S. N. Ethier

University of Utah

Department of Mathematics

155 S. 1400 E., JWB 233

Salt Lake City, UT 84112, USA

e-mail: ethier@math.utah.eduJiyeon Lee

Yeungnam University

Department of Statistics

214-1 Daedong, Kyeongsan

Kyeongbuk 712-749, South Korea

e-mail: leejy@yu.ac.krSupported by the Yeungnam University research grants in 2008.

Abstract

That there exist two losing games that can be combined, either by random mixture or by nonrandom alternation, to form a winning game is known as Parrondo’s paradox. We establish a strong law of large numbers and a central limit theorem for the Parrondo player’s sequence of profits, both in a one-parameter family of capital-dependent games and in a two-parameter family of history-dependent games, with the potentially winning game being either a random mixture or a nonrandom pattern of the two losing games. We derive formulas for the mean and variance parameters of the central limit theorem in nearly all such scenarios; formulas for the mean permit an analysis of when the Parrondo effect is present.

Key words: Parrondo’s paradox, Markov chain, strong law of large numbers, central limit theorem, strong mixing property, fundamental matrix, spectral representation.

Submitted to EJP on February 18, 2009, final version accepted August 3, 2009.

1 Introduction

The original Parrondo (1996) games can be described as follows: Let and

(1)

where is a small bias parameter (less than 1/10, of course). In game , the player tosses a -coin (i.e., is the probability of heads). In game , if the player’s current capital is divisible by 3, he tosses a -coin, otherwise he tosses a -coin. (Assume initial capital is 0 for simplicity.) In both games, the player wins one unit with heads and loses one unit with tails.

It can be shown that games and are both losing games, regardless of , whereas the random mixture (toss a fair coin to determine which game to play) is a winning game for sufficiently small. Furthermore, certain nonrandom patterns, including , , and but excluding , are winning as well, again for sufficiently small. These are examples of Parrondo’s paradox.

The terms “losing” and “winning” are meant in an asymptotic sense. More precisely, assume that the game (or mixture or pattern of games) is repeated ad infinitum. Let be the player’s cumulative profit after games for . A game (or mixture or pattern of games) is losing if a.s., it is winning if a.s., and it is fair if a.s. These definitions are due in this context to Key, Kłosek, and Abbott (2006).

Because the games were introduced to help explain the so-called flashing Brownian ratchet (Ajdari and Prost 1992), much of the work on this topic has appeared in the physics literature. Survey articles include Harmer and Abbott (2002), Parrondo and Dinís (2004), Epstein (2007), and Abbott (2009).

Game can be described as capital-dependent because the coin choice depends on current capital. An alternative game , called history-dependent, was introduced by Parrondo, Harmer, and Abbott (2000): Let

(2)

where is a small bias parameter. Game is as before. In game , the player tosses a -coin (resp., a -coin, a -coin, a -coin) if his two previous results are loss-loss (resp., loss-win, win-loss, win-win). He wins one unit with heads and loses one unit with tails.

The conclusions for the history-dependent games are the same as for the capital-dependent ones, except that the pattern need not be excluded.

Pyke (2003) proved a strong law of large numbers for the Parrondo player’s sequence of profits in the capital-dependent setting. In the present paper we generalize his result and obtain a central limit theorem as well. We formulate a stochastic model general enough to include both the capital-dependent and the history-dependent games. We also treat separately the case in which the potentially winning game is a random mixture of the two losing games (game is played with probability , and game is played with probability ) and the case in which the potentially winning game (or, more precisely, pattern of games) is a nonrandom pattern of the two losing games, specifically the pattern , denoting plays of game followed by plays of game . Finally, we replace (1) by

where ; (1) is the special case .

We also replace (2) by

where , , and ; (2) is the special case and . The reasons for these parametrizations are explained in Sections 3 and 4.

Section 2 formulates our model and derives an SLLN and a CLT. Section 3 specializes to the capital-dependent games and their random mixtures, showing that the Parrondo effect is present whenever and . Section 4 specializes to the history-dependent games and their random mixtures, showing that the Parrondo effect is present whenever either or and . Section 5 treats the nonrandom patterns and derives an SLLN and a CLT. Section 6 specializes to the capital-dependent games, showing that the Parrondo effect is present whenever and with one exception: . Section 7 specializes to the history-dependent games. Here we expect that the Parrondo effect is present whenever either or and (without exception), but although we can prove it for certain specific values of and (such as and ), we cannot prove it in general. Finally, Section 8 addresses the question of why Parrondo’s paradox holds.

In nearly all cases we obtain formulas for the mean and variance parameters of the CLT. These parameters can be interpreted as the asymptotic mean per game played and the asymptotic variance per game played of the player’s cumulative profit. Of course, the pattern comprises games.

Some of the algebra required in what follows is rather formidable, so we have used Mathematica 6 where necessary. Our .nb files are available upon request.

