Eigenvalue separation in some random matrix models

Abstract.

The eigenvalue density for members of the Gaussian orthogonal and unitary ensembles follows the Wigner semi-circle law. If the Gaussian entries are all shifted by a constant amount , where is the size of the matrix, in the large limit a single eigenvalue will separate from the support of the Wigner semi-circle provided . In this study, using an asymptotic analysis of the secular equation for the eigenvalue condition, we compare this effect to analogous effects occurring in general variance Wishart matrices and matrices from the shifted mean chiral ensemble. We undertake an analogous comparative study of eigenvalue separation properties when the size of the matrices are fixed and , and higher rank analogues of this setting. This is done using exact expressions for eigenvalue probability densities in terms of generalized hypergeometric functions, and using the interpretation of the latter as a Green function in the Dyson Brownian motion model. For the shifted mean Gaussian unitary ensemble and its analogues an alternative approach is to use exact expressions for the correlation functions in terms of classical orthogonal polynomials and associated multiple generalizations. By using these exact expressions to compute and plot the eigenvalue density, illustrations of the various eigenvalue separation effects are obtained.

1. Introduction

1.1. The aims of the paper

Our interest is in the shifted mean Gaussian ensemble, the general variance Laguerre ensemble, and the shifted mean chiral ensembles from random matrix theory. The shifted mean Gaussian ensemble consists of real symmetric or complex Hermitian matrices with joint distribution of the elements proportional to

| (1.1) |

where is a fixed matrix of the same type as . It follows immediately from (1.1) that where is a member of the (zero mean) Gaussian orthogonal ensemble () or Gaussian unitary ensemble ). In the early stages of the development of random matrix theory in nuclear physics, Porter studied the real case of (1.1), with all entries of equal to a constant , through computer experiments of the eigenvalue distribution. It was found that typically all but one of the eigenvalues followed the prediction of the Wigner semi-circle law (see e.g. [17]), and so to leading order were supported on . The remaining eigenvalue—the largest—separated from the semi-circle. We owe our knowledge of this to the work of Lang [27], who followed up on this empirical finding with a theoretical study predicting that the largest eigenvalue would occur near .

Jones et al. [25], by way of their analysis of a spherical model of spin glasses [26], made a quantitative study of this effect in the large limit. They showed (see Section 2 below) that with having all elements equal to , the separation of the largest eigenvalue only occurs for , thus exhibiting a phase transition in .

Many year later [5], an analogous effect has been exhibited in the general variance Laguerre (also known as Wishart) ensemble. This ensemble consists of matrices (Wishart matrices) where the joint distribution on the elements of the matrix is proportional to

| (1.2) |

where is the covariance matrix, and as such is required to have all eigenvalues positive. The elements of are real for , and complex for . Writing we see is a Wishart matrix with , and furthermore

| (1.3) |

where the tilde denotes the matrices are similar and so have the same eigenvalues. With

| (1.4) |

(here the notation denotes 1 repeated times) it was shown that the largest eigenvalue separates from the leading support on provided .

It is the objective of this paper to exhibit the mathematical similarities between these two eigenvalue separation phenomena. Moreover, we add to this a third example, namely the shifted mean chiral matrices

| (1.5) |

where is an Gaussian random matrix with distribution given by (1.2) in the case . The matrix is a constant matrix of the same type as . With all elements of equal to , a separation of the largest eigenvalue in modulus (the eigenvalues of (1.5) occur in pairs) only occurs for .

1.2. Related works

In the mathematics literature the problem of the statistical properties of the largest eigenvalue of (1.1) in the case that all entries of are equal to was first studied by Füredi and Komlos [20]. In the more general setting of real Wigner matrices (independent entries i.i.d. with mean and variance ) the distribution of the largest eigenvalue was identified as a Gaussian, so generalizing the result of Lang. Only in recent years did the associated phase transition problem, already known to Jones et al. [25], receive attention in the mathematical literature. In the case of the GUE, this was due to Peché [35], while a rigorous study of the GOE case can be found in the work of Maida [29].

The paper [5] by Ben Arous, Baik and Peché proved the phase transition property relating to (1.2) in the complex case with given by ((1.4) corresponds to ). Subsequent studies by Baik and Silverstein [6], Paul [34] and Bai and Yao [4] considered the real case. Significant for the present study is the result of [4], giving that for (1.2) with given as above, the separated eigenvalues have the law of the GUE. The case —not considered here—corresponding to self dual quaternion real matrices, is studied in the recent work of Wang [41].

The eigenvalue probability density function (1.1) is closely related to the Dyson Brownian motion model [15] in random matrix theory (see Section 3 below). It is also referred to as a Gaussian ensemble with a source. In this context the case of having a finite rank has been studied by a number of authors [9, 22, 8, 1]. However our use of this differs in that we will keep fixed, and exhibit phase separation as a function of the perturbing parameter.

