Detecting a conditional extreme value model

Abstract.

In classical extreme value theory probabilities of extreme events are estimated assuming all the components of a random vector to be in a domain of attraction of an extreme value distribution. In contrast, the conditional extreme value model assumes a domain of attraction condition on a sub-collection of the components of a multivariate random vector. This model has been studied in Heffernan and Tawn (2004), Heffernan and Resnick (2007), Das and Resnick (2008b). In this paper we propose three statistics which act as tools to detect this model in a bivariate set-up. In addition, the proposed statistics also help to distinguish between two forms of the limit measure that is obtained in the model.

Key words and phrases:

Regular variation, domain of attraction, heavy tails, asymptotic independence, conditional extreme value model1. Introduction

Extreme value theory (henceforth abbreviated EVT) is used to model environmental, financial and internet traffic data. Multivariate extreme value theory assumes an extreme-valued domain of attraction condition on the joint distribution of a random vector which after a suitable standardization relates multivariate extreme value theory to regular variation on . Probabilities of critical risk events can be estimated under the regularly varying assumption and then related back to the original co-ordinate system. Such estimates are a function of the dependence structure among the variables in the multivariate model. There is a substantial literature on the behavior of multivariate extreme-value theory both in the presence of asymptotic dependence and asymptotic independence (Coles and Tawn, 1991, Ledford and Tawn, 1996, 1997, 1998, de Haan and de Ronde, 1998, Resnick, 2002, Maulik and Resnick, 2005, de Haan and Ferreira, 2006).

A conditional extreme value (CEV) model was proposed in Heffernan and Tawn (2004), where multivariate distributions were approximated by conditioning on one of the components being in an extreme-value domain. The authors showed that this approach incorporated a variety of examples of different types of asymptotic dependence and asymptotic independence. Their statistical ideas were given a more mathematical framework by Heffernan and Resnick (2007) after slight changes in assumptions to make the theory more probabilistically viable. A further study (Das and Resnick (2008b)) revealed that assuming a conditional extreme value model holds no matter what conditioning variable is chosen is equivalent to assuming a multivariate extreme-value domain of attraction on the entire random vector. It is known that in the presence of asymptotic independence, the limit measure in the multivariate EVT set up has an empty interior; in other words, the limit measure concentrates on the boundary of the state space. In such a case an additional assumption of a CEV model provides more insight into the dependence structure. The CEV model also provides a way for modeling multivariate data assuming a subset rather than the entire vector to be extreme-valued. In this paper we suggest situations where a CEV model can be used and suggest techniques to detect the model and in the process also detect characteristics of the limit measure for the model. The methodologies are suggested for a bivariate data set.

Section 1 provides an introduction and review of the model. Section 2 deals with the detection of a conditional extreme value model. It has been shown in Das and Resnick (2008b) that the CEV model can be standardized to regular variation on a special cone if and only if the limit measure involved is not a product. In case of a product measure in the limit, we need to estimate fewer parameters and calculating probabilities is also simpler. Fougères and Soulier (2008) suggests some estimates for parameters and normalizing constants in the two different cases (product and non-product limit measures). Hence it is important to know whether we are in the product case or not. In Section 2 we propose three statistics whose behavior can first of all indicate the appropriateness of the CEV model and secondly indicate whether the limit measure is a product or not. Section 3 is dedicated to applying our techniques to some simulated and real data coming from Internet traffic studies.

1.1. Preliminaries: The CEV model and some related results

We discuss the model and preliminary results in this subsection. Refer to Heffernan and Resnick (2007) and Das and Resnick (2008b) for further discussion on conditional extreme value models.

A univariate extreme value distribution , for , is defined as

| (1.1) |

where . For , the distribution function is interpreted as . We let be the right closure of ; that is,

Let be a random vector in . For a CEV model we make the following assumptions:

-

(1)

The distribution is in the domain of attraction of an extreme value distribution, , written . This means there exist functions , such that, as ,

(1.2) for

-

(2)

There exist functions and and a non-null Radon measure on Borel subsets of such that for each ,

(1.3) for continuity points of the limit, (1.4) (1.5) (1.6)

A non-null Radon measure is said to satisfy the conditional non-degeneracy conditions if both of (1.4) and (1.5) hold. We say that follows a conditional extreme value model (or CEV model) if conditions (1) and (2) above are satisfied. The reason for this name is that, assuming to be a continuity point of , (1.3), (1.4) and (1.5) imply that

| (1.7) |

Note that (1.3) can be viewed in terms of vague convergence of measures in , the space of Radon measures on .

