Mechanisms of Self-Organization and Finite Size Effects in a Minimal Agent Based Model

Abstract

We present a detailed analysis of the self-organization phenomenon in which the stylized facts originate from finite size effects with respect to the number of agents considered and disappear in the limit of an infinite population. By introducing the possibility that agents can enter or leave the market depending on the behavior of the price, it is possible to show that the system self-organizes in a regime with a finite number of agents which corresponds to the stylized facts. The mechanism to enter or leave the market is based on the idea that a too stable market is unappealing for traders while the presence of price movements attracts agents to enter and speculate on the market. We show that this mechanism is also compatible with the idea that agents are scared by a noisy and risky market at shorter time scales. We also show that the mechanism for self-organization is robust with respect to variations of the exit/entry rules and that the attempt to trigger the system to self-organize in a region without stylized facts leads to an unrealistic dynamics. We study the self-organization in a specific agent based model but we believe that the basic ideas should be of general validity.

1 Introduction

In this paper we discuss in detail the self-organization phenomenon which

emerges in the minimal Agent Based Model (ABM) we have introduced in [1, 2, 3].

This model has the great advantage to be

simple, mathematically well posed and able to reproduce the stylized facts (SF), i.e. the

empirical evidences of real markets [4, 5, 6].

In this respect it can be considered

a “workable model” for which analytical approaches are possible in some cases

and it can be easily modified to introduce variants and elements of realism.

We consider a population of heterogeneous interacting agents whose

strategies are divided in two main classes: fundamentalist and chartist.

Fundamentalist agents believe that the market is stable and fluctuates around a fair value, the fundamental price , that they

estimate by standard economic arguments. The fundamentalist strategy acts in a way to drive

the price towards the fundamental value.

Chartist agents instead try to detect local trends in the market by evaluating the price history.

They try to speculate betting on these trends and so they contribute to the formation of bubbles and crashes.

Agents can change their strategy during the dynamics by following some personal considerations or by imitating other agents behavior (herding).

It is possible to see that, by considering a given finite number of agents, the dynamics shows

an intermittent behavior. This means that

the market is assumed to be dominated by fundamentalists at large times

but bursts of chartists can appear spontaneously leading to high volatility.

In principle the basic assumption of large time stability can be removed

if one would like to consider particularly turbulent situations but in the present study we will

only refer to the simple case mentioned before.

The intermittent behavior is present only for a particular value of the number of agents

and it disappears in the limit of infinite agents.

This phenomenon has been already observed in other similar models

but it has been interpreted as a negative element.

Here we present a completely different perspective by showing that

the finite number of agents necessary to produce the SF is not an artificial feature of the model

to be eliminated.

On the contrary this finite size effect results to be the natural outcome of a process of

self-organization.

The basic concept is that the self-organization can be triggered by leaving the agents

the possibility to enter or exit the market following a mechanism based on a feedback on the

price behavior.

This mechanism encourages agents to enter the market if they perceive an interesting movement

in the price.

On the other hand a very stable market where nothing happens is not appealing for speculators

who are likely to abandon such a market.

From an economic point of view a very stable market can be attractive for some

particular agents who only look for the conservation of their wealth,

but these will not contribute to the SF and are irrelevant with respect to our

discussion.

This dynamics for the agents is implemented by introducing two suitable thresholds which agents consider to decide to enter or leave the market by comparing them with the price movement.

By considering

various initial situations with different starting number of agents

we can observe that the resulting dynamics stabilizes around a finite number of agents

which is the one corresponding to the SF.

This phenomenon corresponds to the self-organization of the system in a state dominated by an intermittency due to finite size effects.

In this respect it is not a case of self-organized criticality [7, 8] but rather of self-organized intermittency.

The fact that real agents can be scared by a market that is too volatile may appear

at first sight problematic with respect to our criteria to enter or exit the market.

This point requires a clarification of the time scales involved.

For a market to be attractive, there has to be some price movement at a relatively

long time-scale corresponding to the operation performed.

On the other hand volatility at shorter time-scales

may indeed appear as a disturbance for an agent.

