Affine Diffusion Processes: Theory and Applications

Abstract

We revisit affine diffusion processes on general and on the canonical state space in particular. A detailed study of theoretic and applied aspects of this class of Markov processes is given. In particular, we derive admissibility conditions and provide a full proof of existence and uniqueness through stochastic invariance of the canonical state space. Existence of exponential moments and the full range of validity of the affine transform formula are established. This is applied to the pricing of bond and stock options, which is illustrated for the Vasiček, Cox–Ingersoll–Ross and Heston models.

1 Introduction

Affine Markov models have been employed in finance since decades, and they have found growing interest due to their computational tractability as well as their capability to capture empirical evidence from financial time series. Their main applications lie in the theory of term structure of interest rates, stochastic volatility option pricing and the modeling of credit risk (see [12] and the references therein). There is a vast literature on affine models. We mention here explicitly just the few articles [2, 4, 8, 10, 13, 14, 16, 20, 26, 27, 29] and [12] for a broader overview.

In this paper, we revisit the class of affine diffusion processes on subsets of and on the canonical state space , in particular. In Section 2, we first provide necessary and sufficient conditions on the parameters of a diffusion process to satisfy the affine transform formula

The functions and in turn are given as solutions of a system of coupled Riccati equations. Arguing by stochastic invariance, in Section 3, we can further restrict the choice of admissible diffusion parameters.

Glasserman and Kim [16] showed recently that the affine transform formula holds whenever either side is well defined under the assumption of strict mean reversion. This is an extension of the findings in [12], where only sufficient conditions are given in terms of analyticity of the right hand side. The strict mean reversion assumption, however, excludes the Heston stochastic volatility model. In our paper, we show that strict mean reversion is not needed (Theorem 3.3). As a by product, we obtain some non-trivial convexity results for Riccati equations. Having the full range of validity of the above transform formula under control, in Section 4, we can then proceed to pricing bond and stock options in affine models. Particular examples are the Vasiček and Cox–Ingersoll–Ross (CIR) short rate models in Section 5, and Heston’s stochastic volatility model in Section 6.

The representation of affine short rate models bears some ambiguity with respect to linear transformations of the state process. This motivates the question whether there exists a classification method ensuring that affine short rate models with the same observable implications have a unique canonical representation. This topic has been addressed in [10, 9, 24, 8]. In Section 7, we recap this issue and show that the diffusion matrix of can always be brought into block-diagonal form by a regular linear transform leaving the canonical state space invariant.

The existence and uniqueness question of the relevant stochastic differential equation is completely solved through stochastic invariance and the block-diagonal transformation in Section 8. The presented proof builds on the seminal result by Yamada and Watanabe [35]. We therefore approach the existence issue differently from [12] which uses infinite divisibility on the canonical state space and the Markov semigroup theory.

2 Definition and Characterization of Affine Processes

Fix a dimension and a closed state space with non-empty interior. We let be continuous, and be measurable and such that the diffusion matrix

is continuous in . Let denote a -dimensional Brownian motion defined on a filtered probability space . Throughout, we assume that for every there exists a unique solution of the stochastic differential equation

| (2.1) |

Definition 2.1.

We call affine if the -conditional characteristic function of is exponential affine in , for all . That is, there exist - and -valued functions and , respectively, with jointly continuous -derivatives such that satisfies

| (2.2) |

for all , and .

Since the conditional characteristic function is bounded by one, the real part of the exponent in (2.2) has to be negative. Note that and for and are uniquely222In fact, may be altered by multiples of . We uniquely fix the continuous function by the initial condition . determined by (2.2), and satisfy the initial conditions and , in particular.

We first derive necessary and sufficient conditions for to be affine.

Theorem 2.2.

Suppose is affine. Then the diffusion matrix and drift are affine in . That is,

| (2.3) | ||||

for some -matrices and , and -vectors and , where we denote by

the -matrix with -th column vector , . Moreover, and solve the system of Riccati equations

| (2.4) | ||||

In particular, is determined by via simple integration:

Proof.

Suppose is affine. For and define the complex-valued Itô process

We can apply Itô’s formula, separately to real and imaginary part of , and obtain

with

Since is a martingale, we have for all a.s. Letting , by continuity of the parameters, we thus obtain

for all , , . Since , this implies that and are affine of the form (2.3). Plugging this back into the above equation and separating first order terms in yields (2.4).

Conversely, suppose and are of the form (2.3). Let be a solution of the Riccati equations (2.4) such that has negative real part for all , and . Then , defined as above, is a uniformly bounded local martingale, and hence a martingale, with . Therefore , for all , which is (2.2), and the theorem is proved. ∎

We now recall an important global existence, uniqueness and regularity result for the above Riccati equations. We let be a placeholder for either or .

Lemma 2.3.

Let and be real -matrices, and and be real -vectors, .

-

(i)

For every , there exists some such that there exists a unique solution of the Riccati equations (2.4). In particular, .

-

(ii)

The domain

is open in and maximal in the sense that for all either or , respectively, .

-

(iii)

For every , the -section

is an open neighborhood of in . Moreover, and for .

-

(iv)

and are analytic functions on .

-

(v)

.

Henceforth, we shall call the maximal domain for equation (2.4).

Proof.

