Available also at www.damianobrigo.it

Updated version to appear in Mathematical Finance

—

Arbitrage-free pricing of Credit Index Options.

The no-armageddon pricing measure and the role of correlation after the

subprime crisis

Abstract

In this work we consider three problems of the standard market approach to pricing of credit index options: the definition of the index spread is not valid in general, the usually considered payoff leads to a pricing which is not always defined, and the candidate numeraire one would use to define a pricing measure is not strictly positive, which would lead to a non-equivalent pricing measure.

We give a general mathematical solution to the three problems, based on a novel way of modelling the flow of information through the definition of a new subfiltration. Using this subfiltration, we take into account consistently the possibility of default of all names in the portfolio, that is neglected in the standard market approach. We show that, while the related mispricing can be negligible for standard options in normal market conditions, it can become highly relevant for different options or in stressed market conditions.

In particular, we show on 2007 market data that after the subprime credit crisis the mispricing of the market formula compared to the no arbitrage formula we propose has become financially relevant even for the liquid Crossover Index Options.

1 Introduction

In this paper we address the issue of the correct pricing of options on credit swaps, where the reference entity is a portfolio of defaultable names. The most common case in the market are Credit Index Options, which are options on the equilibrium level of the spread of a Credit Index, consisting of a standardized portfolio of credit default swaps. Liquidity had improved in the years preceding the subprime crisis in summer 2007, in particular in Europe. Monthly volumes for the option on the i-Traxx Crossover Index were upwards 13 billion at the end of 2006, with options available also on the Main and High Volatility Indices and on Index Tranches. During the credit crisis in 2007, payer options have protected investors from the rise of the credit indices, and trading has restarted on these products just two weeks after the pitch of the crisis at the end of July 2007.

Thus the main reference in the paper will be Credit Index swaptions, although the results apply in general to all market cases in which a spread defined with reference to a portfolio of defaultable entities must be modelled in an arbitrage-free way under an appropriate pricing measure. This includes dynamic notes linked to the performances of Index Spreads and embedded optionality in multiname credit derivatives.

The Credit Index Option gives to the investor the possibility to enter a Forward Credit Index at a prespecified spread, and to receive upon exercise a Front End Protection corresponding to index losses from option inception to option expiry. The initial market approach for pricing Credit Index Options was the use of a Black formula to price the option as a call on the spread, adding then the value of the Front End Protection to the price of the call. This approach has a first major flaw. It neglects the fact that one cannot separate the option from the Front End Protection, since the protection enters the exercise decision. This was pointed out first by Pedersen (2003). This observation led to an improved market standard, taking Front End Protection into account correctly without losing the tractability of the market Black formula approach, based on a redefinition of the underlying Index spread.

However, as we show in this work, also the latter approach presents some relevant problems.

First, there is still one scenario in which a Black formula, even if improved by the use of a Loss-adjusted Index Spread, does not take into account correctly the Front End Protection. In this scenario the pricing formula does not give the correct price of the option, while instead this could be computed in closed-form. We show in this work that, while this mispricing can be negligible for standard options in normal market conditions, it can become highly relevant for less standard options or in stressed market conditions. In particular, we show on 2007 market data that after the subprime credit crisis the mispricing of the market formula compared to the no arbitrage formula we propose has become financially relevant even for the most liquid Crossover Index Options.

A related second problem is that the formula used in market practice to compute the Index Spread is not defined in all states of the world.

The third problem regards the theoretical justification of the use of a Black formula in this context. According to the Fundamental Theorem of Asset Pricing, a rigorous derivation of a Black formula for the pricing of a Credit Index Option requires the definition of an appropriate numeraire for change to the pricing measure under which the underlying spread is a martingale (see Delbaen and Schachermayer (1994), Geman et al. (1995), and Jamshidian (1997)). The problem here is that, since we are dealing with portfolios or indices of defaultable names, the quantity that appears to be the natural choice for a numeraire to simplify pricing is not strictly positive. This makes the standard change of numeraire theory, based on strictly positive numeraires, inapplicable.

One may use a kind of survival measure such as the one introduced by Schonbucher (1999) for single name products, based on a numeraire which is not strictly positive. But such a measure would not be equivalent to the standard risk neutral, forward and swap measures used in mathematical finance, but only absolutely continuous with respect to them. This is practically undesirable, since in a such a case one can describe the dynamics of credit spreads under the survival measure, but cannot use the standard Girsanov Theorem to see the dynamics of credit spreads under the standard measures used in mathematical finance. Thus one could not, for example, extend a standard implementation of a Libor Market Model (Brace, Gatarek and Musiela (1997)) for default-free forward rates, usually done under a forward measure, to include also forward credit spreads.

To the best of our knowledge, the current literature does not solve the above three problems. The only partial exception is Jackson (2005), that deals with the first problem while not solving the second and third ones (in particular he uses a numeraire which is not strictly positive). Instead, here we show that the definition of an index spread valid in general, the correct description of the market payoff leading to a price defined in all states of the world, and the use of a valid strictly positive quantity to define an equivalent pricing measure can be given a general and elegant mathematical solution. The solution is based on the definition of appropriate subfiltrations. Empirical tests show that this solution can also have a relevant impact on the correct price of multiname credit options.

