A fractional diffusion equation for two-point probability distributions of a continuous-time random walk

Abstract

Continuous time random walks are non-Markovian stochastic processes, which are only partly characterized by single-time probability distributions. We derive a closed evolution equation for joint two-point probability density functions of a subdiffusive continuous time random walk, which can be considered as a generalization of the known single-time fractional diffusion equation to two-time probability distributions. The solution of this generalized diffusion equation is given as an integral transformation of the probability distribution of an ordinary diffusion process, where the integral kernel is generated by an inverse Lévy stable process. Explicit expressions for the two time moments of a diffusion process are given, which could be readily compared with the ones determined from experiments.

pacs:

02.50.-r, 05.40.Fb, 05.10.GgThe concept of continuous time random walks (CTRWs), introduced by Montroll and Weiss Montroll almost four decades ago, has been successfully applied to a wide variety of transport problems in physics Bouchaud . In recent years the relationship between CTRWs and a class of Fokker-Planck equations with fractional temporal and/or spatial derivatives has attracted a lot of attention Metzler1 . In this line of research a major focus has been on the investigation of anomalous diffusion Shlesinger , a nonequilibrium phenomenon occurring in scientific fields ranging from astrophysics to biophysics and econophysics. A well known example is a subdiffusive CTRW in a force field, which leads to the well-known fractional Fokker-Planck equation (FFPE) Metzler2 , invoking the fractional Riemann-Liouville differential operator Podlubny . This equation can be written in the equivalent form:

| (1) |

where denotes the Caputo fractional differential operator Podlubny , defined as

| (2) |

for ( is the first derivative of g(t)). is a Fokker-Planck operator. For simple diffusion processes in and Eq. (1) is referred to as fractional diffusion equation (FDE) Schneider ; Podlubny . In the limit Eq. (1) reduces to the ordinary Fokker-Planck equation. Clearly, the Caputo fractional time derivative expresses the non-Markovian character of the underlying CTRW: the probability of finding the random walker at point at time depends on the whole history of the process from time up to . In combination with fractional evolution equations, the CTRW constitutes a versatile stochastic model which can take into account sub- and superdiffusive behaviour in complex systems as diverse as turbulence Friedrich1 , optical lattices, and biological cell motility (see Metzler3 for an extensive review). Recent new developments concern a more fundamental understanding of CTRWs and their application, e.g. the connection to ageing phenomena Barkai , ergodicity breaking Bel and inertial particles diffusing in a potential Friedrich2 .

However one important aspect has long been neglected in the literature on CTRWs and FFPEs. In general the ordinary Fokker-Planck equation is a deterministic evolution equation for the transition probability of the stochastic process, which is assumed to be Markovian. By virtue of the Markovian property one can calculate arbitrary -point pdfs with a single transition probability. On the other hand, in the case of the fractional analog Eq. (1), single-time pdfs are determined, which contain only very limited information about the stochastic process. In order to obtain complete information about a non-Markovian process like the CTRW, one has to consider the infinite set of -point pdfs. Recently, such multi-point statistics have been investigated in different approaches Barsegov ; Baule . In Barsegov , a two-point Green function has been determined with the help of the FFPE backward propagator and allows for the computation of three-point fluorescence lifetime correlation functions. Our previous work Baule discussed joint probability distributions of a CTRW based on a representation in terms of coupled Langevin equations. The purpose of the present paper is to derive a closed evolution equation for the two-point pdf of a CTRW, which is independent of the inverse Lévy-stable process investigated in Baule . This equation is the generalization of the single-time FDE (1) to two times. Considering the widespread interest in Eq. (1), the two-point generalization is expected to provide important further insight into the application of CTRWs to real world systems. In fact, multi-point statistics have already been probed in recent experiments on protein conformational dynamics Yang ; Min and highlight the importance of a more complete theoretical understanding of these statistics in anomalous diffusive systems.

A suitable starting point for the investigation of CTRWs is a representation in terms of coupled Langevin equations introduced by Fogedby Fogedby . Here the motion of a Brownian particle in an external force field in dimensions is described as:

| (3) | |||||

| (4) |

In this framework the CTRW is parametrized by the continuous path variable , which may be regarded as arclength along the trajectory. denotes the physical space and the physical time. Both are given as stochastic processes in the ’eigentime’ . Their statistics are determined by the properties of the stochastic variables and . In this work we consider the special case of statistically independent increments and , i.e. jump lengths and waiting times are uncoupled. Furthermore we want to restrict our considerations to a subdiffusive CTRW without force field. Accordingly, is assumed as a standard Langevin force with properties and . is consequently given as a standard Markovian Wiener process. The subdiffusive characteristics enter via the process . Its increments are assumed to be broadly distributed such that constitutes an asymmetric Lévy-stable process of order with . Lévy-stable processes of this kind induce a diverging characteristic waiting time . We are interested in the process , i.e. the behaviour of the physical space variable as a function of physical time . The pdfs of this process are defined as (e.g. for two points):

