Smile dynamics – a theory of the implied leverage effect

Abstract

We study in details the skew of stock option smiles, which is induced by the so-called leverage effect on the underlying – i.e. the correlation between past returns and future square returns. This naturally explains the anomalous dependence of the skew as a function of maturity of the option. The market cap dependence of the leverage effect is analyzed using a one-factor model. We show how this leverage correlation gives rise to a non-trivial smile dynamics, which turns out to be intermediate between the “sticky strike” and the “sticky delta” rules. Finally, we compare our result with stock option data, and find that option markets overestimate the leverage effect by a large factor, in particular for long dated options.

I Introduction

It is by now well known that the Black-Scholes model is a gross oversimplification of real price changes. Non Gaussian effects have to be factored in order to explain (or possibly to predict) the shape of the so-called volatility smile, i.e. the dependence of the implied volatility of options on the strike price and maturity. Market prices of options, once converted into an effective Black-Scholes volatility, indeed lead to volatility surfaces – the implied volatility depends both on the strike price and the maturity . But matters are even more complicated since the whole surface is itself time dependent: the implied volatility associated to a given strike and maturity changes from one day to the next (see e.g. Rama ). An adequate model for the dynamics of the volatility surface is crucial for volatility risk management and for market making, for instance. Market practice on this issue follows simple rules of thumb Hull , such as the “sticky strike” rule where the volatility of a given strike and maturity remains constant as time evolves. Another rule is “sticky delta” (or “sticky moneyness”) where the volatility associated to a given moneyness stays constant, which means, to a first approximation, that the volatility smile is anchored to the underlying asset price.

From a theoretical point of view, different routes have been suggested over the years to handle smile dynamics. One is to rely on local volatility models, popularized by Dupire Dupire and Derman and Kani Derman , where the underlying is assumed to follow a (geometric) Brownian motion with a local value of the volatility that depends deterministically on the price level and time. As shown by Dupire, it is always possible to choose this dependence such that the smile surface is fitted exactly. This has been considered by many to be a very desirable feature, and such an approach has had considerable success among quants. Unfortunately, this idea suffers from lethal drawbacks. For one thing, this approach predicts that when the price of the underlying asset decreases, the smile shifts to higher prices and vice versa (see the detailed discussion of this point in SABR ). This is completely opposite to what is observed in reality, where asset prices and market smiles tend to move in the same direction. From a more fundamental point of view, local volatility models cannot possibly represent a plausible dynamics for the underlying. The whole approach is, in our mind, a victory of the “fit only” approach to derivative pricing and the demise of theory, in the sense of a true, first principle understanding of option prices in terms of realistic models of asset prices. Contrarily to what many quants believe, even a perfect fit of the smile is not necessarily a good model of the smile.

A more promising path starts from realistic models for the true dynamics of the underlying. Many models have been proposed in order to account for the non-Gaussian nature of price changes: jumps and Lévy processes RamaBook , GARCH and stochastic volatility models Gatheral ; PHL , multiscale multifractal models Muzy ; lisa , mixed jumps/stochastic vol models, etc. One particularly elaborate model of this kind is the so-called SABR model, where the log-volatility follows a random walk correlated with the price itself in order to capture the leverage effect, i.e. the rise of volatility when prices fall (and vice-versa, see below). Interestingly, all these models predict a certain term structure for the cumulants (skewness, kurtosis) of the return distribution over different time scales, which in turn allows one to calculate the parabolic shape of the smile for near-the-money options of different maturities Backus ; CPB ; Book ; SABR . For example, models where returns are independent, identically distributed – IID – variables (like Lévy processes), the skewness is predicted to decay like and the kurtosis as . As we show below, the leverage effect leads to a much richer term structure of the skewness, whereas long-ranged volatility clustering leads to a non trivial term structure of the kurtosis Book .

