Fitting Martingales To Given Marginals

Abstract

We consider the problem of finding a real valued martingale fitting specified marginal distributions. For this to be possible, the marginals must be increasing in the convex order and have constant mean. We show that, under the extra condition that they are weakly continuous, the marginals can always be fitted in a unique way by a martingale which lies in a particular class of strong Markov processes.

It is also shown that the map that this gives from the sets of marginal distributions to the martingale measures is continuous. Furthermore, we prove that it is the unique continuous method of fitting martingale measures to the marginal distributions.

1 Introduction

We consider the problem of finding real valued martingales fitting given marginal distributions and show that, by restricting to a certain class of strong Markov processes, it can be done in a unique way. It is furthermore shown that this is the unique continuous method of matching any specified marginals by martingales.

The existence of martingales with specified marginals has been previously studied by many authors. In particular, Strassen (Strassen, ) showed in 1965 that if is a sequence of probability measures on the real numbers which have constant mean and are increasing in the convex order, then there is a martingale such that the law of is . The property that is increasing in the convex order simply means that is increasing in for every increasing convex function , and the necessity of this condition follows easily from Jensen’s inequality. This result was extended by Kellerer (Kellerer, ) in 1972 to the case where the marginal distributions and the martingale are indexed by time in . It was also shown that can always be chosen to be Markov.

More recently, this problem has been investigated in the context of pricing financial derivatives, where knowledge of the prices of vanilla call and put options provides an implied distribution for the underlying asset price at future times. For example, assuming zero interest rates (for simplicity) the local volatility model constructs the asset price process as a solution to the stochastic differential equation

| (1.1) |

where is a Brownian motion, is the asset price and is the local volatility. Then, as is well known (see (Derman, ) and (Dupire2, )), if is the price of a vanilla call with strike price and maturity , the implied probability density of is and the local volatilities can be recovered from the following forward equation

Alternative methods of matching the implied marginal distributions have been considered, such as jump-diffusions in (Andersen, ), stochastic volatility in (ImpliedPrice, ) and models based on Lévy processes in (LevyModels, ). Also, (Yor, ) gives several constructions, including Skorokhod embedding and time-changed Brownian motion methods.

In this paper, we provide a general way of matching marginal distributions under very mild constraints. Other than the necessary conditions of having constant mean and being increasing in the convex order, the only further constraint placed on the marginals is that they be weakly continuous. That is, if then for every continuous and bounded function . It is shown that such marginals can be fitted in a unique way by a certain class of strong Markov martingales. As this class includes all martingale diffusions, the solution will coincide with the local volatility model when it applies. However, for marginals which are either not smooth or don’t have strictly positive densities, different types of solutions are obtained which cannot be described by an S.D.E. such as (1.1). For example, jump processes and singular diffusions, as described in Section 2.

We also show that that the resulting map from the sets of marginals to the martingales is continuous. So, a small change to marginal distributions results in only a small change to the martingale measure matching these marginals.

Furthermore, it is shown in Theorem 1.5 that not only is our method of fitting the marginals continuous, but it is the only possible continuous method. Consequently, any alternative approach (e.g., those described by (Andersen, ), (ImpliedPrice, ) and (LevyModels, )) must either fail to fit, or very closely approximate, certain marginal distributions, or small changes in the marginals would lead to big changes in the resulting martingale measure.

Let us now define the types of processes to be considered, which should include all continuous and strong Markov processes. However, there are some marginal distributions which cannot be matched by any continuous process. For example, if for all times and decreases in , then there must be a positive probability that jumps from below to above . For this reason, we relax the continuity condition to obtain the following class of processes.

Definition 1.1.

Let be a real valued stochastic process. Then,

-

1.

is strong Markov if for every bounded, measurable and every there exists a measurable such that

for every finite stopping time .

-

2.

is almost-continuous if it is càdlàg, continuous in probability and given any two independent càdlàg processes each with the same distribution as and for every we have

-

3.

is an almost-continuous diffusion if it is strong Markov and almost-continuous.

In (Lowther2, ) it was shown that almost-continuous diffusions arise when taking limits of continuous diffusions in the sense of finite-dimensional distributions. Note that condition 2 is equivalent to saying that cannot change sign without passing through zero, which is clearly true for continuous processes by the intermediate value theorem. In what follows, we often abbreviate ‘almost-continuous diffusion’ to ACD.

An alternative way of representing the marginal distributions which we make use of is through the function . The property that is increasing in the convex order is then equivalent to being an increasing function of . Furthermore, the distribution functions are easily recovered from . This leads to the following space of functions.