2 A general formulation of Parrondo’s games

In some formulations of Parrondo’s games, the player’s cumulative profit after games is described by some type of random walk , and then a Markov chain is defined in terms of ; for example, in the capital-dependent games, where denotes initial capital. However, it is more logical to introduce the Markov chain first and then define the random walk in terms of .

Consider an irreducible aperiodic Markov chain with finite state space . It evolves according to the one-step transition matrix111In the physics literature the one-step transition matrix is often written in transposed form, that is, with column sums equal to 1. We do not follow that convention here. More precisely, here . . Let us denote its unique stationary distribution by . Let be an arbitrary function, which we will sometimes write as a matrix and refer to as the payoff matrix. Finally, define the sequences and by

(3)

and

(4)

For example, let , put , being initial capital, and let the payoff matrix be given by222Coincidentally, this is the payoff matrix for the classic game stone-scissors-paper. However, Parrondo’s games, as originally formulated, are games of chance, not games of strategy, and so are outside the purview of game theory (in the sense of von Neumann).

(5)

With the role of played by

where and are as in (1),

represents the player’s profit after games when playing the capital-dependent game repeatedly. With the role of played by

where ,

represents the player’s profit after games when playing game repeatedly. Finally, with the role of played by , where , represents the player’s profit after games when playing the mixed game repeatedly. In summary, all three capital-dependent games are described by the same stochastic model with a suitable choice of parameters.

Similarly, the history-dependent games fit into the same framework, as do the “primary” Parrondo games of Cleuren and Van den Broeck (2004).

Thus, our initial goal is to analyze the asymptotic behavior of under the conditions of the second paragraph of this section. We begin by assuming that has distribution , so that and hence are stationary sequences, although we will weaken this assumption later.

We claim that the conditions of the stationary, strong mixing central limit theorem apply to . To say that has the strong mixing property (or is strongly mixing) means that as , where

A version of the theorem for bounded sequences (Bradley 2007, Theorem 10.3) suffices here. That version requires that . In our setting, is strongly mixing with a geometric rate (Billingsley 1995, Example 27.6), hence so is . Since are bounded by , it follows that

converges absolutely. For the theorem to apply, it suffices to assume that .

Let us evaluate the mean and variance parameters of the central limit theorem. First,

(6)

and

To evaluate , we first find

from which it follows that

We conclude that

where is the fundamental matrix associated with (Kemeny and Snell 1960, p. 75).

In more detail, we let denote the square matrix each of whose rows is , and we find that

where

(7)

for the last equality, see Kemeny and Snell (loc. cit.). Therefore,

(8)

A referee has pointed out that these formulas can be written more concisely using matrix notation. Denote by (resp., ) the matrix whose th entry is (resp., ), and let . Then

(9)

If , then (Bradley 2007, Proposition 8.3)

and the central limit theorem applies, that is, . If we strengthen the assumption that by assuming that , where , we have (Bradley 2007, proof of Lemma 10.4)

hence by the Borel–Cantelli lemma it follows that a.s. In other words, the strong law of large numbers applies.

Finally, we claim that, if and , then

(10)

Indeed, is stationary and strongly mixing, hence its future tail -field is trivial (Bradley 2007, p. 60), in the sense that every event has probability 0 or 1. It follows that is 0 or 1. Since and , we can invoke the central limit theorem to conclude that this probability is 1. Similarly, we get .

Each of these derivations required that the sequence be stationary, an assumption that holds if has distribution , but in fact the distribution of can be arbitrary, and need not be stationary.

Theorem 1.

Let and be as in (6) and (8).

Under the assumptions of the second paragraph of this section, but with the distribution of arbitrary,

Assume that . It follows that, if is the player’s cumulative profit after games for each , then the game (or mixture or pattern of games) is losing if , winning if , and fair if . (See Section 1 for the definitions of these three terms.)

Proof.

It will suffice to treat the case , and then use this case to prove the general case.

Let be a Markov chain in with one-step transition matrix and initial distribution , so that is stationary, as above.

Let , and define

Then is a Markov chain in with one-step transition matrix and initial state . We can define and in terms of it by analogy with (3) and (4). If , then

and is bounded by . Thus, if we divide by or , the result tends to 0 a.s. as . We get the SLLN and the CLT with in place of , via this coupling of the two sequences. We also get the last conclusion in a similar way. The first equation in (11) follows from the second using bounded convergence. Finally, the random variable has finite moments (Durrett 1996, Chapter 5, Exercise 2.5). The first equation in (12) therefore follows from our coupling.

∎

A well-known (Bradley 2007, pp. 36–37) nontrivial example for which is the case in which and for all . Then (a telescoping sum) for all , hence and by Theorem 1.

However, it may be of interest to confirm these conclusions using only the mean, variance, and covariance formulas above. We calculate

(13)

and

(14)

Since , we can multiply on the right by and use to get .