We have checked this point by analyzing the volatility also at short time-scale

and considering this as a discouraging element for the agents.

The general result is that the introduction of this additional and realistic element

does not modify appreciably the phenomenon of self-organization discussed before.

We have also checked the robustness of the self-organization mechanism along various directions.

For example it is possible to see that

if one tries to force the system to self-organize in a state without the SF

one meets unrealistic scenarios.

In summary we propose a simple mechanism for the agents’ dynamics which is able to explain why real

markets self-organize in a state corresponding to the SF.

This mechanism is based on the idea that speculative agents dislike a too stable market and prefer

to bet on price movements which they interpret as opportunities to exploit

following their strategies.

This mechanism is stable and does not contradict the natural fear of real traders to enter

in risky, highly fluctuating markets with respect to shorter time-scales.

The paper is organized in the following way.

In section 2 we give a schematic description of the ABM introduced in [1, 2, 3].

In section 3 we discuss the basic mechanisms which lead to the self-organization towards

the region with intermittent dynamics and SF.

We also consider some variants and check the stability of the mechanism.

In section 4 we propose a more realistic generalization of the model with two temporal horizons to define the entry/exit strategies of the agents. In this way we can include the tendency of real traders to be scared by a noisy market and show that this does not interfere with the self-organization.

In section 5 the conclusions are drawn and we also outline some possible perspectives

of the present study.

2 The Minimal Agent Based Model in a Nutshell

The mathematical framework

which we consider to study the self-organization mechanism

is the minimal ABM we have introduced in [1, 2, 3]. This ABM is composed of agents that can be chartists () or fundamentalists () and clearly .

The novelty of this model, which makes it a workable tool

to consider a variety of questions, is a simplification of the elements to those which are strictly essential.

In addition the equations for the dynamical evolution are mathematically well posed and general

without any ad hoc assumption [9, 10, 11].

The chartists are recognized as destabilizing agents and an efficient way to describe them is represented by the potential method introduced in

[12, 13, 14, 15].

The action of these investors can be described, in the simplest case, in terms of a repulsive force proportional to the distance between the current price and a suitable moving average .

On the other hand the fundamentalists believe in a fundamental price and bet on a reverting trend towards this value. A simple way to mimic their action is to define an AR(1) process where plays the role of an attractor.

We now assume that the price formation can be described in term of a linearized Walras’ mechanism (i.e. where ) and the complete equation of price dynamics is consequently,

| (1) |

For the sake of simplicity we set , which are respectively the strength of fundamentalist action, of the chartist action and the memory of the moving average. The term is the white noise whose amplitude is fixed by .

The key element of the model is the dynamics of the evolution of the strategies. Here we use the simplified version of the probability of switching a strategy that models only an asymmetric herding effect.

This asymmetry guarantees that fundamentalists will prevail at very long times

(for a more detailed discussion see [1, 2]),

| (2) |

| (3) |

where and are respectively the probability of becoming fundamentalist being chartist and the probability of becoming chartist being fundamentalist. The parameter prevents the dynamics to be captured indefinitely by the absorbing states and . We set with in order to be able to vary the number of agents without quitting the region of parameters in which the probability density function of the population is bimodal [1, 2, 16, 17].

Further and more exhaustive discussions about the intermittent behavior of the population dynamics, the origin of the volatility clustering and in general about the statistical properties of the model can be found in [1, 2, 3].

3 Basic mechanism for the self-organization

3.1 Self-organized intermittency

Eqs. 2 and 3 define the dynamics of and . If we consider

the variable it is possible to see that the distribution

of depends explicitly on the value of the total number of agents active in the market [1, 2].

In particular when is very large

the transition probability from fundamentalist to chartist becomes asymptotically small

and essentially the system becomes frozen in the fundamentalist state.

The resulting price dynamics is then extremely stable

due to the stabilizing effect of fundamentalists.

Clearly such a state does not show the anomalous fluctuations corresponding to the SF.

This means that in the limit of an infinite size system the resulting dynamics looses the interesting properties which lead to the formation of the SF.

This is different from what happens in the majority of physical models where the interesting (critical)

phenomena appear in the thermodynamic limit.