The aim of this paper is to explore the dynamics of the smile around the money, within the lowest order approximation that only retains the skewness effect. We show that such an approximation leads to an explicit prediction for dynamics of the smile, in particular of the implied leverage effect, i.e., the correlation between returns and at the money implied volatilities. Our result only depends on the historical leverage correlation, and predicts a volatility shift intermediate between “sticky strike” (for short maturities) and “sticky delta” (for long maturities), in a way that we detail below. We then compare our result with market option data on stocks and indices, and find that the market on average overestimates the leverage effect by a rather large factor.

II Volatility Smile: Cumulant Expansion and Historical Leverage

Let us first recall the cumulant expansion of the volatility smile, worked out in slightly different form in several papers (see Backus ; CPB ; Book and also Sircar ; SABR ; Durrlemann ). Converted into a Black-Scholes volatility , the price of a near-the-money option of maturity can be generally expressed as:

| (1) |

where is the strike, the price of the underlying, the true volatility of the stock and is the moneyness. and are respectively the skewness and the kurtosis of the forward looking, un-drifted probability of price changes over lag Book . In the above formula we neglect various terms that are usually small (for example, a term in that is small compared to the kurtosis contribution). In the following we will in fact discard the quadratic contribution and study the assymmetry of the volatility smile for options in the immediate vicinity of the money, where the smile is entirely described by the volatility and the skewness. Although both these quantities should be interpreted as forward looking, it proves very useful to see what a purely historical approach has to say. The unconditional historical skewness can be written in full generality as Book :111In fact, this formula assumes that the three-point return cumulant, , is zero when . We have checked empirically that this term is small, even summed over non coinciding times.

| (2) |

where is the skewness of daily returns and is the leverage correlation function of daily returns , which was studied in, e.g. leverage ; Perello . For IID returns, and the skewness decays as . Negative price-volatility correlations produce anomalous skewness, that can even grow with maturity before decaying to zero. An example of this is shown in Fig. 1 for a collection of international indices. A good fit of can be obtained with a pure exponential: , as also shown in Fig. 1 for the OEX. This functional form for the leverage correlation leads to the following explicit shape for the skewness:

| (3) |

It is easy to check that the leverage induced term first increases as , reaches a maximum for and decays back to zero as for large maturities.

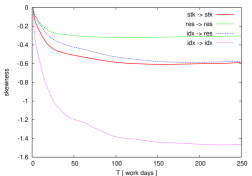

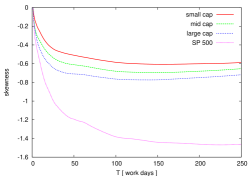

It is also interesting to measure the historical skewness of individual stocks, which is much less pronounced than the index leverage leverage – see Figs. 2-a,b,c for small, mid and large caps, and Fig. 2-d for a direct comparison between different market caps. Here again a purely exponential fit is acceptable, with however parameters and that depend on the stock, mostly through market capitalisation . For the period 2001 – 2006, we find that days across all s, whereas increases by a factor to between and . A possible intuitive explanation for this increase of is that the influence of the market mode is stronger on large cap stocks than on small cap stocks, for which the idiosyncratic contribution is larger. In this case, it would indeed be expected that the leverage of large cap stocks is more akin to an index leverage effect.

In order to better understand this phenomenon, we postulate a simple one-factor model for the returns of a given stock: , where is the market return (which we approximate by the S&P500), and is the idiosyncratic term, uncorrelated with . The total volatility is decomposed into ; typically the second term is two to three times larger than the first one. The total skewness of a stock can be also be decomposed into three different contributions: market-induced vol on the market mode, market-induced vol on the idiosyncratic part and idiosyncratic-induced vol on itself. More precisely, one can write:222There is in principle a fourth contribution describing the effect of the idiosyncratic part of the return of future market volatility, but is is found to be extremely small, as expected intuitively.