This implies that

The Markov chain underlying the capital-dependent Parrondo games has state space and one-step transition matrix of the form

(15)

where . It is irreducible and aperiodic. The payoff matrix is as in (5).

It will be convenient below to define for .

Now, the unique stationary distribution has the form

where .

Further, the fundamental matrix is easy to evaluate (e.g., ).

We conclude that satisfies the SLLN with

and the CLT with the same and with

where satisfies (mod 3), at least if .

We now apply these results to the capital-dependent Parrondo games.

Although actually much simpler, game fits into this framework with one-step transition matrix defined by (15) with

where is a small bias parameter.

In game , it is typically assumed that, ignoring the bias parameter, the one-step transition matrix is defined by (15) with

These two constraints determine a one-parameter family of probabilities given by

(16)

To eliminate the square root, we reparametrize the probabilities in terms of . Restoring the bias parameter, game has one-step transition matrix defined by (15) with

(17)

which includes (1) when .

Finally, game is a mixture of the two games, hence has one-step transition matrix , which can also be defined by (15) with

Let us denote the mean for game by , to emphasize the game as well as its dependence on . Similarly, we denote the variance for game by . Analogous notation applies to games and . We obtain, for game , and ; for game ,

and

and for game ,

and

One can check that for all and .

The formula for was found by Percus and Percus (2002) in a different form. We prefer the form given here because it tells us immediately that game has smaller variance than game for each , provided is sufficiently small. With and , Harmer and Abbott (2002, Fig. 5) inferred this from a simulation.

The formula for was obtained by Berresford and Rockett (2003) in a different form. We prefer the form given here because it makes the following conclusion transparent.

Theorem 2(Pyke 2003).

Let and let games and be as above but with the bias parameter absent. If and , then for all , for , and for all .

Assuming (17) with , the condition is equivalent to .

Clearly, the Parrondo effect appears (with the bias parameter present) if and only if . A reverse Parrondo effect, in which two winning games combine to lose, appears (with a negative bias parameter present) if and only if .

Corollary 3(Pyke 2003).

Let games and be as above (with the bias parameter present).

If and , then there exists , depending on and , such that Parrondo’s paradox holds for games , , and , that is, , , and , whenever .

The theorem and corollary are special cases of results of Pyke. In his formulation, the modulo 3 condition in the definition of game is replaced by a modulo condition, where , and game is replaced by a game analogous to game but with a different parameter . Pyke’s condition is equivalent to . We have assumed and .

We would like to point out a useful property of game . We assume and we temporarily denote , , and by , , and to emphasize their dependence on . Similarly, we temporarily denote and by and . Replacing by has the effect of changing the win probabilities and to the loss probabilities and , and vice versa. Therefore, given , we expect that

a property that is in fact realized by coupling the Markov chains and so that for all . It follows that

(18)

The same argument gives (18) for game . The reader may have noticed that the formulas derived above for and , as well as those for and , satisfy (18).

When , the mean and variance formulas simplify to

and, if as well,

4 Mixtures of history-dependent games

The Markov chain underlying the history-dependent Parrondo games has state space and one-step transition matrix of the form

(19)

where . Think of the states of in binary form: 00, 01, 10, 11. They represent, respectively, loss-loss, loss-win, win-loss, and win-win for the results of the two preceding games, with the second-listed result being the more recent one. The Markov chain is irreducible and aperiodic. The payoff matrix is given by

It will be convenient below to define for .

Now, the unique stationary distribution has the form

where .

Further, the fundamental matrix can be evaluated with some effort (e.g., ).

We conclude that satisfies the SLLN with

and the CLT with the same and with

where satisfies (mod 4), at least if .

We now apply these results to the history-dependent Parrondo games. Although actually much simpler, game fits into this framework with one-step transition matrix defined by (19) with

where is a small bias parameter. In game , it is typically assumed that, ignoring the bias parameter, the one-step transition matrix is defined by (19) with

These two constraints determine a two-parameter family of probabilities given by

(20)

We reparametrize the probabilities in terms of and (with ). Restoring the bias parameter, game has one-step transition matrix defined by (19) with

(21)

which includes (2) when and .

Finally, game is a mixture () of the two games, hence has one-step transition matrix , which also has the form (19).

We obtain, for game , and ; for game ,

and

and for game ,

and

By inspection, we deduce the following conclusion.

Theorem 4.

Let , , and , and

let games and be as above but with the bias parameter absent. If and , then whenever or , whenever or , and whenever or .

Assuming (21) with , the condition is equivalent to

whereas the condition is equivalent to

Again, the Parrondo effect is present if and only if .

Corollary 5.

Let games and be as above (with the bias parameter present).

If or , and if , then there exists , depending on , , and , such that Parrondo’s paradox holds for games , , and , that is, , , and , whenever .

When and , the mean and variance formulas simplify to

and, if as well,

Here, in contrast to the capital-dependent games, the variance of game is greater than that of game . This conclusion, however, is parameter dependent.