The opposite happens in the limit of very small where the population of agents

undergoes very fast changes of strategy and the resulting dynamics is too schizophrenic.

Only for an intermediate number of agents (the specific value depending on the other model parameters)

one can recover the intermittent dynamics of the changes of strategy which leads to the SF.

Of course this situation leads to the basic question of understanding the driving mechanism

which makes real markets self-organize in the intermittent state with a finite number of agents.

The first consideration in this respect is that the number of agents

should be itself a fluctuating variable and not a fixed parameter of the model.

This implies the identification of a mechanism which rules the decision of agents to enter or leave the market

depending on the price behavior.

The idea is that traders are usually attracted to enter in the market if they

detect an interesting signal

in the price behavior which usually is an appreciable movement of the price.

Otherwise, if the market is too stable, no gain opportunities appear and traders leave the market.

We would like to stress that both chartist and fundamentalist agents described in our model are a kind of speculative traders in the sense that they try to profit by betting in future movements of the price.

The behavior of extremely conservative investors

who appreciate a completely stable situation

is not part of this scheme because they do not contribute to the fluctuations leading to the SF.

The price movements which are attractive to agents are estimated in our model by considering a

long-term () estimation of the standard deviation of the price,

| (4) |

This quantity is the one agents consider to decide to enter or leave the market. If is small agents leave the too stable market where no profit opportunities appear. Otherwise if is sufficiently large then significant movements in the price behavior are expected and agents enter the market. This situation can be described in terms of the two threshold values and . In particular agents will (in a probabilistic way) enter the market if and leave the market if :

| (5) |

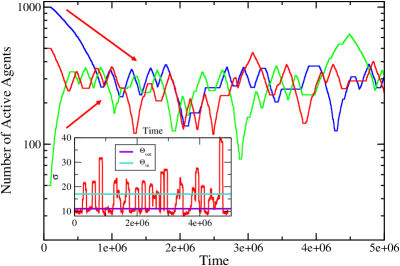

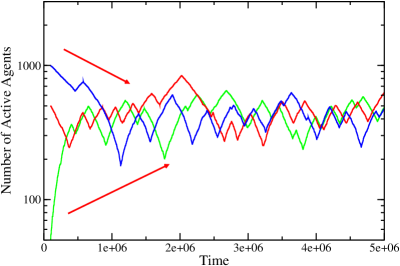

In Fig. 1 we can observe the phenomenon of self-organization.

Starting from a small value of

the large price movements will attract more agents and increases.

Starting instead from a large populations of agents the opposite happens and

decreases. For we have a relatively

stable situation. The self-organization to the intermittent state which leads to the SF

corresponds therefore to the fact that this is the attractive fixed point for the dynamics of the agents related to their threshold strategies. The fact that this occurs in our model for depends on the specific parameters we have adopted but clearly the phenomenon of self-organization is completely general

and robust. In principle, by changing the parameters, one could have the intermittent state at different values of .

In the inset of Fig. 1 we have plotted the intermittent behavior of the estimator as a function of the time compared with the two threshold and .

We can call this attractive intermittent state “quasi-critical” to distinguish it to the usual critical

state of statistical physics model.

Along this line of reasoning we can make two comments with respect to real market:

i) different markets may correspond to very different parameters in our model. For each set of this

parameter there would be a self-organization to a quasi critical value N* leading to the SF.

This permits to explain that the number of agents can be different in different markets

still they all lead to SF with similar properties.

However, this intermittent properties are due to finite size effects and for this reason

a strict universality should not be expected;

ii) in our model the total number of agents has a very precise mathematical meaning.

It corresponds to the number of independent interacting variables in the model.

The interpretation of an effective in a real market is therefore a subtle problem which

requires a careful analysis.

The herding mechanism induces a tendency of agents to behave similarly

but this is not strictly compulsory. In reality if a group of agents, for whatever reason, act coherently

in the market they cannot be considered as mathematically different agents but are essentially a

single agent. For this reason the estimation of the effective number

of independent agents in a real market

represents a very interesting and important problem.

