On Honest Times in Financial Modeling

Ashkan Nikeghbali111Institut für Mathematik,

Universität Zürich, Winterthurerstrasse 190,

CH-8057 Zürich,

Switzerland and

Eckhard Platen222University of Technology Sydney,

School of Finance Economics and Department of

Mathematical Sciences, PO Box 123, Broadway, NSW,

2007, Australia

Abstract. This paper demonstrates the usefulness and importance of the concept of honest times to financial modeling. It studies a financial market with asset prices that follow jump-diffusions with negative jumps. The central building block of the market model is its growth optimal portfolio (GOP), which maximizes the growth rate of strictly positive portfolios. Primary security account prices, when expressed in units of the GOP, turn out to be nonnegative local martingales. In the proposed framework an equivalent risk neutral probability measure need not exist. Derivative prices are obtained as conditional expectations of corresponding future payoffs, with the GOP as numeraire and the real world probability as pricing measure. The time when the global maximum of a portfolio with no positive jumps, when expressed in units of the GOP, is reached, is shown to be a generic representation of an honest time. We provide a general formula for the law of such honest times and compute the conditional distributions of the global maximum of a portfolio in this framework. Moreover, we provide a stochastic integral representation for uniformly integrable martingales whose terminal values are functions of the global maximum of a portfolio. These formulae are model independent and universal. We also specialize our results to some examples where we hedge a payoff that arrives at an honest time.

1991 Mathematics Subject Classification: primary

90A12;

secondary 60G30, 62P20, 05C38, 15A15.

JEL Classification: G10, G13

Key words and phrases: jump diffusion market, honest

times, growth optimal portfolio, benchmark approach, real world

pricing, nonnegative local martingales.

1 Introduction

In this paper we consider a general class of jump-diffusion financial market models under the benchmark approach, described in ?). Our main goal is, within this framework, to provide modelers and investors with extra tools based on the concept of honest times, which are random times that are not stopping times and that are somehow hidden. We show that quantities of interest, such as the law of the time when the global maximum value of a portfolio is reached, or the conditional laws of the global maximum value of a portfolio, can be computed explicitly. Most importantly, these results will be very robust since they do not depend on the specifications of the underlying model. Surprisingly, these results reveal the universal feature that no Markovian setting needs to be assumed. This can be achieved thanks to the use of martingale techniques.

More precisely, we let security prices follow jump diffusions. There exists a range of literature on modeling and pricing for jump diffusions, starting with ?). For a detailed discussion of this area the reader is referred to ?). Different to most authors we will avoid the standard assumption on the existence of an equivalent risk neutral probability measure. In this way important freedom is gained for financial modeling. All tasks of portfolio optimization, derivative pricing, hedging and risk management can still be consistently performed, see ?). The growth optimal portfolio, which maximizes the growth rate of all strictly positive portfolios is the central building block of the market model. It is also the numeraire portfolio in the sense of ?) and ?). When used as numeraire or benchmark, it makes all benchmarked portfolios local martingales and, thus, all nonnegative benchmarked portfolios supermartingales. This supermartingale property excludes automatically a strong form of arbitrage. Furthermore, in a complete market, nonnegative replicating portfolios, when expressed in units of the growth optimal portfolio are minimal when they form martingales. Therefore, benchmarked derivative prices will be obtained as martingales.

An honest time is by definition the end of an optional set, see for example ?), ?) for references and details. For instance, the last time when the maximum of some benchmarked nonnegative portfolio with no positive jumps is reached is an example of an honest time. It is a random time but not a stopping time, which makes its analysis more delicate. Honest times have been intensively studied in stochastic analysis, see e.g. ?), where they play an important role in the theory of enlargements of filtrations, see ?), ?), ?), ?) and ?), in the characterizations of strong Brownian filtrations, ?), ?), and in path decompositions of diffusions, see ?), ?), ?), and ?). Honest times have also recently received some attention in mathematical finance, e.g. for modeling default in ?), for insider trading in ?) and for pricing options in the Black-Scholes framework in [Madan, Roynette & Yor (2008a] (?, ?, ?). In this paper, we shall pursue these last trends in mathematical finance and show that honest times can serve as rather useful and important random quantities in financial modeling.

In some special cases, such as the time of the last zero before time one of a standard Brownian motion or some Bessel process or the laws of last passage times of transient diffusions, the law of an honest time can be explicitly characterized, see ?), ?), ?), ?) and [Nikeghbali (2006b] (?, ?) for examples. We will rely in this paper on a characterization of honest times given in ?) and take this to be our basic reference without further mentioning. The important fact that nonnegative benchmarked portfolios form local martingales in jump diffusion markets will play a crucial role. In this context honest times related to the last maxima of benchmarked securities will be studied. These particular random times are extremely interesting from an investor’s point of view. They can describe, for instance, the time for the highest value ever of the security relative to the benchmark. The law of this time is valuable information for an investor. We will provide a general formula for the law of an honest time (Theorem 4.2). We then specialize it to the last time when a benchmarked nonnegative portfolio reaches its maximum. We shall also provide the conditional distributions of the global maximum of a benchmarked nonnegative portfolio. Moreover, we give a stochastic integral representation for any martingale whose terminal value is a function of the global maximum of a benchmarked nonnegative portfolio. This suggests certain hedging strategies for reaching this payoff which arises at some honest time.