In Section 2 we introduce the setting and describe the Credit Forward Index, that will be the reference underlying of the options considered in the paper. Then we describe the Credit Index Option Payoff and we describe previous literature and market practice on the pricing of Index options. In Section 3 we show the problems in the market approach and we introduce the main technical instrument that will allow us to solve them: subfiltrations. In particular we introduce a new subfiltration apt to credit portfolio products. Then we use this instrument to compute a consistent and arbitrage-free definition of the underlying Index spread. In Section 4 we introduce a new pricing measure and prove the main result of the paper, the formula for no-arbitrage pricing of Index Options, different from the standard market approach. We also show how, performing generalization of some fundamental results of Jamshidian (2004), it is possible to express this formula in terms of numeraire pricing. In Section 5 we apply our results to market data, before and after the summer 2007 subprime crisis, and we show how, in stressed market conditions like those the credit market is experiencing now, the no-arbitrage formula we introduce has a relevant impact on valuation of Credit Index Options, avoiding a mispricing which is associated to the market standard valuation formula.

2 The Market

We are in a complete filtered probability space , where the filtration satisfies the usual hypothesis and we set and for a terminal date . We assume the existence of a bank-account numeraire with price process and an associated risk neutral measure . Defining, in line with Jamshidian (2004), a claim as an -measurable random variable such that is -integrable, the price process of any claim is given by

where indicates expectation under the risk-neutral measure and

is the discount factor from to . We consider defaultable issuers in a portfolio, and we indicate by the time of default of the -th issuer, .

In the following we are going to use Credit Indices as a reference. However our results can be extended to different multiname credit swaps (such as tranches) mainly through a redefinition of the loss from which protection is sought. The Credit Index is a swap contract providing protection against the default of a pool of names, from the beginning of the contract and until maturity . A spread or premium is paid for the Index protection, proportional to an outstanding notional that diminishes as names in the pool default.

There are two main families of indices. The Dow Jones i-Traxx Indices represent (mainly) the European market. The CDX family represent the North American market. In particular, for Main Indices the portfolio is set up to include only investment grade names (in fact the Main Indices are also called Investment Grade Indices), while the Crossover Indices include names with a lower credit quality. In the CDX family there is also a High Yield Index usually including issuers with credit reliability lower than Crossover names.

2.1 The Forward Credit Index

For a unit of Index notional each name has a notional of . It is market standard to give index quotations assuming that also the recovery rate () is the same for all names. The cumulated loss at is

At time the Outstanding Notional is

In a Credit Index the Protection Leg pays, at default times , the corresponding loss , from start date to maturity or until all names have defaulted. The Premium Leg pays, at times , or until all names have defaulted, a premium on the average of the outstanding notional for . The discounted payoff of the Protection Leg is

where the approximation discretizes loss payment times to the standard payment times of the Premium Leg.

The discounted payoff of the Premium Leg is

| (3) | |||

| (5) |

where the discretization considers the outstanding notional as computed at the end of the interval . The interval has length . The value of the two legs is computed by expectation under the risk neutral probability measure . We use the notation . When , we omit the argument writing simply . For the value of the two legs we have

The quantity in curly brackets in (3) is called in market practice the Index Defaultable present Value per Basis Point,

The Payer Forward Index starting at and lasting until has a payoff discounted at given by

while its price is given by

We have introduced forward index quantities because the Forward Index is the underlying of the most common credit portfolio option, the Index Swaption. It is useful to analyze these quantities in terms of single name defaults in order to understand how forward index quotations are made available in the market. In terms of single name quantities, the Protection Leg has value

while the Premium Leg has value

Forward Index quotations are not directly provided by the market, since only spot indices are quoted, namely with , where is a standardized set of annual maturities. Forward quotations are extracted from spot quotations according to the following homogeneity modelling assumptions. The first simplification for quoting indices is to assume that interest rates are independent of default, so

where is the price at of the default-free bond with maturity . The second simplification introduced for quoting indices is the assumption of homogeneous portfolio, corresponding to assuming that all names have the same credit risk, and consequently the same survival and default probability. This default probability common to all names is expressed through intensity modelling (Lando (1998)), with a deterministic, time-dependent intensity . One finally obtains

| (6) |

and

| (7) |

The default intensity is obtained through calibration to Spot Indices, with , and then used to compute quotations for forward indices, providing the underlying of Credit Index options. Credit Index options are introduced in the next section. In treating Index Options we will not confine ourselves to the simplifying hypotheses used by the market standard for index quotations.

2.2 The Credit Index Option

A payer Credit Index Option with inception , strike and exercise date , written on an index with maturity , is a contract giving the right to enter at into an Index with final payment at , as a protection buyer paying a fixed rate , thus entitled to receive protection from losses in the period between and . In addition the protection buyer receives, upon exercise, also the so-called Front End Protection, covering the losses from the option inception at time to the exercise date The Front End Protection and its financial rationale are described below.

The purpose of a Credit Index Option is to allow the protection buyer to lock in a particular premium spread , that the protection buyer has the right (and not the obligation) to make effective at a future time. However, if the above simple payoff was considered without Front End Protection, there would be an additional side-effect: the option buyer would not be protected from losses in the period between and maturity . In order to attract more investors, the standard Credit Index Option payoff includes, in case the option is exercised, the Front End Protection, whose discounted payoff is given by

In this section we present the market approach to the pricing of Credit Index Options, and then in the next sections we point out the open problems and present our solutions. In the simplest market approach, the Index Option is priced as a call option on the Index spread, and then the value of the front-end protection is added to the option price. The Index Spread is defined as the value of that sets the index value to zero,

allowing to write the index value as

The Index option is then priced by decomposing its value as follows

and then by expressing the first component through a standard Black formula,

| (8) |

where is the volatility of the forward spread and

This standard market approach to pricing the index option has a main flaw, as noticed by Pedersen (2003). The above formula neglects the fact that the front end protection is received only upon exercise. Pedersen (2003), defines the option payoff as

| (9) |

and suggests a numerical integration to compute the expectation of payoff (9). The prices of Index swaptions computed with Pedersen’s Formula confirm that the standard approach overprices out-of-the money payer options. Pedersen (2003) results have led to an improved Black Formula approach, based on the redefinition of the underlying Index Spread.

