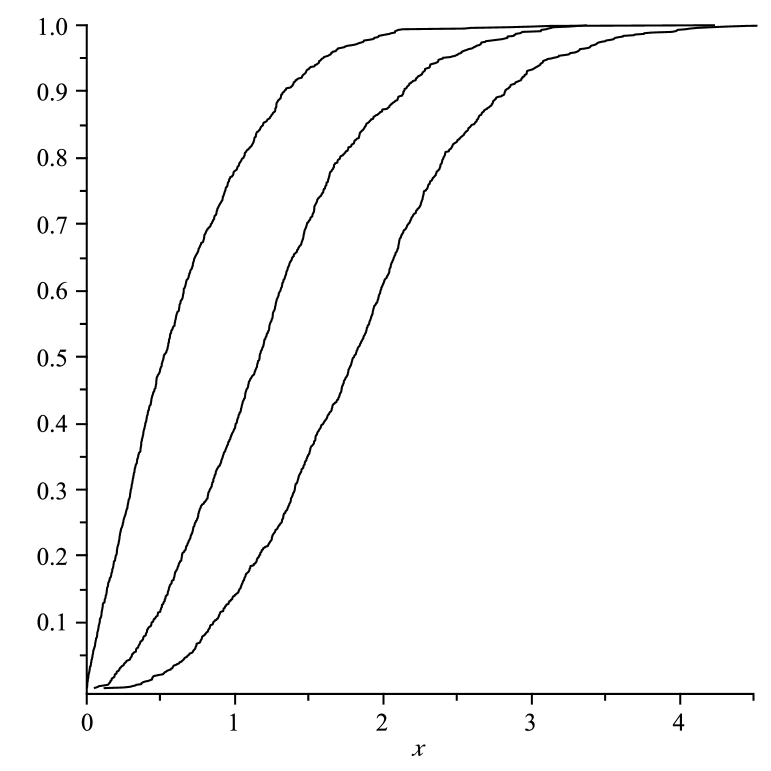

Bernoulli Gaussian

Figure 4 plots the functions , where , for Bernoulli and gaussian distributions.

6.4. Rectangular matrices

We can use our method to consider the least singular value of a rectangular matrix of the dimension , where is a constant. In fact, we can reduce this problem to the square case by adding a (dummy) set of rows vectors which form an orthonormal complement of the row vectors of the matrix. We consider these dummy vectors as the first vectors of the (now square) matrix and repeat the proof. The additional vectors remain the same after the projection and by removing them we obtain an matrix which is asymptotically gaussian. Thus, we will be able to compare the least singular value of the original matrix with this one.

The limiting distribution of the least singular value of random matrices with gaussian entries (for constant) can be computed, at least in principle. However, we cannot find a reference for this. Thus, we are going to phrase the result here in the spirit of Remark 3.6. To this end, denotes the random matrix whose entries are iid copies of .

Theorem 6.5 (Universality for the least singular value of rectangular matrices).

Let be - or -normalized, and suppose for some sufficiently large absolute constant . Let be a constant. Let , and . Then there is a constant such that for any

if is -normalized and

if is -normalized.

Bernoulli Gaussian

Figure 5 plots the functions , where , for Bernoulli and gaussian distributions.

To conclude this section, let us mention two important recent results. In [37], Rudelson and Vershynin obtained strong tail estimates for the smallest singular value of random rectangular matrices of all possible sizes. In [15] Feldheim and Sodin considered the case when is large, and proved universality for the distribution of the least singular value of random matrices with entries having sub-gaussian tails. (In this case the least singular value is large, of order , with high probability.)

6.6. Random matrices with not necessarily identical entries

All results hold if we drop the condition that the entries of have the same distribution. In the proofs, it is only important that the these entries are all normalized, independent, and their -moment is uniformly bounded. The fact that they are iid copies of has not played any important role. The only place where this information was used is in the paragraph following Lemma 3.3 (this allows one to fix the random rows of to be the first ). But we can easily avoid this by conditioning on the choice of the rows of . Thus we have the following extension of Theorem 1.3.

