Quantitative law describing market dynamics before and after interest rate change

Abstract

We study the behavior of U.S. markets both before and after U.S. Federal Open Market Committee (FOMC) meetings, and show that the announcement of a U.S. Federal Reserve rate change causes a financial shock, where the dynamics after the announcement is described by an analogue of the Omori earthquake law. We quantify the rate of aftershocks following an interest rate change at time , and find power-law decay which scales as , with positive. Surprisingly, we find that the same law describes the rate of “pre-shocks” before the interest rate change at time . This is the first study to quantitatively relate the size of the market response to the news which caused the shock and to uncover the presence of quantifiable preshocks. We demonstrate that the news associated with interest rate change is responsible for causing both the anticipation before the announcement and the surprise after the announcement. We estimate the magnitude of financial news using the relative difference between the U. S. Treasury Bill and the Federal Funds Effective rate. Our results are consistent with the “sign effect,” in which “bad news” has a larger impact than “good news.” Furthermore, we observe significant volatility aftershocks, confirming a “market underreaction” that lasts at least 1 trading day.

I Introduction

Interest rate changes by the Federal Reserve provide a significant perturbation to financial markets, which we analyze from the perspective of statistical physics Econophys0 ; Econophys1 ; Econophys2 ; Econophys3 ; Econophys4 ; Econophys5 . The Federal Reserve board (Fed), in charge of monetary policy as the central bank of the United States, is one of the most influential financial institutions in the world. During Federal Open Market Committee (FOMC) meetings, the Fed determines whether or not to change key interest rates. These interest rates serve as a benchmark and a barometer for both American and international economies. The publicly released statements from the scheduled FOMC meetings provide grounds for widespread speculation in financial markets, often with significant consequences.

In this paper, we show that markets respond sharply to FOMC news in a complex way reminiscent of physical earthquakes described by the Omori law Omori1 ; Omori2 . For financial markets, the Omori law was first observed in market crashes by Lillo and Mantegna OmoriLillo , followed by a further study of Weber et al. OmoriWeber , which found the same behavior in medium-sized aftershocks. However, the market crash is only an extreme example of information flow in financial markets. This paper extends the Omori law observed in large financial crises to the more common Federal Reserve announcements, and suggests that large market news dissipates via power-law relaxation (Omori law) of the volatility. In addition to the standard Omori dynamics following the announcement, we also find novel Omori dynamics before the announcement.

The market dynamics following the release of FOMC news are consistent with previous studies of price-discovery in foreign exchange markets following marcroeconomic news releases MacroNews1 ; MacroNews2 . Furthermore, we hypothesize that the uncertainty in Fed actions, coupled with the pre-announced schedule of FOMC meetings, can increase speculation among market traders, which can lead to the observed market underreaction sentiment . Market underreaction, meaning that markets take a finite time to readjust prices following news, is not consistent with the efficient market hypothesis; Several theories have been proposed to account for this phenomena noEMH .

We analyze all scheduled FOMC meetings in the eight-year period 2000-2008 using daily data from http://finance.yahoo.com. Also, for the two-year period 2001-2002, we analyze the intraday behavior for 19 FOMC meetings using Trades And Quote (TAQ) data on the 1-minute time scale.

The paper is organized as follows: In Section II we describe the FOMC meetings and the Fed interest rate relevant to our analysis. In Section III.1 we analyze the response of the S&P100, the top 100 stocks (ranked by 12-month sales according to a 2002 BusinessWeek report) belonging to the 2002 S&P 500 index, over the 2000-2008 period using daily data. Using the relative spread between the 6-Month Treasury Bill and the Federal Funds Effective rate, we relate the speculation prior to the FOMC meetings to the daily market volatility, measured here as the logarithmic difference between the intraday high and low price for a given stock on the day of the announcement. In Section III.2 we study high-frequency intraday TAQ data on the 1-min scale for the S&P100, and find an Omori law with positive exponent immediately following the announcement of Fed rate changes. Further, we relate the intraday market response, (quantified by both the Omori exponent and Omori amplitude), to the change in market expectations before and after the announcement.

II FOMC Meetings, Fed Interest Rates and Treasury Bills

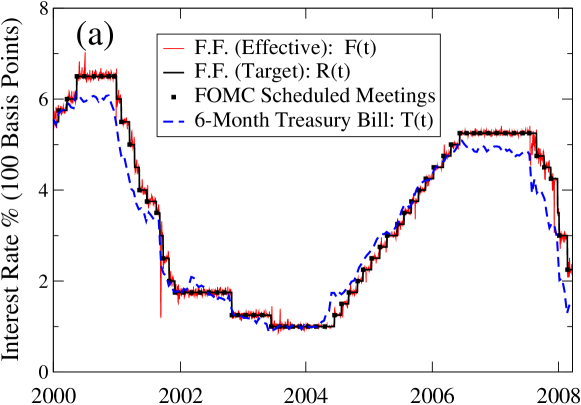

There are many economic indicators that determine the health of the U.S. economy. In turn, the health of the U.S. economy sets a global standard due to the ubiquity of both the U.S. dollar and the economic presence maintained through imports, exports, and the Global Market globalmarkets . The U.S. Federal Reserve Target rate, along with the Effective “overnight” rate, set the scale for interest rates in the United States and abroad. The Target rate is determined at FOMC meetings, which are scheduled throughout the year, with detailed minutes publicly released from these meetings. The Effective rate is a “weighted average of rates on brokered trades” between the Fed and large banks and financial institutions, and is a market realization of the Target rate FED . In Fig. 1 we plot the Federal interest rates over the 8-year period 2000-2008.

Our analysis focuses on the FOMC meetings after January 2000. Historically, the methods for releasing the meeting details have varied. In the 1990s, there was a transition from a very secretive policy towards the current transparent policy FOMCf . Since the year 2000, the Fed has released statements detailing the views and goals of the FOMC. This increase in public information has led to an era of mass speculation in the markets, revolving mainly around key economic indicators such as the unemployment rate, the Consumer Price Index, the money supply, etc. These economic indicators also influence the FOMC in their decision to either change or maintain key interest rates. As a result of this open policy, the Fed has used the “announcement effect” FOMCannouncementeffect to manipulate the federal funds market. Speculation has assumed many forms and new heights, evident in the implementation of new types of derivatives based on federal securities. For instance, options and futures are available at the Chicago Board of Trade which are based on Federal Funds, Treasury Bills, and Eurodollar foreign exchange. These contracts can be used to estimate the implied probability of interest rate changes, utilizing sophisticated methods focussed on the price movement of expiring derivative contracts FOMCnew ; FOMCa ; FOMCc ; FOMCe ; FOMCb ; FOMCd .