| (4) |

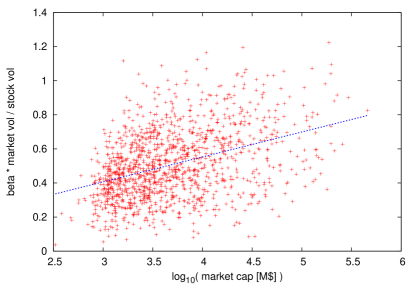

with obvious notations. Note that the market-induced vol contributions are weighted by the ratio of the market factor vol to the total volatility, which decreases for smaller cap stocks. The three ’s are all of the same order of magnitude, with a factor 2-3 larger than the other two. Interestingly the other two contributions cross as a function of : the idiosyncratic-induced vol on itself is dominant at small , whereas the market- and their maturity dependence is shown in Fig. 2 for small, mid and large cap stocks, together with the average total leverage effect. We have checked that the weighted contribution of the three terms add up the total effect, as should be. In Fig. 3 we also show the ratio as a function of the market cap . Although this ratio indeed increases with , another effect that explains the increase of the leverage effect with market cap is the growth of the index/idiosyncratic leverage effect (see Fig. 2).

III The Implied Leverage Effect

We now turn to the dynamics of the smile, in particular of the implied leverage effect that measures how the at-the-money (ATM) implied volatility is correlated with the stock return. For a given day , the implied vol reads, to first order in moneyness:

| (5) |

where

| (6) |

is the expected average squared volatility between now and maturity, and is equal, within this approximation, to the ATM vol:

| (7) |

Now, between and , the price evolves as . How is the smile expected to react? There are two simple rules of thumb commonly used in the market place:

-

•

Sticky Strike (ss): The implied volatility of an option is only a function of the strike, but does not depend on the price of the underlying (at least locally). Formally, . From the above general formula, the change of volatility should be proportional to:

(8) Setting this derivative to zero and focusing to the ATM vol (), one deduces:

(9) -

•

Sticky Delta (s): In this case, the smile is assumed to move with the underlying, so that the implied volatility of a given moneyness does not change. In particular, the ATM vol does not change:

(10)

A purely historical theory of the implied volatility leads to a prediction that is in between the above rules of thumb. One starts from the above implied vol expansion Eq. (5) and consider the impact of the change in the price both on the expected future realized vol and on the moneyness. More precisely, the ATM vol evolves as:

| (11) |

From the definition of the leverage correlation function, and neglecting higher order (kurtosis) correlations, the expected relative change of the future realized volatility is given by:

| (12) |

Collecting all contributions, one finds that the change of ATM vol for a given stock return and a given maturity reads (we drop the dependence):

| (13) |

where we have defined the implied leverage coefficient . We assume, as above, an exponential behaviour for the leverage correlation function, and neglect the contribution (see below). We then find that the theoretical implied leverage is given by:

| (14) |

with . This is the central result of this study. It should be compared to ones obtained from the sticky strike/sticky delta prescriptions:

| (15) |

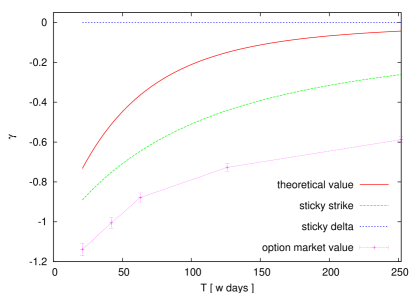

The asymptotic behaviour of these quantities can be compared, one finds (in agreement with the general result of Durrlemann Durrlemann ) and . In other words, the sticky strike always overestimates the implied leverage, but becomes exact for short maturities compared to the leverage correlation time: . The sticky delta procedure, on the other hand, always underestimates the true implied leverage, but becomes a better approximation than the sticky strike for large maturities.

