Uniform Time Average Consistency

of Monte Carlo Particle

Filters

Abstract.

We prove that bootstrap type Monte Carlo particle filters approximate the optimal nonlinear filter in a time average sense uniformly with respect to the time horizon when the signal is ergodic and the particle system satisfies a tightness property. The latter is satisfied without further assumptions when the signal state space is compact, as well as in the noncompact setting when the signal is geometrically ergodic and the observations satisfy additional regularity assumptions.

Key words and phrases:

nonlinear filter; uniform convergence; interacting particles; bootstrap Monte Carlo filter2000 Mathematics Subject Classification:

Primary 93E11; secondary 65C05, 65C35, 37L551. Introduction

Consider a hidden Markov model of the form

where , are independent i.i.d. sequences. The signal represents a dynamical process of interest, but only the noisy observations are available. More generally, may be any Markov process and are assumed to be conditionally independent given . Such models appear in a wide variety of applications (see, e.g., [11]). As the signal is not directly observed, one is generally faced with the problem of estimating the signal on the basis of the observations. To this end, the nonlinear filtering problem aims to compute the conditional distribution of the signal given the observation history in a recursive (on-line) fashion.

The theory of nonlinear filtering is a classic topic in probability [20] and statistics [2]. Unfortunately, the theory suffers in practice from the fact that the conditional distribution is an infinite dimensional object. With the exception of some special cases, the filtering recursion can not be represented in a finite dimensional fashion and its direct implementation is therefore intractable. For this reason, realistic applications have long remained limited.

This state of affairs was revolutionized in the early 1990s by the discovery [12] of a new class of approximate nonlinear filtering algorithms based on Monte Carlo simulation, which are known under various names in the literature: bootstrap filters, interacting particle filters, sequential Monte Carlo filters, etc. Such algorithms are simple to implement (even for complex models), are computationally tractable, typically exhibit excellent performance, and can be rigorously proved to converge to the exact nonlinear filter when the number of samples is large. These techniques have consequently been applied in problems ranging from robotics to finance, and their theoretical properties have been investigated by many authors; we refer to the collection [11] for a general introduction to the theory and applications of Monte Carlo particle filters, while a detailed overview of theoretical developments can be found in the recent monographs [6, 4].

Despite many advances in recent years, however, certain empirically observed properties of Monte Carlo particle filters remain poorly understood theoretically. The aim of this paper is to study one such property: the uniform nature of the particle filter approximation.

1.1. A toy example

The uniform nature of particle filter approximations is most easily illustrated by means of a simple but illuminating numerical example. Let us consider the filtering model

where are i.i.d. . As only the observations are available to us, we aim to compute the conditional mean of the signal . In this very special case, it is well known that the latter can be computed exactly using a finite dimensional algorithm (the Kalman filter).

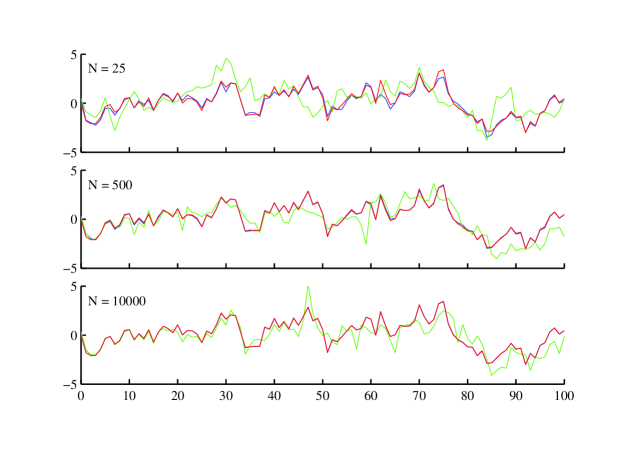

A numerical simulation of this example is shown in figure 1, where we have plotted the exact conditional mean and its approximation obtained by means of the bootstrap particle filter. For sake of illustration, we have plotted also a different ‘naive’ Monte Carlo approximation of the conditional mean which, like the bootstrap filter, is easily proved to converge to the exact conditional mean when the number of Monte Carlo particles is large. [The precise details of these algorithms will be given in section 3 below, and are irrelevant to the present discussion.] Though both algorithms converge, the difference in performance between the two algorithms is striking: the approximation error of the naive algorithm grows rapidly in time, while the error of the bootstrap algorithm appears to be independent of time (see [8] for further computations in this example).

Evidently the fact that both algorithms converge does not capture the key qualitative advantage of the bootstrap filter over the naive algorithm: the bootstrap filter converges to the exact filter uniformly in time, while the naive filter does not. Even if in practice the filter is only of interest on a finite time horizon, the rapid growth of the error of the naive filter is a severe problem as the filter becomes useless after relatively few time steps. In contrast, uniform convergence of the bootstrap filter indicates that its approximation error does not accumulate over time, which is essential for robust performance. It is therefore of considerable practical interest to establish under what conditions approximate filtering algorithms converge uniformly in time.

