Optimal Time to Sell a Stock in Black-Scholes Model: Comment on “Thou shall buy and hold”, by A.

Shiryaev, Z. Xu and X.Y. Zhou

Satya N. Majumdar1 and Jean-Philippe Bouchaud21 Laboratoire de Physique Théorique et

Modèles Statistiques (UMR 8626 du CNRS),

Université Paris-Sud, Bât. 100, 91405 Orsay Cedex, France

2 Science & Finance, Capital Fund Management, 6 Bd

Haussmann, 75009 Paris, France.

Abstract

We reconsider the problem of optimal time to sell a stock studied by Shiryaev, Xu and Zhou SXZ

using path integral methods. This method allows us to confirm the results obtained by these

authors and extend them to a parameter region inaccessible to the method used in SXZ . We also obtain the full

distribution of the time at which the maximum of the price is reached for arbitrary values of

the drift.

I Introduction

In the preceeding paper, A. Shiryaev, Z. Xu and X.Y. Zhou SXZ ask about the optimal time to sell a

stock

over a certain time interval , knowing that the price is a geometrical Brownian motion with

a certain average return over the risk-free rate and a certain volatility . The answer

to this question depends on the value of the adimensional parameter . The method

used by the authors allow them to prove that whenever the optimal selling time

is always at the end of the interval, , whereas in the case . In

financial words, “good” stocks with a sufficiently large average return should be sold as late as

possible, whereas one should immediately get rid of “bad stocks”. These results are clearly very

interesting; however one feels unsatisfied by the fact that the authors’ method do not allow them

to treat the case . They discuss this point in the conclusion, mentioning (a)

a working paper SXZ2 based on an alternative method showing that one should in fact sell immediately

as soon as and (b) that the case is not interesting financially because

“most stocks realize by a large margin”.

The aim of this short note is to reconsider the problem using path integral methods which are well known in

physics but perhaps less well known in financial mathematics. This method allows one to treat all values

of on the same footing. We confirm the results of SXZ and extend them to the

interval. In fact, we show that there is an exact symmetry in the problem that relates

the problem with to the problem with . Our method furthermore allows us to garner

additional results, such as the distribution of the time at which the maximum of the price is reached.

We find that this distribution has inverse square root singularities both at and for all

values of ; however, the amplitude of the divergence at is stronger when and

weaker when . This gives a more precise picture to the results of Shiryaev, Xu and Zhou.

For , the problem is degenerate and the two peaks have exactly the same amplitude (in fact, the

distribution is symmetric under ).

Finally, we do not agree with the statement that is not interesting financially. The numbers

provided in SXZ are based on the S&P500 index returns, and are therefore much too optimistic: first,

there is an obvious selection bias since badly performing stocks leave the index; second, the volatility of

the index is two to three times smaller than the volatility of individual stocks, thanks to the diversification

effect. An annualized volatility above is in fact not uncommon, in particular for small to medium caps –

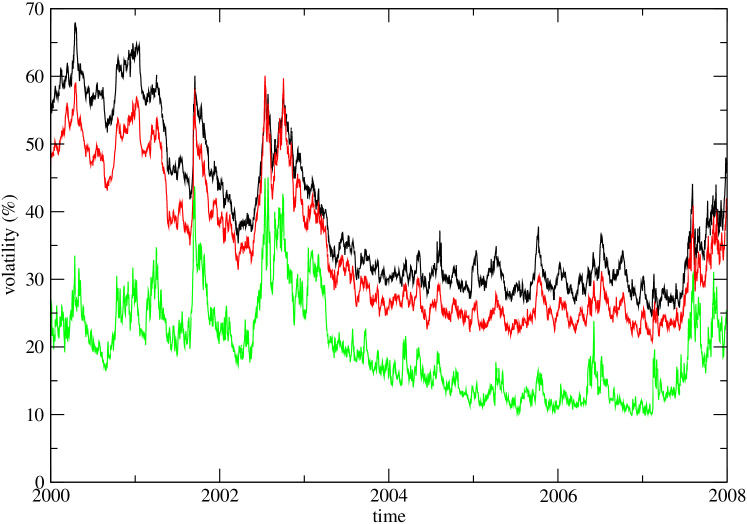

whereas the S&P500 only includes large caps. Fig. 1 shows the time series of the (implied) S&P500 index

volatility and the average stock volatility, in the period 2000-2007. With an average annual return of

, an interest rate of and a volatility of annual, the parameter is found to

be .