IV Comparison with empirical data: indices and individual stocks

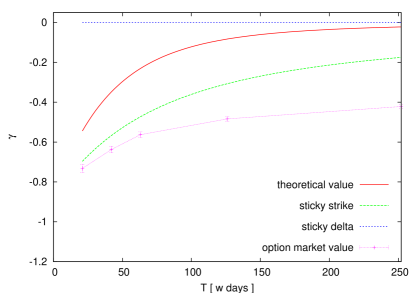

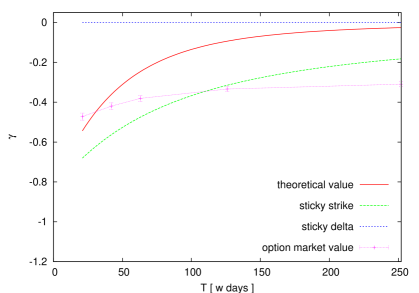

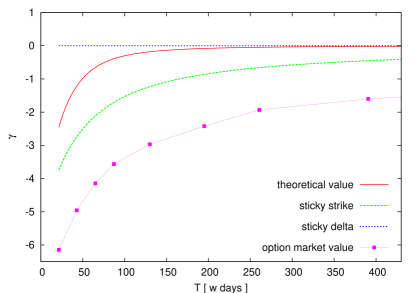

These predictions are compared with empirical data on the implied leverage effect on the OEX index, large cap, mid cap and small cap stocks, in Figs. 4-7. On these plots we show the implied leverage coefficient as a function of maturity. The three curves correspond to (a) the theoretical prediction computed using the historically determined leverage correlation , (b) the sticky strike procedure using the same historical parameters and (c) the data obtained using from the daily change of ATM implied volatilities, . We also show the line corresponding to sticky delta. The implied data is obtained by regressing the relative daily change of ATM implied vols on the corresponding stock or index return, for each maturity. The result is then averaged over all stocks within a given tranche of market capitalisation. Similarly, the coefficient needed to compute the theoretical prediction is obtained by fitting the leverage correlation for each stock individually, normalizing it by the realized volatility over the same period, and then averaging the ratio across different stocks. It turns out that itself is to a good approximation proportional to anyway leverage .

It is clear from these plots that on average, implied volatilities overreact to changes of prices compared to the prediction calibrated on the historical leverage effect, except maybe for small cap stocks where the level of is in the right range at short maturities. The overestimation tends to grow with maturity, since the theoretical prediction is that whereas the implied value appears to saturate at large . In fact, the curve appears to be well fitted by a sticky-strike prediction , but with an effective value of the parameter substantially larger than its historical value. This would be compatible with the fact that market makers use a simple sticky strike procedure, but with a smile that is significantly more skewed than justified by historical data. We only have partial evidence that the implied skew is indeed too large, but cannot check this directly with the data at our disposal at present. However, we believe that this is a very plausible explanation to our findings. We have furthermore checked that our conclusions are stable over different time periods.

In the above theory for , we have explicitely neglected the one-day skewness . Could this term explain the above discrepancy? We have checked that this term gives a small contribution to – at most for short maturities. In fact, the daily skewness of individual stocks is even slightly positive, which should lead to a further (small) reduction of the implied skew and of the implied leverage effect.

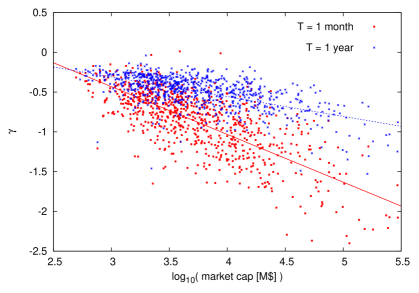

Finally, we have studied more systematically the dependence of on market capitalization . The results are shown in Fig. 8. As expected (and already clear from Figs. 4-6), increases (in absolute value) with ; a good fit of the dependence is:

| (16) |

where and are maturity dependent coefficients.

V Conclusion

In this paper, we have provided a first principle theory for the implied volatility skew and at-the-money implied leverage effect in terms of the historical leverage correlation, i.e. the lagged correlation between past returns and future squared returns. We have compared the theoretical prediction for the implied leverage to two well known rules of thumb to manage the smile dynamics: sticky strike or sticky delta. The sticky strike is exact for small maturities, but is an upper bound to the theoretical result otherwise. The sticky delta is a (trivial) lower bound, which however becomes more accurate than sticky strike at large maturities.