The procedure is described for example in Doctor and Goulden (2007). One defines a Loss-Adjusted index spread by taking Front End Protection into account directly. In fact the actual underlying of the credit index option is the Loss-Adjusted Index,

| (10) |

Thanks to the market standard quotation system, seen in Section 2.1, one has market liquid information available to compute all the above quantities. So it is natural to give a new spread definition, setting to zero rather than . This leads to the following Loss-Adjusted Market Index Spread

| (11) |

that allows to write (9) as

| (12) |

Now one can think of taking as numeraire and as lognormal underlying variable so as to price the option with the Market Credit Index Option Formula:

| (13) |

A receiver Credit Index Option with the same contract specifications as the payer above, is a contract giving the right to enter at into the same Index with final payment at , as a protection seller receiving a fixed rate . Following the same steps as above, the payoff is

and the price is given by

3 Towards an arbitrage-free Index Spread

We have seen in the previous Section that it appears possible to take Front End Protection into account correctly without losing the tractability of the market Black formula approach.

This is an important issue for building a solid and standardized option market. A Black formula approach is for example the standard for pricing swap options in the interest rate world, as justified by the market model framework introduced by Jamshidian (1997) for swaptions and Brace, Gatarek and Musiela (1997) for caps. In this pricing approach, the complexity of the no-arbitrage dynamics of the underlying asset is consistently transferred to a correct numeraire, through change of measure.

However, the market option formula (13) does not represent yet a consistent extension of this approach to Credit Index Options. If one wants to reach a consistent definition of the Index spread and a safely arbitrage-free valuation formula, one needs a specific treatment of the information sets involved, which in presence of default portfolios is more subtle than in the default-free case or even the single-name default case. This is shown in the following.

3.1 Problems of the market formulas

The approach leading to the market option formula (13) has highly improved on the initial market approach leading to (8). However, even the most recent approach fails. The two approaches share the following problems.

-

1.

The definition of the spread is not valid globally, but only when the denominator

is different from zero. Since is the price of a portfolio of defaultable assets, this quantity may vanish, it is not bounded away from zero in all states of the world having positive probability.

-

2.

When the pricing formula (13) is undefined, while instead we will see that the option price is known exactly in such a scenario. We will see, additionally, that in this scenario the above spread does not set the value of the adjusted index to zero.

-

3.

Since it is not strictly positive, would lead to the definition of a pricing measure not equivalent to the standard risk-neutral measure.

To the best of our knowledge, the current literature does not solve these problems. The only partial exception is Jackson (2005), that deals with 2) while not considering 1) and 3). Instead, here we give a solution to the above problems based on the definition of appropriate subfiltrations.

3.2 Subfiltrations for single issuer

Problems similar to those presented in the last section appear also in modelling default of a single name for pricing an option on a Credit Default Swap (CDS). A CDS is like an index swap with one single name. The CDS price for protection from and , in a simple formulation neglecting the accrual terms, is

| (14) |

where indicates the default time of the single reference credit entity.

When faced with an option on a CDS, it is natural to define the CDS equilibrium spread as the level of setting the above price to zero, and to chose as a numeraire for change of measure the single name defaultable present value per basis point

However, this is not a viable numeraire since it has zero value in all states of the world where the underlying name defaults before the option maturity, a set with positive measure. Thus, in all such states of the world the above definition of the CDS equilibrium spread is not valid. These problems of single name credit modelling are dealt with by Jamshidian (2004) and Brigo (2005, 2008). Although the solution proposed in these works cannot be trivially extended to the multiname setting, we recall them in the following since they are the foundations of the results we present here.

Jamshidian (2004) and Brigo (2005, 2008) make use of a subfiltration structure. Following Jeanblanc and Rutkowski (2000), define , where

namely the filtration generated by , thus representing default monitoring up to , while is a filtration representing the flow of all information except default itself (default-free information). A market operator observing only this second filtration can have information on the probability of default but cannot say exactly when, or even if, default has happened. This structure is typical for instance of the Cox process setting, where default is defined as the first jump of a Cox Process. A Cox Process is a process that, conditional on the path followed by the stochastic default intensity , is a Poisson Process of intensity . This definition hinges on assuming default intensity to be -adapted. However, the use of subfiltrations is not limited to Cox Processes.

The advantage of subfiltrations in the context of credit option pricing is that a subfiltration structure allows to define pricing formulas in terms of conditional survival probability which can be assumed to be strictly positive in any state of the world (or at least a.s.). In particular it allows to use a result by Jeanblanc and Rutkowski (2000), based on the definition of conditional expectation. A defaultable payoff with maturity discounted to , , is a payoff that satisfies

| (15) |

allowing us to write the Jeanblanc and Rutkowski Formula

| (16) |

Since a CDS is a defaultable contract, , one can write

| (17) |

Setting expression (17) to zero and solving in one find a definition of with a regular behaviour in all scenarios

since the denominator, being a.s. strictly positive, will also allow to define a probability measure that, under a Cox Process setting, leads to a simple Black formula, as shown in Brigo (2005, 2008):

In order to understand the following developments, it is important to notice why the use of the subfiltration, excluding information on default of the underlying single name, has effectively allowed to solve the above problems in a single name context. The corporate zero-coupon bonds considered in the CDS numeraire definition and the CDS itself are defaultable payoffs, whose value goes to zero at default, so we can use (16) and we can confine ourselves to making assumptions on the stochastic dynamics of the credit spread only on the subfiltration, which is all we need for pricing when . We do not need to treat explicitly the case since all involved payoffs have in this case a value which is known to be zero.