We hope that this short note will shed a useful light on the work of A. Shiryaev, Z. Xu and X.Y. Zhou, and

that it will convince the reader that path integral methods are extremely powerful to solve a variety of

random walk problems. We refer the reader to a short review paper by one of us BF on this topic, see

also MRKY .

Figure 1: Time series of the (implied) S&P500 index

volatility (the VIX, bottom green curve) and the average implied stock volatility for SPX stocks (middle red curve) and

mid-cap stocks (upper black curve), in the period 2000-2007. It is clear that stock volatilities are on average

two to three times larger than the volatility of the index, and that values of above are not uncommon.

II The Set-Up

In this section we give the set-up of the problem using physicists notations. We assume, as in SXZ , that

the price of a stock follows a geometric Brownian motion:

(1)

where is Ito corrected drift and the standard Brownian motion.

We will use below the notation for the drifted Brownian motion,

with by convention . In Ref. SXZ , the authors introduce the notation .

A ‘good’ stock in the financial language corresponds to a positive drift (i.e., )

and a ‘bad’ stock corresponds to a negative drift (). In terms of the real return of the stock,

the condition translates into , where is the excess return over the risk-free rate .

Note that the process that we talk about is the real world process and not the risk-neutral one,

which has no meaning for the question raised in Ref. SXZ .

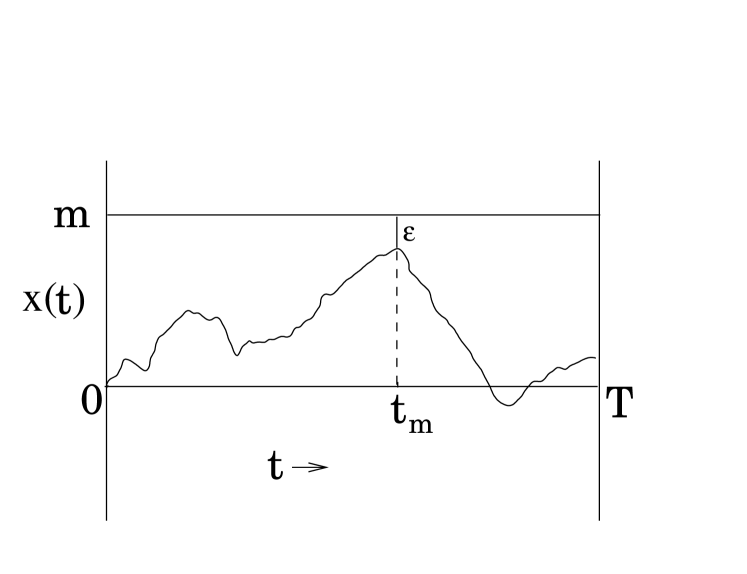

Let us consider the evolution of the stock price over a fixed time interval

. It is intuitively obvious that the maximum of a

drifted Brownian motion

and hence that of the stock price is most likely to occur at (for )

and (for ). Thus, it obviously makes sense to sell a ‘good’ stock

at the end of the interval , whereas a ‘bad’ stock at the begining

of the interval . This intuitive results are put on a more rigorous mathematical

footing in the rest of this note by (i) calculating exactly, using path integral methods, the maximal

relative error as

defined in Ref. SXZ , but for all values of and (ii) also by computing the

full probability density of the time at which the maximum of the price occurs for

all .

Let denote the maximum price of the stock over the

interval , i.e.,

(2)

Evidently, the optimal time to sell the stock is the one where the

difference between the price of the stock and its maximal value

is minimal. A convenient way to estimate this optimal time is to

consider the relative error at a fixed time where

(3)

where denotes the expectation value over all realizations of the Brownian

motion. Minimizing over gives the optimal

time . In other words, is the time at which the ratio

(4)

is maximal. The goal is to estimate and then maximize it

with respect to . Using the

trivial

identity

is the

maximum of the drifted Brownian motion over . Note that

throughout this paper, we will use as the running time and as a

fixed time.

Let us consider the random variable at a fixed time

and let

denote its probability density function (pdf). Once we know

, then from Eq. (6), we can evaluate

(8)

To evaluate the pdf , we need the joint pdf of and

at fixed .

III Joint distribution of and

It is convenient

to compute first the cumulative probability

(9)

where the walk starts at the origin and is the

global maximum of the walk in . This cumulative probability

can be computed using a path-integral approach as detailed below.

Clearly is the probability that a drifted Brownian motion

in , starting from , reaches at a

fixed time and in addition, stays below the level for all .

