Long-range memory stochastic model of the return in financial markets

Abstract

We present a nonlinear stochastic differential equation (SDE) which mimics the probability density function (PDF) of the return and the power spectrum of the absolute return in financial markets. Absolute return as a measure of market volatility is considered in the proposed model as a long-range memory stochastic variable. The SDE is obtained from the analogy with earlier proposed model of trading activity in the financial markets and generalized within the nonextensive statistical mechanics framework. The proposed stochastic model generates time series of the return with two power law statistics, i.e., the PDF and the power spectral density, reproducing the empirical data for the one minute trading return in the NYSE.

keywords:

Models of financial markets , Stochastic equations , Power-law distributions , Long memory processesPACS:

89.65.Gh , 02.50.Ey , 05.10.Gg, url]http://www.itpa.lt/ gontis ,

1 Introduction

High frequency time series of financial data exhibit sophisticated statistical properties. What is the most striking is that many of these anomalous properties appear to be universal. Vast amounts of historical stock price data around the world have helped to establish a variety of so-called stylized facts [1, 2, 3, 4, 5, 6], which can be seen as statistical signatures of financial processes. The findings as regards the PDF of the return and other financial variables are successfully generalized within a non-extensive statistical framework [7]. The return has a distribution that is very well fitted by -Gaussians, only slowly becoming Gaussian as the time scale approaches months, years and longer time horizons. Another interesting statistic which can be modeled within the nonextensive framework, is the distribution of volumes, defined as the number of shares traded.

Interesting stochastic models related to the nonextensive statistics include an ARCH process with random noise distributed according to a -Gaussian as well as some state-dependent additive-multiplicative processes [8]. These models do capture the distribution of returns, but not necessarily the empirical temporal dynamics and correlations. Additive-multiplicative stochastic models of the financial mean-reverting processes provide a rich spectrum of shapes for the probability distribution function (PDF) depending on the model parameters [9]. Such stochastic processes model the empirical PDF’s of volatility, volume and price returns with success when the appropriate fitting parameters are selected. Many other fits are also proposed, including exponential ones [10] applicable for larger time scales.

Nevertheless, there is a necessity to select the most appropriate stochastic models, able to describe volatility as well as other variables in dynamical aspects and long-range correlation aspects.

There is empirical evidence that trading activity, trading volume, and volatility are stochastic variables with the long-range correlation [11, 12, 13] and this key aspect is not accounted for in some widely used models. The ARCH-like, multiscale models of volatility, which assume that the volatility is governed by the observed past price changes over different time scales, have been recently proposed [14, 15]. Trading volume and trading activity are positively correlated with market volatility. Moreover, trading volume and volatility show the same type of long memory behavior [16].

Recently we investigated analytically and numerically the properties of stochastic multiplicative point processes [17, 18], derived a formula for the power spectrum and related the model with the general form of the multiplicative stochastic differential equation [19, 20]. The extensive empirical analysis of the financial market data, supporting the idea that the long-range volatility correlations arise from trading activity, provides valuable background for further development of the long-ranged memory stochastic models [12, 13]. The power law behavior of the autoregressive conditional duration process [21] based on the random multiplicative process and its special case the self-modulation process [22], exhibiting fluctuations, supported the idea of stochastic modeling with a power law PDF and long memory. A stochastic model of trading activity based on an SDE driven Poisson-like process has been already presented in [23]. We further develop an approach of modulating the SDE with a closer connection to the nonextensive statistics in order to model the dynamics of return in this paper.

Long memory (long-term dependence) has been defined in time domain in terms of autocorrelation power law decay, or in frequency domains in terms of power law growth of low frequency spectra. Despite statistical methodology being developed for the data with the long-range dependence and the solid mathematical foundations of the area [25], let us consider behavior of the financial variables only in the frequency domain, analyzing the power spectral density.

In the second Section we present the nonlinear SDE generating a signal with a -Gaussian PDF and power law spectral density. In the third Section we analyze the tick by tick empirical data for trades on the NYSE for 24 shares and adjust the parameters of the proposed equations to the empirical data. A short discussion and conclusions are presented in the final section.

