Minimal Agent Based Model for Financial Markets I: Origin and Self-Organization of Stylized Facts

Abstract

We introduce a minimal Agent Based Model for financial markets to understand the nature and Self-Organization of the Stylized Facts. The model is minimal in the sense that we try to identify the essential ingredients to reproduce the main most important deviations of price time series from a Random Walk behavior. We focus on four essential ingredients: fundamentalist agents which tend to stabilize the market; chartist agents which induce destabilization; analysis of price behavior for the two strategies; herding behavior which governs the possibility of changing strategy. Bubbles and crashes correspond to situations dominated by chartists, while fundamentalists provide a long time stability (on average). The Stylized Facts are shown to correspond to an intermittent behavior which occurs only for a finite value of the number of agents . Therefore they correspond to finite size effect which, however, can occur at different time scales. We propose a new mechanism for the Self-Organization of this state which is linked to the existence of a threshold for the agents to be active or not active. The feedback between price fluctuations and number of active agents represent a crucial element for this state of Self-Organized-Intermittency. The model can be easily generalized to consider more realistic variants.

1 Introduction

In the past years there has been a large interest in the development

of Agent Based Models (ABM) aimed at reproducing and understanding the Stylized

Facts (SF) observed in the financial time series.

The simplest model of price time series is the Random Walk (RW)

introduced by Louis Bachelier in 1900 [1].

The availability of large amounts of data has revealed a variety of

systematic deviations from the RW which are the SF and are

relatively common to all markets.

As we are going to see the properties of the SF resemble Critical Phenomena

and Complex Systems with possible relations to various problems in Statistical

Physics. Many questions are however open and also how far one can go

with these similarities represents a highly debated problem.

The main SF, discussed in detailed in [2, 3, 4] are:

Absence of linear auto-correlations: It is not possible to

predict the direction of the next price change from the previous one.

Only at very short times (minutes or less) some correlations,

positive or negative,

can be present for technical reasons. This property corresponds to the

condition of an efficient market (no simple arbitrage), which implies

that it is not possible to make a profit without risk.

If such a possibility would

occur the market would immediately react and eliminate it.

Heavy Tails: The distribution of returns (price increments)

has a shape which

is markedly different from the Gaussian case (RW).

The probability for large positive or negative fluctuations is much

larger than for a Gaussian distribution. These fat tails have been

fitted in various ways and in some range they can be approximated by a power

law with an exponent ranging from 3 to 5.

This behavior is observed for time scales ranging from minutes to

weeks, while for very long times, a Gaussian distribution seems to be recovered.

Volatility Clustering: The variance of the returns shows a

long range correlation in time.

According to Mandelbrot [5, 6]: “large changes tend to be

followed by large changes, of either sign, and small changes tend to

be followed by small changes”. The correlation of the absolute values

of the square of the returns is usually fitted by a power law

(with exponents ranging from about zero to 1.0 and most probable value around

0.3) which can extend from minutes to weeks.

These three main SF have been interpreted in term of various phenomenological

stochastic models which permit in some cases an estimate of the risk

beyond the Black and Scholes model which corresponds to the simple RW

[6, 7, 8, 9, 10].

In our opinion it would be important to add the following additional elements

which are also essential to built a conceptual framework necessary to

understand market dynamics.

Nonstationarity and Time Scales: A characteristic of the

price dynamics is that it is not clear if one can define a probability

distribution which is stationary in time and, in any case,

it is not easy to estimate the appropriate time scale [11].

This is a crucial point that should be carefully analyzed in any statistical

treatment of the data.

Self-Organization:

A point which is usually neglected

is the fact that the stylized facts usually correspond to a particular situation

of the market. If the market is pushed outside such a situation, it will

evolve to restore it spontaneously.

The question is why and how all markets seem to self-organize in this

special state.

The answer to this question represents a fundamental point in understanding

the origin of the SF.

In this paper we discuss a minimal ABM [12]

which includes the following elements (first considered by Lux and Marchesi in [13, 14]):

-

•

fundamentalists: these agents have as reference a fundamental price derived from standard economic analysis of the value of the stock. Their strategy is to trade on the fluctuations from this reference value and bet on the fact that the price will finally converge towards the reference value. These traders are mostly institutional and their time scale is relatively long. Their effect is a tendency to stabilize the price around the reference value.

-

•

chartists: they consider only the price time series and tend to follow trends in the positive or negative direction. In this respect they induce a destabilizing tendency in the market. These traders have usually a time horizon shorter than the fundamentalists and they are responsible for the large price fluctuations corresponding to bubbles or crashes.

-

•

herding effect: this is the tendency to follow the strategy of the other traders. It should be noted that traders can change their strategy from fundamentalist to chartist and vice-versa depending on various elements.

-

•

price behavior: each trader looks at the price from her perspective and derives a signal from the price behavior. This signal will be crucial in deciding her trading strategy.

These four elements are, in our opinion, the essential irreducible

ones that an ABM should possess and we are going to describe

in detail their combined effects. Of course real market are extremely

more complex but the study of these elements represents a basis on which one

might eventually add more realistic features.

In this perspective we will try to construct a model which is the simplest

possible containing these four elements.

This permits to obtain

a detailed understanding of the origin and nature of the SF

and also to discuss their self-organization.

The main result of this paper is that the SF correspond to finite size

effect in the sense that they disappear in the limit of large

(total number of agents) or large time.

Given that the agents’ strategies can be defined for different time scales

this finite size effects can act at different time and

resemble power laws and critical exponents.

However, in our perspective, these exponents are essentially a fit to

the data without the important property of universality.

This situation has important implication both for the microscopic

understanding of the SF as well as for the analysis and interpretation of

experimental data.

The concept of self-organization arises very naturally from the introduction

of a threshold in the agents’ activity.