Since the right-hand side of (2.4) is formed by analytic functions in on , part (i) follows from the basic theorems for ordinary differential equations, e.g. [1, Theorem 7.4]. In particular, since is the unique solution of (2.4) for . It is proved in [1, Theorems 7.6 and 8.3] that is maximal and open, which is part (ii). This also implies that all -sections are open in . The inclusion is a consequence of the maximality property from part (ii). Whence part (iii) follows. For a proof of part (iv) see [11, Theorem 10.8.2]. Part (v) is obvious. ∎

3 Canonical State Space

There is an implicit trade off between the parameters in (2.3) and the state space :

-

•

must be such that does not leave the set , and

-

•

must be such that is symmetric and positive semi-definite for all .

To gain further explicit insight into this interplay, we now and henceforth assume that the state space is of the following canonical form

for some integers with .

Remark 3.1.

This canonical state space covers most applications appearing in the finance literature. However, other choices for the state space of an affine process are possible:

-

(i)

For instance, the following example for admits as state space any closed interval containing 0:

This degenerate diffusion process is affine, since for all ([12], Section 12). In general, affine diffusion processes on compact state spaces have to be degenerate.

- (ii)

- (iii)

For the above canonical state space, we can give necessary and sufficient admissibility conditions on the parameters. The following terminology will be useful in the sequel. We define the index sets

For any vector and matrix , and index sets , we denote by

the respective sub-vector and -matrix.

Theorem 3.2.

The process on the canonical state space is affine if and only if and are affine of the form (2.3) for parameters which are admissible in the following sense:

| are symmetric positive semi-definite, | (3.1) | |||

| has positive off-diagonal elements. |

In this case, the corresponding system of Riccati equations (2.4) simplifies to

| (3.2) | ||||

and there exists a unique global solution for all initial values . In particular, the equation for forms an autonomous linear system with unique global solution for all .

Before we prove the theorem, let us illustrate the admissibility conditions (3.1) for the diffusion matrix for dimension and the corresponding cases . Note that , hence in the case we have

for an arbitrary positive semi-definite symmetric -matrix . For , we have

for ,

and for ,

where we leave the lower triangle of symmetric matrices blank, denotes a non-negative real number and any real number such that positive semi-definiteness holds.

Proof of Theorem 3.2.

Suppose is affine. That and are of the form (2.3) follows from Theorem 2.2. Obviously, is symmetric positive semi-definite for all if and only if for all , and and are symmetric positive semi-definite for all .

We extend the diffusion matrix and drift continuously to by setting

Now let be a boundary point of . That is, for some . The stochastic invariance Lemma B.1 below implies that the diffusion must be “parallel to the boundary”,

and the drift must be “inward pointing”,

Since this has to hold for all , , and , , we obtain the following set of admissibility conditions

| are symmetric positive semi-definite, | |||

which is equivalent to (3.1). The form of the system (3.2) follows by inspection.

Now suppose satisfy the admissibility conditions (3.1). We show below that there exists a unique global solution of (3.2), for all . In particular, has negative real part for all , and . Thus the first part of the theorem follows from Theorem 2.2.

As for the global existence and uniqueness statement, in view of Lemma 2.3, it remains to show that is -valued and for all . For , denote the right-hand side of the equation for by

and observe that

Let us denote . Since , it follows from the admissibility conditions (3.1) and Corollary B.2 below, setting ,

and for , that the solution of (3.2) has to take values in for all initial points .

Further, for and , one verifies that

for some finite constant which does not depend on . We thus obtain

for

Gronwall’s inequality ([11, (10.5.1.3)]), applied to , yields

| (3.3) |

From above, for all initial points , we know that and therefore by (3.3). Hence the theorem is proved. ∎

Now suppose is affine with characteristics (2.3) satisfying the admissibility conditions (3.1). In what follows we show that not only can the functions and be extended beyond , but also the validity of the affine transform formula (2.2) carries over. This asserts exponential moments of in particular and will prove most useful for deriving pricing formulas in affine factor models.

For any set (), we define the strip

in . The proof of the following theorem builds on results that are derived in Sections A and B below.

Theorem 3.3.

Suppose is affine with admissible parameters as given in (3.1). Let . Then

-

(i)

-

(ii)

where

-

(iii)

and are convex sets.

Proof.

We first claim that, for every with , there exists some and some sequence such that

| (3.4) |

Indeed, otherwise we would have . But then (3.3) would imply , which is absurd. Whence (3.4) is proved.

In the following, we write

Since is affine, by definition we have and (2.2) implies

| (3.5) |

for all , and . Moreover, by Lemma B.5 , is open and star-shaped around in . Hence Lemma A.3 implies that and (3.5) holds for all , for all and .

Now let and , and define

We claim that . Arguing by contradiction, assume that . Since is open, this implies , and thus

| (3.6) |

On the other hand, since is open, for some . Hence (3.5) holds and is uniformly bounded in , by continuity of and in . We infer that the class of random variables is uniformly integrable, see [34, 13.3]. Since is continuous in , we conclude by Lebesgue’s convergence theorem that is continuous in , for all . But for all we have , and thus (3.5) holds for all . In view of (3.4), this contradicts (3.6). Whence and thus . This proves (i)333For an alternative proof of the above, see remark B.7.

Applying the above arguments to444Here we use the Markov property of , see [25, Theorem 5.4.20]. with yields (iv). Part (v) follows, since, by Theorem 3.2, for all .

As for (ii), we first let . From part (iv) it follows that . Conversely, let , and define . We have to show that . Assume, by contradiction, that . From Lemma B.5 , we know that there exists some such that

| (3.7) |

On the other hand, from part (iv) and Jensen’s inequality, we obtain

for all . But this contradicts (3.7), hence , and part (ii) is proved. Since is convex, this also implies (iii). Finally, part (vi) follows from part (ii) and Lemma 2.3. Whence the theorem is proved. ∎

Remark 3.4.

