Theory of Zipf’s Law and of General Power Law Distributions with Gibrat’s law of Proportional Growth ††thanks: The authors acknowledge helpful discussions and exchanges with Xavier Gabaix.

Abstract

We summarize a book under publication with the above title written by the three present authors, on the theory of Zipf’s law, and more generally of power laws, driven by the mechanism of proportional growth. The preprint is available upon request from the authors.

For clarity, consistence of language and conciseness, we discuss the origin and conditions of the validity of Zipf’s law using the terminology of firms’ asset values. We use firms at the entities whose size distributions are to be explained. It should be noted, however, that most of the relations discussed in this book, especially the intimate connection between Zipf’s and Gilbrat’s laws, underlie Zipf’s law in diverse scientific areas. The same models and variations thereof can be straightforwardly applied to any of the other domains of application.

JEL classification: G11, G12

Keywords: Zipf’s law, firm sizes, city sizes, proportional growth, Gibrat’s law, geometric Brownian motion, diffusion, diffusion equation

Executive summary

Zipf’s law is one of the few quantitative reproducible regularities found in economics. It states that, for most countries, the size distributions of city sizes and of firms (with additional examples found in many other scientific fields) are power laws with a specific exponent: the number of cities and of firms with size greater than is inversely proportional to .

Most explanations start with Gibrat’s law of proportional growth but need to incorporate additional constraints and ingredients introducing deviations from it.

Here, we present a general theoretical derivation of Zipf’s law, providing a synthesis and extension of previous approaches. First, we show that combining Gibrat’s law at all firm levels with random processes of firms’ births and deaths yield Zipf’s law under a “balance” condition between firm growth and their death rate.

We find that Gibrat’s law of proportionate growth does not need to be strictly satisfied. As long as the volatility of firms’ sizes increases asymptotically proportionally to the size of the firm and that the instantaneous growth rate increases not faster than the volatility, the distribution of firm sizes follows Zipf’s law. This suggests that the occurrence of very large firms in the distribution of firm sizes described by Zipf’s law is more a consequence of random growth than systematic returns: in particular for large firms, volatility must dominate over the instantaneous growth rate.

We develop the theoretical framework to take into account

-

1.

time-varying firm creation,

-

2.

firms’ exit resulting from both a lack of sufficient capital and sudden external shocks, and

-

3.

the coupling between firms’ birth rate and the growth of the value of the population of firms.

We predict deviations from Zipf’s law under a variety of circumstances, for instance when the balance between the birth rate, the non-stochastic growth rate and the death rate is not fulfilled, providing a framework for identifying the possible origin(s) of the many reports of deviations from the pure Zipf’s law. The tail index that characterizes the hyperbolic decay of the distribution is found to depend on several characteristics of the economic environment. Amongst others, the average growth rate of firms’ asset value, the rate of firms’ birth and the hazard rate of a firm’s sudden death have a direct impact on the value of the tail index.

Reciprocally, deviations from Zipf’s law in a given economy provides a diagnostic, suggesting possible policy corrections. The results obtained here are general and provide an underpinning for understanding and quantifying Zipf’s law and the power law distribution of sizes found in many fields.

A general result unraveled by our study is that Zipf’s law is obtained if and only if a balanced condition is fulfilled: the sum of all the mechanisms responsible for the growth and/or decline of firms must vanish on average. Any departure from this requirement yields a departure of the tail index from its canonical value . This result can allow one to understand why different tail indexes are reported in the literature for different countries around the world. However, the reasons that underpin the validity of the balance condition are not yet clear. No economic law can justify why all these mechanisms should almost exactly compensate one another. In the absence of such economic argument, one has to resort to Gabaix’s explanation based upon the idea that, in order to make stationary the distribution of firm’s sizes, one has to first remove the impact of the overall economy on the growth of each individual firm. Therefore, since the overall economy grows at the same rate as each individual firm, on average, the balance condition is satisfied in the referential of the growing economy.