In this model the transformation standardizes the -variable, i.e., we can assume . Hence a reformulation of (1.3) leads to

| (1.8) | ||||

| for continuity points of where, | ||||

| (1.9) | ||||

We also know (Heffernan and Resnick, 2007, Proposition 1) that the following variational property holds: there exists functions such that for all ,

| (1.10) |

This implies that for some (de Haan and Ferreira, 2006, Theorem B.1.3). Also, can be either 0 or for some (de Haan and Ferreira, 2006, Theorem B.2.1).

Remark 1.1.

The CEV model primarily differs from the multivariate extreme value model in the domain of attraction condition. Das and Resnick (2008b) provides conditions under which a CEV model can be extended to multivariate extreme value model. Under the multivariate extreme value model, each of the variables can be standardized so that we have a multivariate regular variation on the cone ; see de Haan and Resnick (1977) and Chapter 6 of de Haan and Ferreira (2006). The conditional extreme value model can be standardized if and only if the limit measure in (1.3) is not a product measure (Das and Resnick, 2008b). When both and are standardized, we can characterize the limit measure in terms of all Radon measures (finite and infinite) on . Though theoretically elegant, performing standardization in practice is not an easy task.

Thus, it is important to know when the limit is a product measure. A product measure in the limit precludes standardization of both the variables (Heffernan and Resnick, 2007) and means that we do not have a multivariate extreme value model (Das and Resnick, 2008b). However, a product measure makes the estimation of certain parameters and probabilities easier. For instance, in the product case so (see (1.10)) but without the property that is a product, has to be estimated. Furthermore, the limit being a product measure can be considered as a form of asymptotic independence in the CEV model, which can be probabilistically useful (Maulik et al., 2002).

1.2. Appropriateness of the CEV model.

Multivariate extreme value theory provides a rich literature on estimation of probabilities of extreme regions containing few or no data points in the sample. The multivariate theory assumes that each variable is marginally in an extreme value domain of attraction. However, this might not be the right assumption for all data sets. We encounter data where one or some but not all the variables can be assumed to be in an extreme value domain; see Section 3.2. The CEV model is a candidate model in such cases.

Another circumstance where the CEV model can be helpful is if one has a multivariate extreme value model with limit measure possessing asymptotic independence. This means that in the standardized model, the limit measure, , concentrates on the axes through and . So an estimate of the probability of a region where both variables are big will turn out to be zero which may be a useless and misleading estimate. In such a circumstance, finer estimates can be obtained using either hidden regular variation (Maulik and Resnick, 2005) or the CEV model. Both methods provide a non-zero limit measure by using normalization functions which are of different order from the multivariate EV model. The relationship between the multivariate EV model and the CEV model and the respective normalizing functions considered in Das and Resnick (2008b).

So, how do we decide if the CEV model is appropriate for multivariate data?

-

(1)

Start by checking whether any of the marginal variables belongs to the domain of attraction of an extreme value distribution. An informal way to do this is through plots of the estimators of the extreme value parameter (Pickands plot, Moment estimator plot, etc). If the plot attains stability in some range it is reasonable to assume an extreme-value model. More formal methods for testing membership in a domain of attraction using quantile and distribution functions are discussed in de Haan and Ferreira (2006), Chapter 5.2. The special case of a heavy-tailed random variable can be detected using the QQ plot, plotting the theoretical quantiles of the exponential distribution versus the logarithm of the sorted data and checking for linearity in the high values of the data. This is reviewed in Resnick (2007) and Das and Resnick (2008a).

-

(2)

If some, but not all, marginal variables are in a domain of attraction, proceed to see if the data is consistent with the CEV model. See Section 2.

-

(3)

If all variables are in some extreme value domain, check if the multivariate extreme value model is appropriate and if asymptotic independence is present. One way to do this is by checking whether both maximum and minimum of the standardized variables have distributions with regularly varying tails (Coles et al., 1999, Resnick, 2002). If the EV model is appropriate and asymptotic independence is absent, the CEV model does not provide any more information than the EV model. On the other hand if asymptotic independence is present, the CEV model, if detected, provides supplementary information about the joint behavior of the variables away from at least one of the axes.