5 Nonrandom patterns of games

We also want to consider nonrandom patterns of games of the form , in which game is played times, then game is played times, where and are positive integers. Such a pattern is denoted in the literature by .

Associated with the games are one-step transition matrices for Markov chains in a finite state space , which we will denote by and , and a function . We assume that and are irreducible and aperiodic, as are , , …, , …, (the cyclic permutations of ). Let us denote the unique stationary distribution associated with by . The driving Markov chain is time-inhomogeneous, with one-step transition matrices ( times), ( times), ( times), ( times), and so on. Now define and by (3) and (4). What is the asymptotic behavior of as ?

Let us give distribution , at least for now. The time-inhomogeneous Markov chain is of course not stationary, so we define the (time-homogeneous) Markov chain by

(22)

and we note that this is a stationary Markov chain in a subset of . (The overlap between successive vectors is intentional.) We assume that it is irreducible and aperiodic in that subset, hence it is strongly mixing. Therefore,

is itself a stationary, strongly mixing sequence, and we can apply the stationary, strong mixing CLT to the sequence

(23)

We denote by and the mean and variance parameters for this sequence.

The mean and variance parameters and for the original sequence can be obtained from these. Indeed,

where ,

and

where

It remains to evaluate these variances and covariances.

First,

(24)

This formula for is equivalent to one found by Kay and Johnson (2003) in the history-dependent setting.

Next,

(25)

Furthermore,

Consider the factor in the first sum on the right, for example. With denoting the square matrix each of whose rows is , we can rewrite this as

Thus, summing over , we get

(26)

where is the fundamental matrix associated with . We conclude that

It follows that a pattern is losing, winning, or fair according to whether , , or .

Proof.

The proof is similar to that of Theorem 1, except that .

∎

In the examples to which we will be applying the above mean and variance formulas, additional simplifications will occur because has a particularly simple form and has a spectral representation. Denote by the matrix with th entry , and assume that has row sums equal to 0. Denote by the matrix with th entry , and define to be the vector of row sums of . Further, let and suppose that has eigenvalues and corresponding linearly independent right eigenvectors . Put and . Then the rows of are left eigenvectors and for all . Finally, with

we have for all . Additional notation includes for the unique stationary distribution of , and as before for the unique stationary distribution of . Notice that . Finally, we assume as well that whenever or .

A referee has suggested an alternative approach to the results of this section that has certain advantages. Instead of starting with a time-inhomogeneous Markov chain in , we begin with the (time-homogeneous) Markov chain in the product space with transition probabilities

It is irreducible and periodic with period .

Ordering the states of lexicographically, we can write the one-step transition matrix in block form as

where for and for . With as above, the unique stationary distribution for is , where and for . Using the idea in (5) and (5), we can deduce the strong mixing property and the central limit theorem. The mean and variance parameters are as in (9) but with bars on the matrices. Of course, , being the square matrix each of whose rows is ; is as but with and in place of and ; and similarly for .

The principal advantage of this approach is the simplicity of the formulas for the mean and variance parameters. Another advantage is that patterns other than those of the form can be treated just as easily. The only drawback is that, in the context of our two models, the matrices are no longer or but rather and .

In other words, the formulas (28)–(5), although lacking elegance, are more user-friendly.

6 Patterns of capital-dependent games

Let games and be as in Section 3; see especially (17). Both games are losing. In this section we show that, for every , and for every pair of positive integers and except for , the pattern , which stands for plays of game followed by plays of game , is winning for sufficiently small . Notice that it will suffice to treat the case .

We begin by finding a formula for , the asymptotic mean per game played of the player’s cumulative profit for the pattern , assuming . Recall that is given by (15) with , and is given by (15) with and , where . First, we can prove by induction that

where

(31)

Next, with , the nonunit eigenvalues of are

and we define the diagonal matrix .

The corresponding right eigenvectors

are linearly independent for all (including ),

so we define and .

Then

which leads to an explicit formula for , from which we can compute its unique stationary distribution as a left eigenvector corresponding to the eigenvalue 1. With

This formula will allow us to determine the sign of for all , , and .

Theorem 7.

Let games and be as in Theorem 2 (with the bias parameter absent). For every pair of positive integers and except , for all , for , and for all . In addition, for all .

The last assertion of the theorem was known to Pyke (2003). As before, the Parrondo effect appears (with the bias parameter present) if and only if . A reverse Parrondo effect, in which two winning games combine to lose, appears (with a negative bias parameter present) if and only if .

Corollary 8.

Let games and be as in Corollary 3 (with the bias parameter present).

For every , and for every pair of positive integers and except , there exists , depending on , , and , such that Parrondo’s paradox holds for games and and pattern , that is, , , and , whenever .

Proof of theorem.

Temporarily denote by to emphasize its dependence on . Then, given , the same argument that led to (18) yields

(35)

(This also follows from (34).)

