Regularity of the optimal stopping problem for jump diffusions

Abstract.

The value function of an optimal stopping problem for jump diffusions is known to be a generalized solution of a variational inequality. Assuming that the diffusion component of the process is nondegenerate and a mild assumption on the singularity of the Lévy measure, this paper shows that the value function of this optimal stopping problem on an unbounded domain with finite/infinite variation jumps is in with . As a consequence, the smooth-fit property holds.

Key words and phrases:

Optimal stopping, variational inequality, Lévy processes, regularity of the value function, smooth fit principle, Sobolev spaces1. Introduction

On a probability space , consider a one-dimensional jump diffusion process whose dynamics is governed by the following stochastic differential equation:

| (1.1) |

in which is a -dimensional Wiener process, , independent of the Wiener process, is a Poisson random measure on with its mean measure , and is a Lévy measure on . The coexistence of diffusions and infinite activity jumps is motivated by recent studies of Aït-Sahalia and Jacod in [1] and [2].

This paper studies the problem of maximizing the discounted terminal reward by optimally stopping the process before a fixed time horizon . The value function of this problem is defined as

| (OS) |

in which is the set of all stopping times valued between and . A specific example of such an optimal stopping problem is the American option pricing problem, where models the logarithm of the stock price process and represents the pay-off function.

The value function is expected to satisfy a variational inequality with a nonlocal integral term (see e.g. Chapter 3 of [7]). Different concepts of solutions were employed to characterize the value function: Pham used the notion of viscosity solution in [23]. Also see [3], [4] for more recent results in this direction. Lamberton and Mikou worked with Lévy processes and showed in [19] that the value function can be understood in the distributional sense.

When the diffusion component in is nondegenerate, the value function is expected to have higher degree of regularity. Sections 1-3 in Chapter 3 of [7] and [15] analyzed the Cauchy problems for second order partial integro-differential equations and showed the existence and uniqueness of solutions in both Sobolev and Hölder spaces. Also see [20]. The intuition is that the diffusions component dominates the contribution from jumps in determining the regularity of solutions, no matter whether jumps have finite variation or not. However this intuition is only a folklore theorem for obstacle problems. There are some limited results available whose assumptions on obstacles, domains, and the structure of the jumps may not be appropriate for financial applications. For example, Bensoussan and Lions analyzed an obstacle problem for jump diffusions where jumps may have finite/infinite activity with finite/infinite variation; see in Theorem 3.2 in [7] on pp. 234. However, their assumption on the obstacle may not be satisfied by option payoffs. In the mathematical finance literature, when irregular obstacles are considered, the jumps are usually restricted to finite activity or infinite activity with finite variation cases. Zhang studied in [27] an obstacle problem for a jump diffusion with finite active jumps. Also see [22], [26], [5], and [6] for further developments. More recently, Davis et al. in [11], generalizing the results in [17] for the diffusion case, analyzed an impulse control problems for jump diffusions with infinite activity but finite variation jumps. A regularity result which treats obstacle problems with irregular obstacles and infinite variation jumps has been missing in the literature.

In this paper, we allow for infinite activity, infinite variation jumps. We show in Theorem 2.5 that the value function of an obstacle problem solves a variational inequality for almost all points in the domain, and that it is an element in with (see later this section for the definition of this Sobolev space). This regularity result directly implies that the smooth fit property holds and the value function is inside the continuation region. These results confirm the intuition that the nondegenerate diffusions components dominate any type of Lévy jumps in determining the regularity of the value function for obstacle problems. We also develop a non-local version of the interior Schauder estimate in Proposition 3.5, which could be useful to study other integro-differential equations with irregular initial conditions.

The remainder of the paper is organized as follows. After introducing notation at the end of this section, main results are presented in Section 2. Regularity properties of the infinitesimal generator of are analyzed in Section 3. Then main results are proved in Section 4.