3.2 Other possible rules

In section 3.1 we have seen that, by fixing

the thresholds and in a region of values

of the volatility which is intermediate with respect to the two limit cases

and ,

the system self-organizes in the intermittent state corresponding to an intermediate number of agents

.

In doing this we have chosen the threshold values to correspond approximatively to the region

of the fluctuations leading to the SF.

This may induce the idea that by choosing different values of and

one may force the system to self-organize to any preselected state, not necessarily

the one corresponding to the SF.

We are going to see that it is not the case because by choosing unreasonable thresholds’ region

the system does not reach an interesting or unique self-organized state.

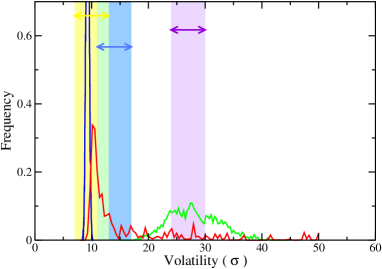

In Fig. 2 we have plotted the histograms of the volatility corresponding

to three different populations with a fixed number of agents with values .

We can see that the volatility of the population is very sharp and it is picked

around a small value of . In the case of the histogram is broader and has a

maximum on a very high level of volatility.

The situation is different in the intermediate case of where

the distribution in very broad and asymmetric. It is picked on small values of volatility but the tails

reach very high values, much more than the population.

The reason for the high values of price fluctuations of the intermediate case ()

with respect to the extreme case () is the following.

A very large price fluctuation corresponds to a situation in which

the chartists action can develop for a certain time. In the highly fluctuating regime ()

the life time of chartist action is too small for this to happen.

On the contrary for the intermediate case chartist fluctuations are more rare but when they

happen they may last for a longer time.

We now consider three different

possibilities for the thresholds values

of and .

These regions are evidenced in Fig. 2 with different colors.

The first region is centered on low values of volatility, the second

on high values and the third on intermediate values. By choosing this

last region, that is the one used in section 3.1, the system self-organizes

in the intermittent state which corresponds to a fluctuating intermediate number of agents .

We are going to see that unrealistic anomalies occur if

one chooses the other two regions.

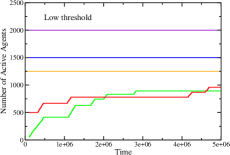

When the region defined by and is centered on low volatility values, and

the starting number of agents is small,

the system size grows until it reaches a number of agents

which leads to an average value of the volatility which is inside the region considered.

Then the fluctuations from this average value are so small that the system is actually locked

in a certain (high) value of the number of agents. The dynamics corresponding to this situation

does not display the SF anymore.

Of course when the starting number of agents is very large its average volatility level

is always inside the considered region and the system size is constant in time.

The dynamics corresponding to a low volatility centered region is shown in Fig. 3(left)

and it does not lead to the phenomenon of the self-organization.

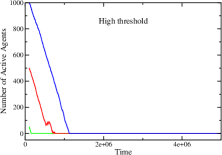

On the contrary, as shown in Fig. 3(right), when the region defined by the thresholds is centered on very high values

of volatility the system size rapidly drops down because the system has an average

volatility which is always smaller than the threshold considered to enter the market.

In this way the system collapses to the unrealistic situation of zero-agent population where

the price fluctuations are only due to the random noise term.

Therefore this study shows that the phenomenon of self-organization and the presence of stylized

facts are intrinsically linked and one cannot force the system to self-organize to a reasonable dynamics which does not lead to the SF.

For example this forbids the possibility of self-organization associated to a random walk dynamics (associate to

the SF).

3.3 Further simplification of the mechanism for the self-organization

In this subsection we consider a simple modification of the mechanism described in section 3.1 to obtain a self-organized market. The idea is that agents enter the market if the volatility is larger than a certain threshold while they leave the market if this volatility is smaller than the threshold .

