Counterparty risk valuation for Energy-Commodities swaps

Abstract

It is commonly accepted that Commodities futures and forward prices, in principle, agree under some simplifying assumptions. One of the most relevant assumptions is the absence of counterparty risk. Indeed, due to margining, futures have practically no counterparty risk. Forwards, instead, may bear the full risk of default for the counterparty when traded with brokers or outside clearing houses, or when embedded in other contracts such as swaps. In this paper we focus on energy commodities and on Oil in particular. We use a hybrid commodities-credit model to asses impact of counterparty risk in pricing formulas, both in the gross effect of default probabilities and on the subtler effects of credit spread volatility, commodities volatility and credit-commodities correlation. We illustrate our general approach with a case study based on an oil swap, showing that an accurate valuation of counterparty risk depends on volatilities and correlation and cannot be accounted for precisely through a pre-defined multiplier.

AMS Classification Codes: 60H10, 60J60, 60J75, 62H20, 91B70

JEL Classification Codes: C15, C63, C65, G12, G13

Keywords: Counterparty Risk, Credit Valuation adjustment, Commodities, Swaps,

Oil models, Convenience Yield models, Stochastic Intensity models.

Fitch Solutions, 101 Finsbury Pavement, EC2A 1RS London

E-mail:

damiano.brigo@fitchsolutions.com

June 24, 2008. Available also at www.damianobrigo.it and at SSRN.com

1 Introduction

In this paper we consider counterparty risk for commodities payoffs in presence of correlation between the default event and the underlying commodity, while taking into account volatilities both for credit and commodities. We focus on Oil but much of our reasoning can be adapted to other commodities with similar characteristics (storability, liquidity, and similar seasonality).

Past work on pricing counterparty risk for different asset classes is in Sorensen and Bollier (1994), Brigo and Masetti (2006) and Brigo and Pallavicini (2007, 2008) for interest rate swaps and exotics underlyings. Leung and Kwok (2005) and Brigo and Chourdakis (2008) worked on counterparty risk for credit (CDS) underlyings.

Here we analyze in detail counterparty-risky (or default-risky) Oil forward and swaps contracts.

In general the reason to introduce counterparty risk when evaluating a contract is linked to the fact that many financial contracts are traded over the counter, so that the credit quality of the counterparty can be relevant. This is particularly appropriated when thinking of the different defaults experienced by some important companies during the last years, especially in the energy sector.

Earlier works in counterparty risk for commodities include for example Cannabaro, Picoult and Wilde (2005), who analyze this notion more from a capital adequacy/ risk management point of view. In particular, their approach is not dynamical and does not consider explicitly credit spread volatility and especially correlation between the underlying commodity and credit spread. In our approach wrong way risk is modeled through said correlation. Mostly, however, the difference is in the purpose. We are valuing counterparty risk more from a pricing than a risk management perspective, resorting to a fully arbitrage free and fine-tuned risk neutral approach. This is why all our processes are calibrated to liquid market information both on forward curves and volatilities. Correlations are harder to estimate but we analyze their impact by letting them range across a set of possible values. A limitation of our approach is that we refer to a single counterparty.

In general we are looking at the problem from the viewpoint of a safe (default-free) institution entering a financial contract with another counterparty having a positive probability of defaulting before the final maturity. We formalize the general and reasonable fact that the value of a generic claim subject to counterparty risk is always smaller than the value of a similar claim having a null default probability, expressing the discrepancy in precise quantitative terms.

We consider Credit Default Swaps for the counterparty as liquid sources of market default probabilities. Different models can be used to calibrate CDS data and obtain default probabilities: here we resort to Brigo and Alfonsi (2005) stochastic intensity model, whose jump extension with analytical formulas for CDS options is illustrated in Brigo and El-Bachir (2008).

As a model for oil we adopt a two factor model shaping both the short term deviation in prices and the equilibrium price level, as in Smith and Schwartz (2000). This model can be shown to be equivalent to a more classical convenience yield model like in Gibson and Schwartz (1990), and a stochastic volatility extension of a similar approach is considered in Geman (2000). What is modeled is the oil spot price, under the implicit assumption that such a spot price process exists. This is not true for electricity, for example, and even for markets like crude oil where spot prices are quoted daily, the exact meaning of the spot is difficult to single out. Nonetheless, we assume, along with most of the industry and with Carmona and Ludkowski (2004), that there is a traded spot asset.

