Universidad de Zaragoza, 50009 - Zaragoza, Spain,

11email: carmen.pellicer@unizar.es, 11email: rilopez@unizar.es

Economic Models with Chaotic Money Exchange

Abstract

This paper presents a novel study on gas-like models for economic systems. The interacting agents and the amount of exchanged money at each trade are selected with different levels of randomness, from a purely random way to a more chaotic one. Depending on the interaction rules, these statistical models can present different asymptotic distributions of money in a community of individuals with a closed economy. Key Words: Complex Systems, Econophysics, Gas-like Models, Money Dynamics, Random and Chaotic numbers, Modeling and Simulation

1 Introduction

Econophysics is born as a new science devoted to study Economy and Financial Markets with the traditional methods of Statistical Physics [1]. This discipline applies many-body techniques developed in statistical mechanics to the understanding of self-organizing economic systems [2]. One of its main objectives is to provide economists with new tools and new insights to deal with the complexity arising in economic systems.

The seminal contributions in this field [3], [4], [5] have to do with agent-based modeling and simulation. In these works, an ensemble of economic agents in a closed economy is interpreted as a gas of interacting particles exchanging money instead of energy. Despite randomness is an essential ingredient of these models, they can reproduce the asymptotic distributions of money, wealth or income found in real economic systems [2].

In the work presented here, the transfers between agents are not completely random as in the traditional gas-like models. The authors introduce some degree of determinism, and study its influence on the asymptotic wealth distribution in the ensemble of interacting individuals. As reality seems to be not purely random [6], the rules of agent selection and money transfers are altered from random to pseudo-random and extended up to chaotic conditions. This unveils their influence in the final wealth distribution in diverse ways. This study records the asymptotic wealth distributions displayed by all these scenarios of simulation.

The paper is organized as follows: Section 2 introduces the basic theory of gas-like economic models. Section 3 describes the four simulation scenarios studied in this work, and the following sections show the results obtained in the simulations. Conclusions are discussed in the final section.

2 The gas-like model: Boltzmann-Gibbs distribution of money

The conjecture of a kinetic theory of (ideal) gas-like model for trading in market was first discussed in 1995 [7]. Then, it was in year 2000, when several noteworthy papers dealing with the distribution of money and wealth [3], [4], [5] presented this theory in more detail.

The gas-like model for the distribution of money assimilates the dynamics of a perfect gas, where particles exchange energy at every collision, with the dynamics of an economic community, where individuals exchange money at every trade. When both systems are closed and the magnitude of exchange is conserved, the expected equilibrium distribution of these statistical systems may be the exponential Boltzmann-Gibbs distribution.

| (1) |

Here, and are constants related to the mean energy or money in the system, and . Theoretically, the derivation (and so the significance) of this distribution is based on the statistical behavior of the system and on the conservation of the total magnitude of exchange. It can be obtained from a maximum entropy condition [8] or from purely geometric considerations on the equiprobability over all accessible states of the system [9].

Different agent-based computer models of money transfer presenting an asymptotic exponential wealth distribution can be found in the literature [3], [10] , [11]. In these simulations, a community of agents with an initial quantity of money per agent, , trade among them. The system is closed, hence the total amount of money is a constant (). Then, a pair of agents is selected and a bit of money is transferred from one to the other. This process of exchange is repeated many times until statistical equilibrium is reached and the final asymptotic distribution of money is obtained.

In these models, the rule of agents selection in each transaction is chosen to be random (no local preference or no intelligent agents). The money exchange at each time is basically considered under two possibilities : as a fixed or as a random quantity. From an economic point of view, this means that agents are trading products at a fixed price or that prices (or products) can vary freely, respectively.

These models have in common that generate a final stationary distribution that is well fitted by the exponential function. Perhaps one would be tempted to affirm that this final distribution is universal despite the different rules for the money exchange, but this is not the case as it can be seen in [3], [10].