It is therefore enough to treat the case . Notice that for all

and , hence for all integers . To show that it will suffice to show that , which is equivalent to showing that

(36)

is positive. We will show that, except when , (6) is positive for all integers .

First we consider the case in which and . Noting that , , and , (6) becomes

On the other hand, if , the left side of the last equation becomes

so .

Next we consider the case of and odd, . Since , we have and , where . Therefore, since is odd,

(37)

where the last identity uses the fact that, when is odd, the odd-numbered binomial coefficients are equal to the even-numbered ones , hence the sum of the odd-numbered ones is .

It follows that, since the case is excluded,

Consider next the case in which and is even. In this case, the last term in (6) is positive, and the remaining terms are greater than .

Next we treat the case separately. Our formula (34) gives

, which is positive since .

It remains to consider the case of and odd, . We must show that

Here the inequality of (37) is too crude. Again, we have and , where , so we can replace by . We can eliminate the term in the fraction, and we can replace the term by ; in the first case we are eliminating a positive contribution, and in the second case we are making a negative contribution more negative. Thus, it will suffice to prove that

for , or equivalently that

for . Now is a polynomial of degree with nonnegative coefficients, so is decreasing on with and . Further, for . Thus, our inequality holds for . It remains to confirm it for . On that interval we claim that

is decreasing, and it clearly approaches 5 as . Thus, it remains to show that for . We compute

as required.

∎

Here are four of the simplest cases:

We turn finally to the evaluation of the asymptotic variance per game played of the player’s cumulative profit. We denote this variance by , and we note that it suffices to assume that to obtain the formula up to .

A formula for analogous to (34) would be extremely complicated. We therefore consider the matrix formulas of Section 5 to be in final form.

Temporarily denote by to emphasize its dependence on . Then, given , the argument that led to (35) yields

For example, we have

As functions of , , , and are increasing, whereas is decreasing. All approach 1 as . Their limits as are respectively 0, 8/9, 25/48, and 621/500.

It should be explicitly noted that

(38)

for all . Since these identities may be counterintuitive, let us derive them in greater detail. We temporarily denote the stationary distributions and fundamental matrices of , , and , with subscripts , , and , respectively. Then

and

so

As for the variances, we recall that

and

But and

so it follows that

An interesting special case of (38) is the case . Technically, we have ruled out this case because we want our underlying Markov chain to be irreducible. Nevertheless, the games are well defined. Assuming , repeated play of game leads to the deterministic sequence

hence and . On the other hand, repeated play of pattern leads to the random sequence

where the number of initial pairs is the number of losses at game before the first win at game (in particular, is nonnegative geometric), and the terms signify independent random variables that are with probability each and independent of . Despite the randomness, the sequence is bounded, so we still have and .

When , the mean and variance formulas simplify to

Pyke (2003) obtained when , but that number is inconsistent with Ekhad and Zeilberger’s (2000) calculation, confirmed above, that .

7 Patterns of history-dependent games

Let games and be as in Section 4; see especially (21). Both games are losing. In this section we attempt to find conditions on and such that, for every pair of positive integers and , the pattern , which stands for plays of game followed by plays of game , is winning for sufficiently small . Notice that it will suffice to treat the case .

We begin by finding a formula for , the asymptotic mean per game played of the player’s cumulative profit for the pattern , assuming . Recall that is defined by (19) with , and is defined by (19) with , , and , where , , and . First, it is clear that for all , where is the matrix with all entries equal to 1/4.

As for the spectral representation of , its eigenvalues include 1 and the three roots of the cubic equation

, where

(41)

With the help of Cardano’s formula, we find that

the nonunit eigenvalues of are

where and are cube roots of unity, and

with

Of course, , , and are each less than 1 in absolute value.

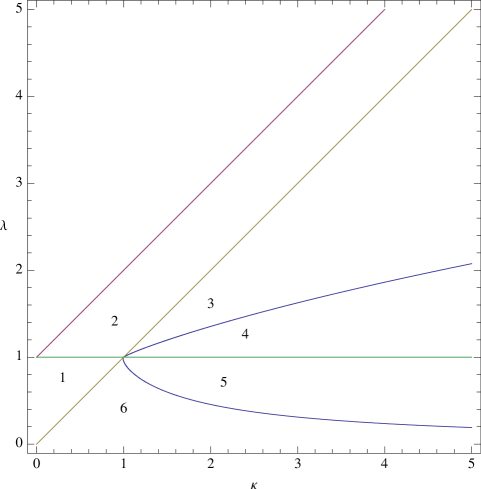

Notice that the definitions of and are slightly ambiguous, owing to the nonuniqueness of the cube roots. (If is replaced in the definitions of , , and by or by , then , , and are merely permuted.) If , then and can be taken to be real and distinct,333Caution should be exercised when evaluating numerically. Specifically, if , Mathematica returns a complex root for . If the real root is desired, one should enter .