1.3. Plan

We begin in Section 2 by showing how in each case the criteria for separation can be deduced from the eigenvalue equation implied by regarding the parameters as the proportionalities in rank 1 (or in the case of (1.5), rank 2) perturbations. In Section 3 we discuss analytic features of the eigenvalue separation effect in the case that the matrices , and are of rank . Working with matrices of fixed size, we make use of a generalized hypergeometric function form of the joint eigenvalue probability density function.

In Section 4, in the case (complex) case, we draw attention to known explicit forms for the -point correlation functions, and show how these are well suited to exhibiting eigenvalue separation both analytically and numerically. The content of Section 5 is to exhibit an analogue of eigenvalue separation for the general variance Laguerre ensemble, variance matrices of the form (1.4), and its generalization in the limit . An applied setting is identified in Section 6 as a motivation for future work.

2. Secular equations

Consider first the shifted mean Gaussian ensemble (1.1), and for definiteness suppose ( real symmetric matrices). The simplest case is when all elements of are constant, equal to say. Then

| (2.1) |

where is a column vector with all entries equal to 1, and is a member of the (zero mean) Gaussian orthogonal ensemble. Diagonalizing , , , and using the fact that is distributed as a standard Gaussian vector shows that from the viewpoint of the eigenvalues, the right hand side of (2.1) can be replaced by . We seek the eigenvalues of this matrix [3].

Lemma 2.1.

The eigenvalues of the matrix

are given by the zeros of the solution of the secular equation (for the use of this terminology, see [3])

| (2.2) |

Assuming the ordering , and that , a corollary of this is that the eigenvalues satisfy the interlacing

| (2.3) |

Proof. With we have

| (2.4) |

The matrix product in the second determinant has rank 1 and so

| (2.5) |

The characteristic polynomial (2.4) vanishes at the zeros of this determinant, but not at the zeros of due to the cancellation with the poles in (2.5). Thus the condition for the eigenvalues is the secular equation (2.2). The interlacing condition can be seen by sketching a graph, taking into consideration the requirement .

We are interested in the position of the largest eigenvalue of or equivalently as a function of and , which unlike the other eigenvalues is not trapped by the eigenvalues of . Following [25], to do this requires using the Wigner semi-circle law for the eigenvalue density of Gaussian orthogonal ensemble matrices,

| (2.6) |

where . Thus in (2.2) we begin by averaging over the components of the eigenvectors and thus replacing each by its mean value unity. Because the density of is given by , for large (2.2) then assumes the form of an integral equation,

| (2.7) |

We seek a solution of this equation for .

Now, for ,

| (2.8) |

But it is well known (see [17]), and can readily be checked directly, that

| (2.9) |

where denotes the -th Catalan number. Substituting (2.9) in (2.8), and using the generating function for the Catalan numbers

we deduce the integral evaluation

| (2.10) |

Substituting this in (2.7) shows a solution with is only possible for , and furthermore allows the location of the separated eigenvalue to be specified.

Proposition 2.2.

The case of the shifted mean Gaussian ensemble (1.1) with ( complex Hermitian matrices) and all elements of constant, is very similar. With a (zero mean) member of the Gaussian unitary ensemble, the shifted mean matrices have the same eigenvalues distribution as the random rank 1 perturbation

| (2.12) |

where is an -component standard complex Gaussian vector. Thus with replaced by the secular equation (2.2) again specifies the eigenvalues. Since the mean of is unity, and the eigenvalue density of Gaussian unity ensemble matrices is again given by the Wigner semi-circle law (2.6), all details of the working leading to Proposition 2.2 remain valid, and so the proposition itself remains valid for shifted mean unitary ensemble matrices.

We turn our attention next to correlated Wishart matrices (1.3), and consider for definiteness the complex case . To begin we make use of the general fact that the non-zero eigenvalues of the matrix products and are equal. This tells us that the non-zero eigenvalues of are the same as those for . With given by (1.4),

| (2.13) |

where is an -component standard complex Gaussian vector and is the matrix constructed from by deleting the first column. For the eigenvalues of this matrix have the same distribution as

| (2.14) |

where are the eigenvalues of , and thus are the eigenvalues of .

We recognize (2.14) as structurally identical to (2.12). Hence the condition for the eigenvalues is given by (2.2) with replaced by , replaced by , replaced by , , . In the limit that with fixed, the density of eigenvalues for complex Wishart matrices follows the Marc̆enko-Pastur law (see e.g. [17])

| (2.15) |

Hence, analogous to (2.10), after averaging and for large with fixed the secular equation becomes the integral equation

| (2.16) |

Substituting (2.15), and changing variables reduces this to read

| (2.17) |

Noting that with , in the latter, following the strategy which lead to (2.10) the integral can be evaluated to give

| (2.18) |

This equation only permits a solution for , which therefore is the condition for eigenvalue separation. Moreover, the position of the separated eigenvalue can be read off according to the following result.

Proposition 2.3.

The same result holds for real Wishart matrices. In this case, in (2.13) we must replace by where is a standard real Gaussian vector, and we must replace by where is a real Gaussian matrix. Only the mean value of , and the density of eigenvalues of , are relevant to the subsequent analysis and as these are unchanged relative to the complex case the conclusion is the same.