| (5) |

As a consequence of above specifications, is non-Markovian and reveals subdiffusive characteristics: . Its statistical properties are closely related to the properties of the process , the inverse of the process . The investigation of the statistics of the inverse Lévy-stable process has been the focus of reference Baule . One of the main results is the following integral transformation for the -point pdf of the process Baule :

| (6) |

denotes the -point pdf of the process and the -point pdf of the Markovian process . Eq. (6) states that the pdf of the non-Markovian process can be determined by a transformation of the corresponding Markovian process. The integral kernel is generated by the inverse Lévy-stable process . Whereas the pdf is obtained in a straightforward way from the Langevin equation (3), the determination of proves to be the crucial point. In the one- and two-point case assumes a simple form in Laplace space.

In the following we present the derivation of the two-point fractional diffusion equation starting from the transformation Eq. (6). The derivation of the single-time FDE (1) proceeds along the same lines and is not shown here. We define Laplace transforms in the usual way: , accordingly for multiple variables . Functions with argument always denote the Laplace transform if not otherwise indicated: . In Laplace space Eq. (6) for the two-point pdf assumes the similar expression:

| (7) |

The Laplace transform of the two-point pdf is explicitly given as Baule :

| (8) | |||||

An equation for is readily derived in the form

| (9) |

with initial conditions

| (10) |

In general the two-point pdf of the Markovian diffusion process is determined by the transition probability: . In turn is obtained from the ordinary Fokker-Planck equation. Due to the Markovian property it is not necessary to formulate a closed evolution equation for , however such an equation can be derived in a straightforward way from the two-point characteristic function of the process . The result is:

| (11) |

where we define a generalized diffusion operator as the inverse Fourier transform

The definition Eq. (A fractional diffusion equation for two-point probability distributions of a continuous-time random walk) holds in the same form in higher dimensions. Furthermore, broadly distributed symmetric increments in Eq. (3) would result in a characteristic exponent . The inverse Fourier transform then leads to a two-point generalization of the fractional Riesz/Weyl operator Metzler1 . The initial conditions of Eq. (11) read:

| (13) |

Now we can proceed as follows. We multiply Eq. (7) by and substitute Eq. (9). After performing partial integrations with respect to and , Eq. (11) can be substituted leading to the following equation:

The specific boundary terms occur due to the partial integrations and assuming . These terms can be absorbed into the Caputo fractional differential operator, which we generalize to two times in a straightforward way. First we note that and are determined from Eq. (8):

| (15) |

takes the analogue form. Both expressions can be substituted into Eq. (A fractional diffusion equation for two-point probability distributions of a continuous-time random walk). In the second term of Eq. (15) the Laplace transform of the single-time distribution occurs Baule : . Consequently, with the help of Eq. (6) for the case the integrations in the boundary terms of Eq. (A fractional diffusion equation for two-point probability distributions of a continuous-time random walk) lead to the single-time distributions and :

| (16) | |||||

Rearranging terms yields:

| (17) |

In order to perform the inverse Laplace transform of this equation we state the two results ( denotes the Gamma function):

| (18) |

and

| (19) |

Furthermore, due to the definition Eq. (5) the boundary conditions of the pdf are as in the Markovian case Eq. (A fractional diffusion equation for two-point probability distributions of a continuous-time random walk): , etc. The Laplace transform of the single-time Caputo operator Eq. (2) reads . Having all this in mind, the inverse Laplace transform of Eq. (A fractional diffusion equation for two-point probability distributions of a continuous-time random walk) then yields our main result:

| (20) | |||||

This is the two-point fractional diffusion equation, generalizing the single-time FDE to two-point probability distributions. Here, a generalization of the single-time Caputo operator to two times is introduced as:

| (21) |

where the denote a double Laplace convolution with respect to and . With the definition of the two-time fractional Caputo derivative Eq. (21) the general form of the diffusion equation is clearly visible. In addition, boundary terms occur which can be interpreted according to the underlying random walk. and describe the propagation when either or . is due to the non-zero probability that the random walker stays at the initial site. The analytical form of this term is obtained by performing the inverse Laplace transform of (Eqs. (A fractional diffusion equation for two-point probability distributions of a continuous-time random walk)):

| (22) |

where . This expression agrees with the interpretation given above. For , the probability of staying at the initial site until is given by the single-time distribution and vice versa. As in the single-time case, the two-point FDE reduces to the form of its Markovian counterpart Eq. (11) for (see the expression in Laplace space Eq. (A fractional diffusion equation for two-point probability distributions of a continuous-time random walk)). Also, the transformation Eq. (6) reproduces this result, since for : (see Eq. (8)). The occurrence of additional boundary terms in Eq. (20) can be considered as a general signature of non-Markovian processes and is even more prominent in the multiple-time case. A generalization to -point probability distributions is obtained in a straightforward way along the lines outlined above.