The linear example considered here is very special in that the filter can be computed exactly. One would therefore never use a particle filter in this setting. We have chosen an example which admits an exact solution as this provides a benchmark with which we can compare the performance of particle filter approximations. On the other hand, exactly the same phenomenon as is illustrated in figure 1 is observed numerically in almost any ergodic filtering problem. A general understanding of this phenomenon is therefore essential in order to guarantee reliable performance of approximate filtering algorithms in nonlinear filtering problems, which almost never admit an exact solution. The aim of this paper is to establish uniform convergence of approximate filtering algorithms, and in particular of particle filters, for a large class of ergodic filtering models.

In the following discussion we denote by the conditional distribution of given the observation history, and by its particle filter approximation with particles. Both are computed recursively, which we denote as and .

1.2. Previous work

Much of what is known about uniform convergence of the particle filter has its origins in the work of Del Moral and Guionnet [7], who established a fundamental connection with filter stability. The basic idea of this approach is as follows. The difference between the approximate and exact filter can be written as a telescoping sum (setting for simplicity )

Suppose the the filter is geometrically stable in the following sense:

| (1) |

where is a suitable norm on probability measures and , are constants. Then

where we have used the fact that one time step of the approximate filtering algorithm introduces an approximation error of order and that the sum over is uniformly bounded. Thus, evidently, the filter is uniformly convergent at a rate .

In order to establish the geometric stability property (1) of the filter, Del Moral and Guionnet impose the mixing assumption on the signal transition probabilities (for some constant and probability measure ) which was originally considered in the filter stability context by Atar and Zeitouni [1]. This is a very strong assumption, more stringent even than uniform ergodicity [21, theorem 16.0.2] of the signal process, and is very difficult to satisfy in practice particularly when the signal state space is not compact. Though various methods have been proposed to extend the class of models to which the mixing assumption is applicable, essentially all subsequent work on uniform convergence of the particle filter [18, 19, 24, 16, 23, 22] has ultimately relied on a form of this strong assumption. Unfortunately, the necessary assumptions are not satisfied in many (if not most) models encountered in applications, so that the practical applicability of the results established to date remains rather limited.

In a sense this conclusion is rather surprising, considering that significant progress has been made in recent years in the understanding of the filter stability problem (see [5] for an extensive review of this topic). For example, Kleptsyna and Veretennikov [15] have recently established geometric stability for a particular class of non-uniformly ergodic filtering models (see also [9, 10] for further variations of this approach), while it has been shown that qualitative stability as a.s. already holds under minimal ergodicity assumptions on the signal [29] or under no assumptions at all on the signal if the observations are informative [28]. The difficulty in applying such results to the uniform convergence problem is that the constants in (1) are independent of both the initial measures and the observation path , which is generally not the case when the signal is not uniformly ergodic. Despite the considerable progress on the filter stability problem, the results cited above provide little control over the dependence of the constant on the initial measures. This presents a significant hurdle in applying these results to the uniform convergence problem.

An entirely different approach for proving uniform convergence properties of particle filters was developed by Budhiraja and Kushner [3] by exploiting certain ergodic properties of nonlinear filters. Filter stability still plays an important role in establishing the ergodic theory, but only qualitative stability results are needed, in contrast with the quantitative control over the convergence rate and constants needed in the approach of Del Moral and Guionnet. Using the recent filter stability results established in [29], the necessary ergodic properties can now be established under extremely mild ergodic assumptions on the signal process. In this paper we revisit the approach of Budhiraja and Kushner and provide a new set of assumptions for the uniform time average convergence of bootstrap-type particle filters in the following sense ( is the dual bounded-Lipschitz norm):

It should be noted that the time average convergence is weaker than uniform convergence established by Del Moral and Guionnet; moreover, this approach does not supply a rate of convergence. On the other hand, we are able to demonstrate convergence for a class of non-uniformly ergodic signals which are presently still out of reach of the more quantitative theory.

1.3. Organization of the paper

In section 2 we introduce the basic nonlinear filtering problem. We then develop a general framework for uniform time average approximation of the nonlinear filter. In section 3 we introduce the bootstrap Monte Carlo filtering algorithm and discuss its basic properties. We show that the theory of section 2 can be applied to the bootstrap filter, provided that a suitable tightness property can be established. In section 4 we develop two classes of sufficient conditions for the requisite tightness property to hold. Both presume that the signal is geometrically ergodic, but different regularity assumptions on the observations are required in the two cases to complete the proof. Finally, appendix A recalls some basic facts about weak convergence, while most proofs in the text are postponed to appendix B.

2. A General Approximation Theorem

The purpose of this section is to introduce the nonlinear filtering problem, and to establish a general framework for its approximation uniformly in time average (not necessarily by a particle filter). The approach of this section follows closely the ideas of Kushner and Huang [17] and of Budhiraja and Kushner [3], but here we have significantly simplified the proofs, generalized the notion of convergence and eliminated some technical assumptions. Our treatment is mostly self-contained, but we have postponed the proofs to appendix B.