Also of interest in relation to (2.13) is the limit with . This is distinct to the case fixed, because the eigenvalue density is no longer given by (2.15), but rather the more general Marc̆enko-Pastur law (see e.g. [17])

| (2.19) |

where

Note that the delta function term in (2.19) is in keeping with the fraction of zero eigenvalues of equalling (recall (2.14)).

In this case the averaged large limit of the secular equation becomes the integral equation

| (2.20) |

where

Proceeding as in the analysis of the integral in (2.8), for we write

| (2.21) |

Use can now be made of the known fact (see e.g. [40])

| (2.22) |

where the coefficient of is the Narayana number . Defining

and introducing the generating function

it is fundamental to the theory of Narayana numbers [38] that

| (2.23) |

where , . Thus with (2.22) substituted in (2.21) the sum can be expressed in the form (2.23) to give

| (2.24) |

Note that in the case we reclaim the evaluation of the integral implied by (2.18).

For both terms in (2.20) are decreasing functions of and so take on their maximum value when . The square root in (2.24) then vanishes, and we find that for (2.20) to have a solution we must have

In this circumstance the value of solving (2.20), and thus the location of the separated eigenvalue can be made explicit.

Proposition 2.4.

The reasoning that tells us Proposition 2.3 holds in the real case implies too that Proposition 2.4 similarly holds in the real case.

It remains to study the eigenvalues of (1.5) in the case that all entries of are equal to . Thus

| (2.25) |

where is the vector with all entries equal to unity. In general a matrix of the form (1.5) has zero eigenvalues and eigenvalues given by the positive square roots of the eigenvalues of , . Correspondingly, the matrix of eigenvectors has the structured form

| (2.26) |

with the eigenvalues ordered from largest to smallest. Here denotes the matrix with the final columns deleted, while denotes with columns of zeros added. The matrix (2.26) is real orthogonal when (1.5) has real entries, and is unitary when the entries of (1.5) are complex.

Substituting (2.25) for in (1.5) and conjugating by (2.26) shows (1.5) has the same eigenvalue distribution as

| (2.31) |

where here * denotes complex conjugation, and

| (2.32) |

With the diagonal matrix in (2) denoted the characteristic polynomial for the matrix sum (2) can be written

| (2.33) |

Use of the general formula

shows that the determinant in (2.33) is equal to the determinant

| (2.34) |

where, with and ,

Substituting (2.34) in (2.33) shows (1.5) again has zero eigenvalues, with the remaining eigenvalues, which come in pairs, given by the zeros of (2.34). From the definitions (2) and (2) we deduce that

and so after averaging over the eigenvectors, and to leading order in with fixed, the eigenvalue condition reduces to

| (2.35) |

The positive solutions of (2.35), say, exhibit the interlacing

and we know that the density of the positive eigenvalues is given by with

| (2.36) |

Hence, after averaging over (2.35) becomes the integral equation

| (2.37) |

This integral is essentially the same as that appearing in (2.17), so the evaluation implied by (2.18) allows the integral in (2.37) for to be similarly evaluated, giving

This is precisely the equation obtained by substituting (2.10) in (2.7), after the identifications (2.36). Hence we obtain for the shifted mean chiral ensemble a result identical to that obtained for the shifted mean Gaussian ensemble given in Proposition 2.2.

3. Green function viewpoint

The shifted mean Gaussian and shifted mean chiral random matrices can be used to formulate the Dyson Brownian motion of random matrices (see e.g. [17]). As we will see, this viewpoint can be used to exhibit the separation of a set of eigenvalues, in the setting that the matrices in (1.1) and (1.5) have a single non-zero eigenvalue and single non-zero singular value say of degeneracy , and that is large. Note that the case corresponds to all entries being equal to and respectively. Asymptotic formulas obtained in the course of so analyzing (1.1) can then be used to show an analogous effect for (1.2).

Consider first (1.1). We are interested in the p.d.f. for the eigenvalues of , given the eigenvalues of . Let this be denoted . The Jacobian for the change of variables from the entries of the matrix to the eigenvalues and eigenvectors is proportional to

(see e.g. [17]) where is the normalized Haar measure for unitary matrices and real orthogonal matrices . Hence the sought conditional eigenvalue p.d.f. is proportional to

| (3.1) |

where

Now, with , and denoting the Schur () or zonal () polynomial indexed by a partition of parts, introduce the generalized hypergeometric function

| (3.2) |

It is a fundamental result in the theory of zonal polynomials that (3.2) relates to (3.1) through the evaluation formula (see e.g. [28])

| (3.3) |

and thus the conditional eigenvalue p.d.f. is proportional to

| (3.4) |

Generalizing (1.1) so that it is now proportional to

| (3.5) |

allows the corresponding eigenvalue probability density function for , say to be written as the solution of a Fokker-Planck equation. This is precisely the same Fokker-Planck equation as appears in the Dyson Brownian motion model of the Gaussian ensembles (see e.g. [17]). It can equivalently be interpreted as the Brownian evolution of a classical gas with potential energy

| (3.6) |

is given explicitly by

| (3.7) |

The Green function solution is that solution which satisfies the initial condition

| (3.8) |

It is given in terms of the generalized hypergeometric function (3.2) according to [7]

| (3.9) | |||

where and here and below is some proportionality constant independent of the primary quantities (here , ) of the equation.