The last condition comes from the fact that if the global maximum ,

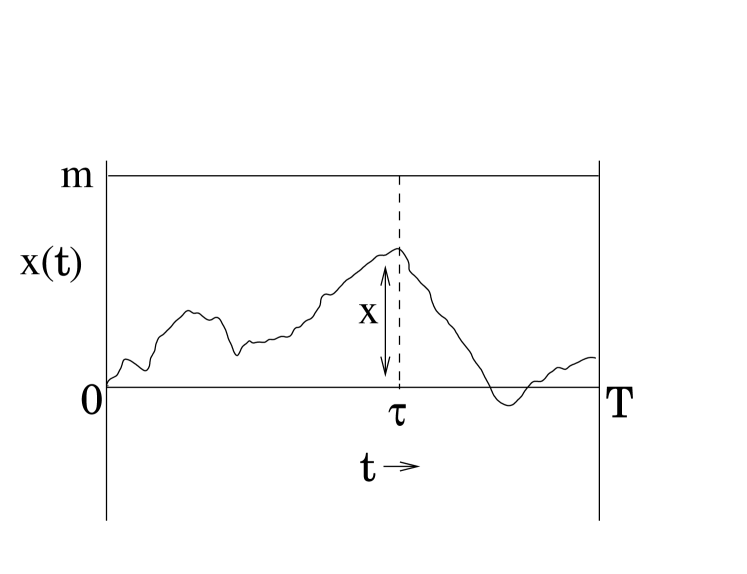

the path necessarily stays below the level for all . An example of

such a path is seen in Fig. 2.

Figure 2: A realization of the drifted Brownian motion in ,

starting at , reaching at and staying below the

level for all .

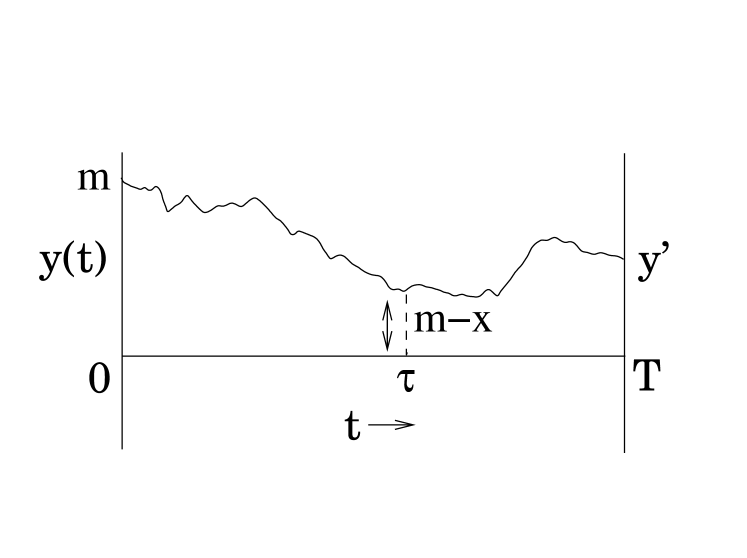

To compute , it is convenient to consider the shifted process

so that the process evolves, as

(10)

Thus the shifted process represents a Brownian motion with a drift

, opposite to that of . In terms of the process ,

is just the probability that the process , starting at , reaches

the point at and stays positive in the whole interval

. An example of such an event is shown in Fig. 3

Figure 3: A realization of the shifted Brownian motion with

drift in ,

starting at , reaching at and staying positive

for all .

For the process in Eq.

(10),

let us first define the propagator that denotes the

probability that the process starting at at , reaches at time ,

but staying positive in between, i.e., in . One can then easily

express in terms of this propagator as (see Fig. 3)

(11)

In writing Eq. (11), we have split the interval into two

parts: and . In the first interval (see Fig. 3), the

process propagates from the initial position to

in time (staying positive in between), hence explaining the first factor

in Eq. (11). In the second interval, the process starting at

the new ‘initial’ position , propagates to a final position

in time , staying positive in between. Also, the final position

can be any positive number and one has to integrate over it. This

explains the second factor in Eq. (11). Of course, in writing

the path decomposition in Eq. (11) we have used the renewal property of a

Brownian motion (valid due to its Markovian nature) which implies that the two intervals (left of

and right of

) are statistically independent.