The structure of the paper is as follows. In Section 2 we describe the underlying general jump diffusion market. In Section 3 important facts on honest times are given and a general formula for their laws is derived. Section 4 provides some examples concerning the actual computation of such laws. For notations and definitions that are used but not explained in the paper we refer to ?) or ?).

2 Jump Diffusion Market

We consider a market where continuously evolving risk is modeled by independent standard Wiener processes , , , , defined on a filtered probability space . We also consider events of certain types, for instance, corporate defaults, operational failures or catastrophic events that are reflected in traded securities. Events of the th type shall be counted by the adapted th counting process , whose intensity is a given predictable, strictly positive process with

| (2.1) |

almost surely for and . Furthermore, we introduce the th normalized jump martingale with stochastic differential

| (2.2) |

for and , which represents the k-th source of event driven risk. We not only compensate but also normalize the above sources of event risk to make these comparable with the previously introduced standard Wiener processes which provide the sources of continuous risk. It is assumed that the above jump martingales do not jump at the same time.

The evolution of traded risk is then modeled by the vector process of independent martingales , where , …, are the above Wiener processes, while , …, represent compensated and normalized counting processes. The filtration is assumed to be the augmentation under of the natural filtration , generated by the vector process . This filtration satisfies the usual conditions and is the trivial -algebra. Note that the conditional variance of the th source of traded risk equals

| (2.3) |

for all , and .

For the securitization of the sources of traded risk, we introduce risky primary security accounts, whose values at time are denoted by , for . Each of these accounts contains shares of one kind with all dividends reinvested. Furthermore, the 0th primary security account , is the locally riskless savings account that continuously accrues the short term interest rate . We assume that the nonnegative th primary security account value at time satisfies the stochastic differential equation (SDE)

| (2.4) |

with initial value , . Since models the savings account, we have and for and . We assume that the processes , , and are finite and predictable, and such that a unique strong solution for the system of SDEs (2.4) exists. To guarantee strict positivity for each primary security account we assume

| (2.5) |

for all , and . Furthermore, we make the following assumption.

Assumption 2.1

The generalized volatility matrix is invertible for every , and allows only downward jumps.

The invertibility of the generalized volatility matrix provides the unique link between the sources of traded risk and the primary security accounts. Negative jumps in equities are the most important ones to model. These are caused, for instance, by defaults and catastrophic events. Therefore, we can focus in our analysis of honest times on models where there are no positive jumps in primary security accounts. This assumption fits well into the concept of honest times, see ?). Assumption 2.1 allows us to introduce the market price of risk vector

| (2.6) |

for . Here is the appreciation rate vector and the unit vector. Using (2.6), we can rewrite the SDE (2.4) in the form

| (2.7) |

for and . For , the quantity expresses the market price of risk with respect to the th Wiener process , and for , it can be interpreted as the market price of th event risk.

The vector process characterizes the evolution of all primary security accounts. We say that a predictable stochastic process , is a strategy if it is -integrable. The th component of denotes the number of units of the th primary security account held at time in a portfolio, . For a strategy we denote by the value of the corresponding portfolio process at time , when measured in units of the domestic currency. Thus, we set

| (2.8) |

for . A strategy and the corresponding portfolio process , are called self-financing if

| (2.9) |

for all . In what follows we will only consider self-financing portfolios.

For a given strategy , generating a strictly positive portfolio process , let denote the fraction of wealth that is invested in the th primary security account at time , that is,

| (2.10) |

for and . By (2.8) these fractions always add to one. In terms of the vector of fractions we obtain for from (2.9), (2.7) and (2.10) the SDE

| (2.11) |

for . The following assumption ensures that no strictly positive portfolio explodes in our market.

Assumption 2.2

We assume that

| (2.12) |

for all and .

Following ?), this allows us to introduce for the given jump diffusion market the growth optimal portfolio (GOP) , which maximizes expected logarithmic utility and, thus, the growth rate of strictly positive portfolios. It satisfies the SDE

| (2.13) | |||||

for , with . This portfolio is also the numeraire portfolio in the sense of ?) and ?), and is in several mathematical manifestations the best performing portfolio. We use as benchmark, and accordingly, call prices, when expressed in units of , benchmarked prices. By the Itô formula, (2.11) and (2.13), a benchmarked portfolio process , with

| (2.14) |

for , satisfies the SDE

| (2.15) | |||||

for . In this equation we wrote instead of , for , and used the notation

| (2.16) |

for , . The SDE (2.15) shows that the dynamics of any benchmarked portfolio is driftless. Thus, a nonnegative benchmarked portfolio forms a local martingale. This also means that a benchmarked nonnegative portfolio is always a supermartingale. It is a well-known fact that whenever a nonnegative supermartingale reaches the value zero, it almost surely remains zero afterwards. Based on this fundamental property of supermartingales, no company and no investor, with nonnegative total tradable wealth, can generate wealth out of zero initial capital. This means that a rather strong type of arbitrage, see ?), is automatically excluded in our market. Note however, free lunches with vanishing risk in the sense of ?), or free snacks and cheap thrills as described in ?), may arise. This emphasizes that our financial market model is rather general. In particular, as shown in [Platen (2002] (?, ?), for the class of models under consideration one does, in general, not have an equivalent risk neutral probability measure. Therefore, the widely used risk neutral pricing methodology may break down. This happens, for instance, when the benchmarked savings account process forms a strict supermartingale and not a martingale in a complete market setting. For example, for realistic models where such phenomenon arises we refer to ?), ?), ?), ?), ?), ?) and ?).