2.1. The hidden Markov model and nonlinear filter

Let and be Polish spaces endowed with their Borel -fields, let and be given transition probability kernels, and let be a given probability measure. We will work with random variables , defined on an underlying probability space , such that is a Markov chain with initial measure and transition probability , and such that are conditionally independent given with . Such a model can always be constructed in a canonical fashion, and is called a hidden Markov model with initial measure , transition kernel and observation kernel .

We will make the following nondegeneracy assumption on the observation kernel.

Assumption 1 (Nondegeneracy).

There is a -finite measure and a strictly positive measurable function such that

We now define the probability kernels and by the following recursion: for all and , we have

with the initial condition . Then it is well known that by the Bayes formula,

For notational convenience we will simply write and . The kernel is called the nonlinear filter and is the one step predictor associated with the hidden Markov model . Unfortunately, these infinite dimensional quantities are typically not explicitly computable. We aim to obtain a computationally tractable approximation.

2.2. Markov and ergodic properties

In the following, we denote by the space of probability measures on endowed with the topology of weak convergence of probability measures and the associated Borel -field. We define on the probability distances

where we have defined and is the Lipschitz constant of . The dual bounded-Lipschitz distance metrizes the weak convergence topology on , while the total variation distance is strictly stronger.

Let us recall that any probability kernel can equivalently be viewed as a -valued random variable on the measure space (see, e.g., [14, lemma 1.40]). In particular, we may consider the filter to be a -valued stochastic process adapted to the filtration . It is well known that this process possesses the Markov property, see, e.g., [26], and the associated ergodic theory will play a key role in the following.

Assumption 2 (Ergodicity).

is positive Harris recurrent and aperiodic, i.e., there is a (unique) -invariant measure such that as for every .

When assumption 1 holds, we may define the update map as

The following result collects the various properties of the filter that will be used below.

Proposition 2.1.

2.3. A general approximation theorem

As the filter can not be computed exactly in practice, we aim to approximate it by a sequence of computationally tractable approximate filters (), such that as . The goal of this section is to investigate what assumptions should be imposed on the filter approximations so that they converge to the exact filter uniformly in time average. We will subsequently apply this result to the setting where is a bootstrap type Monte Carlo particle filter with particles. However, the results of this section are general and could be applied to other types of filter approximation also.

We have seen in the previous section that is a -valued -adapted process, such that is Markov. We will consider approximate filters of a similar type, but we allow them to be adapted to a slighly larger filtration. This is needed to account for the random sampling step in Monte Carlo particle filters, which introduces additional randomness into the algorithm.

Assumption 3 (Approximation).

For every , the process satisfies the following.

-

(1)

is a -valued -adapted process, where is independent of .

-

(2)

is Markov with transition kernel and initial measure .

We obtain the following general approximation theorem.

Theorem 2.2.

Suppose that assumptions 1–3 hold. Moreover, we make the following one step convergence and tightness assumptions on the approximating sequence.

-

(1)

For any bounded continuous and , as , we have

In addition, we have as .

-

(2)

For any sequence as ,

Then the sequence converges to as uniformly in time average:

The proof of this theorem is given in appendix B.2.

Let us note that the uniform time average convergence guaranteed by the theorem allows us to answer related convergence questions as well. For example, we can prove that the time average mean square error of the estimates obtained from the approximate filter converges to the time average mean square error of the estimates obtained from the exact filter, uniformly in time.

Corollary 2.3.

Suppose that the assumptions of theorem 2.2 are satisfied. Then

for any bounded continuous function .

The proof is given in appendix B.3.

Remark 2.4.

Remark 2.5.

The tightness assumption. The second condition of theorem 2.2 ensures, roughly speaking, that the approximate filter does not lose mass to infinity after a long time (at least on average with respect to time and the observations). This is certainly the case for the signal itself by assumption 2, and this property is inherited by the exact filter by virtue of lemma A.2. Tightness of the approximate filter is not automatic, however, and needs to be imposed separately. Though this, too, is arguably a minimal assumption to ensure convergence of the approximate filters, the tightness property appears to be much more difficult to demonstrate in practice. Indeed, this is the main difficulty in applying theorem 2.2 to Monte Carlo particle filters.

An exception is the case where the signal state space is compact; we state this as a lemma, though the result is entirely obvious and requires no proof.

Lemma 2.6.

If is compact, then the second condition of theorem 2.2 is automatically satisfied.

In the compact setting, however, the generality of the ergodic assumption 2 is slightly misleading. Indeed, note that the first condition of theorem 2.2 implies that the signal transition kernel is Feller. Therefore, under the mild assumption that the support of the signal invariant measure has nonempty interior, compactness of the state space implies that the signal is even uniformly ergodic [21, theorem 16.2.5 and theorem 6.2.9]. Moreover, if we assume that is continuous for every (as we will do in order to prove the first condition of theorem 2.2), assumption 1 and compactness of implies that is bounded away from zero for every . In this setting, uniform convergence could be studied more directly using the techniques in [7].