2. Three estimators for detecting the CEV model

Let be a bivariate random sample. In this section we propose three statistics to detect whether our sample is consistent with the CEV model under the assumption that at least one of the variables is in an extreme-value domain, and without loss of generality we assume to be that variable. Our statistics have a consistency property which allows detection of a product form for the limit measure.

Assume is iid from a CEV model as defined in Section 1.1. We first formulate a consequence of (1.3) which will be convenient for our purpose. The following notations will be used.

2.1. A consequence for empirical measures

When the CEV property holds, a family of point processes of ranks of the sample converge vaguely to a Radon measure. By transforming to ranks of the data, we presumably lose efficiency since only the relative ordering in the sample remains unchanged but detection of the CEV property is easier since we no longer need to estimate the various parameters of the model. See de Haan and de Ronde (1998), de Haan and Ferreira (2006), Resnick (2007).

The convergence statement (1.3) of the CEV model defined in Section 1.1 can be interpreted in terms of vague convergence of measures. In preparation for the forthcoming result we recall some commonly used notation and concepts. Let be a locally compact space with a countable base (for example, a finite dimensional Euclidean space). We denote by , the non-negative Radon measures on Borel subsets of . If for , then converge vaguely to (written ) if for all bounded continuous functions with compact support we have

This concept allows us to write (1.3) as

| (2.1) |

in . Standard references include Kallenberg (1983), Neveu (1977) and Resnick (2008, Chapter 3).

Recall the definition of in (1.9) and define the measure by

| (2.2) |

Applying a reciprocal transformation to the second coordinate,

converts into the copula .

Proposition 2.1.

Proof.

From (2.1) and (Resnick, 2007, Theorem 5.3(ii)), as with ,

| (2.3) |

in . Recall are the order statistics of in decreasing order and ordering the ’s in (2.3) allows us to write the equivalent statement

| (2.4) |

Define the measure by

and sometimes, here and elsewhere, we sloppily write . Taking marginal convergence in (2.3), or using (1.2), we have with that

| in . Using an inversion technique (Resnick and Stărică (1995), de Haan and Ferreira (2006), Resnick (2007, page 82)), we get | ||||

| (2.5) | ||||

in , the class of left continuous functions on with range and with finite right limits on . The convergence in (2.5) being to a non-random function, we can append it to the convergence in (2.4) to get the following (Billingsley, 1968, p.27):

| (2.6) |

on .

Let be the subfamily of consisting of non-increasing functions and define

by

where

This is an a.s. continuous map so apply this to (2.6) and

| (2.7) |

For and , the left side of (2.7) on the set is

and since

iff

the left side of (2.7) on the set is

The right side of (2.7) on the set is

so we conclude

| (2.8) |

in Recall was defined in (1.9).

Now assuming is a continuity point of we have

| (2.9) |

or in the topology of weak convergence on , the probability measures on ,

Define a map on by

where

or, for ,

This map is continuous at provided is continuous. To see this, let be continuous on and suppose and . Then

For , convergence to follows by uniform continuity of and the fact that uniformly in . To verify , it suffices to note that is continuous with compact support and then use .

We propose three statistics that can be used to detect whether or not a CEV model is appropriate, and if so, whether the model has a product measure in the limit.

2.2. The Hillish statistic,

The Hill estimator (Hill (1975), Mason (1982), de Haan and Ferreira (2006), Resnick (2007)) is a popular choice for estimating the tail parameter of a heavy-tailed distribution. We say that a distribution function on is heavy-tailed with tail parameter if

| (2.11) |

If are i.i.d from this distribution and are the orders statistics of the sample in decreasing order, then the Hill estimator defined as

is a weakly consistent estimator of as . One way to obtain the consistency is to integrate the tail empirical measure and using its consistency. See Resnick and Stărică (1995) or Resnick (2007, p. 81).

The Hillish statistic, based on the ranks of the sample, converges weakly to a constant limit under the CEV model. The name is derived from the similarity of proof of this convergence with that of the weak consistency of the Hill estimator. Using the notation defined just prior to Section 2.1, and assuming , the Hillish statistic for is defined as

| (2.12) |

The following proposition provides a convergence result of the Hillish statistic under conditions on .

Proposition 2.2.

Proof.