In the paper we find that counterparty risk has a relevant impact on the products prices and that, in turn, correlation between oil and credit spreads of the counterparty has a relevant impact on the adjustment due to counterparty risk. Similarly, oil and credit spread volatilities have reasonable impacts on the adjustment. The impact patterns do not involve the peculiar behaviour one observes in the case of credit underlyings, observed in Brigo and Chourdakis (2008). Nonetheless, the impact is quantitatively relevant, and we illustrate this with a case study based on an oil swap.

The paper is organized as follows: Section 2 lays down the general framework for the valuation of counterparty risk. In section 3 we present the CIR++ specification which serves as the credit model, and in section 4 we outline the two-factor Smith and Schwartz commodity model. Sections 5 and 6 illustrate the counterparty adjustments for forwards and swaps respectively. An example, based on a swap contract with between a bank and an airline company is presented in section 7.

2 General valuation of counterparty risk

We denote by the default time of the counterparty and we assume the investor who is considering a transaction with the counterparty to be default-free. We place ourselves in a probability space . The filtration models the flow of information of the whole market, including credit and defaults. is the risk neutral measure. This space is endowed also with a right-continuous and complete sub-filtration representing all the observable market quantities but the default event (hence where is the right-continuous filtration generated by the default event). We set , the risk neutral expectation leading to prices.

Let us call the final maturity of the payoff we need to evaluate. If there is no default of the counterparty during the life of the product and the counterparty has no problems in repaying the investors. On the contrary, if the counterparty cannot fulfill its obligations and the following happens. At the Net Present Value (NPV) of the residual payoff until maturity is computed: If this NPV is negative (respectively positive) for the investor (defaulted counterparty), it is completely paid (received) by the investor (counterparty) itself. If the NPV is positive (negative) for the investor (counterparty), only a recovery fraction REC of the NPV is exchanged.

Let us call (sometimes abbreviated into ) the discounted payoff of a generic claim at under counterparty risk. This is the sum of all cash flows from to , each discounted back at , and under counterparty risk. This is a stochastic payoff, whose price would be given by risk neutral expectation. We denote by the analogous quantity when counterparty risk is absent, or when the counterparty is default free. All payoffs are seen from the point of view of the “investor” (i.e. the company facing counterparty risk). Then we have and

| (2.1) | |||||

being the stochastic discount factor at time for maturity . This last expression is the general price of the payoff under counterparty risk. Indeed, if there is no early counterparty default this expression reduces to risk neutral valuation of the payoff (first term in the right hand side); in case of early default, the payments due before default occurs are received (second term), and then if the residual net present value is positive only a recovery of it is received (third term), whereas if it is negative it is paid in full (fourth term).

Calling the discounted payoff for an equivalent claim with a default-free counterparty, i.e. , it is possible to prove the following

Proposition 2.1.

(General counterparty-risk credit-valuation adjustment (CR-CVA) formula). At valuation time , and on , the price of our payoff under counterparty risk is

| Positive CR-CVA |

where is the Loss Given Default and the recovery fraction REC is assumed to be deterministic. It is clear that the value of a defaultable claim is the value of the corresponding default-free claim minus an option part, in the specific a call option (with zero strike) on the residual NPV giving nonzero contribution only in scenarios where . Counterparty risk adds an optionality level to the original payoff.

For a proof see for example Brigo and Masetti (2006).

Notice finally that the previous formula can be approximated as follows. Take for simplicity and write, on a discretization time grid ,

| approximated (positive) adjustment |

where the approximation consists in postponing the default time to the first following . From this last expression, under independence between and , one can factor the outer expectation inside the summation in products of default probabilities times option prices. This way we would not need a default model for the counterparty but only survival probabilities and an option model for the underling market of . This is what led to earlier results on swaps with counterparty risk in interest rate payoffs in Brigo and Masetti (2006). In this paper we do not assume zero correlation, so that in general we need to compute the counterparty risk without factoring the expectations.

3 Default modeling assumptions

In this section we consider a reduced form model that is stochastic in the default intensity for the counterparty. We will later correlate the credit spread of this model with the underlying commodity model.

More in detail, we assume that the counterparty default intensity is , and we denote the cumulated intensity by . We assume intensities to be strictly positive, so that are invertible functions.

We assume deterministic default-free instantaneous interest rate (and hence deterministic discount factors ), although our analysis would work well even with stochastic rates independent of oil and credit spreads.

We set ourselves in a Cox process setting, where

with standard (unit-mean) exponential random variable.