Theorem 6.7.

Let be - or -normalized, independent random variables such that for some sufficiently large absolute constants and . Then for all , we have

| (31) |

if are all -normalized, and

if are all -normalized, where is an absolute constant. The implied constants in the notation depend on but are uniform in .

The reader is invited to formalize the extensions of the results in the previous two subsections regarding joint distribution of the least -singular values and rectangular matrices.

Figure 6 shows an empirical demonstration of this theorem.

6.8. Distribution of the condition number

Let be an matrix, its condition number is defined as

Motivated by an earlier study of von Neuman and Goldstein [30], Edelman [9] studied the distribution of when is gaussian. His results can be extended for the general setting in this paper, thanks to Theorem 1.3 and the well known fact that the largest singular value is concentrated strongly around .

Lemma 6.9.

Under the setting of Theorem 1.3, we have, with probability , .

One can prove this lemma by combining [5, Theorem 5.8] with the tools in Appendix F or by following the arguments in [1, 17]. See also [35, 37] for references.

Corollary 6.10.

Let be - or -normalized, independent random variables such that for some sufficiently large absolute constants and . Then for all , we have

| (32) |

if are all -normalized, and

if are all -normalized, where is an absolute constant. The implied constants in the notation depend on but are uniform in .

Appendix A Estimating singular values via random sampling

Lemma A.1 (Random sampling).

Let be integers. be an real or complex matrix with rows . Let be selected independently and uniformly at random, and let be the matrix with rows . Then

Proof.

Let denote the coefficients of , thus . For , the entry of is given by

| (33) |

For , the random variables are iid with mean and variance

| (34) |

and so the random variable (33) has mean zero and variance . Summing over , we conclude that

Discarding the second term in (34) we conclude

Performing the summations, we obtain the claim. ∎

Combining this lemma with the Hoefmann-Wielandt theorem (Lemma B.1) we conclude that

Now observe that if , then by the standard birthday paradox computation444One could remove this condition by reworking the second moment computation in Lemma A.1 when are sampled with replacement (and thus have some slight correlation with each other), but we will not do so here since in our applications will be a small power of ., the rows are distinct with probability . Conditioning on this event, we thus see that if are sampled from without replacement, that

| (35) |

The inequality (35) is valid for deterministic matrices . If is a random matrix (with the being sampled independently of ), then we may take expectations of (35) for each instance of and conclude that

Now assume that the random matrix is row-exchangeable, i.e. the distribution of is stationary with respect to row permutations . For fixed and distinct , the distribution of is independent of the choice of . Crudely bounding by , we conclude

Corollary A.2 (Sampling of row-exchangeable matrices).

Let be integers with , let be a row-exchangeable random matrix with rows , and let be the matrix with rows . Then

Remark A.3.

One could use row-exchangeability here to instead simplify as , but it will turn out that this will not be useful for us, as we will need to truncate in any event in order to assure that is bounded.

Remark A.4.

In our applications, is going to be the inverse of (after conditioning away some bad but rare events in which is close to degenerate), and the summand of most interest on the left-hand side is the summand. We expect to be of size about , and we also expect the to have size about (thanks to Lemma 5.1 and basic heuristics about the distance between a random vector and a random hyperplane). So, as soon as is a non-trivial power of , we expect Corollary A.2 to yield an approximation of the form (11).

Appendix B Linear algebra

In this appendix we collect various basic facts from linear algebra which we will rely upon in this paper. We begin with the Hoeffman-Wielandt theorem, which controls the variation of singular values of a matrix using the Frobenius norm.

Lemma B.1 (Hoeffman-Wielandt theorem).

For any two self-adjoint matrices , we have

As a corollary, for any two matrices , we have

Proof.