Since risk neutral pricing is not available, we need a general consistent alternative for the pricing of contingent claims. We have already seen that benchmarked nonnegative portfolios are supermartingales. It is clear that among those supermartingales that replicate a given future benchmarked payoff, the corresponding martingale provides the least expensive hedge. To value claims consistently in a complete market, we generalize the concept of real world pricing, as introduced in ?) and ?). It makes benchmarked derivative prices to martingales by employing the GOP as numeraire and forms in the resulting pricing formula conditional expectations under the real world probability measure.

More precisely, let be an optional process, and let us define the payoff , which matures at the random time , as the nonnegative random variable with integrable benchmarked value, that is,

| (2.17) |

When is a stopping time, then the payoff is called a contingent claim. We define for its real world price at time by the real world pricing formula

| (2.18) |

for . This is a generalization of the real world pricing concept described in ?).

Note that by using real world pricing for general derivatives, the benchmarked unhedgeable part of a square integrable benchmarked contingent claim has minimal variance since its benchmarked current value is the least-squares projection of its future benchmarked value. On the other hand, replicable claims can be hedged with minimal costs. In the case when there exists a minimal equivalent martingale measure in the sense of ?) or ?), the corresponding risk neutral price is equivalent to the above real world price in (2.18).

3 Honest Times

3.1 A simple characterization

As previously shown, benchmarked nonnegative portfolios turn out to be local martingales and, thus, supermartingales. If these are modeled as transient jump diffusions, then there is always a last time when these benchmarked securities reach their maximum. Such a time is extremely interesting for an investor, since at this time the portfolio reaches its largest value relative to the benchmark. It would be beneficial if an investor could time the selling of a security accordingly. Unfortunately, the time when such a maximum is reached is not a stopping time. However, already the knowledge of the law of such time can provide the investor with precious information.

Such random times are commonly called honest times, see Definition 3.1 below. This class of random times is the most studied one after stopping times. There are several characterizations of honest times. One of these characterizations is given in terms of nonnegative local martingales without positive jumps, which vanish at infinity, and the last time they reach their maximum. This corresponds well to the framework of our financial market.

We first introduce an abstract class of random times that allows us to study a range of interesting problems related to the above type of times.

Definition 3.1

Let be the end of an -optional set , that is,

Then we call an honest time.

An example for an honest time is the above mentioned time when a benchmarked nonnegative portfolio without positive jumps reaches its last maximum. Further examples will be given below. ?) associated with an honest time the supermartingale

and studied its properties. Note that this supermartingale plays a key role in the enlargement of filtrations, as shown in ?), ?) or ?). We now provide a simple characterization of honest times and the associated supermartingales, following the ideas of ?).

Definition 3.2

We say that an -local

martingale belongs to the class , if it

is strictly positive, with no positive jumps and

, where .

Note that the benchmarked primary security account processes , , and all benchmarked portfolios are local martingales. Consequently, all strictly positive benchmarked portfolios with no negative jumps that vanish at infinity belong to this class. With the class we cover benchmarked primary security accounts of realistic models. Negative jumps of equities against the market as a whole are the most important events we need to capture in financial modeling. These are typically triggered by defaults or catastrophes. Portfolios with no short sale constraint based on benchmarked primary security accounts from the class are also from . For notational convenience we introduce for from the class both future and past suprema processes:

and

The following variant of Doob’s maximal inequality, see ?), also called Doob’s maximal identity, has far reaching consequences.

Lemma 3.3 (?))

(Doob’s maximal identity)

For any we have:

| (3.1) |

Hence, is uniformly distributed on . Furthermore, for any stopping time :

| (3.2) |

Here is a uniformly distributed random variable on , independent of .

Proof: Since this result is rather fundamental for our analysis we indicate here its proof. Formula (3.2) is a consequence of equation (3.1), when applied to the martingale and the filtration . Formula (3.1) itself is obvious when , and for , it is obtained by applying Doob’s optional stopping theorem to the local martingale , where .

Remark 3.4

The second part of Lemma 3.3 with (3.2), is a remarkable property that allows us to separate the distribution of from the past, given the present. Without imposing any Markovianity on the market dynamics one has the same probabilistic characterization of the future supremum of a benchmarked process, which only involves the simple uniform distribution. From a finance point of view one can say that even the most complex, possibly non Markovian, jump diffusion dynamics provide at any stopping time the same conditional probability distribution for the maximum of a benchmarked security from as is obtained, for instance, under the Black-Scholes model.