When is not compact, a sufficient condition for tightness is the following.

Lemma 2.7.

If the family is tight, the second condition of theorem 2.2 holds.

We omit the proof, which is straightforward.

3. The Bootstrap Particle Filter

The practical problem in implementing the exact filter is that the conditional distribution is an infinite dimensional object. In applying the theory, one must therefore seek finite dimensional approximations. The idea behind particle filters is to approximate the nonlinear filter by atomic measures with a fixed number of particles , i.e., by measures in the space

Note that the filtering recursion does not naturally leave the set invariant; therefore, approximation is unavoidable. The bootstrap particle filter introduces an additional sampling step in the filtering recursion to project the filter back into the set .

To be precise, define the sampling transition kernel as

Then is the law of a -valued random variable that is generated as follows:

-

(1)

Sample i.i.d. random variables from .

-

(2)

Set .

We now introduce the transition kernel for the bootstrap particle filter as

and we define the initial measure for the bootstrap particle filter as

Note, in particular, that by construction and are supported on for any , so that the bootstrap particle filter is indeed finite dimensional in nature. Moreover, the law of large numbers strongly suggests convergence to the exact filter as at least on finite time intervals; we will make this precise below by verifying the first condition of theorem 2.2.

We have not yet introduced an explicit construction of the random variables on the probability space . However, as all our state spaces are Polish, it is a standard fact (e.g., along the lines of [14, proposition 8.6]) that the joint process can be obtained for any by a canonical construction, provided the probability space carries a countable family of i.i.d. -random variables independent of . The random variables provide the additional randomness introduced by the sampling steps in the bootstrap filtering algorithm, and the construction is such that is -adapted with . As it will not be needed in what follows, the construction of will be left implicit, but the details of the construction should be evident from the bootstrap filtering algorithm 1 (which is clearly very straightforward to implement in practice).

Remark 3.1.

A conceptually simpler naive particle filter could be constructed as follows. By the Bayes formula, the exact filter at time can be expressed as

Therefore, by the law of large numbers, we can approximate as follows:

where , are i.i.d. samples from the law of . Indeed, by the law of large numbers, this approximation is immediately seen to converge to the exact filter as . However, as can be seen in the numerical example in figure 1, the convergence is not uniform in time, and in fact the performance is quite poor (see [8] for a theoretical perspective).

Our aim is to prove that the bootstrap particle filter converges uniformly in time average. We will do this by verifying the conditions of theorem 2.2. Clearly assumption 3 holds by construction, while assumptions 1 and 2 on the filtering model will be presumed from the outset. We now show that the first condition of theorem 2.2 holds under a mild continuity assumption on the filtering model. Tightness is a much more difficult problem, and will be tackled in the next section.

Assumption 4 (Continuity).

The following hold:

-

(1)

is Feller, i.e., is continuous;

-

(2)

For every , the map is continuous and bounded.

Proposition 3.2.

4. Sufficient Conditions for Tightness

By corollary 3.3, all that remains to prove in order to establish uniform time average consistency of the boostrap particle filter is the tightness of particle system generated by the algorithm—i.e., we must rule out the possibility that the particle system loses mass to infinity after running for a long time. It seems intuitively plausible that this can be proved under rather general conditions, as both the signal and filter are already ergodic (see assumption 2 and [29]) and the sampling step in the bootstrap algorithm does not change the center of mass of the filter.

Unfortunately, the tightness problem appears to be much more difficult than one might expect. A rather ominous counterexample in a different setting [25] shows that, contrary to intuition, arbitrarily small perturbations may cause a Markov chain to become transient (and hence lose its tightness property) even when the unperturbed chain is geometrically ergodic. Though the implications to the present setting are unclear, such examples suggest that the problem may be delicate and that tightness can not be taken for granted. In this section, we will provide two sets of general sufficient conditions under which tightness can be verified for the bootstrap particle filter. Both sets of conditions require geometric ergodicity of the signal (which is stronger than assumption 2), and each imposes a different set of restrictions on the observation structure.

Remark 4.1.

Assumptions 1, 2, and 4 are very mild and are satisfied by the majority of ergodic filtering problems. In contrast, the sufficient conditions for tightness below are rather restrictive, and in this sense our results are not entirely satisfactory—establishing tightness under minimal ergodicity and observation assumptions remains an open problem. Nonetheless, the tightness property is purely qualitative and thus appears to be significantly more tractable than the quantitative controls required in other approaches to the uniform convergence problem (indeed, the general conditions imposed below are still out of reach of other approaches). Another interesting possibility is that tightness might be achieved by introducing suitable modifications to the bootstrap filtering algorithm, e.g., by means of a periodic resampling scheme or using some form of regularization.

