Exponential functionals of Brownian motion and class-one Whittaker functions

Abstract

We consider exponential functionals of a Brownian motion with drift in , defined via a collection of linear functionals. We give a characterisation of the Laplace transform of their joint law as the unique bounded solution, up to a constant factor, to a Schrödinger-type partial differential equation. We derive a similar equation for the probability density. We then characterise all diffusions which can be interpreted as having the law of the Brownian motion with drift conditioned on the law of its exponential functionals. In the case where the family of linear functionals is a set of simple roots, the Laplace transform of the joint law of the corresponding exponential functionals can be expressed in terms of a (class-one) Whittaker function associated with the corresponding root system. In this setting, we establish some basic properties of the corresponding diffusion processes.

keywords:

[class=AMS]1 Introduction

Let be a standard one-dimensional Brownian motion with drift . In the paper [19], Matsumoto and Yor consider the process

and prove that it is a diffusion process with infinitesimal generator given by

| (1) |

where is the Macdonald function. As explained in [19], this theorem can be regarded, by Brownian scaling and Laplace’s method, as a generalization of Pitman’s ‘’ theorem [26, 27] which states that, if , then is a diffusion process with infinitesimal generator given by

| (2) |

Note that and . Suppose . Then the diffusion with generator (2) can be interpreted as a Brownian motion with drift conditioned to stay positive. Similarly, the diffusion with generator (1) can be interpreted as the Brownian motion conditioned on its exponential functional having a certain distribution (a Generalised Inverse Gaussian law) in a sense which can be made precise [2, 3]. The relevance of these interpretations in the present context is as follows.

Set and let be an independent copy of which is also independent of . Then the process has the same law as and, moreover, . This is well-known and can be seen for example as a consequence of the classical output theorem for the queue [24]. From this we can see that the process has the same law as that of conditioned (in an appropriate sense) on the event that ; in other words, is a diffusion with infinitesimal generator given by (2), started from zero. This basic idea can be used to obtain a multi-dimensional version of Pitman’s theorem [4, 5, 25], which gives a representation of a Brownian motion conditioned to stay in a Weyl chamber in as a certain functional (which generalizes ) of a Brownian motion in .

Similarly [19], if is an independent copy of , which is also independent of , then the process

has the same law as and, moreover, . This time, we conclude that, for each , the process

the same law as that of conditioned on the event . Carefully letting yields the theorem of Matsumoto and Yor [2]. As explained in [22], the probabilistic proofs of the multi-dimensional versions of Pitman’s theorem given in the papers [4, 25] carry over, in the same way, to the exponential functionals setting, although the task of letting the analogue of go to zero is a highly non-trivial problem in the general setting. Nevertheless, it gives a heuristic derivation that a certain functional of a Brownian motion in should have the same law as a Brownian motion conditioned on a certain collection of its exponential functionals. This leads us to the question considered in the present paper.

We consider a Brownian motion in with drift , and a collection of linear functionals such that the exponential functionals

are almost surely finite. Our aim is to understand which diffusion processes can arise when we condition on the law of . The first step is to understand the law of . We show that the Laplace transform of satisfies a certain Schrödinger-type partial differential equation and proceed to characterise all diffusion processes which can be interpreted as having the law of conditioned on the law of .

In the case when is a simple system (see section 4 below for a definition), these diffusion processes are closely related to the quantum Toda lattice. The Schrödinger operator is

where , and the corresponding diffusion process has infinitesimal generator given by

| (3) |

where is a particular eigenfunction of known as a class-one Whittaker function. In the case and , the class-one Whittaker function is and the infinitesimal generator is given by (1). More generally, for a simple system , the diffusion process with generator given by (3) plays an analogous role, in the exponential functionals setting, as that of a Brownian motion conditioned to stay in the Weyl chamber . These processes have already found an application in the paper [23], where the corresponding multi-dimensional version of the above theorem of Matsumoto and Yor in the ‘type A’ case has been proved and used to determine the law of the partition function associated with a directed polymer model which was introduced in the paper [24].

The outline of the paper is as follows. In section 2 we work in a general setting and establish a Schrödinger type partial differential equation satisfied by the characteristic function of exponential functionals of a multidimensional Brownian motion. We also study a family of martingales related to the conditional laws of exponential functionals that will later appear. In section 3, we identify a family of diffusions which can be interpreted as having the law of the Brownian motion with drift conditioned on the law of its exponential functionals. In section 4, we restrict our attention to the case where the collection of vectors used to define the exponential functionals is a simple system, and give an overview of relevant facts about class-one Whittaker functions. In section 5, we study properties of the conditioned processes in this setting. In the final section, we present some explicit results for the ‘type ’ case.