It suffices to prove the first inequality, which we rewrite as

for self-adjoint . By the fundamental theorem of calculus (or a compactness argument) and the triangle inequality in , it suffices to show the infinitesimal version

of this inequality for fixed and sufficiently small . But if we diagonalise , the left-hand side can be computed (up to errors of ) as times the norm of the diagonal of , and the claim follows. ∎

Using the minimax characterizations

of the singular values, where ranges over -dimensional subspaces of , one obtains Weyl’s bound

| (36) |

for any matrices . Another easy corollary of the minimax characterization is

Lemma B.2 (Cauchy interlacing law).

Let be an matrix, and let be a matrix formed by taking of the rows of . Then

for all , with the convention that for .

Next, we prove the elementary but crucial projection lemma (Lemma 3.3) that relates a random sample of an inverse matrix, to a randomly projected version of the original matrix. For the reader’s convenience, we restate this lemma.

Lemma B.3 (Projection lemma).

Let be integers, let be the real or complex field, let be an -valued invertible matrix with columns , and let denote the rows of . Let be the matrix with rows . Let be the -dimensional subspace of formed as the orthogonal complement of the span of , which we identify with via an orthonormal basis, and let be the orthogonal projection to . Let be the matrix with columns . Then is invertible, and we have

In particular, we have

for all .

Proof.

By construction, we have for all . In particular, lie in , and

for . Thus is invertible, and the rows of are given by . Thus the entry of is given by , while the entry of is given by . Since lie in , and is an isometry on , the claim follows. ∎

Appendix C Correlation between distances

Lemma C.1 (Relationship between different distances).

Let , let be the real or complex field, let be an -valued invertible matrix with columns , and let denote the distance from to the hyperplane spanned by . Let , let denote the orthogonal complement of the span of , and let denote the orthogonal projection onto . Then

Remark C.2.

In practice, we will be able to get good upper and lower bounds on . The above lemma asserts that as long as the are bounded away from zero, all the other will also be bounded away from zero.

Proof.

By relabeling we may take . For , write . By applying to both and , we see that is the distance from to for any . Since is isomorphic to , we see (on replacing with , and with ) that we may assume that , thus is trivial and our task is now to show that

Let be the rows of . By Corollary 5.1, , so our task is now to show that

On the other hand, observe (since is a dual basis to ) that the vector

is orthogonal to and has an inner product of with , and thus must equal . By the triangle inequality and Cauchy-Schwarz we thus obtain the claim. ∎

Appendix D Berry-Esseen type results

Let us first state the classical Berry-Esséen central limit theorem (see e.g. [41]):

Proposition D.1 (Berry-Esséen theorem).

Let be real numbers with

| (37) |

and let be a -normalized random variable with finite third moment . Let denote the random variable

where are iid copies of . Then for any we have

where the implied constant depends on the third moment of . In particular, by (37) we have

Next, we prove the key Proposition 3.4, which can be seen as a high-dimensional extension of Proposition D.1. Let us restate this proposition for the reader’s convenience.

Proposition D.2 (Berry-Esséen-type central limit theorem for frames).

Let , let be the real or complex field, and let be -normalized and have finite third moment . Let be a normalized tight frame for , or in other words

| (38) |

where is the identity matrix on . Let denote the random variable

where are iid copies of . Similarly, let be formed from iid copies of . Then for any measurable set and any , one has

where

is the topological boundary of , and and is the distance using the metric on . The implied constant depends on the third moment of .

Proof.

We shall just prove the upper bound

as the lower bound then follows by applying the claim to the complement of .

Let be a bump function supported on the unit ball of total mass , let be the approximation to the identity

and let be the convolution

| (39) |

where is the indicator function of . Observe that equals on , vanishes outside of , and is smoothly varying between and on . Thus it will suffice to show that

We now use a Lindeberg replacement trick (cf. [24, 32]). Let be iid copies of . From (38) and the fact that the distribution of centered gaussian random variables are completely determined by their covariance matrix, we see that

Thus if we define the random variables

we have the telescoping triangle inequality

| (40) |

For each , we may write

where

By Taylor’s theorem with remainder we thus have

| (41) |

and

| (42) |

in the real case , with a similar formula in the complex case obtainable by decomposing into real and imaginary parts, which we will omit here. A computation using (39) and the Leibnitz rule reveals that all third partial derivatives of have magnitude , and so by Cauchy-Schwarz we have

Observe that , are independent of , and have the same mean and variance (in the complex case , we would use the covariance matrix of the real and imaginary parts rather than just the variance). Subtracting (41) from (42) and taking expectations (using the bounded third moment hypothesis on ) we conclude that

and thus by (40)

On the other hand, by taking traces of (38) we have

and the claim follows. ∎

Remark D.3.