Namely a price which is very stable (which corresponds to a very large )

demotivates agents to trade this

stock and will naturally lead to a decrease of the number of agents.

On the other hand a small number of agents leads to large fluctuations

in the price which presents opportunities of arbitrage and this

will attract more traders.

So, in the end, the system will self-organizes around the number of

traders which corresponds to a situation of intermittency, leading to the SF.

This phenomenon does not correspond to self organized

criticality precisely but rather to a Self Organized Intermittency

(SOI) which occurs for a finite number of agents (on average).

In Sec. 2 we define the basic elements of the minimal ABM in the perspective

of its maximum simplification.

In Sec. 3 we consider in detail the fluctuations induced by the

herding dynamics.

In Sec. 4 we discuss the properties of the SF as arising from the model

for a specific range of parameters.

In Sec. 5 we give an interpretation to the SF in terms of semi-analytical

considerations.

In Sec. 6 we discuss the self-organization of the market dynamics

towards the self-organized regime with the SF.

In Sec. 7 we present our conclusions.

In the next paper [15]

we are going to focus on various statistical properties from

both a numerical and analytical point of view.

We will also discuss in some detail the differences between linear

and multiplicative dynamics.

In the present paper we only consider the linear dynamics for simplicity.

2 Definition of a minimal ABM with Fundamentalists and Chartists

In this section we are going to describe in detail the ABM

introduced in [12].

The model is constructed to be as simple as possible but

still able to reproduce the SF of financial time series.

This simplicity is very important because it permits to derive

a microscopic explanation of the SF in

term of the model parameters.

Elements which consider more realistic situations however can be added

in a systematic way.

This model is inspired by the well known Lux-Marchesi (LM)

model [13, 14]

but

it is much simpler with respect both to the number of parameters and

the rules for the dynamics.

In our model we consider a population of interacting agents which are divided into two main categories: fundamentalists and chartists.

The fundamentalist agents tend to stabilize the market driving the price

towards a sort of reference value

which we call the fundamental price ().

This kind of agents can be identified with long-term traders

and institutional traders [16].

Chartists instead are short-term traders who look for detecting a local trend

in the price fluctuation. This kind of agents tries to gain from detecting

a trend and so they

are responsible for the formation of market bubbles and crashes which

destabilize the market.

In the LM model the destabilizing effect made by chartists is implemented

dividing the chartists agents

into two subcategories: optimists which always buy and pessimists which

always sell.

In our model we can overcome this complication by simplifying the chartists’

behavior.

In fact, the description of chartists is in term of the recently

introduced potential method [17, 18, 19, 20].

Chartist agents detect a trend by looking at the distance between the

price and its smoothed profile

which in our case is the moving average

computed on the previous time steps.

Chartists try to follow the trend and bet that the price will moreover move

away from the actual price.

In this way they create a local bubble which destabilizes the market.

The stochastic equation for the price which describes the chartists behavior

can be written in terms of a RW

with a force whose center is the distance between the price and

the moving average:

| (1) | |||||

| (2) |

where is a parameter which gives the strength of the force, is the moving average performed on the previous steps of the price, is a white noise and is the amplitude of this noise. The factor in the denominator of the force term makes the potential independent of the particular choice of the moving average [17]. This equation has been used in previous papers to analyze real data [17, 19, 20]. The conclusion is that is indeed possible to observe this kind of forces also in real stock-prices. For our model we decided to adopt a simple linear expression for the force .

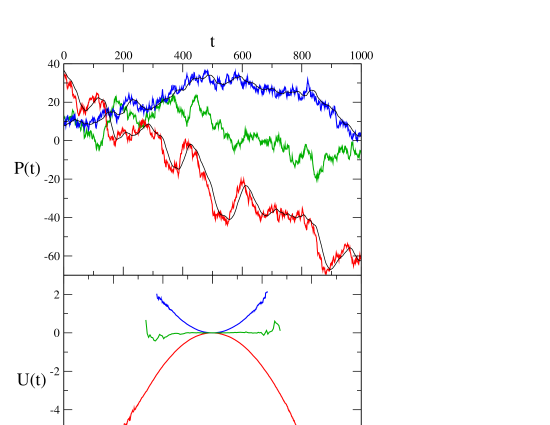

By integrating the force it is also possible to obtain the effective potential which describes the chartists’ behavior. For the case of a simple linear force the potential is quadratic. In Fig. 1 we show the stochastic process described in Eq. (2) with a linear force and the corresponding potential. A random walk is also plotted for comparison.

Depending on the sign of the parameter one can obtain both attractive and repulsive potential. Here we are considering only the repulsive potential which describes the trend-follower behavior of chartists, because the stabilizing attractive case is already carried out by the fundamentalist agents. In fact, fundamentalists try to stabilize the market driving the price towards the fundamental price which in our model is constant in time. The stochastic equation which describes the fundamentalists’ behavior can be written in terms of a random walk with a further term which is responsible for the stabilizing action of fundamentalists:

| (3) |

where is the strength of the fundamentalists’ action. For the moment the total number of agents, , is kept fixed and there are fundamentalists and chartists but agents can decide to change their mind during the simulation by switching their strategy from fundamentalist to chartist and viceversa. The probability to change strategy is based on two terms. The first is an herding term: agents tend to imitate other people behavior proportionally to the relative number of agents in the arrival class. The second is a term, characterized by the parameter , which leaves the agents the possibility to change strategy on the basis of considerations on the price behavior, independently on what the other agents are doing. The price signal which appears in the transition probabilities is proportional to for the probability to become fundamentalist and for that to become chartists. The mathematical expression for the transition probabilities is:

| (4) | |||||

| (5) |

For a realistic representation of the market the fundamentalists should dominate for very long times with intermittent appearance of bubbles or crashes due to the chartists. This is due to the fact that fundamentalists are usually big institutional traders which have on average a major weight in the market. In order to properly reproduce this effect we can introduce an asymmetry in the herding dynamics and, neglecting the price modulation, Eqs. (4) and (5) can be written in the following way:

| (6) | |||||

| (7) |

where the positive parameter define the asymmetry of the model. In the case the model reduces to the symmetric ants model by Kirman [21]. In Sec. 3 we will analyze in detail this asymmetric model and the corresponding equilibrium distribution for the population of chartists and fundamentalists. For the price formation we are going to use a simple linearized form of the Walras’ Law [22]:

| (8) |

where is the excess demand of the market at time .