Then, for applying these results to options, we need the option itself to be priced with (16), and this is possible because single name Credit Options are knock-out options, namely their value is zero after default.

The situation in a multiname setting is different, so it requires a related but different approach, outlined in the next section.

3.3 A new subfiltration for multiname credit derivatives

In a multiname setting we have a plurality of reference entities that can default, so the above subfiltration setting gives us a plurality of possible subfiltrations,

| (18) | |||||

so that is the filtration generated by the default time of the name , with while is a filtration representing the flow of all information except the default of the name . When the information structure of a single name default valuation model is defined implicitly through (18), Jamshidian (2004) calls the resulting model complementary. Complementary models are central in the framework of Jamshidian (2004).

It would be enough to consider any of these possible subfiltrations to avoid the multiname Index spread to have an irregular behaviour (jump to infinity) at default of the entire pool. In terms of single name default times, the value of the spread denominator is

If we could price through a -expectation, analogously to the single name case, we would exclude information on default of the -th name. In this case would never jump to zero, keeping the -expectation of the entire portfolio strictly positive. However, the choice of a single pivotal name would be arbitrary, and, more importantly, using (16) requires that the payoff goes to zero when , which does not happen with the above portfolio.

We find that the most effective possibility for using (16) in this context is the following. We define a sub-filtration that only excludes information on the event that sets to zero. Define a new stopping time

and define implicitly a new filtration such that

so that excludes, from the total flow of market information, the information on the happening of a so-called portfolio “armageddon event”, corresponding to the default of all names in a portfolio. An extremely unlikely event when the option is on an a large Index with high-rating names and the market situation is normal, but that can have a non-negligible risk-neutral probability for products involving optionality on smaller portfolios or in stressed market conditions, as we show in Section 5.

In the following we assume that

Exploiting that , define

so as to write

The quantity is never null, and we will see that it is what we need for an effective definition of the Index Spread and of an equivalent pricing measure for Index Options.

3.4 Consistent computation of the Index Spread

Now, for reaching a valid definition of the spread, there is one remaining step. We need to price the Loss-Adjusted index (10) through the subfiltration. Unfortunately, we notice that applying (16) with playing the role of does not work, since (15) does not hold. In fact the Loss-Adjusted index, differently from , is never null, because even in case we receive front end protection. Now we need a generalization of (16). We can generalize (16) as follows

The first component can now be computed through (16), since is a defaultable payoff:

As for the second component,

See Bielecki and Rutkowski (2001) for more details on the above passages. The final formula is

| (21) |

The second component corresponds to the value of the payoff when we know that all defaults have already happened, and we know the exact “armageddon” time. It is possible to use (21) for pricing a Loss-Adjusted index only if we are able to compute the second component (3.4) without using assumptions on the dynamics of the forward spread, that, analogously to the single name case, we are going to give only for the filtration.

We now apply (21) to the Loss-Adjusted index payoff (10):

We analyze first . Notice that

while

Indeed, since we are conditioning to knowledge that all names have already defaulted, the expectation of front end protection corresponds to the entire notional diminished by the recovery.

We now analyze . Notice that

since protection and premium leg payoffs go to zero when all names in the portfolio default, so, calling

we have

| (22) | |||

Now it is convenient to perform the following decomposition:

so that

Formula (3.4) shows the actual components of the value of the Loss-Adjusted index, and will lead us in the next passages required for reaching a consistent valuation of the Index Option. We see that in a Loss-Adjusted portfolio we cannot define in all scenarios the equilibrium spread as the value of the spread setting the index value (22) to zero, since when the index value will always be . Therefore a consistent definition of the Index spread must avoid the hopeless attempt of globally setting to zero a value that in some scenarios can never be zero.

The financially meaningful definition of the Index Spread, that, as we will see in Section 4.2, also makes it a martingale under a natural pricing measure, considers the level of setting the Index value to zero in all scenarios where some names survive until maturity. Only in such scenarios, in fact, the payoff actually depends on the Index Spread. This corresponds to setting to zero only the first component of the index value (3.4),

which is the price of an armageddon-knock out tradable asset. We obtain the following definition of the equilibrium Arbitrage-free Index Spread

| (25) |

This definition of the index spread is both regular, since is bounded away from zero, and its definition has a reasonable financial meaning, since it does not claim to set to zero a value that cannot be set to zero with probability 1.

4 Arbitrage-free pricing of Index Options

The Index Option has payoff

In this section we evaluate the option, through change to a newly defined pricing measure. However we first need to analyze in more details the payoff.

4.1 Analysis of the Index Option Payoff

The use of subfiltrations and pricing formula (21) induces a redefinition not only of the underlying spread, but also of the value of the Index at Maturity and thus of the Index Option payoff:

where the last passage follows from the properties of indicators. Notice the correct payoff is split in two parts, and differently from (12) it does not lead to Problem 2 of Section 3.1, but instead it represents the actual payoff in all states of the world. Now, using again pricing formula (21), we can reach a fully consistent computation of the value of the Credit Index Option.

Notice , , so

and

This leads to the option pricing formula

So we have reached a formula that really shows the different components of the option value, and allows us to compute them in a convenient way. The third part is just the present value of the option when a portfolio “armageddon event” happens before . The second part takes correctly into account the probability of such an event between now and the option expiry. The first part , that erroneously was the only one considered in the simpler formula (13), is the part that we will compute through a closed-form standard option formula.