Proposition 2.1 yields

| (2.14) |

in . Rewrite (2.14) for as

| (2.15) |

Observe that

| (2.16) |

where as . Hence if we show

then we are done. For finite we know that

| (2.17) |

since (2.15) implies that the integrand converges in probability and we can use Pratt’s Lemma (Resnick, 1999, page 164) for the convergence of the integral. Note that as the right hand side in equation (2.17) converges to . So we need to see what happens outside the compact sets. In particular if we can show that for any ,

| (2.18) | ||||

| (2.19) | and |

then by a standard converging together theorem (Resnick, 2007, Theorem 3.5), we are done. Observe that

| where | ||||

| and | ||||

Hence

| and applying Fatou’s Lemma, this is bounded by | ||||

This shows (2.19) holds and similarly we can show (2.18) holds, and we are done. ∎

Suppose is a sample from a CEV limit model with normalizing functions and variational functions . Let the standardized limit measure be as defined in (1.9). Also . Then is also a sample from a CEV limit model but with normalizing functions and variational functions . In this case the standardized limit measure is and it is easy to check that for ,

| (2.20) |

We also have for

| (2.21) |

Thus, for , we have,

| (2.22) |

The following proposition characterizes product measure in terms of limits of the Hillish statistic for both and .

Proposition 2.3.

Under the conditions of Proposition 2.2, is a product measure if and only if both

Proof.

Evaluating , the limit of the Hillish statistic as proposed in Proposition 2.2, leads us to the above results. Recall that we assume is continuous. Define for any , the family of distribution functions as follows:

where are as defined in (1.10) and the second equality can be obtained by using instead of in the CEV model property (1.3) (Heffernan and Resnick, 2007, page 543). Note that according to our definition. Now,

| (2.23) |

-

(1)

If is a product measure then where . Similarly, . We know that being a product measure is equivalent to . Thus for any . Thus

Also

-

(2)

Conversely assume that . We know that for some . Let us consider the following cases:

-

(a)

. This means and for some . We will show that must be . If , then

Similarly, we can show

Thus for to hold, we must have , which implies and becomes a product measure.

-

(b)

. We will show that this is not possible under the assumption . For ,

for some . Assume first . Then for . Therefore, for such ,

(2.24) Denote

(2.25) Since is non-decreasing

(2.26) Since , we have

(2.27) We claim , since if is either or , then (2.26) and (2.27) imply that almost everywhere which means

which is impossible for all when .

From (2.27) we have

that is,

(2.28) where the integrands are non-negative on both sides using (2.26). Now implies that

Use the transformation and the above equation becomes Therefore we have

Since if and only if from (2.26), we have (2.29) where the integrands on both sides are non-negative. But referring to (2.28) we have (2.30) with equality holding only if the integrand is almost everywhere. Similarly we have (2.31) with equality holding only if the integrand is almost everywhere. The integrand cannot be since it will imply almost everywhere meaning . But our assumption is . Thus with strict inequality holding for both (2.30) and (2.31) we have a contradiction in equation (2.29). Thus we cannot have .

The case with can be proved similarly. Hence the result.

-

(a)

∎

This corollary provides a detection technique for the limit measure being a product measure. Given a sample of size , we plot for values of and then try to see whether it stabilizes close to or not. If the statistic is close to another value, this is evidence that the model is applicable but the limit measure is not product.

2.3. The Pickandsish statistic,

Another way to check the suitability of the CEV assumption and to detect a product measure in the limit is to use the Pickandsish statistic which is based on ratios of differences of ordered concomitants. The statistic is patterned on the Pickands estimate for the parameter of an extreme value distribution (Pickands (1975), de Haan and Ferreira (2006, page 83), Resnick (2007, page 93)). For a fixed , recall that are the order statistics in increasing order from , the concomitants of , the order statistics in decreasing order from . For notational convenience for write . Now define the Pickandsish statistic for ,

| (2.32) |

Proposition 2.4.

Suppose follows a CEV model. Let , Then, as with , we have

| (2.33) |

provided . Here and are defined in (1.10) and .

Proof.

Corollary 2.5.

Suppose there exists such that , and for , . Then under the conditions of Proposition 2.4, is a product measure if and only if

Proof.

Assume that is a product measure. Then , i.e., and . Hence

Therefore, provided and , Proposition 2.4 implies .

Conversely, suppose and , . Hence

| (2.38) |

-

(1)

Suppose which means . Then (2.38) implies which implies . This means is a product measure.