3.1 CIR++ stochastic intensity models

For the stochastic intensity model we set

| (3.1) |

where is a deterministic function, depending on the parameter vector (which includes ), that is integrable on closed intervals. The initial condition is one more parameter at our disposal: We are free to select its value as long as

We take to be a Cox Ingersoll Ross process (see for example Brigo and Mercurio (2001) or (2006)):

where the parameter vector is , with , , positive deterministic constants. As usual, is a standard Brownian motion processes under the risk neutral measure, representing the stochastic shock in our dynamics. We assume the origin to be inaccessible, i.e.

We will often use the integrated quantities

3.2 CIR++ model: CDS calibration

Since we are assuming deterministic rates, the default time and interest rate quantities are trivially independent. It follows that the (receiver) CDS valuation at time becomes model independent and is given by the formula

| (3.2) | |||

| (3.3) | |||

| (3.4) |

This means that if we strip survival probabilities from CDS in a model independent way at time 0, to calibrate the market CDS quotes we just need to make sure that the survival probabilities we strip from CDS are correctly reproduced by the CIR++ model. Since the survival probabilities in the CIR++ model are given by

| (3.5) |

we just need to make sure

from which

| (3.6) |

where we choose the parameters in order to have a positive function (i.e. an increasing ) and is the closed form expression for bond prices in the time homogeneous CIR model with initial condition and parameters (see for example Brigo and Mercurio (2001, 2006)). Thus, if is selected according to this last formula, as we will assume from now on, the model is easily and automatically calibrated to the market survival probabilities for the counterparty (possibly stripped from CDS data).

Once we have done this and calibrated CDS data through , we are left with the parameters , which can be used to calibrate further products. However, this will be interesting when single name option data on the credit derivatives market will become more liquid. Currently the bid-ask spreads for single name CDS options are large and suggest to either consider these quotes with caution, or to try and deduce volatility parameters from more liquid index options. At the moment we content ourselves of calibrating only CDS’s. To help specifying without further data we set some values of the parameters implying possibly reasonable values for the implied volatility of hypothetical CDS options on the counterparty.

4 Commodity model

We consider crude oil as a first important case.

Suppose we have a airline company that buys a forward contract on oil from a bank with a very high credit quality, so that we assume the bank to be default-free. The bank wants to charge counterparty risk to the airline in defining the forward price, as there is no collateral posted and no margining is occurring.

As a model for oil we adopt a two factor model shaping both the short term deviation in prices and the equilibrium price level, as in Smith and Schwartz (2000). This model can be shown to be equivalent to a more classical convenience yield model like in Gibson and Schwartz (1990), and a stochastic volatility extension of a similar approach is considered in Geman (2000). What is modeled is the oil spot price, under the implicit assumption that such a spot price process exists. This is not true for electricity, for example, and even for markets like crude oil where spot prices are quoted daily, the exact meaning of the spot is difficult to single out. Nonetheless, we assume, along with most of the industry, that there is a traded spot asset.

If we denote by the oil spot price at time , the log-price process is written as

where, under the risk neutral measure,

| (4.1) | |||||

| (4.2) |

and is a deterministic shift we will use to calibrate quoted futures prices. The process represents the short term deviation, whereas represents the backbone of the equilibrium price level in the long run.

For applications it can be important to derive the transition density of the spot commodity in this model. For the two factors we have a joint Gaussian transition,

This can be used for exact simulation between times and . As we know that the sum of two jointly Gaussian random variables is Gaussian, we have

from which, in particular, we see that

Hence we can compute the forward price at time of the commodity at maturity when counterparty risk is negligible and under deterministic interest rates, as

| (4.4) |

In particular, given the forward curve from the market, the expression for the shift that makes the model consistent with said curve is

The short term/equilibrium price model , when , is equivalent to the more classical Gibson and Schwartz (1990) model, formulated as

| (4.5) | |||||

the relationships being

5 Forward vs Future prices and counterparty risk

Consider now a forward contract. The propotypical forward contract agrees on the following.

Let be the valuation time. At the future time a party agrees to buy from a second party a commodity at the price fixed today. This is expressed by saying that the first party has entered a payer forward rate agreement. The second party has agreed to enter a receiver forward rate agreement. The value of this contract to the first and second party respectively, at maturity, will be

i.e. the actual price of the commodity at maturity minus the pre-agreed price in the payer case, and the opposite of this in the receiver case. Let us focus on the payer case. When this is discounted back at with deterministic interest rates, and risk neutral expectation is taken, this leads to the price being given by

| (5.1) |

Note that the forward price is exactly the value of the pre-agreed rate that sets the contract price to zero, i.e. . Let us maintain a general in the forward contract under examination.

In the oil model above, the forward contract price is given by plugging Formula (4.4) into (5.1). Let us denote by Fwdp such price (“p” is for payer),

whereas the opposite of this quantity is denoted by Fwdr.