In our applications, and will be a very small power of . The theorem then becomes non-trivial as soon as one obtains an upper bound of the form on the vectors for some absolute constant .

Remark D.4.

Suppose was now an arbitrary complex random variable of zero mean and finite variance. If the covariance matrix of and was a scalar multiple of the identity, then one is essentially in the -normalized case and Proposition D.2 applies. If instead the covariance matrix was degenerate and the had purely real coefficients, then one is in the -normalized case and Proposition D.2 again applies. But the situation is more complicated when the covariance matrix has two distinct non-zero eigenvalues, and depends to the extent to which the phases of are aligned. The question of what happens to the least singular value of in this case seems to be an interesting one (presumably, there is no alignment of phases and one should essentially revert to the -normalized case), but we will not pursue it here.

Appendix E Concentration

Let us state a powerful theorem of Talagrand. Let be probability spaces equipped with measures , and be the product space equipped with the product measure . A point has coordinates .

For a unit vector with non-negative coordinates and , define

For a subset and , let

and

In practice, the following (equivalent) definition of is useful. Define

| (43) |

where , as usual, denotes the Euclidean distance.

We will use heavily the following corollary of Theorem E.1.

Theorem E.2.

Let be the unit disk . For every product probability on , every convex -Lipschitz function , and every ,

where denotes the median of .

This corollary is the complex version of [23, Corollary 4.10] and can be obtained by slightly modifying its proof. We provide the (simple) details for the sake of completeness.

Proof.

By Caratheodory’s theorem there are with such that is an affine combination of the . In other words, there are positive numbers such that and

Let () be the th coordinate of (), respectively. Let be the point in that corresponds to (with respect to the definition of ). We have

Since (here is the only place where we use the fact that has bounded perimeter), it follows

Notice that the right hand side is at least the Euclidean distance from to the convex hull of , so we have

| (44) |

Let be a function as in the statement of the theorem. Let . By the definition of median . Furthermore, as is convex, so is . On the other hand, if , then by the Lipschitz property , which, via (44), implies that . By Theorem E.1, we have

which implies

For the lower tail, set and argue similarly. ∎

An easy change of variables reveals the following generalization of this inequality: if is supported on a dilate of the unit disk for some , rather than itself, then for every we have

| (45) |

Theorem E.2 shows concentration around the median. In applications, it is usually more useful to have concentration around the mean. This can be done via the following lemma, which shows that concentration around the median implies that the mean and the median are close.

Lemma E.3.

Let be a random variable such that for any

Then

The bound 100 is ad hoc and can be replaced by a much smaller constant.

Proof.

Set and let be the distribution function of . We have

The lower bound can be proved similarly. ∎

Lemma E.4 (Concentration estimate).

Let be integers, let , let be the real or complex field, let be -normalised with almost surely, and let be a subspace of of dimension . Let , where are iid copies of . Suppose that for some sufficiently large absolute constant . Then

Proof.

The map is clearly convex and -Lipschitz. Applying (45) we conclude that

| (46) |

for any . On the other hand, if is the orthogonal projection to , then (by the -normalization of ) we have

By Chebyshev’s inequality, we conclude that the median of is at most . A simple calculation reveals that the fact

implies

(This is easiest to see by working in the contrapositive.) Thus,

Integrating this, we see that

if for a sufficiently large , we conclude that

and the claim follows from (46). ∎

Remark E.5.