This linear interpretation, valid

for small price increments, () is a technical

simplification from the more realistic multiplicative dynamics and it is

very useful for an analytical treatment.

The more general multiplicative

case will be discussed in detail in a forthcoming paper [15].

With respect to the dynamics of the ABM the multiplicative case will turn out

to be less stable in terms of parameters while the the linear case is

mathematically less problematic.

In our model the excess demand is simply proportional to

the price signal of

chartists and fundamentalists:

| (9) |

then adding a noise term we have the complete equation for the price formation:

| (10) |

In this case we have that the volume of the agents’ actions is proportional to the signal they perceive. This situation is much simpler than the corresponding price formation for the Lux-Marchesi model where prices can only vary of a fixed amount (tick) and the connection with the excess demand is implemented in a probabilistic way.

3 Herding Dynamics

3.1 Symmetric case

In his seminal paper Kirman [21]

proposed a simple dynamical model to explain a peculiar behavior observed

in ant colonies. Having two identical food sources, ants

prefer alternatively only one of these, and (almost)

periodically switch from one source to the other. In Kirman’s

model this effect is caused by an herding dynamics, in

which the evolution is stochastic and based on the meetings of the ants.

In particular an ant can recruit a companion, and bring it

to its preferred source, with a certain probability.

This model can be used to take into account the herding dynamics of

a population of agents (with fixed), and it is

formalized as follows.

Let us suppose the existence of two microscopic states: an agent

at time can be either a fundamentalist or

a chartist. Defining as the number

of chartists at time (and analogously as

the the number of fundamentalists), the quantity

| (11) |

varying between and describes the macroscopic state of the system.

A possibility to change opinion is given to each agent at any given time step

if she meets an agent with opposite views who succeeds in recruiting her.

Under the hypothesis that the transition probabilities are small

enough, in a single time step there will be no more than one change

of opinion. In this case we can write the transition rates as

| (12) |

where is the probability than one agent passes from the chartist group

to the fundamentalist one, and regulates the speed of the process.

Roughly, this is the approach adopted by Lux and Marchesi to rule the

transitions between agents in their model [14, 13], apart an exponential term depending on agents’ utilities that plays a minor

role in the dynamics. If we adopt the rates of Eq.(12) the dynamics

will admit two absorbing states ( and ). Lux and Marchesi

assign a lower limit of 4 for each class of agents, while

Alfarano et

al. [23], following Kirman [21], suggested a Poissonian term

(that is, independent from the number of agents) to avoid these fixed points. This new term can be

seen as a spontaneous tendency to change one’s mind, independently on the

others.

This corresponds essentially on the term we have discussed in relation

of Eqs. (4-7).

The simplest model is therefore given by the following transition probabilities.

We will adopt this last solution and write the transition probabilities as

| (13) |

Simulating this process one can observe two different behaviors depending on

the choice of the parameters, and in particular on . It can

be shown [21]

that if the system spends most of the time in the two

metastable states and , sometimes

switching from one

to the other. In the case , that is, if the self-conversion term is large enough, the systems fluctuates around .

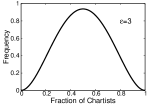

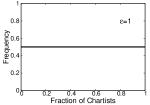

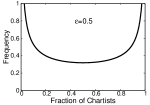

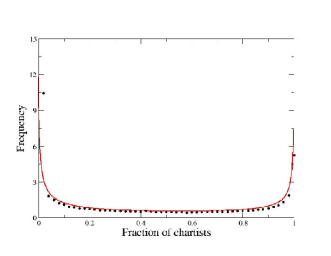

Kirman explicitly derived the functional form of the equilibrium function for ,

| (14) |

In Fig. 2 the three cases , and are shown.

In the first case the distribution has a single peek for . By decreasing the distribution gets

smoother and smoother, until it becomes uniform for . If one further decreases , the distribution develops two peeks and becomes bimodal.

3.2 Asymmetric case

It is possible to generalize the symmetric herding model described above to the

asymmetric case, in order to take account of the fact that institutional

traders, that have more impact on the market than individuals, usually adopt

long-term strategies [16] , as fundamentalists do. Here we propose a

further generalization of the model proposed of Alfarano et al. [24],

which is more convenient for our purposes.

Our asymmetric dynamics is given by:

| (15) |

where regulates the asymmetry between the two metastable states

(the model described in [24] can be recovered in the case ).

We are going to see that the asymmetry introduced by the term

is more realistic than the one due to and with respect to the

objective of having the market dominated (on average) by

fundamentalists at very large times.

It is possible to find the Fokker-Planck equation associated to the process given by Eq.(15). Following Alfarano et al. [24], we consider

the Master Equation in the case in which, on average, we have no more than a change of opinion in a single time step (this approximation is valid if ):

| (16) |

where is the probability to have chartists at time and is the rate of the transition in the brackets. In the continuous limit we can substitute the transition rates in Eq.(16), finding after some passages the Fokker-Planck equation

| (17) |

with drift and diffusion function given respectively by

and

Given these functions, the asymptotic stable distribution for the fraction of chartists is given by the textbook formula

| (18) |

where is a normalization constant (this expression can be obtained setting the temporal derivative of equal to zero and integrating twice the Fokker-Planck equation, see for example [25]).

The explicit expression of the equilibrium distribution can be derived

by appropriate analytical computer codes and it is rather complex.