We may apply our counterparty risk framework to the forward contract, where now , and Fwdp. We obtain as price of the payer forward under counterparty risk from Equation (2.1). We obtain

| Positive counterparty-risk adjustment |

Under the bucketing approximation given by Equation (2), we obtain

If one assumes independence between the underlying commodity and the conterparty default, one may factor the above expectation obtaining

The last term is the price of a option on a forward price, that is known in closed form in the Schwartz and Smith model, although we have to incorporate the shift in our formulation. We have

where is the cumulative distribution function of the standard Gaussian.

So we have the adjustment as a stream of options on forwards weighted by default probabilities.

If we do not assume independence then we need to substitute for the intensity model. Through iterated conditioning we obtain easily

If in particular we select then will be zero.

This price can be computed by joint simulation of , and . We may correlate the credit spread to the commodity by correlating the shock in the default intensity to the shocks in the commodity. If we assume

then the instantaneous correlation of interest is

This is the correlation one may try to infer from the market, through historical estimation or implying it from liquid market quotes. In general the only parameters that have not been calibrated previously are and . If we make for example the assumption that the two are the same,

then we get the model correlation parameters as a function of the already calibrated parameters and of the market correlation as

6 Swaps and counterparty risk

Consider now a swap contract. The propotypical swap contract is actually a portfolio of forward contracts with different maturities, and agrees on the following.

Let be the valuation time. At the future times in , a party agrees to buy from a second party a commodity at the price fixed today, on a notional . This is expressed by saying that the first party has entered a payer swap agreement. The second party has agreed to enter a receiver swap. The value of the payer commodity swap (CS) contract to the first party, at time , will be

Since the last formula is known in our oil model, in terms of the processes and , we easily obtain a formula for the commodity swap by summation.

If we look for the value of that sets the contract price to zero, i.e. the so called forward swap commodity price , we have

Using this rate we can also express the payer commodity swap price at a general strike as

whereas the receiver commodity swap would be

These formulas provide the value of these contracts when a clearing house or margining agreements are in place. However, swaps are often traded outside such contexts and as such they embed counterparty risk.

Our general formula (2.1), for a payer CS, when including counterparty risk, would read in the swap case:

| Positive counterparty-risk adjustment | ||||

Since the forward formula is known in our model, we can proceed similarly to the forward case to value the counterparty risk adjustment for the swap case through simulation. The receiver case is completely analogous.

7 A case study and conclusions

![[Uncaptioned image]](/html/0901.1099/assets/x1.jpg)

As a case study we consider an oil swap. An airline needs to buy oil in the future and is concerned about possible changes in the oil price. To hedge this price movement the airline asks a bank to enter a swap where the bank pays periodically to the airline a (floating) amount indexed at a relevant oil futures price at the coupon date. In exchange for this, the airline pays periodically an amount that is fixed in the beginning.

In the following, we are taking an example of a bank with currently high credit spreads as receiver, and one international airline as the payer of the swap.

We will look at the counterparty risk adjustment from the point of view of each of the two parties separately, by calibrating the credit model adequately in each case.

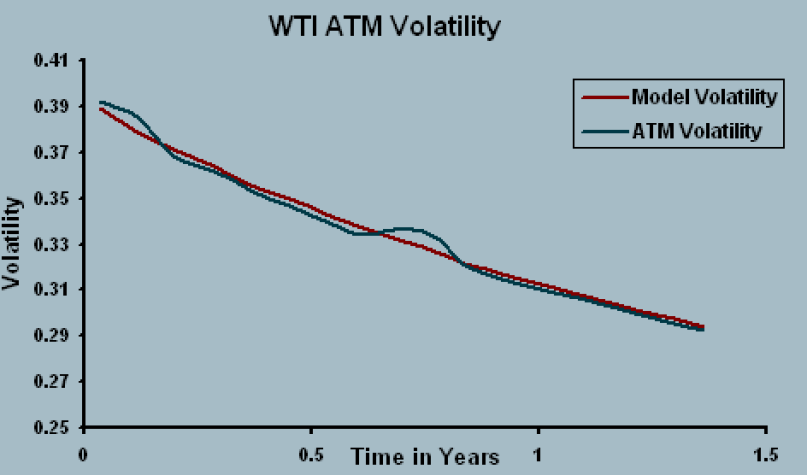

The Oil model has been calibrated to the At The Money Futures options implied volatility shown in Figure 1