2 The stochastic model with a -Gaussian PDF and long memory

Earlier we investigated stochastic processes with long-range memory properties. Starting from the stochastic point process model, which reproduced a variety of self-affine time series exhibiting the power spectral density scaling as power of the frequency [18], later we introduced a Poisson-like process driven by the stochastic differential equation. The latter served as an appropriate model of trading activity in the financial markets [23]. In this section we generalize an earlier proposed nonlinear SDE within the nonextensive statistical mechanics framework to reproduce the long-range memory statistics with a -Gaussian PDF. The -Gaussian PDF of stochastic variable with variance can be written as

| (1) |

where is a constant of normalization and defines the power law part of the distribution. is introduced through the variational principle applied to the generalized entropy [8]

Here the -exponential of variable is defined as

| (2) |

and we assume that the -mean . With some transformation of parameters and

we can rewrite the -Gaussian in a more transparent form:

| (3) |

Looking for the appropriate form of the SDE we start from the general case of a multiplicative equation in the Ito convention with Wiener process :

| (4) |

If the stationary distribution of SDE (4) is the -Gaussian (3), then the coefficients of SDE are related as follows [24]:

| (5) |

From our previous experience modeling one-over-f noise and trading activity in financial markets [17, 18], building nonlinear stochastic differential equations exhibiting power law statistics [19, 20], we know that processes with power spectrum can be obtained using the multiplicative term or even a slightly modified form . Therefore, we choose the term as

| (6) |

and, consequently, by Eq. (5) we have the related relaxation

| (7) |

Then one gets the stochastic differential equation

| (8) |

Note that in the simple case Eq. (8) coincides with the model presented in the article by Queiros et al. [26] with

| (9) |

We will investigate higher values of in order to cache long-range memory properties of the absolute return in the financial markets. We can scale our variables

| (10) |

to reduce the number of parameters and to get simplified equations. Then SDE

| (11) |

describes a stochastic process with a stationary -Gaussian distribution

| (12) |

and the power spectral density of the signal

| (13) | |||||

| (14) |

with , and . Eqs. (13-14) were first derived for the multiplicative point process in [17, 18] and generalized for the nonlinear SDE (8) in [19, 20]. Although Eq. (8) coincides with Eq. (15) in ref. [20] only for high values of the variable , these values are responsible for the power spectrum. Note that the frequency in equation (13) is the scaled frequency matching the scaled time (10). The scaled equations (10)-(14) define a stochastic model with two parameters and responsible for the power law behavior of the signal PDF and power spectrum. Numerical calculations with Eq. (11) confirm analytical formulas (12-14) (see ref. [20]).

We will need a more sophisticated version of the SDE to reproduce a stochastic process with a fractured power spectrum of the absolute return observable in financial markets. Having in mind the statistics of the stochastic model (11) defined by Eqs. (12)-(14) and numerical modeling with more sophisticated versions of the SDE, we propose an equation combining two powers of multiplicativity

| (15) |

Here divides area of diffusion into two different power law regions to ensure the spectral density of with two power law exponents. A similar procedure has been introduced in the model of trading activity [23]. The proposed new form of the continuous stochastic differential equation enables us to reproduce the main statistical properties of the return observed in the financial markets. This provides an approach to the market with behavior dependent on the level of activity and exhibiting two stages: calm and excited. Equation (15) models the stochastic return x with two power law statistics, i.e., the PDF and power spectral density, reproducing the empirical power law exponents of the trading return in the financial markets. At the same time, via the term we introduce the exponential diffusion restriction for the high values of as the markets in the excited stage operate on the limit of nonstationarity. We solve Eq. (15) numerically using the method of discretization. Introducing the variable step of integration

the differential equation (15) transforms to the difference equation

| (16) | |||||

| (17) |

The continuous stochastic variable does not include any time scale as the return defined in a time window should. Having in mind that the return is an additive variable and depends on the number of transactions in a similar way to trading activity, we define the scaled return in the time period as the integral of the continuous stochastic variable . Note that here is measured in scaled time units Eq. (10) and will coincide with a one minute interval of empirical data. This serves as an procedure of adjustment to the real time scale for scaled equations.