Definition 1.2.

Let be the set of functions such that

-

1.

is convex in and continuous and increasing in .

-

2.

as , for every .

-

3.

There exists a real number such that as for every .

Continuity of in is just requiring the marginals to be weakly continuous in , and the third condition is equivalent to them having a constant mean. The property that a process has marginals consistent with some can be expressed as

| (1.2) |

and, conversely, if is a martingale which is continuous in probability then given by (1.2) will be in the space . The notation used here is borrowed from the financial interpretation where are call prices, with maturity and strike , although we just make use of as convenient representations of martingale marginals both in the statements of the main results below and in the proofs later.

We use the space of càdlàg real valued processes (Skorokhod space) with coordinate process on which to represent martingale measures.

Then, is a measurable space and is a càdlàg process adapted to the filtration . The existence and uniqueness of the martingale measure fitting given marginals is now stated,

Theorem 1.3.

For any there exists a unique measure on under which is an ACD martingale and (1.2) is satisfied.

See sections 3 and 4 for the proof of this result, which involves a weak compactness argument to construct the measure and applies a result from (Lowther2, ) concerning limits of almost-continuous diffusions. Then, a backward equation developed in (Lowther4, ) is applied to show uniqueness.

Given any , the notation will be used for the unique ACD martingale measure matching the marginal distributions given by . This defines a map , which we shall show is continuous under the appropriate topologies.

Let be the set of probability measures on . A sequence in converges to in the sense of finite-dimensional distributions if and only if for every random variable of the form

| (1.3) |

for and continuous bounded .

We use the topology of pointwise convergence on , so if and only if for all . Note that this is slightly stronger than weak convergence of the marginal distributions, which would be equivalent to convergence of to . The continuity result for the map from the marginals to the martingale measures is as follows.

Theorem 1.4.

For every denote the unique ACD martingale measure given by Theorem 1.3 by . Then, the function

is continuous, under pointwise convergence on and convergence in the sense of finite-dimensional distributions on .

So, given any sequence converging pointwise to then for every random variable of the form (1.3). The proof of this is left until Section 4.

Not only is the ACD martingale measure fitting the marginal distributions uniquely defined, but it is also the only way of fitting the marginals in a continuous way, as the following result states. Here, we again use the topology of pointwise convergence on and convergence in the sense of finite-dimensional distributions on .

Theorem 1.5.

Suppose that we have a continuous map from a dense subset of to the martingale measures

such that for every the equality is satisfied. Then .

In particular this shows that the choice of the class of almost-continuous diffusions used to fit the marginals is not arbitrary, but was in fact forced upon us. The proof of Theorem 1.5 is left until Section 5, where the idea is that there are certain marginal distributions for which there is only one possible martingale measure. These correspond to extremal elements of , and form a dense subset.

We finally note that the fact that is continuous and monotonic in both and for every implies that pointwise convergence is the same as locally uniform convergence, and the topology is given by the metric

| (1.4) |

So, we are justified in only considering limits of sequences (rather than generalized sequences) in the explanations and proofs of theorems 1.4 and 1.5.

2 Examples

In this section we mention some examples to demonstrate the kinds of processes which can result from different properties of the marginal distributions.

2.1 Continuous diffusions

If is strictly convex in for every , then the support of under the measure given by Theorem 1.3 will be all of and, consequently, will be a continuous process (see (Lowther2, ) Lemma 1.4). If, furthermore, is twice continuously differentiable then it can be shown that is a solution to the stochastic differential equation

| (2.1) |

for a Brownian motion and with given by the forward equation

| (2.2) |

Then, if is Hölder continuous of order , the Yamada-Watanabe theorem ((Rogers, ) V, Theorem 40.1) says that (2.1) uniquely determines the law of . This is the familiar situation covered by the local volatility model, and widely employed in finance (see (Dupire2, )).

2.2 Jump processes

Now suppose that the supports of the marginal distributions are contained in the set of integers. Then, the process must be an integer valued pure jump process. Suppose furthermore that for every and integer . Then, the almost-continuous property says that cannot jump past any integer values, so can only jump between successive integers. Therefore, must be a piecewise constant process with jump sizes . For example, it could be a symmetric Poisson process (i.e., the difference of two standard Poisson processes).

More generally, jump processes can arise whenever the supports of the marginal distributions are not connected intervals. Consider, for example, a smooth in which is strictly convex in , so that the conditions considered in Section 2.1 are satisfied. Then define by

The corresponding marginal distributions then assign zero probability to the interval . Under the resulting martingale measure , the process will behave like a continuous diffusion satisfying the SDE (2.1) whenever or . However, the points will act like reflecting barriers, compensated by sometimes jumping across the interval .