This requires the definition of a viable change of measure, therefore it means solving also Problem 3. We see in the next section that, although this is technically the most demanding of the three problems, the preceding analysis and in particular the introduction of an appropriate subfiltration already gives us the correct tools to deal with this issue.

4.2 An Equivalent measure for Credit Multiname Options

Now we deal with the evaluation of the first part of (4.1), that as we have seen is the only part that contains optionality. First of all we compute

Since

we have

Now it is natural to take the quantity

to define a probability measure allowing to simplify the computation. In fact, differently from which would be the quantity that one should select if subfiltrations had not been introduced, is strictly positive. Only with a strictly positive quantity we remain in the context of probability measures which are equivalent to the risk neutral measure and, by transitivity, to the real world probability measure.

We define the -no-armageddon pricing measure through definition of the Radon-Nykodim derivative of this measure with respect to , restricted to ,

| (27) |

Recall that, by definition of Radon-Nykodim derivative,

The definition of that allows a computational simplification of option pricing is

Notice that , the locally risk-free bank account, is -adapted. For derivatives pricing we need to define the restriction of to , . It is clear that if we define , , as an martingale

we have that is exactly the restriction we are looking for, , since for all

where the last but one passage comes from Kolmogorov’s definition of conditional expectation. Then notice that

so also the Radon-Nykodim derivative restricted to all , , can be expressed in closed form through market quantities. This is sufficient to apply the well-known Bayes rule for conditional change of measure.

Consider a sub -algebra of -algebra and an -measurable , integrable under the measures and , . We have the following result.

Proposition 1

(Bayes rule for conditional change of measure) When is -measurable

Proof. The RHS is by definition -measurable. Exploiting

for any

By definition of conditional expectation,

In our context, we have to compute

and we have

Thus

Noticing that is -measurable, we apply Proposition 1,

Now we analyze the behaviour of the underlying spread under

So is a -martingale under . If we assume

where is a standard brownian motion under and is the instantaneous volatility, we have the following Arbitrage-free Credit Index Option formula

| (29) |

We might have selected a different martingale dynamics, including any smile dynamics, since our results are completely general. We stick to lognormality for consistency with market standards in the pricing of credit options.

4.3 Numeraire Pricing

The -no-armageddon pricing measure introduced above is all we need for arbitrage-free pricing of Index Options. However, it has been defined only on and only -martingales have been considered for developing a pricing formula. This is a strong restriction if we want to extend the above results to more general products, that may depend on the joint dynamics of the Index spread and other quantities, or on the dynamics of the Index spread under different measures. Therefore it appears convenient to introduce an extension of to the global -algebra , and it would be particularly advantageous if this extension could be defined as a measure associated to a standard numeraire, as in Geman et al. (1996).

The -no-armageddon pricing measure introduced above has been defined and used in a way similar to the numeraire measures introduced by Geman et al. (1995) and Jamshidian (1997). However, it is not a numeraire measure, since the quantity used to define this measure is not the price of a tradable asset. In fact is an expectation with respect to , a filtration that does not include all available market information. This is why we went through such a detailed derivation.

For having a numeraire measure we need the Radon-Nikodym derivative to be defined using prices of tradable assets, which by no-arbitrage need to be expectation of -measurable claims. Such a definition implies all the properties typical of the numeraire measures, such as the fact that prices of tradable assets expressed in terms of a numeraire are -martingales under the associated measure.

The issue of extending a measure initially given on a subfiltration of the filtration , and to define this extension as a probability measure associated to a standard numeraire, is dealt with for the single name case by Jamshidian (2004). With reference to Jamshidian (2004) for details on the analytical derivations, in this section we briefly see how this extension can be performed for , adapting results to our context (therefore with stopping time replacing the single name stopping time ).

The quantity

where , is called prenumeraire. Notice it is a terminal payoff, corresponding to the index annuity observed at the terminal date in our time horizon. Notice that , the quantity we used for defining , is

Jamshidian (2004) now suggests to choose as a numeraire any claim such that its fair price is

| (30) |

and to define on a measure as

| (31) |

This is sufficient to define an associated probability measure such that its restriction to does not depend on the choice of as long as (30) is satisfied. This restriction, in particular, coincides with as defined on in Section 4.2, thus justifying the notation used (the easy proof is left to the reader). A very natural choice that we propose is to choose

With this choice, the Radon-Nikodym derivative of with respect to the risk neutral measure is

and trivially coincides with the Radon-Nikodym derivative computed in Section 4.2.

Following Theorem 3.8 in Jamshidian (2004), always with stopping time replacing the single name stopping time , one can check that, with this definition of the pricing measure, the pricing formula for an Index option coincides with (4.2), with the difference that now the pricing measure is defined by (31), rather than only the restriction defined by . The fundamental assumptions used by Jamshidian (2004) for proving this result are that the model is complementary, namely

and positive, namely

for any numeraire . Both properties are natural in our framework. Complementarity has already been explicitly assumed in the model definition, while positivity had been assumed only for the risk neutral measure, but can be with no harm extended to all numeraire measures.

Therefore in this setting the pricing formula (4.2) can be expressed through a global, numeraire-based measure.

5 Empirical Analysis

In the previous part of this work we have provided a rigorous theoretical framework for the pricing of Index options, that was missing in the market approach. This has led to replacing the market option formula (13) with the arbitrage-free option formula (29). In this section we point out that the improvement of the arbitrage-free option formula (29) on the market option formula (13) is not limited to the fact that (29) has a rigorous justification that lacked in the market approach.