It is worth recalling that integration of the signal in the time interval does not change the behavior of the power spectrum for the frequencies . This is just the case we are interested in for the long-range memory analysis of financial variables and we can expect Eqs. (13-14) to work for the stochastic variable as well. We analyzed the influence of signal integration on the PDF in previous modeling of trading activity; see ref. [17]. Integration of the nonlinear stochastic signal increases the exponent of the power law tails in the area of the highest values of the integrated signal. This hides fractured behavior of the PDF, which arises for as a consequence of the two powers in the multiplicative term of Eq. (15).

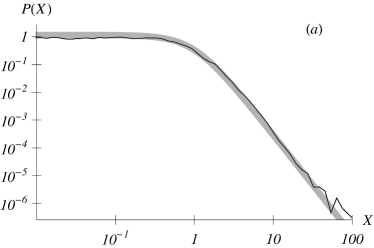

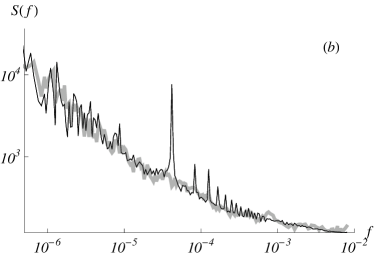

In Fig. 1 we demonstrate (a) the numerically calculated PDF of in comparison with the theoretical distribution Eq. (12) and (b) the numerically calculated power spectrum of with parameters appropriate for reproducing statistics for the absolute return in financial markets.

3 Empirical analysis and model adjustment

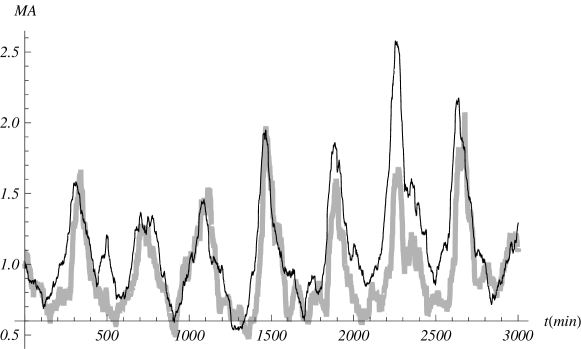

In this section we analyze the tick by tick trades of 24 stocks, ABT, ADM, BMY, C, CVX, DOW, FNM, GE, GM, HD, IBM, JNJ, JPM, KO, LLY, MMM, MO, MOT, MRK, SLE, PFE, T, WMT, XOM, traded on the NYSE for 27 months from January, 2005, recorded in the Trades and Quotes database. We sum empirical tick by tick returns into one-minute returns to adjust the continuous stochastic model presented. There is a problem in the use of a straightforward procedure to determine from empirical data. One expects to have when the return is assumed as a simple stochastic variable [26]. From our point of view the straightforward SDE recovery procedures do not work, as the return in real financial markets is at least double the stochastic process influenced by long memory stochastic trading activity and rapid price fluctuations. On the other hand, if one assumed , then long-range memory features of the process would be lost [20]. Earlier we investigated the nonlinear stochastic equations with , exhibiting the long-range memory properties [19], and proposed one as an appropriate stochastic model of trading activity in the financial markets [23]. Detailed analysis of the empirical data from the NYSE provides evidence that long-range memory properties of the return strongly depend on fluctuations of trading activity. In Fig. 2 we demonstrate strong correlation of the moving average of absolute returns per minute with the moving average of trading activities (number of trades per minute). Here for the empirical sequences of one-minute returns or trading activities we calculate moving averages defined as the centered means for a selected number of minutes ; for example, is

| (18) |

The best correlation can be achieved when the moving averages are calculated in the period from to minutes.

There are a lot of researchers investigating the power law distribution of returns and trading activity in the financial markets [27]. The -Gaussian PDF is a reasonable approximation to the empirical data [7]. The power law exponents for the extreme values of returns and trading activity are nearly the same: [23]. Furthermore, fascinating statistical similarity of two financial variables occurs in the power spectral density exhibiting long-range memory properties with two scaling exponents [23]. All these extraordinary sophisticated statistical properties are reproducible using the SDE (15) introduced in the previous section.

Many non-equilibrium systems exhibit spatial or temporal fluctuations of some parameter. There are two time scales: the scale on which the dynamics is able to reach a stationary state, and the scale for which the fluctuating parameter evolves. A particular case is when the time needed for the system to reach stationarity is much smaller than the scale at which the fluctuating parameter changes. In the long term, the non-equilibrium system is described by the superposition of different local dynamics at different time intervals, which has been called superstatistics [28, 29].