Glasserman and Kim [16] proved the equality in Theorem 3.3 (ii), and the validity of the transform formula (2.2) for all in an open neighborhood of in , under the additional assumption that has strictly negative eigenvalues. That assumption, however, excludes the simple Heston stochastic volatility model in Section 6 below.

Remark 3.5.

4 Discounting and Pricing in Affine Models

We let be affine on the canonical state space with admissible parameters as given in (3.1). Since we are interested in pricing, and to avoid a change of measure, we interpret as risk-neutral measure in what follows.

A short rate model of the form

| (4.1) |

for some constant parameters and , is called an affine short rate model. Special cases, for dimension , are the Vasiček and Cox–Ingersoll–Ross short rate models. We recall that an affine term structure model always induces an affine short rate model.

Now consider a -claim with payoff . Here denotes a measurable payoff function, such that meets the required integrability conditions

Its arbitrage price at time is then given by

| (4.2) |

A particular example is the -bond with . Our aim is to derive an analytic, or at least numerically tractable, pricing formula for (4.2). To this end we shall make use of a change of numeraire technique to price, e.g., Bond options and caplets. Denote the risk free bank account by . For fixed it is easily observed that

hence we may introduce an equivalent probability measure on by its Radon-Nikodym derivative

is called the -forward measure. Note that for ,

| (4.3) |

As a first step towards establishing useful pricing formulas, we derive a formula for the -conditional characteristic function of under , which up to normalization with equals,

| (4.4) |

(use equation (4.3).

Note that the following integrability condition (i) is satisfied in particular if is uniformly bounded from below, that is, if .

Theorem 4.1.

Let . The following statements are equivalent:

-

(i)

for all .

-

(ii)

There exists a unique solution of

(4.5) for .

Proof.

We first enlarge the state space and consider the real-valued process

A moment’s reflection reveals that is an -valued diffusion process with diffusion matrix and drift where

form admissible parameters. We claim that is an affine process.

Indeed, the candidate system of Riccati equations reads

| (4.7) | ||||

Here we replaced the constant solution by in the boxes. Theorem 3.2 carries over and asserts a unique global -valued solution of (4.5) for all . The second part of Theorem 2.2 thus asserts that is affine with conditional characteristic function

for all and .

The theorem now follows from Theorem 3.3 once we set and . ∎

Suppose, for the rest of this section, that either condition (i) or (ii) of Theorem 4.1 is met. As immediate consequence of Theorem 4.1, we obtain the following explicit price formulas for -bonds in terms of and .

Corollary 4.2.

For any maturity , the -bond price at is given as

where we denote

Moreover, for , the -conditional characteristic function of under the -forward measure is given by

| (4.8) |

for all , where is the neighborhood of in from Theorem 4.1.

Proof.

The bond price formula follows from (4.6) with .

For more general payoff functions , we can proceed as follows.

-

•

Either we recognize the -conditional distribution, say , of under the -forward measure from its characteristic function (4.8). Or we derive via numerical inversion of the characteristic function (4.8), using e.g. fast Fourier transform (FFT). Then compute the price (4.2) by integration of

(4.9) Examples are given in Section 5 below.

-

•

Or suppose can be expressed by

(4.10) for some integrable function and some constant . Then we may apply Fubini’s theorem to change the order of integration, which gives

(4.11) This integral can be numerically computed. An example is given in Section 6 below.

The function in (4.10) can be found by Fourier transformation, as the following classical result indicates.

Lemma 4.3.

Let be a measurable function and be such that the function and its Fourier transform

are integrable on . Then (4.10) holds for almost all for

Proof.

From Fourier analysis, see [33, Chapter I, Corollary 1.21], we know that

for almost all . Multiplying both sides with yields the first claim.

An example is the continuous payoff function

of a European call option with strike price on the underlying stock price , where may be any affine function of . Fix a real constant . Then is integrable on . An easy calculation shows that its Fourier transform

is also integrable on . In view of Lemma 4.3, we thus conclude that, for ,

| (4.12) |

which is of the desired form (4.10). We will apply this for the Heston stochastic volatility model in Section 6 below.

A related example is the following

| (4.13) |

which holds for all .

More examples of payoff functions with integral representation, including the above, can be found in [21].

5 Bond Option Pricing in Affine Models

We can further simplify formula (4.9) for a European call option on a -bond with expiry date and strike price . The payoff function is

We can decompose (4.2),

| (5.1) |

for the event . The pricing of this bond option boils down to the computation of the probability of the event under the - and -forward measures.

Similarly, the value of a put equals

| (5.2) |

for the event .

In the following two subsections, we illustrate this approach for the Vasiček and Cox–Ingersoll–Ross short rate models.

5.1 Example: Vasiček Short Rate Model

The state space is , and we set for the Vasiček short rate model

The system (4.5) reads

which admits a unique global solution with

for all . Hence (4.6) holds for all and . In particular, by Corollary 4.2, the bond prices can be determined by and ,

Hence, under the -forward measure, is -conditionally Gaussian distributed with (cf. [3], chapter 3.2.1)

where is defined by

The bond option price formula for the Vasiček short rate model can now be derived via (5.1) and (5.2).