Of course the interval is arbitrary and needs to be fixed. Actually we are going to see that this is not a crucial point in order to obtain the self-organization of the market. In fact we have considered a situation in which agents enter or exit the market by looking only to one suitable threshold . Also in this case the system self-organizes in the intermittent case characterized by an intermediate number of agents. The only difference with the two-thresholds dynamics, as one can see in Fig. 4, is that the number of agents continues to have relatively large fluctuations, which resembles periodic oscillations, even in the self-organized state.

4 Self-organization with risk-scared agents

The threshold mechanism could be apparently problematic because it may be argued that investors could be scared by a too fluctuating market [18]. However, this problem can easily clarified by the analysis of fluctuations at different time scales. The price movement which we interpret as a positive signal for the agents’ strategy corresponds to the volatility at relatively long time scale. On the other hand a large volatility at a shorter time scale would induce a high risk on such a strategy. In this section we consider how this problem may affect the self-organization mechanism. We are going to see that the introduction of this more complex and realistic scenario in the model does not change the essential elements of the self-organization phenomenon.

4.1 Small scale volatility threshold

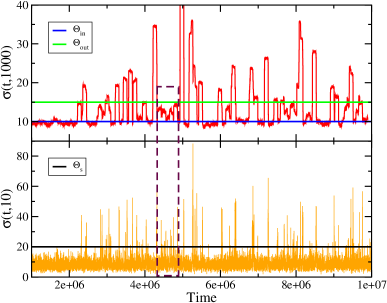

We use the same estimator introduced in section 3.1 (Eq. 4).

Since we want that agents look at fluctuations on two time horizons, at each time step they now have to evaluate fluctuations for two different values of that we call and corresponding respectively to the small time scale and to the large time scale. We set as in the previous section and we choose .

The fear of a too volatile market at a short time scale can be represented by the new threshold .

If the agent will consider the situation as dangerous and she will exit the market

with a certain probability.

If the agent is inactive and the

previous

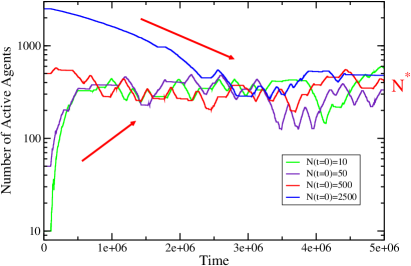

condition is fulfilled she will not enter in the market. Instead if the opposite condition is true (i.e ) the agents compare the long time scale fluctuations with the thresholds and enter/exit according to the same scheme of Eq. 5. In Fig. 5 we show the same analysis of Fig. 1 and we can see that, independently on the starting number of agents, the system tends to the quasi-critical state (i.e. ) with the SF as in the previous section for a suitable choice of the thresholds .

The unique effect introduced by is a slight asymmetry between the rise and the decrease of the number of agents .

The value of we adopt (Fig. 6) is quantitative of the same order of and

, only it corresponds to shorter time scales.

It is also interesting to note that the presence of large fluctuations on the scale of does not imply large fluctuations on the scale of or vice-versa as Fig. 6 points out. In fact we can see in the highlighted region that, while is smaller than , is instead usually larger than .

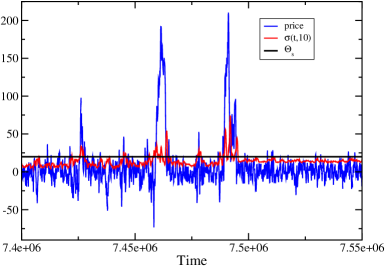

To conclude this section we report in Fig. 7 the price behavior and the fluctuations , the small scale mechanism is active only when the price has large fluctuations on the small scale.

5 Conclusions

In this paper we have presented a critical discussion of the self-organization phenomenon in a market model

dynamics.

We have considered a minimal ABM able to reproduce market SF

as playground to analyze the self-organization phenomenon.

In this model the dynamics strongly depends on the number of agents one considers.

For a finite intermediate number of agents one obtains an intermittent dynamics

which leads to the SF.

In the thermodynamic limit of many agents the price fluctuations decrease and no intermittence

is observed in the dynamics. The result is a super stable market where the SF are not recovered.

Also in the limit of very few agents the SF disappear the price fluctuations being too

high.

The basic question is why real markets self-organize in the quasi critical region with the intermittent dynamics and the SF.