3 Simulation scenarios

Real economic transactions are driven by some specific interest (or profit) between the different interacting parts. Thus, on one hand, markets are not purely random. On the other hand, the everyday life shows us the unpredictable component of real economy. Hence, we can sustain that the short-time dynamics of economic systems evolves under deterministic forces and, in the long term, the recurrent crisis happening in these kind of systems show us the inherent instability of them. Therefore, the prediction of the future situation of an economic system resembles somehow to the weather prediction. We can conclude that determinism and unpredictability, the two essential components of chaotic systems, take part in the evolution of economy and financial markets.

Taking into account these evidences, the study of gas-like economic models where money exchange can have some chaotic ingredient is an interesting possibility. In other words, one could consider an scenario where the selection rules of agents and regulation of products prices in the market are less random and more chaotic. Specifically, mechanisms for pseudo-random and chaotic number generation are considered in this paper.

In the computer simulations presented here, a community of agents is given with an initial equal quantity of money, , for each agent. The total amount of money, , is conserved in time. For each transaction, a pair of agents is selected, and an amount of money is transferred from one to the other. The rules for money exchange will consider a variable in the interval , not necessarily random, in the following way:

-

•

Rule 1: the agents undergo an exchange of money, in a way that agent ends up with a -dependent portion of the total of two agents money, (), and agent takes the rest () [10].

-

•

Rule 2: an -dependent portion of the average amount of the two agents money, ), is taken from and given to [3]. If doesn’t have enough money, the transfer doesn’t take place.

As there are two different simulation parameters involved in these gas-like models (the parameter for selecting the agents involved in the exchanges and the parameter defining the economic transactions), four different scenarios can be obtained depending on the random or chaotic election of these parameters. These scenarios are considered in the following sections and are described as:

-

•

Scenario I: random selection of agents with random money exchanges.

-

•

Scenario II: random selection of agents with chaotic money exchanges.

-

•

Scenario III: chaotic selection of agents with random money exchanges.

-

•

Scenario IV: chaotic selection of agents with chaotic money exchanges.

It is worthy to say at this point, that the words random and pseudo-random express a slight difference in the statistical quality of randomness. The pseudo-random and chaotic numbers are obtained with two chaotic pseudo-random bit generators, selected to this purpose. These are described in [12] and [13], and are based in two 2D chaotic systems: the Hénon Map and the Logistic Bimap. Interactive animations of them can be seen in [14].

The particular properties of these generators [12], [13] make them suitable for the purpose of this study. They are able to produce pseudo-random and chaotic patterns of numbers that can be used as parameters of the simulations. Basically, these generators have two parts: the output of the chaotic maps is used as input of a binary mixing block that randomizes the chaotic signals and generates the final random numbers. Then, one one side, it is possible to take the exit of the chaotic blocks and produce chaotic sequences of numbers. On the other side, they can generate a sequence of numbers with a gradual variation of randomness by controlling a delay parameter taking part in the binary mixing block.

This last feature is obtained by varying the shift factor () in a way that the lower its value, the worse is the random quality of the numbers generated. Specifically, there is also a (around ) above which the properties of the generator can be considered of random quality.

As an example to show this gradual variation of randomness, the generator in [13] is used to produce different binary sequences and initial conditions of (further details [13]). These bits are transformed in integers of bits and transformed to floats dividing by the constant .

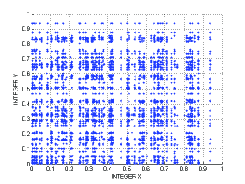

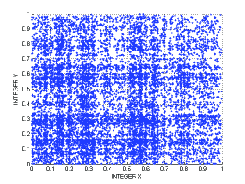

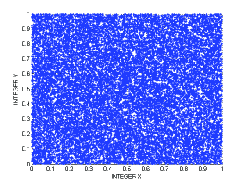

When the shift factor is varied, the random quality of these binary sequences also varies. This can be statistically measured by submitting them to statistical tests and it can be also graphically observed in Fig.1.