Evaluation of the propagator : Using a physicist

interpretation of Eq. (10), we note that the Langevin noise is a Gaussian

white noise with the associated measure, . Substituting, from Eq. (10),

one can express the propagator as a path integral

(12)

where is an indicator function that enforces the path to stay positive in

the interval . The rhs of Eq. (12) can be rearranged (by expanding

the square and performing the time integral) as

(13)

where is the propagator associated with the driftless Brownian motion

(14)

This propagator, which denotes the probability that a driftless Brownian motion

propagates from to in time without crossing the origin in between,

can be evaluated

very simply by the standard method of images Feller ; Redner or

alternatively by the path integral method BF and has the

well known expression

(15)

Substituting this in Eq. (13), one then has the required propagator.

Using this explicit expression for one can also

easily evaluate the following integral

(16)

where is the complementary

error function.

Assembling these results in Eq. (11) gives us an explicit expression for

the cumulative probability

(17)

The joint pdf of at fixed and can then

be

obtained by taking the derivative of with respect to , i.e.,

(18)

IV Evaluation of the relative error

Having obtained the joint pdf in Eqs. (18)

and (17), we can easily find the pdf of the variable

(19)

The above integral can be performed exactly (we skip the details here). One obtains

the following expression

(20)

where

(21)

(22)

Note from the explicit expression of the following symmetry

(23)

which has the simple physical meaning of time-reversal symmetry, i.e., when the

process propagates in the reverse time direction, one gets the same measure

provided one also reverses the sign of the drift .

Having obtained the pdf , one can then evaluate the relative

error where

(24)

Evidently also has the same time-reversal symmetry namely

(25)

While it is difficult to do the integral in Eq. (24) analytically,

one can easily evaluate it

using Mathematica. Besides, the general feature of as a function

of can be inferred by just studying the asymptotic properties of the integral in Eq.

(24) in the

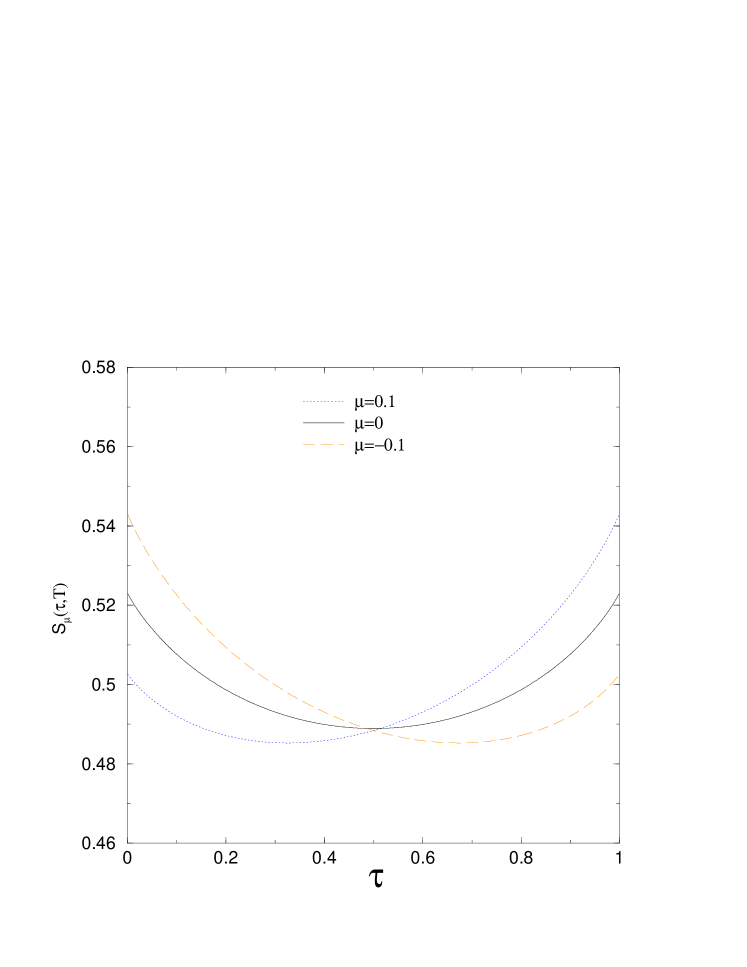

limit and . In Fig. 4, we

show a

plot of for three different values

of , and upon setting and .

Figure 4: Plots of vs. obtained from Eq. (24) for three different

values of the drift

, and . We have set and . The symmetry

is

evident.

Optimal Time : To find the optimal time we need to minimize

, i.e., maximize with respect to . It is

evident from Fig. 4 and also from the expression of that for all values of ,

has two local maxima at the endpoints of the interval , i.e., respectively

at

and . However, for , the maximum at has a larger value implying

that for , . By the symmetry manifest in it

follows that for , the maximum at has a higher value implying for .