Nevertheless a simple approximation will allow us to derive the distribution

which can be easily calculated and it illustrates clearly

the role played by the asymmetry parameter .

The idea is to disregard the terms of order in the drift and in the

diffusion functions. This approximation is valid for and, since we

will deal with at least agents, we can expect that it is rather

appropriate to our case.

Moreover, we are interested only in the case in order to

avoid the unimodality of the asymptotic distribution. This can be obtained setting , with .

The reasons for adopting a parametrization in which is inversely

proportional to are:

(i) qualitatively one may expect that the probability to neglect the

herding behavior decreases when increases.

(ii) in the following we will consider the properties of thee model as a

function of and we believe it is realistic that the system always

stays in the bimodal case. This requires that should not

exceed the value one even for large values of .

With this choice and using the approximation described above, the drift and the diffusion functions become respectively

| (19) |

and

| (20) |

Now we can easily solve the integral in Eq.(18) and derive

| (21) |

The form of Eq. (21) clearly shows that, by increasing , the

values of near to 1 are exponentially suppressed. In other words, if

is small the equilibrium distribution will be bimodal, because

and (compare the Eqs. (21)

and (14)), while by increasing the asymmetry, regulated by

the parameter , becomes more and more important.

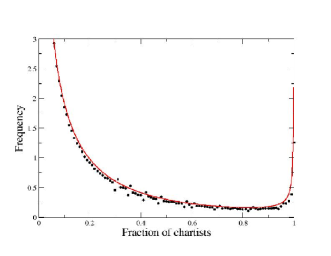

We have also simulated the process described by the

Eq. (15) and we have compared the distributions obtained by integrating the Eq. (18) with the complete

drift and diffusion functions. As it is clear from Fig. 3,

the agreement between theory and simulation is very good.

3.3 Finite size effects

Alfarano et al. [23] computed the time that on average must be waited to see the switch from one metastable state to the other in the symmetric case:

The presence of this characteristic temporal scale implies that this simple

model would give exponential correlation functions for volatility clustering.

However different time scales in agents’ strategies can lead to a

superposition of different characteristic times

and therefore to long-range relaxation.

Examining the functional form of one can see that for

the mean first passage time diverges, because of the

emergence of the two absorbing states. Moreover, keeping constant

and increasing the time spent in one of the metastable states gets longer.

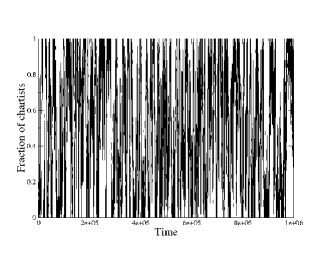

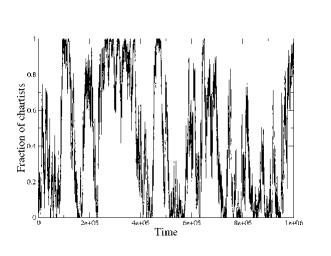

We have simulated the process given by Eq.(12) using different

values of keeping fixed and equal to 0.5. For the velocity

parameter we choose the value 0.02.

As expected, the system oscillates between the two metastable states.

As shown in Fig. 4, the only difference is the frequency of the

passages from one state to the other.

For small values of () the rate to change strategy is very

high and this leads to an unrealistic situation in which fluctuations

are too fast. On the other hand, for large values of

the system get essentially locked in one of the two states and the

fluctuations become frozen.

Only for an intermediate values of ()

the system shows an intermittent behavior which resembles

experimental observations and will lead to the SF.

This finite size effect was first noted in LABEL:LMfinite

in relation to the LM model.

In conclusion, this simple model explains why, in the limit

, models like the Lux-Marchesi one loose their

property to generate the SF.

This result is based on very general properties

and it is easy to expect that it will be a general one

for the entire class of model we are considering.

This implies that in this kind of models, given a fixed

temporal scale, the system

will be able to generate the “right”

amount of fluctuations only within

a specific range of finite values of .

This is a very important observation from both

a conceptual and a practical point of view.

In fact in this class of models the quasi-critical state

linked to the SF, corresponds to a finite size effect

(with respect to and to ) in the sense of Statistical Physics.

Therefore we are not in presence of a real critical behavior

characterized by universal power law exponents.

The fact that in some cases one can fit the experimental data with power laws

can be easily understood by considering that different agents might operate at

different time scales.

This would lead to a superpositions of finite size effects corresponding

to different

time scale switch may appear as a sort of effective power law exponent.

The possibility that a suitable coupling between different time scale exist

leading to genuine critical behavior is of course open.

However, this is not the case for the class

of model we are considering.

In this perspective the variability of the effective exponents

and their breakdown observed in various data [2]

can be a genuine effect not simply due to limitation

or problems with a database.

This of course change the perspective of the data analysis

and of their comparison with the models.

We expect that the behavior of different markets is reasonably

similar because the key elements are essentially the same

but without a strict universality.

In the asymmetric case one must consider two different temporal scales,

say and , the first referring to the formation of the chartists’

bubble and the second relative to its duration. We have investigated with

numerical simulations their dependence on and , finding, as

expected, a divergence of in the limit .

Therefore the introduction of an asymmetry in the

agents dynamics does not change the finite size effect

associated to the quasi-critical behavior and the SF.

4 Stylized Facts from the Model

In this section we discuss the results of some simulations of the minimal

model described

in Sec. 2. In particular we will see that this model is

able to reproduce the main SF of financial markets listed in

the introduction.

In order to clarify all the elements of the model we are going to discuss increasingly complex cases.

(a) Single agent

Considering that in the simplest model all agents are statistically

identical (no real heterogeneity) we can fix our parameters in

such a way that even a single stochastic agent can lead

to an interesting dynamics.

This single agent can be chartist or fundamentalist and

the herding term is not active in this case.