(a) (b) (c)

In Fig.1, we generated bits to obtain integers of bits. The integers obtained from the generator are transformed to flo ats. The variation of the shift factor shows graphically that with no shift at all, , the integers obtained are hardly random. With , the bits generated do not pass the frequency or monobit test and still show a strong no random appearance. When the shift factor grows over , the binary sequences pass Diehard and NIST statistical tests. Graphically in Fig.1(d), it can be assessed to possess high random quality.

4 Scenario I: Random selection of agents with random money exchange

In this section, both simulation parameters are selected to obey certain pseudo-random patterns. Thus, the generators in [13] is used to produce different binary sequences (with initial conditions of see further details in [13]). These bits are transformed in integers of bits and used as simulation parameters to select the agents or the money to exchange.

Then, computer simulations are performed in the following manner. A community of agents is considered with an initial quantity of money of . For each transaction two integer numbers are selected from the generated pseudo-random sequence with a given shift factor . A pair of agents is selected according to these integers with an -modulus operation. Additionally, a third integer number is obtained from another pseudo-random sequence with another shift factor . This integer is used to obtained a float number in the interval . The value of and the rule selected (Rule 1 or Rule 2) for the exchange determine the amount of money that is transferred from one agent to the other.

Choosing with different values it is possible to emulate an environment where the agents are locally selected under a more or less random scenario situation. The same for , the prices of products or services in the market can be emulated to be less random, regulated, or completely arbitrary.

(a) (b) (c)

The simulations take a total time of transactions. In Fig. 2, different cases are considered, taking pseudo random selection of agents or pseudo-random calculation of . Two rules of money exchange were considered, Rule 1 and 2 described in Section 2. The results show that all cases produce a stationary distribution that is well fitted to the exponential function. Although not depicted in Fig. 2 the case, where both agents and traded money are selected randomly, gives very similar results to these cases of Fig. 2, and also similar to the ones obtained in [3].

5 Scenario II: Random selection of agents with chaotic money exchange

In the previous section, it is observed that a variation in the random degree of selection of agents and/or traded money, does not affect the final equilibrium distribution of money. It leads to an exponential in all cases. In this section, the selection of agents is going to be set to random, while the exchange of money is going to be forced to evolve according to chaotic patterns. Economically, this means that the exchange of money has a deterministic component, although it varies chaotically. Put it in another way, the prices of products and services are not completely random. On the other side, the interaction between agents is arbitrary and is chosen randomly.

Taking the chaotic pseudo-random generators a step backwards, directly at the output of the chaotic block with initial conditions and (see [13] and [12] respectively, for details), the chaotic map variables and can be used as simulation parameters. Consequently, the computer simulations are performed in the following manner. A community of agents is considered with an initial quantity of money of . For each transaction two random numbers from a standard random generator are used to select a pair of agents. Additionally, a chaotic float number is produced to obtain the float number in the interval . The value of is calculated as for the Hénon map and as for the Logistic Bimap. This value and the rule selected for the exchange determine the amount of money that is transferred from one agent to the other.

The simulations take a total time of transactions. Different cases are considered, taking the Hénon chaotic map or the Logistic Bimap. Rules 1 and 2 are also considered. New features appear in this scenario. These can be observed in Fig.3

(a) (b) (c)

The first feature is that the chaotic behavior of is producing a different final distribution for each rule. Rule 2 is still displaying the exponential shape in the asymptotic distribution, but Rule 1 gives a different function distribution. It presents a very low proportion of the population in the state of poorness, and a high percentage of it in the middle of the richness scale, near to the value of the mean wealth. Rule 1 seems to lead to a more equitable distribution of wealth.

Basically, this is due to the fact that Rule 2 is asymmetric. Each transaction of Rule 2 represents an agent trying to buy a product to agent and consequently agent always ends with the same o less money. On the contrary, Rule 1 is symmetric and in each interaction both agents , as in a joint venture, end up with a division of their total wealth. Now, think in the following situation: with a fixed , let say , Rule 1 will end up with all agents having the same money as in the beginning, . Using a chaotic evolution of means restricting its value to a defined region, that of the chaotic attractor. Consequently, this is enlarging the distribution around the initial value of but it does not go to the exponential as in the random case [10].