1.1. Notation

For a given open interval with , let us define the -neighborhood of as for . We will also denote , for any , , and by the closure of the indicated set . Let us recall definitions of Sobolev spaces and Hölder spaces in what follows; see [18] pp. 5-7 for further details.

Definition 1.1.

denotes the class of continuous functions on with continuous classical time and spatial derivatives up to the first and second order respectively.

For any positive integer , is the space of functions with generalized derivatives , , , and a finite norm . The space consists of functions whose -norm is finite on any compact subsets of .

For any positive nonintegral real number , is the space of functions that are continuous in with continuous classical derivatives for , and have finite norm , in which , , and , for a constant . The space is the Hölder space when only the spatial variable is considered.

2. Main results

2.1. Model

Let us first specify the jump diffusion in (1.1). We assume that the drift and the volatility of , the discounting factor , and the jump size satisfy the following set of assumptions:

Assumption 2.1.

Let . Coefficients for some , . Moreover, there exist a strictly positive constant such that for all . The jump size is continuously differentiable in and is Hölder continuous in , moreover there exists a constant such that

| (2.1) |

for , or , and .

Without loss of generality, we will take in (2.1) to be equal to one, otherwise we would rescale the process . For the pure jump component in (1.1), we assume that is a Lévy measure on . See [24] for this terminology. In particular, we require that . When , the jump component of (1.1) is a Lévy process. The aforementioned assumptions on coefficients and the jump component ensure that (1.1) admits a unique strong solution (see [16]), which we denote by . This jump diffusion process is said to have finite activity, if is a finite measure on , otherwise it is said to have infinite activity. We say that the jumps of have finite variation, if , otherwise we say that they have infinite variation.

Among all possible Lévy measures, we consider the following large subclass in this paper:

Assumption 2.2.

The Lévy measure satisfies . Moreover it has a density, which we denote by , and this density satisfies on , for some constants and .

Note that the interval can be replaced by any other neighborhood of in our analysis, our choice of this interval is made for notational convenience.

Remark 2.3.

Virtually all Lévy processes used in the financial modeling satisfy above assumption. For jump diffusions models, is a finite measure as in Merton’s and Kou’s model. For normal tempered stable processes, has a power singularity at , with ; see (4.25) in [10]. In particular, this class contains Variance Gamma and Normal Inverse Gaussian where or respectively. For generalized tempered stable processes (see Remark 4.1 in [10]), with and . In particular, CGMY processes in [9] and regular Lévy processes of exponential type (RLPE) in [8] are special examples of this class.

Having introduced the jump diffusion process , let us discuss the problem (OS). We assume that the payoff function satisfies the following set of assumptions:

Assumption 2.4.

The payoff function is positive, bounded and Lipschitz continuous on . That is, there exists positive constants and such that for any and for any . Moreover satisfies for some positive constant in the distributional sense, i.e., for any compactly supported smooth function on .

A typical example, where these assumptions holds, is the American put option payoff for some .

For the problem (OS), we define its continuation region and stopping region as usual:

2.2. Main regularity results

Intuitively, one can expect from Itô’s formula that the value function satisfies the following variational inequality:

| (2.2) |

Here, the integro-differential operator is the infinitesimal generator of . Its application on a smooth test function is

| (2.3) |

where and the integral term

| (2.4) |

In what follows we will not write down the arguments of explicitly or only indicate the argument that we are focusing in order to keep the notation simple.

In general, one does not know a priori whether is sufficiently smooth so that it solves (2.2) in the classical sense. Moreover, it is not even clear whether is well defined in the classical sense. When is Lipschitz continuous on with a Lipschitz continuous derivative in a neighborhood of , it can be shown that is well defined in the classical sense. Indeed, where

Here, the first inequality follows from the Lipschitz continuity of and the assumption that ; the mean value theorem implies the second equality in (2.2) where satisfies ; the last inequality holds due to the Lipschitz continuity of in an -neighborhood of . However, the value function , in general, does not have these regularity properties mentioned above. We only know from Lemma 3.1 in [23] that is Lipschitz continuous in and Hölder continuous in . Nevertheless, we will see that the integral term is well defined in the classical sense in Lemma 3.2 below. In fact, more is true as we show in the next theorem, which is the main result of the paper.