5.2 Example: Cox–Ingersoll–Ross Short Rate Model

The state space is , and we set for the Cox–Ingersoll–Ross short rate model

The system (4.5) reads

| (5.3) | ||||

By Lemma 5.2 below, there exists a unique solution , and thus (4.6) holds, for all and . The solution is given explicitly as

where and

Some tedious but elementary algebraic manipulations show that the -conditional characteristic function of under the -forward measure is given by

where

Comparing this with Lemma 5.1 below, we conclude that the -conditional distribution of the random variable under the -forward measure is noncentral with degrees of freedom and parameter of noncentrality . Combining this with (5.1)–(5.2), we obtain explicit European bond option price formulas.

As an application, we now compute cap prices. Let us consider a cap with strike rate and tenor structure , with . Here, as usual, denote the settlement dates and the reset dates for the th caplet, and is the maturity of the cap. It is well known that the cash flow of a th caplet at time equals the multiple of the cash-flow at of a put option on the -bond with strike price . Hence the cap price equals

In practice, cap prices are often quoted in Black implied volatilities. By definition, the implied volatility is the number, which, plugged into Black’s formula, yields the cap value , where the th caplet price is given as

with

where denotes the corresponding simple forward rate.

As parameters for the CIR model we assume

In Table 1 we summarize the ATM555The cap with maturity is at-the-money (ATM) if its strike rate equals the prevailing forward swap rate . cap prices and implied volatilities for various maturities.

| Maturity Years | strike rate | cap price | implied volatility |

|---|---|---|---|

| 1 | 0.0843 | 0.0073 | 0.4506 |

| 2 | 0.0855 | 0.0190 | 0.3720 |

| 3 | 0.0862 | 0.0302 | 0.3226 |

| 4 | 0.0866 | 0.0406 | 0.2890 |

| 5 | 0.0868 | 0.0501 | 0.2647 |

| 6 | 0.0870 | 0.0588 | 0.2462 |

| 7 | 0.0871 | 0.0668 | 0.2316 |

| 8 | 0.0872 | 0.0742 | 0.2198 |

| 9 | 0.0873 | 0.0809 | 0.2100 |

| 10 | 0.0873 | 0.0871 | 0.2017 |

| 15 | 0.0875 | 0.1110 | 0.1744 |

| 20 | 0.0876 | 0.1265 | 0.1594 |

| 25 | 0.0876 | 0.1365 | 0.1502 |

| 30 | 0.0876 | 0.1430 | 0.1442 |

Lemma 5.1 (Noncentral -Distribution).

The noncentral -distribution with degrees of freedom and noncentrality parameter has density function

and characteristic function

Here denotes the modified Bessel function of the first kind of order .

Proof.

See e.g. [23]. ∎

Lemma 5.2.

Consider the Riccati differential equation

| (5.4) |

where and , with and . Let denote the analytic extension of the real square root to , and define .

-

(i)

The function

(5.5) is the unique solution of equation (5.4) on its maximal interval of existence . Moreover,

(5.6) -

(ii)

If, moreover, , , and then and is -valued.

Proof.

(i): Recall that the square root is the well defined analytic extension of the real square root to , through the main branch of the logarithm which can be written in the form . Hence we may write (5.4) as

where , and it follows that

which can be seen to be equivalent to (5.5). As , numerator and denominator cannot vanish at the same time , and certainly not for near zero. Hence, by the maximality of , (5.5) is the solution of (5.4) for . Finally, the integral (5.6) is checked by differentiation.

(ii): We show along the lines of the proof of Theorem 3.2, that for this choice of coefficients global solutions exist for initial data and stay in . To this end, write , then

and since we have that for all times , see Corollary B.2 below. Furthermore, we see that , hence . This implies, by Gronwall’s inequality ([11, (10.5.1.3)]), that . Hence the lemma is proved. ∎

6 Heston Stochastic Volatility Model

This affine model, proposed by Heston [20], generalizes the Black–Scholes model by assuming a stochastic volatility.

Interest rates are assumed to be constant , and there is one risky asset (stock) , where is the affine process with state space and dynamics

for some constant parameters , , and some . In view of Remark 3.4, we note that here

is singular, and hence cannot have strictly negative eigenvalues.

The implied risk-neutral stock dynamics read

for the Brownian motion . We see that is the stochastic volatility of the price process . They have possibly non-zero covariation

The corresponding system of Riccati equations (3.2) is equivalent to

| (6.1) | ||||

which, in view of Lemma 5.2 (ii) admits an explicit global solution if and . In particular, for and by setting , the solution can be given explicitly as

| (6.2) | ||||

Furthermore, for , we obtain

Theorem 3.3 thus implies that has finite first moment, for any , and

for , which is just the martingale property of .

We now want to compute the price

of a European call option on with maturity and strike price . Fix some small enough with . Formula (4.12) combined with (4.11) then yields

| (6.3) |

Alternatively, we may fix any and then, combining (4.13) with (4.11),

| (6.4) |

Since we have explicit expressions (6.2) for and , we only need to compute the integral with respect to in (6.3) or (6.4) numerically. We have carried out numeric experiments for European option prices using MATLAB. Fastest results were achieved for values by using (6.4) whereas keeping a constant error level the runtime explodes at , which is due to the singularities of the integrand. Also, an evaluation of residua

for suggests that (6.4) is numerically more stable than (6.3).