1 Motivations and organization of the book

One of the broadly accepted universal laws of complex systems, particularly relevant in social sciences and economics, is that proposed by \citeasnounZipf49. Zipf’s law usually refers to the fact that the survival probability that the value of some stochastic variable, usually a size or frequency, is greater than , decays with the growth of as . This in turn means that the probability density functions exhibits the power law dependence

| (1) |

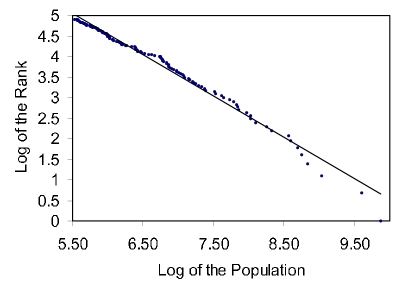

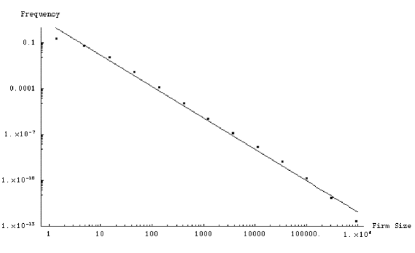

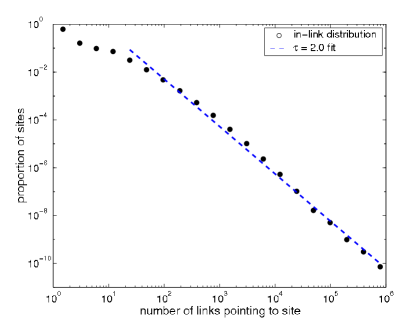

Perhaps the distribution most studied from the perspective of Zipf’s law is that of firm sizes, where size is proxied by sales, income, number of employees, or total assets. Many studies have confirmed the validity of Zipf’s law for firm sizes existing at current time and estimated with these different measures [SimonBonini, IS77, Sutton97, Axtell01, Okuyama1999, Gaffeo03, Aoyama04, Fujiwara_etal_04a, Fujiwara_etal_04b]. Initially formulated as a rank-frequency relationship quantifying the relative commonness of words in natural languages [Zipf49], Zipf’s law accounts remarkably well for the distribution of city sizes [Gabaix99] as well as firm sizes all over the world, as just mentioned. Recently, Zipf’s law has also been found in Web access statistics and Internet traffic characteristics [Huberman1, AlbertBara02] as well as in bibliometrics, informetrics, scientometrics, and library science (see [Huberman2] and references therein). There are also suggestions for applications to other physical and biological, sociological and financial market processes (see list of references in http://linkage.rockefeller.edu/wli/zipf/index_ru.html). Figure 1 illustrates several applications of Zipf’s law to different fields of social and natural sciences.

Among the many more or less successful explanations proposed to understand the origin of Zipf’s law, one of the most promising is the explanation by \citeasnounGabaix99 and \citeasnounIoannidesGabaix03 formulated in the context of the distribution of city sizes, based on Gibrat’s law. \citeasnounGabaix99 assumed that each city exhibits a stochastic growth rate distributed independently from its present size. \citeasnounGabaix99 showed that Gibrat’s law for city growth (together with some important deviations of Gibrat’s law), normalized to the whole population of a given country, leads to distributions of city sizes very close to Zipf’s law. However, the derivation of \citeasnounGabaix99 suffers from a few problems.

First, the exact scale-independent Gibrat’s law leads to a log-normal distribution of city sizes, which is not strictly a power law and only slowly converges to a power law in the limit of large log-variance (and some other conditions), becoming at the same time more and more degenerate. Some additional assumptions are therefore needed in order to produce the stable non-degenerate Zipf’s law. In particular, \citeasnounGabaix99 assumed that, for cities of small sizes, there are some exogenous factors preventing further decaying of their population (see also [LevySolomon96, Malcai_etal99]). More appropriate to social and economic phenomena is the supposition, contrary to preventing population decay, of eliminating cities or firms as they reach a small size. An example is the transition from city to rank of village as the size goes below some threshold. In the context of an economy of firms, it is important to take into account the continuous process with births and deaths playing a central role at time scales as short as a few years. A goal of the present book is to demonstrate that death (as well as birth) processes are especially important to understand the economic foundation of Zipf’s law and its robustness. We will consider two different mechanisms for the exit of a firm: (i) when the firm total asset value becomes smaller than a given minimum threshold (which can vary with time and with countries) and (ii) when an exogenous shock occurs, modeling for instance operational risks, independently of the size of the firm.