We have then compared these theoretical results to data coming from option markets. We find that the implied volatility strongly over-reacts, on average, to change of prices, especially for long dated options. A plausible interpretation is that market makers tend to use a sticky strike rule, with an exaggerated skewness of the volatility smile. It would be interesting to test this hypothesis directly, with full option smile data and not only at-the-money vols like in this study.

We have also provided an empirical study of the market cap dependence of these effects. We find that both the historical and implied leverage effect is stronger for larger cap stocks, with a roughly logarithmic dependence on market cap. Although this is partly explained in terms of the ratio of the idiosyncratic vol to the total vol (smaller for larger cap stocks), we find that the index/idiosyncratic leverage effect is stronger for these large caps. This may relate to the risk aversion interpretation of the leverage effect put forth in leverage : since large cap stocks are followed by more market participants, feedback effects could be stronger there.

References

- (1) Cont R., da Fonseca J., Dynamics of implied volatility surfaces , Quantitative Finance, 2, 45, (2002); Cont R., Durrelmann V., da Fonseca J., Stochastic Models of Implied Volatility Surfaces, Economic Notes, 31, (2002)

- (2) For a nice review on these rules of thumb, see: T. Daglish, J. Hull, W. Suo, Volatility surfaces: theory, rules of thumb and empirical evidence, Quantitative Finance, 7, 507, (2007).

- (3) Dupire B., Pricing with a Smile, Risk Magazine, 7, 18-20 (1994).

- (4) Derman, E., Kani I, Riding on a Smile Risk Magazine, 7, 32-39 (1994); Derman E., Kani I., Zou J. Z., The Local Volatility Surface: Unlocking the Information in Index Options Prices Financial Analysts Journal, (July-Aug 1996), pp. 25-36.

- (5) Hagan P., Kumar D., Lesniewski A., and Woodward D., Managing smile risk, Wilmott magazine, 84-108, September 2002.

- (6) Cont R., Tankov P. : Financial Modelling with Jump Processes, Chapman & Hall / CRC Press, (2003).

- (7) Gatheral J. : The Volatility Surface: A Practitioner’s Guide, Wiley Finance (2006).

- (8) Henry-Labordère P. : Analysis, Geometry, and Modeling in Finance: Advanced Methods in Option Pricing, Chapman & Hall / CRC Press, forthcoming.

- (9) Muzy J.-F., Delour J., Bacry E., Modelling fluctuations of financial time series: from cascade process to stochastic volatility model, Eur. Phys. J. B 17, 537-548 (2000); Bacry E., Delour J. and Muzy J.-F., Multifractal random walk, Phys. Rev. E 64, 026103 (2001).

- (10) Borland L., Bouchaud J.-P., Muzy J.-F., Zumbach G., The dynamics of Financial Markets: Mandelbrot’s multifractal cascades, and beyond, Wilmott Magazine, March 2005. Borland L., Bouchaud J.-P., On a multi-timescale feedback model for volatility fluctuations, arXiv/physics.0507073

- (11) Backus D., Foresi S., Li K. and Wu L., Accounting for Biases in Black-Scholes (1997). CRIF Working Paper series. Paper 30.

- (12) Potters M., Cont R., Bouchaud J.-P., Financial Markets as Adaptive Ecosystems, Europhys. Lett. 41, 239 (1998).

- (13) Bouchaud J.-P., Potters M.: Theory of Financial Risk and Derivative Pricing, Cambridge University Press, (2000 & 2004)

- (14) Fouque J-P, Papanicolaou G., Sircar R. : Derivatives in Financial Markets with Stochastic Volatility, Cambridge University Press, (2000)

- (15) Durrleman V, From Implied to Spot Volatilities. PhD thesis, Department of Operations Research & Financial Engineering, Princeton University, 2004.

- (16) Bouchaud J.-P., Matacz A., Potters M., The leverage effect in financial markets: retarded volatility and market panic Physical Review Letters, 87, 228701 (2001)

- (17) Perello J., Masoliver J., Bouchaud J.-P., Multiple time scales in volatility and leverage correlations: a stochastic volatility model, Appl. Math. Fin. 11, 1 (2004).