One can obtain a more precise result by also computing the variance of ; see [43, Lemma 2.2] for this computation in the model case of the Bernoulli random variable.

Appendix F Random matrices have many small singular values

In this section, we prove Lemma 4.1, which we now restate.

Lemma F.1 (Many small singular values).

Let , and let be -normalized or -normalized, such that almost surely for some sufficiently small absolute constant . Then there are positive constants such that with probability , has at least singular values in the interval .

The first ingredient of the proof is the following result on the rate of convergence to Marchenko-Pastur law.

Theorem F.2 (Rate of convergence to Marchenko-Pastur law).

[5] There are positive constants such that the following holds. Let be - or -normalized random variable with bounded -moment. Then for any ,

In other words, the ESD of the Wishart matrix converges to Marchenko-Pastur law with rate almost surely.

The values for are quite reasonable. In [5, Theorem 8.29], it is shown that one can set and , for any fixed . A more recent result [16, Theorem 1.2] claimed that one can set and .

This theorem, however, does not imply the desired claim, as it only shows that has many small singular values with probability , while we need the failure probability to be exponentially small.

For a constant , let be the number of singular values in the interval . From Theorem F.2, we can at least conclude that

| (47) |

We are going to show that for some sufficiently small positive constant

| (48) |

One can achieve this goal by following, with few minor modifications, the powerful approach introduced by Guionnet and Zeitouni in [17]. We present the details for the sake of completeness and the readers’ convenience.

Consider a random hermitian matrices with independent entries with support in a compact region with diameter . Let be a real, convex , -Lipschitz function and define

where are the eigenvalues of . We are a going to view as the function of the variables . The main difference between the current setting and that of [17] is that here we do not require the real and imaginary parts of be independent.

We use the following two lemmas from [17].

Lemma F.3.

is a convex function.

This lemma is a consequence of [17, Lemma 1.2(a)].

Lemma F.4.

is -Lipschitz.

This lemma can be derived from [17, Lemma 1.2(b)]. We give here a short, different, proof.

Proof.

(Proof of Lemma F.4) Consider two matrices and with entries and and eigenvalues and (in decreasing order), respectively. By Lemma B.1,

On the other hand, by Cauchy-Schwarz and the fact that is -Lipschitz,

It follows that

completing the proof. ∎

By Theorem E.2, we obtain the following theorem, which is an extension of [17, Theorem 1.3] to the case where the real and imaginary parts of are not necessarily independent.

Theorem F.5.

Let be as above. Then there is a constant such that for any

where is the bound on the absolute values of the entries of .

It will be better for us to replace by . By Lemma E.3 and rescaling,

Thus, if , then (by adjusting if necessary) we have

| (49) |

Recall that we are considering the singular values of a (random) non-hermitian matrix instead of the eigenvalues of a hermitian matrix . This problem can be easily dealt with by the standard trick of defining and

It is well known that if the singular values of are , then the eigenvalues of are . The number of singular values of in is thus half of the number of eigenvalues of in . In order to estimate the last quantity, it is natural to define

where is the indicator function of and are the eigenvalues of . This function is, however, not convex and Lipschitz. On the other hand, we can easily overcome this problem by constructing two real functions such that

-

•

are symmetric, convex and -Lipschitz, for some sufficiently large constant .

-

•

for any .

-

•

for any .

-

•

for any .

Define with respect to . Applying (49) to with , for some small positive constant (to be chosen), we have

| (50) |

given the fact that where is sufficiently small and that (the bound on the absolute values of the entries) is a sufficiently small power of .

By (47) and choosing sufficiently small, we can assume . By the triangle inequality and (50), it follows that

The desired bound (48) follows from this and the fact that

Acknowledgement. We would like to thank P. Wood for the figures used in this paper and his careful reading and suggestions, O. Zeitouni for a useful conversation concerning Appendix F, P. Forrester and B. Rider for enlightening remarks.