In the next section, we outline a simple method to measure speculation prior to a scheduled FOMC meeting using the 6-Month Treasury Bill and the Federal Funds Effective (“overnight”) rate. These data are readily available and are updated frequently at the website of the Federal Reserve FED . Because each FOMC meeting is met with speculation (in the weeks before the meeting) and anticipation (in the hours before the announcement), we identify the decision to change or not to change key interest rates as a market perturbation. The market response results from the systematic stress associated with the speculation and anticipation, which are not always in line with the FOMC decision.

III Empirical Results

III.1 Response to FOMC Meetings on Daily Time Scale

In this section we analyze the daily activity before and after 66 scheduled FOMC meetings over the 8-year period 2000-2008, where scheduled meetings are publicly announced at least a year in advance FED . We do not consider unscheduled meetings resulting in rate change, which contain an intrinsic element of surprise, and are historically infrequent (only 4 unexpected Target rate changes over the same period). Of primary importance, is the FOMC committee’s decision to change or not change the Target rate by some percent , where the absolute relative change has typically filled the range between and . This section serves as an initial motivation for the intraday analysis, and will also serve as a guide in developing a metric that captures market speculation. In this section we use the intraday high-low price range to quantify the magnitude of price fluctuations. In particular, we analyze the companies belonging to the S&P 100, and also the subset of 18 banking and finance companies referred to here as the “Bank” sector.

In Fig. 1(a) we plot , the time series for the 6-Month Treasury Bill, along with , the Federal Funds Effective rate, and , the Federal Funds Target rate, over the 8-year period beginning in January 2000. The relative difference between the 6-Month Treasury Bill and the Federal Funds Effective rate is an indicator of the future expectations of the Federal Funds Target rate FOMCf . Note that the 6-Month Treasury Bill has anticipatory behavior with respect to the Federal Funds Target (and hence Effective) rates. Other more sophisticated models utilize futures on Federal Funds and Eurodollar exchange, but these markets are rather new, and represent the highly complex nature of contemporary markets and hedging programs FOMCnew ; FOMCa ; FOMCc ; FOMCe ; FOMCb ; FOMCd . Hence, we use a simple and intuitive method for estimating market speculation and anticipation by analyzing the relative difference between the 6-Month Treasury Bill and the Federal Funds Effective rate.

Fig. 1(b) exhibits the typical interplay between the 6-Month T-Bill and the Federal Funds Effective rate before and after a FOMC meeting. The change in the value of the Effective rate results from market speculation, starting approximately one trading week (5 trading days) prior to the announcement. This change follows from the forward-looking Treasury Bill, which in the example in Fig. 1(b), is priced above the Federal Funds rate even 15 trading days before the announcement.

In order to quantify speculation and anticipation in the market prior to each scheduled FOMC meeting, we analyze the time series of the relative spread between and ,

| (1) |

As an example of this relation, in Fig. 1(c) we plot for the 15 days before and after a typical FOMC meeting resulting in a rate change. In order to study the speculation preceding the scheduled FOMC meeting, we calculate the average relative spread over the day period. We weight the days in the -day period leading up to the FOMC meeting day exponentially, such that the relative spread on the day before the announcement has the weight . Without loss of generality, we choose the value of days corresponding to two trading weeks ThetaDeltaPar . We define the speculation metric,

| (2) |

which is a weighted average of before the announcement, where the sums are computed over the range . The metric for the FOMC meeting can be positive or negative, depending on the market’s forward-looking expectations.

In order to quantify the market response to the speculation , we analyze the market volatility around each FOMC meeting. For a particular stock around the scheduled FOMC meeting, we take the daily high price , and the daily low price , for , where corresponds to , the day of the meeting. We then compute the high-low range for each trading day,

| (3) |

For each stock and each meeting, we scale the range by , the average range over the 41-day time sequence centered around the meeting day, resulting in the normalized volatility . Similarly, we use , the time series for the volume traded over the same period, to compute a weight for each stock corresponding to the normalized volume on the day of the FOMC meeting. We calculate this weight as , where is the average daily volume over the 41-day time sequence centered around the meeting day. We use a volume weight in order to emphasize the price-impact resulting from relatively high trading volume, since there are significant cross-correlations between volume change and price change VolPriceCC . Finally, we compute the weighted average volatility time series over all stocks and all meetings,

| (4) |

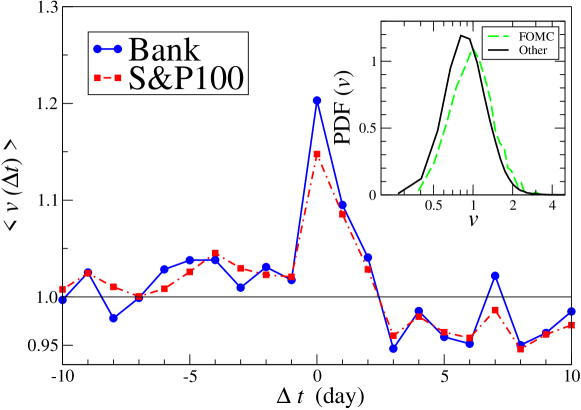

In Fig. 2 we plot the trend of average daily volatility defined in Eq. (4) for the 10 days before and after the scheduled announcements.

We observe a peak in on FOMC meeting days, corresponding to , with a more pronounced peak in the bank sector (Fig. 2). Stocks in the bank sector are strongly impacted by changes in Fed rates, which immediately influence both their holding and lending rates. On average there is a 15-20% increase in volatility on days corresponding to FOMC meetings.