Substituting (3.9) in (3.3) allows the matrix integral to be expressed in terms of the Green function. The significance of this for purposes of studying the asymptotics of in the case that is given by

| (3.10) |

is that for the asymptotic form of must factorize as

| (3.11) |

since the initial condition (3.8) then separates the system into two. Furthermore, we know from [7] that

| (3.12) |

Making use of (3.11) and (3.12) in (3.9), and making use too of the scaling property

| (3.13) |

valid for scalar, allows the following asymptotic expansion to be deduced.

Proposition 3.1.

Let be specified by (3.2). In the limit

| (3.14) |

For future reference we remark that the next order correction in (3.1) is to multiply the right hand side by the factor (see e.g. [12])

| (3.15) |

which to leading order is a constant.

Corollary 3.2.

The conditional eigenvalue probability density , in the case that is given by (3.10) with , factorizes to be proportional to

We recognise the first term as the eigenvalue probability density function for the Gaussian ensemble centred at , and the second term as the eigenvalue probability density function for the Gaussian ensemble centred at the origin.

It is also possible to express the eigenvalue probability density function for the general variance Wishart matrices (1.3) in terms of the generalized hypergeometric function [23]. We will revise this point, and then proceed to make use of Proposition 3.1 to deduce a separation of eigenvalues in the setting that the covariance matrix has eigenvalues equal to and eigenvalues equal to , for . The case corresponds to the setting of Proposition 2.3.

To obtain the generalized hypergeometric function form of the eigenvalue probability density, it is most convenient to consider as the input data not the eigenvalues of the covariance matrix , but rather its inverse . In particular, we are interested in the case that

| (3.16) |

With the eigenvalues of (1.3) denoted and , by making use of relevant Jacobians (see e.g. [17]), is seen to be proportional to

| (3.17) |

The sought expression involving now follows by substituting (3.3), thus giving as being proportional to

| (3.18) |

where

| (3.19) |

In (3.18), the limit and thus in the setting of Proposition 2.3, does not directly correspond to the setting of Proposition 3.1. However, if we first write , making use of (3.13) shows that we seek the asymptotics of

| (3.20) |

where the equality follows from the matrix integral form of , (3.3). We remark that writing is well founded because for (1.3) all eigenvalues are positive, so we expect the variables to be in the limit . Applying Proposition 2.3, modified to include the next order correction term (3.15), to (3.20) and reverting back to the variables gives the asymptotic expansion

| (3.21) |

Substituting this in (3.19) we obtain the form of .

Proposition 3.3.

The eigenvalue probability density for general variance Wishart matrices (1.3), in the case that is given by (3.16), with , factorizes to be proportional to

We recognise the first term as the eigenvalue probability density function for the Laguerre ensemble with , and , and thus with support to leading order at , and the second term as the eigenvalue probability density function for the Laguerre ensemble.

We turn our attention now to the shifted mean chiral matrices (1.5), in the case that has a single non-zero singular value of degeneracy . As already noted, the non-zero eigenvalues come in pairs, and there are zero eigenvalues. Furthermore, the matrix of eigenvectors (2.26) has as the matrix of eigenvectors of , , and the matrix of eigenvectors of . The Jacobian for the change of variables to the positive eigenvalues and eigenvectors is proportional to

| (3.22) |

where is as in (3.17).

With distributed as a Gaussian matrix according to (1.2) with , it follows from (3.22) that the probability density function for the positive eigenvalues of (1.5) is proportional to

| (3.23) |

where is the matrix with all entries equal to 0 except those on the diagonal which are equal to , and is the matrix with all entries equal to zero except those in the first positions of the diagonal, which are equal to . We introduce now the further generalized hypergeometric function (3.2)

| (3.24) |

where is a certain generalized Pochammer symbol (see e.g. [17]). The matrix integral in (3.23) can be evaluated in terms of according to (see e.g. [17])

| (3.25) |

Hence the probability density function for the positive eigenvalues of (1.5) can be written in terms of , being proportional to

| (3.26) |

Suppose now that the distribution of is generalized to take on a parameter dependent form proportional to

| (3.27) |

(cf. (3.5)). It is known (see e.g. [19]) that the p.d.f. of the positive eigenvalues of , with those of regarded as given, satisfies the Fokker-Planck equation (3.7) with

| (3.28) |

Here and . This relates to the generalized hypergeometric function (3.24) through the fact that the Green function solution of this Fokker-Planck equation, say, can be written [7]

| (3.29) | |||

where as in (3.9), and is independent of .