For simplicity we have also neglected the exponential term

related to the price behavior in the transition probabilities.

When the agent switches her behavior from chartist to fundamentalist,

the market dynamics

is in turn given by Eq. (2) or (3).

If the agent is chartists she follows the market trend and creates

bubbles, in this case the

price fluctuations are larger with respect to a simple random walk.

Otherwise if she is fundamentalist the price is driven towards the

fundamental price and the

fluctuations are smaller than the random walk ones.

In this case the price is not diffusive

and it remains almost constant, oscillating around the fundamental price .

In Fig. 5 we show the results of the simulation for

the one-agent model.

We can observe that the price dynamics displays local bubbles corresponding

to periods in which the agent is a chartist.

The price is instead almost constant when the

agent is fundamentalist. Also we can observe periods of high or low

volatility depending

on the strategy of the agent.

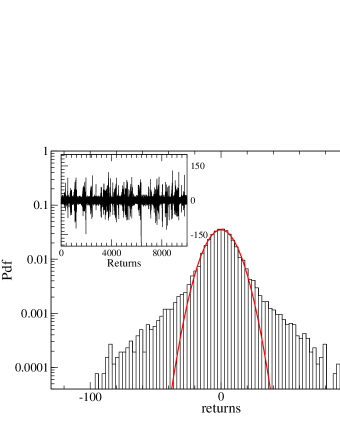

This dynamics clearly leads to fat tails in the distribution

of price increments and also to a certain volatility

clustering that certainly in this case is not due

to the herding dynamics.

This simple example shows that, once we have a full control

of the model parameters, we can trace and reproduce some

SF even with an extremely minimal model.

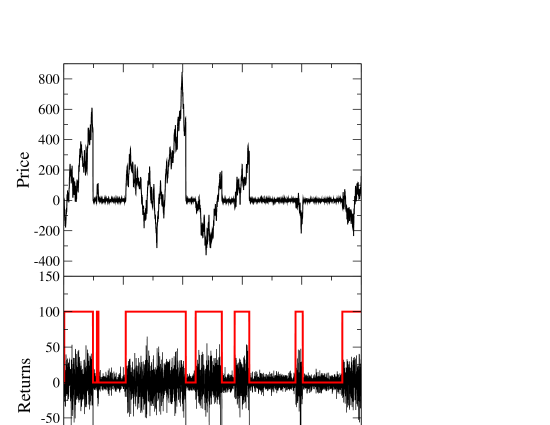

(b) Many statistically equivalent agents

We now consider the more realistic dynamics with a larger

number of agents.

In principle we can tune the parameters to

obtain the SF for any preassigned value of .

For example

in Fig. 6 (upper)

we show the dynamics of the case still without

the exponential price term. Also in this case periods of

high or low volatility

correspond to regions in which chartist or fundamentalist agents dominate.

We have analyzed the SF for this model and both fat tails and volatility

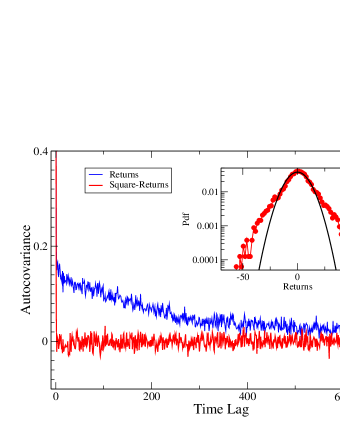

clustering are shown in Fig. 6 (lower).

The square price-fluctuations shows a positive autocorrelation

which (unlike real data)

decays exponentially. As we have discussed this depends

on the fact that this model has a single characteristic time scale.

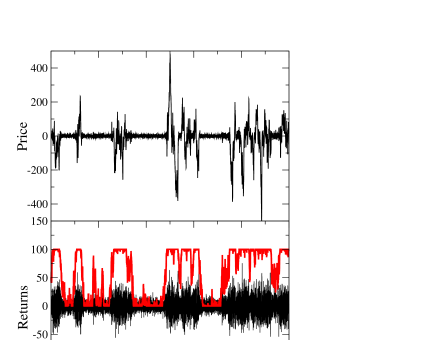

(c) Many heterogeneous agents

The limitation of a single time scale can be easily removed by

introducing a real

heterogeneity in the time scales of the agents’ strategies.

In particular we have introduced a distribution of values for the

parameter which is the

number of steps agents consider for the estimation of the moving

average of the price.

We adopt a distribution of values also for the parameter

which gives the strength of the action of

chartists.

In this case we also introduce the exponential price term in the rate

equations in order to have the most complete version of our model.

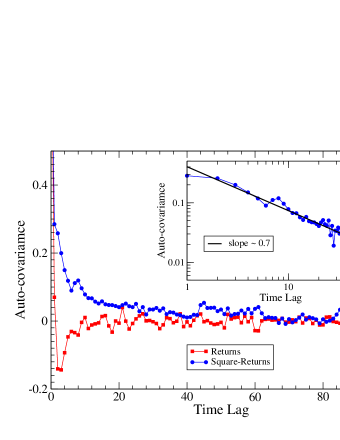

In Fig. 7 we report the SF

corresponding to a uniform distribution between and time

steps

and a uniform distribution between and .

The comparison of these results with those

of the simplified model discussed before permits to

draw the following conclusions:

- The exponential term related to the price behavior

in the transition probabilities enhances the bubbles and crashes

corresponding to the chartists action and it amplifies

the fat tail phenomenon as shown by comparing Fig. 7 (lower)

to Fig. 6 (lower) .This is a qualitative argument because

the two models are actually different and a precise comparison

keeping the same effective parameters is not possible.

- The real heterogeneity of the agents time scales produces in

this case a distribution of transition rates which leads to

a quasi-power law behavior for the volatility correlations as

shown in the inset of Fig. 7 (upper).