Theorem 2.5.

The following corollary is of special interest for the American option problem.

Corollary 2.6.

Under the assumptions of Theorem 2.5,

-

(i)

, i.e., the smooth-fit holds;

-

(ii)

in the region where .

Remark 2.7.

When jumps of have finite variation, i.e., , the proof of the main result is much simpler. This is because, when jumps of have finite variation, the infinitesimal generator can be rewritten so that its integral component has a reduced form. For any test function that is Lipschitz continuous in its first variable, can be decomposed as , in which and

| (2.6) |

The previous integral is clearly well defined. Indeed follows from the Lipschitz continuity of and . Moreover, is also Hölder continuous in its both variables; see Lemma 3.1 below. Since the value function is known to be Lipschitz continuous in its first variable (see Lemma 3.1 in [23]), is already well defined and Hölder continuous. Therefore, in order to study the regularity of , can be treated as a driving term in (2.2). However, this simplification cannot be applied when jumps of have infinite variation, i.e., .

3. Regularity properties of the integro-differential operator

3.1. The integral operator

The integral operator has two basic features. First, has a singularity at . As a result, maps functions with certain degree of regularity to functions with less regularity. This is contrast to the case in which is a finite measure. In that case is already well defined, for any with at most linear growth, and this integral has the same regularity as ; see [26]. Second, is a nonlocal operator. Therefore, regularity of on a given interval depends on outside . In this subsection, we shall study these two features in detail and analyze the regularity of when is either a function in certain Hölder or Sobolev spaces.

Consider as an operator between Hölder spaces. When jumps of have finite variation, we can work with the reduced integral operator in (2.6). It has the following regularity property.

Lemma 3.1.

Let Assumption 2.2 hold with and . For any which is Lipschitz continuous in its first variable and -Hölder continuous in its second variable,

However when jumps of have infinite variation, the integral term is no longer well defined for Lipschitz continuous functions. Hence we work with and its integral part in the forms of (2.3) and (2.4). We will see that if we choose an appropriate test function , is still well defined and Hölder continuous in both its variables. Regularity estimates of the following type have been obtained in [25] and [21].

Lemma 3.2.

Let Assumption 2.2 hold with and .

-

(i)

Suppose that satisfies for some and any . If, moreover, for some , then and

(3.1) for a positive constant depending on , , and .

-

(ii)

If for some , then and

(3.2) for a positive constant depending on and .

Here when ; is an arbitrary number in when .

Proof of Lemma 3.2.

Statement (ii) is a special case of Statement (i) when the domain is taken to be , instead of . In particular, ; see Definition 1.1. It then suffices to prove statement (i). For notational simplicity, represents a generic constant throughout the rest of proof.

Step 1: Estimate . For any ,

where the second inequality follows from the mean value theorem with ; the third inequality is the result of the -Hölder continuity of on and ; the fourth inequality holds thanks to Assumption 2.2.

Step 2: Show that is Hölder continuous in . For and , we break up into three parts:

where variables and are ignored in and the constant will be determined later. Let us estimate each above integral term separately. First, an estimate similar to that in Step 1 shows that Second, it follows from the Lipschitz continuity of , -Hölder continuity of , and that

Similarly, . Therefore,

where the second inequality follows from Assumption 2.2. Third, it is clear from the Lipschitz continuity of and (2.1) that .

Now pick . Since and , we have , , and . All above estimates combined imply that

for a constant independent of , , and .

When is considered as an operator between Sobolev spaces, it maps functions to functions on a smaller domain.

Lemma 3.3.

Let Assumption 2.2 hold. Consider a function such that is bounded and is locally bounded on . Then for any and ,

| (3.4) |

for some constant depending on , , and .

Remark 3.4.

When has finite variation jumps, i.e., , in (3.4) can be chosen as zero. Hence norm of only depends on and .