In order to account for the double stochastic nature of return fluctuations - a hidden slowly diffusing long-range memory process and rapid fluctuations of the instantaneous price changes — we decompose the empirical one-minute return series into two processes: the background fluctuations and the high amplitude rapid fluctuations dependent on the first one modulating. To perform this decomposition we assume that the empirical return can be written as instantaneous -Gaussian fluctuations with a slowly diffusing parameter dependent on the moving average of the return :

| (19) |

where is a -Gaussian stochastic variable with the PDF defined by Eq. (3) (the parameter is ). In Eq. (19) the parameter depends on the modulating moving average of returns, , and the empirically defined power law exponent . From the empirical time series of the one-minute returns one can draw histograms of corresponding to defined values of the moving average . The -Gaussian PDF is a good approximation to these histograms and the adjusted set of for selected values of gives an empirical definition of the function

| (20) |

The -Gaussians with and linear function (20) give a good approximation of fluctuations for all stocks and values of modulating . The long-term PDF of moving average can be approximated by a -Gaussian with and . All these empirically defined parameters form the background for the stochastic model of the return in the financial market.

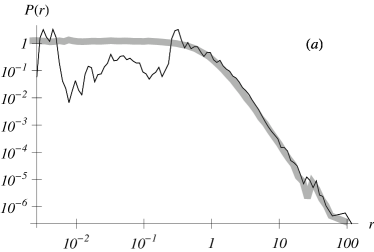

We propose to model the long-range memory modulating stochastic return by , where is a continuous stochastic variable defined by Eq. (15). The remaining parameters and can be adjusted to the empirical data and have values and . In Fig. 3 we provide a comparison of the empirical PDF, averaged over 24 stocks of NYSE, of one-minute returns normalized to the standard deviation and the power spectrum with the corresponding statistics of the proposed double stochastic model. This serves as an evidence of possibility of modeling the financial variables using nonlinear stochastic equations with elements of nonextensive statistics. Noticeable difference in theoretical and empirical PDFs for small values of are related with the prevailing prices of trades expressed in integer values of cents. Obviously we do not account for this discreteness in our continuous description. In the empirical power spectrum one-day resonance — the largest spike with higher harmonics — is present. This seasonality — an intraday activity pattern of the signal — is not included in the model either and this leads to the explicable difference from observed power spectrum.

4 Discussion and conclusions

In the previous work [23] we provided evidence that long-range memory fluctuations of trading activity in the financial markets may be considered as the background stochastic process responsible for the fractal properties of other financial variables. This background stochastic process can be reproduced using a nonlinear SDE (15) with multiplicative noise composed of two powers of a stochastic variable. The two powers in the SDE reveal different behaviors of the market in the periods of different trading activity. In this paper we generalized the form of the background SDE within the nonextensive statistical mechanics framework to reproduce fascinating statistical properties of the financial variables with a -Gaussian PDF and fractured behavior of the power spectrum.

In the prevailing relatively calm periods, with and multiplicativity specified by , markets behave as stationary stochastic processes with a -Gaussian PDF, . In the periods of excited behavior, when , the PDF approaches a nonstationary regime, . This leads to the excess values of financial variables, which have to be restricted by the additional limits in the SDE, term giving the exponential restriction of diffusion at the excess value . These rare escapes of a continuous stochastic variable smoothed by an integration procedure do not very considerably contribute to the main PDF of a financial variable. However, these escapes condition the behavior of the power spectrum, reducing the exponent of the power law distribution in the region of higher frequencies. In the case of the return, the background stochastic process defined by Eq. (15) is hidden by the secondary high amplitude -Gaussian stochastic process . Though the background fluctuations are considerably lower than the secondary ones, this drives the whole process through the empirically defined Eqs. (19) and (20).