On the other hand this different time scales have the effect of

decorrelating the agents dynamics and the overall amplitude of the volatility

is reduced.

-The short time anti-correlation for the returns (Fig. 7 upper), can be related

to the long time predominance of fundamentalist and will be discussed in detail

in paper II [15].

5 Microscopic origin of the Stylized Facts

As pointed out pointed out before, the intermittent behavior that characterizes the

oscillations of

agents’ strategies is crucial to generate the Stylized Facts.

One must choose a certain temporal

window and a correct value of to obtain the “right” amount of

fluctuations (the other parameters being fixed). In fact, while a low value

of produces too many fluctuations, a high value of will prevent the formation

of the chartists bubble at all. Therefore the Stylized Facts in our model can be regarded

as finite size effects, that is, they disappear in the thermodynamic limit.

Given the general nature of these results we may conjecture that it should apply

toa broad class of agents model and it is not a special property

of our specific model.

This has important consequences for both data analysis and for the

structure of the models

proposed to investigate the origin of Stylized Facts. The fact that the exponents of the

power laws characterizing financial markets don’t seem to be universal

[2]

can be

easily explained in this framework.

The apparent power laws observed in many data find a natural explanation

in the presence of a distribution of agents’ strategies in terms

of their time horizons and strength. Concerning universality, even if this

is not strictly present in this model, it is reasonable to expect a certain

similarity in all markets. This is due to the fact that the key elements

to generate the SF are of very general nature as we are going to explain in

the following discussion.

The simplicity of the model permits to interpret the origin of Stylized Facts

directly from the agents’ strategies in the market. To this purpose it will

be useful to define the concept of effective action. In our model

agents not only decide between selling and buying, they operate in the market proportionally

to the signal or , selling or buying quantities

which are proportional to this signal.

Besides this, while in Statistical Mechanics

the study of the dynamics of a model is usually done with a fixed value of

(and eventually infinite), nothing in financial markets permits us to justify this

assumption. An agent can either enter or exit from the market on the basis of various

considerations, and in addition she can varies the volume of the exchanges in the market.

In summary, we must consider the effective action present in the market as the sum of these

two effects, the fact that an agent can operate with different volumes and the fact that

agents can enter or exit from the market.

Let us now suppose that for some reason at time there is a price fluctuation

(in any direction) . Following our line of reasoning, this will produce

an increase of the effective action, because both fundamentalists and chartists will

see a signal in the market, and this action will produce more price fluctuations, and so on.

So action leads to more action. On the contrary, if the market doesn’t show

opportunities to be profitable, agents will be discouraged from operating and so

periods of low fluctuations will be followed by periods of low fluctuations.

This mechanism resembles the GARCH process, in which the volatility at time

depends on the volatility at time and also on the return at time [26]:

| (22) |

We recall that the GARCH process was originally proposed as a phenomenological scheme to

reproduce the phenomena of volatility clustering and fat tails.

In our case we propose a microscopic interpretation of something

similar to the GARCH process which, however, is now related to the

specific agents dynamics.

On the other hand our model doesn’t show any appreciable linear correlation between

price increments, even if the arbitrage condition is not explicitly implemented

in the model.

This can be understood in the following way. Consider a price increment (with sign)

at time . The next price increment will depend not only from the

previous fluctuation, as it is for volatility, but also on all the other variables

of the system,

like the number of chartists, the specific values of and and so on.

Schematically we can write:

| (23) |

All these additional variables are in general not correlated in a direct

way with the price fluctuations, so they lead to a decorrelation

of the price increments, as is, instead, in the case of volatility.

This line of reasoning explains qualitatively the presence of volatility clustering and

the absence of linear correlations in financial markets. We believe that these

considerations are of general nature and therefore they should be valid for all

markets and models.

Within our class of models, however, this general behavior does not reach the

status of universal behavior in the sense of Statistical Physics.

6 Self Organized Intermittency

In the previous section we have seen that our model is able to

generate the SF of financial markets and it is possible to control their

origin and nature in great detail.

However, in our model, as in most of the models in the literature,

these SF occur only in a very specific and limited region of

the models’ parameters.

This is a problem which is seldom discussed in the literature

but in our opinion poses a vary basic question: why the market dynamics

evolves spontaneously, or self-organizes, in the specific region of parameters which

corresponds to the SF? In this section we are going to discuss in detail a possible

answer to this fundamental question.

In usual Critical Phenomena of Statistical Physics

there is a basic difference between the

parameters of the model (usually called coupling constants) and

the number of elements considered.

Models with different coupling constants, but belonging to the same universality class,

evolve towards the same critical properties in the asymptotic limit of very large

and very large time.

This situation is called universality and it is often present

in equilibrium critical phenomena in which the critical region requires

an external fine tuning of various parameters.

This is a typical situation of competition between order and disorder

which occurs at the critical point.

Self-organization instead occurs in a vast class of models

characterized by a non linear dissipative dynamics far from equilibrium.

Popular examples of these self organized models

are

the fractal growth models like

of Diffusion Limited Aggregation (DLA), the Dielectric Breakdown Model (DBM)

and the Sandpile Model [27, 28, 29, 30].

In these models the nonlinear dynamics

drives spontaneously system towards a critical state.

This can occur from a variety of initial configurations and parameters

and define a state that is always the same , the critical one.

For these reasons this phenomenon has been named Self-Organized Criticality (SOC) [31].

It is important to note that this self-organization is also an asymptotic

phenomenon, in the sense that it occurs in the limit of large N and large time.

For financial markets the possible analogy with SOC

phenomena

is very tempting. However we are going to see that there are basic fundamental differences

with the above concepts which require the developments of a different theoretical framework.

In this section we are going to introduce the first step along this line.

A very important observation is the fact that the SF appear only for a specific value of

the number of agents . This result may appear as problematic in view of the above

discussion about self-organization.