Let us briefly recall the relevant notion of geometric ergodicity. A function is said to possess compact level sets if the set is compact for every . Given such a function , we define the -total variation distance between as

We will call the Markov chain geometrically ergodic if there is a function with compact level sets, a -invariant measure , and constants and such that

Note that geometric ergodicity is strictly stronger than assumption 2. Geometric ergodicity is often easily verified in terms of Lyapunov-type conditions on the transition kernel and is satisfied in many practical applications; see the monograph [21] for an extensive development of this theory.

4.1. Case I: bounded observations

We will first consider the following assumptions.

Assumption 5 (Tightness: Case I).

The following hold.

-

(1)

The signal is geometrically ergodic (, has compact level sets).

-

(2)

There exist strictly positive functions such that

Assumption 5 is typically satisfied when the observations are of the additive noise type with a bounded observation function. As an example, consider the observation model on the observation state space , where are i.i.d. -random variables independent of for some strictly positive covariance matrix , and is a continuous and bounded observation function. Then we can set

and assumptions 1 and 4 are clearly satisfied for this observation model. Moreover, evidently

where , satisfy the requirement in assumption 5.

4.2. Case II: strongly unbounded observations

To satisfy assumption 5, the observation function will generally need to be bounded. Our second set of assumptions is essentially the opposite scenario: we consider an observation model where is strongly unbounded, i.e., converges to infinity in every direction (the requirement below that has compact level sets).

Assumption 6 (Tightness: Case II).

Let , and suppose that where are i.i.d. random variables independent of . We assume the following:

-

(1)

The signal is geometrically ergodic (, has compact level sets).

-

(2)

, are continuous, for some .

-

(3)

The law of the observation noise has a strictly positive, bounded and continuous density with respect to the Lebesgue measure on .

-

(4)

There is a nonincreasing , a norm on , and such that

-

(5)

There are constants , , and with , such that

Remark 4.2.

Note that when assumption 6 is satisfied, we may always choose to be the Lebesgue measure and , which is strictly positive and is bounded and continuous for every . We therefore automatically satisfy assumption 1 and the observation part of assumption 4. Moreover, geometric ergodicity implies that assumption 2 holds also. Finally, note that as is by definition presumed to have compact level sets, the assumption implies that has compact level sets also, i.e., is strongly unbounded.

A typical example where assumption 6 is satisfied is the following. Let , and consider the observation model where for some strictly positive covariance matrix , and where is bi-Lipschitz (i.e., it is Lipschitz, invertible, and its inverse is Lipschitz) and is a bounded continuous function. Moreover, assume that the signal is geometrically ergodic where satisfies the growth condition for some . Let us verify the requirements of assumption 6 in this setting.

First, the law of has a density with respect to the Lebesgue measure. Therefore is bounded, continuous, and strictly positive, and we may evidently set (which defines a norm), (which is nonincreasing), and . Moreover, it is easily established that

where we have used that for some by the bi-Lipschitz property of . We may therefore estimate

where we have written for (one can choose ) and . Finally, as any Gaussian has finite moments, .

4.3. Uniform time average consistency

We have now introduced two sets of assumptions on the filtering model. Our main result states that either of these assumptions is sufficient for uniform time average consistency of the bootstrap particle filter.

Theorem 4.3.

The proof is given in appendix B.5.

Appendix A Some Basic Facts on Weak Convergence

The purpose of this appendix is to recall some basic facts on weak convergence of probability measures and transition kernels that are particularly useful in the setting of this paper.

A.1. Weak convergence of kernels

We begin by showing that weak convergence of transition probability kernels, in a sufficiently strong sense, can be iterated.

Lemma A.1.

Let , be a sequence of transition kernels on a Polish space , and let be another such kernel. Then for every bounded continuous

if and only if for any , we have as whenever .

Proof.

The if part follows trivially by choosing , , and . To prove the only if part, suppose we have established that the result holds for . Then it clearly holds also for . By induction, it therefore suffices to consider the case .

As , we can construct using the Skorokhod representation theorem a sequence of random variables a.s. such that , . Let be bounded and continuous, and note that and . But by our assumption a.s., so the claim follows immediately using dominated convergence. ∎

A.2. Tightness of random measures

As many of the stochastic processes in this paper are measure-valued, we require a simple condition for tightness of a family of measure-valued random variables. The following necessary and sufficient condition is quoted from [13, corollary 2.2]. As usual, if is a -valued random variable, we denote by the probability measure defined by for all . Note that this is the barycenter of .

Lemma A.2.

Let be a family of -valued random variables on . Then this family is tight if and only if the family of probability measures is tight.

A.3. Tightness in product spaces

The following elementary lemma will be used repeatedly.

Lemma A.3.

Let be a family of probability measures on , where are Polish. Then this family is tight iff its marginals and are tight.

The proof is straightforward and follows along the lines of [27, lemma 1.4.3].