In order to quantify the impact of a single FOMC announcement on day , we define the average market volatility

| (5) |

Here, and refer to the average and sum over records corresponding only to the day . Again, is a normalized weight, where now is the average daily volume over the entire 8-year period, since we compare many meetings across a large time span.

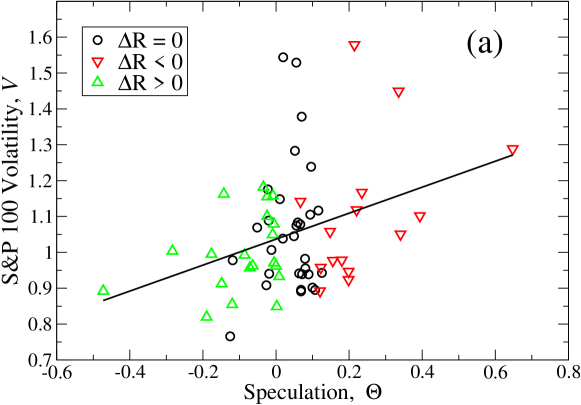

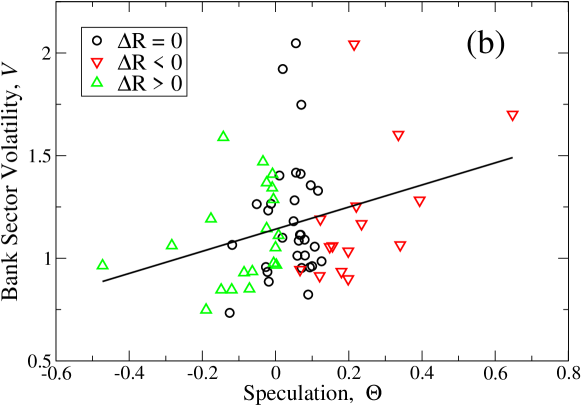

In Fig. 3 we plot the average volatility of the (a) S&P100 and (b) the subset of 18 banking stocks versus . For negative values of , for which corresponding to an expected rate increase, we observe a less volatile market response. Conversely, for larger positive values of , for which corresponding to a rate cut, there tends to be larger market fluctuations. Hence, the market responds differently to falling and rising rates, where the direction in rate change often reflects the overall health of the economy as viewed by the FOMC. Typically, the FOMC implements rate increases to fight inflation, whereas rate decreases often follow bad economic news or economic emergency. Hence, our findings are consistent with the empirical “sign effect”, in which “bad” news has a greater impact in markets than does “good” news MacroNews2 . Furthermore, there is also a tendency for large average volatility even when is small, possibly stemming from the extreme surprise characteristic of some FOMC decisions. In these cases, more sophisticated methods are needed to improve the predictions of market movement.

III.2 Intraday response to FOMC decision via an Omori Law

In the previous section we studied the market response on the daily scale. Now we ask the question, “What is the intraday response to FOMC news?” Here we analyze the TAQ data over the 2-year period Jan. 1, 2001 to Dec. 31, 2002. The reported times for the FOMC announcement are listed in Table 1 data . Inspired by the non-stationary nature of financial time series, methods have been developed within the framework of non-equilibrium statistical mechanics to describe phenomena ranging from volatility clustering ReturnIntervals1 ; ReturnIntervals3 ; ReturnIntervals2 to financial correlation matrices marketcorr0 ; marketcorr1 ; marketcorr2 .

We use the Omori law, originally proposed in 1894 to describe the relaxation of after-shocks following earthquakes, to describe the response of the market to FOMC announcements. Defined in Ref. OmoriLillo , the Omori law quantifies the rate of large volatility events following a singular perturbation at time . The shock may be exogenous (resulting from external news stimuli) or endogenous (resulting from internal correlations, e.g. “herding effect”) SornettePhysA ; SornetteEndoExo ; information ; earnings ; SornettePNAS . This rate is defined as,

| (6) |

where is the Omori power-law exponent.

Here we study the rate of events greater than a volatility threshold , using the high-frequency intraday price time series . The intraday volatility (absolute returns) is expressed as , where we use minute. To compare stocks, we scale each raw time series in terms of the standard deviation over the entire period analyzed, and then remove the average intraday trading pattern as described in Ref. OmoriWeber . This establishes a common volatility threshold , in units of standard deviation, for all stocks analyzed.

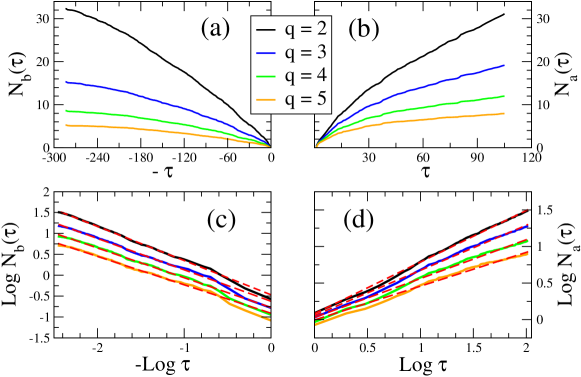

In the analysis that follows, we focus on , the cumulative number of events above threshold ,

| (7) |

which is less noisy compared to . Using , we examine the intraday market dynamics for 100 S&P stocks, before and after the FOMC announcement at , which typically occurs at 2:15 PM ET (285 minutes after the opening bell) for scheduled meetings.