A finite value of cannot lead to universality

and so the presence of the SF in virtually all markets

(with very different number of agents)

appears rather mysterious.

In this

perspective a situation in which the SF are generated only in the limit

of large would have appear more natural.

Also our model shows clearly that

the intermittent behavior corresponding to the SF must necessary occur for a finite value

of . It is easy to realise that this conclusion has a general nature with respect to the

four essential ingredients of our class of models. An additional problem, in trying to

explain the self-organization of the SF,

comes from the fact, that in addition to N, the model contains several other parameters.

So, even if one would be able to produce the SF in the large limit, the self organization

with respect to the other parameters would remain unclear.

From our studies we are going to propose a conceptually different

mechanism of the

self-organization phenomenon. Consider a certain market with its characteristic

parameters. This values will govern the rate equation of the agents dynamics as

described by Eqs. 4and 5

and in Fig. 4.

For any set of these parameters there will be a characteristic value of

which separates the regions with large fluctuations with the ones with small fluctuations,

as shown for example in Fig. 4

The SF appears precisely around this finite value of , which corresponds to the right amount

of intermittency.

So our basic question about the SO is now transformed in a question related to the number of

agents. Why the system should have precisely this number of agents acting on the market?

This question can now be answered in the following way.

We have seen that if is very large the system gets locked in the fundamentalist state

and this leads to a very stable dynamics of the price.

Such a situation will produce very small signals for the agent strategies.

If we assume that

an agent operates in an certain market only if her signal is larger than a minimum threshold,

it is easy to realise that in the stable price situation, corresponding to large ,

the number of active agents will decrease.

On the other hand in the case of very few agents, the price dynamics shows very

high fluctuations [12]

and this produces large signals for the agents and will attract

more agents in the market.

Mathematically this concept can be implemented by

introducing a trashold to the price fluctuations which

corresponds to the decision of agents to be

active or not active in the particular market.

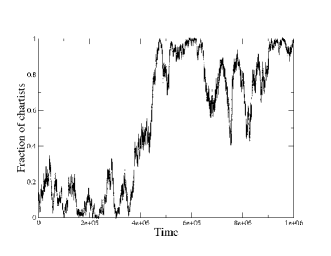

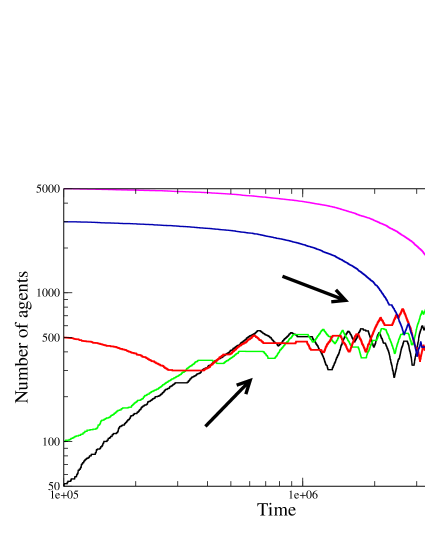

We have introduced this threshold in our model and a typical result

is shown in Fig. 8

We can see that the variable number of agents evolves spontaneously

towards the characteristic value of corresponding to the

intermittent state and the SF.

Since this state is not precisely critical in the sense of Statistical Physics

we propose to call this phenomenon Self 0organized intermittency (SOI).

This new vision has important implications in various directions. On one hand it seems

to be a reasonably natural and robust explanation of the self-organization towards the

quasi-critical state, on the other hand the quasi-critical state leading to the SF

is unavoidably linked to finite size effect. A first consequence is that in the limit

of large , or

in the limit of large time, the SF disappear. A fact which seems to be indeed reproduced

by price time series [2].

Another consequence is that genuine critical exponents and universality can not be expected

in this framework. The fact that several datasets can be fitted by power laws is however

not surprising. Since different agents may have different time horizons in

their trading strategies, one has a superposition of finite size effects which

may appear as a power law in some range. This perspective implies that the discrepancy

in the effective exponents for different dataset and for different time scales [2]

may be a genuine intrinsic property instead of spurious effect due to the incompleteness of

the data.

A key element of the present scheme is the nonstationarity of the system with respect

to the value of which represent a major departure from usual critical

phenomena. On the other hand this non stationarity appears to be a very important

element in real financial markets.

7 Conclusions

Our starting point has been a detailed analysis of the LM model first

in terms of the role played by the total number of players and also

on the study of the stability of the SF with respect to the variation

of the other parameters. A particular puzzling point was the fact that

the SF are present only for a finite value of in the LM

model) and not in the asymptotic limit .

Starting from this consideration our aim has been to introduce a

minimal ABM based on F and C which would permit to clarify these

points and eventually also to discuss the self-organization. A basic technical

simplification is the description of the chartists in terms of the

newly introduced effective potential model. This and other similar

simplifications permit us to analyze in detail the mathematical

properties of the model. In order to achieve the deepest

understanding also analytically of the dynamics we have focused for

the moment on the linear returns. In paper II [15]

we are going to consider also the extension to logarithmic returns

but in the limit of small fluctuations the two approach essentially

coincide.

The main results of our model are:

- Detailed understanding of the origin of the SF with respect to the

microscopic

dynamics of the agents.

- Demonstration that in this class of model the SF correspond to

finite size effects and not to universal critical exponents. This

finite size effect, however, can be active at

different time scales.

- Bubbles of chartists can be triggered spontaneously by a

multiplicative cascade which can originate from tiny random

fluctuations. This situation resembles in part the avalanches of the

Sandpile Model in Statistical Physics [31].

- We have shown the importance of the non stationarity in the dynamics

of the number of active agents and we introduced a characteristic

threshold to decide when

an agent can enter or exit from the market.

- This threshold and the relative non stationarity are proposed to

represent the key element in the self-organization mechanism. This self

organization, however, leads to an intermittency related to finite

size effects. For this reasons we define it as

Self-Organized-Intermittency (SOI).