Appendix B Proofs

This appendix contains the proofs that were omitted from the main text.

B.1. Proof of Proposition 2.1

Note that is a function of only. Therefore

where we have used the hidden Markov property and . Using the Markov property of and the tower property of the conditional expectation, we obtain

As , the expression for follows immediately. The expression for the initial measure follows along similar lines.

Ergodic property: We begin by proving existence of the invariant measure. Consider a copy of the hidden Markov model started at the stationary distribution . Using stationarity, the process can be extended to negative times also. Now consider the measure-valued process (the regular conditional probability always exists in a Polish state space). It is easily seen that this is a stationary Markov process with transition kernel . Thus the law of is an invariant measure for .

It remains to establish uniqueness of the invariant measure. Endow the Polish space with the Polish metric , where is a Polish metric on . In lemma B.1 below, it is shown that assumption 2 implies that

whenever is -Lipschitz. Let and be two -invariant measures. Then the marginals of and on the signal state space are invariant measures for . But assumption 2 implies that is the unique invariant measure for the signal, so we must have . By the Polish assumption, we therefore have the disintegrations

It follows that

whenever is uniformly bounded and -Lipschitz. But this class of functions is measure determining, so and must coincide. The proof is complete. ∎

Lemma B.1.

Proof.

Consider a copy of the hidden Markov model started at the initial measure , and define recursively and , with and . Then for , the measure coincides with the law of , and similarly coincides with the law of . Thus

But assumptions 1 and 2 allow us to apply the filter stability result [29, corollary 5.5], which implies that as . This completes the proof. ∎

B.2. Proof of Theorem 2.2

The proof of theorem 2.2 proceeds in several steps. Throughout this section (appendix B.2) we always presume that the assumptions of theorem 2.2 are in force.

We begin by proving that the convergence holds on every finite time horizon.

Lemma B.2.

for any and bounded continuous .

Proof.

As is independent of , we can write . Therefore

where we have used assumption 3 and the tower property of the conditional expectation. Define the bounded continuous function as . By lemma A.1 and the first condition of theorem 2.2, we have as . Therefore

Substituting in the above expression completes the proof. ∎

We now strengthen this lemma to prove -convergence.

Lemma B.3.

for any .

Remark B.4.

The quantity is well defined, as is measurable by [30, corollary A.2]. We will therefore employ such expressions in the following without further comment.

Proof.

Fix . As takes values in the Polish space , there exists a compact subset such that . Moreover, by the Arzelà-Ascoli theorem, there is an and such that whenever . Define the open set . Then for any , so

As is closed and by lemma A.1 and the first condition of theorem 2.2, applying the Portmanteau theorem to the second term and lemma B.2 to the first term gives

But was arbitrary, so the proof is complete. ∎

We have now established convergence of the filters as for a fixed time . The idea is now to repeat the proofs for the case where we let the number of particles and time go to infinity simultaneously. We will repeat almost identically the steps used in the last two lemmas, where the finite time weak convergence used in the proofs is replaced by the following ergodic lemma (recall that is the unique invariant measure of ).

Lemma B.5.

For any sequence as , define the probability measures

for every . Then as .

Proof.

We first show that the family is tight. It suffices to show that the marginals are tight by lemma A.3. But the first marginal of is , which converges to the signal invariant measure by assumption 2. This establishes tightness of the first marginal. By lemma A.2, tightness of the second marginal follows from the second condition of theorem 2.2.

Having established tightness, it remains to show that every convergent subsequence of converges to . In fact, it suffices to show that the limit of every convergent subsequence must be an invariant measure of , as the latter is unique by proposition 2.1.

Lemma B.6.

For any sequence as ,

for any bounded continuous function .

Proof.

As in the proof of lemma B.2, we can write

where . By lemma B.5

where we have used the expression for in terms of the stationary copy given in the proof of proposition 2.1. The proof would evidently be complete if we can show that

To this end, we proceed as follows. First, note that

where we have used the tower property of the conditional expectation and Jensen’s inequality. But by the Markov property of , we can write

where the function does not depend on . Using assumption 2, it follows easily that

But , so by the Markov property of

for all . Letting in this expression and using that

by [29, theorem 4.2] (which holds by virtue of assumptions 1 and 2), the proof is complete. ∎

Lemma B.7.

For any sequence as ,

Proof.

Fix , and choose a compact subset such that . Construct and as in the proof of lemma B.3. Then we can estimate

Applying lemma B.6 to the first term, lemma B.5 and the Portmanteau theorem to the second term, and assumption 2 to the third term, we find that

But was arbitrary, so the proof is complete. ∎

We can now complete the proof of theorem 2.2.

Proof of Theorem 2.2.