Next, we present implied volatilities obtained by (6.4) setting . As initial data for and model parameters, we chose

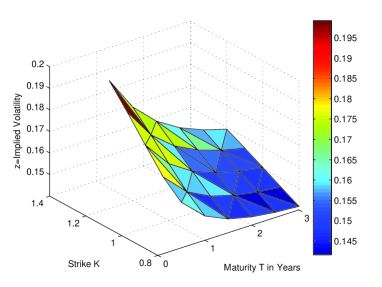

Table 2 shows implied volatilities from call option prices at for various strikes and maturities , computed with (6.4) for . These values are in well accordance with MC simulations (mesh size , number of sample paths ). The corresponding implied volatility surface is shown in Figure 1.

| T-K | 0.8000 | 0.9000 | 1.0000 | 1.1000 | 1.2000 |

|---|---|---|---|---|---|

| 0.5000 | 0.1611 | 0.1682 | 0.1785 | 0.1892 | 0.1992 |

| 1.0000 | 0.1513 | 0.1579 | 0.1664 | 0.1751 | 0.1835 |

| 1.5000 | 0.1464 | 0.1524 | 0.1594 | 0.1665 | 0.1734 |

| 2.0000 | 0.1438 | 0.1492 | 0.1551 | 0.1611 | 0.1668 |

| 2.5000 | 0.1424 | 0.1473 | 0.1524 | 0.1574 | 0.1623 |

| 3.0000 | 0.1417 | 0.1460 | 0.1505 | 0.1549 | 0.1591 |

Remark 6.1.

We note that the Heston model is often written in the equivalent form

To see the relation of the parameters of this form and the one used in this section, we simply set , and then get

from which we read off

and all other parameters coincide.

7 Affine Transformations and Canonical Representation

As above, we let be affine on the canonical state space with admissible parameters . Hence, in view of (2.1), for any the process satisfies

| (7.1) | ||||

and .

It can easily be checked that for every invertible -matrix , the linear transform

satisfies

| (7.2) |

Hence, has again an affine drift and diffusion matrix

| (7.3) |

respectively.

On the other hand, the affine short rate model (4.1) can be expressed in terms of as

| (7.4) |

This shows that and (7.4) specify an affine short rate model producing the same short rates, and thus bond prices, as and (4.1). That is, an invertible linear transformation of the state process changes the particular form of the stochastic differential equation (7.1). But it leaves observable quantities, such as short rates and bond prices invariant.

This motivates the question whether there exists a classification method ensuring that affine short rate models with the same observable implications have a unique canonical representation. This topic has been addressed in [10, 9, 24, 8]. We now elaborate on this issue and show that the diffusion matrix can always be brought into block-diagonal form by a regular linear transform with .

We denote by

the diagonal matrix with diagonal elements , and we write for the -identity matrix.

Lemma 7.1.

There exists some invertible -matrix with such that is block-diagonal of the form

for some integer and symmetric positive semi-definite matrices . Moreover, and meet the respective admissibility conditions (3.1) in lieu of and .

Proof.

From (2.3) we know that is block-diagonal for all if and only if and are block-diagonal for all . By permutation and scaling of the first coordinate axes (this is a linear bijection from onto itself, which preserves the admissibility of the transformed and ), we may assume that there exists some integer such that and for . Hence and for are already block-diagonal of the special form

For , we may have non-zero off-diagonal elements in the -th row . We thus define the -matrix with -th column and set

One checks by inspection that is invertible and maps onto . Moreover,

From here we easily verify that

and thus

Since , the first assertion is proved.

The admissibility conditions for and can easily be checked as well. ∎

Theorem 7.2 (Canonical Representation).

Any affine short rate model (4.1), after some modification of if necessary, admits an -valued affine state process with block-diagonal diffusion matrix of the form

| (7.5) |

for some integer .

8 Existence and Uniqueness of Affine Processes

All we said about the affine process so far was under the premise that there exists a unique solution of the stochastic differential equation (2.1) on some appropriate state space . However, if the diffusion matrix is affine then cannot be Lipschitz continuous in in general. This raises the question whether (2.1) admits a solution at all.

In this section, we show how can always be realized as unique solution of the stochastic differential equation (2.1), which is (7.1), in the canonical affine framework and for particular choices of .

We recall from Theorem 2.2 that the affine property of imposes explicit conditions on , but not on as such. Indeed, for any orthogonal -matrix , the function yields the same diffusion matrix, , as .

On the other hand, from Theorem 3.2 we know that any admissible parameters in (2.3) uniquely determine the functions as solution of the Riccati equations (3.2), for all . These in turn uniquely determine the law of the process . Indeed, for any and , we infer by iteration of (2.2)

Hence the joint distribution of is uniquely determined by the functions and . By further iteration of this argument, we conclude that every finite dimensional distribution, and thus the law, of is uniquely determined by the parameters .

We conclude that the law of an affine process , while uniquely determined by its characteristics (2.3), can be realized by infinitely many variants of the stochastic differential equation (7.1) by replacing by , for any orthogonal -matrix . We now propose a canonical choice of as follows:

- •

-

•

Set , , and

Chose for any measurable -matrix-valued function satisfying

(8.1) In practice, one would determine via Cholesky factorization, see e.g. [31, Theorem 2.2.5]. If is strictly positive definite, then turns out to be the unique lower triangular matrix with strictly positive diagonal elements and satisfying (8.1). If is merely positive semi-definite, then the algorithm becomes more involved. In any case, will depend measurably on .

- •

We thus have shown:

Theorem 8.1.

Let be admissible parameters. Then there exists a measurable function with , and such that, for any , there exists a unique -valued solution of (7.1).