References

- [1] N. Alon, M. Krivelevich and V. Vu, Concentration of eigenvalue of random matrices, Israel Math. Journal, 131 (2002), 259-267

- [2] Z.D. Bai, Convergence rate of expected spectral distributions of large random matrices, Part II. Sample covariance matrices, Ann. Probab. 21 (1993), 625- 648.

- [3] Z.D. Bai, B. Miao, J. Tsay, A note on the convergence rate of the spectral distributions of large random matrices, Statist. Probab. Lett. 34 (1997), 95–101.

- [4] Z. D. Bai, B. Miao, J.-F. Yao, Convergence rates of spectral distributions of large sample covariance matrices, SIAM J. Matrix Anal. Appl. 25 (2003), 105–127.

- [5] Z. D. Bai and J. Silverstein, Spectral analysis of large dimensional random matrices, Science press, 2006.

- [6] J. Bourgain, P. Wood and V. Vu, On the singularity probability of random discrete matrices, submitted.

- [7] P. Drineas, R. Kannan, Ravi, M. Mahoney, Fast Monte Carlo algorithms for matrices. I. Approximating matrix multiplication. SIAM J. Comput. 36 (2006), no. 1, 132–157

- [8] G. Ben Arous, S. Péché, Universality of local eigenvalue statistics for some sample covariance matrices, Comm. Pure Appl. Math. 58 (2005), 1316–1357.

- [9] A. Edelman, Eigenvalues and condition numbers of random matrices, SIAM J. Matrix Anal. Appl. 9 (1988), 543–560.

- [10] A. Edelman, The distribution and moments of the smallest eigenvalue of a random matrix of Wishart type, Linear Algebra Appl. 159 (1991), 55–80.

- [11] P. J. Forrester, The spectrum edge of random matrix ensembles, Nuclear Phys. B 402 (1993), 709–728.

- [12] P. J. Forrester, Exact results and universal asymptotics in the Laguerre random matrix ensemble, J. Math. Phys. 35 (1994), no. 5, 2539–2551.

- [13] P. J. Forrester, N. S. Witte, The distribution of the first eigenvalue spacing at the hard edge of the Laguerre unitary ensemble, Kyushu J. Math. 61 (2007), no. 2, 457–526.

- [14] A. Frieze, R. Kannan, S. Vempala, Fast Monte-Carlo algorithms for finding low-rank approximations, J. ACM 51 (2004), no. 6, 1025–1041.

- [15] O. N. Feldheim and S. Sodin, A universality result for the smallest eigenvalues of certain sample covariance matrices, preprint.

- [16] F. Götze and A. Tikhomirov, The rate of convergence of spectra of sample covariance matrices, preprint.

- [17] A. Guionnet and O. Zeitouni, Concentration of the spectral measure for large matrices, Elec. Com. Prob. 5.

- [18] K. Johansson, Shape fluctuations and random matrices, Comm. Math. Phys. 209, 437-476 (2000).

- [19] I. Johnstone, On the distribution of largest principal component, Ann. Statist. 29, 2001.

- [20] J. Kahn, J. Komlós, E. Szemerédi, On the probability that a random matrix is singular, J. Amer. Math. Soc. 8 (1995), 223–240.

- [21] J. Komlós, On the determinant of matrices, Studia Sci. Math. Hungar. 2 (1967) 7–22.

- [22] J. Komlós, On the determinant of random matrices, Studia Sci. Math. Hungar. 3 (1968) 387–399.

- [23] M. Ledoux, The concentration of measure phenomenon, Mathematical Surveys and Monographs, Volume 98, AMS 2001.

- [24] J. W. Lindeberg, Eine neue herleitung des exponentialgesetzes in der wahrscheinlichkeitsrechnung, Math. Z. 15 (1922), 211–225.

- [25] A. Litvak, A. Pajor, M. Rudelson, N. Tomczak-Jaegermann, Smallest singular value of random matrices and geometry of random polytopes, Adv. Math. 195 (2005), no. 2, 491–523.

- [26] M.L. Mehta, Random Matrices and the Statistical Theory of Energy Levels, Academic Press, New York, NY, 1967.