2 Exponential functionals and associated partial differential equations

In this section, we work in a general setting and establish a Schrödinger type partial differential equation satisfied by the characteristic function of exponential functionals of a multidimensional Brownian motion. We also study a family of martingales related to the conditional laws of exponential functionals that will later appear.

Let be a collection of distinct, non-zero vectors in such that

| (4) |

is non-empty. Let be a standard Brownian motion in with drift . For , set

Here, where denotes the usual inner product on .

2.1 Partial differential equation for the characteristic function

The process is a diffusion with generator

We first check that this operator is hypoelliptic.

Proposition 2.1.

The operator

is hypoelliptic on and therefore, for the random variable admits a smooth density with respect to the Lebesgue measure.

Proof.

We use Hörmander’s theorem. Since the ’s are pairwise different and non zero, there exists such that

Consider now the vector field

and let us denote

The Lie bracket between and is given by

Similarly, by iterating this bracket times, we get

Since the ’s are pairwise different and non zero, we deduce from the Van der Monde determinant that at every the family

is a basis of . It implies that the Lie bracket generating condition of Hörmander is sastisfied so that the operator is hypoelliptic. ∎

Let now and, for , define

and

Proposition 2.2.

-

1.

The semigroup generated by the Schrödinger operator

admits a heat kernel and we have

-

2.

The function is the unique bounded function that satisfies the partial differential equation

and the limit condition

Proof.

-

1.

It is a straightforward consequence of the Feynman-Kac formula that exists and is given by

Integrating this with respect to , we obtain

-

2.

It is again a straightforward consequence of the Feynman-Kac formula that solves the partial differential equation, and the limit condition is easily checked. Let us now prove uniqueness. We have to show that if is a bounded solution of the equation that satisfies

then . For that, let us observe that under the above conditions, for , the process

is a bounded martingale that goes to 0 when . It follows that this martingale is identically zero almost surely, which implies .

∎

For later reference, we rephrase the second part of the previous proposition as follows:

Corollary 2.3.

The function is the unique solution to

| (5) |

such that is bounded and

Example 2.1.

The following example has been widely studied (see, for example, [8, 19] and references therein). Suppose , and . Then

where is a standard one-dimensional Brownian motion, and

In this case, solves the equation

This equation is easily solved by means of Bessel functions. By taking into account the boundary condition when , we recover the formula [19, Theorem 6.2]:

| (6) |

where is the Macdonald function [18]:

| (7) |

The formula (6) can also be derived using the fact [8] that has the same law as , where is a gamma distributed random variable with parameter .

Example 2.2.

The following example has also been studied in the literature [12, 14]. Suppose , , , and . Then

where is a standard one-dimensional Brownian motion, and

In this case, solves the equation

This is Schrödinger’s equation with the so-called Morse potential. It is solved by means of Whittaker functions and by taking into account the boundary condition when , we get

where is the Whittaker function (see [18, pp.279]):

2.2 Conditional densities

We prove now that the random variable has a smooth density with respect to the Lebesgue measure of and morever give an expression of the conditional densities only in terms of this density.

Proposition 2.4.

The random variable has a smooth density with respect to the Lebesgue measure of and for

where is the natural filtration of .

Proof.

If we denote by the characteristic function of :

then,

Therefore, the process is a martingale. This implies that the function is harmonic for the operator . This operator being hypoelliptic, this implies that has a smooth density with respect to the Lebesgue measure of . The result about the conditional densities stems from the injectivity of the Laplace transform. ∎

In particular, we deduce from the previous proposition that if for , we denote

for , then the process is a martingale. It implies that for any , satisfies the following partial differential equation:

It also implies that is a solution of the partial differential equation:

Example 2.3.

Suppose , and . Then is distributed as , where is a gamma law with parameter , that is

and we have

Example 2.4.

Suppose , , and . Then, as seen before,

and for ,

By using in the previous integral the change of variable , we deduce the following nice formula

This conditional Laplace transform can be inverted (see for instance [9]) but, unlike the one-dimensional case, it does not seem to lead to a nice formula for :

where is the parabolic cylinder function such that

that is

3 Brownian motion conditioned on its exponential functionals

In this section, we study the Doob transforms of the process associated with the conditioning of . We first start with the bridges which are the extremal points.