Moreover, the law of is uniquely determined by , and does not depend on the particular choice of .

The proof of the following lemma uses the concept of a weak solution. The interested reader will find detailed background in e.g. [25, Section 5.3].

Lemma 8.2.

For any , there exists a unique -valued solution of (8.2).

Proof.

First, we extend continuously to by setting , where we denote .

Now observe that solves the autonomous equation

| (8.3) |

Obviously, there exists a finite constant such that the linear growth condition

is satisfied for all . By [22, Theorems 2.3 and 2.4] there exists a weak solution666A weak solution consists of a filtered probability space carrying a continuous adapted process and a Brownian motion such that (8.3) is satisfied. The crux of a weak solution is that is not necessarily adapted to the filtration generated by the Brownian motion . See [35, Definition 1] or [25, Definition 5.3.1]. of (8.3). On the other hand, (8.3) is exactly of the form as assumed in [35, Theorem 1], which implies that pathwise uniqueness777Pathwise uniqueness holds if, for any two weak solutions and of (8.3) defined on the the same probability space with common Brownian motion and with common initial value , the two processes are indistinguishable: for all . See [35, Definition 2] or [25, Section 5.3]. holds for (8.3). The Yamada–Watanabe Theorem, see [35, Corollary 3] or [25, Corollary 5.3.23], thus implies that there exists a unique solution of (8.3), for all .

Admissibility of the parameters and and the stochastic invariance Lemma B.1 eventually imply that is -valued for all . Whence the lemma is proved. ∎

Appendix A On the Regularity of Characteristic Functions

This auxiliary section provides some analytic regularity results for characteristic functions, which are of independent interest. These results enter the main text only via the proof of Theorem 3.3. This section may thus be skipped at the first reading.

Let be a bounded measure on , and denote by

its characteristic function888This is a slight abuse of terminology, since the characteristic function of is usually defined on real arguments . However, it facilitates the subsequent notation. for . Note that is actually well defined for where

We first investigate the interplay between the (marginal) moments of and the corresponding (partial) regularity of .

Lemma A.1.

Denote for , and let and .

If exists then

On the other hand, if then and

for all , and .

Proof.

As usual, let denote the th standard basis vector in . Observe that is the characteristic function of the image measure of on by the mapping . Since , the assertion follows from the one-dimensional case, see [30, Theorem 2.3.1].

The second part of the lemma follows by differentiating under the integral sign, which is allowed by dominated convergence. ∎

Lemma A.2.

The set is convex. Moreover, if is an open set in , then is analytic on the open strip in .

Proof.

Since is a convex function, its domain is convex, and so is every level set for .

Now let be an open set in . Since any convex function on is continuous on the open interior of its domain, see [32, Theorem 10.1], we infer that is continuous on . We may thus assume that is open in and non-empty for large enough.

Let and be a sequence in with . For large enough, there exists some such that . This implies and hence

Hence the class of functions is uniformly integrable with respect to , see [34, 13.3]. Since for all , we conclude by Lebesgue’s convergence theorem that

Hence is continuous on .

It thus follows from the Cauchy formula, see [11, Section IX.9], that is analytic on if and only if, for every and , the function is analytic on . Here, as usual, we denote the th standard basis vector in .

We thus let and . Then there exists some such that for all . In particular, and are bounded measures on . By dominated convergence, it follows that the two summands

are complex differentiable, and thus is analytic, in . Whence is analytic on . Since , the lemma follows. ∎

In general, does not have an open interior in . The next lemma provides sufficient conditions for the existence of an open set in .

Lemma A.3.

Let be an open neighborhood of in and an analytic function on . Suppose that is star-shaped around and for all . Then and on .

Proof.

We first suppose that for the open polydisc

for some . Note the symmetry .

As in Lemma A.1, we denote for . By assumption, for all . Hence is analytic on , and the Cauchy formula, [11, Section IX.9], yields

where for all . This power series is absolutely convergent on , that is,

From the first part of Lemma A.1, we infer that possesses all moments, that is, for all . From the second part of Lemma A.1 thus

From the inequality , for , and the above properties, we infer that for all ,

Hence , and Lemma A.2 implies that is analytic on . Since the power series for and coincide on , we conclude that on , and the lemma is proved for .

Now let be an open neighborhood of in . Then there exists some open polydisc with . By the preceding case, we have and on . In view of Lemma A.2 it thus remains to show that .

To this end, let . Since is star-shaped around in , there exists some such that for all and is analytic in . On the other hand, there exists some such that for all , and for . This implies

for . By Lemma A.2, the right hand side is an analytic function in . We conclude by Lemma A.4 below, for defined as the image measure of on by the mapping , that . Hence the lemma is proved. ∎

Lemma A.4.

Let be a bounded measure on , and an analytic function on , such that

| (A.1) |

for all , for some numbers . Then (A.1) also holds for .

Proof.

Denote and define , such that

| (A.2) |

We assume, by contradiction, that . Then there exists some and such that and such that can be developed in an absolutely convergent power series

In view of Lemma A.2, is analytic, and thus , on . Hence we obtain, by dominated convergence,

By monotone convergence, we conclude

for all . But this contradicts (A.2). Whence , and the lemma is proved. ∎

Appendix B Invariance and Comparison Results for Differential Equations

In this section we deliver invariance and comparison results for stochastic and ordinary differential equations, which are used in the proofs of the main Theorems 3.2, 3.3 and 4.1 and Lemma 8.2 above.