Proof.

Utilizing truncation and smooth mollification, one can construct a sequence of smooth function such that converges to in and converges to in as (c.f. Section 5.3 and Appendix C.4 in [12]). Therefore, it suffices to prove the statement for a smooth function .

To this end, observing that , the integral can be bounded above by three integral terms:

In the rest of proof, the -norm of each above term is estimated respectively. First,

where the first inequality follows from Fubini’s theorem and Jensen’s inequality since ; the second inequality is a result of the assumption that and Assumption 2.2; the third inequality follows from Hölder inequality with ; the fourth inequality utilizes Fubini’s theorem; and the fifth inequality holds since for any and . Second, since for , and , it follows that

Third, it is clear that , since is bounded.

Now, recall . The statement then follows from above -norm estimates on , . ∎

3.2. An interior estimate

The norm estimate of the integral term in Lemma 3.3 helps to derive the following norm estimate for solutions of the Cauchy problem below. This estimate is a nonlocal version of the parabolic Calderon-Zygmund estimate (c.f. Theorem 9.1 in [18] pp.341).

Proposition 3.5.

Remark 3.6.

The main idea of the following proof is to treat as a driving term and utilize the classical Calderon-Zygmund estimate for local PDEs. However, as we have seen in Lemma 3.3, norm of controls norm of , which in turn bounds the norm of via the Calderon-Zygmund estimate. Therefore, a careful balance between extending domains and controlling norm of needs to be maintained in the following proof. This is contrast to the case where only finite variation jumps are considered. As we have seen in Remark 3.4, and control the norm of which bounds the -norm of . Hence, in the case of finite variation jumps, (3.5) can be obtained directly from the classical Calderon-Zygmund estimate for local PDEs.

Proof.

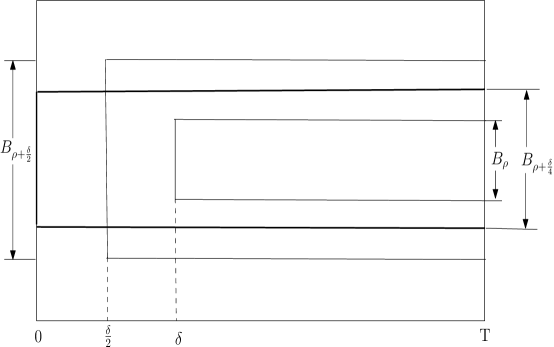

The constant denotes a generic constant throughout this proof. Domains used in this proof are displayed in Figure 1.

For a constant which will be determined later, let us choose a cut-off function such that , inside and outside . Moreover can be chosen to satisfy

| (3.6) |

The function satisfies

in which . Appealing to Theorem 9.1 in [18] pp.341, we can find a constant such that

| (3.7) |

where all -norms on the right-hand-side are taken on .

In what follows, we will estimate the terms on the right-hand-side of (3.7) respectively. First, when ,

where the first inequality follows from the choice of ; the second inequality follows from Lemma 3.3 with , , and . When , a similar estimate can be obtained. In that case, the rest of proof is similar to that for case, hence we only present the proof for henceforth. Second, it is clear that Third, we will estimate the norm of . To this end, let us derive a bound for in what follows. It follows from (3.6) that

where is the Lebesgue measure. Estimates on other terms of can be performed similarly to obtain

Utilizing above estimates on the right-hand-side of (3.7), we obtain

Multiplying on both hand sides of the previous inequality,

where . Denote . The previous inequality gives the following recursive inequality

Now choosing a sufficiently small such that , we obtain from the above inequality that

Note that is finite for any , since the norm of is finite in any compact domain of , and is increasing in . We then obtain from iterating the previous inequality that

In terms of norms, the previous inequality reads

∎

4. Proof of main results

4.1. The penalty method

We use the penalty method (see e.g. [14] and [26]) to analyze the following variational inequality:

| (4.1) |

The nonlocal integral term introduces several technical difficulties in applying the penalty method. In this section, we will focus on the case where has infinite variation jumps, i.e., Assumption 2.2 holds with . When has finite variation jumps, i.e., , the integral operator has the reduced form in (2.6), see Remark 2.7. Then all proofs are similar but easier than those in the infinite variation case.