This issue does not arise with and can be avoided with by redefining . in which case is real and and are complex conjugates; in particular, , , and are distinct. If , then and can be taken to be real and equal, in which case , , and are real with . If , then and can be taken to be complex conjugates, in which case , , and are real and distinct; in fact, they can be written

where , which implies that . See Figure 1.

Figure 1: The parameter space , restricted to and . In regions 1, 2, 3, and 6, ( is real, and are complex conjugates); in regions 4 and 5, (, , and are real). If the conjecture stated below is correct, then, in regions 1, 3, and 4, for all ; in regions 2, 5, and 6, for all .

If we define the vector-valued function by

then

are corresponding right eigenvectors, and they are linearly independent if and only if the eigenvalues are distinct. If the eigenvalues are distinct, we define and .

Thus, (43) and (45) provide explicit, albeit complicated, formulas for for all . They are valid provided only that (ensuring that has distinct eigenvalues) and (ensuring that the denominators of the formulas are nonzero).

We can extend the formulas to by noting that, in this case, 0 is an eigenvalue of and the two remaining nonunit eigenvalues, which can be obtained from the quadratic formula, are distinct from 0 and 1 unless . Here we are using the assumption that , hence . This allows a spectral representation in such cases and again leads to formulas for for all , which we do not include here. Writing the numerator of temporarily as , notice that the two nonunit, nonzero eigenvalues coincide, when , with the roots of , and this ordered pair of eigenvalues is also a zero of . This explains why the singularity on the curve is removable.

We cannot prove the analogue of Theorem 7 in this setting, so we state it as a conjecture.

Conjecture.

Let games and be as in Theorem 4 (with the bias parameter absent). For every pair of positive integers and , if or , if or , and if or .

Corollary 9.

Assume that the conjecture is true for some pair satisfying or .

Let games and be as in Corollary 5 (with the bias parameter present).

For every pair of positive integers and , there exists , depending on , , , and , such that Parrondo’s paradox holds for games , , and pattern , that is, , , and , whenever .

We can prove a very small part of the conjecture. Let be the set of positive fractions with one-digit numerators and denominators, that is, , and note that has 55 distinct elements.

Theorem 10.

The conjecture is true if (a) , (b) and , or (c) , , , , , and .

Remark.

Parts (a) and (b) are the fair cases. Part (c) treats 2123 unfair cases (702 winning, 1421 losing), including the case and studied by Parrondo, Harmer, and Abbott (2000). (The assumption that is redundant.) The proof of part (c) is computer assisted.

Proof.

We begin with case (a), . In this case , hence , while

hence . We conclude that for all in this case. The argument fails only when because, assuming that , only then is or is . But in that case game is indistinguishable from game , so again for all .

Next we consider case (b), and either or . We write the numerator of temporarily as .

Each nonunit eigenvalue of is a root of the cubic equation

with coefficients (41). With , this equation, multiplied by , becomes

Moreover, we have .

If , then (the eigenvalues are distinct with and complex conjugates). In this case, has complex roots, so and ; in addition, and , being roots of , have sum and product , hence . Therefore, and .

Finally, has as a factor and , hence .

On the other hand, if , then (the eigenvalues are real and distinct). In this case, two of the three eigenvalues , , and are roots of , so the argument just given in the case applies in this case as well with the two mentioned eigenvalues replacing and .

We turn to case (c), but let us begin by treating the general case. Given and with , , and , we clearly have . The conjecture says that and have the same sign as for all .

We assume in addition that and .

If , then we can take real and and complex conjugates. It follows that is real and and are complex conjugates. Similarly, is real and and are complex conjugates. Therefore,

If , then , , and are real and distinct, as we have seen, and therefore are real. In either case, has the same sign as if

(46)

is positive.

Notice that (46) increases in and is positive for large enough. Given with , , and , there exists , depending on , such that (46) is positive for all . It is then enough to verify by direct computation that has the same sign as for . In fact, we believe, but cannot prove, that is never larger than 3. If true, this would imply that the conjecture holds for and . (We are using the observations that is continuous in and that the set of such that and is dense. We are also implicitly using the fact, not yet proved, that on the curves and , except at .)

The case is more complicated. Observe that has the same sign as if

(47)

is positive, a stronger condition than requiring that (46) be positive. Notice that (7) increases in and is positive for large enough. Given , again with , , and , there exists , depending on , such that (7) holds for all . It is then enough to verify by direct computation that has the same sign as for . It appears that can be quite large.

We have carried out the required estimates in Mathematica for the 2123 cases of part (c). There were no exceptions to the conjecture. Table 1 lists a few of these cases.

∎

Table 1: A few of the 2123 cases treated by Theorem 10(c).

is the smallest positive integer that makes (46) positive.

is the smallest positive integer that makes (7) positive.

region

of Fig. 1

1

1

2

6

1

6

3

1

3

1

1

6

1

2

3

6

1

27

2

1

3

4

1

1

5

1

2

Here are four of the simplest cases:

Notice that the final factor in the numerator and the final factor in the denominator of are both positive. (Consider two cases, and .) The same is true of , .