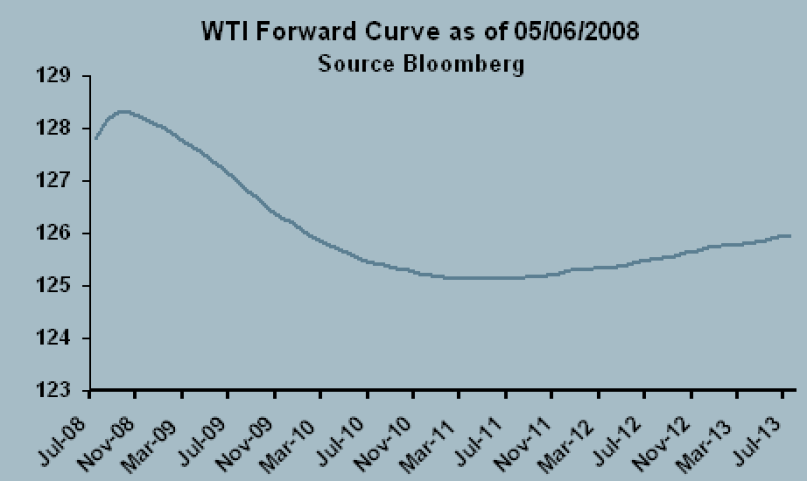

The shift has been calibrated in order to fit the forward curve extracted from West Texas Intermediate Futures in Figure 2

We reformulated the commodity model by setting the parameter in the long term equilibrium price to zero, as it can be included implicitly in the deterministic shift . The resulting Oil model parameters are shown in Table 1.

| \rW | |||

|---|---|---|---|

| \rW0.7170 | 0.3522 | 0.19 | -0.0392 |

The oil swap we consider has a final maturity of 5 years, monthly payments and strike given by USD, that is the strike setting to zero the value of the 5 years default free oil swap. is equal to one (barrel).

7.1 Counterparty Risk from the Payer Perspective (the Airline computes counterparty risk)

First, we use the CDS spreads for the bank, which are given in Table 2

| maturity (years) | 0.5 | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|---|

| spread (bps) | 345 | 332 | 287 | 256 | 232 | 2.17 |

The yield curve is given in Table 3

| maturity (years) | 3/12 | 6/12 | 2 | 5 | 10 | 30 |

|---|---|---|---|---|---|---|

| yield (percent) | 2.68 | 2.92 | 3.40 | 4.27 | 4.87 | 5.376 |

In the following we assume the bank credit quality to be characterized by a CIR++ stochastic intensity model that, as spread levels, is consistent with Table 2 through the shift , while allowing for credit spread volatility through the CIR dynamics. We use the base CIR parameter set given in Table 4. Later, we change the spread volatility parameter by reducing it through multiplicative factors smaller than one, and recalibrate the model shift to maintain consistency with Table 2. This way we investigate the impact of the spread volatility on the counterparty adjustment.

| 0.0560 | 0.6331 | 0.0293 | 0.5945 |

The graphs in Fig. 3 and Fig. 5 illustrate some of our results for the CR-CVA. The counterparty risk is expressed as a percentage of a 5Y maturing swap fixed leg value, which is 6852.35 USD.

First we observe the effect of varying the commodity volatility while keeping the credit intensity volatility fixed at 111The CDS implied volatility associated to these parameters is 26%. Brigo (2005, 2006), under the CDS market model, shows that implied volatilities for CDS options can easily exceed

The commodity volatility was varied by applying multiplicative factors to the two factors instantaneous volatilities and .

![[Uncaptioned image]](/html/0901.1099/assets/x4.png)

Fixed Leg Price maturity 5Y: 6852.35 USD for a notional of 1 Barrel per Month, CR-CVA as a (%) of the Fixed leg price