We start with an invariance result for the stochastic differential equation (2.1).

Lemma B.1.

Suppose and in (2.1) admit a continuous and measurable extension to , respectively, and such that is continuous on . Let and define the half space

its interior , and its boundary .

Intuitively speaking, (B.1) means that the diffusion must be “parallel to the boundary”, and (B.2) says that the drift must be “inward pointing” at the boundary of .

Proof.

Fix and let be a solution of (2.1). Hence

Since and are continuous, there exists a stopping time and a finite constant such that

and

for all . In particular, the stochastic integral part of is a martingale. Hence

We now argue by contradiction, and assume first that . By continuity of and , there exists some and a stopping time such that for all . In view of the above this implies

This contradicts for all , whence (B.2) holds.

As for (B.1), let be a finite constant and define the stochastic exponential . Then is a strictly positive local martingale. Integration by parts yields

where is a local martingale. Hence there exists a stopping time such that for all ,

Now assume that . By continuity of and , there exists some and a stopping time such that for all . For , this implies

This contradicts for all . Hence (B.1) holds, and part (i) is proved.

It is straightforward to extend Lemma B.1 towards a polyhedral convex set with half-spaces , for some elements and some . This holds in particular for the canonical state space . Moreover, Lemma B.1 includes time-inhomogeneous999Time-inhomogeneous differential equations can be made homogeneous by enlarging the state space. ordinary differential equations as special case. The proofs of the following two corollaries are left to the reader.

Corollary B.2.

Let denote the -th canonical half space in , for . Let be a continuous map satisfying, for all ,

Then any solution of

with satisfies for all .

Corollary B.3.

Let and be continuous - and -valued parameters, respectively, such that whenever . Then the solution of the linear differential equation in

with satisfies for all .

Here and subsequently, we let denote the partial order on induced by the cone . That is, if . Then Corollary B.3 may be rephrased, for , by saying that the operator is -order preserving, i.e. .

Next, we consider time-inhomogeneous Riccati equations in of the special form

| (B.3) |

for some parameters satisfying the following admissibility conditions

| (B.4) |

The following lemma provides a comparison result for (B.3). It shows, in particular, that the solution of (B.3) is uniformly bounded from below on compacts with respect to if .

Lemma B.4.

Proof.

After these preliminary comparison results for the Riccati equation (B.3), we now can state and prove an important result for the system of Riccati equations (3.2). The following is an essential ingredient of the proof of Theorem 3.3. It is inspired by the line of arguments in Glasserman and Kim [16].

Lemma B.5.

Let denote the maximal domain for the system of Riccati equations (3.2). Let . Then

-

(i)

is star-shaped around zero.

-

(ii)

satisfies either or . In the latter case, there exists some such that .

Proof.

We first assume that the matrices are block-diagonal, such that , for all .

Fix . We claim that . It follows by inspection that solves (B.3) with

and . Lemma B.4 thus implies that is nice behaved, as

| (B.6) |

for all . By the maximality of we conclude that , which implies , as desired. Hence is star-shaped around zero, which is part (i).

Next suppose that . Since is open, this implies and thus . From part (i) we know that for all and . On the other hand, there exists a sequence such that for all . By continuity of on , we conclude that there exists some sequence with and hence

| (B.7) |

Applying Lemma B.4 as above, where initial time is shifted to , yields

Corollary B.3 implies that is -order preserving. That is, . Hence, in view of (B.6) for ,

On the other hand, elementary operator norm inequalities yield

Together with (B.7), this implies . From Lemma B.6 below we conclude that for some . Moreover, in view of Lemma B.4, we know that is increasing . Therefore . Applying (B.6) and Lemma B.6 below again, this also implies that . It remains to set and observe that and thus

is uniformly bounded from below for all . Thus the lemma is proved under the premise that the matrices are block-diagonal for all .

The general case of admissible parameters is reduced to the preceding block-diagonal case by a linear transformation along the lines of Lemma 7.1. Indeed, define the invertible -matrix

where the -matrix has -th column vector

It is then not hard to see that , and

satisfy the system of Riccati equations (3.2) with , and replaced by the admissible parameters

Moreover, are block-diagonal, for all . By the first part of the proof, the corresponding maximal domain , and hence also , is star-shaped around zero. Moreover, if , then

and there exists some such that

Hence the lemma is proved. ∎

Lemma B.6.

Let , and and be sequences in such that

for all . Then the following are equivalent

-

(i)

-

(ii)

for some .

In either case, and .

Proof.

: since and , we conclude that for some .

: this follows from .

The last statement now follows since . ∎

Remark B.7.

We may without loss of generality assume block-diagonal form of , (cf. the final part of the proof of Lemma B.5). Assume, by contradiction, that for some , . Then, as in the first proof, we may deduce the existence of such that

| (B.8) |

holds for some . Set , . Then for the following differential inequality holds,

| (B.9) | ||||

and . Hence noting we obtain by Lemma B.4 for all

On the other hand, for some positive constant , for all , hence , which contradicts (B.8).

References

- [1] H. Amann, Ordinary differential equations, vol. 13 of de Gruyter Studies in Mathematics, Walter de Gruyter & Co., Berlin, 1990. An introduction to nonlinear analysis, Translated from the German by Gerhard Metzen.

- [2] L. B. G. Andersen and V. V. Piterbarg, Moment explosions in stochastic volatility models, Finance and Stochastics, 11 (2007), pp. 29–50.