We can view (3.29) as allowing in (3.26) to be rewritten in terms of the Green function. But as in (3.10), with

| (3.30) |

the asymptotic form of must, for , factorize as

| (3.31) |

Furthermore, we know from [7] that

| (3.32) |

while for large , the fact that with (3.28) reduces to (3.6) tells us that

| (3.33) |

and is thus given by (3.12). This enables us to deduce the following asymptotic expansion, and then proceed to deduce the form of .

Proposition 3.4.

Let be specified by (3.24). In the limit

| (3.34) |

Corollary 3.5.

The conditional eigenvalue probability density , in the case that is given by (3.30) with , factorizes to be proportional to

We recognise the first term as the eigenvalue probability density function for the Gaussian ensemble centred at , and the second term as the eigenvalue probability density function for the chiral ensemble centred at the origin.

4. Explicit form of the correlations for

According to (3.1) and (3.17), the matrix integral in (3.3) fully determines the eigenvalue probability density function for the shifted mean Gaussian and general variance Wishart ensembles. Furthermore, we know from (3.23) that the matrix integral in (3.25) fully determines the eigenvalue probability density function for the shifted mean chiral ensemble. In the case the matrix integrals in (3.17) and (3.25) are over the Haar measure on the unitary group, and can be evaluated in terms of determininants (see e.g. [17]). In fact each of (3.1), (3.17) and (3.23) can then be written as the product of two determinants. From this functional form, using the general theory of biorthogonal ensembles [10], it is then possible to proceed to compute the general -point correlation functions as an determinant,

| (4.1) |

for a certain kernel function . In this section the eigenvalue separation phenomenon for , exhibited at the level of the eigenvalue probability density function in the previous section, will be analyzed both analytically and numerically in terms of the correlation functions.

Consider first the shifted mean Gaussian ensemble, and suppose that in (3.1) has a single non-zero eigenvalue of degeneracy , as assumed in Section 3. Define

| (4.2) |

where denotes the Hermite polynomial. Then we know from [13] that

| (4.3) |

where, with a simple closed contour encircling zero and , and are so called incomplete Hermite functions specified by

| (4.4) |

According to (4.1) setting in (4.3) gives the eigenvalue density. This being a function of one variable, it is well suited to a graphical representation. Indeed the quantities (4.2) and (4) making up (4.3) are all readily computed numerically, so allowing for particular values of and the density to be tabulated and then graphed. In regard to (4), we first make use of the integral representations of the Hermite polynomial

| (4.5) | |||||

to evaluate the contour integrals. Consider for definiteness . First computing the residue at , then computing the contribution of the singularity at the origin by writing

and using the first of the integral formulas in (4.5) shows

| (4.6) |

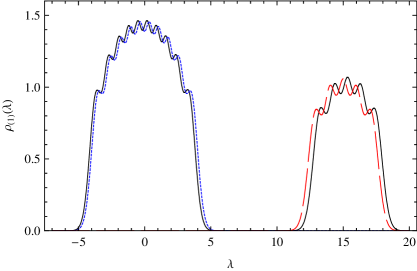

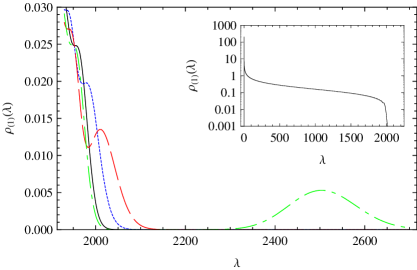

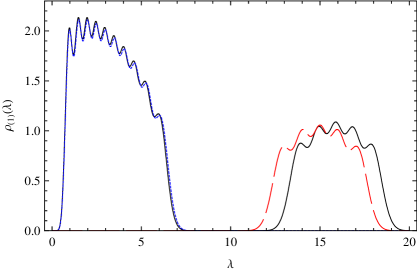

An example of a numerical calculation illustrating Corollary 3.2 is given in Figure 1. Another application is to use a numerical evaluation of (4.3) to illustrate the onset of the eigenvalue separation for large as specified in Proposition 2.2. This we do in Figure 2. For these numerical calculations, we evaluated the integrals in (4) for arbitrary obtaining expressions involving sums of Hermite polynomials as in (4.6) and used them in (4.3).

For general we can show analytically that the large form of is consistent with Corollary 3.2 by establishing the following asymptotic result.

Proposition 4.1.

For

| (4.7) |

Proof. We see from the first formula in (4) that

where the second equality follows from the first integral formula in (4.5). For the second integral formula in (4), use of the second integral form of the Hermite polynomials in (4.5) shows

Substituting in the LHS of (4.7) and comparing with (4.2) gives the RHS of (4.7).

According to (4.3) and (4.7), for the correlation kernel is the sum of two terms, one with support in the neighbourhood of the origin, and the other with support in the neighbourhood of . Furthermore, these two terms are the correlation kernel for the GUE and the GUE, the latter shifted to be centred about (note that the factor in (4.7) does note effect the determinant (4.1)).