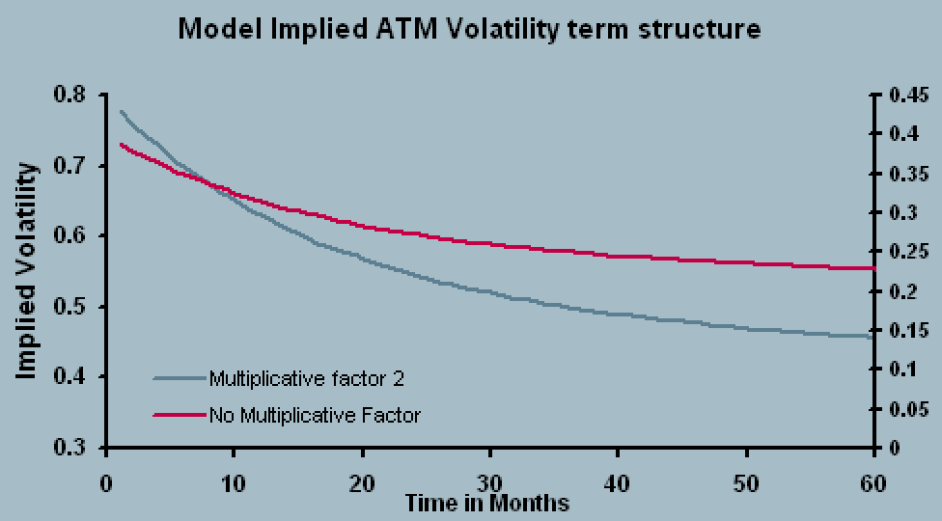

As an indication of implied volatility levels, the term structure of the commodity implied volatility when we apply the multiplicative factor 2 is given in Fig. 4

Secondly, we observe the effect of varying the intensity volatility while keeping the commodity spot volatility fixed at as implied by Table 1.

![[Uncaptioned image]](/html/0901.1099/assets/x6.png)

Fixed Leg Price maturity 5Y: 6852.35 USD for a notional of 1 Barrel per Month, CR-CVA as a (%) of the Fixed leg price

The same results are presented in a different way in Tables 5 and 6. In these tables, we give the absolute value of the adjustment in USD. We also express it as an adjusted Strike price that the payer might choose to pay to its counterparty by taking into account the estimated adjustment:

| \rH | intensity volatility | 0.0295 | 0.295 | 0.59 |

|---|---|---|---|---|

| \rW-68.9 | Adjustement in USD | 63.49 | 25.17 | 21.58 |

| \rW | Adjusted Strike | 124.84 | 125.54 | 125.60 |

| \rG-27.6 | CR-CVA (USD) | 69.99 | 45.89 | 41.5 |

| \rG | Adjusted Strike | 124.71 | 125.16 | 125.24 |

| \rW-13.8 | CR-CVA (USD) | 71.83 | 55.02 | 51.48 |

| \rW | Adjusted Strike | 124.68 | 124.99 | 125.05 |

| \rG0 | CR-CVA (USD) | 73.3 | 65.23 | 63.42 |

| \rG | Adjusted Strike | 124.66 | 124.80 | 124.84 |

| \rG+13.8 | CR-CVA (USD) | 74.62 | 76.63 | 77.36 |

| \rG | Adjusted Strike | 124.63 | 124.59 | 124.58 |

| \rW+27.6 | CR-CVA (USD) | 75.88 | 88.93 | 93.08 |

| \rW | Adjusted Strike | 124.61 | 124.37 | 124.29 |

| \rG+68.9 | CR-CVA (USD) | 79.32 | 130.39 | 152.05 |

| \rG | Adjusted Strike | 124.54 | 123.61 | 123.21 |

Fixed Leg Price maturity 5Y: 6852.35 USD for a notional of 1 Barrel per Month, Fair Strike without Counterparty Risk 126 USD.

| \rH | Comdty spot vol | 0.033 | 0.1642 | 0.3285 | 0.657 |

|---|---|---|---|---|---|

| \rW-68.9 | CR-CVA (USD) | 1.17 | 11.05 | 21.58 | 57.11 |

| \rW | Adjusted Strike | 125.98 | 125.79 | 125.60 | 124.95 |

| \rG-27.6 | CR-CVA (USD) | 1.63 | 21.75 | 41.5 | 107.48 |

| \rG | Adjusted Strike | 125.97 | 125.60 | 125.24 | 124.03 |

| \rW-13.8 | CR-CVA (USD) | 1.8 | 26.71 | 51.48 | 133.49 |

| \rW | Adjusted Strike | 125.96 | 125.51 | 125.05 | 123.55 |

| \rG0 | CR-CVA (USD) | 1.98 | 32.4 | 63.42 | 164.27 |

| \rG | Adjusted Strike | 125.96 | 125.41 | 124.84 | 122.98 |

| \rG+13.8 | CR-CVA (USD) | 2.15 | 38.85 | 77.36 | 200.08 |

| \rG | Adjusted Strike | 125.96 | 125.28 | 124.58 | 122.33 |

| \rW+27.6 | CR-CVA (USD) | 2.34 | 46.05 | 93.08 | 240.41 |

| \rW | Adjusted Strike | 125.96 | 125.15 | 124.29 | 121.59 |

| \rG+68.9 | CR-CVA (USD) | 2.92 | 72.47 | 152.05 | 397.87 |

| \rG | Adjusted Strike | 125.95 | 124.67 | 123.21 | 118.70 |

Fixed Leg Price maturity 5Y: 6852.35 USD for a notional of 1 Barrel per Month, Fair Strike without Counterparty Risk 126 USD.