Lemma 3.1 (Equation of the bridges).

Let . The law of the process conditioned by

solves the following stochastic differential equation:

where, is a standard Brownian motion

Proof.

This follows directly from Proposition 2.4 and Girsanov’s theorem. ∎

Example 3.1.

The following example is considered [21]. Suppose , and . Then the equation becomes

Let be the law of and be the coordinate process on the space of continuous functions . If is a probability measure on , in what follows (see [3]), we call the probability

the law of the process conditioned by

Proposition 3.1.

Let be a bounded and positive function such that . The law of the process conditioned by

solves the following stochastic differential equation:

where, is a standard Brownian motion and is given by

with

Proof.

Following [3], we have to write the stochastic differential equation associated with the conditioning

But

so that we get the expected conditioned stochastic differential equation by Girsanov theorem.

∎

In the previous proposition, the drift depends only on if, and only if,

for some . Therefore:

Corollary 3.2.

For , the law of the process conditioned by

is the law of a Markov process. Moreover, in that case, it solves in law the following stochastic differential equation

| (8) |

We now show that the pathwise uniqueness property holds for the stochastic differential equation (8). In what follows, we denote

Let us observe that for the generator , we have a useful intertwining with the Schrödinger operator that will be used several times in the sequel.

Proposition 3.3.

Proof.

If is a smooth function then we have

Since

the result readily follows. ∎

We can now deduce:

Theorem 3.1.

Let . If is a Brownian motion, then for , there exists a unique process adapted to the filtration of such that:

| (9) |

Moreover, in law, the process is equal to conditioned by:

Proof.

Let . Since the function is locally Lipschitz, up to an explosion time we have a unique solution for the equation (9). Our goal is now to show that almost surely . For that, we construct a suitable Lyapunov function for the generator .

Let

It is easily seen that when , . Moreover, from the intertwining,

Therefore

It implies that the process is a positive supermartingale. Since when , we deduce that almost surely .

Example 3.2.

Suppose and and . Then

| (10) |

Let us denote the heat kernel of . From the intertwining, we have

where is the heat kernel of . This kernel can be explicitly computed (see [1] or [20, Remark 4.1]):

with

We deduce from that

so that is an entrance point for the diffusion with generator .

The resolvent kernel of is also easily computed:

And we can observe that

Example 3.3.

The resolvent kernel of , is for :

and we get:

so that is also an entrance point for the diffusion with generator .

Motivated by the two previous examples, the question of existence of entrance laws for the diffusion with generator is natural. As a general result, we can prove:

Proposition 3.4.

Assume , and , then is an entrance point for the diffusion with generator .

Proof.

Without loss of generality, we can assume that . Let us recall solves the Schrödinger equation

and that solves the equation:

Let . Since

we deduce that is increasing. Moreover, it is easily seen that . Therefore . Hence .

Now, from the comparison principle for stochastic differential equations, we deduce that if, for , we denote and the solutions of the stochastic differential equations,

where is a standard Brownian motion, then we have almost surely

Since is an entrance point for the diffusion , we deduce that is an entrance point for the diffusion with generator .

∎

We conjecture the existence of entrance laws for , but let us observe that, in general, we do not have unicity. Indeed, let us consider the following example

In that case, by using one dimensional results, we compute:

where . The heat kernel of is also explicitly given by

And we deduce that when with ,

Therefore, in that case we get an infinite set of entrance laws when .

4 Whittaker functions

From now on we consider the case where is a simple system. In other words:

-

1.

The vectors are linearly independent;

-

2.

the group generated by reflections through the hyperplanes

is finite;

-

3.

is a fundamental domain for the action of on ;

-

4.

for all .

In this setting, the Schrödinger operator

is the Hamiltonian of the (generalized) quantum Toda lattice (see, for example, [28]). The function considered in the previous section can be expressed in terms of a particular eigenfunction of , known as a class-one Whittaker function.

4.1 Class one Whittaker functions

Class one Whittaker functions associated with semisimple Lie groups were introduced by Kostant [17] and Jacquet [15], and have been studied extensively in the literature. They are closely related to Whittaker models of principal series representations and play an important role in the study of automorphic forms associated with Lie groups [6]. They also arise as eigenfunctions of the (generalised) quantum Toda lattice [17, 28]. For completeness we will describe briefly the abstract definition of class-one Whittaker functions, following [13].