We turn finally to the evaluation of the asymptotic variance per game played of the player’s cumulative profit. We denote this variance by , and we note that it suffices to assume that in the calculation to obtain the formula up to .

A formula for analogous to (43) and (45) would be extremely complicated. We therefore consider the matrix formulas of Section 5 to be in final form.

For example, we have

for . The formula for is omitted above; is the ratio of two polynomials in and of degree 16, the numerator having 110 terms.

When and , the mean and variance formulas simplify to

8 Why does Parrondo’s paradox hold?

Several authors (e.g., Ekhad and Zeilberger 2000, Rahmann 2002, Philips and Feldman 2004) have questioned whether Parrondo’s paradox should be called a paradox. Ultimately, this depends on one’s definition of the word “paradox,” but conventional usage (e.g., the St. Petersburg paradox, Bertrand’s paradox, Simpson’s paradox, and the waiting-time paradox) requires not that it be unexplainable, only that it be surprising or counterintuitive. Parrondo’s paradox would seem to meet this criterion.

A more important issue, addressed by various authors, is, Why does Parrondo’s paradox hold? Here we should distinguish between the random mixture version and the nonrandom pattern version of the paradox. The former is easy to understand, based on an observation of Moraal (2000), subsequently elaborated by Costa, Fackrell, and Taylor (2005). See also Behrends (2002). Consider the capital-dependent games first. The mapping from into the unit square defines a curve representing the fair games, with the losing games below and the winning games above. The interior of the line segment from to lies in the winning region if (i.e., ) and in the losing region if (i.e., ), as can be seen by plotting the curve (as in, e.g., Harmer and Abbott 2002). These line segments correspond to the random mixtures of game and game . Actually, it is not necessary to plot the curve. Using (16), we note that the curve defined by is simply the graph of (), and by calculating we can check that is strictly convex on and strictly concave on .

The same kind of reasoning applies to the history-dependent games, except that now the mapping from into the unit cube defines a surface representing the fair games, with the losing games below and the winning games above. The interior of the line segment from to lies in the winning region if (i.e., and ) or (i.e., and ). It is possible but difficult to see this by plotting the surface on a computer screen using 3D graphics. Instead, we note using (20) that the surface defined by is simply the graph of (, , ).

So with for , we compute

and observe that for if and only if both and , or both and . In other words, restricted to the line segment from to is strictly convex under these conditions. This confirms the stated assertion.

The explanations for the nonrandom pattern version of the paradox are less satisfactory. Ekhad and Zeilberger (2000) argued that it is because “matrices (usually) do not commute.” The “Boston interpretation” of H. Eugene Stanley’s group at Boston University claims that it is due to noise. As Kay and Johnson (2003) put it, “losing cycles in game B are effectively broken up by the memoryless behavior, or ‘noise’, of game A.” Let us look at this in more detail.

We borrow some assumptions and notation from the end of Section 5. Assume that . Denote by the matrix with th entry , and assume that has row sums equal to 0. Denote by the matrix with th entry , and define to be the vector of row sums of . Let be the unique stationary distribution of , and let be the unique stationary distribution of . Then the asymptotic mean per game played of the player’s cumulative profit for the pattern when is

If it were the case that , then we would have

and the Parrondo effect would not appear. If we attribute the fact that

is not equal to to the “noise” caused by game , then we can justify the Boston interpretation.

The reason this explanation is less satisfactory is that it gives no clue as to the sign of , which indicates whether the pattern is winning or losing. We propose an alternative explanation (the Utah interpretation?) that tends to support the Boston interpretation. To motivate it, we observe that can be interpreted as the asymptotic mean per cycle of plays of game and plays of game of the player’s cumulative profit when . If is large relative to , then the plays of game might reasonably be interpreted as periodic noise in an otherwise uninterrupted sequence of plays of game . We will show that

exists and is finite for every . If the limit is positive for some , then for that and all sufficiently large. If the limit is negative for some , then for that and all sufficiently large. These conclusions are weaker than those of Theorem 7 and the conjecture but the derivation is much simpler, depending only on the fundamental matrix of , not on its spectral representation.

Here is the derivation. First, , where is the unique stationary distribution of . Now

where is the square matrix each of whose rows is . We conclude that as and therefore that

where denotes the fundamental matrix of (see (7)). Since and , it is the factor, or the “noise” caused by game , that leads to a (typically) nonzero limit.

In the capital-dependent setting we can evaluate this limit as

where is as in (31), while in the history-dependent setting it becomes

Of course we could derive these limits from the formulas in Sections 6 and 7, but the point is that they do not require the spectral representation of —they are simpler than that. They also explain why the conditions on are the same in Theorems 2 and 7, and the conditions on and are the same in Theorem 4 and the conjecture.