6 Scenario III: Chaotic selection of agents with random money exchange

In this section, the selection of agents is going to evolve chaotically, while the exchange of money is random. Economically, this means that the locality of the agents or their preferences to exchange with each other is somehow deterministic but with a complex evolution. Thus, some commercial relations are going to be restricted. On the other hand, regulation of prices is random and they are going to evolve freely.

The chaotic generators are used directly at the output of the chaotic block, exactly as in the previous section. Again a community of agents with initial money of is taken and the chaotic map variables and will be used as simulation parameters. For each transaction two chaotic floats in the interval are produced. The value of these floats are and for the Hénon map and and for the Logistic Bimap. These values are used to obtain and as in previous section. Additionally, a random number from a standard random generator are used to obtain the float number in the interval . The value of and the selected rule determine the amount of money that is transferred from one agent to the other.

The simulations take a total time of transactions. Different cases are considered, taking the Hénon chaotic map or the Logistic Bimap, and Rules 1 and 2. As a result, an interesting point appears in this scenario with both rules. This is the high number of agents that keep their initial money in Fig. 4(a) and (b). The reason is that they don’t exchange money at all. The chaotic numbers used to choose the interacting agents are forcing trades between a deterministic group of them and hence some commercial relations result restricted.

(a) (b) (c)

In can be observed in Fig. 4(a) and (b), that the asymptotic distributions in this scenario again resemble the exponential function. The Logistic Bimap is symmetric (coordinates and ) and it produces the effect of behaving like scenario II but with a restricted number of agents.

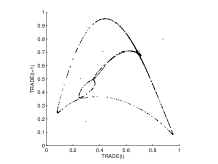

Amazingly, the Hénon Map with Rule 2 leads to a distribution with a heavy tail, a Pareto like distribution. A high proportion of the population (around 420 agents) finish in the state of poorness, while there are a minority of agents with great fortunes distributed up to the range of . This is due to the asymmetry of the rule, where agent always decrements its money, and the asymmetry of coordinates and in the Hénon chaotic Map used for the selection of agents. This double asymmetry makes some agents prone to loose in the majority of the transactions, while a few others always win.

7 Scenario IV: Chaotic selection of agents with chaotic money exchange

In this section, the selection of agents and the exchange of money are chaotic. Economically, this means that commercial relations are complex and some transactions are restricted. The exchange of money is going to vary disorderly, but in a more deterministic way. The prices of products and services are not completely random.

As in the previous sections, the chaotic generators are used directly at the output of the chaotic block. Again the chaotic map variables, and , will be used as simulation parameters. The computer simulations are performed in the following manner. A community of agents is considered with an initial quantity of money of . For each transaction, four chaotic floats in the interval are produced. Two of these floats are and for the Hénon map or and for the Logistic Bimap. These values are used to obtain and through simple multiplication (i.e.: ). Additionally, a chaotic float number is produced to obtain the float number in the interval . The value of is calculated as for the Hénon map or as for the Logistic Bimap. This value and the selected rule of exchange determine the money that is transferred between agents.

(a) (b) (c)

The simulations take a total time of transactions. Also, in this scenario, we take the Hénon chaotic map or the Logistic Bimap, and Rules 1 and 2 are considered. As a result, the same properties of both asymptotic distributions are maintained respect to section , then the same differences between rules are observed,as shown in Fig.5

Here, again a high number of agents keep their initial money. The chaotic choice in Fig.5 (c) is forcing trades between a specific group of agents, and then this type of locality makes some commercial relations restricted. The different behavior for Rule 1 and 2 is similar to scenario III. Rule 2 still presents an exponential shape, but Rule 1 gives a different function distribution with a maximum near the mean wealth. We remark that Rule 1 is able to generate a more equitable society when chaotic mechanisms are implemented in both processes, the agents selection and the money transfer.