| FOMC Date | (%) | T | ||

|---|---|---|---|---|

| 01/03/01** | 6 | -0.5 | -0.077 | 210 |

| 01/31/01 | 5.5 | -0.5 | -0.083 | 285 |

| 03/20/01 | 5 | -0.5 | -0.091 | 285 |

| 04/18/01** | 4.5 | -0.5 | -0.100 | 90 |

| 05/15/01 | 4 | -0.5 | -0.111 | 285 |

| 06/27/01 | 3.75 | -0.25 | -0.063 | 285 |

| 08/21/01 | 3.5 | -0.25 | -0.067 | 285 |

| 09/17/01** | 3 | -0.5 | -0.143 | 0 |

| 10/02/01 | 2.5 | -0.5 | -0.167 | 285 |

| 11/06/01 | 2 | -0.5 | -0.200 | 285 |

| 12/11/01 | 1.75 | -0.25 | -0.125 | 285 |

| 01/30/02 | 1.75 | 0 | 0.00 | 285 |

| 03/19/02 | 1.75 | 0 | 0.00 | 285 |

| 05/07/02 | 1.75 | 0 | 0.00 | 285 |

| 06/26/02 | 1.75 | 0 | 0.00 | 285 |

| 08/13/02 | 1.75 | 0 | 0.00 | 285 |

| 09/24/02 | 1.75 | 0 | 0.00 | 285 |

| 11/06/02 | 1.25 | -0.5 | -0.286 | 285 |

| 12/10/02 | 1.25 | 0 | 0.00 | 285 |

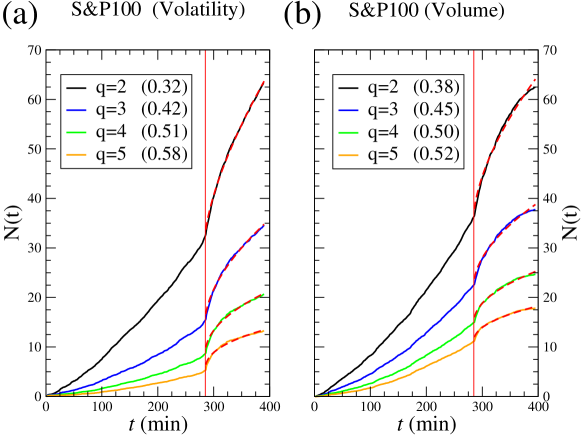

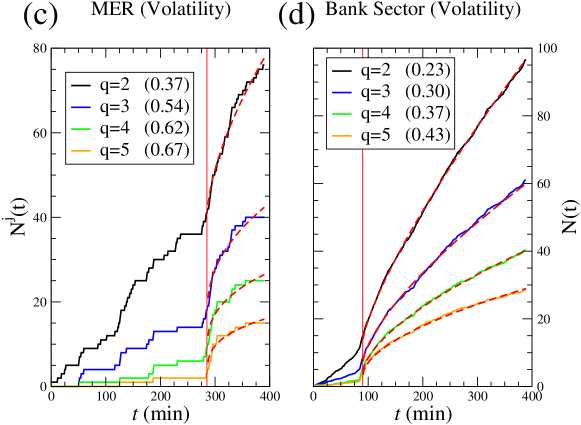

In Figs. 4(a,b) we plot the average volatility response of the stocks analyzed, where

| (8) |

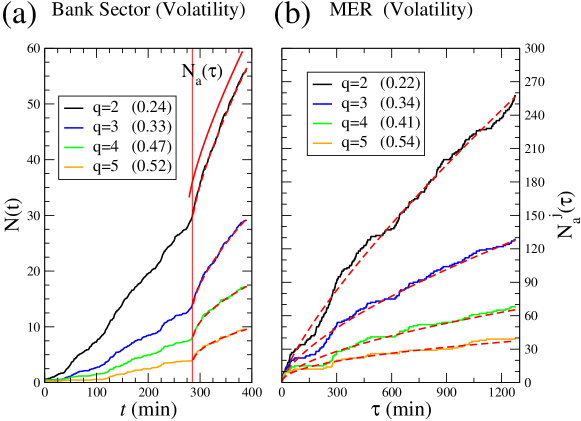

This average is obtained by combining the individual Omori responses, , of the stocks. Such averaging does not cancel the Omori law, but allows for better statistical regression. This is especially useful for an Omori law corresponding to large volatility threshold , where a single stock might not have a sufficient number of events. In Fig. 4(c) we plot the trade pattern of Merrill Lynch on Tuesday 08/21/01, and also in Fig. 5 for the following three days, demonstrating that the Omori relaxation can persists for several days.

The abrupt change in the curvature of illustrates the volatility clustering which begins around the time of the announcement , corresponding to the vertical line at minutes in Figs. 4(a-c). For comparison, we find that the average time series calculated from all days without FOMC meetings is approximately linear with time throughout the entire day, indicating that the sudden increase in excess volatility before and after announcement times results from the FOMC news. Volatility clustering in financial data sampled at the 1-minute scale persists for several months, with a significant crossover in the observed power-law autocorrelations occurring around minutes ( days) timescales ; markettimeseries1 ; markettimeseries2 .

In order to compare the dynamics before and after the announcement, we first separate the intraday time series into two time series , and . Then, to treat the dynamics symmetrically around the intraday announcement time SornettePNAS ; ShortTermRxn , we define the displaced time as the temporal distance from the minute powlawfit . As an illustration, we plot in Fig. 6 for the 4 corresponding curves exhibited in Fig. 4(a). We then employ a linear fit to both and on a log-log scale to determine the Omori power-law exponents before the news and after the news. In analogy, we define the amplitude before as and after as , as defined in Eq. (7).

Typically , which reflects the pronounced increase in the rate of events above the volatility threshold after the time of the announcement. We also observe , which corresponds to a time series in which the pre-shocks or after-shocks farther away from the announcement (for large ) are dominant over the volatility cascade around time . For comparison, is constant for stochastic processes with no memory, corresponding to . Hence, for an empirical value , the rate is indistinguishable from an exponential decay for , where is the characteristic exponential time scale. However, for larger values of , the exponential and power-law response curves are distinguishable, especially if several orders of magnitude in is available.

For all meetings analyzed, we find that increases with , meaning that the relatively large aftershocks decay more quickly than the relatively small aftershocks. Hence, the largest volatility values cluster around the announcement time . For comparison, values are calculated in OmoriLillo using and in OmoriWeber using for large financial crashes. For our data set, the cumulative probability that a given volatility value is greater than volatility threshold is and . Furthermore, we reject the null hypothesis that volatilities are distributed evenly across all days, finding that of the volatility values greater than are found on FOMC meeting days, whereas only are expected under the null hypothesis that large volatilities are distributed uniformly across all trading days. The increase for indicates that FOMC meetings days are more volatile than other days at the significance level. We also observe that the amplitudes of the Omori law generally obey the inequality , resulting from the large response immediately following the news.