Indeed, for options on particular portfolios, or for peculiar market situations, the correct accounting of the portfolio armageddon risk avoids painful mistakes in valuation. As a consequence of the crisis that struck credit markets in summer 2007, related to the burst of the subprime loans-linked structured finance bubble, the market is currently in one of those situations when the correct accounting of the portfolio armageddon risk is crucial. In the following empirical tests we consider market data of March 2007, before the subprime crisis, market data of August 2007, in the middle of the crisis, and finally more recent data of December 2007. We focus on options on the i-Traxx Europe Crossover index, that have a short maturity (less than one year) and have been particularly traded and liquid in recent years. Following the JPM quotation terminology, we name Call Options the options on the Receiver side (that allow an investor to be long on credit risk), and Put Options the options on the Payer side (that allow an investor to be short on credit risk).

5.1 The data

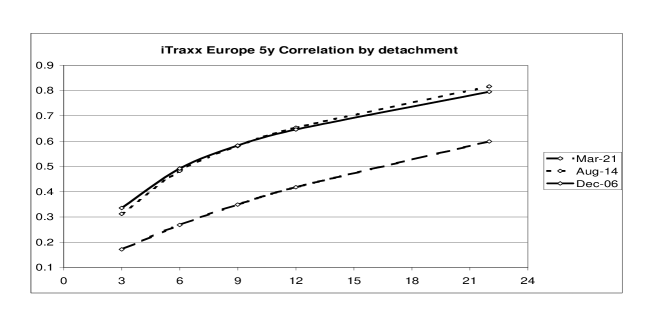

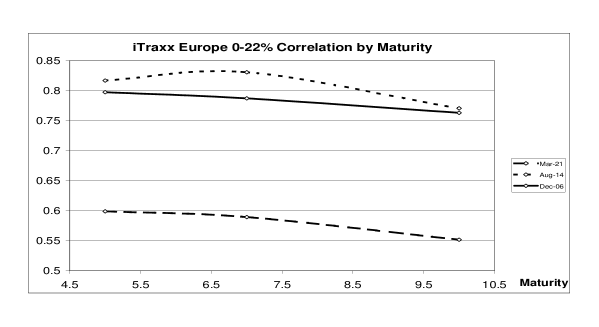

In Table 1 and in Figures 1 and 2 one sees market quotations for the main reference credit market products. Notice that they include information on Index Tranches, quoted through the so-called base correlation. In fact the arbitrage-free option formula (29) introduces an explicit dependence on default correlation information, that instead does not enter directly the market option formula (13).

This comes from the definition of the spread in (25) and from the component of the option price, that, under the assumption of independence of interest rate and default risk, is

It depends on the conditional -probability of a portfolio armageddon in given that there was no armageddon before . Ceteris paribus, an armageddon event will be more likely in a context of higher correlation. We have included also correlation information from the CDX (American) market, since the two credit markets have been historically very close.

|

||||||||||||||||||||

| Table 1: Credit market data (5y mat) on the 3 trading days considered. |

A brief explanation of the correlation quotation system, and of how it is used in market practice is here in order. The credit market associates to each portfolio tranche , with detachment expressed in percentage points, a correlation value , called base correlation. This value, together with the default intensities of the single names, allows to compute the price of a tranche with the market standard Gaussian Copula conventional model, for which we refer for example to Glasserman et al. (2007) and references therein. The fact that a single correlation is provided is a consequence of the homogeneous portfolio assumption, implying that all names in a portfolio have identical features, including equal interdependence across all couples of issuers in the pool. This provides a relatively easy and intuitive valuation and quotation method, that we comply with in the following. We may use some advanced loss model such as the GPL model of Brigo et al. (2006), able to calibrate consistently market tranches. We prefer to follow the Gaussian Copula since it is a recognized market standard.

For pricing i-Traxx Crossover Index Options we need computing probabilities, thus one needs the correlations associated to the most senior tranche possible: the one that is affected when, and only when, all portfolio issuers default. It is the tranche that covers losses from a fraction to a fraction of the portfolio notional. For the 50 name Crossover Index, with 40% recovery, these detachment points correspond to tranches where . We have two problems in terms of market availability of the data. First, market quotations are given only up to . Second, correlation is not quoted directly for the i-Traxx Crossover but only for the i-Traxx Main Index. When the correlation for a non-standard portfolio, or for a non-standard detachment, is not provided by the market, it is common practice (see Baheti and Morgan (2007)) to use interpolation/extrapolation and mapping techniques for obtaining these correlations from the array of available base correlations in Figure 1. However, due to lack of standardization and theoretical justification, we prefer to take a more conservative and robust approach, explained in the following.

It is market common agreement that correlation clearly increases with size of equity tranches, as one can see in Figure 1. In the i-Traxx market there is also a less marked tendency of correlation to decrease with maturity (see Figure 2). We are interested in tranches , with maturities lower than one year. Therefore, according to both market tendencies visible on iTraxx data, and in particular to the first one, we should consider a correlation higher than of Table 1, the i-Traxx correlation for the largest tranche and shortest maturity quoted. We may expect a correlation even higher than the highest level quoted by the CDX market, .

However we do not increase correlation further, but instead we consider a range of equally spaced correlations in-between the most senior base correlations of i-Traxx () and CDX (). Thus, while extrapolation would suggest, for the seniority we need, to increase correlation beyond any quoted , we limit this correlation to the market quoted CDX . This has two advantages. First we are robust towards a possible limit to the increase of correlation, due to the fact that the Crossover is a less senior Index.111As explained in Baheti and Morgan (2007), a less senior index such as the Crossover Index is more subject to idiosyncratic rather than systemic risk, thus correlation should be somewhat reduced. However, analysis of the most senior index in the North America market, the CDX.NA.IG, and the most junior, CDX.NA.HY, shows that this difference is very low for very senior tranches such as those we are interested in. Indeed, correlation is high for very senior tranches to represent that their risk is related mainly to systemic credit events. Such events, by definition, do not depend on the specific portfolio considered. Secondly, our choice tends to underestimate the probability of , compared to the standard market approach of extrapolating correlations. This implies also that, in the following tests, the difference between our arbitrage-free pricing of Index Options and the standard Market pricing is more likely to be underestimated, rather than overestimated.