Exactly at , both local maxima at and have the same value

( is completely symmetric around the midpoint ) implying that

for , both and are optimal.

The optimal value is actually easier to evaluate since for or

(at the end-points), the integral in Eq. (24) can be carried out explicitly.

Omitting details of this integration, we get the following expression for the optimal relative error

for all

(26)

Note that the optimal relative error is evidently a symmetric function of as manifest

in the above result.

In the preceeding paper SXZ , Shiryaev, Xu and Zhou also obtained an expression of

the optimal relative error by a completely different method.

Their notations are slightly different from above. In their notation,

and also their result for is in terms of the probability distribution of a Gaussian

random variable

with zero mean and unit variance,

which is related to the complimentary error function via

(27)

However, their method allows them to obtain an explicit expression for the optimal relative error

only in the range (i.e., ) and (i.e., ).

In these ranges, their expressions for the optimal relative error (Eqs. (9) and (11) in SXZ )

reduce precisely to our compact result in Eq. (26), upon identifying

and as in Eq. (27). However,

they do not have any result in the range , i.e., for . In contrast,

our result in Eq. (26) is valid for all (and hence for all ) and

is therefore more general. In addition, their method somehow does not detect the symmetry

of under which is manifest in our path integral approach.

V The exact distribution of the time of the occurrence of the maximum for a Brownian

motion

with drift

Minimizing the relative error with respect to is one way of estimating

the optimal time at which one should sell a stock over a fixed investment time

horizon , as explained above. Another alternative and direct measure would be to

first derive the probability density of the time at which the maximum of a

stock price over actually occurs. This density will typically have

a peak (or more peaks). The value of at which the strongest peak of

occurs can then be taken as an alternative measure for the optimal time to sell a stock, since the

maximum of the price is most likely to occur at .

In this section, we compute exactly the density of for a Brownian motion

with

drift .

Since the stock price is just the exponential of under the Black-Scholes

scenario,

the maximum of the stock price occurs exactly at the same time where

itself achieves its maximum.

For the case , the density was computed by Lévy Levy and is given

by the derivative of an arcsine form, i.e.,

(28)

Recently, using an appropriate path integral method, the density of was computed exactly for a

Brownian motion up to

its first-passage time RM and also for a variety of constrained Brownian motions

such as Brownian excursions, Brownian bridges, Brownian meanders etc. MRKY . Here we adapt

this

path integral method to compute the density for a Brownian motion

with arbitrary drift .

To compute the density the strategy would be to first compute

the joint density of as well as the maximum itself, i.e.,

and then integrate over to obtain the marginal density, . The joint density is the proportional to the

sum of the statistical weights of all paths that start at the origin , reaches

the value for the first-time at and then stays below the level

at all subsequent times up to ,i.e., in the interval . To enforce the conditions

that in the two intervals and and that

exactly at the

path reaches

, poses a problem for a continuous-time

Brownian motion. This is because if a Brownian motion crosses a level at a given time

then it must cross and re-cross the same level an infinite number of times in the

vicinity of . Hence it is impossible to enforce the above constraints simultaneously for

a continuous-time Brownian motion. Note that for lattice random walks this

does not pose any problem. To get around this

difficulty with the continuous-time Brownian motion,

one introduces a small cut-off RM ; MRKY , i.e., one assumes that the path, starting

at

reaches the level at time , staying below for all

and then starting at at stays below the level for all (see

Fig. 5 for such a realization). Finally one takes the limit

at the

end of the calculation.

Figure 5: A realization of the drifted Brownian motion in ,

starting at , reaching at and staying below the

level for all .

Comparing Figs. (2) and (5), it is clear that the paths that contribute to the joint probability

density are identical to those that contribute to

with the replacements and in Eq. (17), i.e.,

. Substituting

and in Eq. (17) and taking the limit

we find, to leading order in ,

(29)

where the constant of proportionality , which is function of , is determined

from the normalization, .

This fixes . Integrating (now the cut-off

has been set to ) over finally gives the marginal density

in a closed form

(30)

where

(31)

The density given in Eqs. (30) and (31) is the main result of

this section.

Evidently, for , one recovers from this the well known arcsine result of Lévy in Eq.

(28).