Let be a connected, noncompact, semisimple Lie group with finite centre. Let be the Lie algebra of with complexification . Denote by the Killing form on . Let be a maximal compact subgroup of with Lie algebra and denote the complexification of by . Let be the orthogonal complement of in with respect to the Killing form. Let be the corresponding Cartan involution. Let be a maximal abelian subspace in and denote its complexification by . Denote by the set of all non-zero roots of relative to . For , denote by the dimension of the root space

Let be a positive system of roots in and let be the corresponding set of simple roots. Let and . Then is an Iwasawa decomposition of . Let be a non-degenerate (unitary) character of . Let be the unique Lie algebra homomorphism of into such that for . For each , let be a basis of satisfying . Denote by the restriction of to and set . Denote by and the universal enveloping algebras of and , respectively. Let denote the Harish-Chandra homomorphism from , the centraliser of in , into . For and , define . The space of Whittaker functions on associated with , denoted , is the space of smooth functions on which satisfy:

-

1.

for , and , and

-

2.

for .

Set . For , define where is the Iwasawa decomposition of . Let be the longest element in . The class-one Whittaker function associated with is defined by

| (11) |

The convergence of this integral was established by Jacquet [15]. For and , write . Let

We record the following lemma for later reference.

Lemma 4.1.

Let . Then is uniformly bounded for .

Proof.

Remark 4.1.

In the above, is the Harish-Chandra -function.

4.2 Fundamental Whittaker functions

Since , all of the important information about is contained in its restriction to . This leads to a more concrete description which can be presented entirely in the context of the root system . Readers not familiar with root systems may find it helpful to think of the ‘type ’ case, for example if . In this case, we can identify (and its dual) with

and take , and , where is the standard basis for . In general, the root system is crystallographic, that is, the numbers are all integers, and the -span of is a regular lattice in . Since the Killing form is positive definite on , it induces an inner product on , which extends to a nondegenerate bilinear form on . The following construction is due to Hashizume [13]. Consider the lattice , and set For each , define a set of real numbers recursively as follows. Set and

| (12) |

with the convention that if . In [13] it is shown that the series

converges absolutely and uniformly for and . Define to be the set of such that:

-

1.

for all ;

-

2.

for all ;

-

3.

for any pair such that .

For denote by the length of . For , define , recursively as follows. For ,

where

If and such that , then

Let be the set of such that is not a root. The Harish-Chandra -function is given by

where

and

Now define, for ,

| (13) |

Observe that satisfies the functional equations

| (14) |

Although the above construction places a restriction on , it is known that, for each , can be extended to an entire function of . In [13] it is shown that, for , , so that

The functions defined by

are called fundamental Whittaker functions. In [13] it is also shown that, for each , form a basis for .

4.3 The quantum Toda lattice

As observed by Kostant [17], Whittaker functions are eigenfunctions for the (generalised) quantum Toda lattice. Denote by the Laplacian on corresponding to the Killing form. For , the class-one Whittaker function (as a function on ) satisfies the partial differential equation

| (15) |

For , this can be seen directly via the recursion (12) for the coefficients in the series expansion of the fundamental Whittaker functions . In [13, Lemma 7.1] it was shown that, for ,

| (16) |

By lemma 4.1, if , then is uniformly bounded for . Recalling Corollary 2.3—note that the proof of uniqueness given there is valid for —we deduce the following characterisation of .

4.4 Weyl-invariant class-one Whittaker functions and an alternating sum formula

In this section we present a variation of the formula (13) which generalises a formula given in [16] for the case and leads naturally to a normalisation for the class-one Whittaker functions which is invariant under the Weyl group . Using this, we also confirm a conjecture of Stade [29] that a class-one Whittaker function can be expressed as an alternating sum of appropriately normalised fundamental Whittaker functions.

Let

Proposition 4.2.

For ,

Proof.

From (13) we have

It therefore suffices to show that, for all ,

We prove this by induction on . If , we have

Using the duplication formula

| (17) |

we can write

and so

Thus,

and the claim is proved for . For and with ,

by the induction hypothesis. ∎

Consider the normalised Whittaker functions

By the above proposition and the functional equation

| (18) |

we have:

Corollary 4.3.