The generalized new form of the continuous stochastic differential, equation (15), enables us to reproduce the main statistical properties of the return, observed in the financial markets. All parameters introduced are recoverable from the empirical data and are responsible for the specific statistical features of real markets. The model does capture the distribution of the return, the empirical temporal dynamics and correlations evaluated through the power spectral density of absolute return. The model definition with two powers of multiplicative noise enables us to reproduce the power spectral density with two different scaling exponents, as observed in the empirical data. Stochastic modeling of the financial variables with the nonlinear SDE is consistent with the nonextensive statistical mechanics and provides new opportunities to capture empirical statistics in detail.

Acknowledgements

We would like to express our appreciation to B. Kaulakys for his valuable advice and remarks. The authors acknowledge the support by the Agency for International Science and Technology Development Programs in Lithuania and EU COST Action MP0801 Physics of Competition and Conflicts .

References

- [1] R.N. Mantegna H.E. Stanley, Nature 376 (1995) 46-49.

- [2] R. Engle, Econometrica 66 (1998) 1127-1162.

- [3] V. Plerou, P. Gopikrishnan, L.A. Amaral, M. Meyer, H.E. Stanley, Phys. Rev. E 60 (1999) 6519-6529.

- [4] R. Engle, Econometrica 68 (2000) 1-22.

- [5] P.Ch. Ivanov, A. Yuen, B. Podobnik, Y. Lee, Phys. Rev. E 69 (2004) 056107.

- [6] J.B. Bouchaud, M. Potters, Theory of Financial Risks and Derivative Pricing, Cambridge University Press, Cambridge, 2004.

- [7] Cf.M. Gell-Mann, C. Tsallis, Nonextensive Entropy - Interdisciplinary Applications, Oxford University Press, NY, 2004.

- [8] S.M. Duarte Queiros, C. Anteneodo, C. Tsallis, Power-law distributions in economics: a nonextensive statistical approach, in: Proc. Of SPIE 5848 (2005) 151. physics/0503024.

- [9] C. Anteneodo, R. Riera, Phys. Rev. E 72 (2005) 026106.

- [10] B. Podobnik, D. Horvatic, A. Petersen H.E. Stanley, Europhysics Letters 85 (2009) 50003.

- [11] R.F. Engle, A.J. Paton, Quant. Finance 1 (2001) 237.

- [12] V. Plerou, P. Gopikrishnan, X. Gabaix et al, Quant. Finance 1 (2001) 262.

- [13] X. Gabaix, P. Gopikrishnan, V. Plerou, H.E. Stanley, Nature 423 (2003) 267.

- [14] L. Borland, On a multi-timescale statistical feedback model for volatility fluctuations, 2004 arXiv:cond-mat/0412526.

- [15] S.M. Duarte Queiros, EPL, 80 (2007) 30005.

- [16] I.N. Lobato, C. Velasco, J. Bus. Econom. Statist. 18 (2000) 410-427.

- [17] V. Gontis, B. Kaulakys, Physica A 343 (2004) 505-514.

- [18] B. Kaulakys, V. Gontis, M. Alaburda, Phys. Rev. E 71 (2005) 051105.

- [19] B. Kaulakys, J. Ruseckas, V. Gontis, M. Alaburda, Physica A 365 (2006) 217.

- [20] B. Kaulakys, M. Alaburda, J. Stat. Mech. (2009) P02051.

- [21] A-H. Sato, Phys. Rev. E 69 2004 047101.

- [22] M. Takayasu, H. Takayasu, Physica A 324 (2003) 101.

- [23] V. Gontis, B. Kaulakys, J. Ruseckas, Physica A 387 (2008) 3891-3896.

- [24] C.W. Gardiner, Handbook of Stochastic Methods for Physics, Chemistry and Natural Sciences, Springer-Verlag, Berlin, 1985.

- [25] J. Beran, Statistics for long-Memory Processes, Chapman & Hall, New York, 1994.

- [26] S.M. Duarte Queiros, L.G. Moyano, J. de Souza, C. Tsallis, Eur. Phys. J. B 55 (2007) 161-167.

- [27] M.M. Dacorogna, R. Gencay, U.A. Muller, R.B. Olsen, O.V. Pictet, An Introduction to High-Frequency Finance, Academic Press, San Diego, 2001.

- [28] C. Beck and E. G. Cohen, Physica A 322 (2003) 267.

- [29] S. Abe, C. Beck, and E. G. D. Cohen, Phys.Rev.E 76 (2007) 031102.