Suppose that

Then we can find subsequences and such that

Suppose first that is a bounded sequence. Then lemma B.3 gives

so we have a contradiction. But if is an unbounded sequence, we can find a further subsequence such that , and by lemma B.7

which is again a contradiction. The proof is complete. ∎

B.3. Proof of Corollary 2.3

Note that we can estimate

The result is now easily obtained by following the same steps as in the proof of theorem 2.2. ∎

B.4. Proof of Proposition 3.2

We begin by proving a general continuity result for .

Lemma B.8.

as whenever as .

Proof.

It follows immediately from the definition that the barycenter of is for any . Therefore, by lemma A.2, the sequence is tight. It thus suffices to prove that every convergent subsequence converges to . Let be any subsequence such that for some . Note that for any probability measure

In particular, this shows that

for any bounded continuous function . Thus we must have . ∎

We can now complete the proof.

Proof of Proposition 3.2.

As is bounded and continuous (assumption 4), we have

for every whenever is bounded and continuous and . This implies that for every , so in particular is bounded and continuous for every whenever is a bounded continuous function. Using the Feller property of and lemma B.8, it follows that whenever and

for every and bounded continuous function . But then we obtain by dominated convergence

It remains to show that . This follows immediately, however, from lemma B.8, the fact that is continuous, and dominated convergence. The finite time convergence now follows from lemma B.3 (which does not rely on assumption 2), and the proof is complete. ∎

B.5. Proof of Theorem 4.3

As both assumptions require geometric ergodicity, we fix throughout the corresponding function (which, by definition, is presumed to have compact level sets). To complete the proof, it only remains to prove the tightness assumption of corollary 3.3. We will in fact verify the simpler sufficient condition in lemma 2.7 through the following elementary result.

Lemma B.9.

Suppose that . Then the tightness assumption holds.

Proof.

In the following, it is convenient to introduce the measure-valued process

so that . Note that is the bootstrap particle filter approximation to the one step predictor (in fact, our main results are easily adapted to establish uniform time average convergence of to ). The following result is the key tool that allows us to establish tightness. The condition of this lemma—essentially, the requirement that the update step does not ‘expand’ too much—will be verified separately under the assumptions 5 and 6.

Lemma B.10.

Suppose the signal is geometrically ergodic and . If there exist constants such that for all , then .

Proof.

Note that for all . Therefore

But note that , as we may average over the last sampling step. Therefore

As the signal is assumed geometrically ergodic, we have and

for some constants , . In particular, we find that for any measures

Therefore we can estimate

In particular, we find that

By the assumption of the lemma we now obtain

But as , so . By lemma B.11 below

But as , the proof is evidently complete. ∎

In the previous proof, we needed the following.

Lemma B.11 (Discrete Grönwall).

Suppose , are nonnegative scalars such that

Then it must be the case that

Proof.

As , it suffices to prove the first inequality in

We proceed by induction. Clearly the statement is true for . Now suppose we have verified the statement for all . Then by assumption

But the rightmost expression is evidently a telescoping sum which reduces to

The proof is complete. ∎

It remains to show that . Here we distinguish between the two separate cases of assumptions 5 and 6. The results below complete the proof of theorem 4.3.

B.5.1. Case I

In the setting of assumption 5, the result is straightforward.

Proof.

Note that

We may therefore estimate

Taking the expectation of both sides completes the proof. ∎

B.5.2. Case II

In the setting of assumption 6 we will need the following result, whose proof we recall for the reader’s convenience, to control the growth of the update step.

Lemma B.13 (Chebyshev’s covariance inequality).

Let be nondecreasing functions and let be any probability measure on . Then

i.e., the covariance of and is always nonnegative.

Proof.

Note that

But by our assumptions the integrand is nonnegative, and the result follows. ∎

We obtain the following result.

Lemma B.14.

Suppose that assumption 6 holds and . Then .

Proof.

We choose to be the Lebesgue measure and . Note that

As all finite dimensional norms are equivalent, we have for all and some . Using where , we can therefore estimate

In particular, using that , we find

But is nonincreasing and is nondecreasing, so by lemma B.13

Now note that

Substituting in the above expression, we obtain

Finally, note that

which is bounded uniformly in by our assumptions. Therefore

which completes the proof. ∎

References

- [1] R. Atar and O. Zeitouni. Exponential stability for nonlinear filtering. Ann. Inst. H. Poincaré Probab. Statist., 33(6):697–725, 1997.

- [2] L. E. Baum, T. Petrie, G. Soules, and N. Weiss. A maximization technique occurring in the statistical analysis of probabilistic functions of Markov chains. Ann. Math. Statist., 41:164–171, 1970.

- [3] A. Budhiraja and H. J. Kushner. Monte Carlo algorithms and asymptotic problems in nonlinear filtering. In Stochastics in finite and infinite dimensions, Trends Math., pages 59–87. Birkhäuser Boston, Boston, MA, 2001.

- [4] O. Cappé, E. Moulines, and T. Rydén. Inference in hidden Markov models. Springer Series in Statistics. Springer, New York, 2005.