7.2 Counterparty Risk from the Receiver Perspective (the Bank computes counterparty risk)

Now we place ourselves from the point of view of the bank, and we use the CDS spreads for the airline, which are given in Table 7

| maturity (years) | 0.5 | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|---|

| spread (bps) | 76 | 82 | 104 | 122 | 139 | 154 |

We use the same discount curve as in Table 3.

Here, the airline credit quality is represented by a CIR++ stochastic intensity model that, as spreads levels, is consistent with Table 7 through the shift , while allowing for credit spread volatility through the CIR dynamics. We use the base CIR parameter set given in Table 8. Later, we reduce the spread volatility parameter via multiplicative factors smaller than one, and recalibrate the shift to maintain each time the model consistent with Table 7. This way we investigate again the impact of the spread volatility on the counterparty adjustment.

| 0.0000 | 0.5341 | 0.0328 | 0.2105 |

As before, we observe the effect of varying the commodity volatility and of the airline credit intensity volatility, starting from as from Table 1 and . We apply the same multiplicative factors as before and the results are summarized in the graphs in Fig. 7 and Fig. 6.

![[Uncaptioned image]](/html/0901.1099/assets/x7.png)

Fixed Leg Price maturity 5Y: 6852.35 USD for a notional of 1 Barrel per Month, CR-CVA as a (%) of the Fixed leg price

![[Uncaptioned image]](/html/0901.1099/assets/x8.png)

Fixed Leg Price maturity 5Y: 6852.35 USD for a notional of 1 Barrel per Month, CR-CVA as a (%) of the Fixed leg price

| \rH | intensity volatility | 0.0295 | 0.295 | 0.59 |

|---|---|---|---|---|

| \rW-68.9 | CR-CVA (USD) | 29.62 | 38.95 | 46.62 |

| \rW | Adjusted Strike | 126.54 | 126.71 | 126.85 |

| \rG-27.6 | CR-CVA (USD) | 28.41 | 32.58 | 35.82 |

| \rG | Adjusted Strike | 126.52 | 126.59 | 126.66 |

| \rW-13.8 | CR-CVA (USD) | 28.21 | 31.02 | 32.4 |

| \rW | Adjusted Strike | 126.52 | 126.57 | 126.59 |

| \rG0 | CR-CVA (USD) | 27.99 | 29.37 | 29.16 |

| \rG | Adjusted Strike | 126.51 | 126.54 | 126.53 |

| \rG+13.8 | CR-CVA (USD) | 27.78 | 27.72 | 26.09 |

| \rG | Adjusted Strike | 126.51 | 126.51 | 126.48 |

| hline \rW+27.6 | CR-CVA (USD) | 27.49 | 26.15 | 23.42 |

| \rW | Adjusted Strike | 126.50 | 126.48 | 126.43 |

| \rG+68.9 | CR-CVA (USD) | 26.48 | 22.23 | 16.31 |

| \rG | Adjusted Strike | 126.48 | 126.41 | 126.30 |

Fixed Leg Price maturity 5Y: 6852.35 USD for a notional of 1 Barrel per Month, Fair Strike without Counterparty Risk 126 USD.

| \rH | Comdty spot vol | 0.033 | 0.1642 | 0.3285 | 0.657 |

|---|---|---|---|---|---|

| \rW-68.9 | CR-CVA (USD) | 0.12 | 26.33 | 46.62 | 80.26 |

| \rW | Adjusted Strike | 126.00 | 126.48 | 126.85 | 127.47 |

| \rG-27.6 | CR-CVA (USD) | 0.09 | 19.33 | 35.82 | 59.23 |

| \rG | Adjusted Strike | 126.00 | 126.35 | 126.65 | 127.08 |

| \rW-13.8 | CR-CVA (USD) | 0.08 | 17.35 | 32.4 | 53.64 |

| \rW | Adjusted Strike | 126.00 | 126.32 | 126.59 | 126.98 |

| \rG0 | CR-CVA (USD) | 0.07 | 15.42 | 29.16 | 48.59 |

| \rG | Adjusted Strike | 126.00 | 126.28 | 126.53 | 126.89 |

| \rG+13.8 | CR-CVA (USD) | 0.06 | 13.58 | 26.09 | 43.88 |

| \rG | Adjusted Strike | 126.00 | 126.25 | 126.48 | 126.80 |

| \rW+27.6 | CR-CVA (USD) | 0.05 | 11.86 | 23.42 | 39.09 |

| \rW | Adjusted Strike | 126.00 | 126.22 | 126.43 | 126.72 |

| \rG+68.9 | CR-CVA (USD) | 0.03 | 7.4 | 16.31 | 27.16 |

| \rG | Adjusted Strike | 126.00 | 126.13 | 126.30 | 126.50 |

Fixed Leg Price maturity 5Y: 6852.35 USD for a notional of 1 Barrel per Month, Fair Strike without Counterparty Risk 126 USD.