2.3 Singular diffusions

Now suppose that is strictly convex in for every so that, as in section 2.1, we can conclude that is continuous under the associated ACD martingale measure. If, however, is not twice differentiable in then the marginal distributions will not be continuous with respect to the Lebesgue measure, and will not satisfy a stochastic differential equation such as (2.1).

For example, suppose that satisfies all of the properties considered in section 2.1 and define

Note that is not differentiable at and the corresponding marginal distributions have an atom at . Under the ACD martingale measure , the process will behave like a continuous diffusion satisfying (2.1) away from . However, , so is sticky at , spending a positive time there. If, furthermore, is strictly increasing in then will not be constant over any time intervals.

Similarly, it is not difficult to construct marginal distributions so that is rational with probability and with support equal to , resulting in continuous processes spending almost all their time in the rational numbers. This is the case with the Feller-McKean diffusion ((Rogers1, ) III.23), and similar situations can arise as a limit of random walks with randomly generated rates (see (Fontes, )).

3 Existence

We show how ACD martingales can be constructed with specified marginal distributions by taking limits of processes which match the marginals at finite sets of times. A weak compactness argument is used to prove existence of the limit.

For any set , let consist of the real valued functions on . We consider as a topological space using the topology of pointwise convergence, and denote its Borel -algebra by . The weak topology on the probability measures on is the topology generated by the maps for all real valued continuous and bounded functions on . We denote the coordinate process on by ,

which has natural filtration given by,

Then, for any measure on we use to denote the measure on obtained from the law of under with restricted to .

In particular, if is countable then is a Polish space, as it has a countable dense subset consisting of those such that is rational for all and zero for all but finitely many , and the topology is given by a complete metric

where .

Furthermore, a sequence of probability measures on converges to in the sense of finite-dimensional distributions if and only if weakly for every finite subset of .

We now prove the result that we need in order to be able to find limits of sequences of martingale measures. The idea here is to use weak compactness in order to pass to convergent subsequences.

A set of probability measures on a Polish space is said to be tight if for every there exists a compact set with for all , and is then weakly compact. In particular, for any tight sequence of probability measures , there is a probability measure and subsequence converging weakly to (see (HeWangYan, ) Theorem 15.39.) This allows us to find martingale measures with specified marginals as limits of sequences.

Lemma 3.1.

Let and be a sequence of martingale measures on such that .

Then, there exists a subsequence and a martingale measure on such that in the sense of finite-dimensional distributions. Furthermore, is a martingale under , continuous in probability and satisfies .

Proof.

First, choose any and . For every ,

As this can be made arbitrarily small by making large, we see that for every there exists a such that for every . Letting be a countable dense subset of and , this shows that there exists a sequence such that

Letting be the compact set of all satisfying ,

So the sequence is tight and, by passing to a subsequence if necessary, we may assume that it convergence weakly to a probability measure on .

For every and , weak convergence gives

Letting increase to infinity and using dominated convergence,

| (3.1) |

If are in , is -measurable, continuous and such that is bounded, and then,

Letting increase to infinity and using dominated convergence shows that is a -submartingale. So,

Therefore, is a -submartingale. Furthermore, as , (3.1) shows that is independent of and is a -martingale. This allows us to extend to all using for any in . We now show that is continuous in probability. As it is a martingale, it has almost-sure left and right limits for every (for set ). Assuming that , taking the difference of the right and left limits of equation (3.1) in and using the continuity of gives,

So, for every , showing that . As is a martingale and right-continuous in probability, it has a càdlàg version and, therefore, there is a measure on satisfying . Furthermore, is a martingale which is continuous in probability under . Taking limits of also shows that .

It only remains to show that in the sense of finite dimensional distributions. We use proof by contradiction, so suppose that this is not the case. Then there would exist a random variable of the form (1.3) for a finite subset of for which does not converge to . Passing to a subsequence if necessary, we may suppose that

| (3.2) |

for some and every . Setting the above argument shows that, by passing to a further subsequence, there exists a measure on such that . In particular, and, by right-continuity in , it follows that and contradicting (3.2). ∎

Combining Lemma 3.1 with the results of (Lowther2, ) gives the following, which will be used to construct ACD martingale measures with specified marginals by taking limits of measures matching the marginals at finitely many times.

Lemma 3.2.