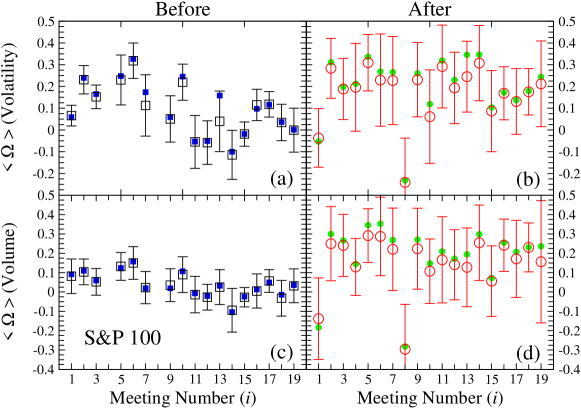

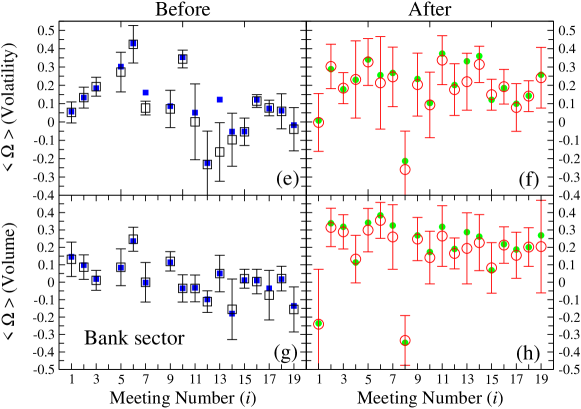

Although we focus mainly on price volatility in this paper, we also observe Omori dynamics in the high-frequency volume time series , defined as the cumulative number of shares traded in minute . In Figs. 7 (a-d) for the S&P 100 and Figs. 7 (e-h) for the bank sector, we compare the average of Omori exponents and for both volatility and volume dynamics, and for volatility threshold value . We compute the average Omori exponents using two averaging methods, the “individual” method and the “portfolio” method.

To analyze the time series after the announcement , we first average the exponents obtained for each individual stock , yielding . This “individual” method provides an error bar corresponding to the sample standard deviation . The second “portfolio” method determines a single from in Eq. (8). Comparing the open-box (individual method) and closed-box (portfolio method) symbols in Fig. 7, we observe that both methods yield approximately the same average value of . Note that for the subset = {1,4,8} of the unscheduled FOMC meetings, is smaller than usual, capturing the intense activity following surprise announcements. Hence, unexpected FOMC announcements can produce an inverse Omori law exhibiting convex relaxation () over a short horizon if the news contains a large amount of inherent surprise. The 8th meeting corresponds to the opening of the markets after Sept. 11, 2001.

For the time series before the announcement , individual stocks often do not have sufficient activity to provide accurate power-law fits. Hence, to estimate the sample standard deviation , we produce partial combinations, using . We then compute a standard deviation from the values calculated from . The values correspond to the error bars for in Fig. 7.

We also compute a single value from the portfolio average , which corresponds to the limit . The values of using the two methods are consistent. Interestingly, the values of calculated from volume data are all close to zero. However, using the Student T-test we reject the null hypothesis that each average value is equal to zero at the significance level for 15 out of 17 dates.

Fig. 7 shows the range of values for each of the 19 FOMC meetings we analyze. There are 8 panels comparing the values (i) between the dynamics before and after , (ii) between the volatility and volume dynamics, and (iii) between set of all stocks comprising the and the set of stocks comprising the banking sector. We hypothesize that the differences in the Omori values, before and after the announcement, are related to the anticipation and perceived surprise of the FOMC news. Furthermore, for the dynamics after the news, we find anomalous negative values for two surprise FOMC announcements and . Also, we find that volume values are more regular across all meeting events, suggesting that volume and price volatility contain distinct market information Earnings ; VolPriceRxn .

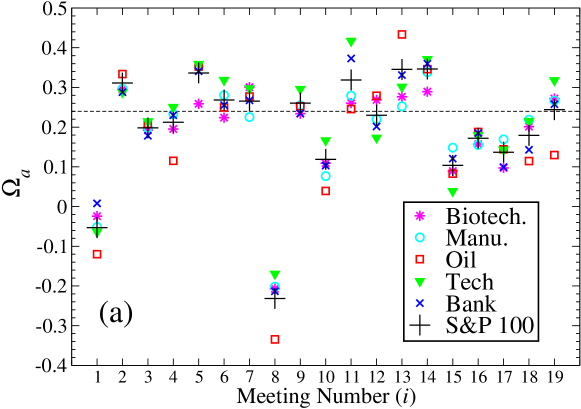

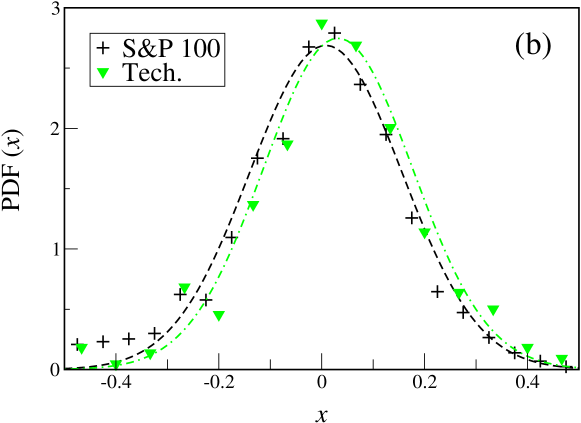

In order to find potential variations in the response dynamics for different stock sectors, in Fig. 8(a) we compare the values after the announcement for approximately equal-sized sectors using volatility threshold . We observe that the differences in the average values of the sectors are fairly small, indicating a broad market response. We also observe that the technology sector (Tech.), composed of hardware, software, and IT companies, often has the largest average value. Larger exponents, which correspond to shorter relaxation times, could result from the intense trading in the Tech sector during the Tech/IT bubble, which peaked in the year 2000. In follow-up analysis, we find in marketshocks that stocks with higher trading activity, quantified as the average number of transactions per minute, have larger in response to market shocks, and thus, faster price discovery. In order to compare the variation in the individual values of , we plot the pdf of exponents for all stocks and meetings in Fig. 8(b) using the shifted variable . We conclude from a Z-test at the significance level that Tech sector Omori exponents are larger on average, .