Note that the density also has a symmetry similar to that in Eq. (25)

namely

(32)

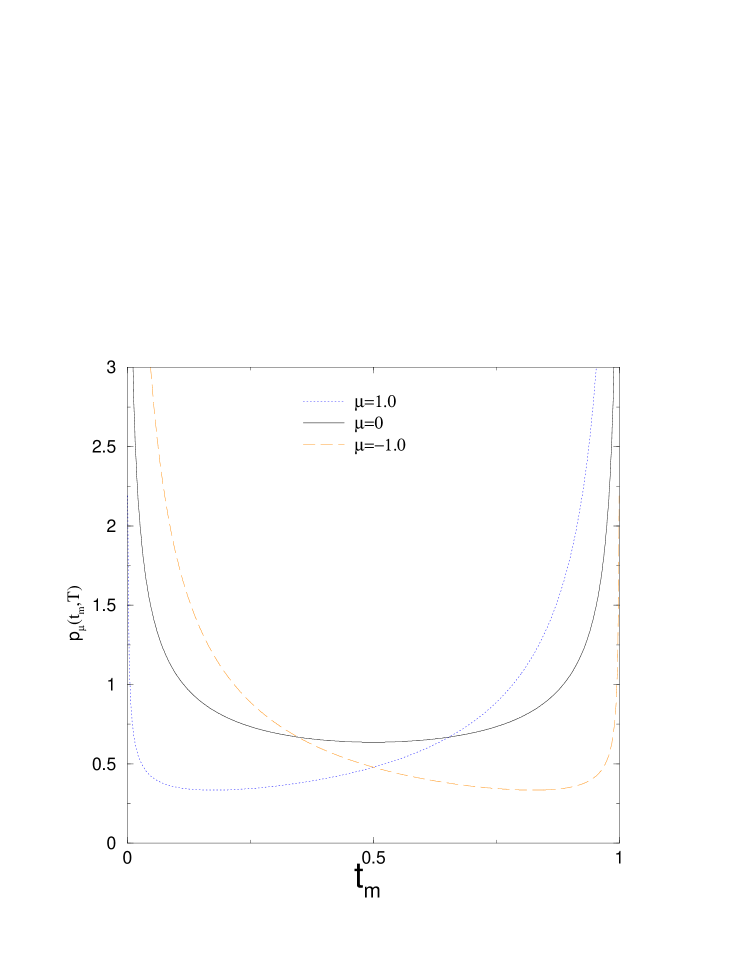

This symmetry is also evident in Fig. 6 where we plot the density in Eq.

(30) for , and upon setting and .

Figure 6: Plots of vs. for three different values of the drift

, and . We have set and . The symmetry

is

evident.

We note from Eq. (30) as well as from Fig. 6 that for all values of , the density

has two peaks (actually has square root divergences) at the two end points

and ,

(33)

(34)

where the amplitude

(35)

However, for , the divergence at is stronger than that at since . On the other hand, for , the opposite is true. At , both ends have

the same divergences as the density is completely symmetric around . Thus, we conclude

that the maximum of the Brownian motion with drift is most likely to occur at

for , at for , and for both and are equally likely.

This then leads us to identify the optimal time to sell the stock (within the black-Scholes

economy model) to be for , for , and (equally

likely) for . Thus, based on the analysis of the density

we draw the same

conclusion as was obtained from the optimization of the relative error in the previous sections.

References

(1) A. Shiryaev, Z Xu, and X.Y. Zhou, Thou Shalt Buy and Hold, Quantitative Finance (2008),

preceeding paper.

(2) M. Dai, H. Jin, Y. Zhong, X.Y. Zhou, working paper, 2008.

(3) S.N. Majumdar, Brownian Functionals in Physics and Computer Science, Current

Science, 89, 2076 (2005) (also available at cond-mat/0510064).

(4) S.N. Majumdar, J. Randon-Furling, M.J. Kearney, and M. Yor, On the Time to Reach

Maximum for a Variety of Constrained Brownian Motions, J. Phys. A: Math. Theor. 41, 365005 (2008).

(5) W. Feller, An Introduction to Probability Theory and Its

Applications, vol-I and II (Wiley, New York, 1968).

(6) S. Redner, A Guide to First-passage Processes

(Cambridge University Press, Cambridge 2001).

(7) P. Lévy, Sur Certains Processus Stochastiques Homogènes, Composition

Mathematica, 7, 283 (1939).

(8) J. Randon-Furling and S.N. Majumdar, Distribution of the Time at which the

Deviation of a Brownian Motion is Maximum before its

First-passage Time, Journal of Stat. Mech.: Th. and Exp. P10008 (2007).