- [3] D. Brigo and F. Mercurio, Interest rate models—theory and practice, Springer Finance, Springer-Verlag, Berlin, second ed., 2006. With smile, inflation and credit.

- [4] R. H. Brown, S. S. M, Rogers, L. C. G., S. Mehta, and J. Pezier, Interest rate volatility and the shape of the term structure [and discussion], Philosophical Transactions of the Royal Society of London, Series A, 347 (1994), pp. 563–576.

- [5] M.-F. Bru, Wishart Processes, Journal of Theoretical Probability, 4 (1991), pp. 725–751.

- [6] B. Buraschi, P. Porchia, and F. Trojani, Correlation risk and optimal portfolio choice. Working paper, University St.Gallen, 2006.

- [7] L. Chen, D. Filipović, and H. V. Poor, Quadratic term structure models for risk-free and defaultable rates, Math. Finance, 14 (2004), pp. 515–536.

- [8] P. Cheridito, D. Filipović, and R. L. Kimmel, A note on the Dai–Singleton canonical representation of affine term structure models. Forthcoming in Mathematical Finance, 2008.

- [9] P. Collin-Dufresne, R. S. Goldstein, and C. S. Jones, Identification of maximal affine term structure models, J. of Finance, 63 (2008), pp. 743–795.

- [10] Q. Dai and K. J. Singleton, Specification analysis of affine term structure models, J. of Finance, 55 (2000), pp. 1943–1978.

- [11] J. Dieudonné, Foundations of modern analysis, Pure and Applied Mathematics, Vol. X, Academic Press, New York, 1960.

- [12] D. Duffie, D. Filipović, and W. Schachermayer, Affine processes and applications in finance, Ann. Appl. Probab., 13 (2003), pp. 984–1053.

- [13] D. Duffie and R. Kan, A yield-factor model of interest rates, Mathematical Finance, 6 (1996), pp. 379–406.

- [14] D. Duffie, J. Pan, and K. Singleton, Transform analysis and asset pricing for affine jump-diffusions, Econometrica. Journal of the Econometric Society, 68 (2000), pp. 1343–1376.

- [15] J. Fonseca, M. Grasseli, and C. Tebaldi, A multi-factor volatility Heston model. forthcoming in Quantitative Finance, 2009.

- [16] P. Glasserman and K.-K. Kim, Moment explosions and stationary distributions in affine diffusion models. To appear in Mathematical Finance, 2008/2009.

- [17] C. Gourieroux and R. Sufana, Wishart quadratic term structure models. Working paper, CREF HRC Montreal, 2003.

- [18] C. Gourieroux and R. Sufana, A classification of two factor affine diffusion term structure models, J. of Financial Econometrics, 4 (2006), pp. 31–52.

- [19] M. Grasseli and C. Tebaldi, Solvable affine term structure models, Mathematical Finance, 18 (2008), pp. 135–153.

- [20] S. Heston, A closed-form solution for options with stochastic volatility with appliactions to bond and currency options, Rev. of Financial Studies.

- [21] F. Hubalek, J. Kallsen, and L. Krawczyk, Variance-optimal hedging for processes with stationary independent increments, Ann. Appl. Probab., 16 (2006), pp. 853–885.

- [22] N. Ikeda and S. Watanabe, Stochastic differential equations and diffusion processes, vol. 24 of North-Holland Mathematical Library, North-Holland Publishing Co., Amsterdam, 1981.

- [23] N. Johnson and S. Kotz, Distributions in statistics. Continuous univariate distributions. 2., Houghton Mifflin Co., Boston, Mass., 1970.

- [24] S. Joslin, Can unspanned stochastic volatility models explain the cross section of bond volatilities? Working Paper, Stanford University, 2006.

- [25] I. Karatzas and S. E. Shreve, Brownian motion and stochastic calculus, vol. 113 of Graduate Texts in Mathematics, Springer-Verlag, New York, second ed., 1991.

- [26] M. Keller-Ressel, Moment explosions and long-term behavior of affine stochastic volatility models. to appear in Mathematical Finance.

- [27] , Affine processes- theory and applications in finance, PhD thesis Vienna University of Technology, (January, 2009).

- [28] V. Lakshmikantham, N. Shahzad, and W. Walter, Convex dependence of solutions of differential equations in a Banach space relative to initial data, Nonlinear Anal., 27 (1996), pp. 1351–1354.

- [29] R. W. Lee, The moment formula for implied volatility at extreme strikes, Mathematical Finance. An International Journal of Mathematics, Statistics and Financial Economics, 14 (2004), pp. 469–480.

- [30] E. Lukacs, Characteristic functions, Hafner Publishing Co., New York, 1970. Second edition, revised and enlarged.

- [31] A. Neumaier, Introduction to numerical analysis, Cambridge University Press, Cambridge, 2001.

- [32] R. T. Rockafellar, Convex analysis, Princeton Landmarks in Mathematics, Princeton University Press, Princeton, NJ, 1997. Reprint of the 1970 original, Princeton Paperbacks.

- [33] E. M. Stein and G. Weiss, Introduction to Fourier analysis on Euclidean spaces, Princeton University Press, Princeton, N.J., 1971. Princeton Mathematical Series, No. 32.

- [34] D. Williams, Probability with martingales, Cambridge Mathematical Textbooks, Cambridge University Press, 1991.

- [35] T. Yamada and S. Watanabe, On the uniqueness of solutions of stochastic differential equations, J. Math. Kyoto Univ., 11 (1971), pp. 155–167.