Motivated by the metric defined in Eq. (2), which quantifies speculation and anticipation in the market preceding FOMC meetings, we now develop a second metric to describe surprise through the change in market speculation following the announcement. This metric compares the anticipation leading up to the announcement with the revised speculation following the FOMC decision. This can be quantified through the relative change in , which provides a rough measure of the market stress that is released in the financial shock. Qualitatively, relates the average value of the spread before and after the scheduled meeting. We define,

| (9) |

| (10) |

where the sum is computed over the range trading days, with trading days and trading days. The factor when the Fed increases or maintains the Target rate , while when the Fed decreases the Target rate.

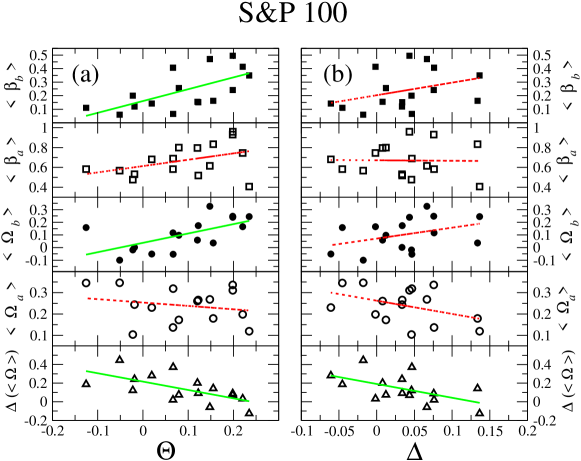

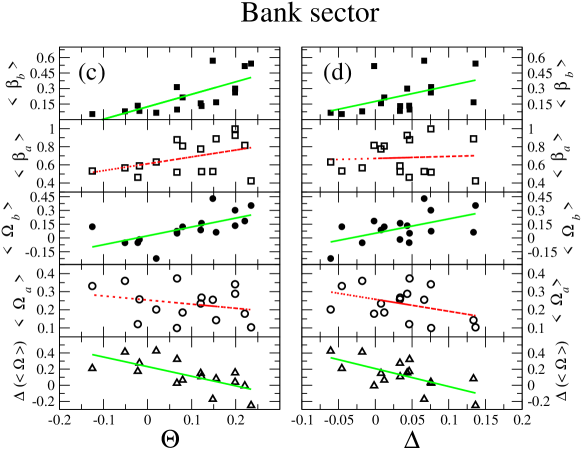

In Figs. 9 (a-d) we relate the amplitudes and , and also the exponents and to the speculation metric and the surprise metric . We observe that larger and larger are related to larger amplitude quantifying the preshock dynamics. However, we do not find a statistically significant relation between or and the aftershock parameters, suggesting that the relaxation dynamics following FOMC news are less predictable. Nevertheless, the aftershock dynamics are consistently more pronounced, with . We interpret Figs. 9(a) and (c) as follows: when , corresponding to “good” market sentiment and possible rate increase, the dynamics before the announcement have small and small reflecting low activity. After the announcement, the values of and increase, corresponding to a fast response of medium size. In the case of , corresponding to “bad” market sentiment resulting from speculation of a rate cut, the dynamics before the announcement have large and large , corresponding to a strong but quick buildup of volatility. After the announcement, the dynamics have large and small , corresponding to a strong and lasting relaxation dynamics. The interpretation of Figs. 9(b) and (d) is similar to the interpretation of Figs. 9(a) and (c), in that both surprise () and expected () bad news, correspond to a stronger and longer-lasting relaxation dynamics.

IV Discussion

Information flows through various technological avenues, keeping the ever-changing world up-to-date. All news carries some degree of surprise, where the perceived magnitude of the news certainly depends on the recipient. In financial markets, where speculation on investment returns results annually in billions of dollars in transactions, news plays a significant role in perturbing the complex financial system both on large and small scales, reminiscent of critical behavior with divergent correlation lengths 3pillars . Perturbations to the financial system are easily transmitted throughout the market by the long-range interactions that are found in the networks of market correlations marketcorr0 ; marketcorr1 ; marketcorr2 . Afterwards, the effects of the perturbation may persist via the long-term memory observed in volatility time series timescales ; markettimeseries1 ; markettimeseries2 , with fluctuation scaling obeying the emperical Taylor’s law taylorslawstocks ; scalingtempcorr .

We have shown that the Omori law describes the dissipation of information following the arrival of Federal Open Market Committee (FOMC) news. This type of relaxation is consistent with the substructure of financial crash aftershocks observed on various scales OmoriWeber . In particular, we systematically study the dynamical response of the stock market to perturbative information in the form of a Federal Reserve FOMC interest rate announcements, which can be expected (scheduled) or unexpected (as in cases of emergency).

In the case of unexpected news, as in Fig. 4(d), a pronounced response may result from reduced market liquidity, since traders do not have ample time to prepare and adjust MacroNews2 . Our findings suggest that the dynamics of “rallies” based on other forms of news, such as earning reports, upgrades and downgrades of stocks by major financial firms, unemployment reports, merging announcements etc., might also be governed by the Omori law with parameters that depend on the type of news. The impact of macroeconomic news has been analyzed for foreign exchange markets MacroNews2 , where it is found that high levels of volatility are present following both scheduled and surprise news.

According to the efficient market hypothesis noEMH , the time scale over which news is incorporated into prices should be very small. However, consistent with previous studies, we find “market underreaction” sentiment evident in the finite time scale (found here to be at least 1 trading day) over which the volatility aftershocks are significant. Moreover, we quantify the dynamics before and after, and show that the Omori parameters are related to investor sentiment sentiment , here measured by comparing the 6-month the Treasury Bill and the Federal Funds rates.