Another shortcoming of Gabaix’s approach is the simplifying supposition that all cities originate at the same instant , and then only grow stochastically, obeying the balanced Gibrat’s law mentioned above. We believe that it is more realistic, especially for the description of the behavior of the asset value of firms (which is more dynamic than the formation of cities), that the births of firms occur according to a random point process characterized by some mean rate . Jointly, one should take into account the well-documented evidence that firms die, for instance when their size go under some low asset value level. It turns out that taking into account the random flow of firm births and deaths, in combination with Gibrat’s law, leads to the pure and non-degenerate Zipf’s law, without the need to the rather artificial modification of Zipf’s law for small sizes [We note that the fact that deviation of Gibrat’s law has been documented for small firms is another issue, as the documented deviations do not necessarily obey the assumptions needed in Gabaix’s derivation.] As a bonus, the approach in terms of the dynamics of birth-death together with stochastic growth, that we develop here, leads to specific predictions of the conditions under which deviations from Zipf’s law occur, which help rationalize the empirical evidence documented in the literature. The conditions involve either deviations from Gibrat’s law in the stochastic growth process of firms or the existence of an unbalanced growth or decay of the mean birth rate of new firms, as we explain in details below.

For transparency of derivations and for convenience of analytic calculations, we use a continuous version of Gibrat’s law, allowing us to benefit from the properties of the Wiener process and the mathematical framework of Kolmogorov’s diffusion equations. We unearth new properties associated with the stochastic behavior of firm assets. We show that the death of firms at some low value level as well as possibly significant deviations from Gibrat’s law do not affect the asymptotic validity of Zipf’s law in the limit of large firm sizes. By analyzing a large class of diffusion processes modeling the behavior of firm assets with growth rates very different from Gibrat’s condition, we find general conditions for the validity of Zipf’s law. Specifically, we have discovered stochastic growth models with non-Gibrat properties, leading to Zipf’s and related power laws for the current density of firms’ asset values.

The book is organized as follows. Chapter 2 presents the continuous version of Gibrat’s law and some peculiarities of the stochastic behavior of the geometric Brownian motion of firms’ asset values, resulting from Gibrat’s law.

Chapter 3 describes the proposed model for the current density of firms’ asset values, taking into account the random flow of the birth of firms. We show that, if some natural balance condition holds, which is analogous to \citeasnounGabaix99 normalizing condition, while the mean birth rate of firms is independent of time (), then the exact Zipf’s law holds true.

Amazingly, despite the relevance of Gibrat’s law and the corresponding geometric Brownian motion in a wide range of physical, biological, sociological and other applications, many researchers do not make use of many of the interesting properties exhibited by realizations of the geometric Brownian motion, in order to derive detailed explanations of Zipf’s and related power laws. Thus, in chapter 4, we gather little-known information concerning the statistical properties of realizations of the geometric Brownian motion, which play a significant role for the understanding of the roots and conditions of the validity of Zipf’s law.

Chapter 5 discusses in detail the influence on the validity of Zipf’s law of the occurrence of the death of firms when their value falls below some low level. In chapter 6, we derive an equation for the steady-state density of firm asset values, which enables us to explore in detail the consequences of deviations from Gibrat’s law at moderate asset values on the validity of Zipf’s law at higher asset values.

Chapters 7 and 8 are devoted to discussing possible deviations from Zipf’s law due respectively to the sudden death of firms and the time dependence of the birth rate. It is shown that, even in such situations, Zipf’s law holds if some generalized balance condition is valid. In particular, we discuss the robustness of Zipf’s law to variations of the mean birth rate and of the rate of growth of the mean asset value of particular firms. The second part of Section 8 presents a simple coupled model describing the possible connection between the stochastic behavior of firms’ asset values and the mean birth rate.