Let be a sequence of ACD martingale measures on and be such that . Then, there exists a subsequence converging in the sense of finite-dimensional distributions to an ACD martingale measure satisfying .

Proof.

First, Lemma 3.1 says that there exists a subsequence converging in the sense of finite-dimensional distributions to a martingale measure satisfying (1.2) under which is continuous in probability. However, Corollary 1.3 of (Lowther2, ) states that under such a limit, is an almost-continuous diffusion. ∎

To complete the proof of the existence of the ACD martingale measure, it just needs to be shown that it is possible to fit the marginals arbitrarily closely and Lemma 3.2 will provide us with the required limit. There are, however, many different ways in which we can go about this. For example, we could construct a diffusion as the solution of a stochastic differential equation to match smooth . Alternatively, finite state Markov chains could be used to approximate the marginals by finite distributions. However, one way to exactly match the marginals at any finite set of times is to use a Skorokhod embedding to time change a Brownian motion, as we describe now. This uses the methods described in (Hobson2, ).

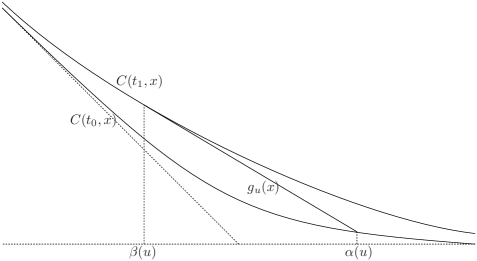

Fix any and times . Also, let be the associated one dimensional measures, satisfying . Then, define the distribution function . For set , and let be

Then, is chosen to satisfy . This uniquely defines when (see Figure 1), otherwise we set . Also, set . This is right-continuous and increasing from to , so is another distribution function.

If is a Brownian motion with initial distribution and is its maximum process, then a stopping time can be defined by

| (3.3) |

Then is a uniformly integrable martingale and has law equal to . See (Hobson2, ) for details (Proposition 2.2 and Corollary 2.1).

Lemma 3.3.

Let and . Then, there exists an ACD martingale such that for .

Proof.

Let be a Brownian motion with initial measure and be the stopping time (3.3). Let be any continuous function increasing from to . For example, . We also set for and for . Defining the stopping times

the ACD martingale can then be constructed as . The distributions of and are and ((Hobson2, ) Proposition 2.2). As is uniformly integrable, will be a martingale. The paths of are very simple — if is the first time at which then

So can only have a single jump at time , at which .

It only remains to show that is an almost-continuous diffusion. Continuity in probability is easy. As and by the martingale property, it follows that almost-surely.

The stopping times are hitting times of the strong Markov process , where , so the time changed process will also be strong Markov. However, if and is constant as soon as , so must be strong Markov.

We finally show that is almost-continuous, so choose a càdlàg process independent and identically distributed as . If , and for then we can let be the first time at which , at which point we must have . In fact, must be the first time at which , and so is previsible. So, the martingale property gives and and, as , , we have . ∎

This is easily extended to match the marginals at a finite set of times.

Corollary 3.4.

Let and be finite. Then, there exists an ACD martingale measure on such that for all .

Proof.

If is a single time, then can be taken to be the measure under which is independent of with the required distribution. For we use induction on . Suppose that there is an ACD martingale measure matching the required marginals at times . By Lemma 3.3 there is an ACD martingale measure matching the required marginals at times . Noting that has the same distribution under both and , we can join these two measures together at time to get , which is the unique measure on such that

for all bounded random variables where is -measurable and is -measurable. That is an ACD martingale under follows from the fact that it satisfies these properties over each of the intervals and . ∎

Finally for this section, Corollary 3.4 is applied to construct the required ACD martingale measure.

Lemma 3.5.

For every there is an ACD martingale measure on satisfying .

4 Uniqueness

Using a generalized form of the backward Kolmogorov equation, it was shown in (Lowther4, ) that continuous and strong Markov martingales are uniquely determined by their marginal distributions. In this section we apply the arguments developed there to ACD martingales. The idea is that if is a diffusion satisfying the stochastic differential equation (2.1) and it is assumed that is twice continuously differentiable, then the backward Kolmogorov equation

can be combined with the forward equation (2.2) to obtain the following martingale condition for ,

This applies to twice continuously differentiable functions . Multiplying by a smooth with compact support in , integration by parts gives

| (4.1) |

This expression is defined for differentiable functions, and differentiability in can be relaxed by replacing terms such as by the Lebesgue-Stieltjes integral . The class of functions we consider is as follows.

Definition 4.1.