Starting from the minimal model introduced in this paper and

considering that one can obtain a detailed microscopic understanding

of its dynamics, it is easy to identify a number of realistic variances

which can be introduced as generalizations of the model. In future

works we will consider this variantes. However, the present model was

aimed at a different target. The idea was to define the minimal set

of elements which could lead to the SF and to the SO phenomenon.

Acknowledgments

We are grateful to Simone Alfarano, Guido Caldarelli, Alessio Del Re, Doyne Farmer, Fabrizio Lillo, Thomas Lux, Rosario Mantegna, Miguel Virasoro, and Constantino Tsallis for interesting discussions.

References

- [1] L. Bachelier. Théorie de la spéculation. Annales Scientifiques de l’Ecole Normale Supérieure, III-17:21–86, 1900. [Ph.D. thesis is mathematics].

- [2] R. Cont. Empirical properties of assets returns: stylized facts and statistical issues. Quantitative Finance, 1:223–236, 2001.

- [3] R. N. Mantegna and H.E. Stanley. An Introduction to Econophysics: Correlation and Complexity in Finance. Cambridge University Press, New York, NY, USA, 2000.

- [4] J. P. Bouchaud and M. Potters. Theory of Financial Risk and Derivative Pricing: From Statistical Physics to Risk Management. Cambridge University Press, 2003.

- [5] B.B. Mandelbrot. The variation of certain speculative prices. Journal of Business, 36:394–419, 1963.

- [6] B.B. Mandelbrot. Fractals and Scaling in Finance. Springer Verlag, New York, 1997.

- [7] R.F Engle. Autoregressive conditional heteroskedasticity with estimates of the variance of u.k. inflation. Econometrica, 50:987–1008, 1982.

- [8] C. Tsallis, C. Anteneodo, L. Borland, and R. Osorio. Nonextensive statistical mechanics and economics. Physica A, 324:89, 2003.

- [9] L. Borland. Option pricing formulas based on a non-gaussian stock price model. Phys. Rev. Lett., 89(9):098701, Aug 2002.

- [10] F. Baldovin and A. Stella. Scaling and efficiency determine the irreversible evolution of a market. PNAS, 104:19741–19747, 2007.

- [11] B. LeBaron. Time scales, agents, and empirical finance. In Medium Econometrische Toepassingen (MET). Erasmus University, 2006.

- [12] V. Alfi, L. Pietronero, and A. Zaccaria. Minimal agent based model for the origin and self-organization of stylized facts in financial markets. submitted, 2008, 0807.1888.

- [13] T. Lux and M. Marchesi. Scaling and criticality in a stochastic multi-agent model of a financial market. Nature, 397:498–500, 1999.

- [14] T. Lux and M. Marchesi. Volatility clustering in financial markets: A micro-simulation of interacting agents. International Journal of Theoretical and Applied Finance, 3:675–702, 2000.

- [15] V. Alfi, M. Cristelli, L. Pietronero, and A. Zaccaria. Minimal agent based model for financial markets II: statistical properties of the linear and multiplicative dynamics. to be submitted, 2008.

- [16] G. Vaglica, F. Lillo, E. Moro, and N. Mantegna. Scaling laws of strategic behavior and size heterogeneity in agent dynamics. Phys. Rev. E, 77:036110, 2008.

- [17] M. Takayasu, T. Mizuno, and H. Takayasu. Potential force observed in market dynamics. Physica A, 370:91–97, October 2006.

- [18] T. Mizuno, H. Takayasu, and M. Takayasu. Analysis of price diffusion in financial markets using PUCK model. Physica A, 382:187–192, August 2007, arXiv:physics/0608115.

- [19] V. Alfi, F. Coccetti, M. Marotta, L. Pietronero, and M. Takayasu. Hidden forces and fluctuations from moving averages: A test study. Physica A, 370:30–37, 2006.

- [20] V. Alfi, A. De Martino, A. Tedeschi, and L. Pietronero. Detecting the traders’ strategies in minority-majority games and real stock-prices. Physica A, 382:1, 2007.

- [21] A. Kirman. Ants, rationality and recruitment. Quarterly Journal of Economics, 180:137–156, 1993.

- [22] M. Kreps. A Course in Microeconomic Theory. Princeton University Press, 1990.

- [23] S.Alfarano, T.Lux, and F.Wagner. Time-variation of higher moments in a financial market with heterogeneous agents: an analytical approach. Journal of Economic Dynamics & Control, 32:101–136, 2008.

- [24] S. Alfarano, T. Lux, and F. Wagner. Estimation of agent-based models: the case of an asymmetric herding model. Comput. Econ., 26(1):19–49, 2005.

- [25] C.W. Gardiner. Handbook of stochastic methods: for physics, chemistry and the natural sciences. Springer, Berlin, 1990.

- [26] T. Bollerslev. Generalized autoregressive conditional heteroskedasticity. J. Econometrics, 31:307–327, 1986.

- [27] T. A. Witten and L. M. Sander. Diffusion-limited aggregation, a kinetic critical phenomenon. Phys. Rev. Lett., 47(19):1400–1403, Nov 1981.

- [28] L. Niemeyer, L. Pietronero, and H. J. Wiesmann. Fractal dimension of dielectric breakdown. Phys. Rev. Lett., 52(12):1033–1036, Mar 1984.

- [29] Per Bak, Chao Tang, and Kurt Wiesenfeld. Self-organized criticality: An explanation of the 1/f noise. Phys. Rev. Lett., 59(4):381–384, Jul 1987.

- [30] H.J. Jensen. Self-organized criticality. Cambridge University Press, Cambridge, 1998.

- [31] P. Bak. How Nature Works: The Science of Self-Organised Criticality. Copernicus Press, New York, 1996.