We propose a simple mechanism which triggers this self-organization in a population of agents

which can enter or exit the market.

The rule followed by the agents to decide to enter or leave the market is based on the idea that

the price must undergo some appreciable movements to appear appealing for speculative

traders. On the contrary a super stable market with the price slowly fluctuating around a fundamental

value does not display much profit opportunity and agents are not interested in.

We have studied the robustness of the self-organization with respect to variations of the threshold parameters.

The result is that it is not possible to force the system to self-organize in a state without the SF.

We also consider the fact that agents may be discouraged to enter a risky, noisy market.

This requires the analysis of fluctuations at long time scale (price movements) and short

time scale (risky volatility).

The result is that the introduction of these additional realistic effects does not appreciably modify

the self-organization phenomenon.

We believe to have characterized in a reasonably, realistic and general scheme the self-organization leading to the SF

in terms of the agents’ strategies to enter or exit the market.

This is a new concept, usually neglected in ABM, which, in our opinion, should instead be considered

in the attempts to understand the origin of the SF in economic time series.

References

- [1] V. Alfi, L. Pietronero, and A. Zaccaria. Minimal agent based model for the origin and self-organization of stylized facts in financial markets. 2008. arXiv:0807.1888.

- [2] V. Alfi, M. Cristelli, L. Pietronero, and A. Zaccaria. Minimal agent based model for financial markets I: Origin and self-organization of stylized fatcs. 2008. arXiv:0808.3562.

- [3] V. Alfi, M. Cristelli, L. Pietronero, and A. Zaccaria. Minimal agent based model for financial markets II: Statistical properties of the linear and multiplicative dynamics. 2008. arXiv:0808.3565.

- [4] R. N. Mantegna and H.E. Stanley. An Introduction to Econophysics: Correlation and Complexity in Finance. Cambridge University Press, New York, NY, USA, 2000.

- [5] J. P. Bouchaud and M. Potters. Theory of Financial Risk and Derivative Pricing: From Statistical Physics to Risk Management. Cambridge University Press, 2003.

- [6] R. Cont. Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance, 1:223–236, 2001.

- [7] P. Bak. How Nature Works: The Science of Self-Organised Criticality. Copernicus Press, New York, 1996.

- [8] H.J. Jensen. Self-organized criticality. Cambridge University Press, Cambridge, 1998.

- [9] T. Lux and M. Marchesi. Scaling and criticality in a stochastic multi-agent model of a financial market. Nature, 397:498–500, 1999.

- [10] W. Brian Arthur, John H. Holl, Blake Lebaron, Richard Palmer, and Paul Tayler. Asset pricing under endogenous expectations in an artificial stock market. pages 15–44. Addison-Wesley, 1997.

- [11] Irene Giardina and Jean-Philippe Bouchaud. Bubbles, crashes and intermittency in agent based market models. EPJB, 31:421–437, 2003.

- [12] V. Alfi, F. Coccetti, M. Marotta, L. Pietronero, and M. Takayasu. Hidden forces and fluctuations from moving averages: A test study. Physica A, 370:30–37, 2006.

- [13] V. Alfi, A. De Martino, A. Tedeschi, and L. Pietronero. Detecting the traders’ strategies in minority-majority games and real stock-prices. Physica A, 382:1, 2007.

- [14] M. Takayasu, T. Mizuno, and H. Takayasu. Potential force observed in market dynamics. Physica A, 370:91–97, October 2006.

- [15] T. Mizuno, H. Takayasu, and M. Takayasu. Analysis of price diffusion in financial markets using PUCK model. Physica A, 382:187–192, August 2007.

- [16] A. Kirman. Ants, rationality and recruitment. Quarterly Journal of Economics, 180:137–156, 1993.

- [17] S. Alfarano and T. Lux. A noise trader model as a generator of apparent financial power laws and long memory. Economics working papers 2005,13, Christian-Albrechts-University of Kiel, Department of Economics, 2005.

- [18] M. Pagano. Endogenous market thinness and stock price volatility. The Review of Economic Studies, 56:2, 1989.