For each , consider the following penalty problem:

| (4.2) |

Here is a mollified sequence of such that , , and for any ; see [14] pp.27 for its construction. The mollified sequence can be chosen such that constants , and , appearing in Assumption 2.4, are independent of . The penalty term is chosen to satisfy following properties:

| (4.3) |

where , , and are finite thanks to Assumption 2.1. Indeed, can be chosen as a smooth mollification of the function .

Now we show that each penalty problem (4.2) has a classical solution. To this end, let us first recall the Schauder fixed point theorem (see Theorem 2 in [13] pp. 189).

Lemma 4.1.

Let be a closed convex subset of a Banach space and let be a continuous operator on such that is contained in and is precompact. Then has a fixed point in .

Lemma 4.2.

Proof.

We will first prove the existence on a sufficiently small time interval via the Schauder fixed point theorem, then extend this solution to the interval .

Let us consider the set , where and will be determined later. It is clear that is a bounded, closed and convex set in the Banach space . For any , consider the following Cauchy problem for :

| (4.4) |

We define an operator via using the solution of (4.4). Let us check the conditions for the Schauder fixed point theorem are satisfied in the following four steps:

Step 1: is well defined. Since with , Lemma 3.2 part (ii) implies that with . On the other hand, using properties of , and , one can check that . Therefore, Theorem 5.1 in [18] pp. 320 implies that (4.4) has a unique solution . Hence , since is smooth.

Step 2. . It follows from Lemma 2 in [13] pp. 193 that there exists a positive constant , depending on , such that

| (4.5) |

where , is the constant in Step 1, and is a sufficiently large constant. Let be such that and let . Since , it then follows from (4.5) that

| (4.6) |

This confirms that .

Step 3. is a precompact subset of . For any , an estimate similar to (4.5) shows that for any , for some constant depending on and . Since bounded subsets of are precompact subsets of (see Theorem 1 in [13] pp.188), then is a precompact subset in .

Step 4. is a continuous operator. Let be a sequence in such that , we will show . From (4.4), satisfies the Cauchy problem

It follows again from Lemma 2 in [13] pp. 193 that

Now all conditions of the Schauder fixed point theorem are checked, hence has a fixed point in , which is denoted by . Moreover, it follows from results in Step 1 that .

Finally, let us extend to the interval . We can replace by in (4.4), since is finite thanks to the result after Step 4 and because the choice of in Step 2 only depends on and . If we choose a sufficiently large , depending on , such that (4.6) holds on , then is finite thanks to the argument after Step 4. Now one can repeat this procedure to extend the time interval by each time, until it contains . ∎

After the existence of classical solutions for (4.2) is established, we will study properties of the sequence in the rest of this subsection. The following maximum principle is a handy tool in our analysis.

Lemma 4.3.

Suppose that , and are bounded and the Levy measure satisfies . Assume also that we are given a function bounded from below on . If satisfies and is bounded from below on , then for implies that on .

Proof.

Let and on for some positive constants and . For any positive , consider the following function:

where will be determined later and is an increasing function such that in a neighborhood of and for sufficiently large . It is clear that and derivatives and are bounded. Then is bounded on . Indeed, there exists a constant such that

Combining above estimate with , one can find a sufficient large constant such that

Now define . The previous estimate gives

| (4.7) |

On the other hand, due to , moreover for because is increasing and . Therefore, we claim that for . Indeed, if there exists such that , must take its negative minimum at some point . Note that this is also a global minimum for on , hence , , , , and . As a result, which contradicts with (4.7). Now for fixed point , the statement follows from sending the constant in to . ∎

This maximum principle implies the uniqueness of classical solutions for the penalty problem (4.2).

Proof.