For ,

where

In particular, satisfies the functional equation

4.5 The type case.

Let . Then we can identify with , and take , and . Let . Then . For , write . The recursion (12) becomes with . The solution is given by

and so

where is the modified Bessel function of the first kind. In this case, acts on by multiplication. By the duplication formula (17), we have

Thus, using the functional equation (18), we obtain

where

is the Macdonald function. Note that and the normalised Whittaker functions are given by and .

4.6 The type case.

In this case we can identify with and take , where is the standard basis for . Set , and . For and , write . Set and . Then the recursion (12) becomes

where and for . The solution is given by the following formula, due to Bump [6]:

where

The following integral representation is due to Vinogradov and Takhtadzhyan [30]:

| (19) |

For , we have the following simplification:

Using the integral representation (19), Bump and Huntley [7] derived an asymptotic expansion of which is valid for large values of and . The leading term in the expansion is independent of the parameter and given by

| (20) |

From this we deduce the following lemma, which we record for later reference.

Lemma 4.2.

Let . If with , then

where

4.7 Asymptotics for large

Consider the analytic function on defined by

where . Set

and

Proposition 4.4.

Let . For all and ,

5 Whittaker functions and exponential functionals of Brownian motion

Define for . Throughout this section we will identify with via the Killing form and note that . Let be a Brownian motion in with covariance given by the Killing form and drift . Then, by Corollary 2.3 and Proposition 4.1, we have:

Proposition 5.1.

In this context, the diffusion considered in section 3 has generator given by

Note that this is well-defined for all . Set

and write . It follows from the intertwining

| (21) |

that the heat semigroup associated with is given by

| (22) |

where is the heat semigroup associated with .

Let and consider the operator , defined (on a suitable domain) by

where . Set . In the type and cases, for each , is a non-negative definite function of and hence is a Markov operator. For the type case, this follows from the integral representation (7) and, for the type case, it follows from the integral representation (19). We remark that in fact it can be seen from an integral formula of Givental [11] in the type case. We conjecture that is a Markov operator, in general. In the type case, it is shown in [19] that intertwines the semigroup associated with with the semigroup of a Brownian motion with drift . This intertwining relation extends to the general setting:

Proposition 5.2.

On a suitable domain,

Proof.

5.1 Brownian motion in a Weyl chamber and Duistermaat-Heckman measure

Let and, for , define . By Proposition 4.4, the diffusion with generator

converges weakly as to a Brownian motion with drift conditioned (in the sense of Doob) never to exit the Weyl chamber (see [4] for a definition of this process). In the limiting case , the generator of the Brownian moton conditioned never to exit is given by

where . Note also that, as ,

Thus, the intertwining operator converges, in a weak sense, to a positive integral operator with kernel given by , where is the Duistermaat-Heckman measure associated with the point , characterised by

This operator is discussed in [4]. The intertwining

plays a meaningful role in the multi-dimensional generalisations of Pitman’s theorem obtained in [4, 5, 25]. The operator has recently been shown to play a similar role in the multi-dimensional version of the theorem of Matsumoto and Yor obtained in [23] for the type case; it is a positive integral operator with a kernel which can be interpreted as a kind of ‘tropical’ analogue of the Duistermaat-Heckman measure.

6 The type case

Consider the type case, as in section 4.6. For , and . The Weyl chamber is . Let be a Brownian motion in with drift . For , set

Let . Then, in the notation of section 4.6,

Note that, for ,

By Proposition 5.1 and the integral formula (19),

Let us observe that this Laplace transform can be inverted. Indeed, by using the fact that

we obtain

and therefore, denoting the density of , we get

6.1 The intertwining kernel

Suppose . The intertwining operator satisfes . Let , and write . By the integral formula (19),