7.3 Conclusions

The patterns we observe in the counterparty-risk credit valuation adjustment (CR-CVA) are natural. Starting with the receiver case, for a fixed credit spread volatility, the receiver CR-CVA increases in oil volatility and decreases in correlation. Given the embedded oil option, the increase with respect to oil volatility is natural (as is in the payer case). As concerns correlation, as this increases, the oil tends to move in line with credit spreads. This means that higher credit spreads will lead to higher oil values, and the option will end up less in the money as the oil spot goes up. The opposite appears in the payer case. Patterns in credit spread volatility are similarly explained.

The size of the CVA hence depends on the precise value of the volatility and correlation dynamic parameters that cannot be explained via rough multipliers.

References

- (1) Brigo, D. (2005). Market Models for CDS Options and Callable Floaters, Risk, January issue. Also in: Derivatives Trading and Option Pricing, Dunbar N. (Editor), Risk Books, 2005.

- (2) Brigo, D. (2006). Constant Maturity Credit Default Swap Valuation with Market Models, Risk, June issue.

- (3) Brigo, D., and Alfonsi, A. (2005) Credit Default Swaps Calibration and Derivatives Pricing with the SSRD Stochastic Intensity Model, Finance and Stochastic, Vol. 9, N. 1.

- (4) Brigo, D., and El–Bachir, N. (2008). An exact formula for default swaptions pricing in the SSRJD stochastic intensity model. To appear in Mathematical Finance.

- (5) Brigo, D., and Masetti, M. (2006) Risk Neutral Pricing of Counterparty Risk. In Counterparty Credit Risk Modeling: Risk Management, Pricing and Regulation, ed. Pykhtin, M., Risk Books, London.

- (6) Brigo, D., Mercurio, F. (2001) Interest Rate Models: Theory and Practice - with Smile, Inflation and Credit, Second Edition, 2006, Springer Verlag.

- (7) Brigo, D., and Pallavicini, A. (2007). Counterparty Risk under Correlation between Default and Interest Rates. In: Miller, J., Edelman, D., and Appleby, J. (Editors), Numercial Methods for Finance, Chapman Hall.

- (8) Brigo, D., and Pallavicini, A. (2008). Counterparty risk and Contingent CDS with stochastic intensity hybrid models. Risk Magazine, February issue.

- (9) Cannabaro, E., Picoult, E., and Wilde, T. (2005). Counterparty Risk. Energy Risk, May issue.

- (10) Carmona, R., and Ludkovski, M. (2004). Spot Convenience Yield Models for Energy Markets. AMS Mathematics of Finance, G. Yin Y. Zhang eds., vol. 351 of Contemporary Mathematics, pp. 65 80, 2004.

- (11) Cherubini, U. (2005) Counterparty Risk in Derivatives and Collateral Policies: The Replicating Portfolio Approach. In: Proceedings of the Counterparty Credit Risk 2005 C.R.E.D.I.T. conference, Venice, Sept 22-23, Vol 1.

- (12) Collin-Dufresne, P., Goldstein, R., and Hugonnier, J. (2002). A general formula for pricing defaultable securities. Econometrica 72: 1377-1407.

- (13) Geman, H. (2000). Scarcity and price volatility in oil markets. EDF trafing technical report.

- (14) R. Gibson and E. S. Schwartz (1990). Stochastic convenience yield and the pricing of oil contingent claims, Journal of Finance XLV (3), 959–976.

- (15) Leung, S.Y., and Kwok, Y. K. (2005). Credit Default Swap Valuation with Counterparty Risk. The Kyoto Economic Review 74 (1), 25–45.

- (16) Schwartz, E., and Smith, J. (2000). Short-Term Variations and Long-Term Dynamics in Commodity Prices. Management Science, Vol. 46, No. 7, July 2000 pp. 893 911

- (17) Sorensen, E.H., and Bollier, T. F. (1994) Pricing Swap Default Risk. Financial Analysts Journal, 50, 23-33.