It is also conceivable that Omori law decay of market aftershocks also exists in the traded volume time series and the bid-ask spread time series ShortTermRxn ; limitorderOmori . Recently, Joulin et al. information use a similar method to describe the relaxation of trading following news streaming from feeds such as Dow Jones and Reuters, and compare to the relaxation following anomalous volatility jumps. Joulin et al. information also find Omori law relaxation, with exponent following a news source, and following an endogenous jump; interestingly, they find that the amplitude of the Omori law is larger for news sources than for endogenous jumps. For further comparison, Weber et al. OmoriWeber find for the 38 days following the market crash on September 11, 1986. One distinct difference between these studies, is the source of the news: Joulin et al. pool together thousands of news sources, some possibly pertaining to only a single stock; we focus on one particular type of news, the FOMC Target rate decision, which has a broad impact on the whole market and economy. It is possible that the difference between anticipated news and idiosyncratic news is the important criterion to consider when analyzing market response functions in relation to exogenous events. Here, we find novel dynamics before anticipated announcements.

In the case of FOMC news, speculation can be quantified by measuring the relative difference between the effective Federal Funds rate and the Treasury Bill in the weeks leading up to a scheduled meeting. We develop a speculation metric, , and relate it to , the volatility on the day of the meetings, finding that the market behaves more erratically when the Treasury Bill predicts a decrease in the Federal Funds Target rate. A rate decrease often occurs in response to economic shocks, whereas a rate increase is often used to fight inflation. Hence, the asymmetric response in Fig. 3 to rising and falling rates is consistent with the “sign effect”, where it has been found that bad news causes a larger market reaction than good news MacroNews2 , and that the asymmetry may result from the increased uncertainty in expectations among traders.

We analyze the four Omori-law parameters , , and calculated for 19 FOMC meetings. We conjecture that the Omori-law parameters are related to the market’s speculation, anticipation and surprise on the day of the FOMC meeting. In order to quantify speculation of rate cuts and rate increases, we define the measure , which is the relative spread between the Treasury Bill and the Federal Funds rates, before the meeting. In order to quantify surprise, we develop , which measures the change in the relative spread between the Treasury Bill and the Federal Funds rates, before and after the meeting. We relate both and to the dynamical response of the market on the day of the meeting. We find that relatively small values and relatively large amplitude values, corresponding to longer relaxation time and large response, follow from “bad” news, as in the case of the market reaction to the World Trade Center attacks in 2001. In all, these results show that markets relax according to the Omori law following large crashes and Federal interest rate changes, suggesting that the perturbative response of markets belongs to a universal class of Omori laws, independent of the magnitude of news.

V Acknowledgements

We thank L. DeArcangelis and M. Levy for helpful suggestions and NSF for financial support.

References

- (1) R. N. Mantegna and H. E. Stanley Econophysics: An Introduction (Cambridge University Press, Cambridge England, 1999).

- (2) J. P. Bouchaud, M. Potters Theory of Financial Risk, (Cambridge University Press, Cambridge England, 2000).

- (3) J. P. Bouchaud, Power laws in economics and finance: some ideas from physics. Quantitative Finance 1, 105 (2001).

- (4) X. Gabaix, P. Gopikrishnan, V. Plerou, and H. E. Stanley, A Theory of Power-Law Distributions in Financial Market Fluctuations. Nature 423, 267 (2003).

- (5) J. D. Farmer, M. Shubik and E. Smith, Is Economics the next physical science? Physics Today 58 (9), 37 (2005).

- (6) H. E. Stanley, V. Plerou and X. Gabaix, A statistical physics view of financial fluctuations: Evidence for scaling and universality. Physica A 387, 3967 (2008).

- (7) F. Omori, On the aftershocks of earthquakes. Journal of the College of Science, Imperial University of Tokyo 7, 111 (1894).

- (8) T. Utsu, A statistical study of the occurrence of aftershocks. Geophysical Magazine 30, 521 (1961) .

- (9) F. Lillo, R. N. Mantegna, Power-law relaxation in a complex system: Omori law after a financial market crash. Phys. Rev. E 68, 016119 (2003).

- (10) P. Weber, F. Wang, I. Vodenska-Chitkushev, S. Havlin and H. E. Stanley, Relation between volatility correlations in financial markets and Omori processes occuring on all scales. Phys. Rev. E 76, 016109 (2007).

- (11) A. Almeida, C. Goodhart and R. Payne, The effects of Macroeconomic News on High Frequency Exchange Rate Behavior. Journal of Financial and Quantitative Analysis 33, 383 (1998).

- (12) T. G. Andersen, T. Bollerslev, F. X. Diebold, and C. Vega, Micro Effects of Macro Announcements: Real-Time Price Discovery in Foreign Exchange. Amer. Econ. Rev. 93, 38 (2003).

- (13) N. Barberis, A. Shleifer, R. Vishny, A model of investor sentiment. J. Fin. Econ. 49, 307 (1998).

- (14) V. L. Bernard, J. K. Thomas, Evidence that stock prices do not fully reflect the impliacations of current earnings for future earnings J. of Accounting and Economics 13, 305 (1990).

- (15) W. N. Goetzmann, L. Li, K. G. Rouwenhorst, Long-Term Global Market Correlations. J. of Business 78, 1 (2005).

-

(16)

Historical Data for key Federal Reserve Interest Rates:

http://www.federalreserve.gov/releases/h15/data.htm

http://www.federalreserve.gov/fomc/fundsrate.htm - (17) J. D. Hamilton, O. Jorda, A Model of the Federal Funds Rate Target. J. of Political Economy 110, 1135 (2002).

- (18) J. D. Hamilton, Daily changes in fed funds futures prices. J. of Money, Credit, and Banking 41(4), 567 (2009).

- (19) S. Demiralp, O. Jorda, Daily changes in fed funds futures prices. Federal Bank of New York Economic Policy Review 8 (1), 29 (2002)

- (20) J. B. Calrson, B. R. Craig and W. R. Melick, Recovering Market Expectations of FOMC Rate Changes with Options on Federal Funds Futures. Journal of Futures Markets 25, 1203 (2005).

- (21) M. Piazzesi, E. Swanson, Futures Prices as Risk-Adjusted Forecasts of Monetary Policy. Journal of Monetary Economics 55 (4), 677 (2008).

- (22) K. N. Kuttner, Monetary policy suprises and interest rates: Evidence from the Fed funds futures market. J. of Monetary Economics 47, 523 (2001).

- (23) S. Kwan, On Forecasting Future Monetary Policy: Has Forward-Looking Language Mattered? Federal Reserve Bank San Francisco Economic Letter 15, 1 (2007).