5.2 Results: before and after the Subprime crisis

Consider now Tables 2 and 3, reporting our Credit Index option pricing results. In the upper subtables we see results for the 20 December 2007 maturity index option on March 21 2007. In the first row is the price of a standard Index Option using the market option formula (13). This price is fully consistent with market quotations, that include both a price quotation and an implied volatility quotation. From the implied volatility quotation one can compute the price through the market option formula (13), and check that it coincides with the price quotation.

Below is the price computed with the arbitrage-free option formula (29), using the same implied volatility provided by market quotations, and with the different correlation values considered.

The two formulas give very similar results, with differences around 1 bp or even lower. Such a difference does not appear to be relevant under a financial point of view, also considering that, as shown in Table 4, for the 20 December 2007 Index Option the upside part of the bid/offer spread (difference between ask price and mid price) for Put options is always more than bps and the downside part of the bid/offer spread (difference between mid price and bid price) for the Call option is smaller but in any case larger than bps. Notice that the upside part is the relevant one when the No-Arbitrage option overprices the market quotes, and viceversa. This appears to be a good estimate of the threshold over which a pricing difference starts to be financially relevant.

Now we move to August 14, 2007. We see in Table 1 that, although the pitch of the credit indices rally was already over (Crossover spread touched 463 bps at the end of July 2007), the market situation has changed radically compared to March 2007. Both Index spreads and Tranche correlations have dramatically increased.

Taking into account the new market conditions shown in Table 1, we evaluate a 9 month maturity option, thus corresponding to the option evaluated on March 21. Results are presented in the mid subtables of Tables 2 and 3. Here the difference between the price computed with the market option formula (13) and the price with the arbitrage-free option formula (29) is much larger. Looking at Call Options in Table 2, we see that the option with the lowest strike has a price with the arbitrage-free option formula (29) which is little more than a half of the price computed with the market option formula (13), because the perceived higher systemic risk, triggered by the subprime crisis, has made the risk-neutral probability of an armageddon event not negligible anymore.

The price differences appear particularly large, under a financial point of view, if compared to the values of Table 4, that reports the appropriate market bid-ask quotations for the longest maturity Index Options quoted in any of the three trading days considered. Indeed, for all strikes and all possible correlation values, the difference between market pricing and no arbitrage pricing is higher than the appropriate bid-ask spread.

Therefore taking correctly into account the possibility of portfolio armageddon is not only an issue that allows the definition of the spread and of the pricing measure to be regular under a mathematical point of view, but for options on the Crossover Index it is also of financial relevance in some peculiar market situations, such as the credit crunch of summer 2007.

| March 21, 2007 | ||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||

| August 14, 2007 | ||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||

| Dec 6, 2007 | ||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||

| Table 2: Prices in bps of Call Options on i-Traxx Crossover 5y On-the-Run. Maturity 9m |

| March 21, 2007 | ||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||

| August 14, 2007 | ||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||

| Dec 06, 2007 | ||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||

| Table 3: Prices in bps of Put Options on i-Traxx Crossover 5y On-the-Run. Maturity 9m. |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Table 4. Market Bid-Ask on quoted Index Options. |

For Put options of Table 3, price differences appear more moderate, since only for the highest correlation considered (corresponding to the CDX correlation222The correlation values we report for the CDX market on August and December 2007 may appear exceptionally high, however we point out that for CDX exceeded on the last trading week of November 2007.) the difference exceeds the relevant bid-ask, in spite of the fact that in some cases such differences are higher than 20 bps.

One may reasonably argue that the liquidity of the market in August 2007 was particularly low, and the situation, being the immediate aftermath of an unexpected crisis, was extremely peculiar and not likely to last for any relevant time or to appear again in the market.

In order to verify this argument, we wait until December 2007, and we price a 9-month option taking into account the December 06, 2007, market situation. The results appear to belie the above argument. In spite of the slightly lower Crossover spreads, the market still discounts a high perceived systemic risk, expressed by extremely high base correlation quotes. As a consequence, the correct accounting of the market-implied risk-neutral probability of a portfolio armageddon is still very relevant. This is shown both by Call prices, where the differences range from 15% to almost 60% of the Market Formula Price, and by Put quotations, where the number of cases when the difference between the two formulas exceeds the available bid-ask is even higher than in August 14. This relevant impact on option prices of the risk of a systemic crisis appears one of the possible reasons for the fact that the liquidity in the credit option market, after summer 2007, is concentrated on the shortest maturities.

We also mention that, although the historical probability of total portfolio default appears clearly negligible when we are considering large portfolios of investment grade issuers (such as the i-Traxx 125-name Main Index), there is evidence in the literature that also this risk is priced, so that its risk-neutral probability is not negligible. An example is in Brigo et al. (2006), where it is shown that the Generalized Poisson Loss Model needs to include a jump process associated to an armageddon event, if one wants to price correctly market tranches of different subordination and maturity written on the iTraxx Main Index.