In addition to the mechanisms in terms of birth, death and random growth which have been considered in the previous chapters, we envision that the next level of development of a complete mathematical theory of firms needs to take into account the mechanism of mergers between firms (referred to as M&A for “merger and acquisition”), as well as it symmetric, the phenomenon of creation of spin-off firms created from parent firms which privatize a part of their existing business as separate units. For this, the long tradition in physics concerning the investigation of the processes of coagulation (merger) and of fragmentation (spin-off) could provide a fertile reservoir of ideas and techniques [Aldous99, Leyvraz03]. Chapter 9 presents the integro-differential equation that expresses the coupling between firms introduced by M&A and spinoffs and provides preliminary results. This section is more an appetizer and encouragement for future works than a complete treatment.

Table of contents

2. Continuous Gibrat’s law and Gabaix’s derivation of Zipf’s law

2.1 Definition of continuous Gibrat’s law

2.2 Geometric Brownian motion

2.3 Self-similar properties of the geometric Brownian motion

2.4 Time reversible geometric Brownian motion

2.5 Balance condition

2.6 Log-normal distribution

2.7 Gabaix’s steady-state distribution

3. Flow of firm creation

3.1 Empirical evidence and previous works on the arrival of new firms

3.2 Mathematical formulation of the flow of firms’ births at random instants

3.3 Steady-state density of firms’ asset values obeying Gibrat’s law

3.4 Quick and dirty explanation of the origin of the power law distribution of firm szies

4. Useful properties of realizations of the geometric Brownian motion

4.1 Relationship between the distributin of firm’s waiting times and sizes

4.2 Mean growth versus stochastic decay

4.3 Geometrically transparent definitions of stochastically decaying and growing processes

4.4 Majorant curves of stochastically decaying geometric Brownian motion

4.5 Maximal value of stochastically decaying geometric Brownian motion

4.6 Extremal properties of realizations of stochastically growing geometric Brownian motion

4.7 Quantile curves

4.8 Geometric explanation of the steady-state density of a firm’s asset value

5. Exit or “death” of firms

5.1 Empirical evidence and previous works on the exit of firms

5.2 Life-span above a given level

5.3 Distribution of firms’ life durations above a survival level

5.4 Killing of firms upon first reaching a given asset level from above

5.5 Life-span of finitely living firms

5.6 Influence of firms’ death on the balance condition

5.7 Firms’ death does not destroy Zipf’s law

6. Deviations from Gibrat’s law and implications for generalized Zipf’s laws

6.1 Diffusion process with constant volatility

6.2 Steady-state density of firms’ asset values in the presence of deviations from Gibrat’s law

6.3 Integrated flow

6.4 Semi-geometric Brownian motion

6.5 Generalized semi-geometric Brownian motion

6.5.1 Statistic properties of generalized semi-GBM

6.5.2 Deterministic skeleton of the mean density of firm sizes

6.5.3 Stochastic equation for the process

6.5.4 Size dependent drift and volatility

6.6 Zipf’s law for the steady-state density of firms’ asset values when the firm exit level is zero

6.7 Zipf’s laws when Gibrat’s law does not hold

7. Firms’ sudden deaths

7.1 Definition of the survival function

7.2 Exponential distribution of sudden deaths

7.3 Implications of the existence of sudden firm exits for semi-geometric Brownian motions

7.4 Zipf’s law in the presence of sudden deaths

7.5 Explanation of the generalized balance condition

7.6 Some consequences of the generalized balance condition

7.7 Zipf’s law as a universal law with a large basin of attraction

7.8 Rate of sudden death depending on firm’s asset value

7.9 Rate of sudden death depending on firm’s age

8. Non-stationary mean birth rate

8.1 Exponential growth of firms’ birth rate

8.2 Deterministic skeleton of Zipf’s law

8.3 Mean density of firms younger than age

8.4 Simple model of birth rate coupled with the overall firms’ value

8.5 Dynamics of mean birth rate

9. Conclusions and future directions

9.1 Importance of balance conditions for Zipf’s law

9.2 Mergers and acquisitions and spin-offs: general formalism

9.3 Mergers and acquisitions and spin-offs with Brownian internal growth

9.4 Mergers and acquisitions and spin-offs with GBM for the internal growth process

References

- [1] \harvarditemAdamic and Huberman2000Huberman1 Adamic, L.A. and B.A. Huberman (2000) The nature of markets in the World Wide Web Quarterly Journal of Electronic Commerce 1, 5-12.