Lemma 4.2 and the definition of Hölder spaces combined imply that is a bounded classical solution. Now suppose there exists another solution , then satisfies

It follows from the mean value theorem that for some , where thanks to (4.3)-(iv). Now it follows from Lemma 4.3, with that on . The same argument applied to gives the reverse inequality. ∎

Utilizing the maximum principle, we will analyze properties of the sequence in the following results.

Proof.

It follows from Lemma 4.2 that is bounded on for each . In this proof, we will show that the bounds are uniform in . First, it follows from (4.3) part (i) that . Moreover, for . Then first inequality in the statement follows from Lemma 4.3 directly. Second, consider , it satisfies

Combining (4.3) part (ii) and , we have . Hence,

| (4.8) |

where the first equality follows from the mean value theorem. Now applying Lemma 4.3 to above equation with (see (4.3) part (iv)), we obtain on for any , which confirms the second inequality in the statement of the lemma. ∎

Proof.

Formally differentiating (4.2) with respect to gives the following equation:

| (4.9) |

Here , where the second integral is well defined for Lipschitz bounded function because from (2.1) and from Assumption 2.2. We will show that is indeed a classical solution of (4.9). To this end, let us consider the equation

Using Assumption 2.1 and Lemma 4.2, one can check that the driving term and all coefficients of the previous equation are Hölder continuous. It then follows from Theorem 3.1 in [15] on pp. 89 that the last equation has a classical solution, say . Define . It is straight forward to check that is a classical solution of the following equation

Since and are both bounded, then is also bounded. As a result, estimate (3.6) in Theorem 3.1 of [15] on pp. 89 implies that is bounded solution of the last equation. However, Corollary 4.4 already shows that is the unique bounded solution of the last solution, therefore , hence on and is a classical solution of (4.9).

Now we shall show is bounded uniformly in . Consider , where is given by Assumption 2.4 and will be determined later. The function satisfies the following equation

| (4.10) |

Recall that and are bounded from Assumption 2.1. Observe that because and . Moreover, is bounded uniformly in thanks to Lemma 4.5. Therefore, one can find a sufficiently large , independent of , such that . On the other hand, is also positive due to (4.3)-(iv) and . As a result, the right-hand-side of (4.10) is positive. Now since is bounded from below, moreover the Lévy measure associated to satisfies (see (2.1) and Assumption 2.2), we then have from Lemma 4.3 with that on . Hence on , for some positive independent of . The upper bound can be shown similarly by working with . ∎

Proof.

Let us first show that is uniformly bounded from below. Indeed,

where the inequality follows from and . As a result, is bounded from above. This is because

where the second equality follows from (4.3) part (iii). Therefore,

The previous inequality and the mean value theorem combined imply that

for some . Hence the statement of the lemma follows applying Lemma 4.3 to the previous inequality and choosing . ∎

Corollary 4.8.

Let assumptions of Lemma 4.7 hold. Then is bounded uniformly in .

4.2. Proof of Theorem 2.5 and Corollary 2.6

Proof of Theorem 2.5.

The proof consists of two steps. First, we show that there exists a function which solves (4.1) and for any integer , compact domain , and . Second, we confirm that is the value function for the problem (OS).

Step 1: First, it follows from Lemma 4.2 that , , and are continuous, hence locally bounded on . Therefore for each . Second, Lemmas 4.5 and 4.6 show that and are bounded on , uniformly in . Moreover, the penalty term is also bounded uniformly in due to Corollary 4.8. Therefore these boundedness properties and Proposition 3.5 with together imply that

| (4.11) |

Thanks to the weak compactness of the Sobolev space , , we can then find a subsequence converging to zero and a function , such that . Here represents the weak convergence; c.f. Appendix D.4. in [12] pp. 639. In fact this convergence can be shown to be pointwise and uniform in the index. Indeed, (4.11) and the Sobolev embedding theorem (c.f. Lemma 3.3 in [18] pp. 80) combined imply that

Choosing so that and using the previous uniform estimate along with the Arzelà-Ascoli theorem, we then find a further subsequence of , which is still denoted by , such that converge to uniformly on . Since each is continuous, is also continuous on .