In the case of general variance complex Wishart matrices (1.3) with specified by (3.16), the correlations are given by (4.1) with and

| (4.8) |

(see [13]). Here , and with denoting the Laguerre polynomial

| (4.9) |

while and have been termed incomplete multiple Laguerre functions and are specified by

| (4.10) |

Making use of the integral representation for the Laguerre polynomials

| (4.11) |

allows to be expressed in terms of these polynomials. For example, by considering separately the neighbourhoods of zero and as in the derivation of (4.6), we can use (4.11) to show

To relate to Laguerre polynomials requires the identity

which when used in (4.11) implies the integral representation

From this we obtain, for example,

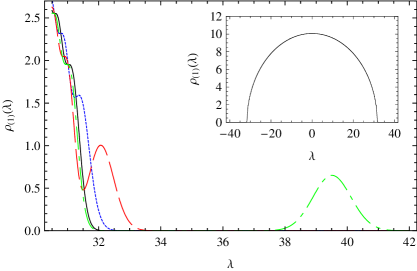

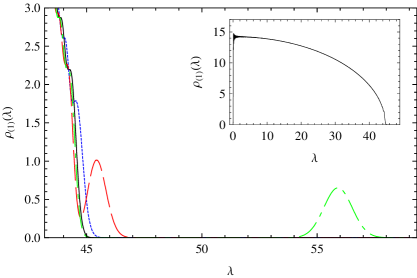

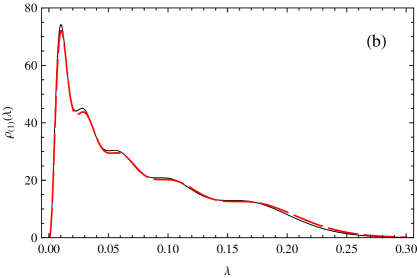

With the integrals (4) thus made explicit for arbitrary , (4.8) in the case , and for particular and can readily be tabulated and graphed. An example illustrating Proposition 3.3 is given in Figure 3. However, unlike the situation with (4.3), the structure (4.8) is not well suited to exhibit the eigenvalue separation effect of Proposition 3.3 in a single plot. This is due to the dependence on rather than in the first term on the RHS. We can also make use of a numerical evaluation of (4.8) in the case to illustrate the onset of the eigenvalue separation for large and near 1/2, as predicted by Proposition 2.3. This is done in Figure 4.

It remains to consider the shifted mean complex chiral matrices (1.5) in the case that has a single non-zero singular value of degeneracy as in Section 3. According to [14] the correlations are specified by

| (4.12) |

where

| (4.13) |

In (4.13) is specified by (4.9), while

| (4.14) | |||

| (4.15) |

The functions , can be expressed in terms of Laguerre polynomials. To see this, for we require the integral formula

| (4.16) |

while for we require

| (4.17) |

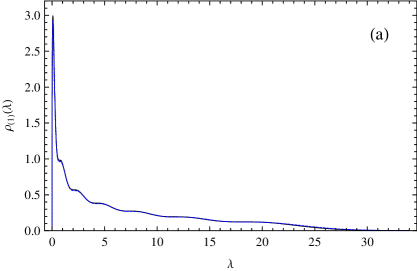

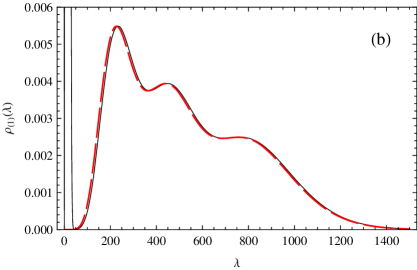

Once have been expressed in terms of Laguerre polynomials, the kernel (4.13) is for and particular readily computed numerically. A plot illustrating the eigenvalue separation property Corollary 3.5 is given in Figure 5. A further plot illustrating the onset of the large separation of a single eigenvalue, for appropriate as specified in Proposition 2.5, is given in Figure 6.

The correlation (4.12) for general can be shown analytically to be consistent with Corollary 3.5. For this the behaviour of the summation (4.13) is required.

Proposition 4.2.

For large

| (4.18) |

while for large with fixed

| (4.19) |

Hence for large

| (4.20) |

Proof. We require the formula

| (4.21) |

and the asymptotic expansion

| (4.22) |

Consider first . For large we see that the main contribution comes from the singularity at . Writing , making use of (4.21) and (4.22), then expanding the exponent to second order in while keeping only the leading term in the rest of the integrand shows

The contour integral can be evaluated in terms of a Hermite polynomial according to the first formula in (4.5), and furthermore can be replaced by in the prefactors not involving the difference . This gives (4.18).

Consider now . Making use of (4.21) and (4.22), then expanding the exponent to second order about the stationary point at and deforming the contour into the direction of steepest descents shows

Recalling now the second integral formula for the Hermite polynomials in (4.5) gives (4.19). Substituting (4.18) and (4.19) in the LHS of (4.20), and recalling (4.2) gives the RHS of (4.20).