- [27] V. A. Marchenko, L. A. Pastur, The distribution of eigenvalues in certain sets of random matrices, Mat. Sb. 72 (1967), 507–536.

- [28] T. Nagao, K. Slevin, Laguerre ensembles of random matrices: nonuniversal correlation functions, J. Math. Phys. 34 (1993), no. 6, 2317–2330.

- [29] T. Nagao, M. Wadati, Correlation functions of random matrix ensembles related to classical orthogonal polynomials, J. Phys. Soc. Japan 60 (1991), no. 10, 3298–3322.

- [30] J. von Neuman and H. Goldstein, Numerical inverting matrices of high order, Bull. Amer. Math. Soc. 53, 1021-1099, 1947.

- [31] L. A. Pastur, Spectra of random self-adjoint operators, Russian Math. Surveys 28 (1973), 1–67.

- [32] V. Paulauskas and A. Rackauskas, Approximation theory in the central limit theorem, Kluwer Academic Publishers, 1989.

- [33] B. Rider, J. Ramirez, Diffusion at the random matrix hard edge, to appear in Comm. Math. Phys.

- [34] M. Rudelson, Lower estimates for the singular values of random matrices, C. R. Math. Acad. Sci. Paris 342 (2006), 247–252.

- [35] M. Rudelson, R. Vershynin, The least singular value of a random square matrix is . C. R. Math. Acad. Sci. Paris 346 (2008), no. 15-16, 893–896.

- [36] M. Rudelson, R. Vershynin, The Littlewood-Offord Problem and invertibility of random matrices, Advances in Mathematics 218 (2008), 600–633.

- [37] M. Rudelson, R. Vershynin, The least singular value of a random rectangular matrix, Comptes rendus de l’Acad mie des sciences - Math matique 346 (2008), 893–896.

- [38] S. Smale, On the efficiency of algorithms of analysis, Bull. Amer. Math. Soc. 13, 87-121 (1985).

- [39] A. Soshnikov, A note on universality of the distribution of the largest eigenvalues in certain sample covariance matrices, J. Statist. Phys. 108 (2002), no. 5-6, 1033–1056.

- [40] D. Spielman, S.-H. Teng, Smoothed analysis of algorithms, Proceedings of the International Congress of Mathematicians, Vol. I (Beijing, 2002), 597–606, Higher Ed. Press, Beijing, 2002.

- [41] D. Stroock, Probability theory. An analytic view, Cambridge University Press, Cambridge, 1993.

- [42] M. Talagrand, A new look at independence, Ann. Prob. 24 (1996), no. 1, 1–34.

- [43] T. Tao, V. Vu, On random matrices: Singularity and Determinant, Random Structures and Algorithms 28 (2006), 1–23.

- [44] T. Tao, V. Vu, Inverse Littlewood-Offord theorems and the condition number of random discrete matrices, to appear in Annals of Mathematics.

- [45] T. Tao, V. Vu, The condition number of a randomly perturbed matrix, STOC’07—Proceedings of the 39th Annual ACM Symposium on Theory of Computing, 248–255, ACM, New York, 2007.

- [46] T. Tao and V. Vu, On the singularity probability of random Bernoulli matrices, Journal of the A. M. S. 20 (3), 2007, 603-628.

- [47] T. Tao, V. Vu, Random Matrices: The circular Law , Commun. Contemp. Math. 10 (2008), no. 2, 261–307.

- [48] T. Tao, V. Vu, Random matrices: A general approach for the least singular value problem , preprint.

- [49] T. Tao, V. Vu, Random matrices: Universality of ESDs and the circular law, submitted.

- [50] T. Tao, V. Vu, From the Littlewood-Offord problem to the Circular Law: universality of the spectral distribution of random matrices, to appear in the Bulletin of AMS.

- [51] Y. Q. Yin, Limiting spectral distribution for a class of random matrices, J. Multivariate Anal. 20 (1986), 50–68.