Let us show that solves (4.1). On the one hand, since , we have for each . Hence

for any compactly supported smooth function . Here the identity above follows from applying the dual operator of to and utilizing the dominated convergence theorem. The previous inequality then yields on in the distributional sense, which implies the same inequality on in the distributional sense, since the choices of and are arbitrary. On the other hand, Lemma 4.7 shows that . Then after sending . Therefore, we obtain on in the distributional sense. It then remains to show when . To this end, take any such that . Since both and are continuous, one can find a sufficiently small and a small neighborhood of , such that for any inside this neighborhood. Utilizing the uniform convergence of and , we can then find sufficiently small such that in the aforementioned neighborhood. Hence , due to (4.3)-(ii), which induces . After sending , we conclude that in the distributional sense when . Finally, since , also solves (4.1) at almost every point in .

Step 2: Let us first show that is a viscosity solution of (4.1). We will use the definition of viscosity solutions in [23]. Denote by the class of functions which have at most linear growth, i.e., for some and any . Then viscosity solutions of (4.1) are defined as follows: Any is a viscosity supersolution (subsolution) of (4.1) if

for any function such that and () for any other point . The function is said to be a viscosity solution of (4.1) if it is both supersolution and subsolution.

Let us show that is a viscosity subsolution of (4.1). Fix , consider , otherwise is automatically satisfied. Without loss of generality we can assume that is the strict maximum of in a neighborhood , otherwise the test function can be modified appropriately. On the other hand, since converges to uniformly in compact domains, we can find sufficiently small such that attains its maximum over at . Moreover, as . Since is a classical solution of (4.2) (see Lemma 4.2), it is also a viscosity solution. Hence . Now, since and converges to , we obtain . As a result, by sending . This confirms that is a viscosity subsolution of (4.1).

For the supersolution property, since , it suffices to show that for any test function . This follows from the similar arguments which we used for the subsolution property in the previous paragraph.

Proof of Corollary 2.6.

(i) Combining Theorem 2.5 and the Sobolev embedding theorem (c.f. Lemma 3.3 in [18] pp. 80), we have , where and . Choosing so that , the continuity of follows from Definition 1.1.

(ii) Let us first show that is well defined and Hölder continuous. Since (which follows due to (i)), choosing sufficiently large so that , by Lemma 3.2 part (i). Now, for and such that , consider the following boundary value problem:

| (4.12) |

It is straightforward to show that is the unique viscosity solution for the previous problem using the fact that is the unique viscosity solution for (2.2). On the other hand, since the boundary and terminal values of (4.12) are continuous and the driving term is Hölder continuous, it follows from Theorem 9 in [13] pp. 69 that (4.12) has a classical solution . Hence on , since is also a viscosity solution. Therefore, . The statement now follows, since is an arbitrary subset of . ∎

References

- [1] Y. Aït-Sahalia and J. Jacod, Estimating the degree of activity of jumps in high frequency data, The Annals of Statistics, 37 (2009), pp. 2202–2244.

- [2] , Is Brownian motion necessary to model high frequency data?, The Annals of Statistics, 38 (2010), pp. 3093–3128.

- [3] A. L. Amadori, Obstacle problem for nonlinear integro-differential equations arising in option pricing, Ricerche di Matematica, 56 (2007), pp. 1–17.

- [4] G. Barles and C. Imbert, Second-order elliptic integro-differential equations: viscosity solutions’ theory revisited, Annales de l’Institut Henri Poincaré. Analyse Non Linéaire, 25 (2008), pp. 567–585.

- [5] E. Bayraktar, A proof of the smoothness of the finite time horizon American put option for jump diffusions, SIAM Journal on Control and Optimization, 48 (2009), pp. 551–572.