Remark 3.5

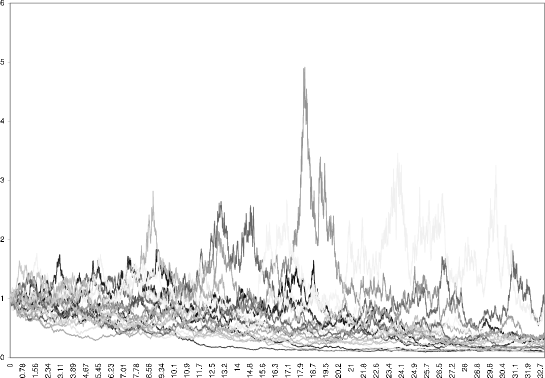

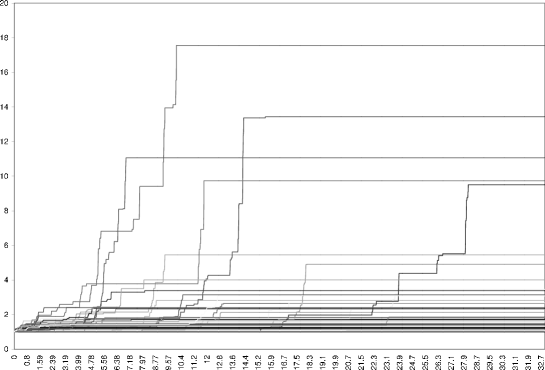

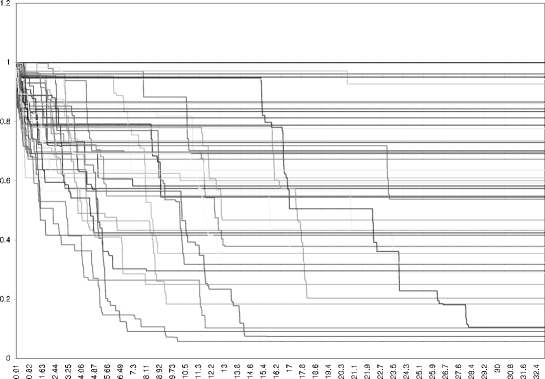

Under the minimal market model (MMM) (see ?)), benchmarked primary security accounts are the inverse of time transformed squared Bessel processes of dimension four, and thus from the class . For illustrations we show in Figure 3.1, using realistic parameters, twenty trajectories of these strict local martingales. One notes here substantial movements upwards but overall a systematic decline, consistent with the strict local martingale property. In Figure 3.2, we display the running maximum for fifty paths . Note that there seems to be no average value identifiable if we would add more paths and would extend the time horizon. We then show in Figure 3.3 the inverse of the running maxima. They seem to fit well a uniform distribution on , as is suggested by Lemma 3.3.

The following proposition is rather interesting:

Proposition 3.6 (?))

Let be a local martingale, which belongs to the class , with and . When we consider the honest time

| (3.3) |

we have the formula

for all .

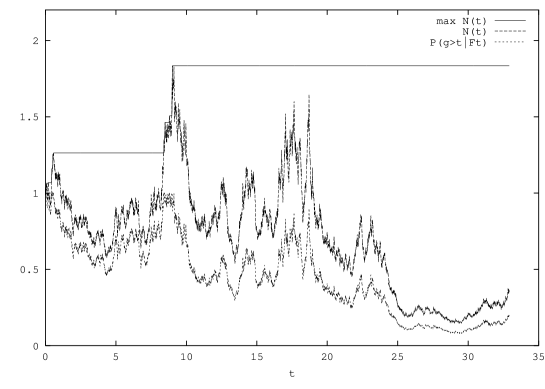

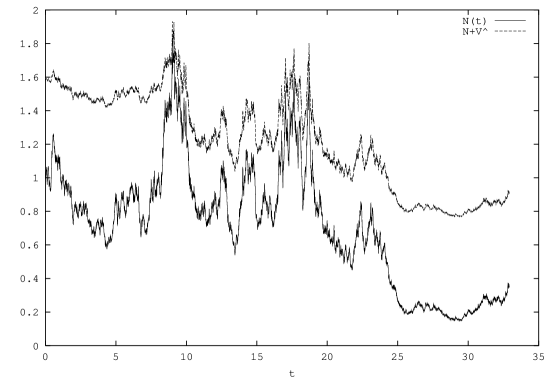

This means that the ratio of the benchmarked security over its maximum until time , provides us with the conditional probability that the time of the total maximum is still ahead. When the benchmarked value of a security substantially declines over time, compared to its maximum until time , then the conditional probability of the time of the total maximum being still ahead is becoming rather small equating the ratio . This important insight holds without any further modeling assumption. In Figure 3.4, we illustrate this by displaying trajectories of , and .

A direct application of the above result together with the Itô formula yields the representation

| (3.4) |

From the uniqueness of the Doob-Meyer decomposition it results that represents the increasing part of whilst expresses its martingale part. Since is of the class , is a uniformly integrable martingale, even in BMO. To keep the presentation as simple as possible, we make the assumption for the following two results, that all -local martingales are continuous.

Corollary 3.7

Assume that all -local martingales are continuous. Let be defined in (3.3), then the quantity is the dual predictable projection of the indicator , and for any positive predictable process one has

| (3.5) |

Furthermore, the random time defined in (3.3) is an honest time and avoids any -stopping time , that is, .

This result is very useful for the quantitative analysis of functionals that involve honest times. The following theorem establishes a converse result to Proposition 3.5.

Theorem 3.8 (?))

Assume that all -local martingales are continuous, and let be an honest time which avoids any -stopping time, then there exists a continuous, nonnegative local martingale with and , such that

| (3.6) |

for all .