-

(2)

Suppose and . Then (2.38) implies . This implies , a contradiction to . So this supposition is not possible.

-

(3)

Suppose and for . Then (2.38) implies . This means , a contradiction to . So this supposition is not possible.

Hence we have that is a product measure if for we have . ∎

2.4. Kendall’s Tau

Classically, Kendall’s tau statistic (McNeil et al. (2005)) is used to measure the strength of association between two rankings. We use a slightly modified version of the statistic using data pertaining to the maximum -values: , their concomitants and the ranks of . The Kendall’s tau statistic is

| (2.39) |

This statistic can also be used to show the appropriateness of the CEV model and to decide if the limit measure is a product. We show that under the CEV model as defined in (2.39) converges in probability to a limiting constant and when the CEV model holds with a product measure, the limit is 0.

First we prove a lemma on copulas in which leads to proving convergence for the statistic . Recall that a two dimensional copula is any distribution function defined on with uniform marginals (McNeil et al. (2005)).

Lemma 2.6.

Suppose are copulas on , is continuous and . Then

| (2.40) |

Proof.

Since , the convergence is uniform, that is, we have

Therefore

∎

Remark 2.1.

From Lemma 2.6 we get that if are random probability measures and is continuous, then

| (2.41) |

Define the following copulas on :

| (2.42) | ||||

| (2.43) |

Proposition 2.7.

Proof.

Proposition 2.1 implies that as with , for ,

Therefore, for ,

since H is continuous, and replacing by does not matter in the limit. This shows that . From Lemma 2.6 and Remark 2.1 we have

Now note that

Hence we have as with ,

If is a product, for ,

Hence

and the result follows. ∎

Proposition 2.7 would detect that a limit is not a product if the statistics stabilizes at a non-zero value. We have not been able to prove a limit of 0 implies a product measure and doubt the truth of this statement.

Remark 2.2.

The three statistics provided above each have their own advantages and disadvantages.

-

•

They are not hard to calculate.

-

•

For the CEV model we have shown that all these statistics stabilize as with .

-

•

The rank-based statistics Hillish and Kendall’s tau are smooth in nature as the rank transform removes the extremely high or low values.

-

•

The disadvantage of the Pickandsish statistic is that its plot lacks smoothness and exhibits erratic behavior for small data sets.

-

•

Obtaining distributional properties for these statistics would require further limit conditions on the variables, presumably some form of second order behavior.

3. Examples and applications

In this section we apply the three estimators proposed in Section 2 to data sets and judge their performances in the various cases. First we deal with simulated data from specific models discussed in Das and Resnick (2008b). Then we apply our techniques to Internet traffic data.

3.1. Simulation from known CEV limit models

Example 3.1.

Let and be independent random variables with and . Then the following convergence holds in (actually it is an equality)

where denotes the standard normal distribution function. We have a CEV model here with . The limit measure is a product. Hence, theoretically

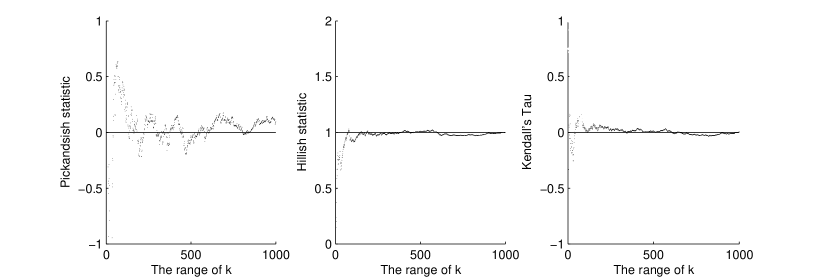

We simulate a sample of size and plot the above estimators for . For the Pickandsish statistic we have chosen .

The simulated data supports the theoretical results stated.

Example 3.2.

Let and be independent Pareto random variables where and with . Define Then we can check that the following holds in : For and large,

Theoretically the values of the limits of and are as follows.