Acknowledgments

The research for this paper was carried out during J. Lee’s visit to the Department of Mathematics at the University of Utah in 2008–2009. The authors are grateful to the referees for valuable suggestions.

References

Abbott, Derek (2009) Developments in Parrondo’s paradox. In: In, V., Longhini, P., and Palacios, A. (eds.) Applications of Nonlinear Dynamics: Model and Design of Complex Systems. Series: Understanding Complex Systems. Springer-Verlag, Berlin, 307–321.

Ajdari, A. and Prost, J. (1992) Drift induced by a spatially periodic potential of low symmetry: Pulsed dielectrophoresis. Comptes Rendus de l’Académie des Sciences, Série 2315 (13) 1635–1639.

Berresford, Geoffrey C. and Rockett, Andrew M. (2003) Parrondo’s paradox. Int. J. Math. Math. Sci.2003 (62) 3957–3962. MR2036089 (2004j:91068).

Billingsley, Patrick (1995) Probability and Measure, third edition. John Wiley & Sons Inc., New York.

MR1324786 (95k:60001).

Bradley, Richard C. (2007) Introduction to Strong Mixing Conditions, Volume 1. Kendrick Press, Heber City, UT.

MR2325294 (2009f:60002a).

Cleuren, B. and Van den Broeck, C. (2004) Primary Parrondo paradox. Europhys. Lett.67 (2) 151–157.

Costa, Andre, Fackrell, Mark, and Taylor, Peter G. (2005) Two issues surrounding Parrondo’s paradox. In: Nowak, A. S. and Szajowski, K. (eds.) Advances in Dynamic Games: Applications to Economics, Finance, Optimization, and Stochastic Control, Annals of the International Society of Dynamic Games 7, Birkhäuser, Boston, 599–609. MR2104716 (2005h:91066).

Durrett, Richard (1996) Probability: Theory and Examples, second edition. Duxbury Press, Belmont, CA. MR1609153 (98m:60001).

Ekhad, Shalosh B. and Zeilberger, Doron (2000) Remarks on the Parrondo paradox. The Personal Journal of Shalosh B. Ekhad and Doron Zeilberger. http://www.math.rutgers.edu/~zeilberg/pj.html

Epstein, Richard A. (2007) Parrondo’s principle: An overview. In: Ethier, S. N. and Eadington, W. R. (eds.) Optimal Play: Mathematical Studies of Games and Gambling. Institute for the Study of Gambling and Commercial Gaming, University of Nevada, Reno, 471–492.

Harmer, Gregory P. and Abbott, Derek (2002) A review of Parrondo’s paradox. Fluct. Noise Lett.2 (2) R71–R107.

Kay, Roland J. and Johnson, Neil F. (2003) Winning combinations of history-dependent games. Phys. Rev. E67 (5) 056128. arXiv:cond-mat/0207386.

Kemeny, John G. and Snell, J. Laurie (1960) Finite Markov Chains. D. Van Nostrand Company, Inc., Princeton, NJ.

MR0115196 (22 #5998).

Key, Eric S., Kłosek, Małgorzata M., and Abbott, Derek (2006) On Parrondo’s paradox: How to construct unfair games by composing fair games. ANZIAM J.47 (4) 495–511. MR2234017. arXiv:math/0206151.

Moraal, Hendrik (2000) Counterintuitive behaviour in games based on spin models. J. Phys. A: Math. Gen.33 L203–L206.

MR1778614 (2001d:91049).

Parrondo, Juan M. R. (1996) Efficiency of Brownian motors. Presented at the Workshop of the EEC HC&M Network on Complexity and Chaos, Institute for Scientific Interchange Foundation, Torino, Italy.

Parrondo, Juan M. R., Harmer, Gregory P., and Abbott, Derek (2000) New paradoxical games based on Brownian ratchets. Phys. Rev. Lett.85 (24) 5226–5229. arXiv:cond-mat/0003386.

Parrondo, J. M. R. and Dinís, Luis (2004) Brownian motion and gambling: From ratchets to paradoxical games. Contemp. Phys.45 (2) 147–157.

Percus, Ora E. and Percus, Jerome K. (2002) Can two wrongs make a right? Coin-tossing games and Parrondo’s paradox. Math. Intelligencer24 (3) 68–72. MR1927042 (2003f:91025).

Philips, Thomas K. and Feldman, Andrew B. (2004) Parrondo’s paradox is not paradoxical. Social Sciences Research Network. http://ssrn.com/abstract=581521

Pyke, Ronald (2003) On random walks and diffusions related to Parrondo’s games. In: Moore, M., Froda, S., and Léger, C. (eds.) Mathematical Statistics and Applications: Festschrift for Constance Van Eeden. Institute of Mathematical Statistics, Lecture Notes–Monograph Series 42, Beachwood, OH, 185–216. MR2138293 (2006e:60062). arXiv:math/0206150.