8 Conclusions

The work presented here focuses on the statistical distribution of money in a community of individuals with a closed economy, where agents exchange their money under certain evolution laws. The several theoretical models and practical simulation results in this field, implement rules where the interacting agents or the money exchange between them are traditionally selected as fixed or random parameters ( [2], [4], [10]).

Here, a novel perspective is introduced. As reality tends to be more complex than purely fixed or random, it seems interesting to consider chaotic driving forces in the evolution of the economic community. Therefore, a series of agent-based computational results has been presented, where the parameters of the simulations are altered from random to pseudo-random and extended up to chaotic conditions.

In a first scenario, the exponential Boltzmann-Gibbs distribution is obtained for two different rules of money exchange under pseudo-random conditions. Consequently, pseudo-randomness do not distinguish between different evolution rules and richness is shared among agents in an exponential and unequal mode.

Introducing chaotic parameters in three other different scenarios leads to different results, in the sense that restriction of commercial relations is observed, as well as a different asymptotic wealth distribution depending on the rule of money exchange. It is remarkable that a more equitable distribution of wealth is obtained in one of the evolution rules when some of the dynamical parameters are driven by a chaotic system. This can be qualitatively observed in the distributions of money that have been obtained and reported for two different scenarios.

The authors hope that this study may provide new clues in the nature of economic self-organizing systems.

Acknowledgements The authors acknowledge some financial support by spanish grant DGICYT-FIS200612781-C02-01.

References

- [1] Mantegna R., Stanley H.E.: An Introduction to Econphysics: Correlations and Complexity in Finance. Cambridge University Press, Cambridge (1999)

- [2] Yakovenko V.M.: Econophysics, Statistical Mechanics Approach to. See arXiv:0709.3662v4 [q-fin.ST], to appear in Encyclopedia of Complexity and System Science, Springer (2009)

- [3] Dragulescu A.A., Yakovenko V.M.: Statistical mechanics of money. The European Physical Journal B, 17:723-729 (2000)

- [4] Chakraborti A., Chakrabarti B.K.: Statistical mechanics of money: how saving propensity affects its distribution. The European Physical Journal B, 17:167-170 (2000)

- [5] Bouchaud J.P., Mézard M.: Wealth condensation in a simple model economy. Physica A 282:536-545 (2000)

- [6] Sanchez J.R., Gonzalez-Estevez J., Lopez-Ruiz R., Cosenza M.: A Model of Coupled Maps for Economic Dynamics. European Physical Journal Special Topics 143:241-243 (2007)

- [7] Chakrabarti B.K., Marjit S.: Self-organization in Game of Life and Economics. Indian Journal Physics B 69:681-698 (1995)

- [8] Jaynes J.T.: Information Theory and Statistical Mechanics. Physical Review E 106:620-630 (1957)

- [9] López-Ruiz R., Sañudo J., Calbet X.: Geometrical derivation of the Boltzmann factor. American Journal of Physics 76:780-781 (2008)

- [10] Patriarca M., Chakraborti A., Kaski K.: Gibbs versus non-Gibbs distributions in money dynamics Physica A 340:334-339 (2004). arXiv:cond-mat/0312167v1

- [11] Hayes B.: Follow the money. American Siencist 90:400 (2002)

- [12] Suneel M.: Cryptographic Pseudo-Random Sequences from the Chaotic Hénon Map. See arXiv:cs/0604018v2 [cs.CR] (2006)

- [13] Pellicer-Lostao C., López-Ruiz R.: Pseudo-Random Bit Generation based on 2D chaotic maps of logistic type and its Applications in Chaotic Cryptography. Lectures Notes on Computer Science (LNCS) 5073:784-796 (2008)

- [14] Pellicer-Lostao C., López-Ruiz R., “Orbit Diagram of the Hénon Map” and “Orbit Diagram of Two Coupled Logistic Maps” from The Wolfram Demonstrations Project. URL: http://demonstrations.wolfram.com/