- [5] D. Crisan and B. Rozovsky, editors. The Oxford University Handbook of Nonlinear Filtering. Oxford University Press, 2009. To appear.

- [6] P. Del Moral. Feynman-Kac formulae. Probability and its Applications (New York). Springer-Verlag, New York, 2004. Genealogical and interacting particle systems with applications.

- [7] P. Del Moral and A. Guionnet. On the stability of interacting processes with applications to filtering and genetic algorithms. Ann. Inst. H. Poincaré Probab. Statist., 37(2):155–194, 2001.

- [8] P. Del Moral and J. Jacod. Interacting particle filtering with discrete-time observations: asymptotic behaviour in the Gaussian case. In Stochastics in finite and infinite dimensions, Trends Math., pages 101–122. Birkhäuser Boston, Boston, MA, 2001.

- [9] R. Douc, G. Fort, E. Moulines, and P. Priouret. Forgetting the initial distribution for hidden Markov models. Stochastic Process. Appl., 119:1235–1256, 2009.

- [10] R. Douc, E. Gassiat, B. Landelle, and E. Moulines. Forgetting of the initial distribution for non-ergodic hidden Markov chains. Ann. Appl. Probab., 2009. To appear.

- [11] A. Doucet, N. de Freitas, and N. Gordon, editors. Sequential Monte Carlo methods in practice. Statistics for Engineering and Information Science. Springer-Verlag, New York, 2001.

- [12] N. J. Gordon, D. J. Salmond, and A. F. M. Smith. Novel approach to nonlinear/non-Gaussian Bayesian state estimation. Radar and Signal Processing, IEE Proceedings F, 140:107–113, 1993.

- [13] A. Jakubowski. Tightness criteria for random measures with application to the principle of conditioning in Hilbert spaces. Probab. Math. Statist., 9(1):95–114, 1988.

- [14] O. Kallenberg. Foundations of modern probability. Probability and its Applications (New York). Springer-Verlag, New York, second edition, 2002.

- [15] M. L. Kleptsyna and A. Y. Veretennikov. On discrete time ergodic filters with wrong initial data. Probab. Theory Related Fields, 141(3-4):411–444, 2008.

- [16] H. R. Künsch. Recursive Monte Carlo filters: algorithms and theoretical analysis. Ann. Statist., 33(5):1983–2021, 2005.

- [17] H. J. Kushner and H. Huang. Approximate and limit results for nonlinear filters with wide bandwidth observation noise. Stochastics, 16(1-2):65–96, 1986.

- [18] F. Le Gland and N. Oudjane. Stability and uniform approximation of nonlinear filters using the Hilbert metric and application to particle filters. Ann. Appl. Probab., 14(1):144–187, 2004.

- [19] F. LeGland and N. Oudjane. A robustification approach to stability and to uniform particle approximation of nonlinear filters: the example of pseudo-mixing signals. Stochastic Process. Appl., 106(2):279–316, 2003.

- [20] R. S. Liptser and A. N. Shiryayev. Statistics of random processes. I. Springer-Verlag, New York, 1977. General theory, Translated by A. B. Aries, Applications of Mathematics, Vol. 5.

- [21] S. P. Meyn and R. L. Tweedie. Markov chains and stochastic stability. Communications and Control Engineering Series. Springer-Verlag London Ltd., London, 1993.

- [22] J. Olsson, O. Cappé, R. Douc, and E. Moulines. Sequential Monte Carlo smoothing with application to parameter estimation in nonlinear state space models. Bernoulli, 14(1):155–179, 2008.

- [23] J. Olsson and T. Rydén. Asymptotic properties of particle filter-based maximum likelihood estimators for state space models. Stochastic Process. Appl., 118(4):649–680, 2008.

- [24] N. Oudjane and S. Rubenthaler. Stability and uniform particle approximation of nonlinear filters in case of non ergodic signals. Stoch. Anal. Appl., 23(3):421–448, 2005.

- [25] G. O. Roberts, J. S. Rosenthal, and P. O. Schwartz. Convergence properties of perturbed Markov chains. J. Appl. Probab., 35(1):1–11, 1998.

- [26] Ł. Stettner. On invariant measures of filtering processes. In Stochastic differential systems (Bad Honnef, 1988), volume 126 of Lecture Notes in Control and Inform. Sci., pages 279–292. Springer, Berlin, 1989.

- [27] A. W. van der Vaart and J. A. Wellner. Weak convergence and empirical processes. Springer Series in Statistics. Springer-Verlag, New York, 1996. With applications to statistics.

- [28] R. van Handel. Discrete time nonlinear filters with informative observations are stable. Electr. Commun. Probab., 13:562–575, 2008.

- [29] R. van Handel. The stability of conditional Markov processes and Markov chains in random environments. Ann. Probab., 2009. To appear.

- [30] R. van Handel. Uniform observability of hidden Markov models and filter stability for unstable signals. Ann. Appl. Probab., 19:1172–1199, 2009.