From Eq. (20) the two-time moments of the subdiffusive CTRW can be calculated without invoking the properties of the inverse Lévy-stable process . Consider e.g. the simplest moment . Multiplicating Eq. (20) with , and integrating from to yields , where is the strength of the stochastic force in the Langevin equation (3). A solution of this equation can be calculated in Laplace space. Since we use the usual convention the boundary terms due to the Laplace transformation of all vanish. One immediately obtains the solution , which reads in real space:

| (23) |

Due to the fact, that is given as the transformation Eq. (6) only even higher order moments are non-zero. They obey the general recursion formula (for non-negative integers , ):

| (24) | |||||

In the case we obtain:

| (25) | |||||

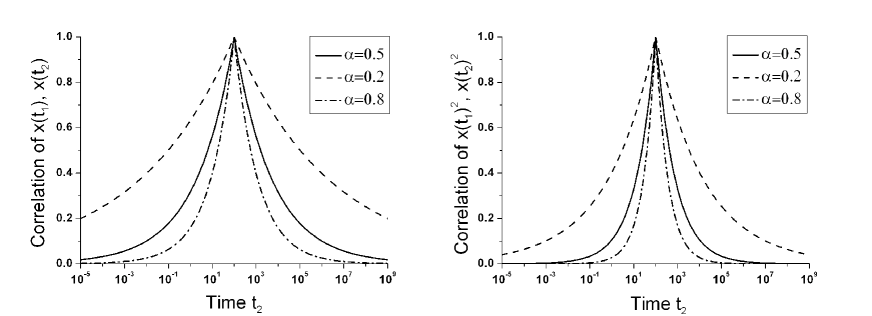

Here, denotes the hypergeometric function (see e.g. Abram ). Figure 1 shows a semi-logarithmic plot of the correlations corresponding to Eq. (23) and Eq. (25) as functions of for three different -values. Both correlations exhibit a clear power law decay for : and respectively. It would be interesting to determine these correlations from experiments.

We have demonstrated that a consistent generalization of the well-known single-time fractional diffusion equation to two-point pdfs can be derived on the basis of the coupled Langevin equations introduced by Fogedby as a representation of CTRWs. Special features of the two-point FDE are a two-time fractional differential operator of the Caputo-type and the occurrence of additional boundary terms. Its solution is expressed in terms of an integral transformation of the two-point pdf of the corresponding normal diffusion process. As in the single-time case the limit reduces the FDE to its Markovian counterpart. Furthermore we derived recursion relations for arbitrary two-time moments of the subdiffusive CTRW. It should be noted that the occurrence of fractional derivatives is a consequence of the properties of the stochastic process which determines the temporal behaviour of the CTRW. Thus the derivation of evolution equations, as presented in this paper, should apply to a whole class of systems, which can be described by two independent stochastic processes for and . Here the simplest case has been solved, namely specified as a Wiener process. For this case, we have determined explicit expressions for the two-time moments, which could be readily compared with moments obtained from experiments. An investigation of the multi-point statistics of other CTRW related processes, e.g. the anomalous diffusion of weakly damped inertial particles Friedrich2 , is left for future work.

References

- (1) E. W. Montroll and G. H. Weiss, J. Math. Phys. 6, 167 (1965).

- (2) J.-P. Bouchaud and A. Georges, Phys. Rep. 195, 127 (1990).

- (3) R. Metzler and J. Klafter, Phys. Rep. 339, 1 (2000).

- (4) M. F. Shlesinger, G. M. Zaslavsky, and J. Klafter, Nature 363, 31 (1993).

- (5) R. Metzler, E. Barkai, and J. Klafter, Phys. Rev. Lett. 82, 3563 (1999).

- (6) I. Podlubny, Fractional Differential Equations (Academic Press, New York, 1999).

- (7) W. R. Schneider and W. Wyss, J. Math. Phys. 30, 134 (1989).

- (8) R. Friedrich, Phys. Rev. Lett. 90, 084501 (2003).

- (9) R. Metzler and J. Klafter, J. Phys. A 37, R161 (2004).

- (10) E. Barkai, Phys. Rev. Lett. 90, 104101 (2003).

- (11) G. Bel and E. Barkai, Phys. Rev. Lett. 94, 240602 (2005).

- (12) R. Friedrich, F. Jenko, A. Baule, and S. Eule, Phys. Rev. Lett. 96, 230601 (2006).

- (13) V. Barsegov and S. Mukamel, J. Phys. Chem. A 108, 15 (2004).

- (14) A. Baule and R. Friedrich, Phys. Rev. E 71, 026101 (2005).

- (15) H. Yang et al., Science 302, 262 (2003).

- (16) W. Min et al., Phys. Rev. Lett. 94, 198302 (2005) .

- (17) H. C. Fogedby, Phys. Rev. E 50, 1657 (1994).

- (18) Handbook of Mathematical Functions, edited by M. Abramowitz and C. A. Stegun (Dover, New York, 1972).