Now for we have,

For calculating the Kendall’s tau statistics observe that from definition we have:

| Hence we have | ||||

| Therefore | ||||

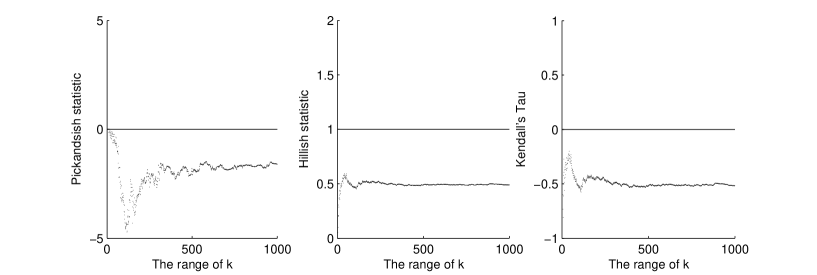

For and , theoretically we have

We simulate a sample of size with and plot the three statistics for . For the Pickandsish statistic we have chosen .

The graphs are consistent with the obtained theoretical limits.

3.2. Internet traffic data

Internet traffic data has often provided scope for heavy-tail modeling. Variables such as file size, transmission duration and session length have been observed to be heavy-tailed (Maulik et al., 2002, Resnick, 2003, Sarvotham et al., 2005).

We study a particular data set of GPS-synchronized traces that were recorded at the University of Auckland http://wand.cs.waikato.ac.nz/wits. The raw data contains measurements on packet size, arrival time, source and destination IP, port number, Internet protocol, etc. We consider traces corresponding exclusively to incoming TCP traffic sent on December 8, 1999, between 3 and 4 p.m. The packets were clustered into end-to-end (e2e) sessions which are clusters of packets with the same source and destination IP address such that the delay between arrival of two successive packets in a session is at most two seconds. We observe three variables :

The data have been downloaded and processed into sessions by Luis Lopez Oliveros, Cornell University.

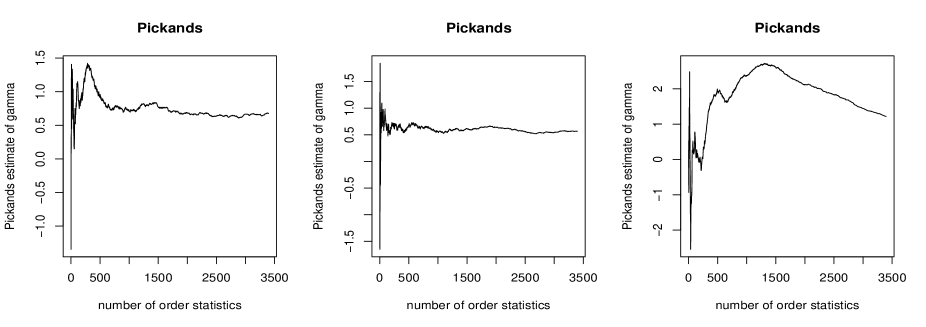

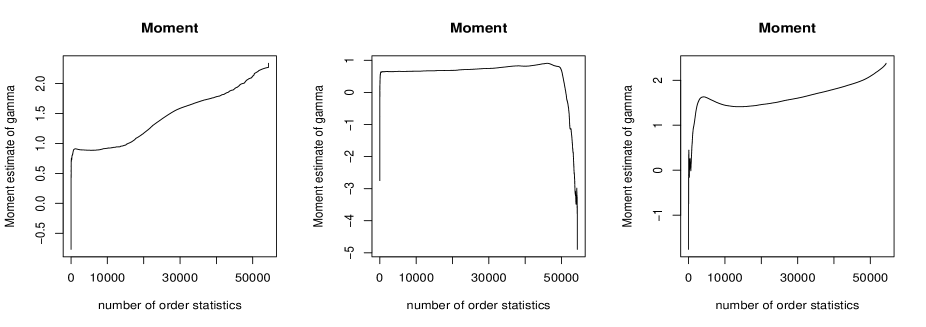

First we check whether the individual variables are heavy-tailed or not. The Pickands estimator and moment estimators are weakly consistent for the extreme value parameter (de Haan and Ferreira (2006)) when the distribution of the variable under consideration is in as in (1.1). We plot these estimators over and observe whether they stabilize over an interval. The Pickands plot indicates that the Pickands estimates of the extreme value parameter are stable for size and duration but not for the transfer rate. The moment plot on the other hand shows that the moment estimate of the extreme-value parameter stabilizes for duration but does not do that clearly for either size or transfer rate. Recall that the CEV model is applicable if either of the variables is in the domain of attraction of an extreme-value distribution. Clearly there is an indication that transfer rate might not be in an extreme value domain.