Denote by the set of functions such that

-

•

is Lipschitz continuous in and càdlàg in ,

-

•

for every and then

-

•

the left and right derivatives of with respect to exist everywhere.

Also, let be the functions with compact support in .

In particular, if is a càdlàg martingale then will be convex in and càdlàg and increasing in , so . Using to denote the left limit of in , it was shown in (Lowther4, ) (Lemma 2.2) that for the partial derivatives and exist almost everywhere with respect to the measure . This enables the following definition to be made. Here, where we suppress the arguments of functions inside the integral signs they are understood to be .

Definition 4.2.

For every define the linear map

Comparing with the right hand side of (4.1), we expect the martingale condition to be , which is indeed the case for continuous processes. However, to include discontinuous processes jump terms need to be added, leading to the following definition.

Definition 4.3.

Let be a càdlàg martingale. Then, for every define the linear map

where is defined by and

| (4.2) |

The sum of will be integrable (see (Lowther4, )), so is well defined. We have the following necessary martingale condition.

Lemma 4.4.

Let be a càdlàg martingale and . If is a martingale then .

See (Lowther4, ), Theorem 3.8. To prove Theorem 1.3, the converse of this statement needs to be shown and, for almost-continuous processes, we need to demonstrate that the jump terms can be eliminated to express the martingale condition solely in terms of .

Fortunately, the jump terms will indeed drop out of the expression for as long as is chosen such that is linear in across each of the connected components of the complement of the support of . To show this, we make use of the marginal support, which was defined in (Lowther1, ) to be the set constructed from the supports of the marginal distributions of as,

We now prove the following.

Lemma 4.5.

Let be an ACD martingale and satisfy for every and outside the support of . Then, .

Proof.

It was shown in Corollary 4.8 of (Lowther1, ) that for an almost-continuous process, the set

is almost surely disjoint from the marginal support of . Then, the condition of the lemma gives on , so

| (4.3) |

for all , almost surely. Finally, as there are only countably many times for which and is continuous in probability, whenever and (4.3) gives . ∎

The following result shows that it will be enough to only consider functions satisfying outside the marginal support of .

Lemma 4.6.

Let be an ACD martingale, and be convex with bounded derivative . Then, there exists an such that

| (4.4) |

for every , where is convex in , right-continuous and decreasing in , and outside the marginal support of .

Proof.

First, by theorems 1.5 and 1.6 of (Lowther1, ), can be chosen to be convex in with derivative and satisfying equation (4.4) for all . Theorem 1.7 of (Lowther1, ) also says that is continuous on the marginal support of over the range . We can extend across any bounded connected component of by linear interpolation. Also, we can linearly extrapolate w.r.t. above the supremum of with gradient and below the infimum with gradient . This gives outside the support of . For simplicity, over , fix to be a linear function of independent of . Then, for , Jensen’s inequality gives

from which it follows that for every in the support of . By linear interpolation and extrapolation of outside the support of , this inequality is satisfied for all . So, is decreasing in . We now define to be the limit of as strictly decreases to . Then, is convex in , right-continuous and decreasing in , and has derivative satisfying . By continuity, whenever and is in the support of , so also satisfies (4.4).

It only remains to show that for and outside the support of . First, suppose that is in a bounded connected component of . As was chosen to be linearly interpolated outside the support of ,

The reverse inequality follows from the convexity of and at points and (by continuity). So, .

Now suppose that is in a connected component of . As is a martingale with , we must have for all . But was chosen to be linearly extrapolated with gradient over ,

so we again have . Finally, by the same argument, for in a connected component of . ∎

For a general , need not be a semimartingale, so it will be necessary to consider the more general class of Dirichlet processes. These processes were introduced by Follmer in (Follmer2, ), generalized to the non-continuous case in (Stricker1, ) and (Coquet, ), then further extended to the form required here in (Lowther3, ) and (Lowther4, ). So using the notation of (Lowther4, ), a process is said to have zero continuous quadratic variation if its quadratic variation exists and satisfies . For brevity, we say that a process is a z.c.q.v. process if it is càdlàg, adapted and has zero continuous quadratic variation. A Dirichlet process is then defined as the sum of a semimartingale and a z.c.q.v. process. Quadratic covariations of Dirichlet processes are well defined, and for any semimartingale and Dirichlet process the integral can be defined using integration by parts,

The following result then says that gives a measure of the drift of the Dirichlet process for any . Here, denotes the functions which decompose as for a càdlàg martingale and finite variation process satisfying

for all .

Lemma 4.7.