Additionally, there is a category of credit portfolio options for which, even in normal market conditions, the probability of the portfolio to be wiped out by defaults is never negligible, even in normal market conditions: it is the case of Tranche options, in particular for the most risky equity or mezzanine tranches. For such options, that are often embedded in cancelable tranches, this issue is always crucial in all market situations. Thus, for an option on a Tranche, using a formula analogous to the arbitrage-free option formula (29) is fundamental for correct pricing in all market situations. Clearly, for a tranche option, the Tranched Loss

must replace the Loss and is the first time when .

6 Conclusion

In this work we have considered three fundamental problems of the standard market approach to the pricing of portfolio credit options: the definition of the index spread is not valid in general, the payoff considered leads to a pricing which is not defined in all states of the world, the candidate numeraire to define a pricing measure is not strictly positive, which would lead to an non-equivalent pricing measure.

We have given to the three problems a general mathematical solution, based on a novel way of modelling the flow of information through the definition of a new subfiltration. Using this subfiltration, we take into account consistently the possibility of default of all names in the portfolio, that is neglected in the standard market approach. We have shown that, while this mispricing can be negligible for standard options in normal market conditions, it can become highly relevant for less standard options or in stressed market conditions. In particular, we show on 2007 market data that after the subprime credit crisis the mispricing of the market formula compared to the no arbitrage formula we propose has become financially relevant even for the liquid Crossover Index Options.

The definition of an equivalent pricing measure through subfiltrations, and the related results on the dynamics of a well defined portfolio credit spread, lay the foundations of an extension to a multiname credit setting of the no-arbitrage approach known as Market Models, dating back to Brace, Gatarek and Musiela (1997) and Jamshidian (1997). Such extension is considered by Jamshidian (2004), Brigo (2005) and Brigo and Morini (2005) for the case of single name credit products. Here, instead, we consider the extension to a multiname setting, that is technically from the case of single name modelling, and also shows a different market applicability. In fact the Market Models approach is characterized by the fact of allowing precise arbitrage-free consistency in the modelling of market rates and spreads, and of requiring information on volatilities and correlations of such rates and spreads. These features have made the approach very successful in the interest rate derivatives market, but they hardly hold for single name credit derivatives, split among different reference with rare options. Instead, the reference iTraxx and CDX Indices now absorb the larger part of the credit derivative market, providing a reference market from which information for modelling market quantities can be extracted. Even after the credit spread rally in summer 2007, multiname indices experienced a return to trading activity while the single name credit market was still dried out.

References

- [1] Armstrong, A., and Rutkowski, M. (2007), Valuation of Credit Default Index Swaps and Swaptions. Working paper, UNSW.

- [2] Baheti, P. and Morgan, S. (2007), Base Correlation Mapping, Lehman Brothers Quantitative Credit Research, Vol. 2007 (1), pp. 3-20.

- [3] Brigo, D. (2005), Market Models for CDS Options and Callable Floaters, Risk Magazine, January issue.

- [4] Brigo, D. (2008), CDS Options through Candidate Market Models and the CDS-Calibrated CIR++ Stochastic Intensity Model. In: Wagner, N. (Editor), Credit Risk: Models, Derivatives and Management, Taylor & Francis, forthcoming.

- [5] Brigo, D., and Morini, M. (2005), CDS Market Models and Formulas, Proceedings of the 18th Annual Warwick Option Conference, September, 30, 2005.

- [6] Brigo, D., Pallavicini, A., and Torresetti, R, (2007), Calibration of CDO Tranches with the dynamical Generalized-Poisson loss model , Risk Magazine, May issue.

- [7] Bielecki T., Rutkowski M. (2001), Credit risk: Modeling, Valuation and Hedging. Springer Verlag.

- [8] Brace, A., D. Gatarek, and M. Musiela (1997), The market model of interest rate dynamics. Mathematical Finance, 7 , pp. 127–154.

- [9] Delbaen F., and Schachermayer W., (1994), A General Version of the Fundamental Theorem of Asset Pricing, Matematische Annalen, 300, pp.463-520.

- [10] Doctor, S., and Goulden, J. (2007), An Introduction to Credit Index Options and Credit Volatility, JPMorgan, Credit Derivatives Research, Vol. 2007.

- [11] Geman, H., ElKaroui, N., and Rochet, J.C. (1995), Changes of Numeraire, Changes of Probability Measure and Pricing of Options, Journal of Applied Probability 32, 443-458.

- [12] Glasserman, P., Kang, W., and Shahabuddin, P. (2007), Large Deviations in Multifactor Portfolio Credit Risk, Mathematical Finance 17 (3), pp 345-379.

- [13] Jackson, A. (2005) A New Mehtod for Pricing Index Default Swaptions, Proceedings of the 18th Annual Warwick Option Conference, September 30 2005, Warwick, UK.

- [14] Jamshidian, F.. (1997). Libor and swap market models and measures. Finance and Stochastics, 4, pp. 293–330.

- [15] Jamshidian, F. (2004). Valuation of Credit Default Swaps and Swaptions. Finance and Stochastics 8, 343-371.

- [16] Jeanblanc, M., and Rutkowski, M. (2000). Default Risk and Hazard Process. In: Geman, Madan, Pliska and Vorst (eds), Mathematical Finance Bachelier Congress 2000, Springer Verlag.

- [17] Lando, D. (1998) On Cox Processes and Credit Risky Securities, Derivatives Research, Vol. 2, , pp. 99-120.

- [18] Pedersen, C.M. (2003) Valuation of Portfolio Credit Default Swaptions, Lehman Brothers Quantitative Credit Research, Vol. 2003.

- [19] Schönbucher, P. (2000). A Libor market model with default risk, preprint.

- [20] Schönbucher, P. (2004). A measure of survival, Risk Magazine, January issue.