This theorem states the remarkable fact that every honest time in a continuous market is, in fact, the last time when a certain nonnegative local martingale reaches its maximum. If the continuous market is complete, it is the last time that a nonnegative benchmarked portfolio reaches its maximum. Furthermore, it follows by (3.6) that the conditional expectation for the logarithm of the maximum of a benchmarked nonnegative portfolio is of the form

| (3.7) |

for . Note that the logarithm of is finite and is a martingale. This provides an investor with the possibility to identify explicitly the conditional expectation of the logarithm of the total maximum over the maximum until time . It is important to realize that the conditional expectation in (3.7) is model independent, and is therefore very robust. More generally, as is explained in the next subsection, one can even obtain the conditional distributions of . This allows to evaluate general payoffs depending on .

3.2 Conditional distributions of and stochastic

integral representations

In this subsection, we need not assume continuity of the local martingales.

The following relation can be rather useful in pricing derivative payoffs since it applies to all benchmarked primary security accounts and nonnegative portfolios from . It gives access to the conditional expectation of functions of , quantities all investors would like to know. Most importantly, the results are again model independent. For sake of completeness and to illustrate how a fundamental result such as Doob’s maximal identity leads easily to nontrivial statements, we reproduce a proof of the following result:

Proposition 3.9 (?))

For any Borel bounded or positive function , and from , we have:

Proof: The proof is based on Doob’s maximal identity; in the following, is a random variable, which follows the standard uniform law and which is independent of .

A straightforward change of variable in the last integral also gives:

and this completes the proof.

Now, from a financial point of view, it would be very useful to obtain a representation of (3.9) as a stochastic integral. This would be very valuable for hedging purposes. Remarkably, this can also be achieved without assuming continuity of nor any predictable representation property for the underlying filtration. Again, this result is universal since model independent. The next proposition extends the classical Azéma-Yor martingales:

Proposition 3.10 (?))

Let be from , be a locally bounded Borel function and define . Then, is a local martingale and we have the representation:

| (3.9) |

It is now easy to see that is of the form (3.9). Indeed:

Hence,

with

and

| (3.10) |

Moreover, again from formula (3.9), we obtain the following representation of as a stochastic integral:

Proposition 3.11

We obtained in (3.11) a martingale representation for . This can be exploited for hedging a payoff that involves the total maximum of a benchmarked nonnegative portfolio from . It turns out that a call payoff would have infinite expected value. However, a put payoff with benchmarked strike has according to the real world pricing formula (2.18) and (3.9) at time the benchmarked value

that is

| (3.12) |

or equivalently

Obviously, for , the value of the put is zero, since it gives the right but not the obligation to receive the strike when paying . By (3.10) we can determine the number of units

| (3.13) | |||||

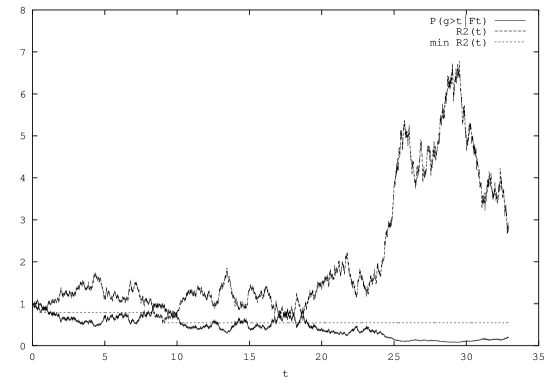

that one has to hold in at the time to hedge the payoff. The remainder of the wealth in the hedge portfolio should be invested in the GOP . Note that when , the hedge portfolio collapses to zero and remains there. The above put option can be used to protect against downward moves of . For instance, one can add the put to the security obtaining as the benchmarked value of the resulting portfolio. For the price of , one purchases then at time protection of some kind against downward moves of . Figure 3.5 displays a corresponding scenario where we show , as it already appeared in Figure 3.4, and when was set equal to . In this scenario the strike was not reached by during the period displayed. One notes that the value stays always above , which it should by construction. However, we also see that does practically not fall much below a level of about , which is close to the final value of . This illustrates the kind of protection that is giving against downward moves of . For periods when comes closer to , goes up. However, when falls quite drastically, demonstrates its put feature. Overall it appears that benefits from extreme upward moves of . In the long term, the systematic downward movement of will be in asymptotically limited to .

This simple example indicates that there exist many ways of creating new financial products or managing risk using the above results on honest times. What is most striking for the above pricing and hedging results, involving payoffs based on , is the fact that these are model independent and therefore very robust. This is a property that makes the methodology very attractive for areas where modeling risk over a long period of time has been of much concern, as it is in pension fund management and insurance. Furthermore, it is not that one wants to actually receive the payoff , it is more that one is aiming for it. In this manner the use of honest times creates a new perspective for risk management.

4 Law of an Honest Time

After having invested over some time period in a security, it is a successful strategy to sell such security when its benchmarked value comes close to its total maximum . The problem with such buy low sell high strategy is that the investor cannot decide at a given time if the total maximum has occurred or not because this arises at an honest time which is not a stopping time. For an investor it is therefore of interest to know at least the law of the hidden time of the total maximum of a benchmarked security. This allows her or him to judge whether it is realistic to hope, over a given time frame, to reach the total maximum. We will give below a formula that will be useful for the explicit computation of the law of an honest time.

Proposition 4.1

Under the assumptions of Theorem 3.8 the law of the honest time is given as

| (4.1) |

Proof: We have by (3.4) and (3.6)

Taking expectation on both sides and exploiting the fact that

is a uniformly integrable

martingale yields (4.1).