Let be a càdlàg martingale and . Then there is a unique decomposition

| (4.5) |

for martingale and previsible z.c.q.v. process with . Furthermore, for any with ,

and,

For the proof of this, see (Lowther4, ) lemmas 5.4 and 8.1. The proof of the martingale condition for ACD martingales will make use of Lemma 4.7 to show that the process in decomposition (4.5) is zero. This will be done by showing that the time reversed conditional variation, below, is zero. First, the reverse filtration is

and is defined by

where the supremum is taken over all sequences in and all -measurable random variables . The following result from (Lowther4, ) (Lemma 7.2) will be required to bound the variation of .

Lemma 4.8.

Let be a càdlàg real valued process and be a z.c.q.v. process such that is integrable and .

Suppose furthermore that is -measurable for all and that there exists a measurable such that for all . Then, has integrable variation satisfying

In order to apply Lemma 4.8 it will be necessary to calculate , which we do by making use of the quasi-left-continuity of . Recall that a càdlàg process is quasi-left-continuous if for every previsible stopping time .

Lemma 4.9.

Every ACD martingale is quasi-left-continuous.

Proof.

Let be an ACD martingale, , and be bounded and Lipschitz continuous with coefficient . Then, there exists a bounded such that is Lipschitz continuous in with coefficient and,

| (4.6) |

for every (see (Lowther1, ) Theorem 1.5 or (Lowther2, ) Lemma 4.3). By linearity, this extends to all stopping times taking only finitely many values in .

If and is continuous and bounded, then the continuity of at together with bounded convergence gives

If we let increase to then will go to , and we see that the above equality also holds for . As is uniformly continuous in , this shows that is continuous in for every in the support of . So, is continuous on the marginal support of . By lemmas 4.3 and 4.4 of (Lowther1, ), the continuity in probability of implies that the paths of and lie in the marginal support of at all times. So, by taking limits of stopping times which take finitely many values in , equation (4.6) extends to all stopping times. Similarly, taking increasing limits of stopping times gives

for all previsible stopping times . We now note that in probability as . So, by uniform continuity in , on the marginal support of , giving

So, if is any bounded measurable function and , we can multiply by and take expectations,

Finally, by the monotone class lemma, this extends to all bounded measurable functions and taking gives . ∎

Finally, we prove the martingale condition .

Theorem 4.10.

Let be an ACD martingale and satisfy for and outside the support of . Then, is a martingale if and only if .

Proof.

First, Lemma 4.5 gives . Then, if is a martingale Lemma 4.4 gives . Conversely, suppose that and let be decomposition (4.5). Also, choose any twice continuously differentiable with compact support and set , which is a previsible z.c.q.v. process (see (Lowther4, ) Lemma 5.5). We will show that the necessary conditions to apply Lemma 4.8 to are satisfied.

First, for every previsible stopping time , and the quasi-left-continuity of gives

By previsible section (e.g., (HeWangYan, ) Corollary 4.11), it follows that this equality holds simultaneously at all times. In particular

| (4.7) |

for all times at which . As at all but countably many times, and is continuous in probability, the right hand side of (4.7) equals when . Also, as is previsible and is quasi-left-continuous, the left hand side is also zero when . So, (4.7) holds for all times, and is a function of , as required by Lemma 4.8.

We now show that . To do this, first choose any and let be bounded and a difference of convex Lipschitz continuous functions. Lemma 4.6 says that there is an such that for outside the support of and,

for . Then, integration by parts gives

| (4.8) |

(see (Lowther4, ) equation 5.5 and Lemma 5.6). As is a martingale over it is clear that . Also, is twice continuously differentiable and Ito’s formula shows that it is in (see (Lowther4, ) Lemma 4.3). So, by Lemma 8.2 of (Lowther4, ), the product is also in . So, we can take expectations of (4.8) to get

| (4.9) |

for . Here, we have used that fact that the final term on the right hand side of (4.8) is a local martingale and applied Lemma 4.7. Taking limits as decreases to , (4.9) holds for . Then, the monotone class lemma shows that (4.9) holds for all bounded and measurable functions . So, if is a bounded -measurable random variable, the Markov property for gives

and, .

Proof of Theorem 1.3.

Lemma 3.5 shows existence of the ACD martingale measure. To prove uniqueness, suppose that we have two such measures and . Choose any and convex and Lipschitz continuous . By Lemma 4.6 there is an such that outside the marginal support of and satisfying

for all . Letting increase to gives -a.s.. So, we may set for all , and will be a -martingale.