- [6] E. Bayraktar and H. Xing, Analysis of the optimal exercise boundary of American options for jump diffusions, SIAM Journal on Mathematical Analysis, 41 (2009), pp. 825–860.

- [7] A. Bensoussan and J.-L. Lions, Impulse control and quasivariational inequalities, Gauthier-Villars, Montrouge, 1984.

- [8] S. I. Boyarchenko and S. Z. Levendorskiĭ, Non-Gaussian Merton-Black-Scholes theory, vol. 9 of Advanced Series on Statistical Science & Applied Probability, World Scientific Publishing Co. Inc., River Edge, NJ, 2002.

- [9] P. Carr, H. Geman, D. B. Madan, and M. Yor, Stochastic volatility for Lévy processes, Mathematical Finance, 13 (2003), pp. 345–382.

- [10] R. Cont and P. Tankov, Financial modelling with jump processes, Chapman & Hall/CRC Financial Mathematics Series, Chapman & Hall/CRC, Boca Raton, FL, 2004.

- [11] M. Davis, X. Guo, and G. Wu, Impulse control of multidimensional jump diffusions, SIAM Journal on Control and Optimization, 48 (2010), pp. 5276–5293.

- [12] L. C. Evans, Partial differential equations, vol. 19 of Graduate Studies in Mathematics, American Mathematical Society, Providence, RI, 1998.

- [13] A. Friedman, Partial differential equations of parabolic type, Prentice-Hall Inc., Englewood Cliffs, N.J., 1964.

- [14] , Variational Principles and Free-boundary Problems, John Wiley & Sons Inc., New York, 1982.

- [15] M. G. Garroni and J.-L. Menaldi, Green functions for second order parabolic integro-differential problems, vol. 275 of Pitman Research Notes in Mathematics Series, Longman Scientific & Technical, Harlow, 1992.

- [16] I. Gihman and A. V. Skorohod, Stochastic Differential Equations, Springer Berlag, Berlin, 1972.

- [17] X. Guo and G. Wu, Smooth fit principle for impulse control of multidimensional diffusion processes, SIAM Journal on Control and Optimization, 48 (2009), pp. 594–617.

- [18] O. A. Ladyženskaja, V. A. Solonnikov, and N. N. Uralchva, Linear and Quasi-linear Equations of Parabolic Type, American Mathematical Society, Providence, Rhode Island, 1968.

- [19] D. Lamberton and M. Mikou, The critical price for the American put in an exponential Lévy model, Finance and Stochastics, 12 (2008), pp. 561–581.

- [20] S. Lenhart, Integro-differential operators associated with diffusion processes with jumps, Applied Mathematics and Optimization, 9 (1982/83), pp. 177–191.

- [21] R. Mikulevičius and C. Zhang, On the rate of convergence of weak Euler approximation for nondegenerate SDEs driven by Lévy processes, Stochastic Processes and their Applications, 121 (2011), pp. 1720-1748.

- [22] H. Pham, Optimal stopping, free boundary, and American option in a jump-diffusion model, Applied Mathematics and Optimization, 35 (1997), pp. 145–164.

- [23] , Optimal stopping of controlled jump diffusion processes: a viscosity solution approach, Journal of Mathematical Systems, Estimation, and Control, 8 (1998), pp. 1–27.

- [24] K. Sato, Lévy processes and infinitely divisible distributions, vol. 68 of Cambridge Studies in Advanced Mathematics, Cambridge University Press, Cambridge, 1999.

- [25] L. Silvestre, Regularity of the obstacle problem for a fractional power of the laplace operator, Communications on Pure and Applied Mathematics, 60 (2006), pp. 67–112.

- [26] C. Yang, L. Jiang, and B. Bian, Free boundary and American options in a jump-diffusion model, European Journal of Applied Mathematics, 17 (2006), pp. 95–127.

- [27] X. L. Zhang, Méthodes Numériques pour le Calcul des Options Américaine dans des Modèles de diffusion avec sauts, PhD thesis, l’Ecole Nationale des Ponts et Chaussées, Paris, 1994.