- [2] \harvarditemAdamic and Huberman2002Huberman2 Adamic, L.A. and B.A. Huberman (2002) Zipf s law and the Internet, Glottometrics 3, 143-150.

- [3] \harvarditemAldous1999Aldous99 Aldous, D.J. (1999) Deterministic and stochastic models for coalescence (aggregation and coagulation): a review of the mean-field theory for probabilists, Bernoulli 5(1), 3-48.

- [4] \harvarditemAoyama et al.2004Aoyama04 Aoyama, H., Y. Fujiwara, W. Souma, in: H. Takayasu, eds. (2004) Proceedings of Second Nikkei Symposium on Econophysics, Springer, Tokyo.

- [5] \harvarditemAxtell2001Axtell01 Axtell, R.L. (2001) Zipf Distribution of U.S. Firm Sizes, Science 293, 1818-1820.

- [6] \harvarditemBarabasi and Albert2002AlbertBara02 Barabasi, A.-L., and R. Albert (2002) Statistical mechanics of complex networks, Reviews of Modern Physics 74, 47-97.

- [7] \harvarditemFujiwara et al.2004Fujiwara_etal_04a Fujiwara, Y., C. Di Guilmi, H. Aoyama, M. Gallegati and W. Souma (2004) Do Pareto Zipf and Gibrat laws hold true? An analysis with European Firms, Physica A 335, 197.

- [8] \harvarditemFujiwara et al. 2004Fujiwara_etal_04b Fujiwara, Y., H. Aoyamac, C. Di Guilmib, W. Soumaa and M. Gallegati (2004) Gibrat and Pareto Zipf revisited with European firms, Physica A 344 (1-2), 112-116.

- [9] \harvarditemGabaix1999Gabaix99 Gabaix, X. (1999) Zipf’s Law for Cities: An Explanation. Quarterly Journal of Economics 114, 739-767.

- [10] \harvarditemGaffeo et al.2003Gaffeo03 Gaffeo E., M. Gallegati and A. Palestrini (2003) On the Size Distribution of Firms. Additional Evidence from the G7 Countries, Physica A, 324, 117-123.

- [11] \harvarditemIjri and Simon1977IS77 Ijri, Y. and H. A. Simon (1977) Skew Distributions and the Sizes of Business Firms (North-Holland, New York).

- [12] \harvarditem Ioannides and Gabaix 2003IoannidesGabaix03 Ioannides, Y. M. and X. Gabaix (2003) The Evoluation of City Size Distributions, in Handbook of Urban and Regional Economics, J.V. Henderson and J-F Thisse (eds).

- [13] \harvarditemLeyvraz2003Leyvraz03 Leyvraz, F. (2003) Scaling theory and exactly solved models in the kinetics of irreversible aggregation, Physics Reports 383, 95-212.

- [14] \harvarditemLevy and Solomon1996LevySolomon96 Levy, M. and S. Solomon (1996) Power laws are logarithmic Boltzmann laws. International Journal of Modern Physics C 7, 595.

- [15] \harvarditemMaillart et al.2008MSSVK08 Maillart, T., D. Sornette, S. Spaeth and G. Von Krogh (2008) Empirical Tests of Zipf’s law Mechanism In Open Source Linux Distribution, submitted to Physical Review Letters.

- [16] \harvarditemMalcai et al.1999Malcai_etal99 Malcai, O., O. Biham and S. Solomon (1999) Power-law distributions and Lévy-stable intermittent fluctuations in stochastic systems of many autocatalytic elements,Physical Review. E 60 (2), 1299-1303.

- [17] \harvarditemOkuyama et al.1999Okuyama1999 Okuyama, K., M. Takayasu, H. Takayasu (1999) Zipf’s law in income distribution of companies, Physica A 269, 125-131. \harvarditemSimon and Bonini1958SimonBonini Simon, H. and C. Bonini (1958) The Size Distribution of Business Firms The American Economic Review 48(4), 607-617.

- [18] \harvarditemSutton1997Sutton97 Sutton, J. (1997) Gibrat’s legacy, Journal of Economic Literature 35, 40-59.

- [19] \harvarditemZipf1949Zipf49 Zipf, G.K. (1949) Human behavior and the principle of least effort, Addison-Wesley Press, Cambridge, Mass., USA.

- [20]