However, it is clear that the stopped process is also an ACD martingale under both and . So, setting we can apply Theorem 4.10 to get . Another application of Theorem 4.10 shows that is also a -martingale and,

So has the same pairwise distributions under both and . As they are Markov measures with common initial distribution, this gives . ∎

Proof of Theorem 1.4.

Choose any and sequence such that . We use proof by contradiction to show that , so suppose that this is false. Then there would exist an and a random variable of the form (1.3) such that

| (4.10) |

infinitely often. By passing to a subsequence if necessary, we may suppose that this inequality holds for every . Then, Lemma 3.2 says that by passing to a further subsequence we have for an ACD martingale measure satisfying (1.2). So, the uniqueness part of Theorem 1.3 gives , and contradicting (4.10). ∎

5 Extremal Marginals

Note that the space is a convex subset of the space of all real-valued functions on . For any convex subset of a vector space there is a concept of extremal points — they are the points which cannot be expressed as a convex combination of other elements in the set. More precisely, for a convex subset of a vector space , an element is said to be extremal if given any and any such that then . We shall call an element of extremal if it is extremal among the convex set of all other elements of with the same values at time .

Definition 5.1.

A is extremal if given any and such that and then .

It can then be shown that there is a unique martingale measure fitting the marginals given by an extremal element of .

Lemma 5.2.

Let be extremal. Then, there exists a unique martingale measure on satisfying .

Proof.

As Theorem 1.3 says that such a martingale measure exists, we only need to prove uniqueness. Let us start by showing that any such measure is Markov. Given any and -measurable random variable with , define by for and,

| (5.1) | |||

for . It is easily checked that are in , and . As is extremal, this implies . For , putting into (5.1) gives

so , and is indeed Markov.

Let us now suppose that , are two such martingale measures. Choose any and -measurable random variable with , and define by for and,

| (5.2) | |||

for . Again, it is easily checked that are in with and . As is extremal this implies . For , putting into (5.2) gives

for all . Therefore, and are Markov measures for with the same pairwise and initial distributions, so . ∎

Theorem 1.5 will follow once it is shown that the extremal elements are dense in . For we will construct extremal elements of which match any given increasing sequence of times. We start by showing that there is an extremal element matching at two times. The method used here corresponds to the ACD martingales constructed in Section 3 (Lemma 3.3), which was based on the Skorokhod embedding described in (Hobson2, ), so let us recall some of the definitions from Section 3.

Given a let be the corresponding marginal distributions satisfying . Fixing , define the distribution function and for set . For set

and define by . This uniquely defines whenever (see Figure 1), otherwise we take .

We define by setting equal to for , for and,

| (5.3) |

for , where is set to . We show that this does indeed give an extremal element of .

Lemma 5.3.

Suppose that and . Then defined by (5.3) is an extremal element of such that equals for and for .

Proof.

For , is a convex function of lying between and (see Figure 1). To show that it just needs to be shown that it is continuous and increasing in . So, pick any . Then, and . For any this gives

Also, if then

So, is increasing in .

Now choose any with , and choose to minimize . To see that this exists, note that choosing small enough so that gives

but the limit as is . So, by continuity, it must have a minimum.

Choosing such that gives , and it follows that . Therefore, maps the interval onto and must be continuous.

It only remains to show that is extremal, so suppose that for , , and

In order to show that we shall make repeated use of the simple fact that if a non-trivial convex combination of two increasing functions is constant, then those functions must also be constant. In particular, for all so we must also have for and . Similarly, for .

Now choose any and set , . Then for , the definition of gives , so it is also true that for .

Also, if then . Therefore . Furthermore, for all in

As are increasing functions of , this shows that they are constant as runs through this interval. Therefore, are linear functions of over . So, we have shown that

Now suppose that there exists an such that . Choose such that and set , . It follows that , so the fact that and are convex in and increasing in gives

Taking the right hand limits in gives .

Similarly, if then and the above argument gives . So .

This shows that the function has a non-positive derivative everywhere and must be decreasing, so the limit as implies that is identically . So , from which it follows that . ∎

The previous lemma allows us to construct an extremal element of matching at an increasing sequence of times.

Corollary 5.4.

Suppose that and are in . Then there is an extremal such that for each .

Proof.

Without loss of generality, we assume that . By Lemma 5.3 there exists extremal such that equals for and equals for (). Define by for .

It is clear that . It just needs to be shown that it is extremal. So suppose that

| (5.4) |

for , , and . We use induction on to show that for . For this is a required condition, so suppose that and that this holds for all . If then is extremal, and (5.4) gives for .