where , and . It follows, by a straightforward calculation, that we can write

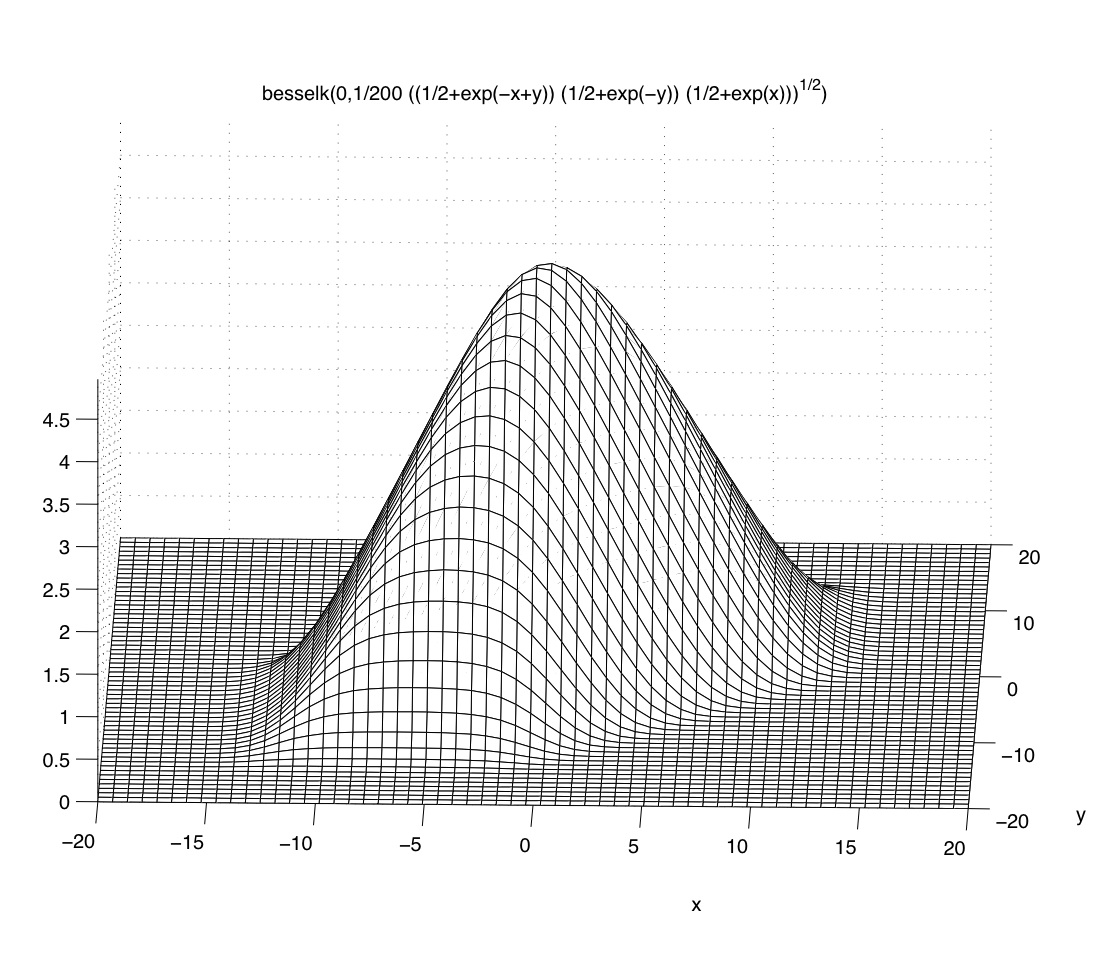

where

A plot of , with fixed, is shown in Figure 1. As explained in [23], the measure with density given by can be interpreted as a kind of ‘tropical’ analogue of the Duistermaat-Heckman measure associated with the point .

6.2 Behaviour at

From the asymptotic expansion of [7], for any we have as (in the sense that and ). This suggests that the process with generator

has a unique entrance law starting from , given by

where, for each ,

The existence of this entrance law is established (more generally, for type ) in the paper [23]. It is clear from the proof given there that it should be unique. On the other hand:

Proposition 6.1.

Let be the diffusion with generator started at . If and , with , then

converges in probability to , where

Proof.

Acknowledgements. We are grateful to the anonymous referees for helpful suggestions. Research of second author was supported in part by Science Foundation Ireland grant number SFI 04-RP1-I512.

References

- [1] L. Alili, H. Matsumoto and T. Shiraishi. On a triplet of exponential brownian functionals. Séminaire de probabilités de Strasbourg, 35 (2001) 396–415.

- [2] F. Baudoin. Further exponential generalization of Pitman’s theorem. Electron. Comm. Probab. 7 (2002), 37–46 (electronic).

- [3] F. Baudoin. Conditioned stochastic differential equations: Theory, Examples and Applications to finance, Stoch. Proc. Appl., Vol. 100, 1, pp. 109-145, (2002).

- [4] Ph. Biane, Ph. Bougerol and N. O’Connell. Littelmann paths and Brownian paths. Duke Math. J. 130 (2005), no. 1, 127–167.