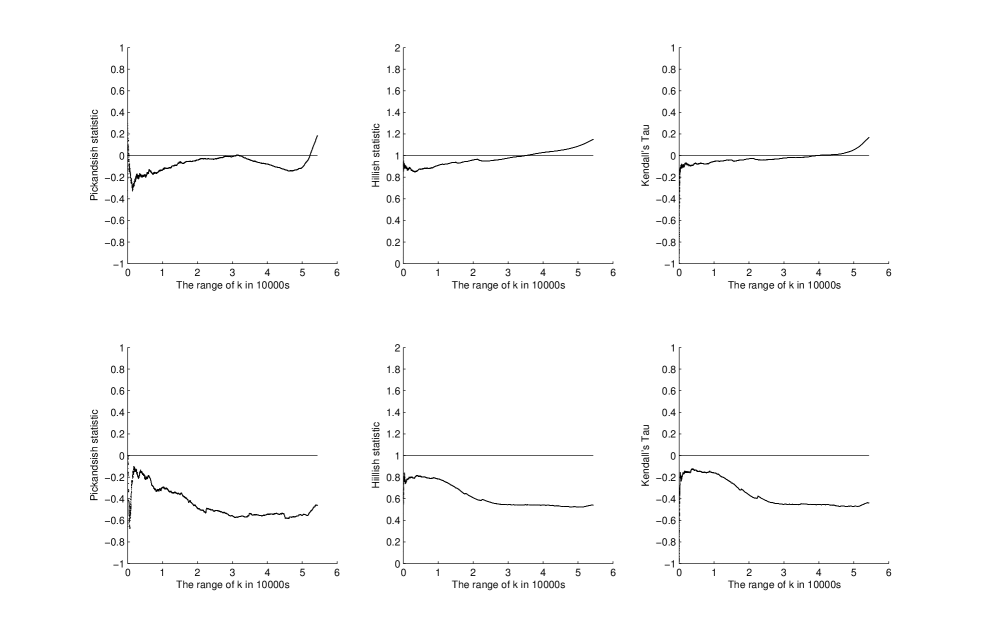

Now we turn to the three statistics we have devised in this paper first to detect whether we have a CEV model and then to check whether the limit measure is a product. First we consider the pair assuming the distribution of is in for some . Then we consider the pair assuming the distribution of is in for some .

Observe from Figure 4 that neither of the three statistics stabilizes for the observations . Hence a CEV model might not be the right model to apply. On the other hand for , all the statistics stabilize at some point. But it is clear they are not stabilizing at a point to indicate product measure. Hence we have evidence to model (transfer rate, duration) as a CEV model with a non-product limit. Note that this also indicates that we should be able to standardize to regular variation on .

4. Conclusion

The CEV model is intended to provide us with a deeper understanding of multivariate distributions which have some components in an extreme-value domain. In our discussion, we have provided statistics to detect the CEV model in a bivariate set up. These three statistics perform differently for different data sets as we have noted in our examples. A further step would be to find asymptotic distributions for these statistics. On another direction, it would be nice to obtain statistics for detection of conditional models in a multivariate set up of dimension more than two.

References

- Billingsley (1968) P. Billingsley. Convergence of Probability Measures. John Wiley & Sons Inc., New York, 1968.

- Coles and Tawn (1991) S. G. Coles and J. A. Tawn. Modelling extreme multivariate events. J. R. Statist. Soc. B, 53:377–392, 1991.

- Coles et al. (1999) S.G. Coles, J.E. Heffernan, and J.A. Tawn. Dependence measures for extreme value analyses. Extremes, 2(4):339–365, 1999.

- Das and Resnick (2008a) B. Das and S. I. Resnick. QQ plots, random sets and data from a heavy tailed distribution. Stoch. Models, 24(1):103–132, 2008a. ISSN 1532-6349.

- Das and Resnick (2008b) B. Das and S. I. Resnick. Conditioning on an extreme component: Model consistency and regular variation on cones. Submitted to Bernoulli, 2008b. URL http://arxiv.org/abs/0805.4373.

- de Haan and de Ronde (1998) L. de Haan and J. de Ronde. Sea and wind: multivariate extremes at work. Extremes, 1(1):7–46, 1998.

- de Haan and Ferreira (2006) L. de Haan and A. Ferreira. Extreme Value Theory: An Introduction. Springer-Verlag, New York, 2006.