Although formula (4.1) seems to be rather simple it still requires the knowledge of the mean of . Obviously, the law of an honest time is no longer model independent. Numerical methods, in particular Monte Carlo methods, as described for instance in ?), can be very useful in such computations. However, it is of great advantage in the study of an honest time if one can derive an explicit analytic formula for its law. Below we provide a theorem that can be useful when aiming to compute explicitly the law of an honest time.

Theorem 4.2

Under the assumptions of Theorem 3.8 define for . Then for any bounded or positive Borel function , we have

| (4.2) |

In particular, the Laplace transform of the law of is obtained as

| (4.3) |

for .

Proof: From Corollary 3.7, or equally by differentiating formula (4.1), it follows for any Borel bounded function

This result allows us to derive some explicit examples for the law of an honest time when the underlying nonnegative local martingale belongs to some class of well-known diffusions. We begin with the standard asset price model in finance, the Black-Scholes model. We set

| (4.4) |

which follows a geometric Brownian motion for . Here denotes a standard Wiener process under the real world probability measure and we assume . The honest time considered here, that is the time of the total maximum of , is then given as

Proposition 4.3

The law of is characterized by its Laplace transform

| (4.5) |

for .

Proof: We can use (4.3) to compute the law of . For this we will use the Laplace transform of , which is obtained in ?) and also given in ?) as

| (4.6) |

for and . Substituting formula (4.6) into (4.3) yields

Remark 4.4

: It is interesting to note that by (4.5) the honest time has the same law as the first hitting time of a level twice the value of an independent exponential random variable by a Brownian motion with drift, that is,

| (4.7) |

with , where follows a standard Brownian motion. Indeed, formula (4.5), or its translation (4.7), can be seen as a particular case of the path decomposition of a transient diffusion, here , as presented in ?), p.112, Proposition (6,29). More precisely, from this proposition (or from Doob’s maximal identity), it follows that

From the same proposition, we also learn that conditionally on , the process is distributed as , since is the Doob -transform of with .

The Black-Scholes model is still a simple model. Therefore, the following result is of interest to give access to a much richer class of models. By the Dubins-Schwarz theorem, see ?), we have the following characterization of local martingales of the class , which reduces the problem of finding the law of an honest time for a general model to that of a geometric Brownian motion after some time change.

Proposition 4.5

Under the assumptions of Theorem 3.8 let be an honest time. Then there exists a unique local martingale with a.s. and , where is an -Brownian motion, such that

Proof: From ?) it follows that there exists a local martingale such that and . Moreover, the local martingale is unique and . From the Dubins-Schwarz theorem there exists then an -Brownian motion in -time such that . If we denote by , the generalized inverse of defined by

then we can define the honest time

Consequently, is also given by

Squared Bessel processes play an essential role in various financial models. This includes, for instance, the constant elasticity of variance model, see ?); the affine models, see ?); and the minimal market model, see [Platen (2002] (?, ?). To study honest times in some of these models let denote a squared Bessel process of dimension . In this case is transient, see ?). Furthermore, for any squared Bessel process with index the process with

| (4.8) |

is a nonnegative, strict local martingale and from the class with . By application of Proposition 3.6 one obtains for the honest time with the conditional probability

| (4.9) |

for all . For illustration, we show in Figure 4.1, in the case of dimension , some simulated paths of , and the evolution of the conditional probability (4.9).

Moreover, by Doob’s maximal identity (3.1) the random limit is uniformly distributed on for the case of dimension . This is an interesting observation for the rather realistic minimal market model, where such dynamics arise. Figure 3.3 displays the running values of for such scenarios.

Proposition 4.6

The Laplace transform of the honest time given in (4.9) is for of the form

| (4.10) |

where and is the modified Bessel function of the second kind, see ?).

Proof: We first recall the Laplace transform of the random variable , , from ?) and ?) in the form

| (4.11) |

In the special case of dimension , as it arises for the stylized minimal market model in [Platen (2002] (?, ?), we have and it follows that

Another interesting special case is obtained for the squared Bessel process of dimension , where we are able to provide the following explicit formula for the density.

Corollary 4.7

Proof: For the squared Bessel process of dimension we have and from (4.11)

The linearity of the Laplace transform and a close look at a table

of inverse Laplace transforms, see for instance

?), then yields (4.12).

Note that the above density (4.12) of the honest time is dependent on the initial level of the squared Bessel process. Such dependence was not observed in the case of geometric Brownian motion.

Consider for the moment , the inverse of a benchmarked savings account, which is the discounted GOP. Then the honest time in (4.9) describes the ideal time to invest in the GOP funds that were held in the savings account, waiting for investment in the best performing portfolio, the GOP. The formulae (4.11) and (4.12) describe the laws of this time for Bessel models. This information could be used by the investor for the optimal timing of investment decisions.

To have an even richer class of models for benchmarked securities than those just discussed, we consider the general case of a transient diffusion . It generates a local martingale in the class via the ratio , , . Here is the differentiable scale function of , see ?), which we can choose such that and . Then we have by Proposition 3.6 again

where and is defined as . The law of the honest time can then be characterized as follows.

Proposition 4.8

The Laplace transform of the above honest time is for of the form

| (4.13) |

Here is a continuous solution of the equation

| (4.14) |

with denoting the infinitesimal generator of the diffusion .

The function is characterized as the unique (up to a multiplicative constant) solution of (4.14) by demanding that is decreasing and satisfies some appropriate boundary conditions. The reader is referred to ?) for further details on the function and its relation to hitting times.