- [5] Ph. Bougerol and T. Jeulin. Paths in Weyl chambers and random matrices. Probab. Theory Related Fields 124 (2002), no. 4, 517–543.

- [6] D. Bump. Automorphic forms on GL(3,. Lecture Notes in Mathematics, 1083. Springer-Verlag, Berlin, 1984.

- [7] D. Bump and J. Huntley. Unramified Whittaker functions for . J. Anal. Math. 65 (1995) 19-44.

- [8] D. Dufresne. The integral of geometric Brownian motion. Adv. Appl. Prob. 33 (2001) 223 241.

- [9] R. Ghomrasni. On distribution associated with the generalized Levy’s stochastic area formula. StudiaSci. Math. Hungar. Vol. 41, No. 1 (2004), 93-100.

- [10] S.G. Gindikin and F.I. Karpelevich. The Plancherel measure for Riemannian symmetric spaces with non-positive curvature. Dokl. Akad. Nauk USSR 145 (1962) 252–255.

- [11] A. Givental. Stationary phase integrals, quantum Toda lattices, flag manifolds and the mirror conjecture. Topics in Singularity Theory, AMS Transl. Ser. 2, vol. 180, AMS, Rhode Island (1997) 103–115.

- [12] C. Grosche. The path integral on the Poincaré upper half-plane with a magnetic field and for the Morse potential. Ann. Phys. 187, No. 1 (1988) 110-134.

- [13] M. Hashizume. Whittaker functions on semisimple Lie groups. Hiroshima Math. J. 12 (1982), no. 2, 259–293.

- [14] N. Ikeda and H. Matsumoto. Brownian motion on the Hyperbolic plane and Selberg trace formula. J. Func. Anal. 163 (1999), 63-110.

- [15] H. Jacquet. Fonctions de Whittaker associées aux groupes de Chevalley. Bull. Soc. Math. France 95 1967 243–309.

- [16] S. Kharchev and D. Lebedev. Integral representations for the eigenfunctions of a quantum periodic Toda chain. Letters in Mathematical Physics 50 (1999), 53–77.

- [17] B. Kostant. Quantisation and representation theory. In: Representation Theory of Lie Groups, Proc. SRC/LMS Research Symposium, Oxford 1977, LMS Lecture Notes 34, Cambridge University Press, 1977, pp. 287–316.

- [18] N.N. Lebedev. Special Functions and their Applications. Dover, 1972.

- [19] H. Matsumoto and M. Yor. A version of Pitman’s theorem for geometric Brownian motions. C. R. Acad. Sci. Paris 328, Série 1 (1999) 1067–1074.

- [20] H. Matsumoto and M. Yor. Exponential functionals of Brownian motion, I: Probability laws at a fixed time. Probability Surveys 2005, Vol. 2, 312–347.

- [21] H. Matsumoto and M. Yor. A relationship between Brownian motions with opposite drifts. Osaka J. Math. 38 (2001).

- [22] N. O’Connell. Random matrices, non-colliding processes and queues. Séminaire de Probabilités, XXXVI, 165–182, Lecture Notes in Math., 1801, Springer, Berlin, 2003.

- [23] N. O’Connell. Directed polymers and the quantum Toda lattice. arXiv:0910.0069

- [24] N. O’Connell and M. Yor. Brownian analogues of Burke’s theorem. Stochastic Process. Appl. 96 (2001) 285–304.

- [25] N. O’Connell and M. Yor. A representation for non-colliding random walks. Elect. Commun. Probab. 7 (2002) 1-12.

- [26] J.W. Pitman. One-dimensional Brownian motion and the three-dimensional Bessel process, Adv. Appl. Probab. 7 (1975) 511-526.

- [27] L. C. G. Rogers and J. Pitman. Markov functions. Ann. Probab. 9 (1981) 573–582.

- [28] M. Semenov-Tian-Shansky. Quantisation of open Toda lattices. In: Dynamical systems VII: Integrable systems, nonholonomic dynamical systems. Edited by V. I. Arnol’d and S. P. Novikov. Encyclopaedia of Mathematical Sciences, 16. Springer-Verlag, Berlin, 1994, pp. 226–259.

- [29] E. Stade. Poincaré series for -Whittaker functions. Duke Math. J. 58 (1989) 695–729.

- [30] A. Vinogradov and L. Takhtadzhyan. Theory of Eisenstein series for the group and its application to a binary problem. J. Soviet Math. 18 (1982) 293–324.