Substituting (4.20) in (4.12) we see that for the correlation kernel separates into two parts, and that the resulting correlations are those corresponding to the two ensembles identified in Corollary 3.5.

5. A further asymptotic limit for the general variance Laguerre ensemble

We see from (3.18) that the general variance Wishart matrices (1.3), in the case that is specified by (3.16), is well suited to asymptotic analysis of the limit. In the setting of Proposition 2.3 this corresponds to , so the analysis leading to the eigenvalue separation therein has no bearing to this limit. Starting with (4.8), and with , the scaled correlation functions corresponding to this limit were analyzed in [13]. The scaling was specified by setting and , fixed. Here we will consider the limit with fixed.

Proposition 5.1.

The eigenvalue probability density for general variance Wishart matrices in the case that is given by (3.16), with , factorizes to be proportional to

We recognise the first term as the eigenvalue probability density function for the Laguerre ensemble with and thus with support to leading order at , and the second term as the eigenvalue probability density function for the Laguerre ensemble with .

6. Concluding remarks

The prime motivation for our work was to advance the understanding of the precise effect shifting the mean in the Gaussian probability distribution for the elements (1.1) has on the eigenvalue distribution. We sought to compare this to analogous effects for general variance Wishart matrices, and shifted mean chiral ensembles. We also had in mind the application of our work in the fields of biological webs, food chains, plant and animal ecology, and networks, neural and otherwise.

During the period of the 1950s through the 1970s there was an intense activity by ecologists in studying the role played by biodiversity on ecological systems. In particular, how the number of species of a community affected its stability. There was quite conflicting evidence as to whether complexity increased or decreased or had no effect on the stability of an ecosystem.

The coup de grace came with the classic work of May [30, 31, 32] from purely a theoretical approach. This work has inspired literally a vast amount of literature on the complexity-stability issue in these and other arenas. May used the notions and technical details from the mathematics of random matrix theory in formulating his simple as he called them mathematical models with their predication that increasing complexity decreases the stability of the system.

This pioneering work has motivated in the past 35 years and will continue to do so into the future the debate on the complexity- stability issue. In particular, it has been evidenced that under certain specific conditions in the system that complexity can either increase or decrease the system’s stability. In an interesting toy model [24] the authors have studied an ecological system where they use a small matrix where the elements are taken from a random distribution of interaction coefficients. They found that the non zero mean of the distribution can lead to either an increase or decrease in the stability of the system. (See also some very early work of 1971 [33] discussed by May [31, 32].)

Although May’s work was strongly influenced by random matrix theory, there has been little application of the mathematics of random matrix theory to these vitally interesting areas and issues. Specifically, it is the distribution of the largest eigenvalue(s) of a random matrix that determines its stability. As we have shown in this paper, a non zero mean in the probability distribution for the elements of a random matrix severely affects its eigenvalue distribution and hence its stability.

Very recent works [18, 37, 2, 11] studying the eigenvalues of the real Ginibre ensemble [21] have strong potential bearing on the further application to biological webs and neural networks [36, 16, 39]. The generalization to the case of complex eigenvalues is very important and we plan to study this in our future work.

Acknowledgements

KEB was supported by the NSF through grant #DMR-0427538 and by the Texas Advanced Research Program through grant #95921. NEF appreciates the support received during a visit early this year from this NSF grant, and from the M-OSRP Center of Professor Arthur B. Weglein, who he gratefully thanks for everything. PJF was supported by the Australian Research Council.

References

- [1] M. Adler, J. Delépine, and P. van Moerbeke, Dyson’s non-intersecting Brownian motions with a few outliers, arXiv:0707.0442, 2007.

- [2] G. Akemann and E. Kanzieper, Integrable structure of Ginibre’s ensemble of real random matrices and Pfaffian integration theorem, J.Stat.Phys. 129 (2007), 1159-1281.

- [3] J. Anderson, A secular equation for the eigenvalues of a diagonal matrix perturbation, Linear Alg. Applications 246 (1996), 49–70.

- [4] Z. Bai and J.-F. Yao, Central limit theorems for eigenvalues in a spiked population model, Ann. l’Institut H. Poicaré 44 (2008), 447–474.

- [5] J. Baik, G. Ben Arous, and S. Péché, Phase transition of the largest eigenvalue for nonnull complex sample covariance matrices, Annals of Prob. 33 (2005), 1643–1697.

- [6] J. Baik and J.W. Silverstein, Eigenvalues of large sample covariance matrices of spiked population models, J. Mult. Anal. 97 (2006), 1382–1408.

- [7] T.H. Baker and P.J. Forrester, The Calogero-Sutherland model and generalized classical polynomials, Commun. Math. Phys. 188 (1997), 175–216.

- [8] M. Bertola and S.Y. Lee, First colonization of a hard edge in random matrix theory, arXiv:0804.1111, 2008.

- [9] P.M. Bleher and A. Kuijlaars, Large limit of Gaussian random matrices with external sources I, Comm. Math. Phys. 252 (2004), 43–76.