Proof of Proposition 4.8: Let us consider the hitting time

for and . The Laplace transform of follows by ?) and ?) in the form

| (4.15) |

It suffices to substitute in (4.15) and then apply the resulting expression in (4.3).

Let us conclude this paper with the following remarks.

In this paper, we have not provided any specific rule on how to use the knowledge of the law of an honest time for trading strategies. One way would be to look for the closest stopping time to , with respect to some suitable distance. Such problems have already been solved by ?) in the case of the Brownian motion with drift. In a forthcoming work, we will address this problem both analytically and numerically, for various models.

For sake of clarity, we have not included any discussion about situations where the nonnegative local martingale does not converge anymore to , but rather to some random variable . Such results would be of interest in the case when the trading period is , for representing some fixed deterministic time or some stopping time. In such situations, the computations are more involved and are the topic of current research. It is also obvious that the above presented results are useful in the study of insider trading, see ?) and ?) or ?). Forthcoming work will address this issue by using honest times.

References

- Amendinger, Imkeller & Schweizer (1998 Amendinger, J., P. Imkeller, & M. Schweizer (1998). Additional logarithmic utility of an insider. Stochastic Process. Appl. 75(2), 263–286.

- Azéma (1972 Azéma, J. (1972). Une remarque sur les temps de retour. Trois applications. In Séminaire de Probabilités VI, Volume 258 of Lecture Notes in Math., pp. 35–50. Springer, Berlin.

- Barlow (1978 Barlow, M. T. (1978). Study of a filtration expanded to include an honest time. Z. Wahrsch. Verw. Gebiete 44, 307–324.

- Barlow, Emery, Knight, Song & Yor (1998 Barlow, M. T., M. Emery, F. B. Knight, S. Song, & M. Yor (1998). Autour d’un théoréme de tsirelson sur des filtrations browniennes. In Sém. Probability, XXXII, Volume 1686 of Lecture Notes in Math., pp. 264–305.

- Barlow, Pitman & Yor (1989 Barlow, M. T., J. W. Pitman, & M. Yor (1989). Une extension multidimensionnelle de la loi de l’arc sinus. In Sém. Probability, XXIII, Volume 1372 of Lecture Notes in Math., pp. 294–314.

- Becherer (2001 Becherer, D. (2001). The numeraire portfolio for unbounded semimartingales. Finance Stoch. 5, 327–341.

- Borodin & Salminen (2002 Borodin, A. N. & P. Salminen (2002). Handbook of Brownian Motion - Facts and Formulae (2nd ed.). Birkhäuser.

- Chung (1973 Chung, K. L. (1973). Probabilistic approach in potential theory. Ann. Inst. Fourier 23(3), 313–322.

- Cont & Tankov (2004 Cont, R. & P. Tankov (2004). Financial Modelling with Jump Processes. Financial Mathematics Series. Chapman & Hall/CRC.

- Cox (1975 Cox, J. C. (1975). Notes on option pricing I: constant elasticity of variance diffusions. Stanford University, (working paper, unpublished).

- Delbaen & Schachermayer (2006 Delbaen, F. & W. Schachermayer (2006). The Mathematics of Arbitrage. Springer Finance. Springer.

- Dellacherie, Maisooneuve & Meyer (1992 Dellacherie, C., B. Maisooneuve, & P. Meyer (1992). Probabilités et potentiel. In Chapitres XVII-XXIV: Processus de Markov (fin). Compléments de calcul stochastique. Herman.

- du Toit & Peskir (2007 du Toit, J. & G. Peskir (2007). Predicting the time of the ultimate maximum for brownian motion with drift. preprint, University of Manchester.

- Duffie & Kan (1994 Duffie, D. & R. Kan (1994). Multi-factor term structure models. Philos. Trans. Roy. Soc. London Ser. A 347, 577–580.

- Elliott, Jeanblanc & Yor (2000 Elliott, R. J., M. Jeanblanc, & M. Yor (2000). On models of default risk. Math. Finance 10, 179–196.

- Fernholz & Karatzas (2005 Fernholz, E. R. & I. Karatzas (2005). Relative arbitrage in volatility-stabilized markets. Annals of Finance 1(2), 149–177.

- Föllmer & Schweizer (1991 Föllmer, H. & M. Schweizer (1991). Hedging of contingent claims under incomplete information. In M. H. A. Davis and R. J. Elliott (Eds.), Applied Stochastic Analysis, Volume 5 of Stochastics Monogr., pp. 389–414. Gordon and Breach, London/New York.

- Grorud & Pontier (1998 Grorud, A. & M. Pontier (1998). Insider trading in a continuous time market model. Int. J. Theor. Appl. Finance 1, 331–347.

- Hofmann, Platen & Schweizer (1992 Hofmann, N., E. Platen, & M. Schweizer (1992). Option pricing under incompleteness and stochastic volatility. Math. Finance 2(3), 153–187.

- Imkeller (2002 Imkeller, P. (2002). Random times at which insiders can have free lunches. Stochastics Stochastics Rep. 74, 465–487.

- Jeulin (1980 Jeulin, T. (1980). Semi-martingales et grossissements d’une filtration, Volume 833 of Lecture Notes in Math. Springer.

- Jeulin & Yor (1985 Jeulin, T. & M. Yor (1985). Grossissements de filtrations: exemples et applications, Volume 1118 of Lecture Notes in Math. Springer.