So, by induction, . ∎

Finally we complete the proof of Theorem 1.5, showing that given by Theorem 1.3 is the unique continuous map to the martingale measures and matching all possible sets of marginals.

Proof of Theorem 1.5.

Choose any and be a random variable of the form (1.3). We just need to show that .

First, Corollary 5.4 gives a sequence of extremal elements of such that for all and, consequently, .

Then, as is dense in , there is a sequence such that as , where is the metric on given by (1.4).

Now, fixing any , Lemma 3.1 says that, by passing to a subsequence if necessary, there exists a martingale measure satisfying equation (1.2) and such that in the sense of finite-dimensional distributions as . However is extremal so, by Lemma 5.2, . Therefore, for every we can choose an such that

In particular, so the continuity of shows that tends to in the sense of finite dimensional distributions as goes to infinity. Similarly, tends to giving,

References

- (1) Leif Andersen and Jasper Andreasen. Jump-diffusion processes: Volatility smile fitting and numerical methods for option pricing. Review of Derivatives Research, 4(3):231–262, 2000.

- (2) Mark Britten-Jones and Anthony Neuberger. Option prices, implied price processes, and stochastic volatility. The Journal of Finance, 55(2):839–866, 2000.

- (3) Peter Carr, Hélyette Geman, Dilip B. Madan, and Marc Yor. From local volatility to local Lévy models. Quant. Finance, 4(5):581–588, 2004.

- (4) François Coquet, Jean Mémin, and Leszek Słomiński. On non-continuous Dirichlet processes. J. Theoret. Probab., 16(1):197–216, 2003.

- (5) Emanuel Derman and Iraj Kani. Riding on a smile. Risk, 7(2):32–39, February 1994.

- (6) Bruno Dupire. Pricing and hedging with smiles. In Mathematics of derivative securities (Cambridge, 1995), volume 15 of Publ. Newton Inst., pages 103–111. Cambridge Univ. Press, Cambridge, 1997.

- (7) H. Föllmer. Dirichlet processes. In Stochastic integrals (Proc. Sympos., Univ. Durham, Durham, 1980), volume 851 of Lecture Notes in Math., pages 476–478. Springer, Berlin, 1981.

- (8) L. R. G. Fontes, M. Isopi, and C. M. Newman. Random walks with strongly inhomogeneous rates and singular diffusions: convergence, localization and aging in one dimension. Ann. Probab., 30(2):579–604, 2002.

- (9) Sheng-wu He, Jia-gang Wang, and Jia-an Yan. Semimartingale theory and stochastic calculus. Kexue Chubanshe (Science Press), Beijing, 1992.

- (10) David G. Hobson. The maximum maximum of a martingale. Séminaire de probabilités de Strsbourg, 32:250–263, 1998.

- (11) Hans G. Kellerer. Markov-Komposition und eine Anwendung auf Martingale. Math. Ann., 198:99–122, 1972.

- (12) George Lowther. A generalized backward equation for one dimensional processes. Pre-print available as arxiv:0803.3303v2 [math.PR] at arxiv.org, August 2008.

- (13) George Lowther. Limits of one dimensional diffusions. Pre-print available as arXiv:0712.2428v2 [math.PR] at arxiv.org, August 2008.

- (14) George Lowther. Nondifferentiable functions of one dimensional semimartingales. Pre-print available as arXiv:0802.0331v2 [math.PR] at arxiv.org, August 2008.

- (15) George Lowther. Properties of expectations of functions of martingale diffusions. Pre-print available as arXiv:0801.0330v1 [math.PR] at arxiv.org, January 2008.

- (16) Dilip B. Madan and Marc Yor. Making Markov martingales meet marginals: with explicit constructions. Bernoulli, 8(4):509–536, 2002.

- (17) L. C. G. Rogers and David Williams. Diffusions, Markov processes, and martingales. Vol. 2. Wiley Series in Probability and Mathematical Statistics: Probability and Mathematical Statistics. John Wiley & Sons Inc., New York, 1987.

- (18) L. C. G. Rogers and David Williams. Diffusions, Markov processes, and martingales. Vol. 1. Cambridge Mathematical Library. Cambridge University Press, Cambridge, 2000. Foundations, Reprint of the second (1994) edition.

- (19) V. Strassen. The existence of probability measures with given marginals. Ann. Math. Statist, 36:423–439, 1965.

- (20) C. Stricker. Variation conditionnelle des processus stochastiques. Ann. Inst. H. Poincaré Probab. Statist., 24(2):295–305, 1988.