- [10] A. Borodin, Biorthogonal ensembles, Nucl. Phys. B 536 (1998), 704–732, 2008.

- [11] A. Borodin and C.D. Sinclair, The Ginibre ensemble of real random matrices and its scaling limits, arXiv:0805.2986v1

- [12] A.K. Chattopadhyay and K.C.S. Pillai, Asymptotic expansions for the distributions of characteristic roots when the parameter matrix has several multiple roots, Multivariate Analysis III (P.R. Krishnaiah, ed.), Academic Press, New York, 1973, pp. 117–127.

- [13] P. Desrosiers and P.J. Forrester, Hermite and Laguerre -ensembles: asymptotic corrections to the eigenvalue density, Nucl. Phys. B 743 (2006), 307–332.

- [14] by same author, A note on biorthogonal ensembles, J. Approx. Th. 152 (2007), 167–187.

- [15] F.J. Dyson, A Brownian motion model for the eigenvalues of a random matrix, J. Math. Phys. 3 (1962), 1191–1198.

- [16] J.Feng, V.K. Jirsa, and M.Ding, Synchronization in networks with random interactions: Theory and applications, Chaos 16 (2006), 015019.

- [17] P.J. Forrester, Log-gases and Random Matrices, www.ms.unimelb.edu.au/~matpjf/matpjf.html.

- [18] P.J. Forrester and T. Nagao, Eigenvalue statistics of the real Ginibre Ensemble, Phys. Rev. Lett. 99, (2007) 050603.

- [19] P.J. Forrester, T. Nagao, and G. Honner, Correlations for the orthogonal-unitary and symplectic-unitary transitions at the hard and soft edges, Nucl. Phys. B 553 (1999), 601–643.

- [20] Z. Furedi and J. Komlos, The eigenvalues of random symmetric matrices, Combinatorica 1 (1981), 233–241.

- [21] J. Ginibre, Statistical ensembles of complex, quaternion, and real matrices, J. Math. Phys. 6, (1965) 440-449.

- [22] T. Imamura and T. Sasamoto, Polynuclear growth model, GOE2 and random matrix with deterministic source, Phys. Rev. E 71 (2005), 041606.

- [23] A.T. James, Distributions of matrix variates and latent roots derived from normal samples, Ann. Math. Statist. 35 (1964), 475–501.

- [24] V.A.A. Jansen and G.D. Kokoris, Complexity and stability revisited, Ecology Letters 6, (2003), 498–502.

- [25] R.C. Jones, J.M. Kosterlitz, and D.J. Thouless, The eigenvalue spectrum of a large symmetric random matrix with a finite mean, J. Phys. A 11 (1978), L45–L48.

- [26] J.M. Kosterlitz, D.J. Thouless, and R.C. Jones, Spherical model of a spin glass, Phys. Rev. Lett. 36 (1976), 1217–1220.

- [27] D.W. Lang, Isolated eigenvalue of a random matrix, Phys. Rev. 135 (1964), B1082–B1084.

- [28] I.G. Macdonald, Hall polynomials and symmetric functions, 2nd ed., Oxford University Press, Oxford, 1995.

- [29] M. Maida, Large deviations for the largest eigenvalue of rank one deformations of Gaussian ensembles, Elec. J. Prob. 12 (2007), 1131–1150.

- [30] R.M. May, Will a large complex system be stable?, Nature 238 (1972), 413–414.

- [31] by same author, Stability and complexity in model ecosystems, Princeton University Press, Princeton, 1973.

- [32] by same author, Some mathematical questions in biology, edited by J.D. Cowan, American Mathematical Society, Washington, DC, 1974.

- [33] S. Makridakis and R. Weintraub, On the synthesis of general systems, General System 16, (1971) 42-50, 51-54.

- [34] D. Paul, Asymptotics of large sample covariance matrices of spiked population model, Statistica Sinica 17 (2007), 1617–1642.

- [35] S. Péché, The largest eigenvalue of small rank perturbations of Hermitian random matrices, Prob. Theor. Rel. Fields 134 (2006), 127–173.

- [36] K. Rajan and L.F. Abbott, Eigenvalue spectra of random matrices for neural networks, Phys. Rev. Lett. 97 (2006), 188104.

- [37] H-J. Sommers and W. Wieczorek, General eigenvalue correlations for the real Ginibre ensemble, J. Phys. A 129, (2008), 405003(24pp).

- [38] R.P. Stanley, Enumerative combinatorics, vol. 2, Cambridge University Press, 1999.

- [39] M. Timme, T. Geisel, and F. Wolf, Speed of synchronization in complex networks of neural oscillators: analytic results based on random matrix theory, Chaos 16, (2006) 015108

- [40] K.W. Wachter, The strong limits of random matrix spectra for sample matrices of independent elements, Annal. Prob. 6 (1978), 1–18.

- [41] D. Wang, Spiked models in Wishart ensembles, arXiv:0804.0889.