- de Haan and Resnick (1977) L. de Haan and S.I. Resnick. Limit theory for multivariate sample extremes. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete, 40:317–337, 1977.

- Fougères and Soulier (2008) A. Fougères and P. Soulier. Modelling and estimation of conditional excesses. 2008. URL http://arXiv.org/0806.2426.

- Heffernan and Resnick (2007) J.E. Heffernan and S.I. Resnick. Limit laws for random vectors with an extreme component. Ann. Appl. Probab., 17(2):537–571, 2007. ISSN 1050-5164. doi: 10.1214/105051606000000835.

- Heffernan and Tawn (2004) J.E. Heffernan and J.A. Tawn. A conditional approach for multivariate extreme values (with discussion). JRSS B, 66(3):497–546, 2004.

- Hill (1975) B.M. Hill. A simple general approach to inference about the tail of a distribution. Ann. Statist., 3:1163–1174, 1975.

- Kallenberg (1983) O. Kallenberg. Random Measures. Akademie-Verlag, Berlin, third edition, 1983. ISBN 0-12-394960-2.

- Ledford and Tawn (1996) A.W. Ledford and J.A. Tawn. Statistics for near independence in multivariate extreme values. Biometrika, 83(1):169–187, 1996. ISSN 0006-3444.

- Ledford and Tawn (1997) A.W. Ledford and J.A. Tawn. Modelling dependence within joint tail regions. J. Roy. Statist. Soc. Ser. B, 59(2):475–499, 1997. ISSN 0035-9246.

- Ledford and Tawn (1998) A.W. Ledford and J.A. Tawn. Concomitant tail behaviour for extremes. Adv. in Appl. Probab., 30(1):197–215, 1998. ISSN 0001-8678.

- Mason (1982) D. Mason. Laws of large numbers for sums of extreme values. Ann. Probab., 10:754–764, 1982.

- Maulik and Resnick (2005) K. Maulik and S.I. Resnick. Characterizations and examples of hidden regular variation. Extremes, 7(1):31–67, 2005.

- Maulik et al. (2002) K. Maulik, S.I. Resnick, and H. Rootzén. Asymptotic independence and a network traffic model. J. Appl. Probab., 39(4):671–699, 2002. ISSN 0021-9002.

- McNeil et al. (2005) A.J. McNeil, R. Frey, and P. Embrechts. Quantitative Risk Management. Princeton Series in Finance. Princeton University Press, Princeton, NJ, 2005. ISBN 0-691-12255-5. Concepts, techniques and tools.

- Neveu (1977) J. Neveu. Processus ponctuels. In École d’Été de Probabilités de Saint-Flour, VI—1976, pages 249–445. Lecture Notes in Math., Vol. 598, Berlin, 1977. Springer-Verlag.

- Pickands (1975) J. Pickands. Statistical inference using extreme order statistics. Ann. Statist., 3:119–131, 1975.

- Resnick (2008) S. I. Resnick. Extreme values, regular variation and point processes. Springer Series in Operations Research and Financial Engineering. Springer, New York, 2008. ISBN 978-0-387-75952-4. Reprint of the 1987 original.

- Resnick (1999) S.I. Resnick. A Probability Path. Birkhäuser, Boston, 1999.

- Resnick (2002) S.I. Resnick. Hidden regular variation, second order regular variation and asymptotic independence. Extremes, 5(4):303–336, 2002.

- Resnick (2003) S.I. Resnick. Modeling data networks. In B. Finkenstadt and H. Rootzén, editors, SemStat: Seminaire Europeen de Statistique, Extreme Values in Finance, Telecommunications, and the Environment, pages 287–372. Chapman-Hall, London, 2003.

- Resnick (2007) S.I. Resnick. Heavy Tail Phenomena: Probabilistic and Statistical Modeling. Springer Series in Operations Research and Financial Engineering. Springer-Verlag, New York, 2007. ISBN: 0-387-24272-4.

- Resnick and Stărică (1995) S.I. Resnick and C. Stărică. Consistency of Hill’s estimator for dependent data. J. Appl. Probab., 32(1):139–167, 1995. ISSN 0021-9002.

- Sarvotham et al. (2005) S. Sarvotham, R. Riedi, and R. Baraniuk. Network and user driven on-off source model for network traffic. Computer Networks, 48:335–350, 2005. Special Issue on ”Long-range Dependent Traffic”.