- (24) J. B. Carlson, B. Craig, P. Higgins and W. R. Melick FOMC Communications and the Predictability of Near-Term Policy Decisions. Economic Commentary of the Federal Reserve Bank of Cleveland, 1-3 (2006).

- (25) For the calculation of and , we choose values of and to be on the order of a couple trading weeks prior to the announcement, so that we isolate fresh speculation leading into the meeting. The parameter provides an effective cutoff period, after which the weights begin to decrease quickly. Conversely, the weights corresponding to days close to the meeting, , are effectively constant. The values of and do not change much with varying choice of or . Without loss of generality, we choose days, and days.

- (26) B. Podobnik, D. Horvatic, A. M. Petersen, and H. E. Stanley, Cross-Correlations between Volume Change and Price Change. Proc. Natl. Acad. Sci. 106, 22079 (2009).

- (27) We find historical information about FOMC meetings using resources at the Federal Reserve websit and using newspaper archives. Intraday time of announcement, , are often quoted in New York Times finance articles by Richard W. Stevenson the day after FOMC announcements. They are also evident in the intraday Omori plots of in Fig. 4.

- (28) K. Yamasaki, L. Muchnik, S. Havlin, A. Bunde, and H. E. Stanley, Scaling and memory in volatility return intervals in financial markets. Proc. Natl. Acad. Sci. 102, 9424 (2005).

- (29) F. Wang, K. Yamasaki, S. Havlin, and H. E. Stanley, Scaling and Memory of Intraday Volatility Return Intervals in Stock Market. Phys. Rev. E 73, 026117 (2006).

- (30) F. Wang, P. Weber, K. Yamasaki, S. Havlin, and H. E. Stanley, Statistical regularities in the return intervals of volatility. Eur. Phys. J. B 55, 123 (2007).

- (31) R. N. Mantegna, Hierarchical structure in financial markets. Eur. Phys. J. B 11, 193 (1999).

- (32) L. Laloux, P. Cizeau, J. P. Bouchaud and M. Potters, Noise Dressing of Financial Correlation Matrices. Phys. Rev. Lett. 83, 1467 (1999).

- (33) V. Plerou, P. Gopikrishnan, B. Rosenow, L. A. N. Amaral, and H. E. Stanley, Universal and Non-Universal Properties of Cross-Correlations in Financial Time Series. Phys. Rev. Lett. 83, 1471 (1999); V. Plerou, P. Gopikrishnan, B. Rosenow, L.A.N. Amaral, T. Guhr, and H. E. Stanley, Phys. Rev. E 65, 066126 (2002).

- (34) D. Sornette, A. Helmstetter, Endogenous versus exogeneous shocks in systems with memory. Physica A 318, 577 (2003).

- (35) D. Sornette, Y. Malevergne, J. F. Muzy, What causes crashes? Risk 16, 67 (2003).

- (36) A. Joulin, A. Lefevre, D. Grunberg, J. P. Bouchaud, Stock price jumps: news and volume play a minor role. Wilmott Magazine Sept/Oct 46, 1 (2008). (arXiv:cond-mat/0803.1769).

- (37) O. Guedj, J. P. Bouchaud, Experts’ earning forecasts: bias, herding, and gossamer information. IJTAF 8 (7), 933 (2005). arXiv:cond-mat/0410079.

- (38) R. Crane, D. Sornette, Robust dynamic classes revealed by measuring the response function of a social system. Proc. Natl. Acad. Sci. 105, 15649 (2008).

- (39) R. Cont, M. Potters, J. P. Bouchaud, Scaling in Stock Market Data: Stable Laws and Beyond. Proceedings of the Les Houches workshop, Les Houches, France, March 10-14, 1997: 1-11.

- (40) Y. Liu, P. Cizeau, M. Meyer, C.-K. Peng, and H. E. Stanley, Correlations in economic time series. Physica A 245, 437 (1999); Y. Liu, P. Gopikrishnan, P. Cizeau, M. Meyer, C.-K. Peng, and H. E. Stanley, Phys. Rev. E 60, 1390 (1999).

- (41) P. Gopikrishnan, V. Plerou, L. A. N. Amaral, M. Meyer, and H. E. Stanley, Scaling of the Distributions of Fluctuations of Financial Market Indices. Phys. Rev. E 60, 5305 (1999).

- (42) A. G. Zawadowsk, G. Andor, J. Kertész, Short-term market reaction after extreme price changes of liquid stocks. Quantitative Finance 6, 283 (2006).

- (43) In Fig. 4 we plot , where corresponds to the opening bell at 9:30 AM. Quantitatively, we calculate the Omori exponents using the displaced time from the announcement time . In terms of the displaced time , we separate into two separate time series where and with . The parameter is a “padding” that eliminates the last 60 minutes of (the first 60 minutes of ), which eliminates opening effects and improves the regression analysis around .

- (44) D. Morse, Price and trading volume reaction surrounding earnings announcement: A closer examination. Journal of Accounting Research 19, 374 (1981).

- (45) O. Kim and R. E. Verrecchia, Trading volume and price reactions to public announcements. Journal of Accounting Research 29, 302 (1991).

- (46) A. M. Petersen, F. Wang, S. Havlin, H. E. Stanley, Market dynamics immediately before and after financial shocks: quantifying the Omori, productivity and Bath laws. Phys. Rev. E 82, 036114 (2010).

- (47) H. E. Stanley, Scaling, Universality, and Renormalization: Three Pillars of Modern Critical Phenomena. Rev. Mod. Phys. 71: S358 (1999).

- (48) Z. Eisler, I. Bartos, J. Kertész, Scaling theory of temporal correlations and size-dependent fluctuations in the traded value of stocks. Phys. Rev. E 73, 046109 (2006).

- (49) Z. Eisler, I. Bartos, J. Kertész, Fluctuation scaling in complex systems: Taylor’s law and beyond. Adv. Phys. 57, 89 (2008).

- (50) A. Ponzi, F. Lillo, R. N. Mantegna, Market reaction to a bid-ask spread change: A power-law relaxation dynamics. Phys. Rev. E 80, 016112 (2009).