- Kent (1978 Kent, J. T. (1978). Some probabilistic properties of bessel functions. Ann. Probab. 6, 760–770.

- Kloeden & Platen (1999 Kloeden, P. E. & E. Platen (1999). Numerical Solution of Stochastic Differential Equations, Volume 23 of Appl. Math. Springer. Third printing.

- Lévy (1939 Lévy, P. (1939). A multistep approximation scheme for the Langevin equation. C.R.A.S 208, 318–321. Errata p. 776.

- Lewis (2000 Lewis, A. L. (2000). Option Valuation Under Stochastic Volatility. Finance Press, Newport Beach.

- Loewenstein & Willard (2000 Loewenstein, M. & G. A. Willard (2000). Local martingales, arbitrage, and viability: Free snacks and cheap thrills. Econometric Theory 16(1), 135–161.

- Long (1990 Long, J. B. (1990). The numeraire portfolio. J. Financial Economics 26, 29–69.

- Madan, Roynette & Yor (2008a Madan, D., B. Roynette, & M. Yor (2008a). From Black-Scholes formula to local times and last passage times for certain submartingales. preprint Universit’e Pierre et Marie Curie.

- Madan, Roynette & Yor (2008b Madan, D., B. Roynette, & M. Yor (2008b). Option prices as probabilities. Finance Research Letters 26, 79–87.

- Madan, Roynette & Yor (2008c Madan, D., B. Roynette, & M. Yor (2008c). Unifying Black-Scholes type formulae which involve last passage times up to a finite horizon. Asia-Pacific Financial Markets.

- Mansuy & Yor (2006 Mansuy, R. & M. Yor (2006). Random Times and (Enlargement of Filtrations) in a Brownian Setting, Volume 1873 of Lecture Notes in Math. Springer.

- Merton (1976 Merton, R. C. (1976). Option pricing when underlying stock returns are discontinuous. J. Financial Economics 2, 125–144.

- Millar (1977 Millar P.W. (1977). Random times and decomposition theorems. Proc. Symp. Pure Math. 31, 91–103.

- Millar (1978 Millar P.W. (1978). A path decomposition for Markov processes. Annals of probability 6, 345–348.

- Miller & Platen (2005 Miller, S. & E. Platen (2005). A two-factor model for low interest rate regimes. Asia-Pacific Financial Markets 11(1), 107–133.

- Nikeghbali (2006a Nikeghbali, A. (2006a). Enlargements of filtrations and path decompositions at non stopping times. Probab. Theory Related Fields 136(4), 524–540.

- Nikeghbali (2006b Nikeghbali, A. (2006b). An essay on the general theory of stochastic processes. Probability Surveys 3, 345–412.

- Nikeghbali (2006c Nikeghbali, A. (2006c). Some random times and martingales associated with BES processes . Alea 2, 67–89.

- Nikeghbali & Yor (2006 Nikeghbali, A. & M. Yor (2006). Doob’s maximal identity, multiplicative decompositions and enlargements of filtrations. Illinois J. of Mathematics 50(4), 791–814.

- Pitman & Yor (1981 Pitman, J. & M. Yor (1981). Bessel processes and infinitely divisible laws. In D. Williams (Ed.), Stochastic integrals, Volume 851 of Lecture Notes in Math. Springer.

- Pitman & Yor (1999 Pitman, J. & M. Yor (1999). Laplace transforms related to excursions of a one-dimensional diffusion. Bernoulli 5(2), 249–255.

- Platen (2001 Platen, E. (2001). A minimal financial market model. In Trends in Mathematics, pp. 293–301. Birkhäuser.

- Platen (2002 Platen, E. (2002). Arbitrage in continuous complete markets. Adv. in Appl. Probab. 34(3), 540–558.

- Platen (2004 Platen, E. (2004). A class of complete benchmark models with intensity based jumps. J. Appl. Probab. 41, 19–34.

- Platen & Heath (2006 Platen, E. & D. Heath (2006). A Benchmark Approach to Quantitative Finance. Springer Finance. Springer.

- Protter (2004 Protter, P. (2004). Stochastic Integration and Differential Equations (2nd ed.). Springer.

- Revuz & Yor (1999 Revuz, D. & M. Yor (1999). Continuous Martingales and Brownian Motion (3rd ed.). Springer.

- Salminen (1985 P. Salminen (1985). On local times of a diffusion. In Sém. Probability, XIX, Volume 1123 of Lecture Notes in Math., pp. 63–79.

- Salminen (1997 P. Salminen (1997). On last exit decompositions of linear diffusions. Studia. Scient. Math. Hungarica 33, 251–262.

- Sin (1998 Sin, C. A. (1998). Complications with stochastic volatility models. Adv. in Appl. Probab. 30, 256–268.

- Williams (1974 Williams, D. (1974). Path decomposition and continuity of local time for one-dimensional diffusions i. J. London Math. Soc. 3(28), 3–28.

- Yor (1978 Yor, M. (1978). Grossissements d’une filtration et semi-martingales: théorèmes généraux. In Sém. Probability, XII, Volume 649 of Lecture Notes in Math., pp. 61–69.

- Yor (1997 Yor, M. (1997). Some Aspects of Brownian Motion, Part II. Some Recent Martingale Problems. Birkhäuser, Basel.